Embed Size (px)

Citation preview

Financing the Biofuels Industry

Mike Bryan

CEO

BBI International300 Union Blvd., Suite 325

Denver, CO USA [email protected]

Introduction to BBI

BBI International

BBI International founded in 1995 by Mike and Kathy Bryan

Over 130 full-time employees Three Divisions:

Conference Division Media Division Project Development Division

An independent source of information and data for owners, lenders and policy makers

BBI International

Leading biofuels consulting company in the US with more than 200 renewable energy projects completed in the last seven years

Expertise in ethanol and biodiesel production from starch, sugar, cellulose and oilseed/animal fat based feedstocks

Expertise in emerging technologies for the production of ethanol and chemicals from lignocellulosic feedstocks

Expertise in ethanol and biodiesel project development

Financing the Biofuels Industry

Key Concerns Faced Today Construction

Unproven builders or lack of time Performance guarantees

Demand Economics Determine volumes consumed & pricing cycles What is the maximum biofuels market for Mexico? World Demand

Crush Margin (feedstock prices in relation to ethanol) Risk management

Lack of long term contracts for ethanol Plant Management…who will manage the facility?

What does it take to Attract Financing?

The Five “C’s” of Credit:

Capacity Repayment ability Capital Financial condition Character Management Collateral Quality and value ConditionsMarket & Economics

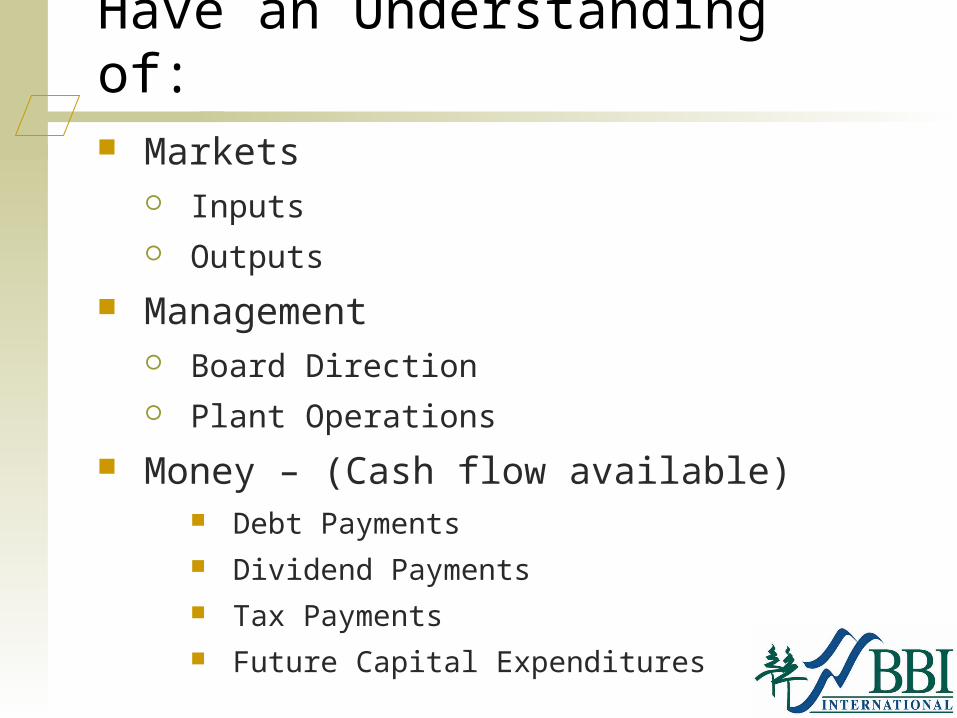

Have an Understanding of: Markets

Inputs Outputs

Management Board Direction Plant Operations

Money – (Cash flow available) Debt Payments Dividend Payments Tax Payments Future Capital Expenditures

Project Finance

We define project finance as the ability to raise funds to finance an economically viable project. Debt Capital Equity Capital

The providers of these funds look to the cash flow Not the Income Statement Cash flows needed:

To service debt (loan payments) To pay a return on invested capital (dividends)

Risk Management

Risk management by definition has to do with “maximizing the areas where we have some control over the outcome while minimizing the areas where we have absolutely no control over the outcome and linkage between effect and cause is hidden from us.”

Against the Gods – Peter Bernstein

Types of Legal Structures

Sole Proprietorship

General & Limited Partnership

Corporation (C or S corp.)

Limited Liability Companies (LLC)

Farm / Agricultural Cooperatives (Coop)

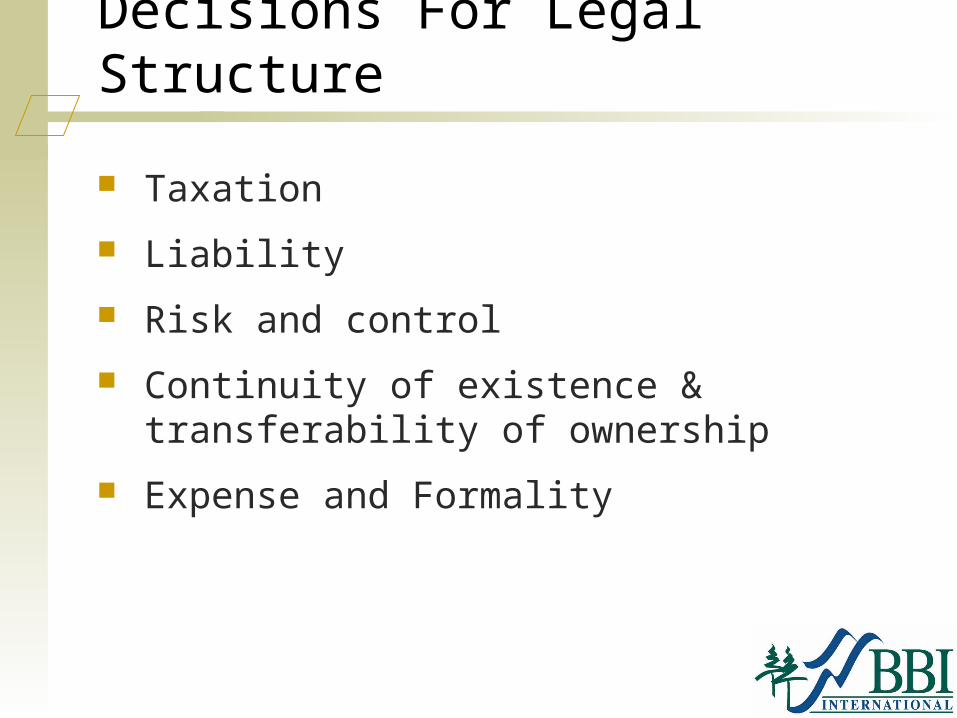

Decisions For Legal Structure

Taxation

Liability

Risk and control

Continuity of existence & transferability of ownership

Expense and Formality

Financial Structures

The providers of capital look to the cash flow for payment on their contributions.

All Equity

Senior Debt and Equity

Senior Debt, Sub Debt, and Equity

Lease Buy Back

Bonds

Securities instrument

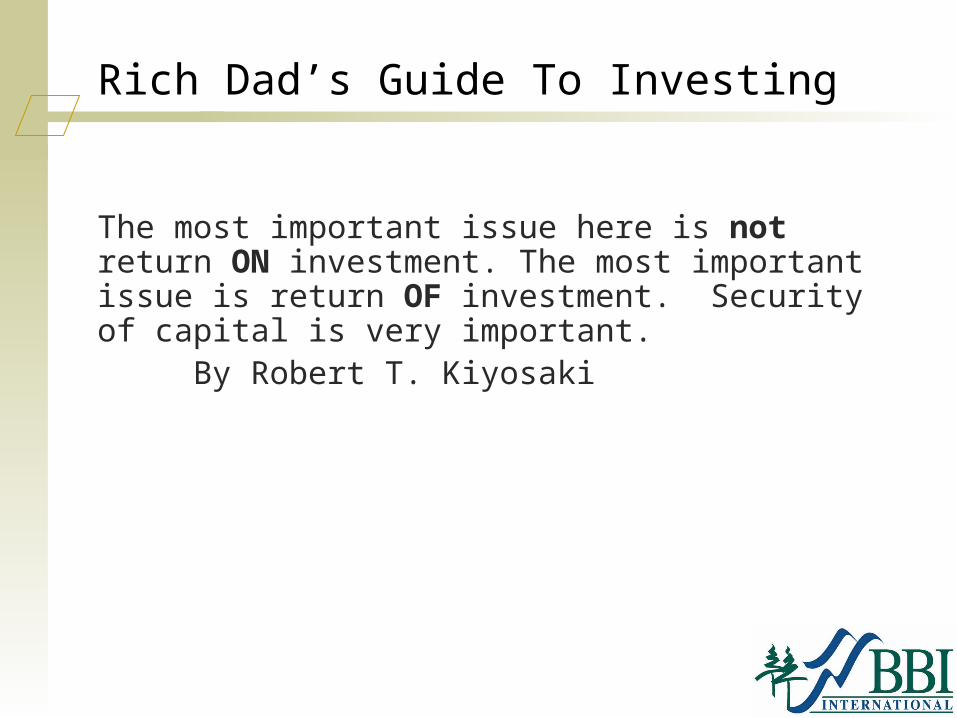

Rich Dad’s Guide To Investing

The most important issue here is not return ON investment. The most important issue is return OF investment. Security of capital is very important.

By Robert T. Kiyosaki

Financial Structures

Covenants Liquidity

Repayment Capacity

Leverage

Risk Management

Conditions for Ensuring Success

Liquidity

Working Capital: $0.04 per liter

At start up of the plant

Depending on the time of year

Varies depending on inventory carrying cost

Feedstock

Ethanol

Energy costs

Debt & Equity Ratio

Total cost of plant, property and equipment

All pre-production, organizational and general operating funds through the end of construction

Beginning working capital, (cash to cover outflow of funds so you do not over draw your bank account)

Base Loan Criteria in USA

Debt to Equity 40% to 60% Equity for Producer Owned 25% to 50% Equity for Investor Owned

or $.21 to $.26 per liter of total debt per

project

Construction Risks

Risk of design and construction of the project Risk of the project meeting the performance

specification Risk of completion and by a fixed date Risk of performance of contractors

consultants, subcontractors and suppliers Risk on Contractor insolvency

Turnkey, Lump Sum Fixed Price, or Guaranteed Max Price

Date Certain

Full Wrap to hold Contractor Liable

Draw down (payment) schedule

Milestone payments and construction schedule

Types of Construction Contracts

Performance Bonds or other Insurance type products

10% retained on each construction invoice

Date Certain for mechanical, substantial final completion for Liquidated Damages

Mitigating Risk in Construction

Liquidated Damages is payment for loss revenue

Performance guarantee Emissions compliance

Capacity

Energy Utilization

Production

Yield

Best on set times for Measurement

Mitigating Risk in Construction

Owners Scope of work & budget

Site

Working Capital

Financing

Other Contractor Scope of Work & budget

Technology

Equipment plans

Site layout

Permitting

Other

Clearly Define the Scope

Operational Risk

Price Risk

Supply and Demand Risk

Transportation Risk

Performance – plant operation

Ethanol Crush Margin

Revenue from Ethanol, DDGS and CO2

Minus

The total cost of feedstock plus the usage of energy needed to turn corn into ethanol (natural gas or coal)

Feasibility Study

Evaluating the Potential for Success!

Key Elements of an Ethanol Feasibility Study

Site selection Feedstock analysis Market analysis

Ethanol DDGS CO2

Financial analysis Construction costs Owner’s costs Operating costs Projected profitability and sensitivity studies

Site Selection

Typically 16 hectares in a rural area with: Low cost feedstock Good rail access Good road access Adequate utilities at reasonable cost Close proximity to co-product markets Access to ethanol markets Access to labor

Financial Analysis

Use conservative assumptions – 10 year pricing for corn and ethanol

Use ROI or IRR for profitability Assume 50% equity 25% minimum ROI, 30% for better projects Returns are most sensitive to feedstock and

ethanol pricing

Owner’s Costs

Land, roads, rail & site development Administration building/furnishings Utilities, water treatment, fire water Permits Startup costs and training Construction interest and loan fees Inventory costs Owner’s Costs add 8-10¢ per liter to the

overall project cost

BBI Feasibility Study

Executive Summary Site Assessments and Recommendation Feedstock Analysis Ethanol Market Analysis DDG & CO2 Market Analysis Detailed Financial Analysis with

Sensitivity Study & 10-year Pro Forma Competitive Analysis Summary and Recommendations

Commercialization Strategy

The successful model Site with adequate feedstock supply, utilities,

transportation and markets Utilize successful design/build firms Hire experienced ethanol marketing and risk

management firms Assemble first rate management team Raise 50% equity Projected Return on Equity should be 30% or

higher

For More Information Contact

Fundación E MisiónLic. Isabel Gómez MacíasPresidentaTel: (33) 3678-9153Fax: (33) 3678-9200