Embed Size (px)

Citation preview

FINISHED VEHICLE SUPPLY CHAIN:

Transportation and more

3 years of APL Logistics VASCOR Automotive 1

Emerging modes of transportation 2

Regulatory Framework 4

Presentation Outline

Beyond Transportation 3

2

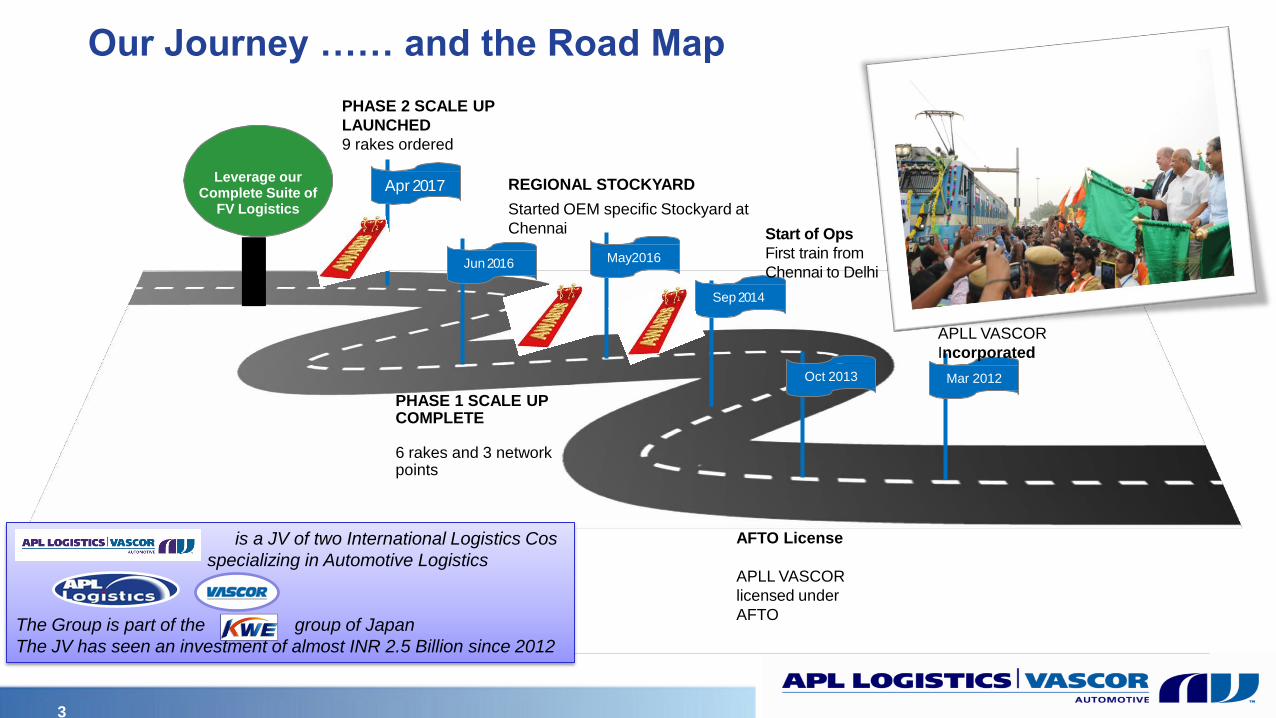

Mar 2012

Jun 2016 May2016

Oct 2013

Sep 2014

Apr 2017 Leverage our

Complete Suite of FV Logistics

REGIONAL STOCKYARD

Started OEM specific Stockyard at

Chennai

PHASE 1 SCALE UP COMPLETE

6 rakes and 3 network points

Start of Ops

First train from

Chennai to Delhi

AFTO License

APLL VASCOR

licensed under

AFTO

APLL VASCOR

Incorporated

Our Journey …… and the Road Map

PHASE 2 SCALE UP

LAUNCHED

9 rakes ordered

is a JV of two International Logistics Cos

specializing in Automotive Logistics

The Group is part of the group of Japan

The JV has seen an investment of almost INR 2.5 Billion since 2012

3

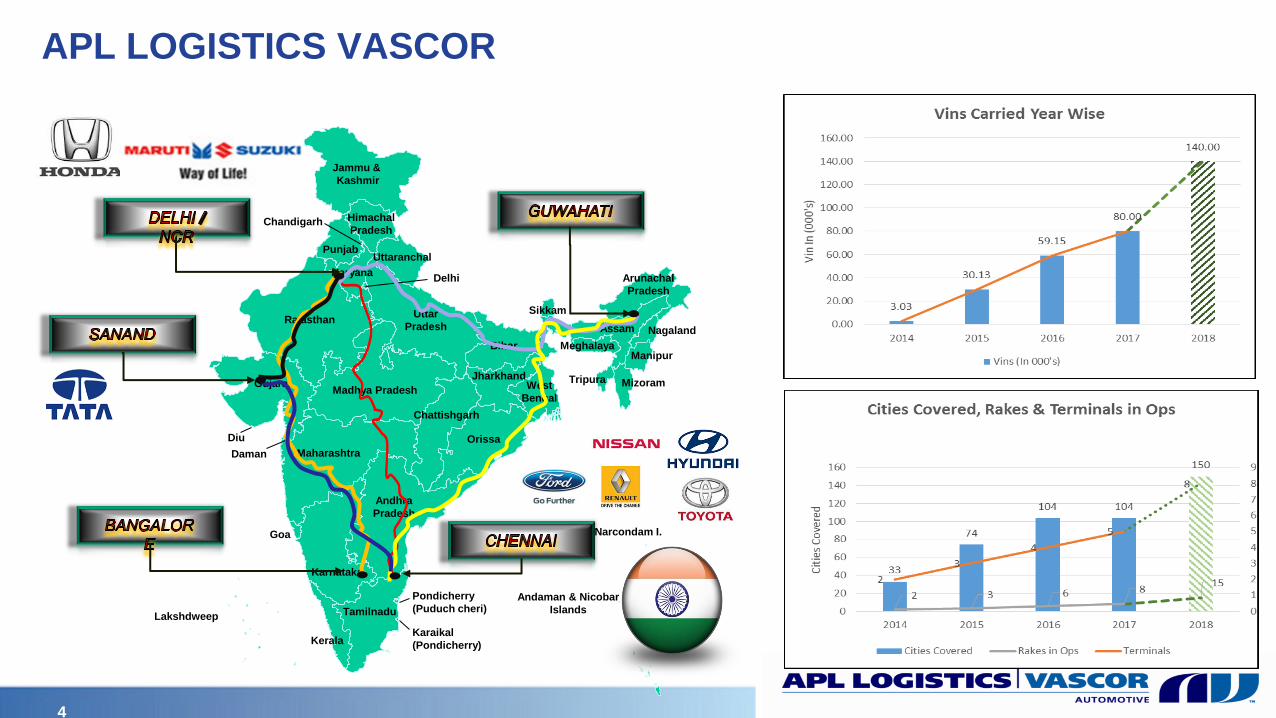

APL LOGISTICS VASCOR

Jammu &

Kashmir

Punjab

Chandigarh Himachal

Pradesh

Uttaranchal

Uttar

Pradesh

Haryana Delhi

Rajasthan

Gujarat Madhya Pradesh

Bihar

Chattishgarh

Maharashtra

Goa

Karnataka

Kerala

Lakshdweep Tamilnadu

Andaman & Nicobar

Islands

Narcondam I.

Barren I.

Andhra

Pradesh

Orissa

Jharkhand West

Bengal

Sikkam

Meghalaya

Assam

Manipur

Arunachal

Pradesh

Nagaland

Mizoram Tripura

Diu

Daman

Karaikal

(Pondicherry)

Pondicherry

(Puduch cheri)

4

3 years of APL Logistics VASCOR Automotive 1

Emerging modes of transportation 2

Regulatory Framework 4

Beyond Transportation 3

Presentation outline

5

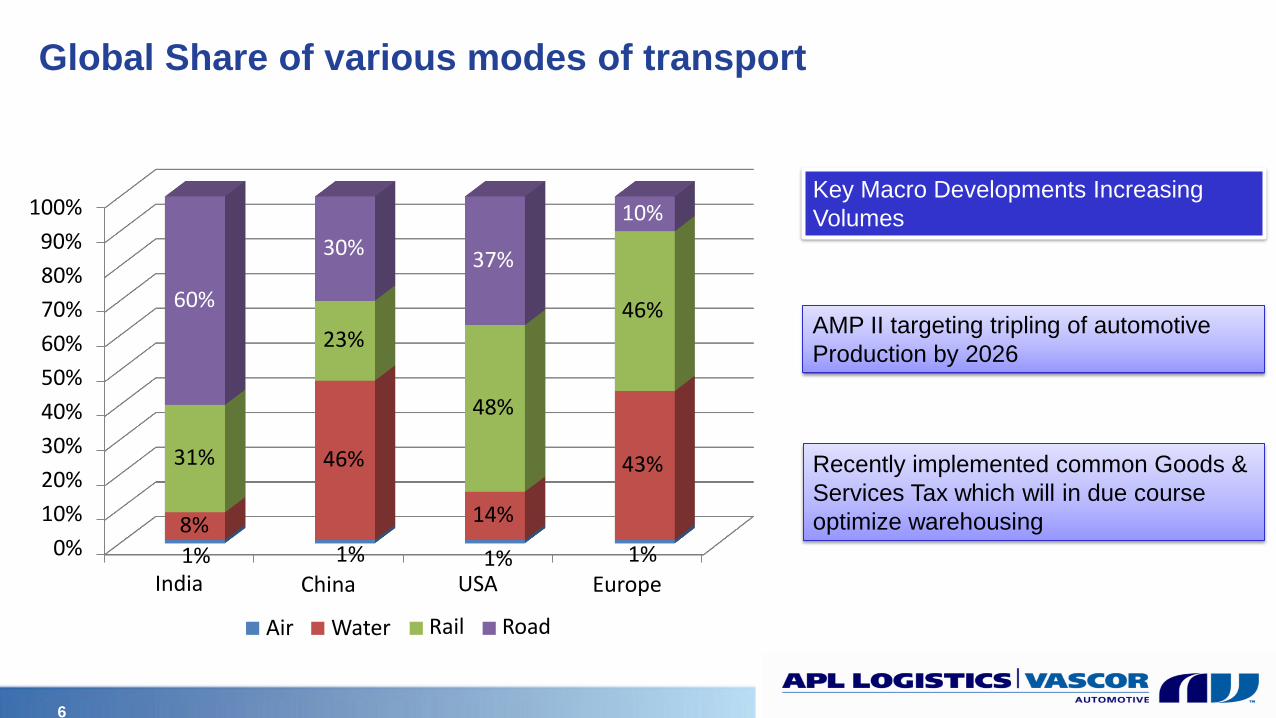

Global Share of various modes of transport

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0% 1%

Europe

8%

1% India

46%

14%

1% USA

43% 31%

23%

48%

46% 60%

30% 37%

10%

1%

China

Air Water Rail Road

Key Macro Developments Increasing

Volumes

AMP II targeting tripling of automotive

Production by 2026

Recently implemented common Goods &

Services Tax which will in due course

optimize warehousing

6

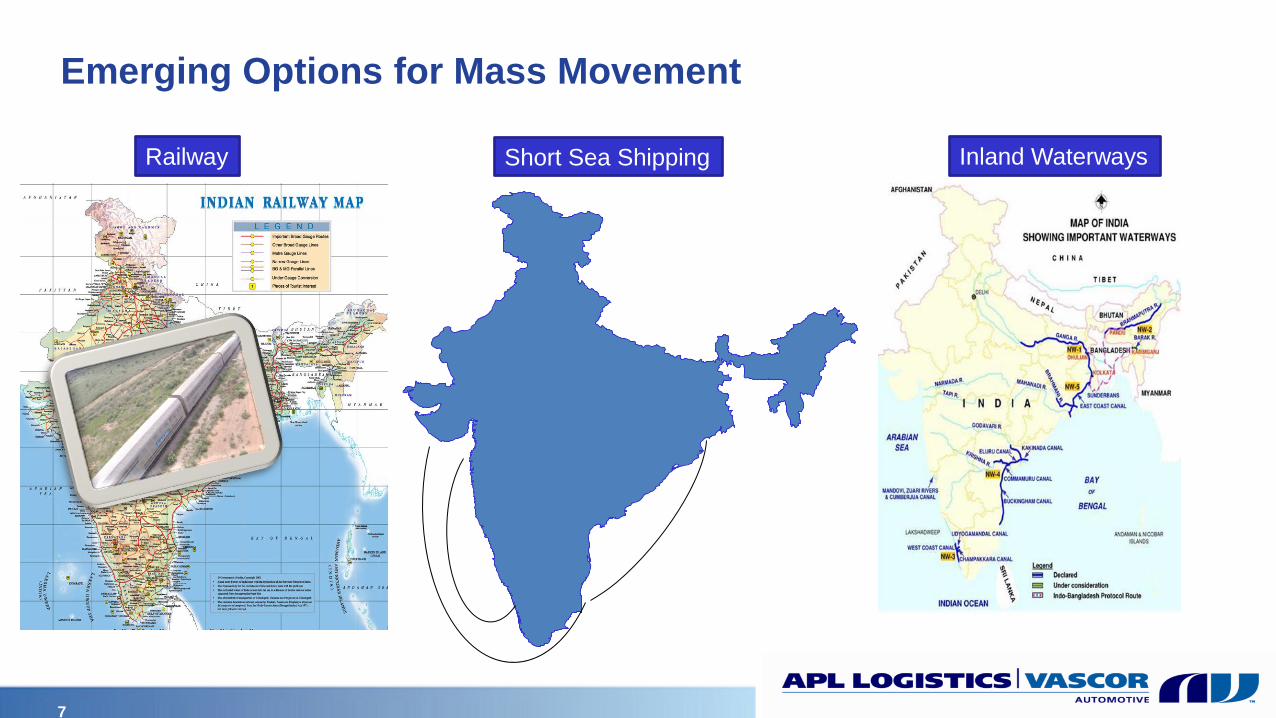

Emerging Options for Mass Movement

Railway Short Sea Shipping Inland Waterways

7

3 years of APL Logistics VASCOR Automotive 1

Emerging modes of transportation 2

Regulatory Framework 4

Beyond Transportation 3

Presentation outline

8

FINISHED VEHICLE LOGISTICS is not just transportation…

Vehicle Inventory & Processing

• Mixing Yard Management

• Vehicle Accessorization

• Plant Releasing

• Drive Away Delivery

• Rail Loading and Unloading

Vehicle Supply Chain Management

• Vehicle Inspections

• In-Transit Repair Management

• Vehicle Transportation Management

• Claims Management

Value Added Services

• Business Intelligence and Analysis

• Engineering Services

• In-Plant Production Support

Finished

Vehicle

Logistics

9

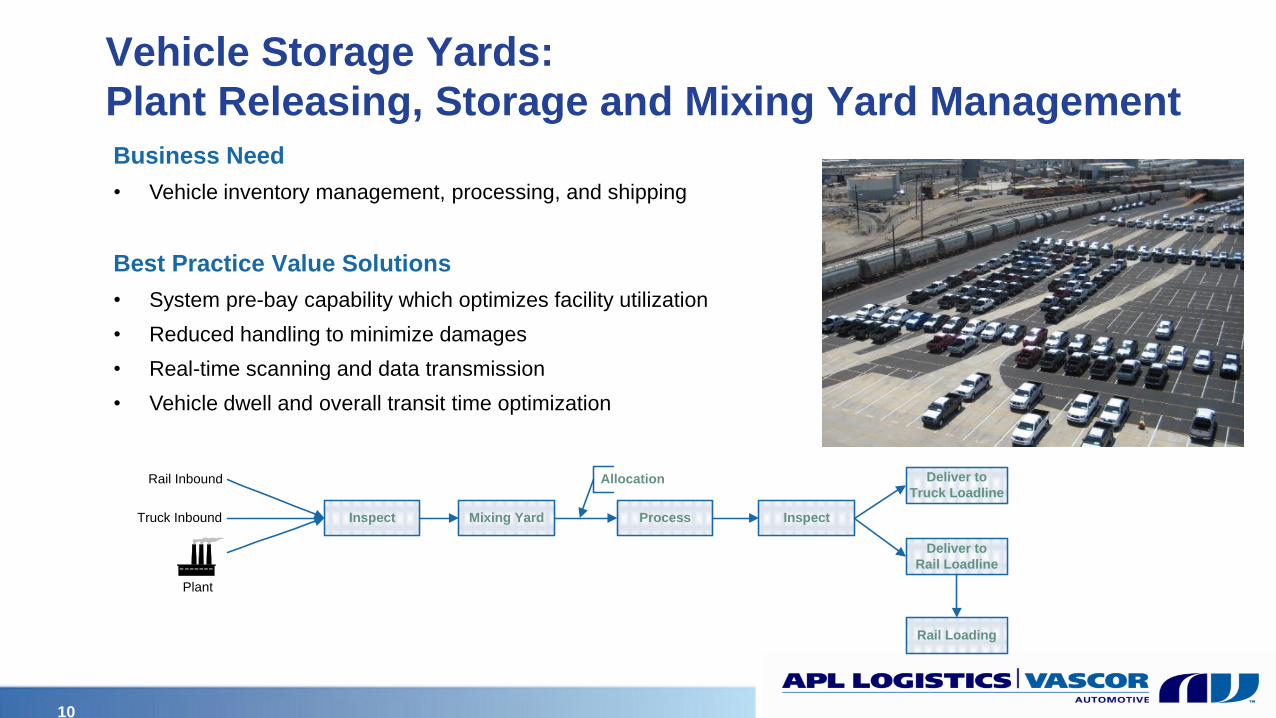

Vehicle Storage Yards:

Plant Releasing, Storage and Mixing Yard Management

Business Need

• Vehicle inventory management, processing, and shipping

Best Practice Value Solutions

• System pre-bay capability which optimizes facility utilization

• Reduced handling to minimize damages

• Real-time scanning and data transmission

• Vehicle dwell and overall transit time optimization

Mixing YardInspect Inspect

Deliver to

Truck LoadlineRail Inbound

Truck Inbound

Plant

Allocation

Deliver to

Rail Loadline

Process

Rail Loading

10

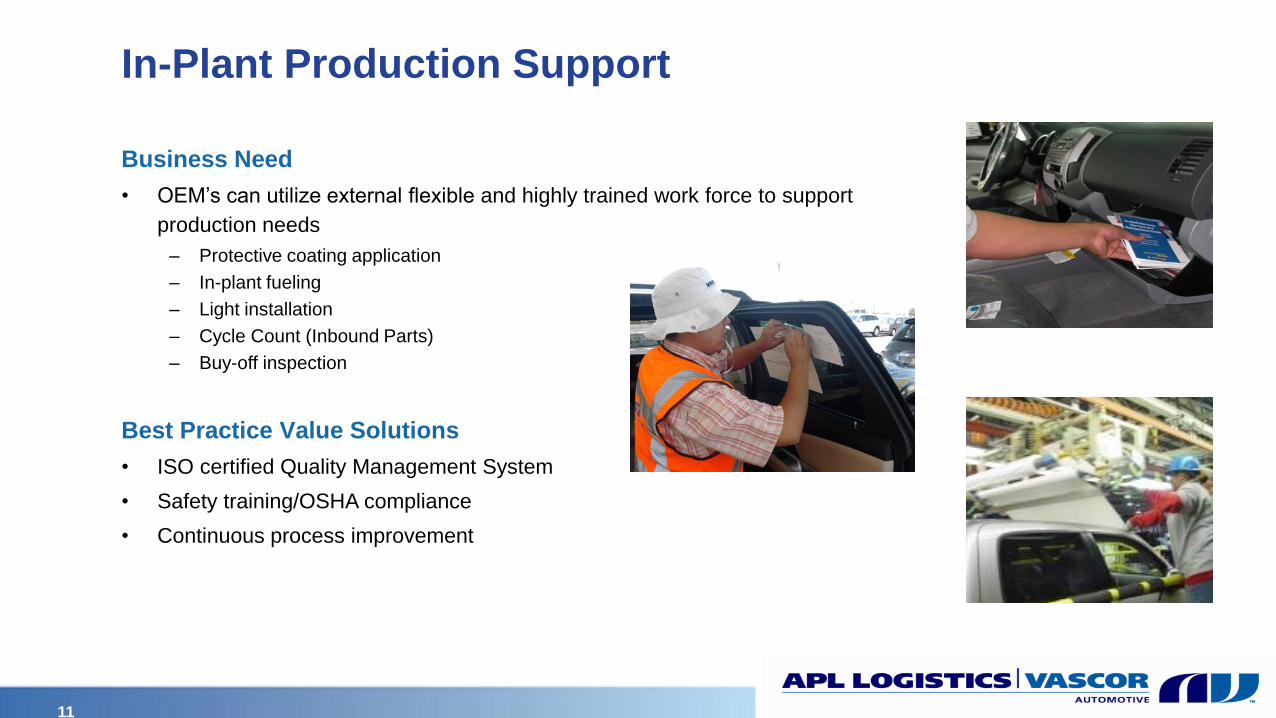

In-Plant Production Support

Business Need

• OEM’s can utilize external flexible and highly trained work force to support

production needs

– Protective coating application

– In-plant fueling

– Light installation

– Cycle Count (Inbound Parts)

– Buy-off inspection

Best Practice Value Solutions

• ISO certified Quality Management System

• Safety training/OSHA compliance

• Continuous process improvement

11

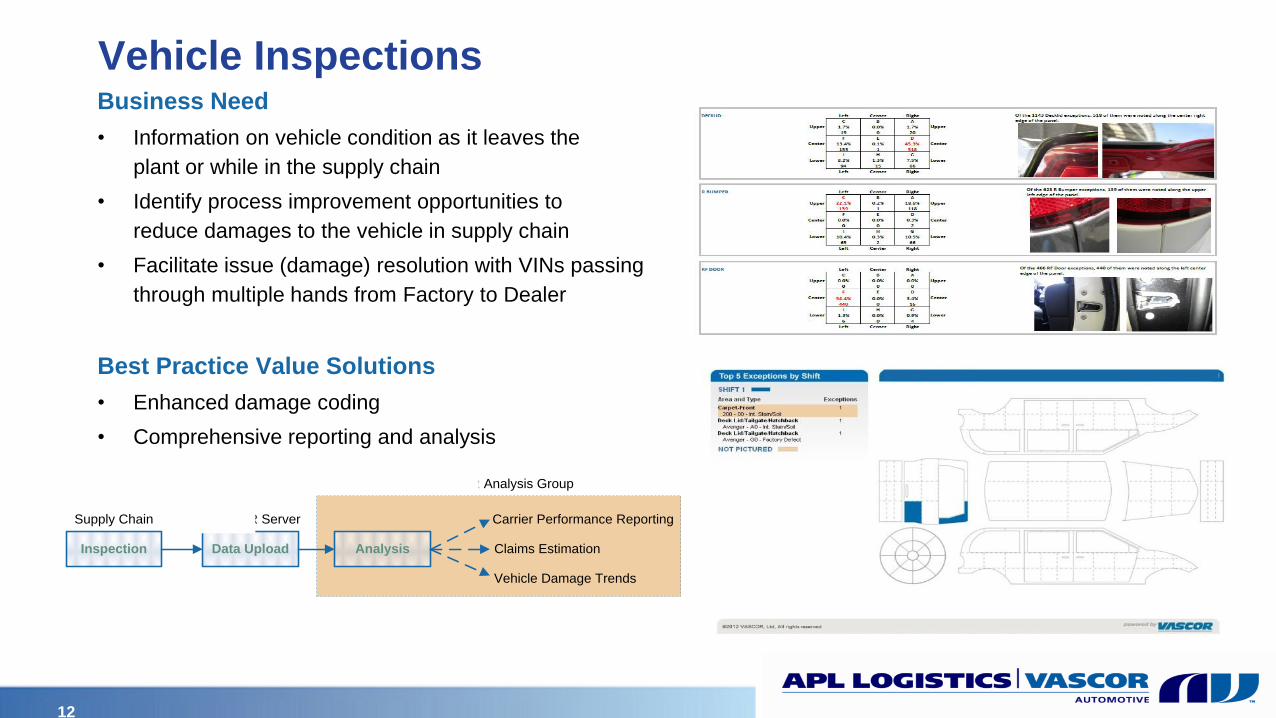

Vehicle Inspections Business Need

• Information on vehicle condition as it leaves the

plant or while in the supply chain

• Identify process improvement opportunities to

reduce damages to the vehicle in supply chain

• Facilitate issue (damage) resolution with VINs passing

through multiple hands from Factory to Dealer

Best Practice Value Solutions

• Enhanced damage coding

• Comprehensive reporting and analysis

AnalysisInspection Data Upload

Supply Chain VASCOR Server

VASCOR Analysis Group

Carrier Performance Reporting

Vehicle Damage Trends

Claims Estimation

12

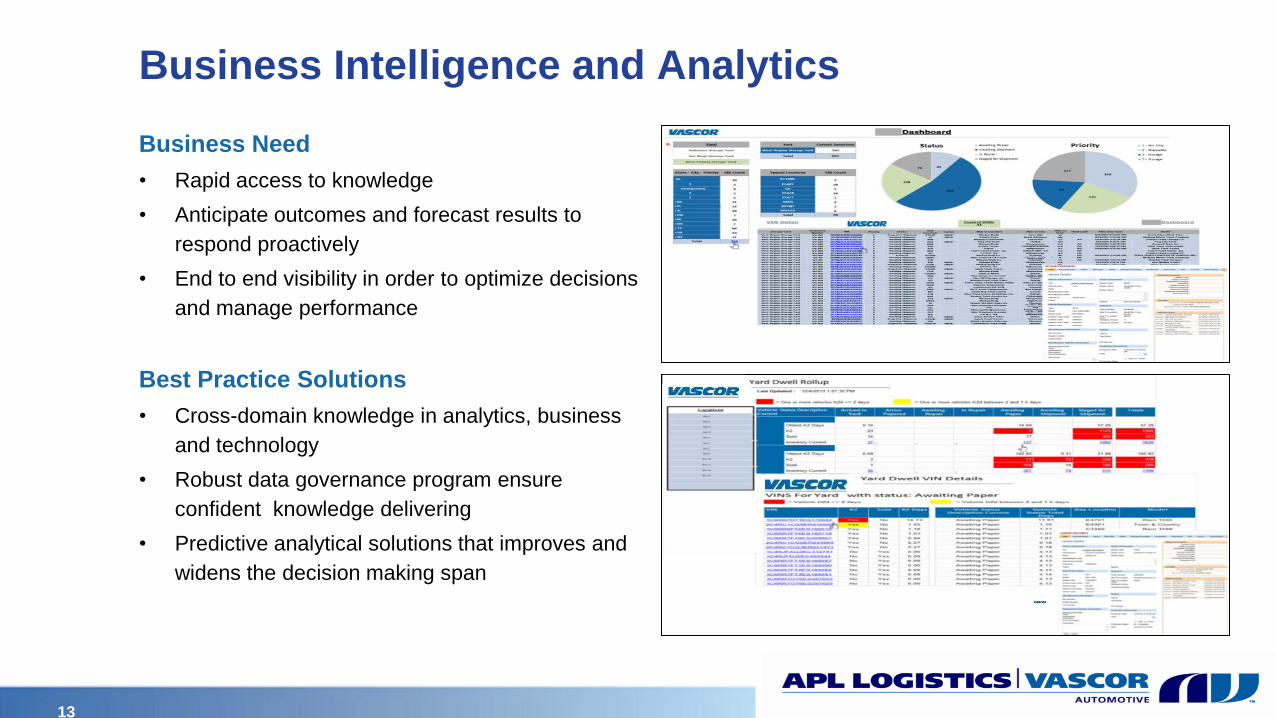

Business Intelligence and Analytics

Business Need

• Rapid access to knowledge

• Anticipate outcomes and forecast results to

respond proactively

• End to end visibility in order to optimize decisions

and manage performance

Best Practice Solutions

• Cross-domain knowledge in analytics, business

and technology

• Robust data governance program ensure

confident knowledge delivering

• Predictive analytical solutions that improves and

widens the decision making span

13

Information Systems

Infrastructure

Communication Business Intelligence

Accounting

Supply Chain Visibility

ONE STOP SOLUTION

14

3 years of APL Logistics VASCOR Automotive 1

Emerging modes of transportation 2

Regulatory Framework 4

Beyond Transportation 3

Presentation Outline

15

Regulatory Framework: Indian Railway

Indian Railway recently relaxed entry norms in a bid to encourage more participation in the AFTO Policy

– Cost of AFTO license and # of rakes is not why others haven’t entered

Lobbying points for all of us :

– Economic returns from the business

Freight has to allow fair returns – the capital investments are very large

We operate specialized rail cars ; any rate hike will render the rail cars unusable

Asset Productivity

– Transit times must improve as current average speed is 18 kmph

– Down time for inspections/other must be optimized

Policy Stability

– Participation through steering policy – lowering the cost to enter is not enough

– Two things must happen for the India Railroad to grow this business and expand the network

Allow those that enter to make a reasonable return on their investment

– Adjust rates and payment terms

Limit the competition provided by the India Railroad

– Require AFTO license for those who utilize IR rakes

16

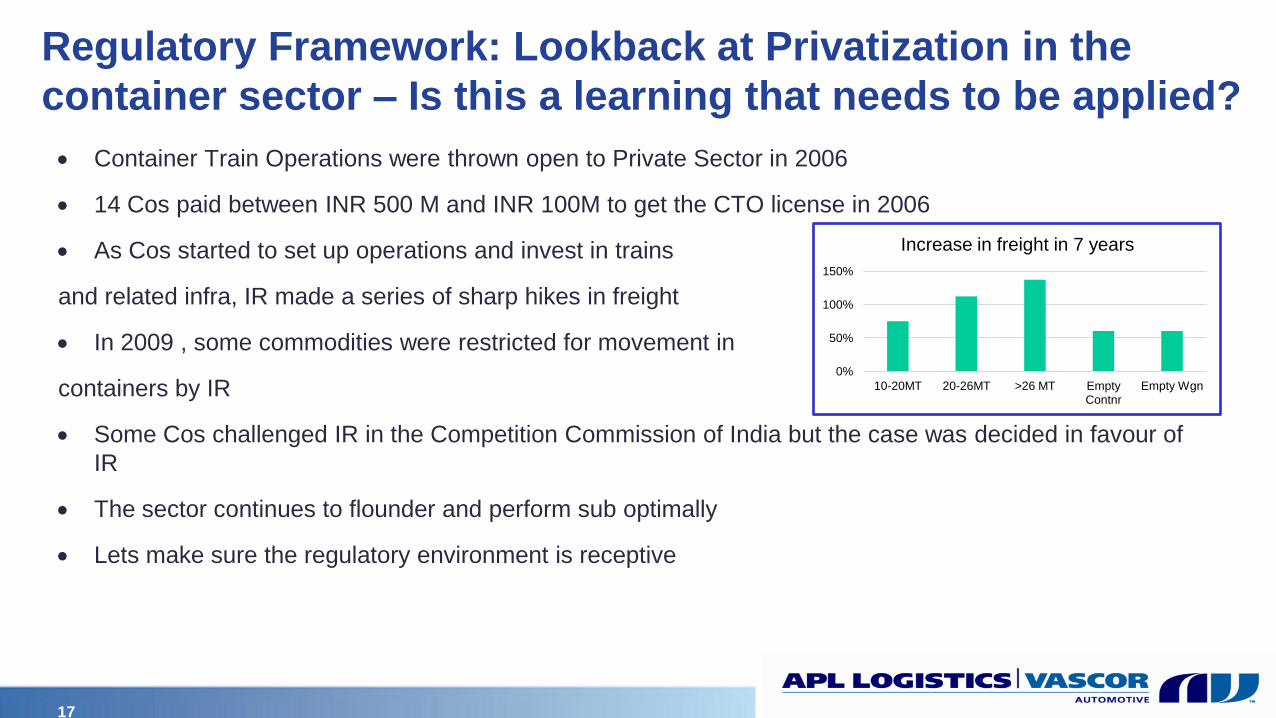

Regulatory Framework: Lookback at Privatization in the

container sector – Is this a learning that needs to be applied?

Container Train Operations were thrown open to Private Sector in 2006

14 Cos paid between INR 500 M and INR 100M to get the CTO license in 2006

As Cos started to set up operations and invest in trains

and related infra, IR made a series of sharp hikes in freight

In 2009 , some commodities were restricted for movement in

containers by IR

Some Cos challenged IR in the Competition Commission of India but the case was decided in favour of

IR

The sector continues to flounder and perform sub optimally

Lets make sure the regulatory environment is receptive

0%

50%

100%

150%

10-20MT 20-26MT >26 MT Empty Contnr

Empty Wgn

Increase in freight in 7 years

17

Thank You

Look forward to growing the business

in India