Embed Size (px)

Citation preview

Firms and ProductionFirms and Production

1

OutlineOutline

• Supply curvesSupply curves

• Firms and Organizations

i d k• Firms and Markets

• Firm’s Objectives

• Outputs

• InputsInputs

• Production and cost functions

2

Supply curvesSupply curves• Tuesday in exchange economies

– Price=Marginal willingness to pay

– Price=Marginal willingness to Sell

• Two weeks ago we saw that consumers and producers could meet in markets– When supply meets demand

– Price=Marginal willingness to payg g p y

– Price=Marginal cost

• But where does the supply curve come from?But where does the supply curve come from?

3

Firms and OrganizationsFirms and Organizations• Supply comes from decisions made by firms

I th f f h il th– In the case of consumers we focus heavily on the individual.

– For production we can’t do that because good are rarely p g yproduced by a single person.

• Important for two reasons– Need to figure out how the collective is organized

– The size of the collective matters to costf l d• Economies of scale and scope

• and diseconomies…

4

Types of FirmsTypes of Firms

• Proprietorship e g family businessProprietorship, e.g. family business

• Partnership, e.g. law, accounting practice

C i• Corporation– limited liability by shareholders

– legal “person”

– managed by agents of shareholders

• Non‐profit corporation– only certain activities achieve tax‐free statusy

5

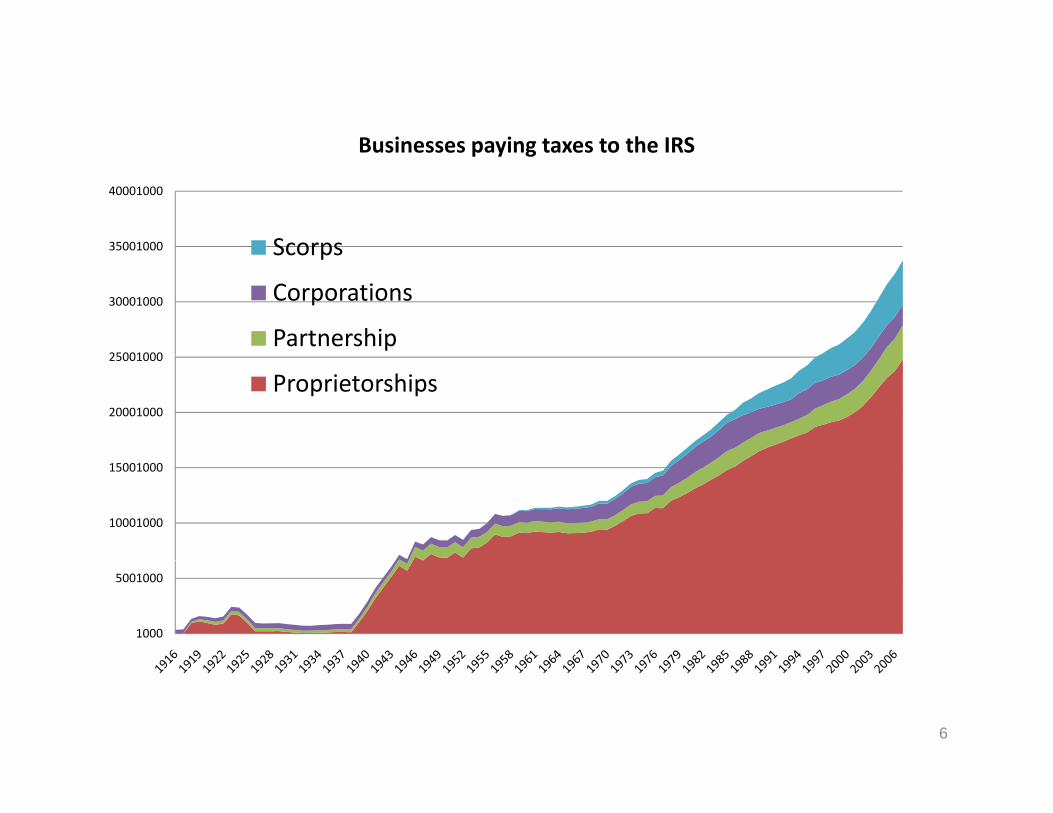

Businesses paying taxes to the IRS

35001000

40001000

Businesses paying taxes to the IRS

Scorps

25001000

30001000

Scorps

Corporations

Partnership

20001000

25001000

Proprietorships

10001000

15001000

1000

5001000

6

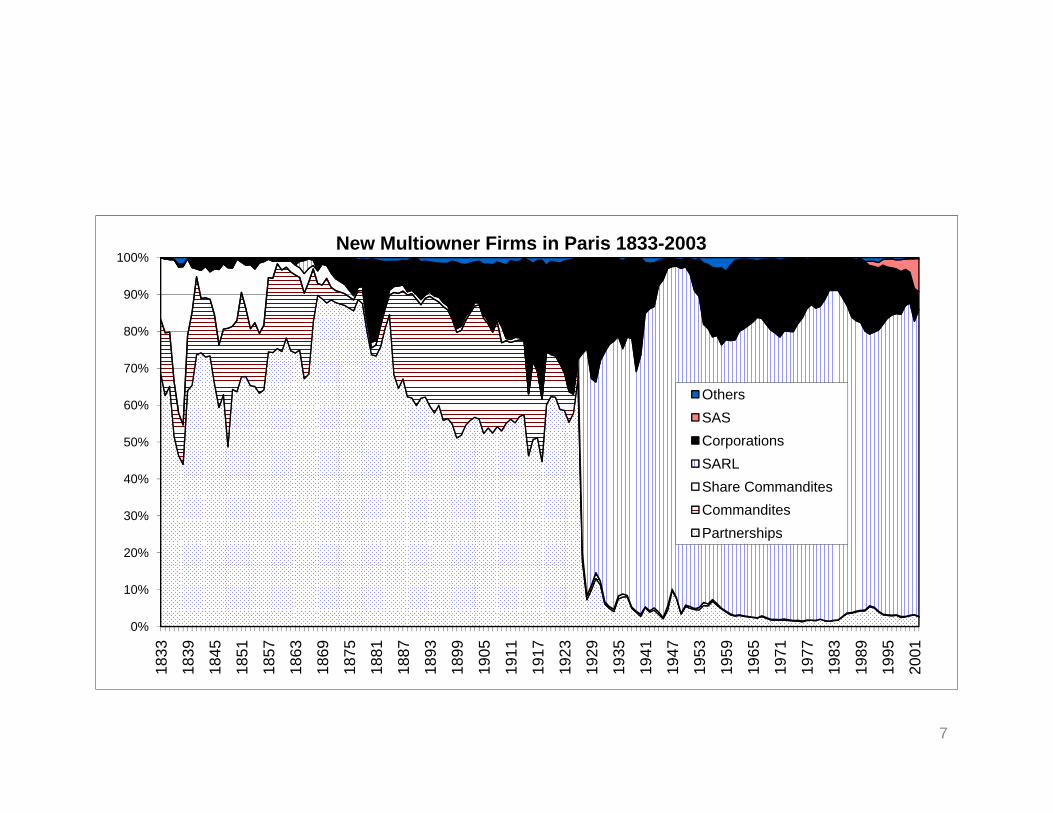

100%New Multiowner Firms in Paris 1833-2003

80%

90%

100%

50%

60%

70%

OthersSASCorporations

20%

30%

40%SARLShare CommanditesCommanditesPartnerships

0%

10%

833

839

845

851

857

863

869

875

881

887

893

899

905

911

917

923

929

935

941

947

953

959

965

971

977

983

989

995

001

18 18 18 18 18 18 18 18 18 18 18 18 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 20

7

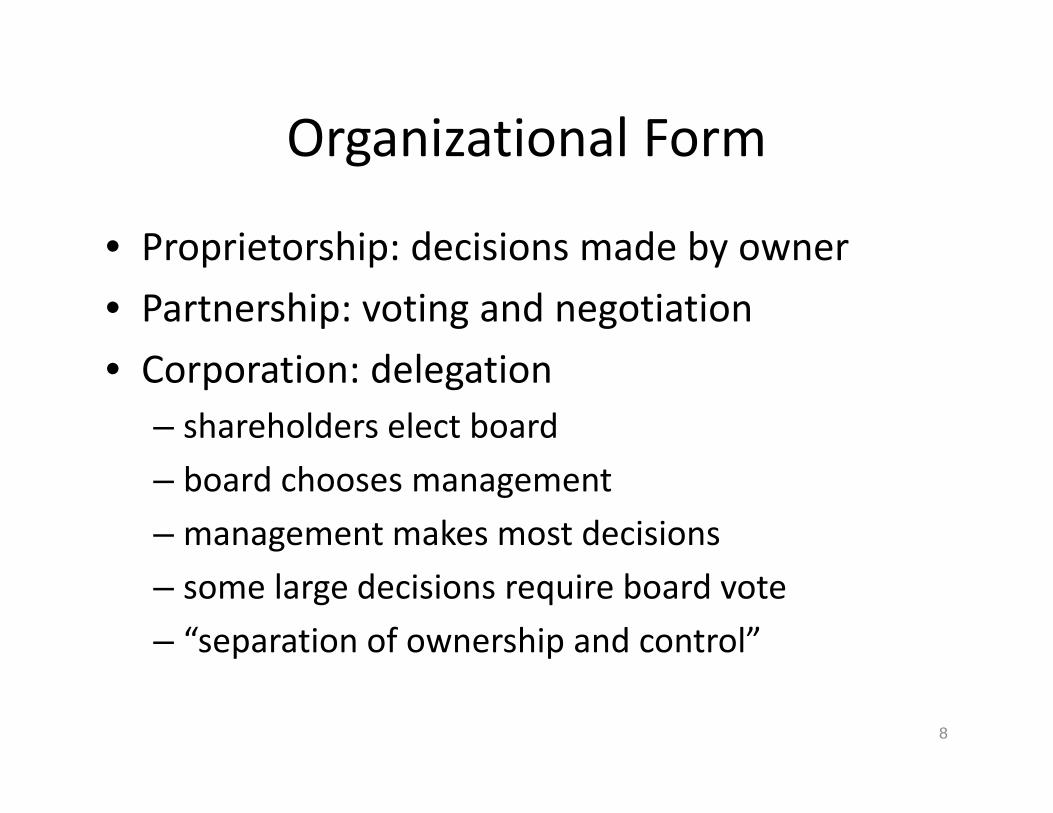

Organizational FormOrganizational Form

• Proprietorship: decisions made by ownerProprietorship: decisions made by owner

• Partnership: voting and negotiation

C i d l i• Corporation: delegation– shareholders elect board

– board chooses management

– management makes most decisions

– some large decisions require board vote

– “separation of ownership and control”

8

Firms and MarketsFirms and Markets

• Supply chainsSupply chains– Most firms buy their inputs from a firm and sell their inputs to anothertheir inputs to another.

• What is going on?Coase– Coase

• Firms exist to reduce transactions costs in markets

• Markets exist to reduce transactions cost in firms• Markets exist to reduce transactions cost in firms

9

Digression! Transaction costsDigression! Transaction costs

• Payment borne by buyer (above what goes toPayment borne by buyer (above what goes to seller) or by seller (that reduces what she gets from buyer) in transactionfrom buyer) in transaction.

• In marketsC t t t t lit ifi ti l– Cost transport, taxes, quality verification, supply or demand uncertainty…

I fi• In firms– Cost of monitoring effort, quality, added risk…

10

Firms and MarketsFirms and Markets

• If there are no transactions costs.If there are no transactions costs.– Firm size is indeterminate

• Can be a communist state• All workers can work for themselves

• If there are no transaction costs– Then boundaries of the firm set by trade‐off– For a particular transaction/relationship which is

h fi k ?cheaper firm or market?

• Does technology favor the firm or the market?

11

Firm’s ObjectivesFirm s Objectives

• First pass Maximize profitsFirst pass. Maximize profits.

• In reality more complicated. Firm has not objective of its ownobjective of its own.– It has the objective of the people who control it

Th i i h i l– They want to maximize their personal return.

– If sole proprietorship => max profit

– If not well that is only one issue.

12

Firm DecisionsFirm Decisions

• Firm as project

• The entrepreneur– Chose an organizational formChose an organizational form

– Chose a technology

– Chose a set inputs– Chose a set inputs

• The last three are interdependent.I hi l ill l i i l f– In this class we will neglect organizational form

– Today also take technology as give

13

What is a technology?What is a technology?

• A complete recipeA complete recipe

• A menu of recipes that allow you to trade off different inputsdifferent inputs

• A menu of recipes that allow you to trade off l d h ilong run and short run investments

All for the production of a good or service.

• So it’s a production functionSo it s a production function

14

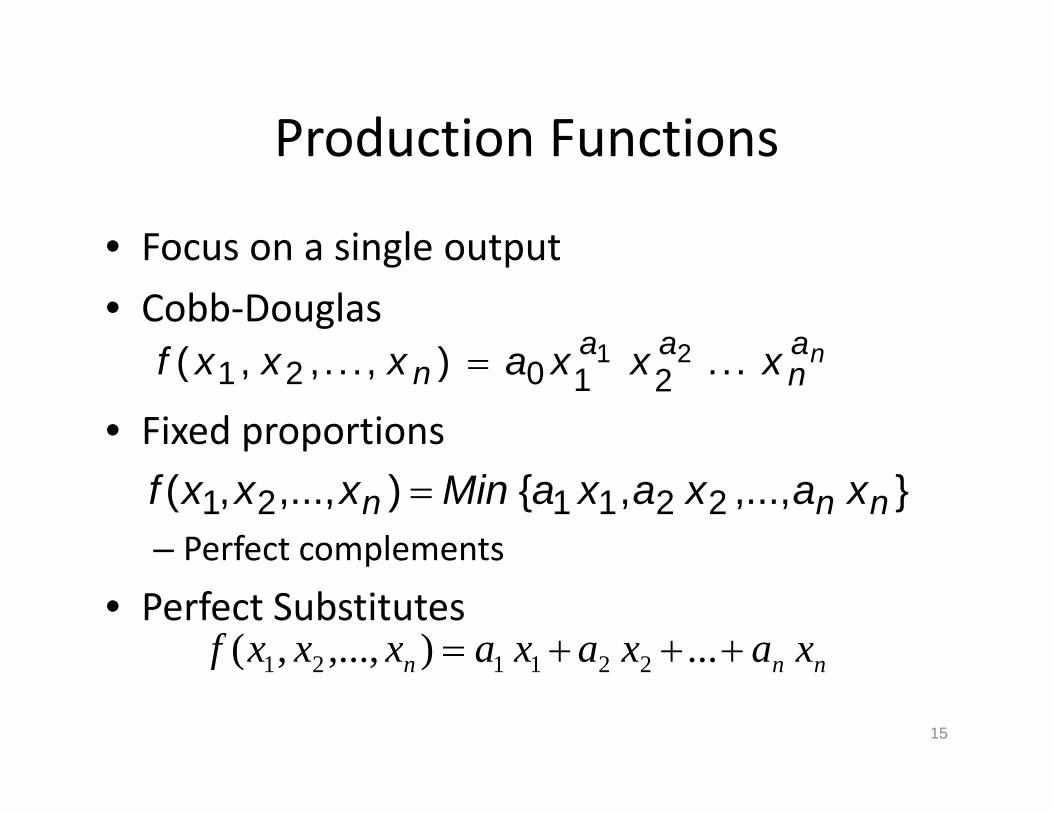

Production FunctionsProduction Functions

• Focus on a single outputFocus on a single output

• Cobb‐Douglas naaa xxxaxxxf )( 21

• Fixed proportions

nnn xxxaxxxf ...),...,,( 21

21021

– Perfect complements

}...,,,{),...,,( 221121 nnn xaxaxaMinxxxf e ec co p e e s

• Perfect Substitutesnnn xaxaxaxxxf ...),...,,( 221121 nnnf ), ,,( 221121

15

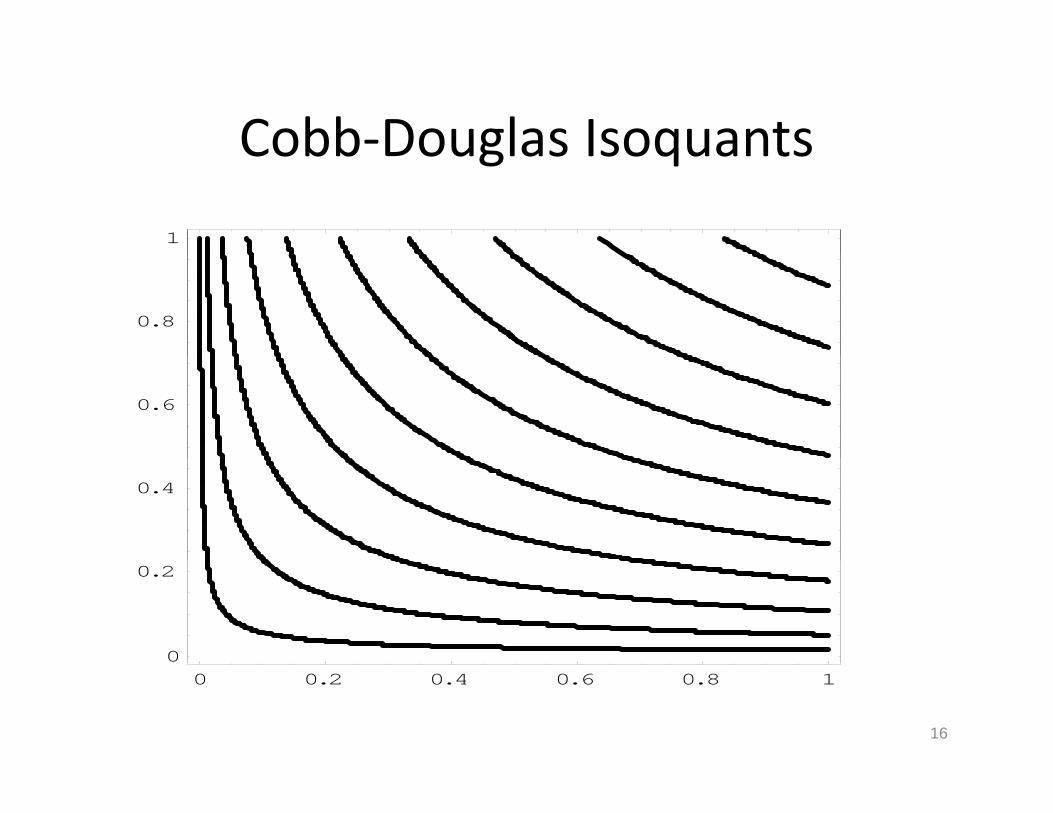

Cobb‐Douglas IsoquantsCobb Douglas Isoquants

1

0.8

0.6

0.4

0

0.2

0 0.2 0.4 0.6 0.8 1

16

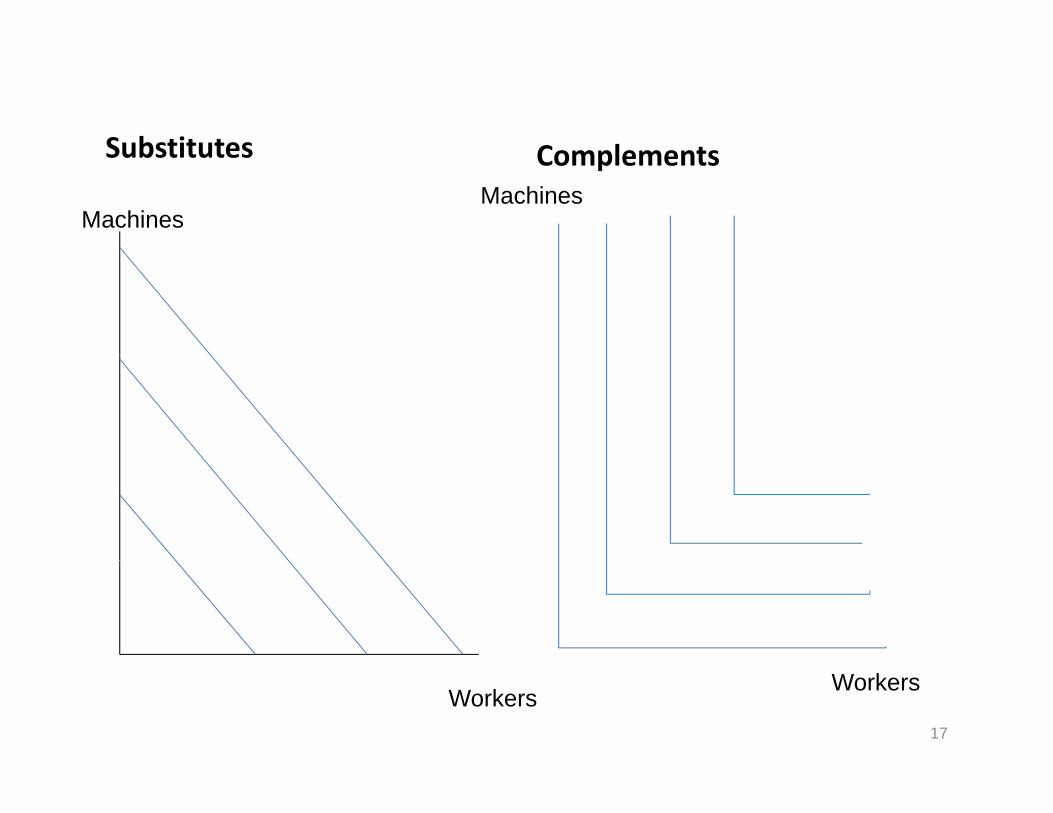

Substitutes ComplementsSubstitutes Complements

MachinesMachines

17

WorkersWorkers

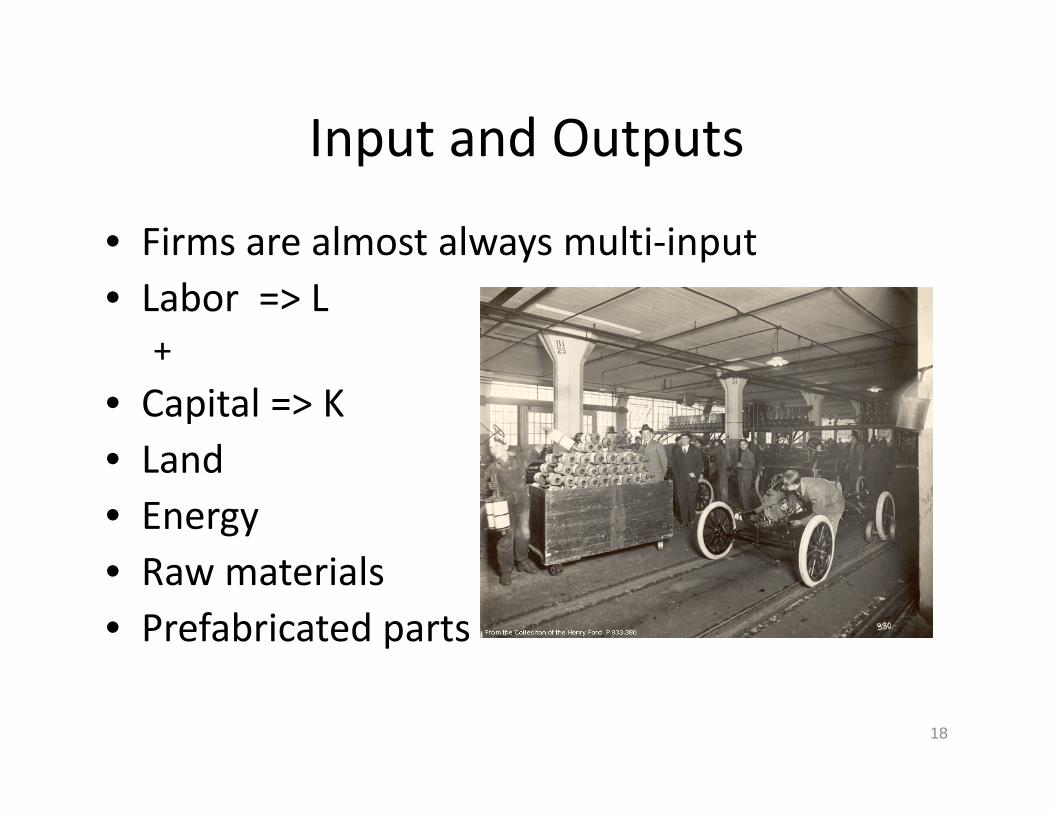

Input and OutputsInput and Outputs

• Firms are almost always multi‐inputFirms are almost always multi input• Labor => L

++

• Capital => K• Land• Land• EnergyR t i l• Raw materials

• Prefabricated parts

18

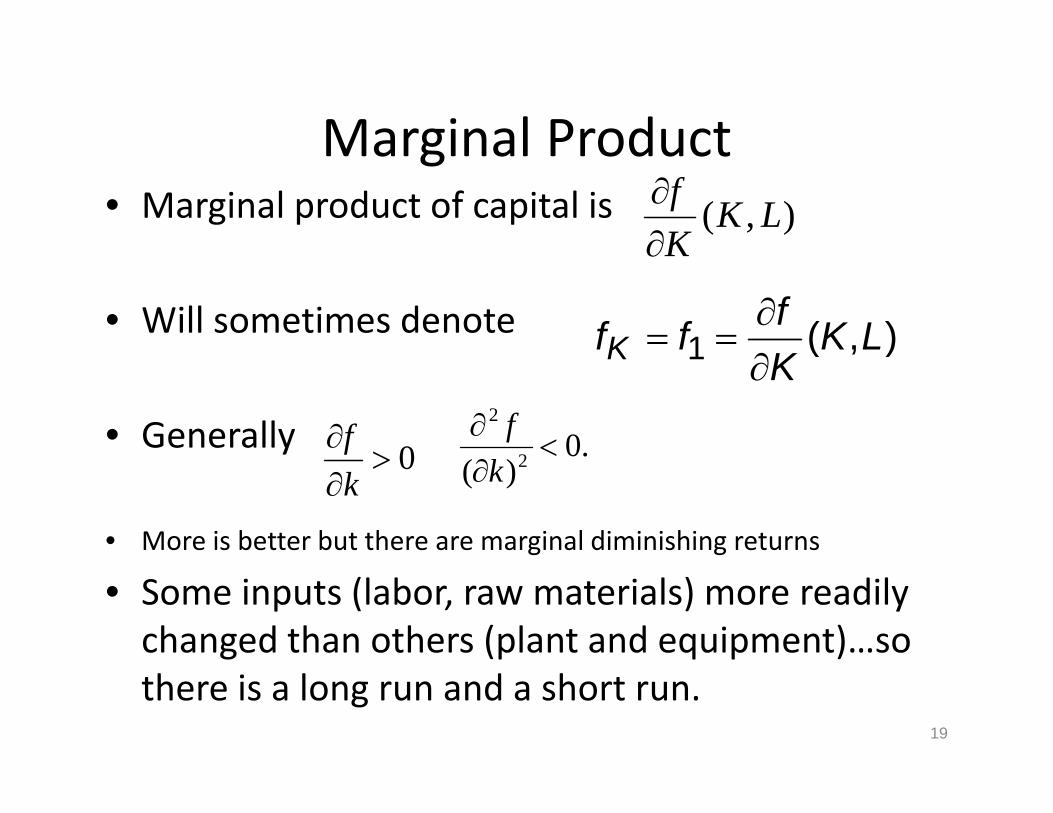

Marginal ProductMarginal Product• Marginal product of capital is ),( LK

Kf

• Will sometimes denote

K

),(1 LKKfffK

• Generally

)(1 KK

0f .02

2

f

• More is better but there are marginal diminishing returns

0k )( 2k

• Some inputs (labor, raw materials) more readily changed than others (plant and equipment)…so there is a long run and a short run.

19

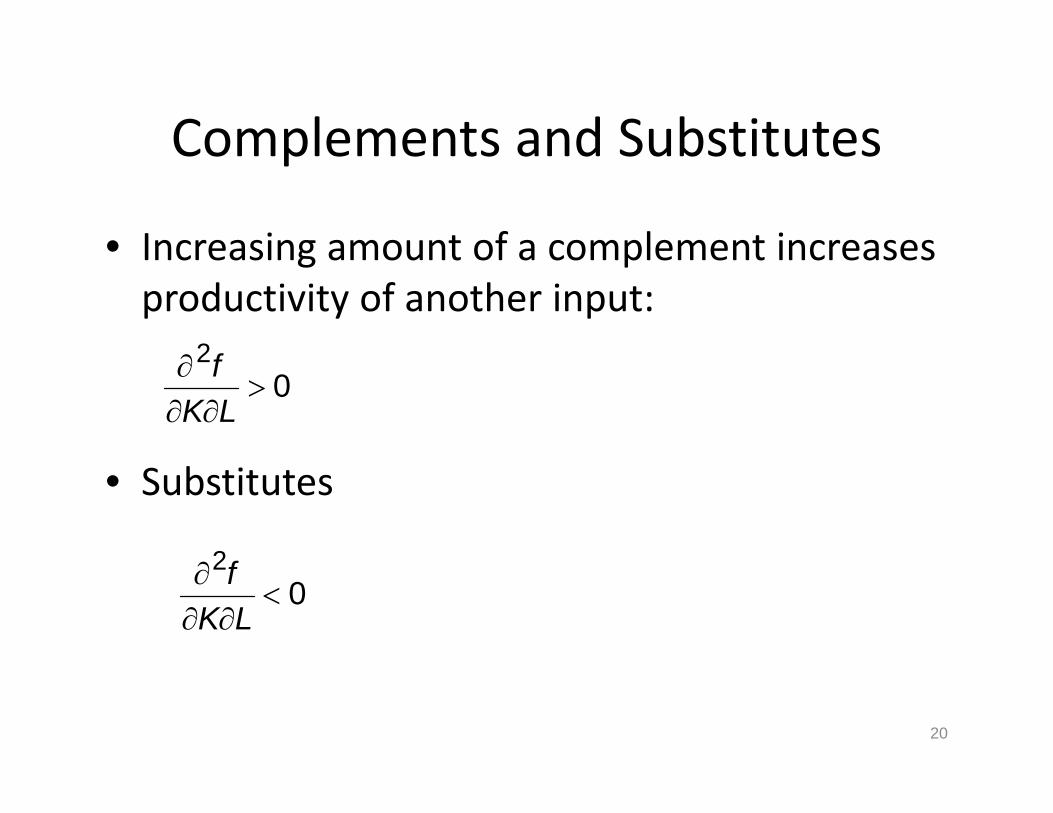

Complements and SubstitutesComplements and Substitutes

• Increasing amount of a complement increasesIncreasing amount of a complement increases productivity of another input:

2 f 02

LKf

• Substitutes

2f 02

LKf

20

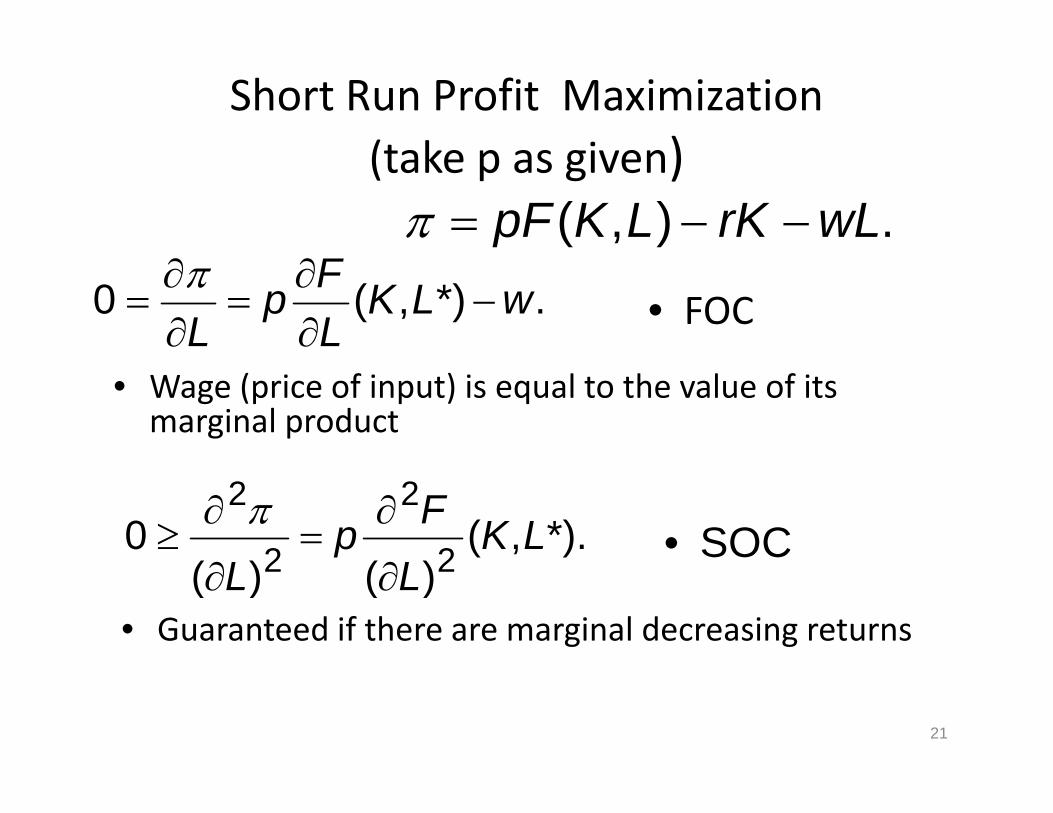

Short Run Profit Maximization(take p as given)(take p as given)

.),( wLrKLKpF

• FOC.*),(0 wLKLFp

L

• Wage (price of input) is equal to the value of its marginal product

*).,()()(

02

2

2

2LKFp

• SOC)()( 22 LL

• Guaranteed if there are marginal decreasing returns

21

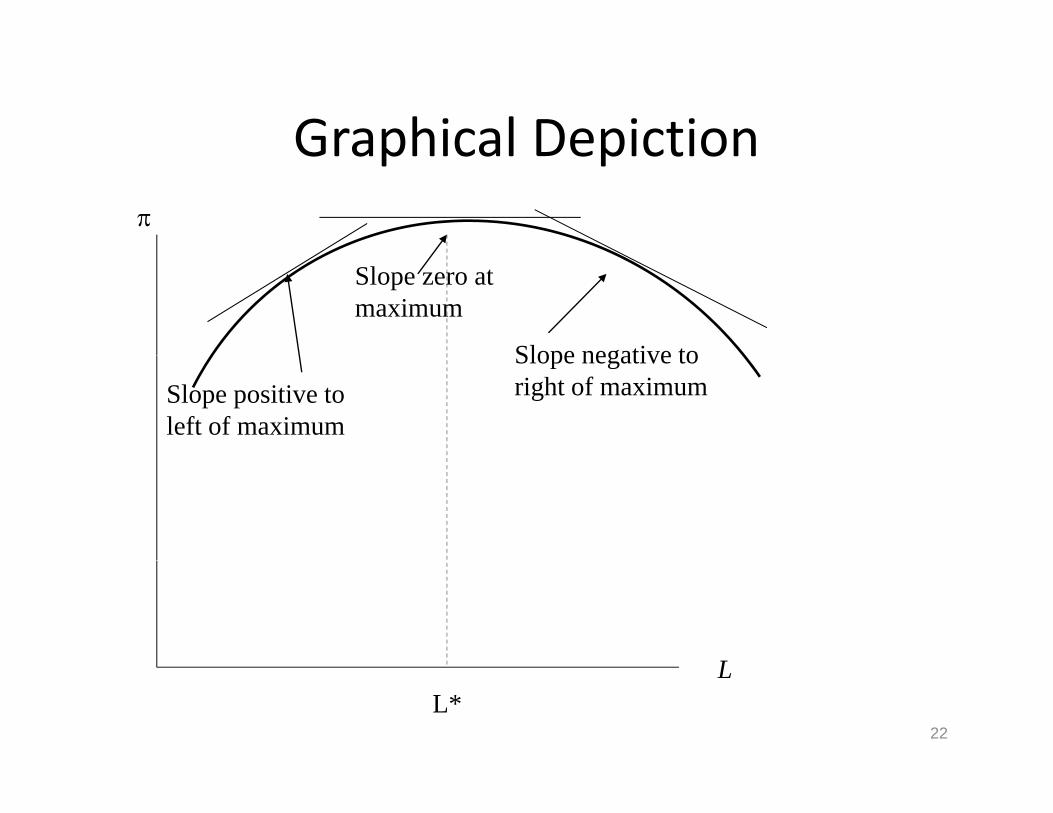

Graphical DepictionGraphical Depiction

Slope zero at maximum

Slope negative toSlope positive to left of maximum

Slope negative to right of maximum

LL*

L

22

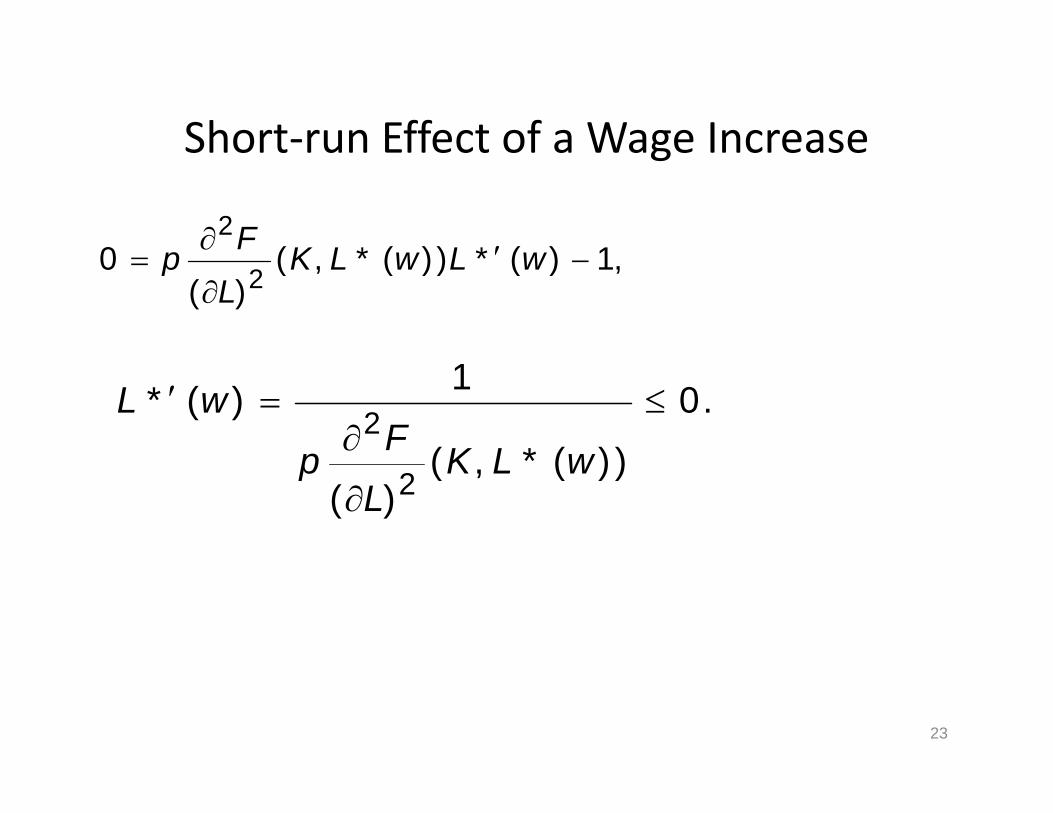

Short‐run Effect of a Wage IncreaseShort run Effect of a Wage Increase

1)(*))(*(02

wLwLK

Fp ,1)(*))(*,(

)(0

2

wLwLK

Lp

.0

))(*(

1)(*

2

wLKF

p

wL

))(*,()( 2

wLKL

p

23

Aside: Revealed PreferenceAside: Revealed Preference

• Revealed preference is a powerful techniqueRevealed preference is a powerful technique to prove comparative statics

• Works without assumptions about continuity• Works without assumptions about continuity or differentiability

S 1 2 l l• Suppose w1 < w2 are two wage levels

• The entrepreneur chooses L1 when the wage is w1 and L2 when the wage is w2

24

Revealed Preference ProofRevealed Preference Proof

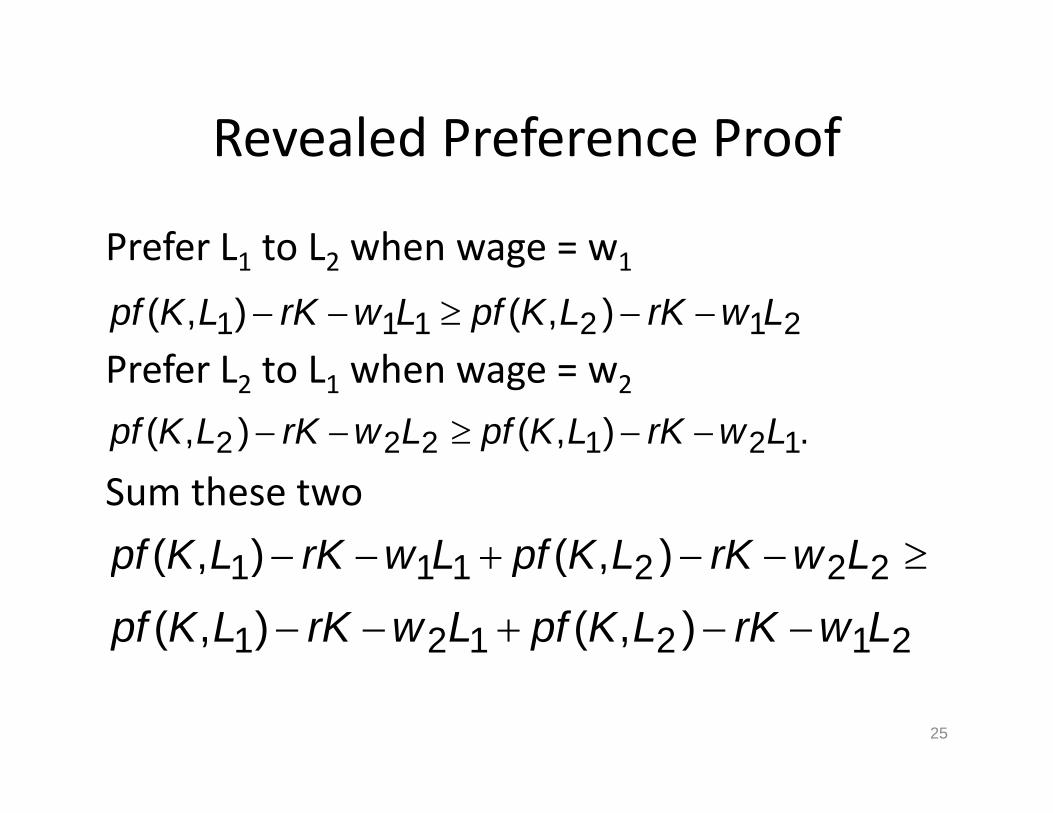

Prefer L1 to L2 when wage = w1Prefer L1 to L2 when wage = w1

f h212111 ),(),( LwrKLKpfLwrKLKpf

Prefer L2 to L1 when wage = w2

.),(),( 121222 LwrKLKpfLwrKLKpf

Sum these two

222111 )()( LwrKLKpfLwrKLKpf 222111 ),(),( LwrKLKpfLwrKLKpf

212121 ),(),( LwrKLKpfLwrKLKpf

25

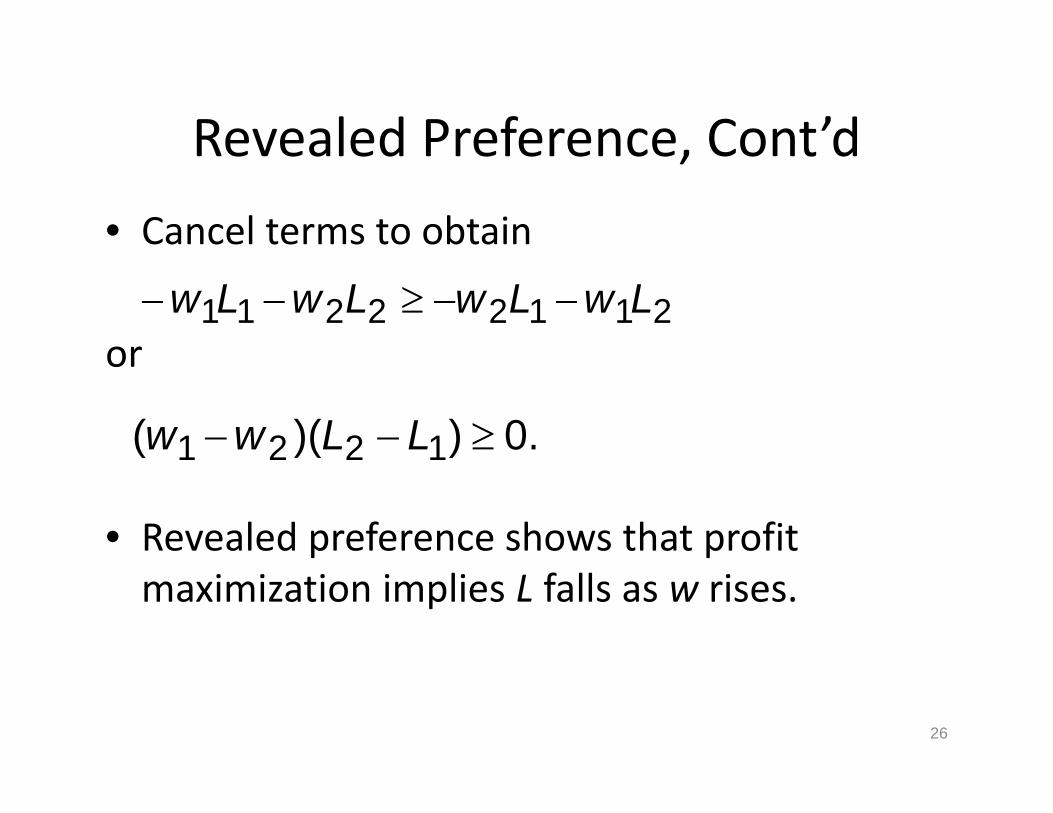

Revealed Preference, Cont’dRevealed Preference, Cont d

• Cancel terms to obtain

or21122211 LwLwLwLw

or

.0))(( 1221 LLww

• Revealed preference shows that profit

))(( 1221

maximization implies L falls as w rises.

26

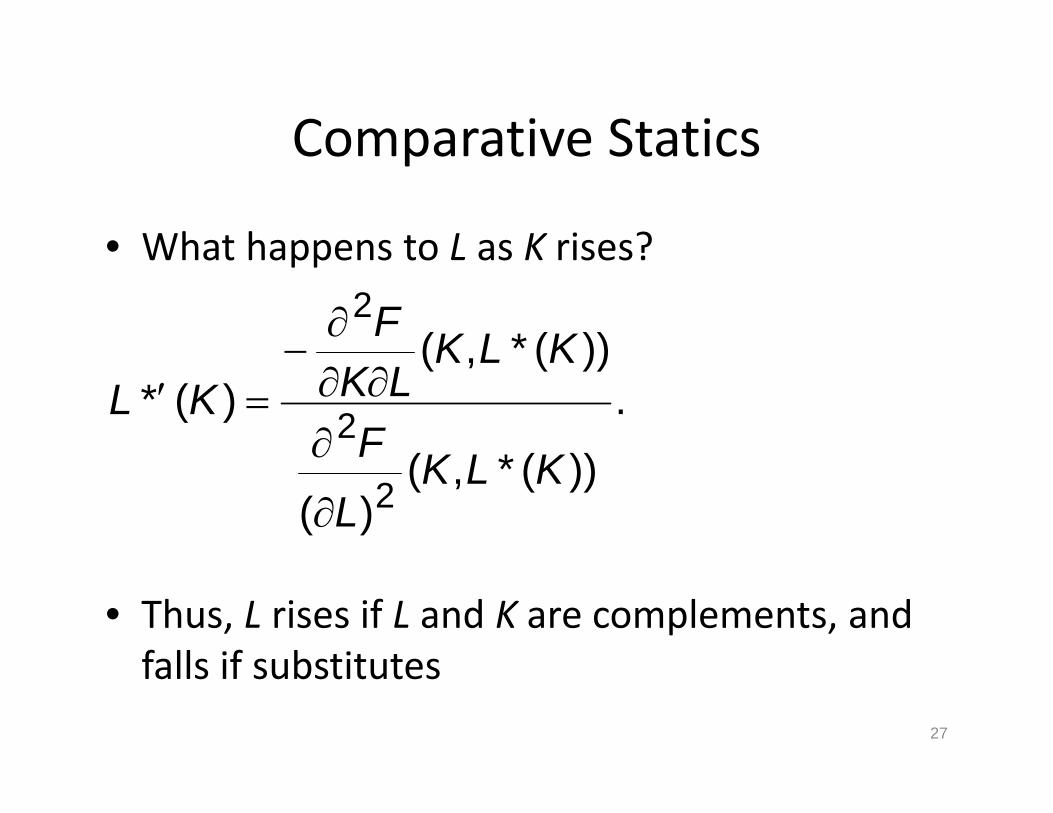

Comparative StaticsComparative Statics

• What happens to L as K rises?What happens to L as K rises?

))(*(2

KLKF

.))(*(

))(,()(*

2KLKF

KLKLKKL

))(*,()( 2

KLKL

• Thus, L rises if L and K are complements, and falls if substitutesfalls if substitutes

27

ApplicationsApplications

• Computers use has reduced demand forComputers use has reduced demand for secretarial services (substitutes)

• Increased technology generally has increased• Increased technology generally has increased demand for high‐skill workers (complements)

C i l f b i f i l l b• Capital often substitutes for simple labor (tractors, water pipes) and complements kill d l b ( i hi )skilled labor (operating machines)

28

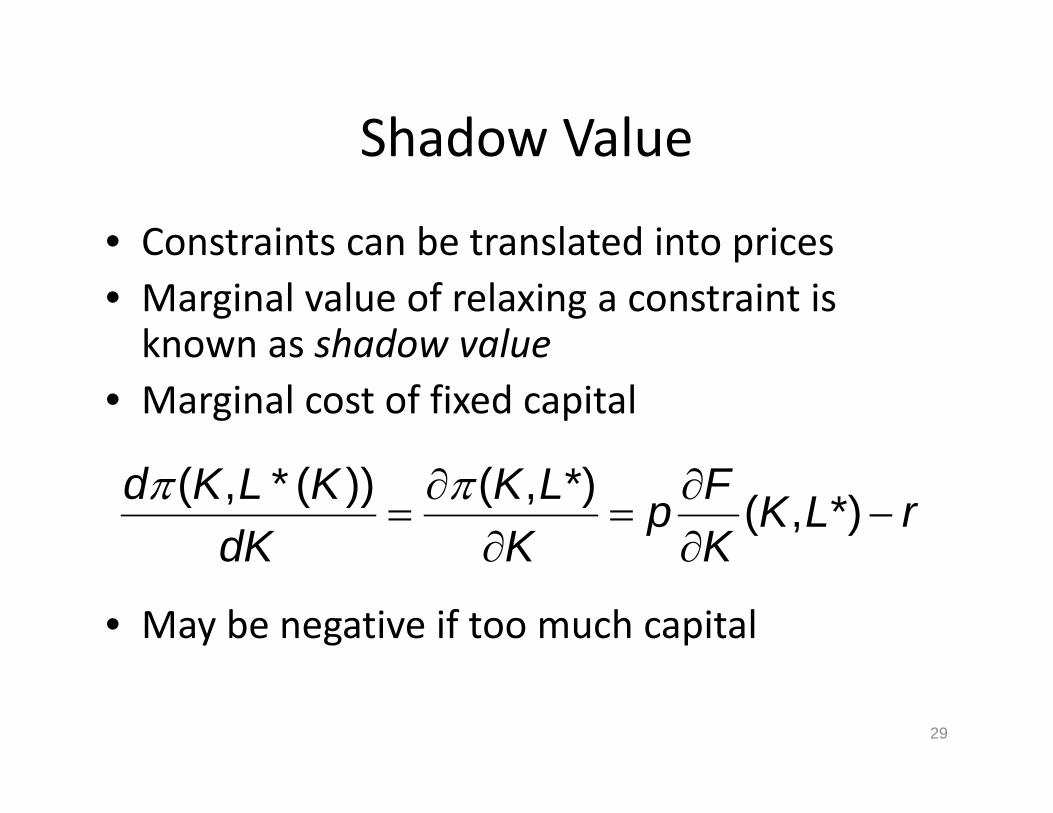

Shadow ValueShadow Value

• Constraints can be translated into pricesConstraints can be translated into prices• Marginal value of relaxing a constraint is known as shadow valueknown as shadow value

• Marginal cost of fixed capital

rLKKFp

KLK

dKKLKd

*),(*),())(*,(

• May be negative if too much capital

KKdK

29

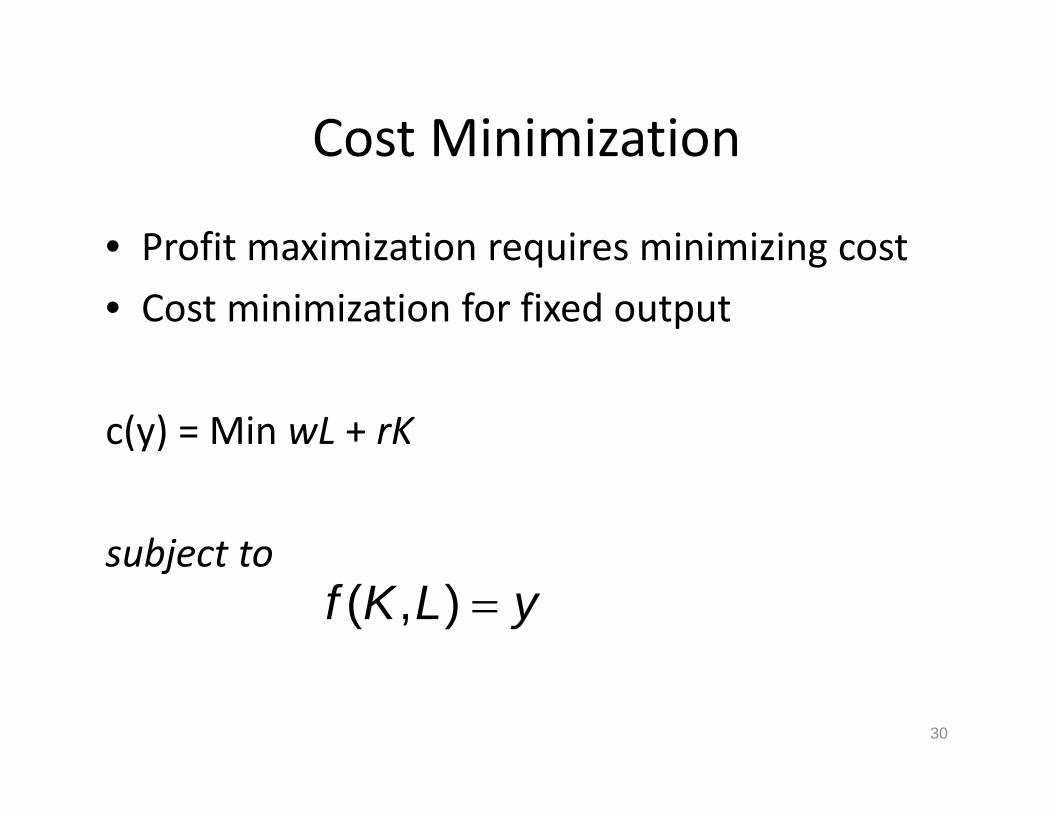

Cost MinimizationCost Minimization

• Profit maximization requires minimizing costProfit maximization requires minimizing cost

• Cost minimization for fixed output

c(y) = Min wL + rK

subject tosubject to yLKf ),(

30

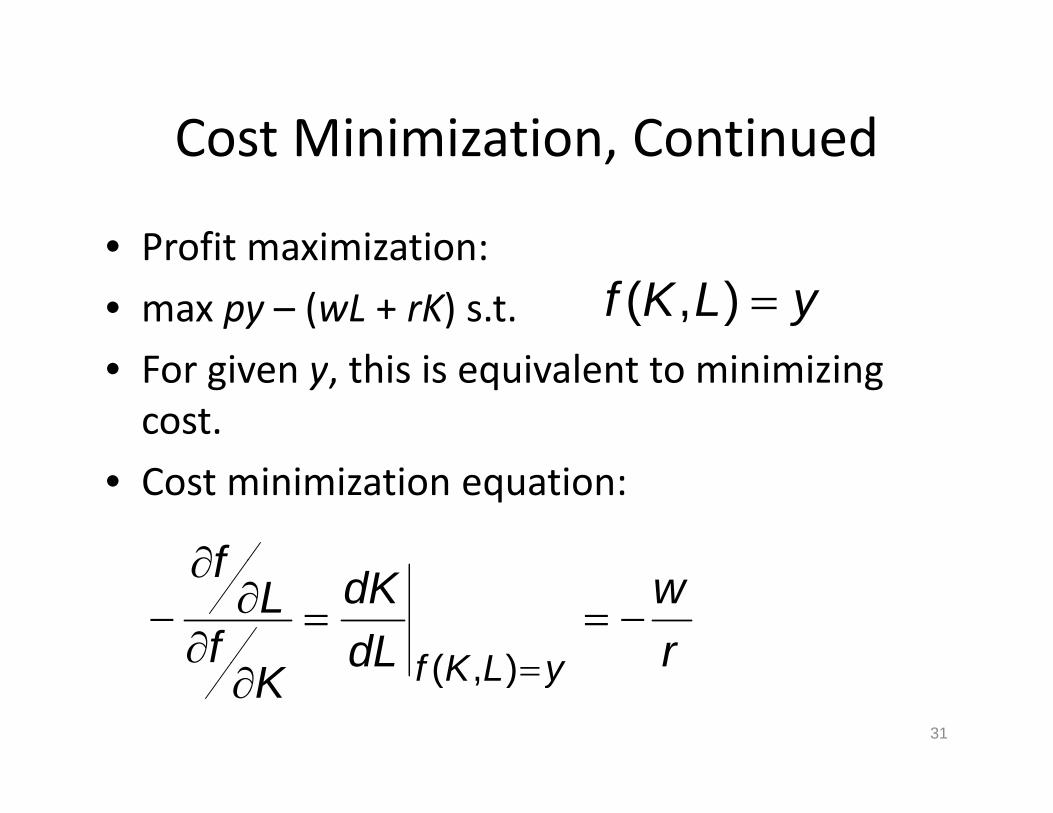

Cost Minimization, ContinuedCost Minimization, Continued

• Profit maximization:Profit maximization:

• max py – (wL + rK) s.t.

i hi i i l i i i i

yLKf ),(• For given y, this is equivalent to minimizing cost.

• Cost minimization equation:

f

rw

dLdK

fL

f

yLKf

)( rdLK yLKf ),(

31

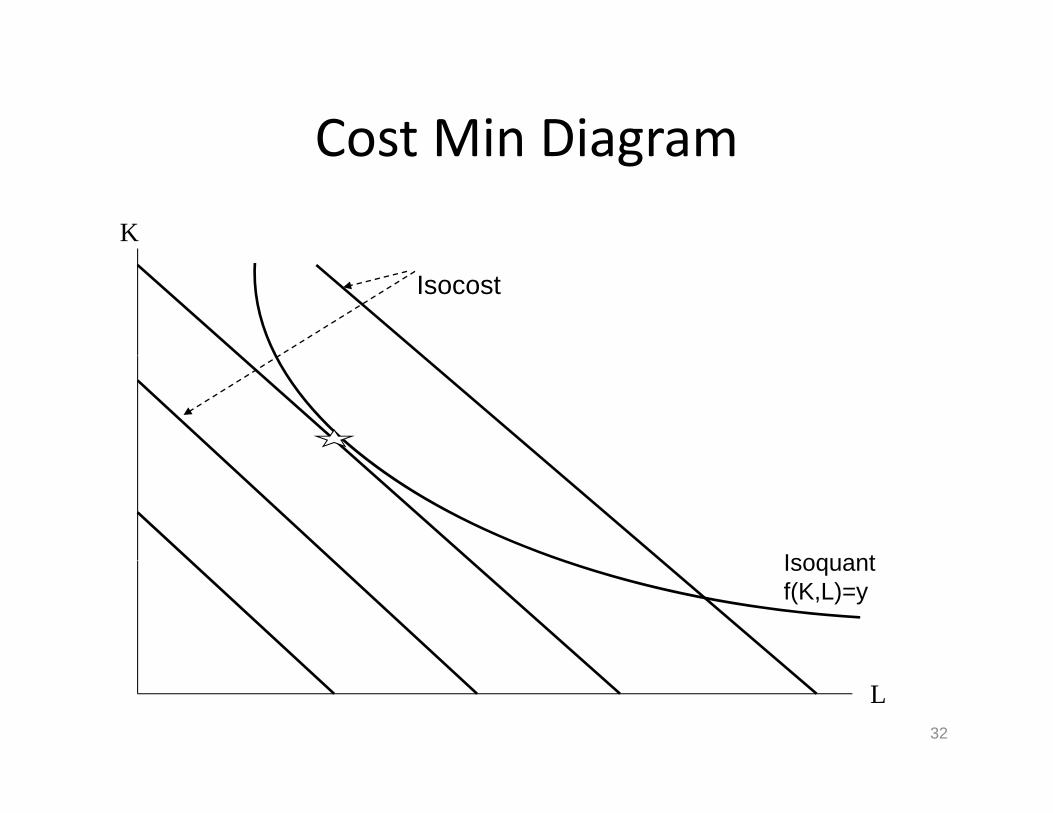

Cost Min DiagramCost Min Diagram

K

Isocost

IsoquantIsoquant f(K,L)=y

L32

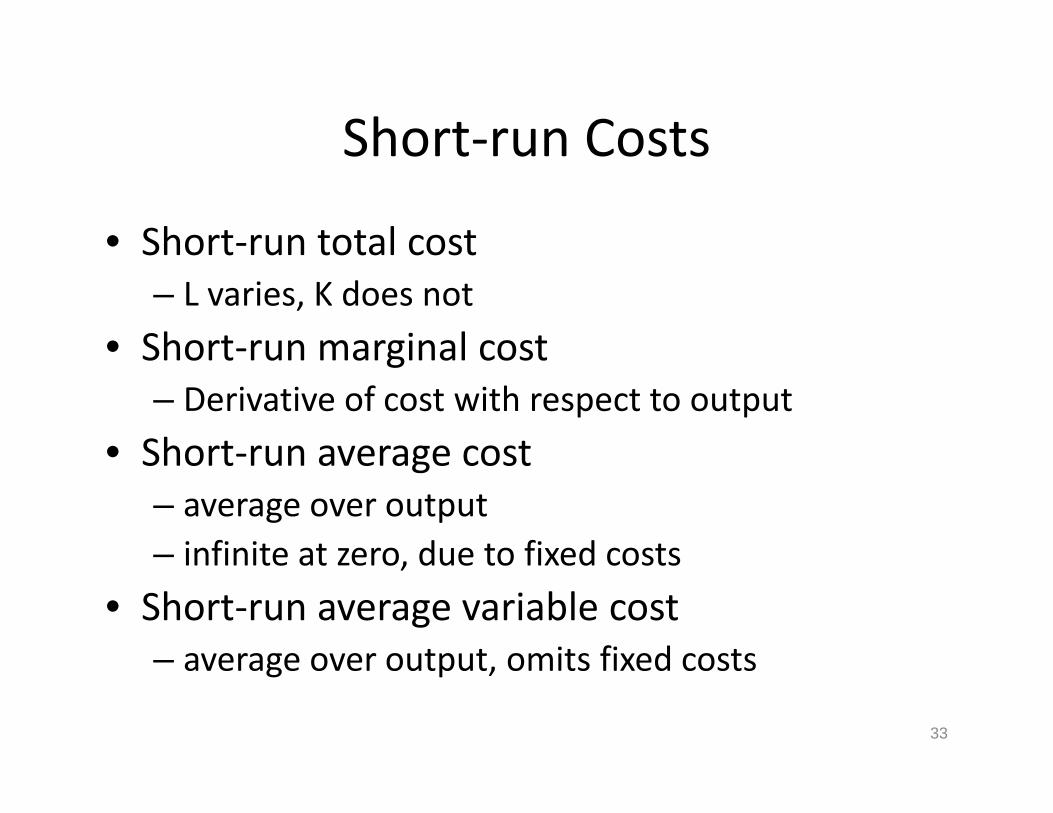

Short‐run CostsShort run Costs

• Short‐run total costShort run total cost– L varies, K does not

• Short‐run marginal costShort run marginal cost– Derivative of cost with respect to output

• Short‐run average costShort run average cost– average over output– infinite at zero due to fixed costsinfinite at zero, due to fixed costs

• Short‐run average variable cost– average over output omits fixed costsaverage over output, omits fixed costs

33