Embed Size (px)

DESCRIPTION

First American bank case solution : A case of credit default swaps (cds).

Citation preview

First American Bank: Credit Default Swaps

SUNWOO HWANG*

* KDI School of Public Policy and Management, Hoegi-ro 87, Dongdaemun-gu, Seoul, 130-868, Korea.

HBS Case Study

Introduction

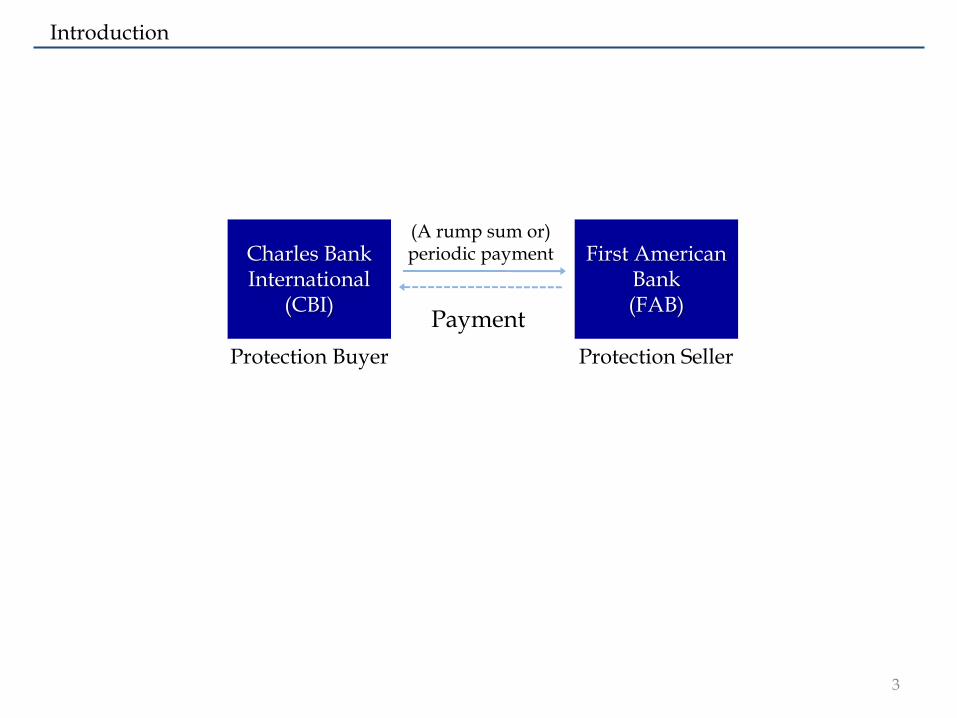

Introduction

3

Charles Bank International

(CBI)

First American Bank (FAB)

(A rump sum or) periodic payment

Protection Buyer Protection Seller

Payment

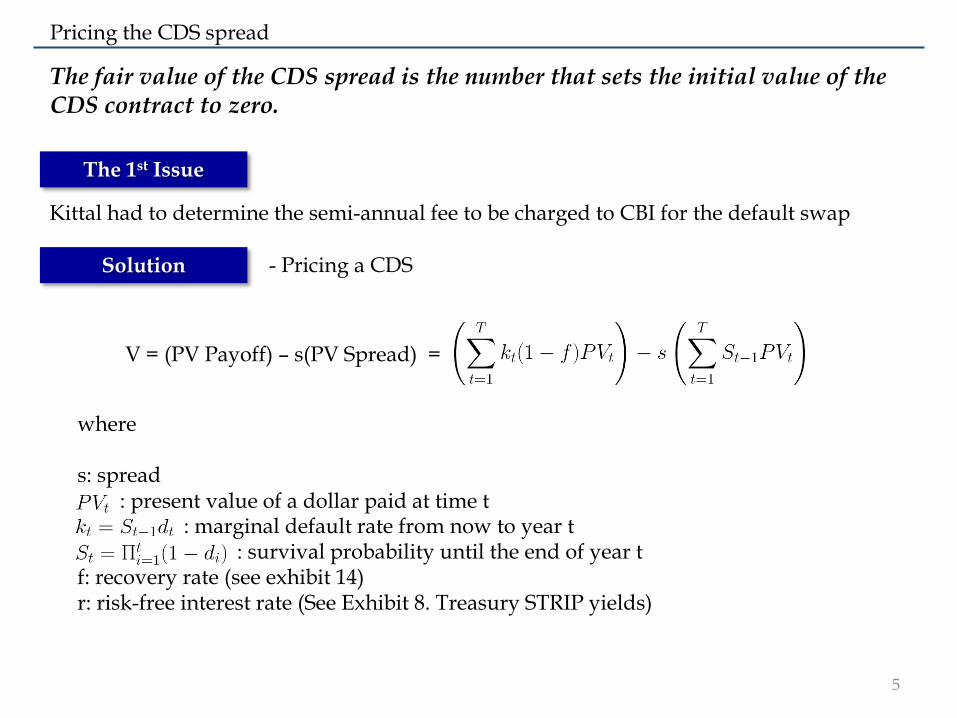

The 1st Issue

Pricing the CDS spread

5

The fair value of the CDS spread is the number that sets the initial value of the CDS contract to zero.

V = (PV Payoff) – s(PV Spread) =

where

s: spread: present value of a dollar paid at time t

: marginal default rate from now to year t : survival probability until the end of year t

f: recovery rate (see exhibit 14)r: risk-free interest rate (See Exhibit 8. Treasury STRIP yields)

The 1st Issue

Solution

Kittal had to determine the semi-annual fee to be charged to CBI for the default swap

- Pricing a CDS

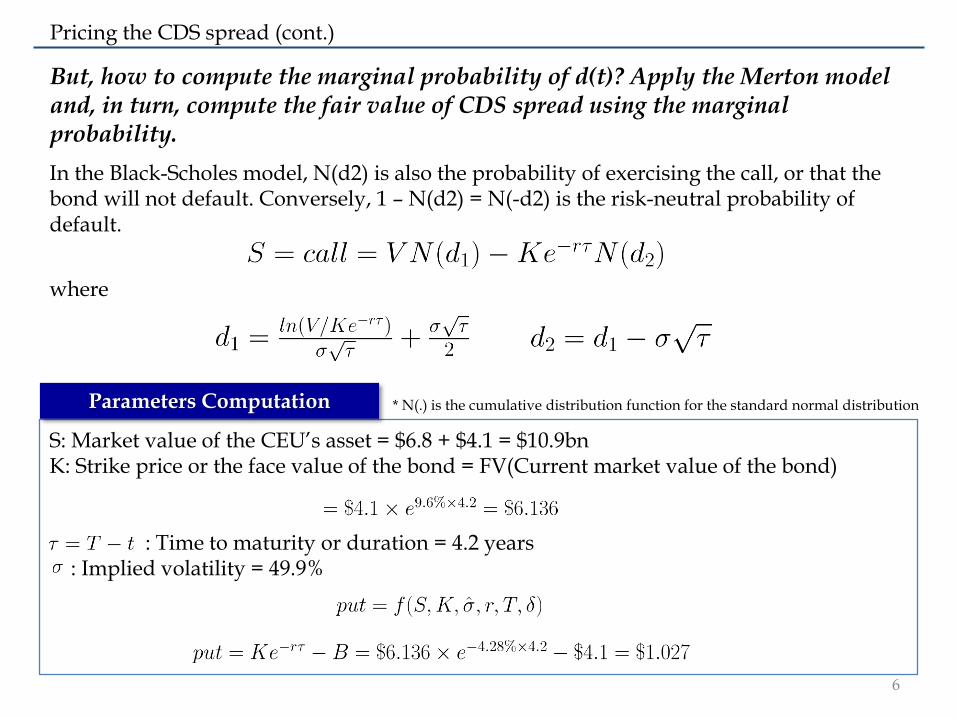

Pricing the CDS spread (cont.)

6

But, how to compute the marginal probability of d(t)? Apply the Merton model and, in turn, compute the fair value of CDS spread using the marginal probability.

In the Black-Scholes model, N(d2) is also the probability of exercising the call, or that the bond will not default. Conversely, 1 – N(d2) = N(-d2) is the risk-neutral probability of default.

where

* N(.) is the cumulative distribution function for the standard normal distribution

S: Market value of the CEU’s asset = $6.8 + $4.1 = $10.9bnK: Strike price or the face value of the bond = FV(Current market value of the bond)

: Time to maturity or duration = 4.2 years: Implied volatility = 49.9%

Parameters Computation

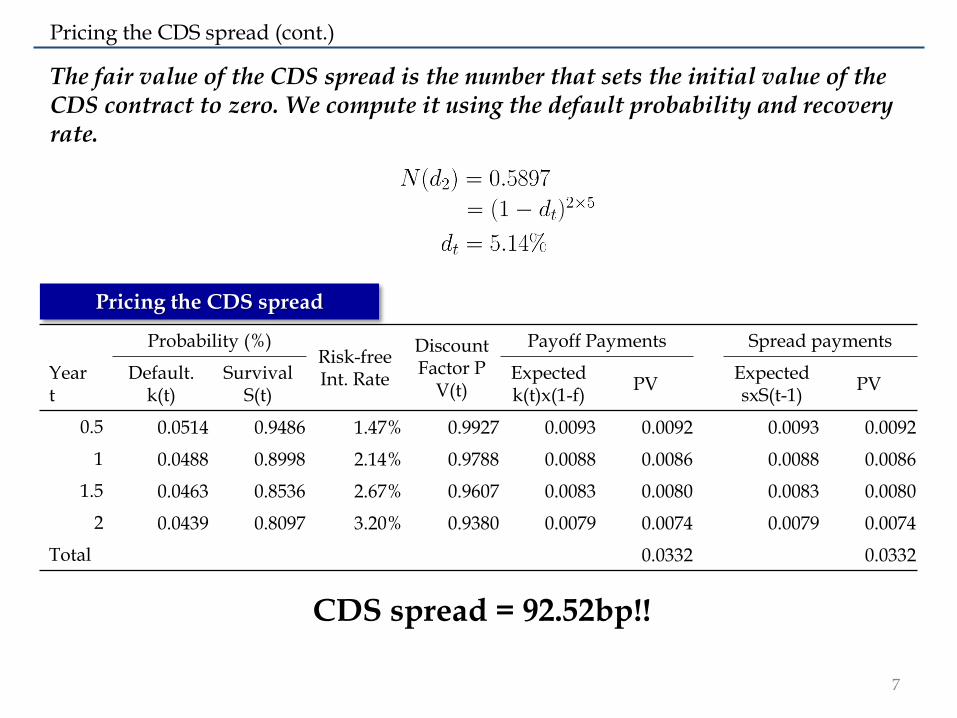

Pricing the CDS spread (cont.)

7

The fair value of the CDS spread is the number that sets the initial value of the CDS contract to zero. We compute it using the default probability and recovery rate.

Probability (%)Risk-free Int. Rate

Discount Factor P

V(t)

Payoff Payments Spread payments

Yeart

Default.k(t)

SurvivalS(t)

Expectedk(t)x(1-f)

PVExpectedsxS(t-1)

PV

0.5 0.0514 0.9486 1.47% 0.9927 0.0093 0.0092 0.0093 0.0092

1 0.0488 0.8998 2.14% 0.9788 0.0088 0.0086 0.0088 0.0086

1.5 0.0463 0.8536 2.67% 0.9607 0.0083 0.0080 0.0083 0.0080

2 0.0439 0.8097 3.20% 0.9380 0.0079 0.0074 0.0079 0.0074

Total 0.0332 0.0332

CDS spread = 92.52bp!!

Pricing the CDS spread

The 2nd Issue

Solution to the Second Issue

9

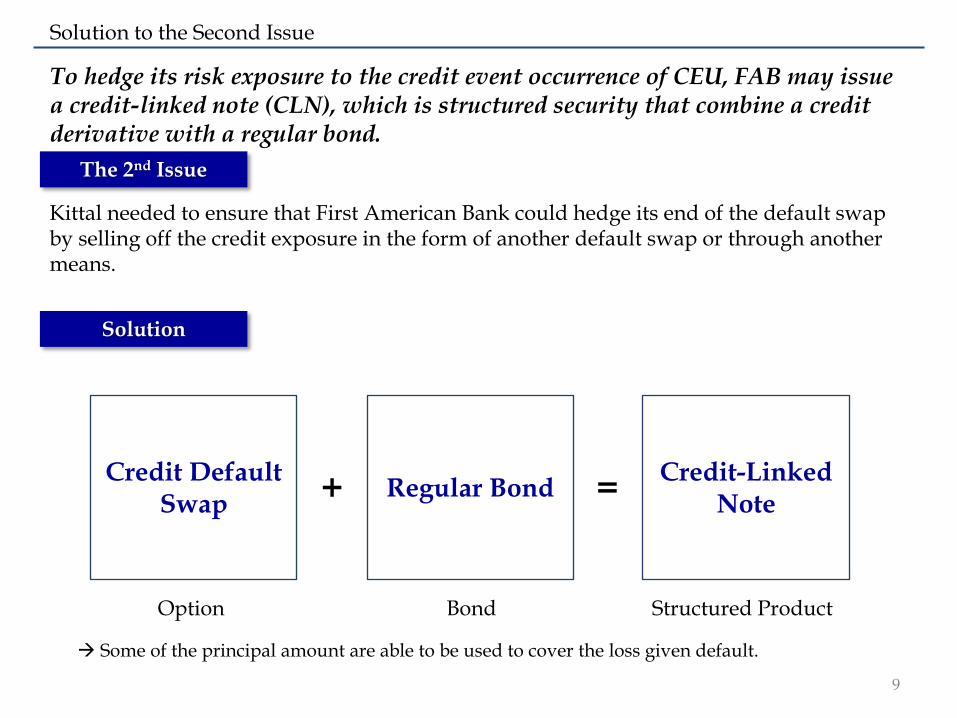

To hedge its risk exposure to the credit event occurrence of CEU, FAB may issue a credit-linked note (CLN), which is structured security that combine a credit derivative with a regular bond.

The 2nd Issue

Solution

Kittal needed to ensure that First American Bank could hedge its end of the default swap by selling off the credit exposure in the form of another default swap or through another means.

Credit Default Swap

Regular Bond+Credit-Linked

Note=

Option Bond

Some of the principal amount are able to be used to cover the loss given default.

Structured Product

Accounting interpretation

10

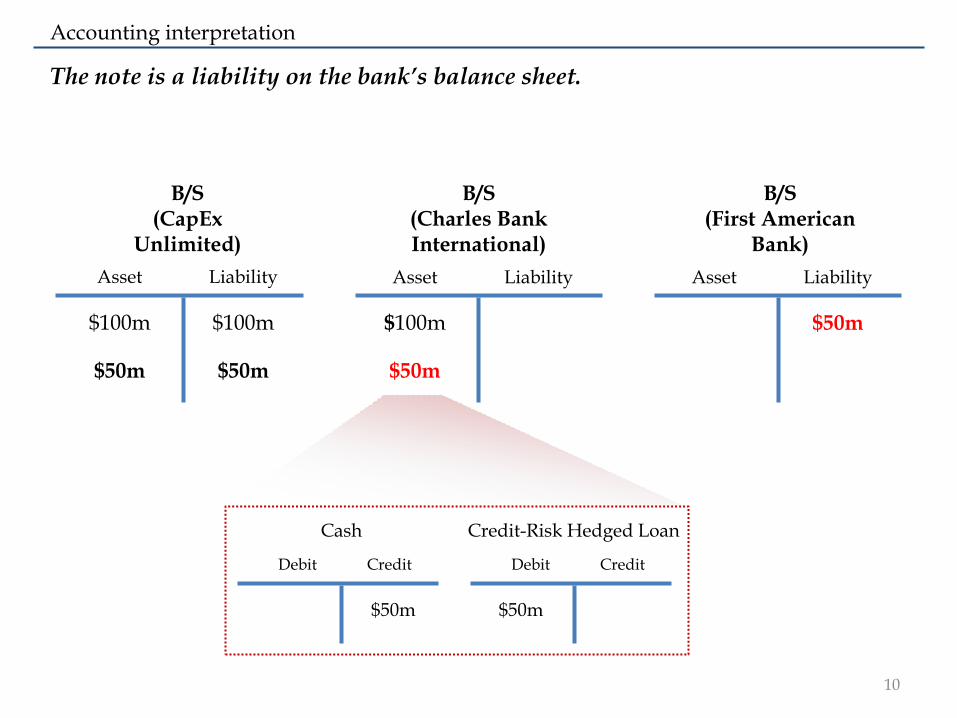

The note is a liability on the bank’s balance sheet.

B/S (CapEx

Unlimited)

B/S (Charles Bank International)

B/S (First American

Bank)

$100m $100m

Asset Liability Asset Liability Asset Liability

$50m $50m

$100m

$50m

$50m

Cash

Debit Credit

$50m

Credit-Risk Hedged Loan

Debit Credit

$50m

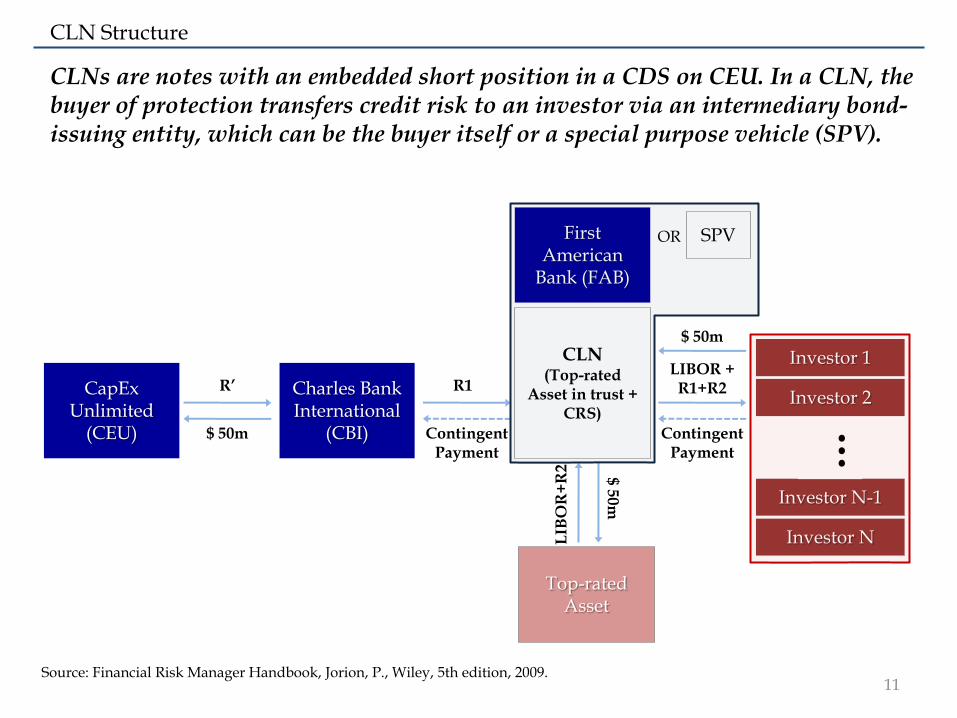

CLN Structure

11

CLNs are notes with an embedded short position in a CDS on CEU. In a CLN, the buyer of protection transfers credit risk to an investor via an intermediary bond-issuing entity, which can be the buyer itself or a special purpose vehicle (SPV).

CapExUnlimited

(CEU)

Charles Bank International

(CBI)

First American

Bank (FAB)

Investor 1

Investor 2

Investor N-1

Investor N

…

Top-rated Asset

Contingent Payment

$ 50m

$ 50m$ 5

0m

R’ R1LIBOR +

R1+R2

LIB

OR

+R

2

CLN (Top-rated

Asset in trust + CRS)

SPVOR

Contingent Payment

Source: Financial Risk Manager Handbook, Jorion, P., Wiley, 5th edition, 2009.

CLN Structure (cont.)

12

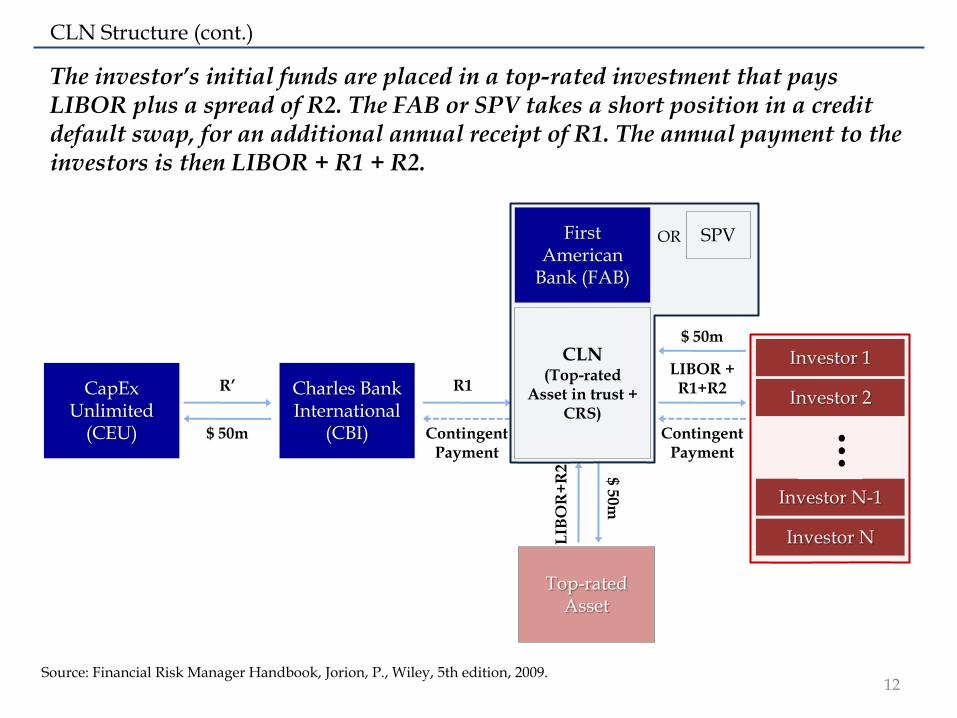

The investor’s initial funds are placed in a top-rated investment that pays LIBOR plus a spread of R2. The FAB or SPV takes a short position in a credit default swap, for an additional annual receipt of R1. The annual payment to the investors is then LIBOR + R1 + R2.

Source: Financial Risk Manager Handbook, Jorion, P., Wiley, 5th edition, 2009.

CapExUnlimited

(CEU)

Charles Bank International

(CBI)

First American

Bank (FAB)

Investor 1

Investor 2

Investor N-1

Investor N

…

Top-rated Asset

Contingent Payment

$ 50m

$ 50m$ 5

0m

R’ R1LIBOR +

R1+R2

LIB

OR

+R

2

CLN (Top-rated

Asset in trust + CRS)

SPVOR

Contingent Payment

Additional Remarks

- Investors receive a high coupon but will lose some of the principal if CEU defaults on its debt.

- This structure achieves its goal of reducing the bank’s exposure if CEU defaults.

- In this case, because the note is a liability of the bank, the investor is exposed to a default of either ECU or of the bank FAB.

13

Pros and Cons

Attractiveness

- Relative to a regular investment in, say, a note issued by the government of the United States, this structure may carry a higher yield if the CDS spread is greater than the bond yield spread.

- This structure may also be attractive to investors who are precluded from investing directly in derivatives.