Embed Size (px)

DESCRIPTION

First Presbyterian Church CollegeCARE Ministries presents Smart Personal Finance Workshop. By Dave Berkow & Kevin Kelley. Banking. The Role of Banks. Banks are in business to earn a profit! HOW???? Interest, Fees, Financial Advice Banks provide security! HOW???? - PowerPoint PPT Presentation

Citation preview

First Presbyterian ChurchCollegeCARE Ministries

presents

Smart Personal Finance Workshop

By Dave Berkow

& Kevin Kelley

Banking

The Role of Banks• Banks are in business to earn a profit!

– HOW????– Interest, Fees, Financial Advice

• Banks provide security!– HOW????– FDIC (Federal Deposit Insurance Corporation)

• Insures deposits up to $250,000

• Banks make mistakes– Balance your accounts

Types of Money

• Currency• Debit Cards

• Checks• Credit Cards

http://www.checksinthemail.com/

Types of Money• Advantages of Using Checks

– Safety• Valuable only to payee• Legal proof of payment• If lose checkbook, money is safe

– Convenience– Help keep financial records– You can send via mail– Online account access

Your Checking Account

• What do you need to Opening a Checking Account?– Be 18 years old or older– Signature card (record of signature)– Valid identification– Initial deposit (some banks will give you money

to open an account)

• Account signatures• Add your parents

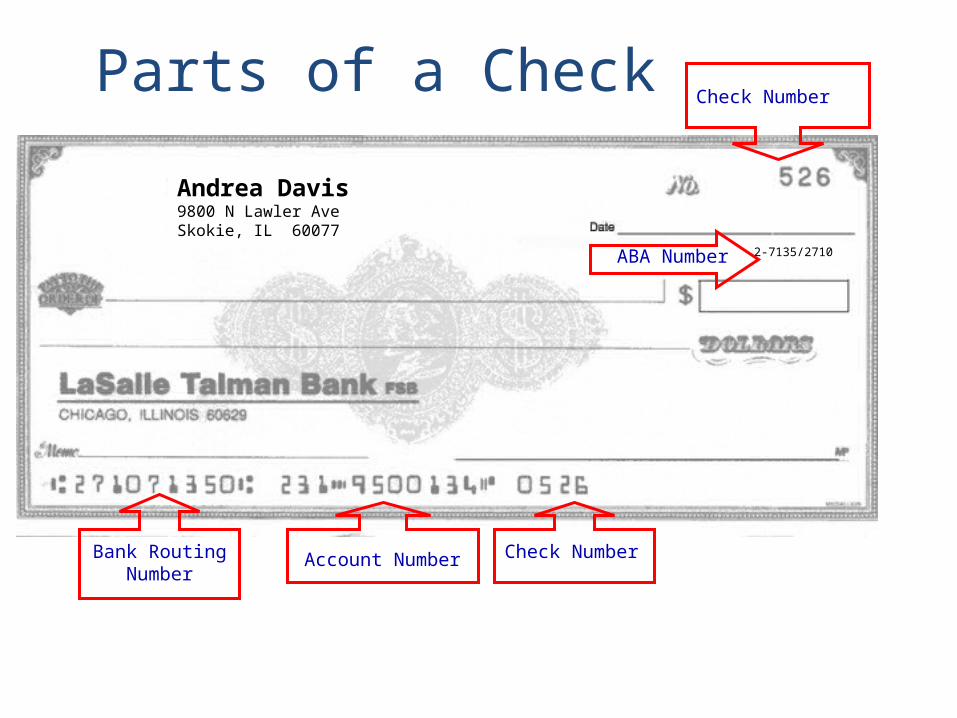

Parts of a Check

2-7135/2710

Check Number

Check NumberBank RoutingNumber

Account Number

ABA Number

Andrea Davis9800 N Lawler AveSkokie, IL 60077

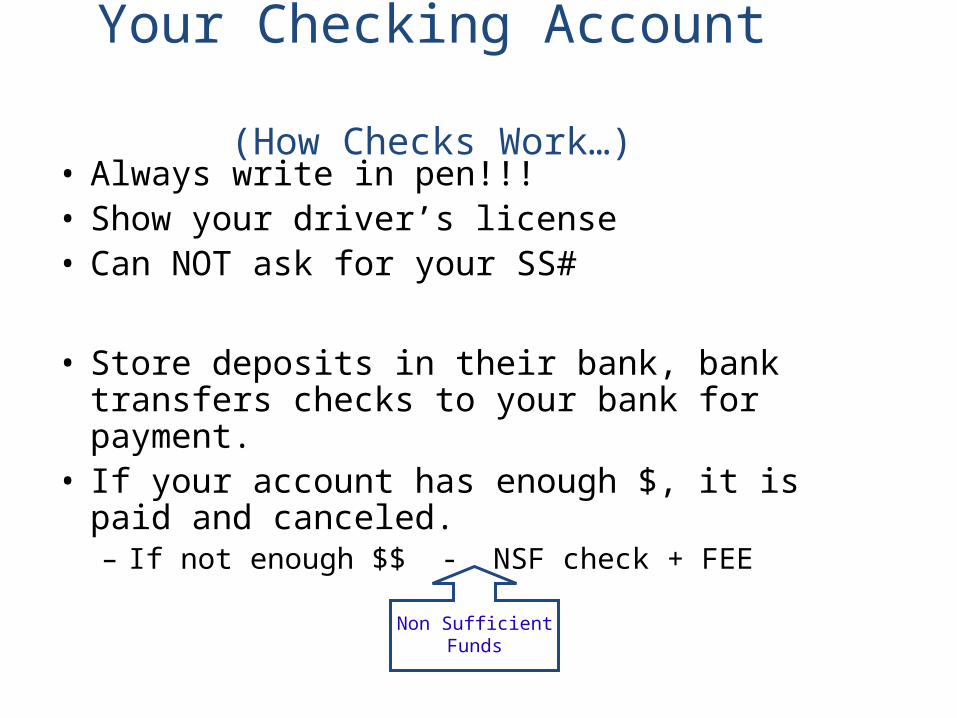

Your Checking Account (How Checks Work…)

• Always write in pen!!!• Show your driver’s license• Can NOT ask for your SS#

• Store deposits in their bank, bank transfers checks to your bank for payment.

• If your account has enough $, it is paid and canceled.– If not enough $$ - NSF check + FEE

Non Sufficient Funds

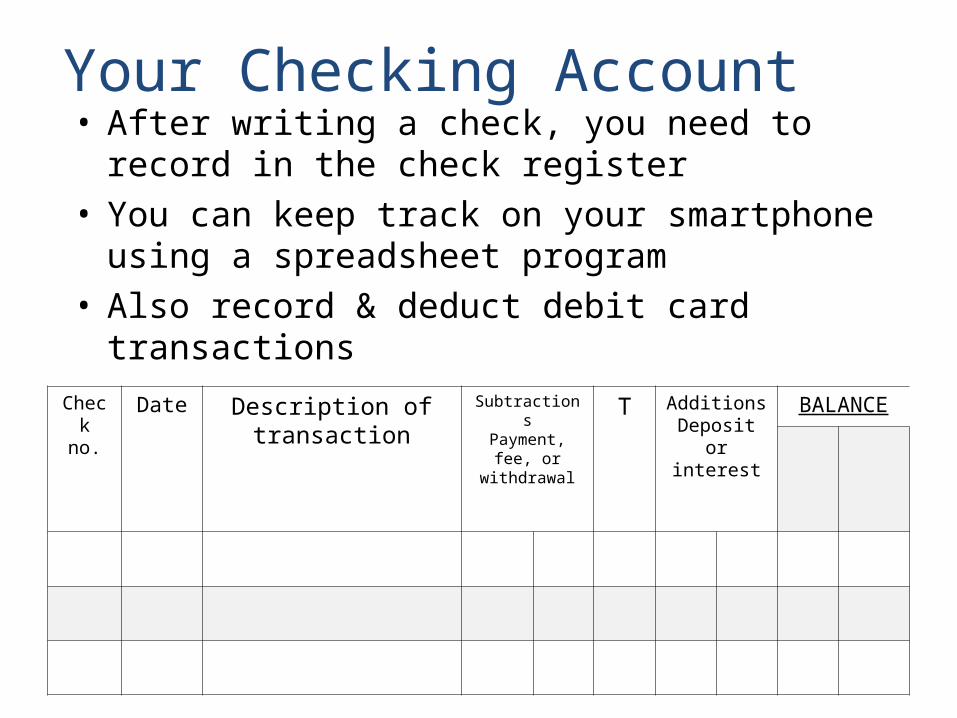

Your Checking Account• After writing a check, you need to record in the

check register• You can keep track on your smartphone using a

spreadsheet program• Also record & deduct debit card transactions

Checkno.

Date Description of transaction

SubtractionsPayment, fee, or withdrawal

T AdditionsDeposit or

interest

BALANCE

• WARNING: The speed of deducting $$ from your checking account will increase. Be certain you have enough money before you write the check.

Endorsements• Instructions and permission to

the bank about what to do with the check:– Cash it– Put it in your account– Put some in your account and

take some in cash– Pass it along to someone else

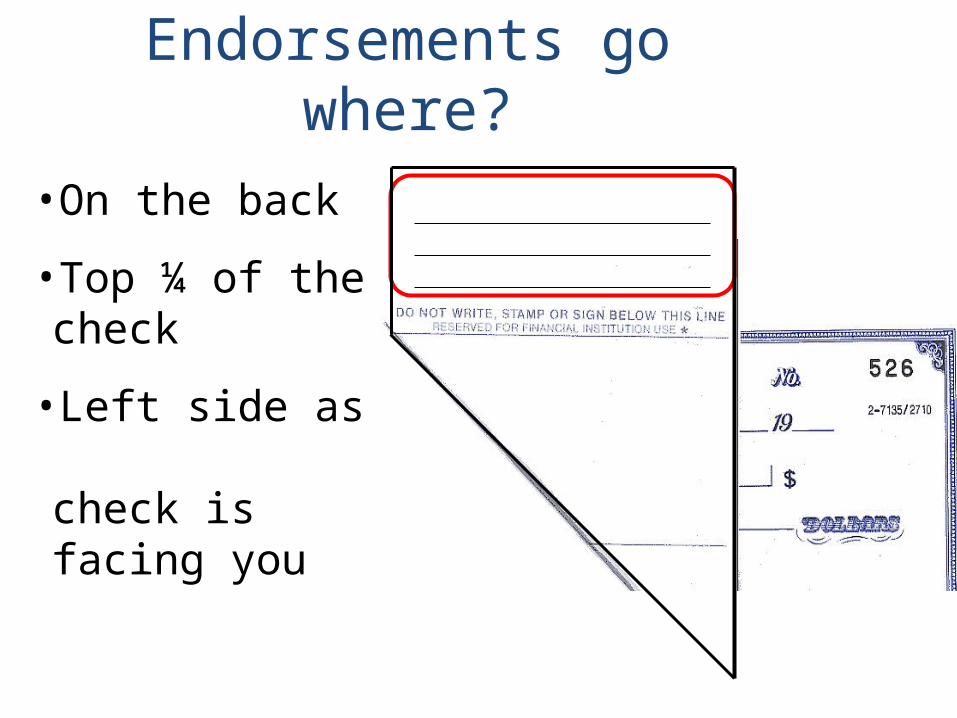

Endorsements go where?

•On the back

•Top ¼ of the check

•Left side as check is facing you

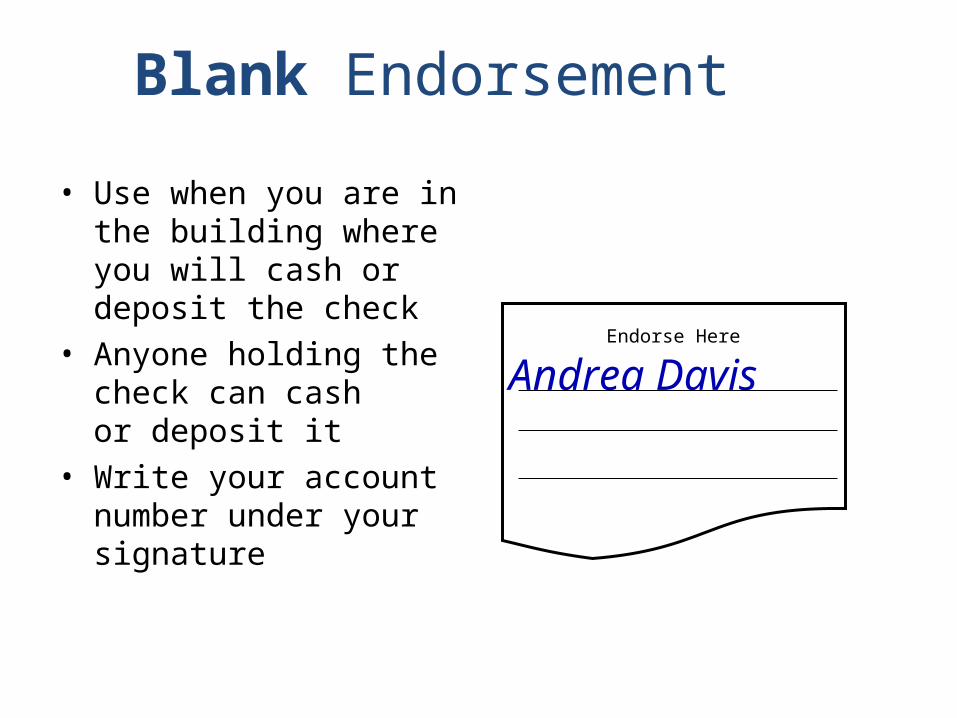

Blank Endorsement

• Use when you are in the building where you will cash or deposit the check

• Anyone holding the check can cash or deposit it

• Write your account number under your signature

Endorse Here

Andrea Davis

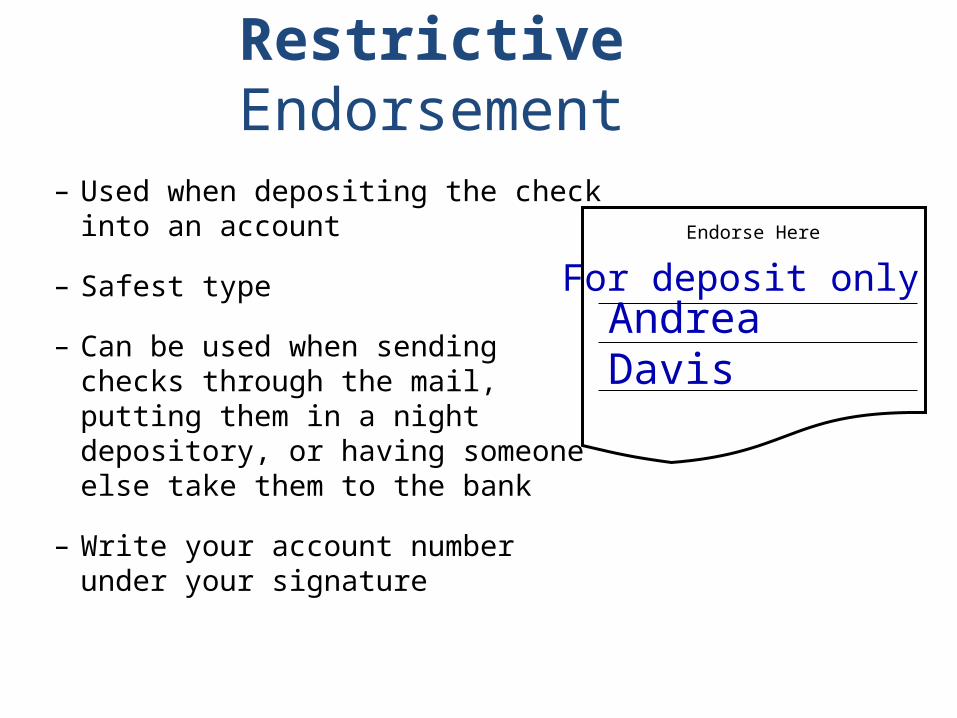

Restrictive Endorsement

– Used when depositing the check into an account

– Safest type

– Can be used when sending checks through the mail, putting them in a night depository, or having someone else take them to the bank

– Write your account number under your signature

Endorse Here

For deposit onlyAndrea Davis

Your Checking Account

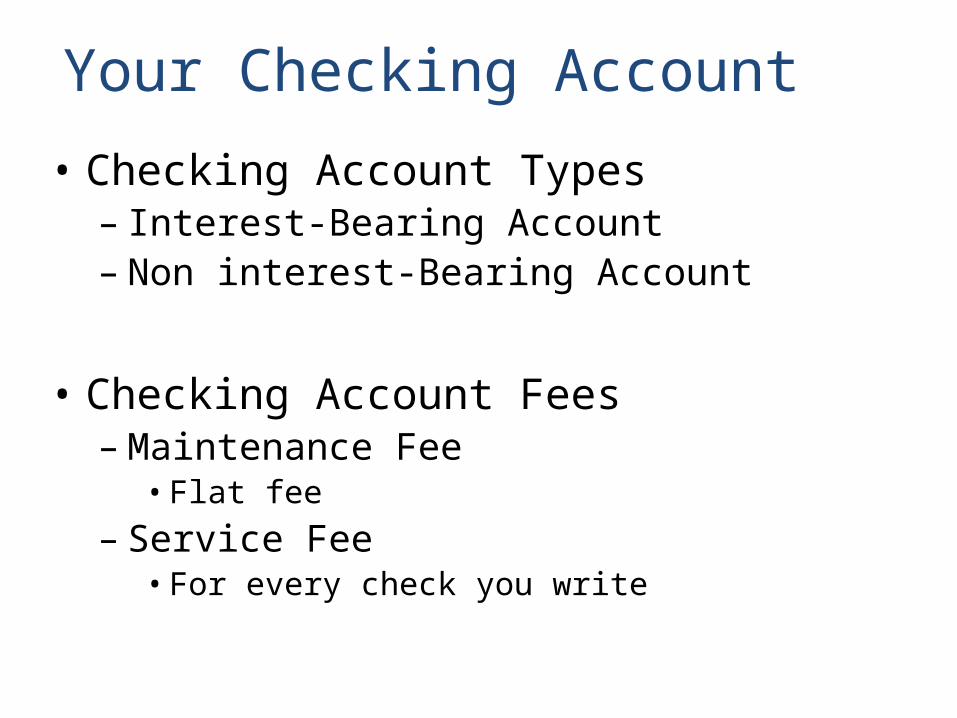

• Checking Account Types– Interest-Bearing Account– Non interest-Bearing Account

• Checking Account Fees– Maintenance Fee

• Flat fee – Service Fee

• For every check you write

Electronic Banking

• Automated Teller Machines• Electronic Funds Transfer – move

money from 1 account to another by computer

• Use of Electronic Funds– Direct Deposit– Debit Cards– Automatic Bill Payment

• Pay by Phone• Automatic Withdrawals

– Online Banking

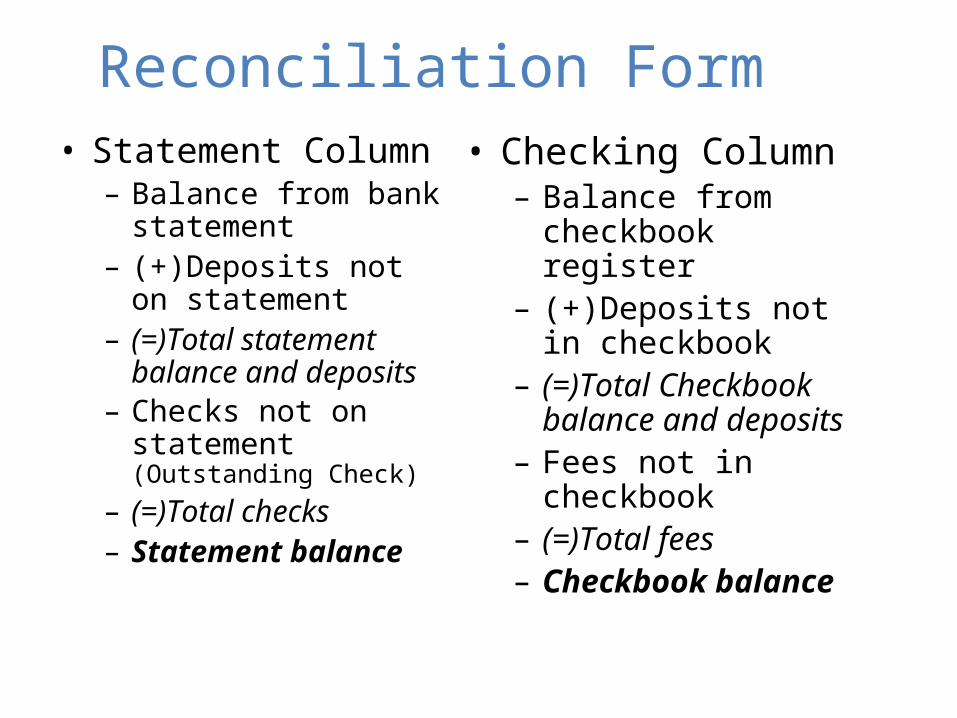

Reconciliation Form• Statement Column

– Balance from bank statement

– (+)Deposits not on statement

– (=)Total statement balance and deposits

– Checks not on statement (Outstanding Check)

– (=)Total checks– Statement balance

• Checking Column– Balance from checkbook

register– (+)Deposits not in

checkbook– (=)Total Checkbook

balance and deposits– Fees not in checkbook– (=)Total fees – Checkbook balance

Savings Accounts

• Earn greater interest than checking• May have withdrawal restrictions• Use for funds not immediately required

Debit Cards

• Used like a check to access funds in your checking account

• Can also be linked to a savings account• Potential pitfalls

– liability

The Daily ShowThe Daily ShowTrendspotting---Credit

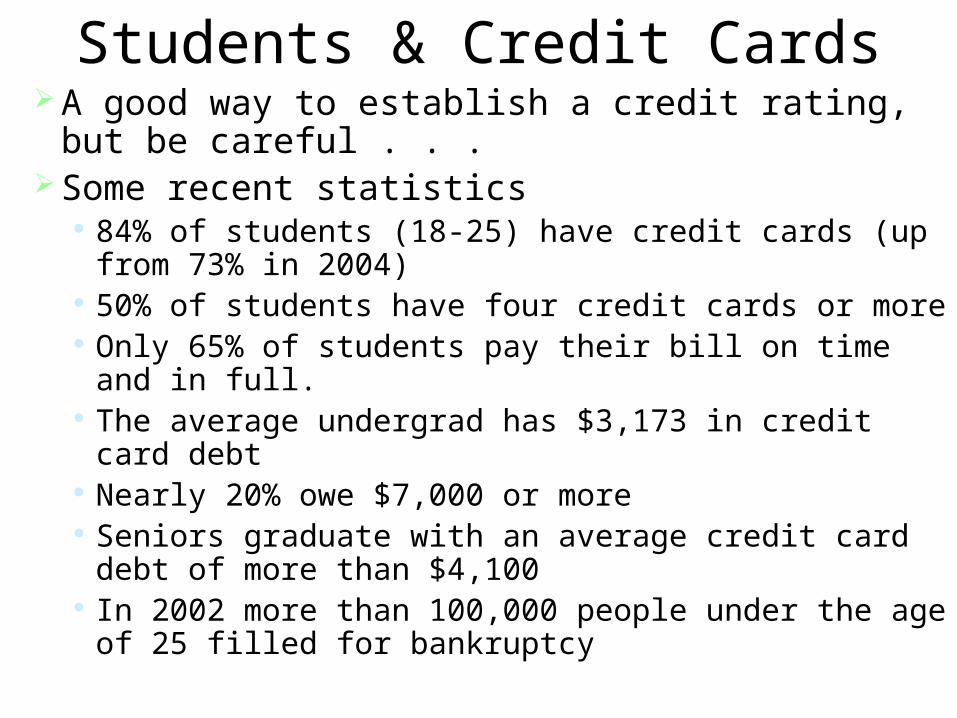

Students & Credit Cards A good way to establish a credit rating, but be

careful . . . Some recent statistics

84% of students (18-25) have credit cards (up from 73% in 2004)

50% of students have four credit cards or more Only 65% of students pay their bill on time and in full. The average undergrad has $3,173 in credit card debt Nearly 20% owe $7,000 or more Seniors graduate with an average credit card debt of

more than $4,100 In 2002 more than 100,000 people under the age of 25

filled for bankruptcySource: http://www.creditcards.com/credit-card-news/credit-card-industry-facts-personal-debt-statistics-1276.php#topofpage

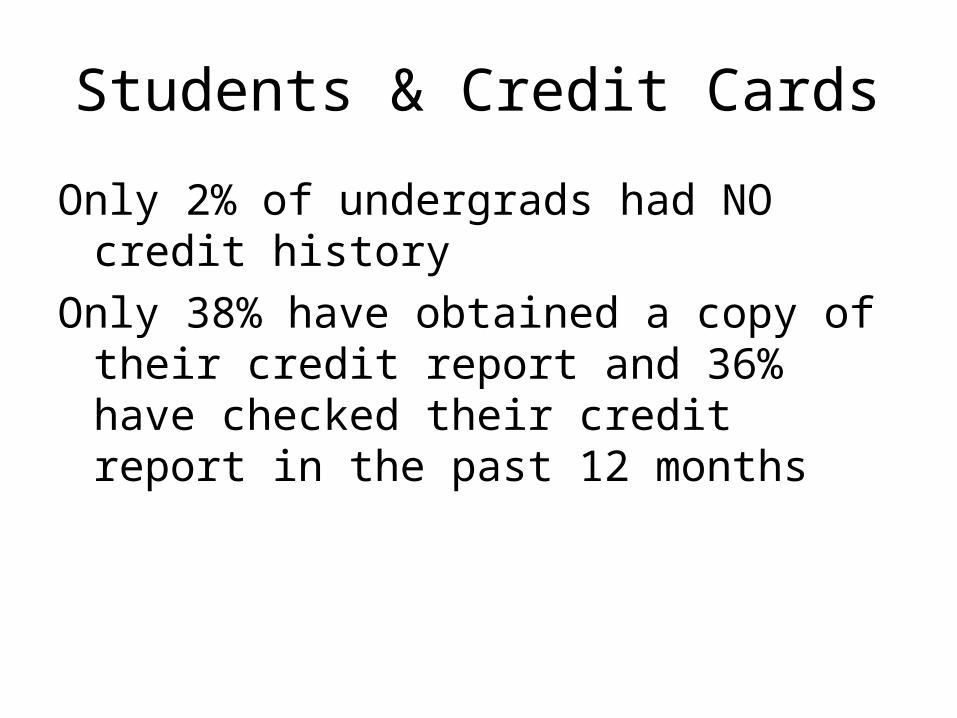

Students & Credit Cards

Only 2% of undergrads had NO credit historyOnly 38% have obtained a copy of their credit

report and 36% have checked their credit report in the past 12 months

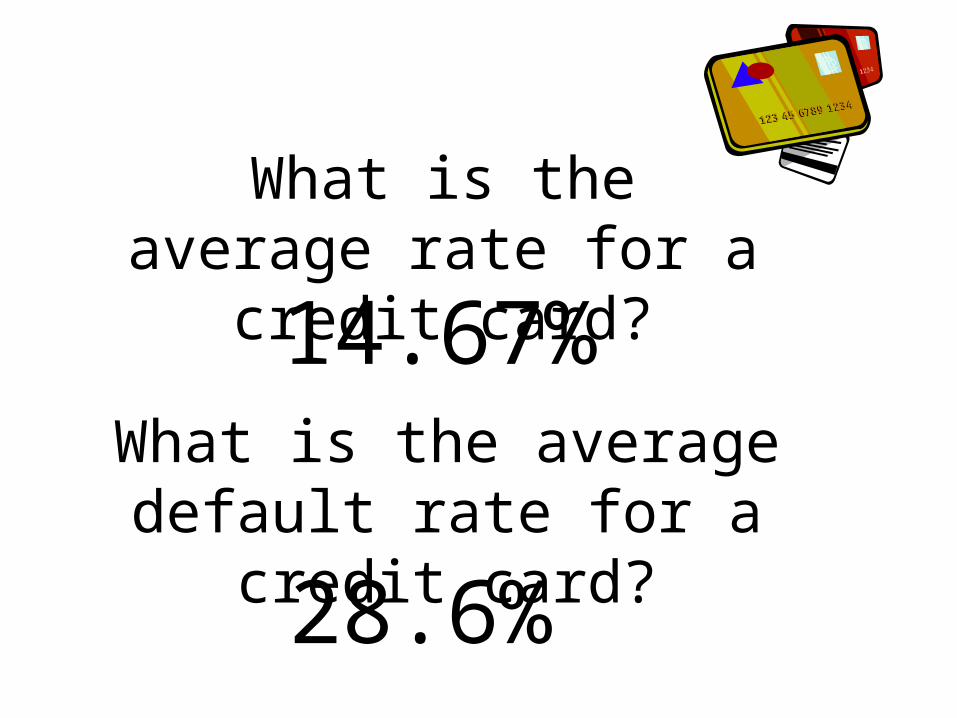

What is the average rate for a credit card?

14.67%What is the average

default rate for a credit card?28.6%

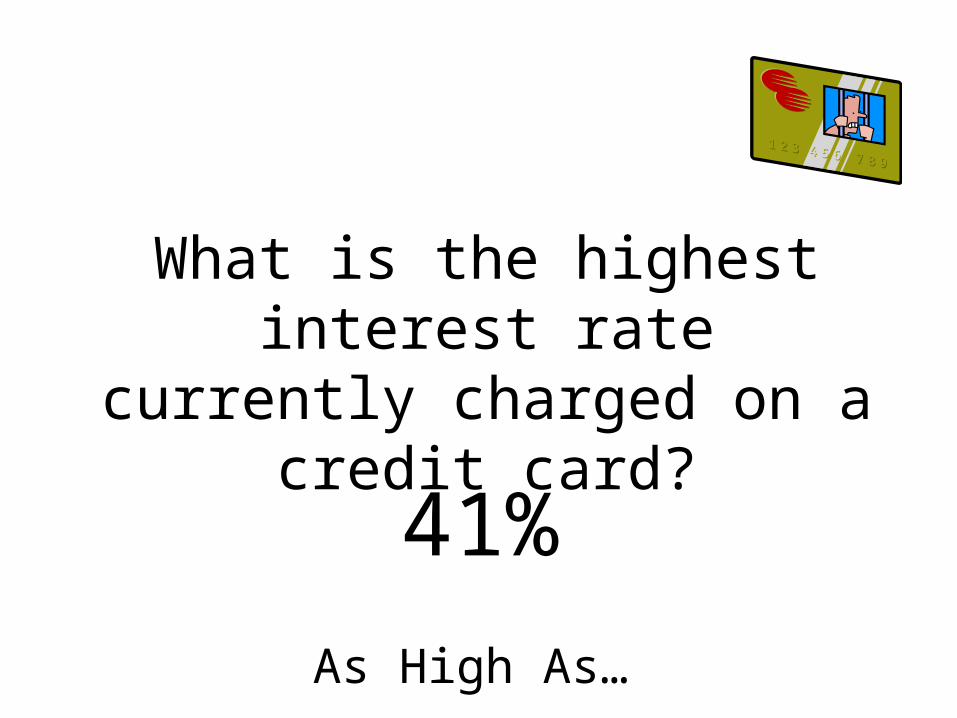

What is the highest interest rate currently

charged on a credit card?

41%

As High As…

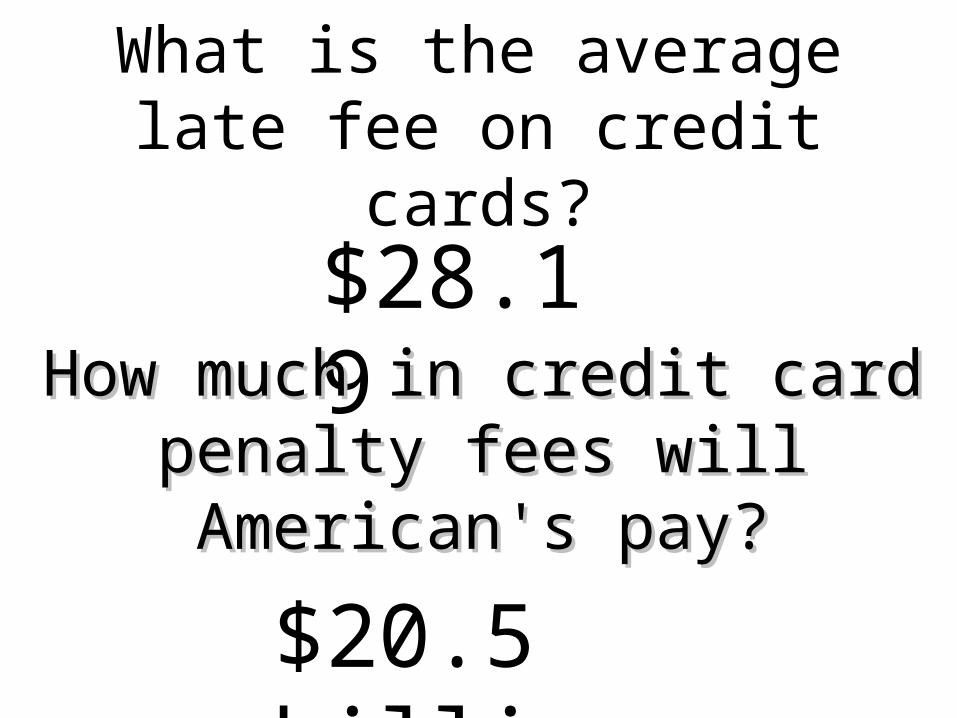

What is the average late fee on credit cards?

$28.19How much in credit card How much in credit card

penalty fees will penalty fees will American's pay?American's pay?

$20.5 billion

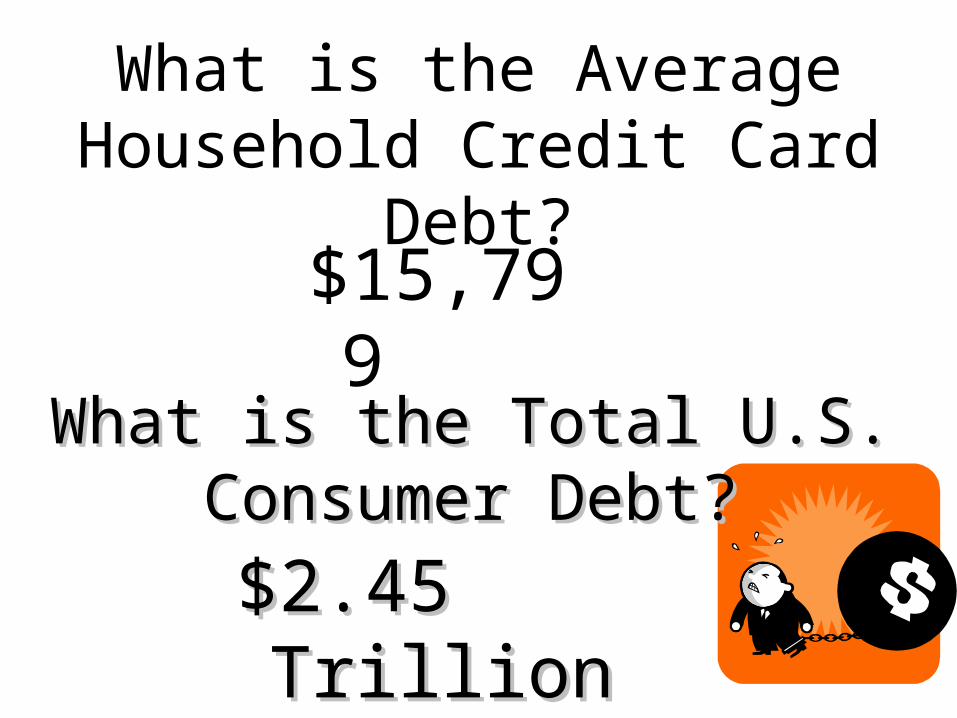

What is the Average Household Credit Card

Debt?$15,799

What is the Total U.S. What is the Total U.S. Consumer Debt?Consumer Debt?

$2.45 Trillion$2.45 Trillion

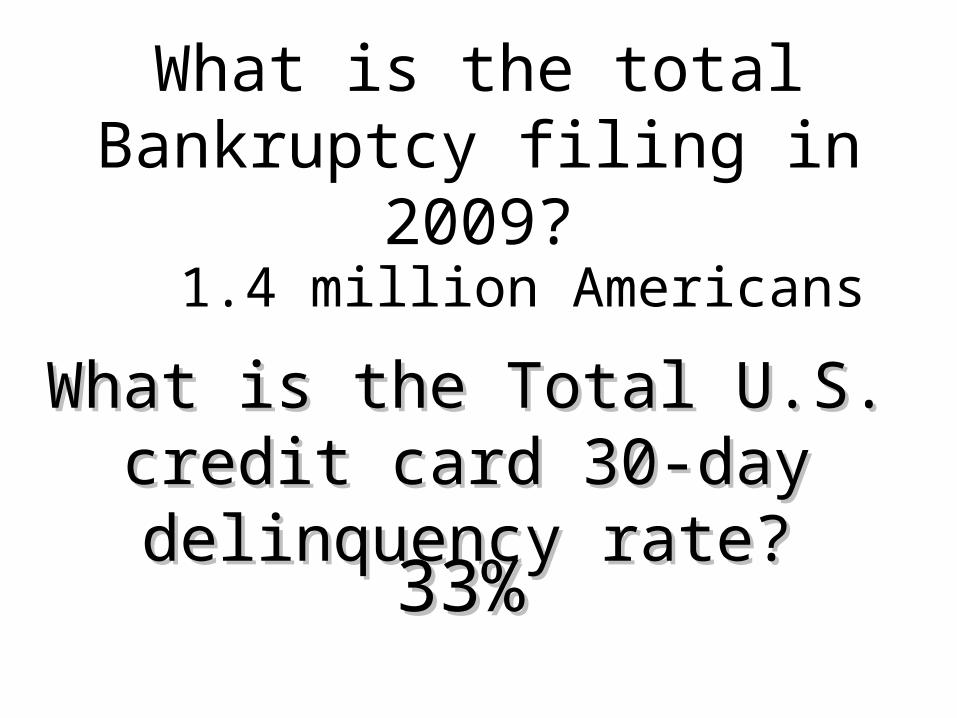

What is the total Bankruptcy filing in 2009?

1.4 million AmericansWhat is the Total U.S. credit What is the Total U.S. credit

card 30-day delinquency card 30-day delinquency rate?rate?33%33%

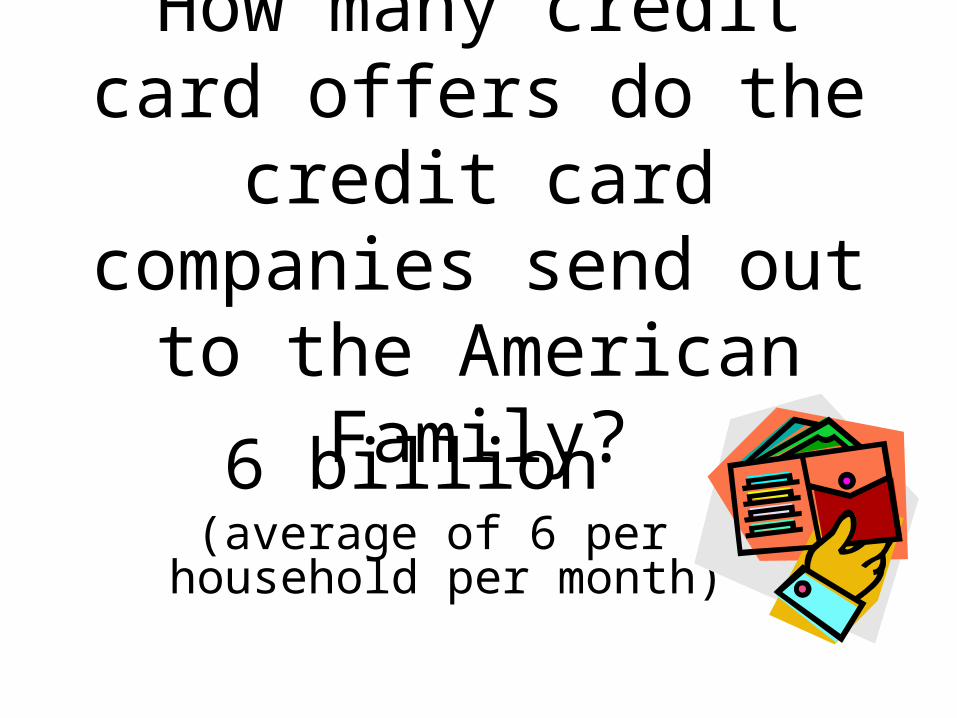

How many credit card offers do the credit

card companies send out to the American

Family?6 billion

(average of 6 per household per month)

True or False?

You can easily get credit if you have never borrowed before and have not had any credit problems.

FALSE You can help yourself to obtain larger amounts of

financing if you use small amounts of credit first and repay them as agreed.

TRUE

True or False?

Interest rates can vary greatly from lender to lender.

TRUE Applying for as many credit cards as possible

will improve your credit rating. (ex. AE credit card, Best Buy credit card)

FALSE

True or False?

If you pay your balance in FULL each month, you will never pay interest.

TRUE

What if you bought ...

• This plasma TV costing $2,000

• And what if you use your credit card to buy the television and you make monthly payments of $300?

• Assume you never miss a payment and the annual percentage rate on your card is 8%.

What will the television end up costing you?

How long will it take to pay for it?

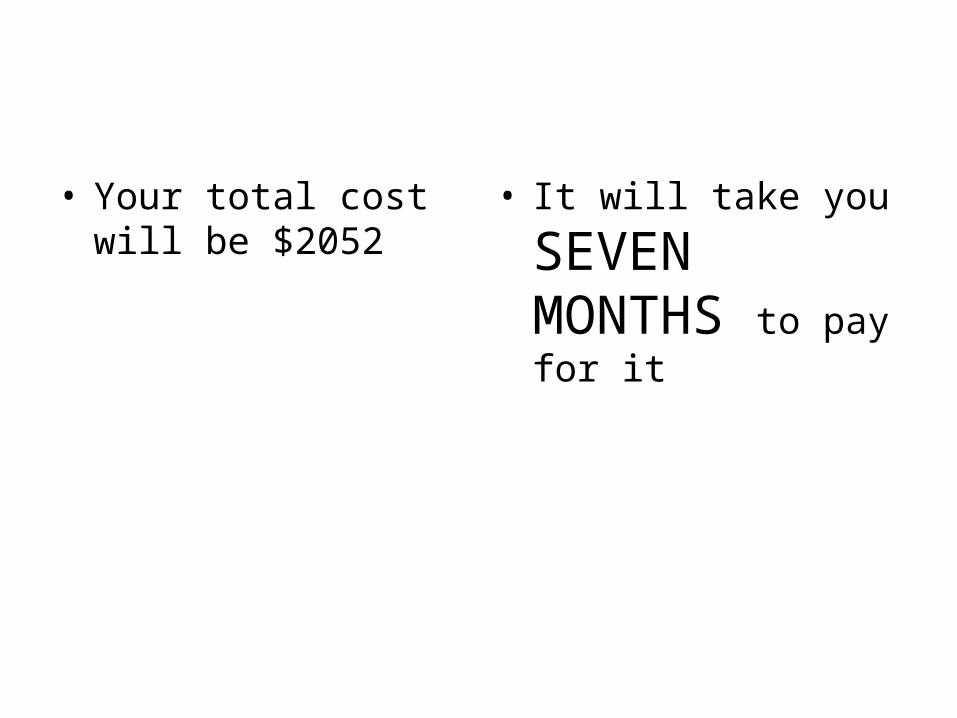

• Your total cost will be $2052

• It will take you

SEVEN MONTHS to pay for it

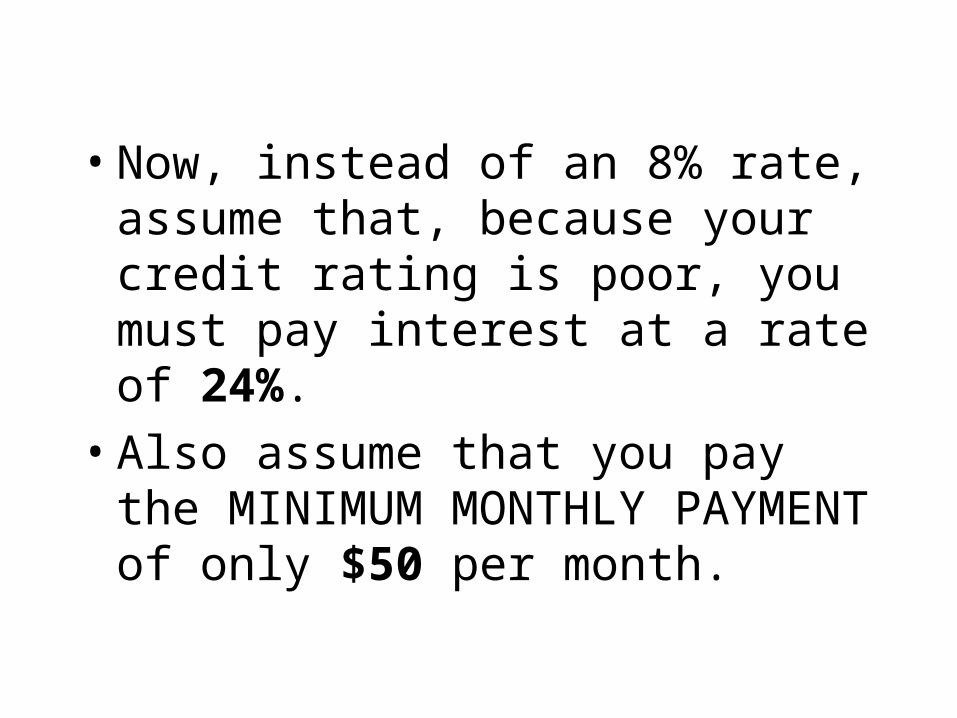

• Now, instead of an 8% rate, assume that, because your credit rating is poor, you must pay interest at a rate of 24%.

• Also assume that you pay the MINIMUM MONTHLY PAYMENT of only $50 per month.

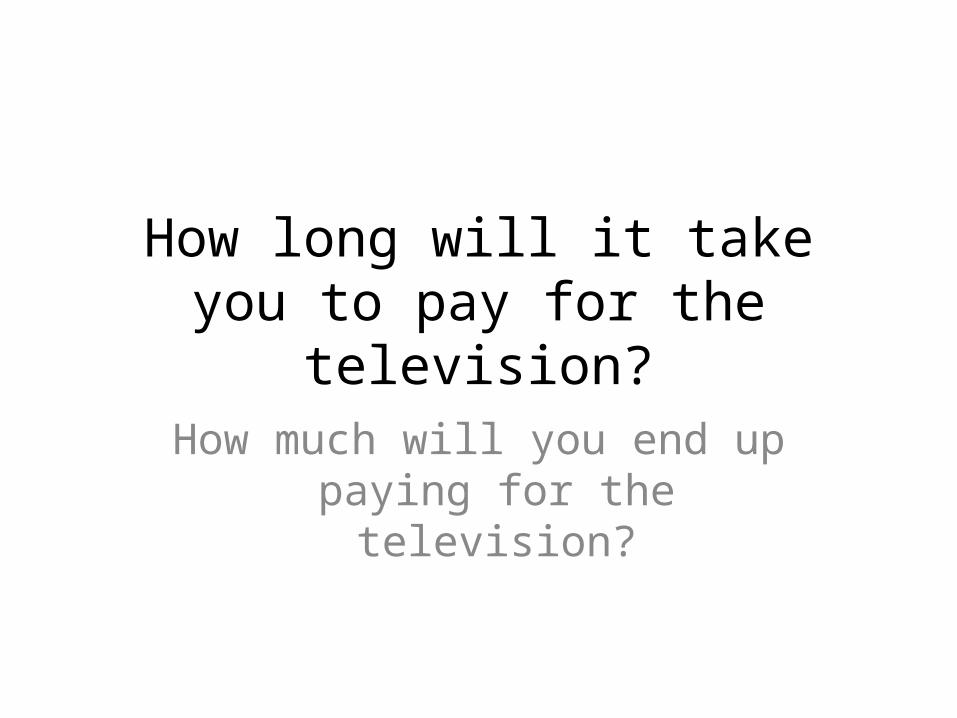

How long will it take you to pay for the television?

How much will you end up paying for the television?

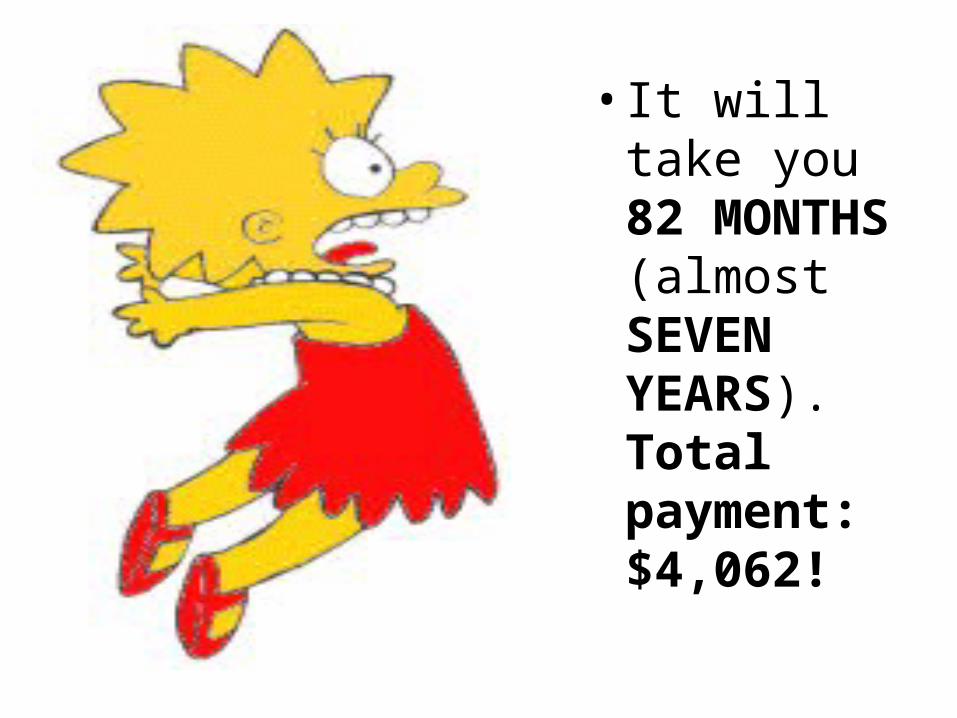

• It will take you 82 MONTHS (almost SEVEN YEARS). Total payment: $4,062!

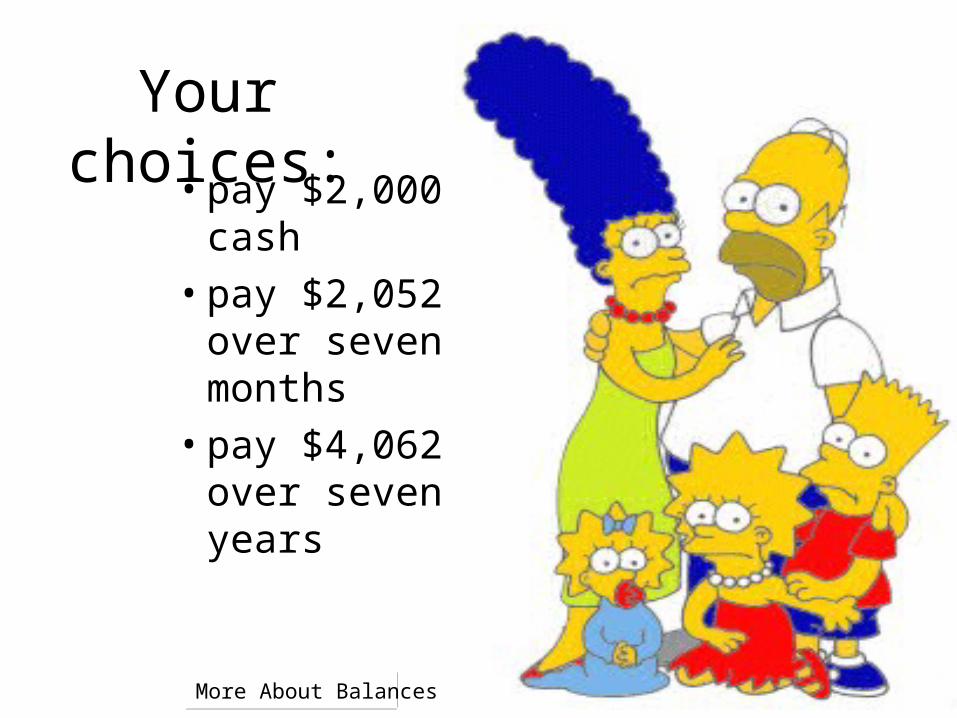

Your choices:• pay $2,000

cash

• pay $2,052 over seven months

• pay $4,062 over seven years

More About Balances

Read the credit card agreement

• What is meaning of the following provision: “Your APRs may increase if . . . you fail to make payment to another creditor when due . . . .”?

• What’s this provision called?

– “Universal default clause”

• Credit CARD Act of 2009 cut back on – but did not completely ban -- these provisions.– Card issuers cannot raise rates on existing balances

based on a universal default clause

– But they can raise rates immediately on new charges for any reason or no reason at all (as long as the credit card agreement gives them this right)

– They can even raise rates on existing balances if you are 60 days late on your payments

True or False?

• You pay no interest on a debit card purchase.

TRUE

• A debit card works just like a check. Your ATM card is probably a debit card.

Credit card companies are constantly searching for the next

“unbanked population”• What does this term mean?

– Industry term for potential credit card customer groups that have not previously had access to credit cards.

• What was the key unbanked population that credit card issuers discovered in the 1990s?

YOU!!College-bound students became a lucrative new market starting in the 1990s*

Recent Developments

Regular Charge Accounts(aka: Charge Account)

Must pay entire amount each month Often within 25-30 days after billing date.

No stated interest rate…Do not pay interest Must come in grip with credit problems every

month

Examples:

Revolving Charge Accounts Carry a balance from one month to the next. Minimum payment due or more APR is the annual percentage rate of interest the is

charged for credit. The maximum rate that may be charged is

controlled by state law.

Buy when the time is right…and pay when the time is right.

Examples:

To Summarize on Card Shopping*

• How do you figure out the right card for you? Shop by– APR

– Introductory rate (don’t be seduced)

– By affinity

– By annual fee (don’t pay one)

– By other fees

Your credit history

• Begins now—when you choose and use credit cards

• Includes your missteps for as long as 7 years

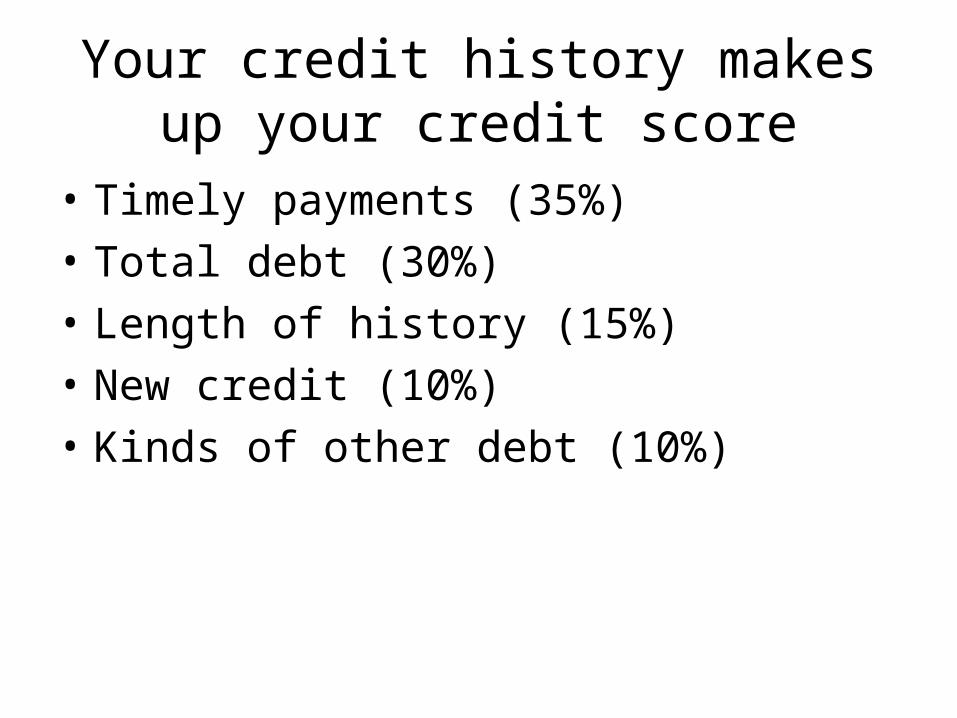

Your credit history makes up your credit score

• Timely payments (35%)• Total debt (30%)• Length of history (15%)• New credit (10%)• Kinds of other debt (10%)

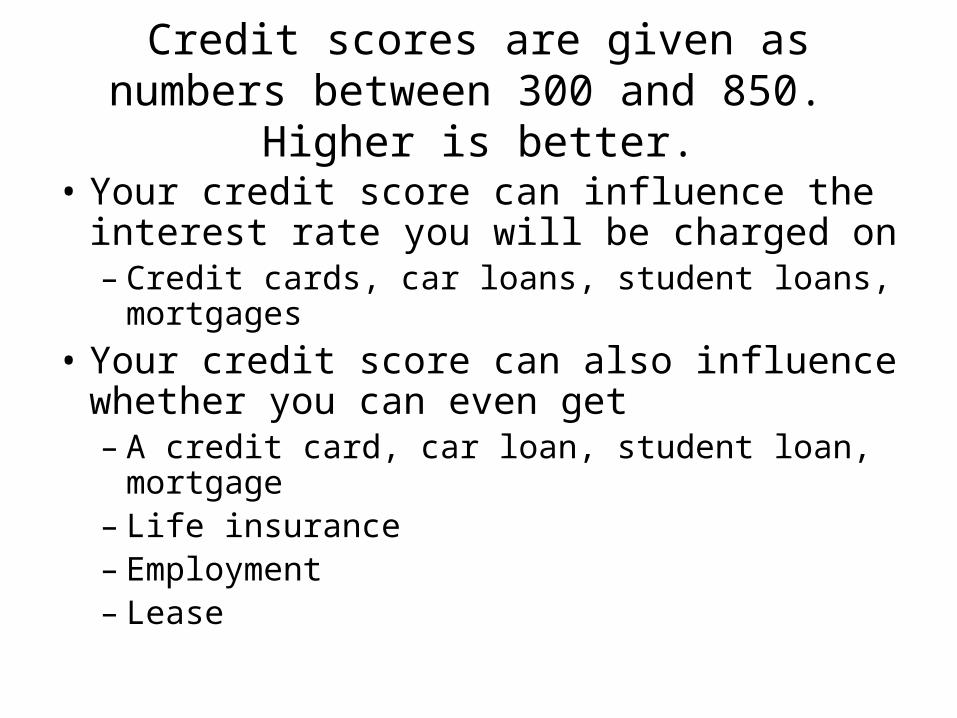

Credit scores are given as numbers between 300 and 850. Higher is better.

• Your credit score can influence the interest rate you will be charged on– Credit cards, car loans, student loans, mortgages

• Your credit score can also influence whether you can even get– A credit card, car loan, student loan, mortgage– Life insurance– Employment– Lease

The single most important component of your credit score is whether you make

payments on time

• Your parents can make a payment for you.• Your parents cannot make a late payment not late.

• A late payment stays on your credit history and impacts your credit score for as long as 7 years.

Using your credit card

• Avoiding fees

• Minimizing interest

Don’t exceed your credit limit (avoid the over-the-limit fee)

• Know what your unpaid balance is before you charge more

• Know what amount will be put through to your credit card account (what is “blocking”?)

• Know what you may need to charge before you can make your next payment (budget)

• Know what you are statistically like to need to charge… (realistic budget)

If you pay the bill in full and on time,

• There will be no unpaid balance• So, no interest• So, no fees

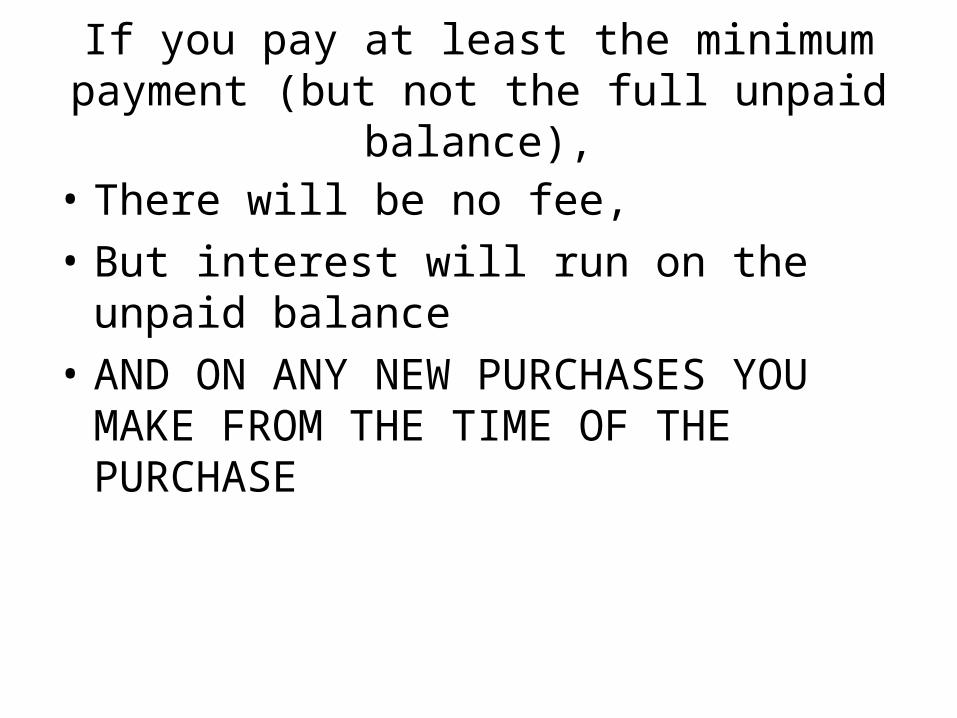

If you pay at least the minimum payment (but not the full unpaid balance),

• There will be no fee,• But interest will run on the unpaid balance• AND ON ANY NEW PURCHASES YOU MAKE

FROM THE TIME OF THE PURCHASE

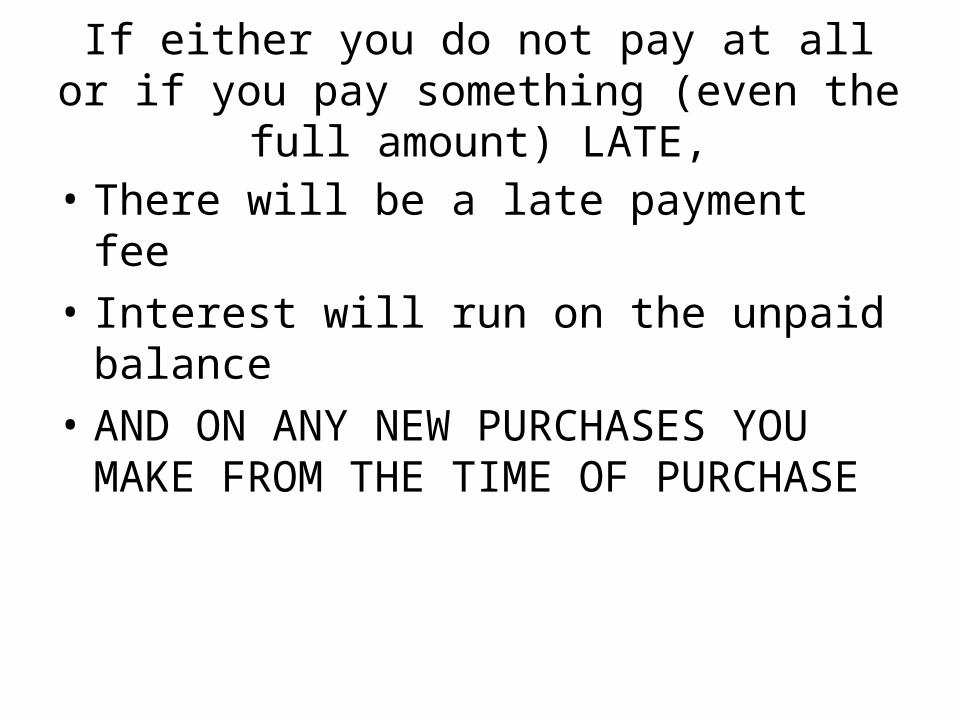

If either you do not pay at all or if you pay something (even the full amount) LATE,

• There will be a late payment fee• Interest will run on the unpaid balance• AND ON ANY NEW PURCHASES YOU MAKE

FROM THE TIME OF PURCHASE

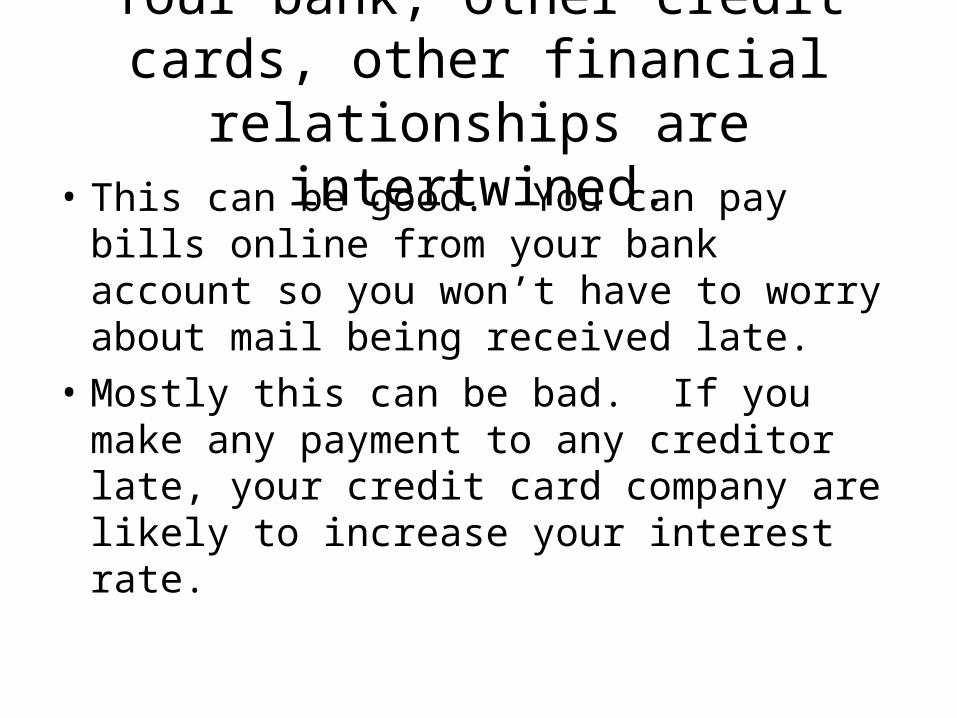

Your bank, other credit cards, other financial relationships are intertwined.• This can be good. You can pay bills online

from your bank account so you won’t have to worry about mail being received late.

• Mostly this can be bad. If you make any payment to any creditor late, your credit card company are likely to increase your interest rate.

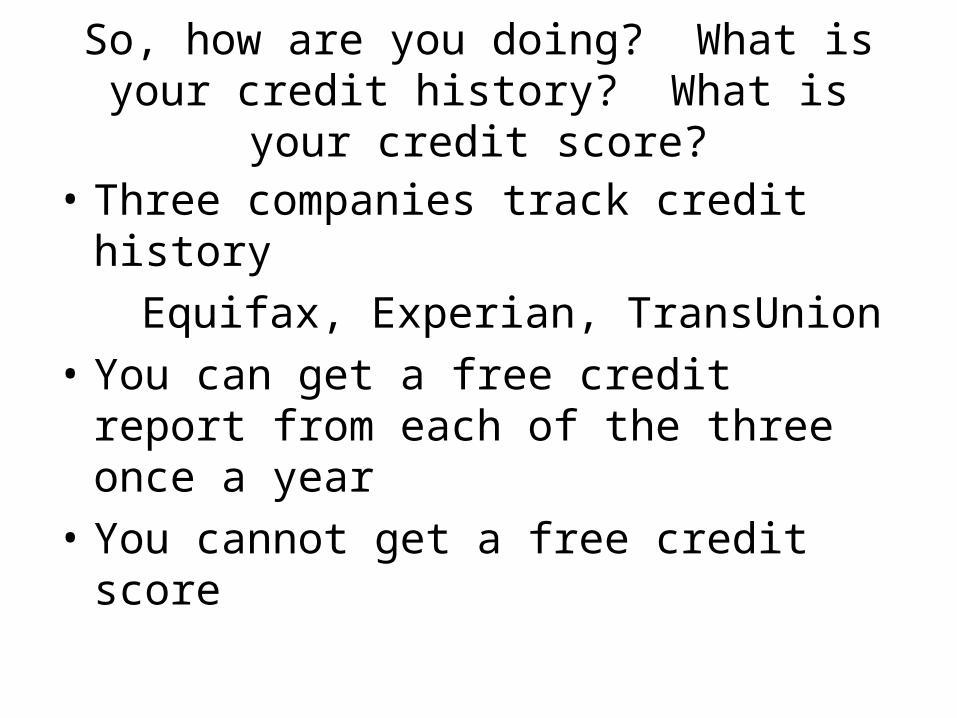

So, how are you doing? What is your credit history? What is your credit score?

• Three companies track credit historyEquifax, Experian, TransUnion

• You can get a free credit report from each of the three once a year

• You cannot get a free credit score

There is only one source for the free credit report to which you are legally entitled under federal law.

www.annualcreditreport.com

• Other source that advertise free credit reports require you to pay for something else such as your credit score, monitoring in order to get the “free” credit report.

Useful links

• www.ftc.gov (Federal Trade Commission)– Select Credit & Loans under “Quick Finder”

• www.controlyourcredit.gov (US Treasury)

• www.ace.uiuc.edu/cfe/ccs/– (University of Illinois Extension)

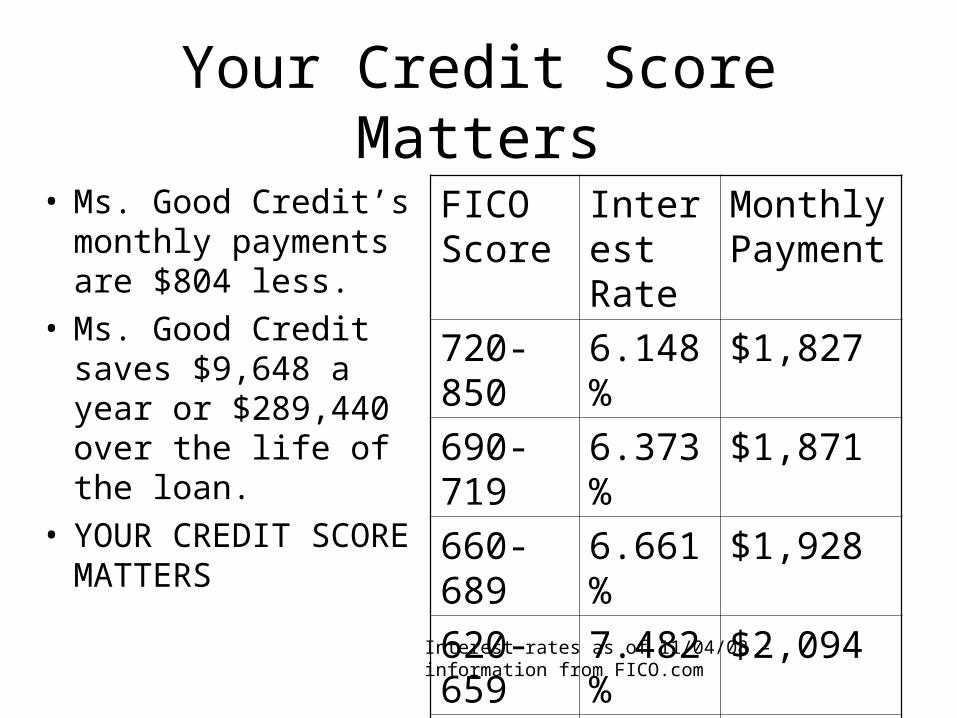

Your Credit Score Matters

• Ms. Good Credit and Ms. Bad Credit both graduated from the same college, both work downtown at the same business and both are purchasing identical one bedroom condos in the same building in the Lincoln Park area.

• Both are going to take out a 30 year mortgage for $300,000.

• Ms. Good Credit has a credit score of 770.• Ms. Bad Credit missed a few payments while in

college and has a credit score of 570.

Your Credit Score Matters

• Due to her 770 FICO score Ms. Good Credit qualifies for a mortgage at 6.148%.

• Due to her 570 FICO score Ms. Bad Credit qualifies for a mortgage at 9.993%.

• How much less will Ms. Good Credit pay a month (and over the life of the loan)?

Your Credit Score Matters

• Ms. Good Credit’s monthly payments are $804 less.

• Ms. Good Credit saves $9,648 a year or $289,440 over the life of the loan.

• YOUR CREDIT SCORE MATTERS

FICO Score

Interest Rate

Monthly Payment

720-850 6.148% $1,827

690-719 6.373% $1,871

660-689 6.661% $1,928

620-659 7.482% $2,094

590-619 9.406% $2,502

500-589 9.993% $2,631

Interest rates as of 11/04/08 – information from FICO.com

True or False?

• When you apply for a job, your prospective employer may review your credit report.

TRUE• A prospective

employer can review your credit report if you give written authorization. More employers are asking to see credit reports.

How do you build a good credit history?

• According to Fair Isaacs Corp., the 5 biggest factors helping credit are:

1. Good payment history

2. Carry low or no balance relative to the card limit

3. Lengthy credit history

4. Inquiries from creditors who grant credit

5. Diverse types of credit

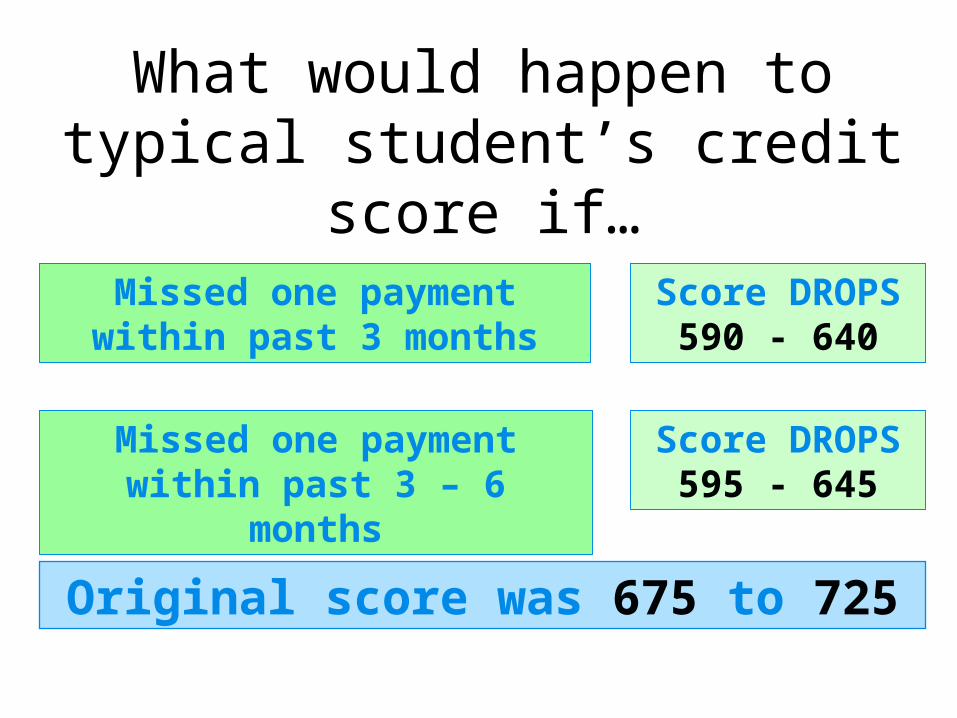

What would happen to typical student’s credit score if…

Score DROPS 590 - 640

Missed one payment within past 3 months

Missed one payment within past 3 – 6 months

Score DROPS 595 - 645

Original score was 675 to 725

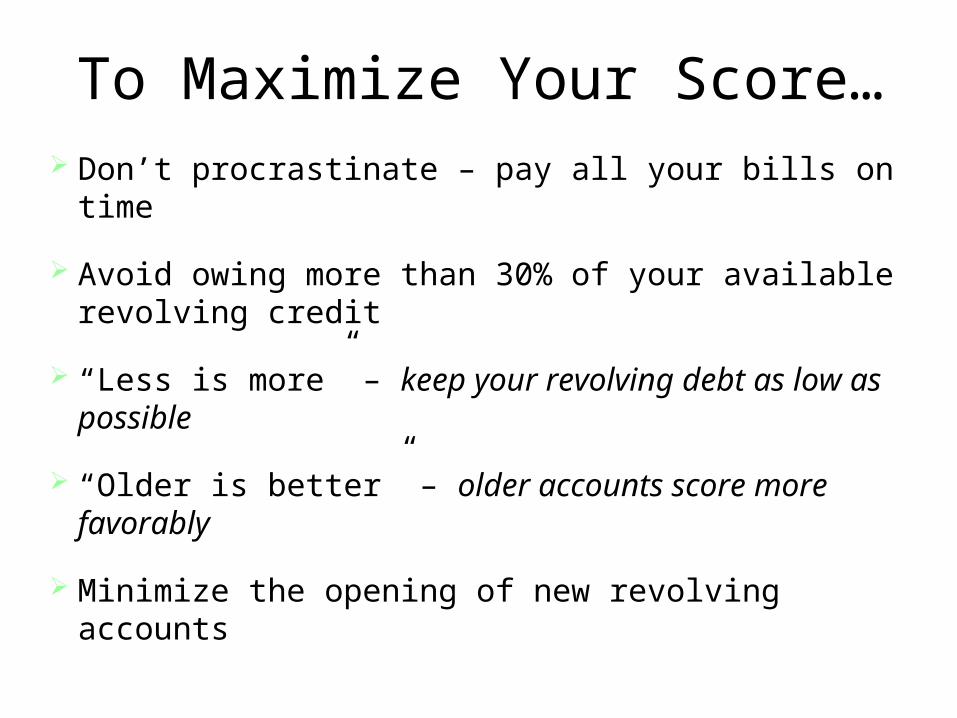

To Maximize Your Score… Don’t procrastinate – pay all your bills on time

Avoid owing more than 30% of your available revolving credit

“Less is more” – keep your revolving debt as low as possible

“Older is better” – older accounts score more favorably

Minimize the opening of new revolving accounts

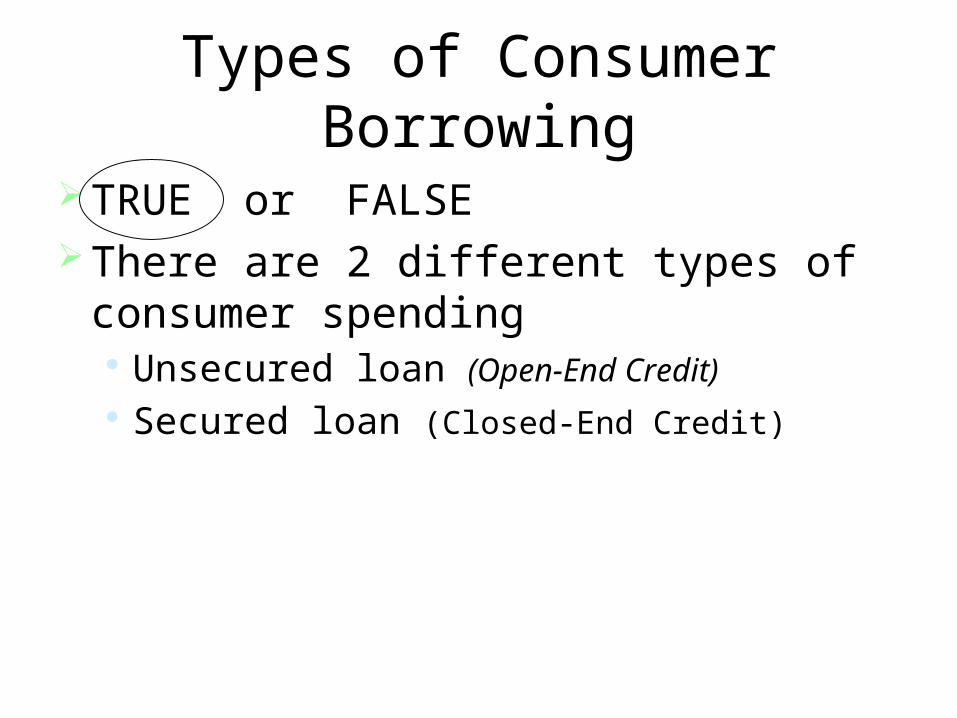

Types of Consumer Borrowing

TRUE or FALSE There are 2 different types of consumer

spending Unsecured loan (Open-End Credit) Secured loan (Closed-End Credit)

Section 3

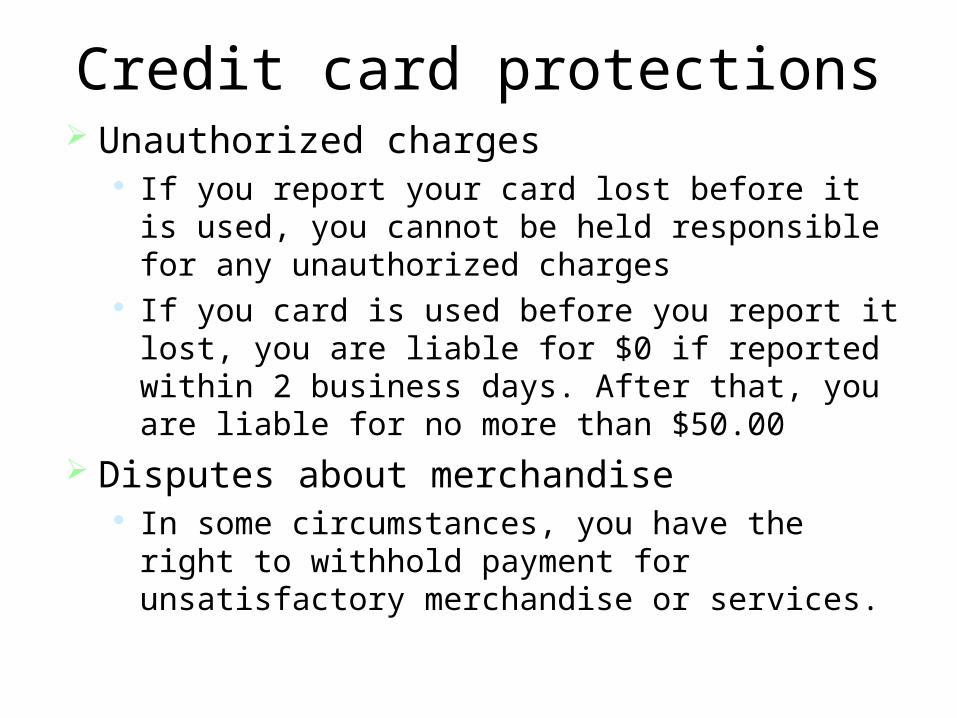

Credit card protections Unauthorized charges

If you report your card lost before it is used, you cannot be held responsible for any unauthorized charges

If you card is used before you report it lost, you are liable for $0 if reported within 2 business days. After that, you are liable for no more than $50.00

Disputes about merchandise In some circumstances, you have the right to withhold

payment for unsatisfactory merchandise or services.

Consumer Credit Responsibilities

Credit is a privilege, not a right! Accept responsibility Know your debt capacity Self-Control with Credit

• Pay more than the minimum • Avoid too many credit cards• Pay with cash• Keep accurate records

Even more Scams

ATM SCAM

Credit Card Don’ts

Don’t get a card with a high limit Don’t get more than 1 card Don’t use them for cash advances Don’t charge more than you can pay off in a

month Don’t let banks increase your credit limit

Source: USA Funds Life Skills -Module 1

Credit Card Do’s

Limit the number of cards you have Use a debit card vs. a credit card Use a card that has no annual fee and lower

interest rates Know all of your card’s hidden fees Always pay more than the minimum amount

each month Pay on time, all the time.

TWO SMART MONEY TIPS FOR COLLEGE STUDENTS

77

TIP ONE: STUDENT LOANS

• College costs• Sources• Grants and scholarships• Student loan features• Loan costs v. college quality

78

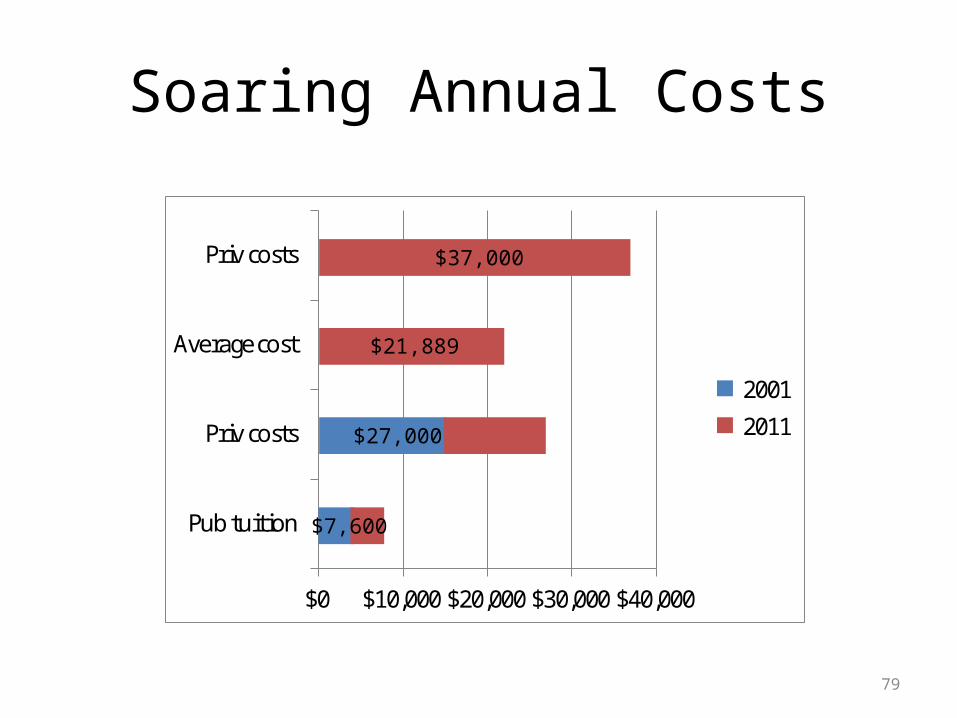

Soaring Annual Costs

79

$0 $10,000 $20,000 $30,000 $40,000

Pub tuition

Priv costs

Average cost

Priv costs

2001

2011

$37,000

$21,889

$27,000

$7,600

Student loan debt

• 2010 graduates– $24,000 - $27,000/student borrower

80

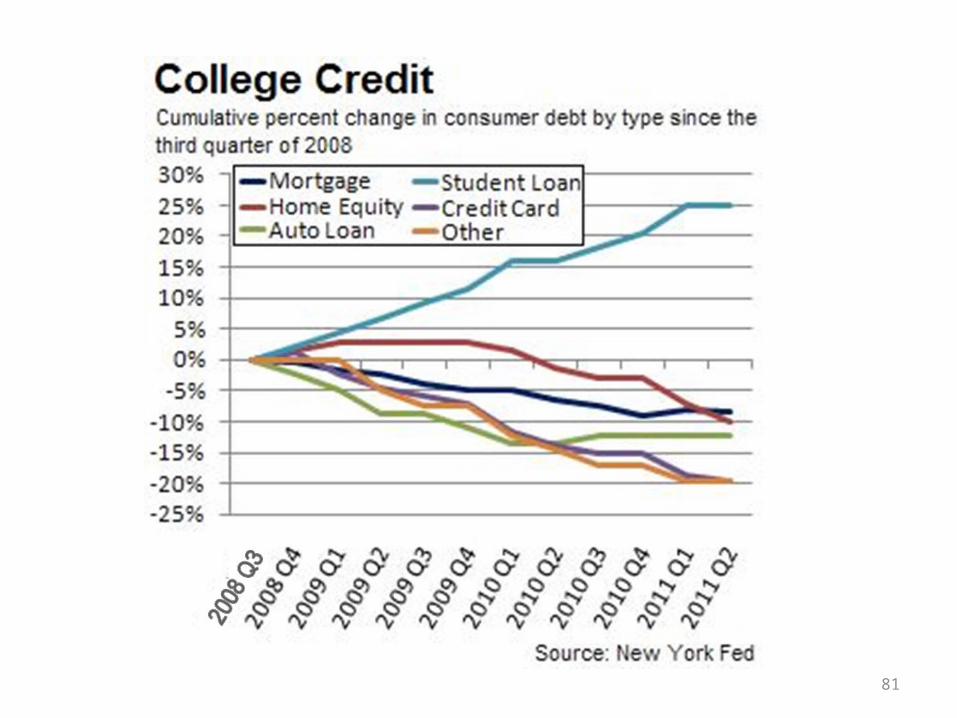

81

TIP ONE: STUDENT LOANS

• College costs• Sources• Grants and scholarships• Student loan features• Loan costs v. college quality

82

• Where do students get the money to pay for college?

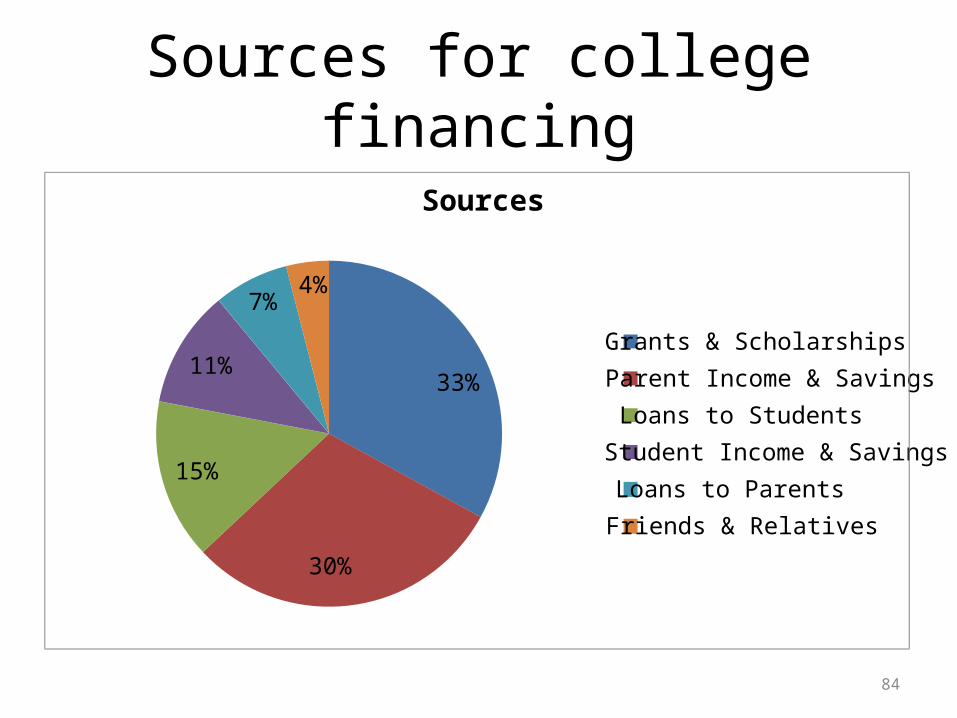

Sources for college financing

84

33%

30%

15%

11%

7%4%

Sources

Grants & Scholarships

Parent Income & Savings

Loans to Students

Student Income & Savings

Loans to Parents

Friends & Relatives

TIP ONE: STUDENT LOANS

• College costs• Sources• Grants and scholarships• Student loan features• Loan costs v. college quality

85

Grants

86

Pell Grants

• $5500/student/year

• need-based

87

Scholarships

• Apply early• Need based and merit-based scholarships• Scholarship Sources

– Ask your school’s college counselor– fastweb.com– collegeanswer.com– collegeboard.com

88

Surprising scholarships

89

Duct tape

90

Twin Scholarship

91

TIP ONE: STUDENT LOANS

• College costs• Sources• Grants and scholarships• Student loan features• Loan costs v. college quality

92

2 types of student loans

• Federal

• Private

93

• F ree

• A pplication for

• F ederal

• S tudent

• A id

• Remember: 1-1-13

4 Types of Federal Loans

• PLUS

95

Stafford subsidized

• Need-based• Cap: $23,000 for college career

96

Stafford unsubsidized

• Cap: $57K• Interest rate set by statute

97

Perkins Loans

• Need-based• College picks recipients• Interest rate set by statute

98

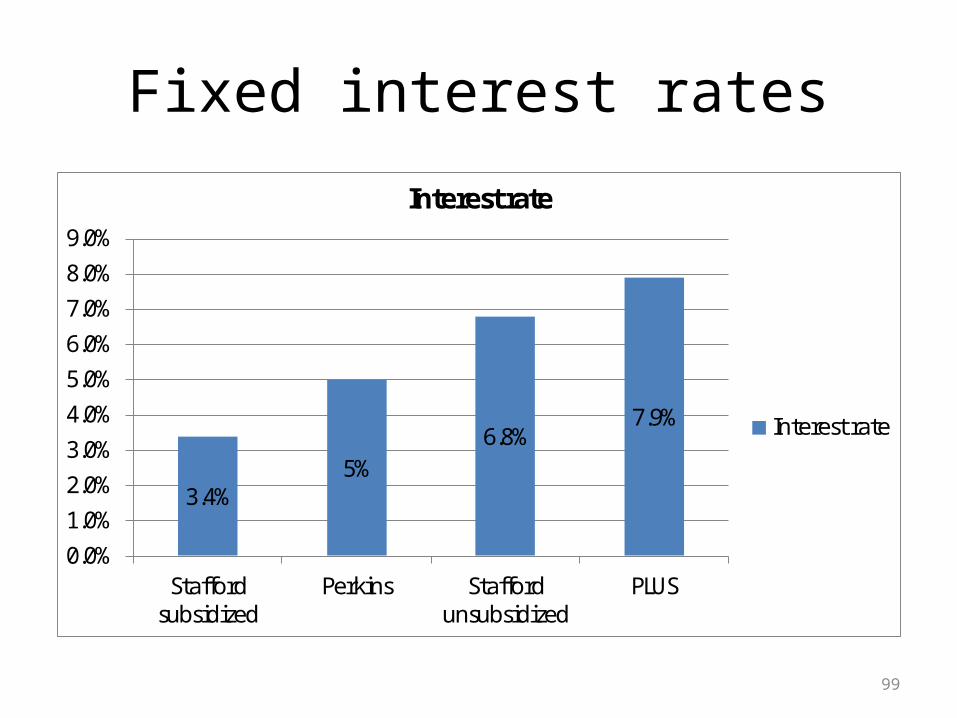

Fixed interest rates

3.4%5%

6.8%7.9%

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

Stafford subsidized

Perkins Stafford unsubsidized

PLUS

Interest rate

Interest rate

99

Friendly payment options/rights

• Need-based payment deferral or forbearance

100

Interest deferral while in school

101

Private Loans

• Myrichuncle.com

102

Other private loan features

• Immediate payment• Negotiated deal• No right to postpone or extend payments• Fees

103

Other private loan features

104

Great web site

•www.FinAid.org

105

TIP ONE: STUDENT LOANS

• College costs• Sources• Grants and scholarships• Student loan features• Loan costs v. college quality

106

3 approaches

• Monthly loan payments in your chosen career

107

Another approach

• Bang for buck

108

Summarize

• Figure out how much in student loans you need

• Work college aid officers• Fed loans first, private loans last• Is your school “cost efficient”?• Loan debt versus first year salary

109

Earnings Statements & Tax Forms

• Must file income return annually• Most students can use Form 1040-EZ• Gather your documents

– W-2s– Pay stubs– Interest earned Form 1099

Earnings Statements & Tax Forms(con’t)

• Filing must be done by April 15 each year– Once through it, it is not that difficult– Turbo tax software makes the process easy to do

electronic filing

• Keep all tax related documents for 7 years