Embed Size (px)

Citation preview

Fiscal challenges in Slovenia

IMAD, Ljubljana, 19 June 2012

Mitja Košmrl, DG ECFIN

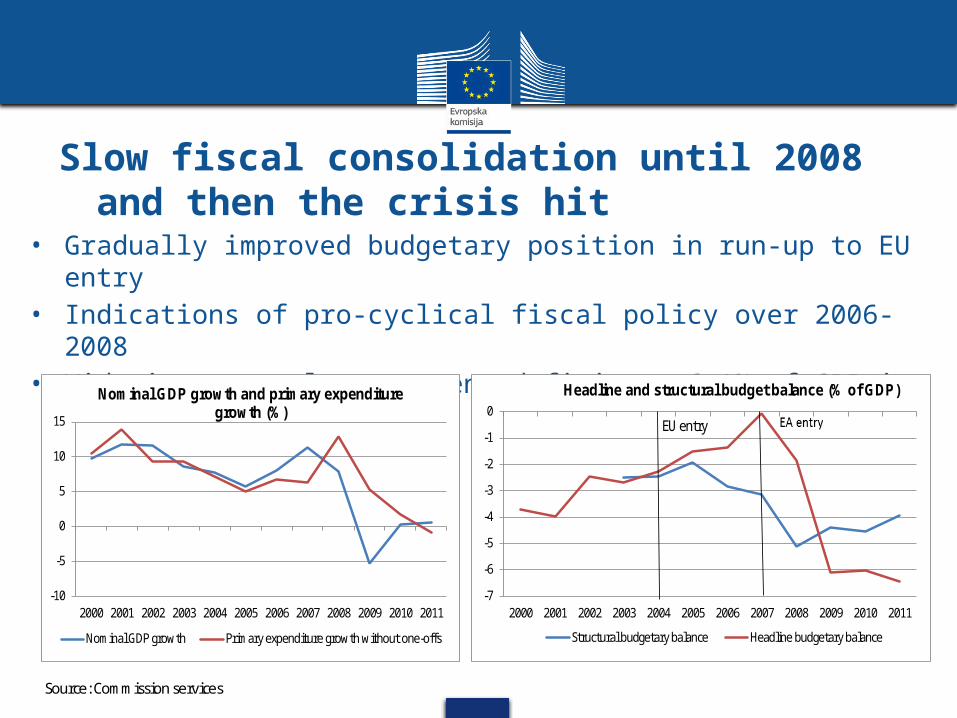

Outline

1. Recent public finance developments including the May 2012 austerity package

2. Structural challenges for public finances3. Links between financial sector and public

finances4. Costs and benefits of fiscal consolidation

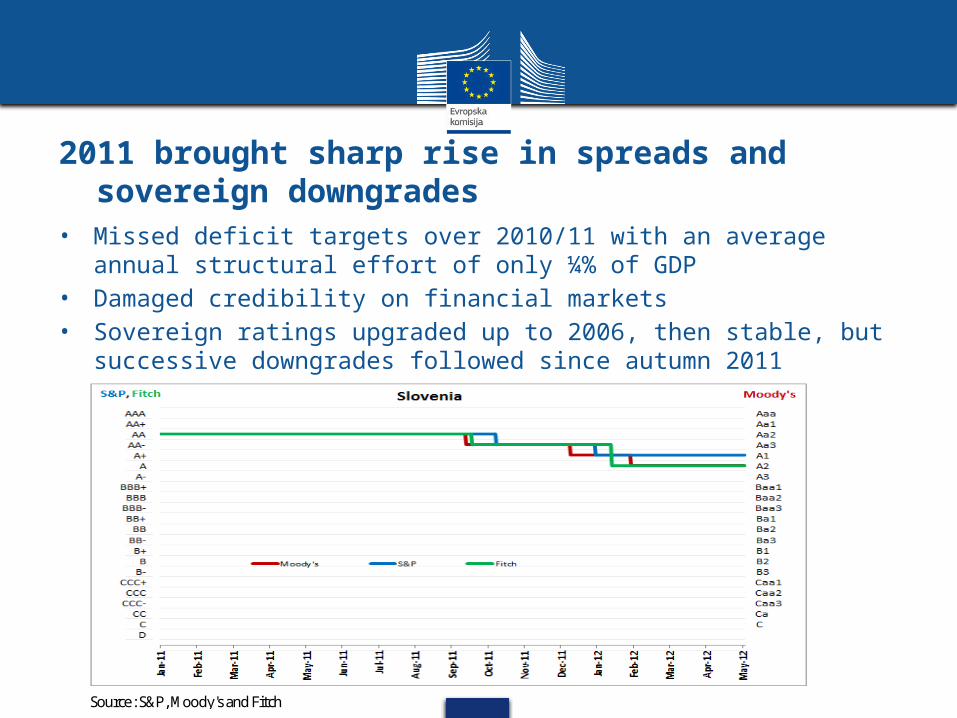

Slow fiscal consolidation until 2008 and then the crisis hit

• Gradually improved budgetary position in run-up to EU entry• Indications of pro-cyclical fiscal policy over 2006-2008• Widening general government deficit to 6.1% of GDP in 2009

Source: Commission services

-7

-6

-5

-4

-3

-2

-1

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Headline and structural budget balance (% of GDP)

Structural budgetary balance Headline budgetary balance

EU entry

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nominal GDP growth and primary expenditure growth (%)

Nominal GDP growth Primary expenditure growth without one-offs

2011 brought sharp rise in spreads and sovereign downgrades

• Missed deficit targets over 2010/11 with an average annual structural effort of only ¼% of GDP

• Damaged credibility on financial markets• Sovereign ratings upgraded up to 2006, then stable, but successive

downgrades followed since autumn 2011

Source: S&P, Moody's and Fitch

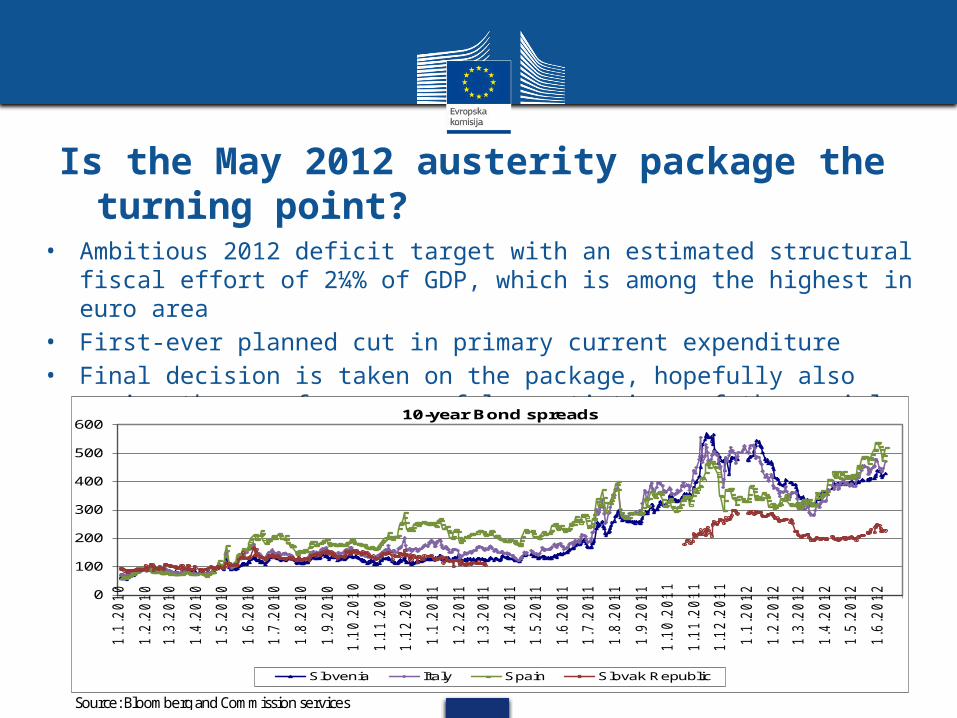

Is the May 2012 austerity package the turning point?

• Ambitious 2012 deficit target with an estimated structural fiscal effort of 2¼% of GDP, which is among the highest in euro area

• First-ever planned cut in primary current expenditure• Final decision is taken on the package, hopefully also paving the way

for successful negotiations of the social agreement 2012-2016

Source: Bloomberg and Commission services

0

100

200

300

400

500

600

1.1

.20

10

1.2

.20

10

1.3

.20

10

1.4

.20

10

1.5

.20

10

1.6

.20

10

1.7

.20

10

1.8

.20

10

1.9

.20

10

1.1

0.2

01

0

1.1

1.2

01

0

1.1

2.2

01

0

1.1

.20

11

1.2

.20

11

1.3

.20

11

1.4

.20

11

1.5

.20

11

1.6

.20

11

1.7

.20

11

1.8

.20

11

1.9

.20

11

1.1

0.2

01

1

1.1

1.2

01

1

1.1

2.2

01

1

1.1

.20

12

1.2

.20

12

1.3

.20

12

1.4

.20

12

1.5

.20

12

1.6

.20

12

10-year Bond spreads

Slovenia Italy Spain Slovak Republic

Many challenges remain

• Risks to government revenue and expenditure projections in 2012 and beyond

• Additional measures are likely to be needed for 2013 to ensure the correction of the excessive deficit

• Many consolidation measures have expiry dates so they will need to be replaced with permanent ones

• Public finance challenges of a more structural nature:1. Long-term sustainability2. Medium-term budgetary framework3. Risks from the financial sector

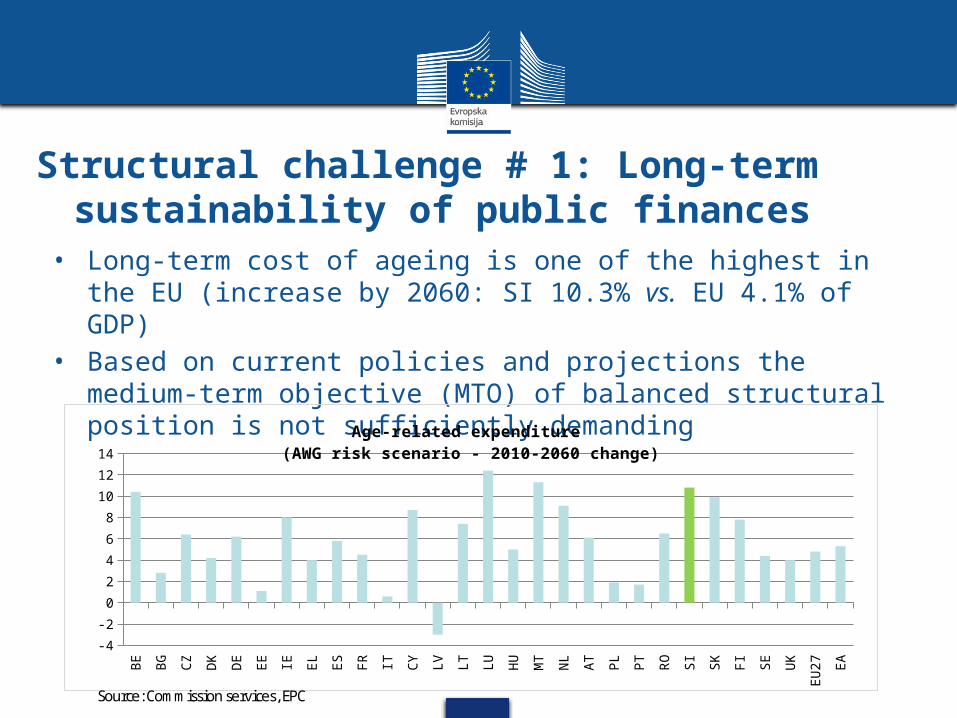

Structural challenge # 1: Long-term sustainability of public finances

• Long-term cost of ageing is one of the highest in the EU (increase by 2060: SI 10.3% vs. EU 4.1% of GDP)

• Based on current policies and projections the medium-term objective (MTO) of balanced structural position is not sufficiently demanding

BE

BG

CZ

DK

DE

EE IE EL

ES

FR IT CY

LV LT LU HU

MT

NL

AT PL

PT

RO SI

SK FI SE

UK

EU

27

EA

-4

-2

0

2

4

6

8

10

12

14

Age-related expenditure (AWG risk scenario - 2010-2060 change)

Source: Commission services, EPC

Recommendations to Slovenia under the European semester

• Commission asks that pension reform should:• equalise the statutory retirement age for men and

women• raise the statutory retirement age in line with

increasing life expectancy• reduce early retirement possibilities, and• review the indexation system for pensions

Structural challenge # 2: Medium-term budgetary framework (MTBF)

• MTBF and expenditure rule are insufficiently binding and insufficiently focused on achieving sound medium-term budgetary position and securing long-term sustainability of public finances

• The Fiscal Council does not yet weigh on fiscal strategy development

• Uncertainty about the plans to adopt a constitutional debt rule

• Recommendation to Slovenia under the European semester to strengthen the MTBF

Structural challenge # 3: Risks from the financial sector

• 2011: recapitalisations of NLB (impact on deficit: 0.7% of GDP) and NKBM

• Second recapitalisation of NLB due by end-June• Uncertainty about budgetary impact of this and possible

further recapitalisations for state-owned banks (the state as majority owner carries the burden of responsibility)

• Possible need for further financial sector support also mentioned by rating agencies as reason for recent downgrades of sovereign ratings

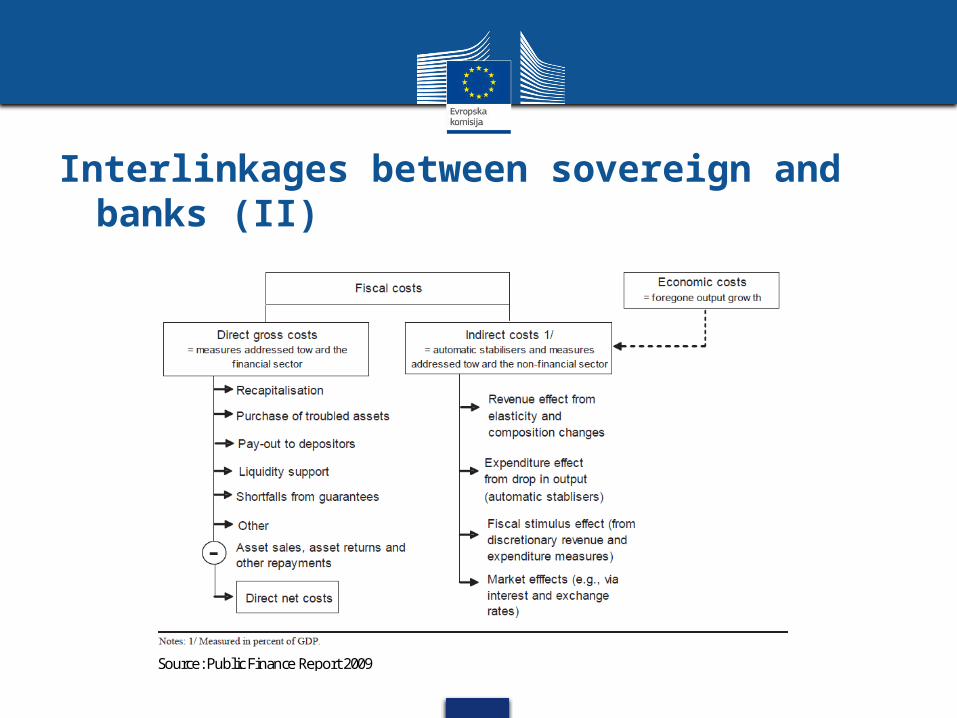

Interlinkages between sovereign and banks (I)

• In general, rising sovereign-risk premia, being to an extent a result of problems in the banking system, may spill back to the banking system through various channels:• falling mark-to-market values of government bonds

generate losses on the asset side• lower values of government bonds impact negatively on

banks' liquidity positions• banks' funding costs increase due to a worsened access

to funding on the liability side, and • greater sovereign risks erode the potential for official

support

Interlinkages between sovereign and banks (II)

Source: Public Finance Report 2009

How to reduce fiscal costs?

• Costs for the government depend ultimately on the seriousness of the situation in banks and on how accurately and quickly bank losses are assessed and acted upon

• Direct fiscal costs are lower and recovery rates are higher when the bank resolution strategy is (Public Finance Report 2009):• implemented swiftly and transparently• underpinned by broad political support• supported by strong public institutions and legal

frameworks• consistent in terms of fair and uniform treatment of

market participants, and• accompanied by a clear exit strategy

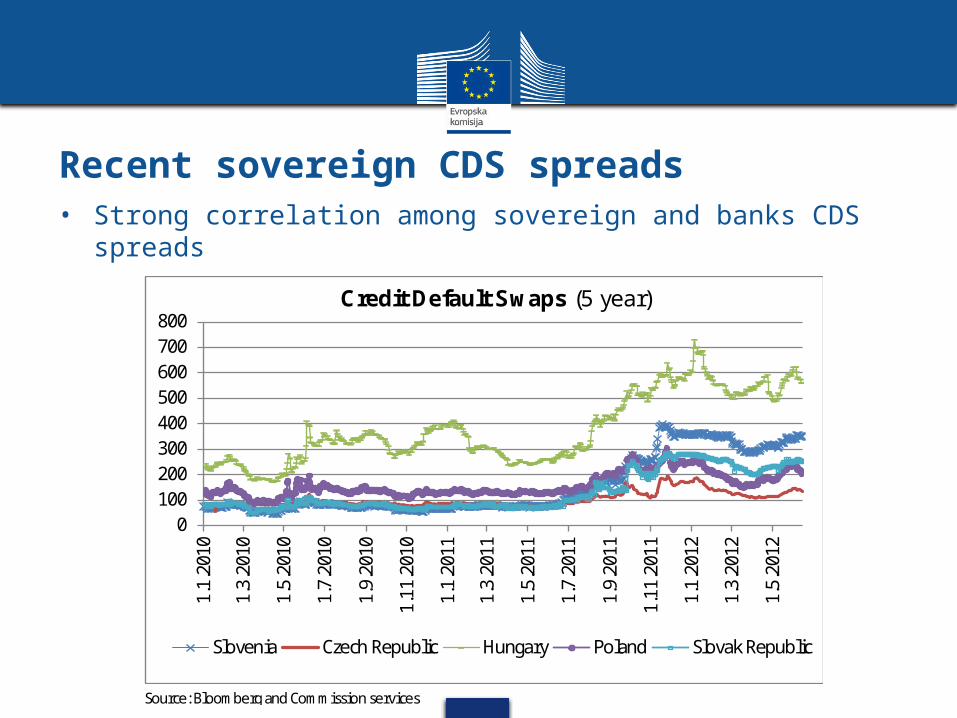

Recent sovereign CDS spreads• Strong correlation among sovereign and banks CDS spreads

0100200300400500600700800

1.1.

2010

1.3.

2010

1.5.

2010

1.7.

2010

1.9.

2010

1.11

.201

0

1.1.

2011

1.3.

2011

1.5.

2011

1.7.

2011

1.9.

2011

1.11

.201

1

1.1.

2012

1.3.

2012

1.5.

2012

Credit Default Swaps (5 year)

Slovenia Czech Republic Hungary Poland Slovak Republic

Source: Bloomberg and Commission services

Recommendations to Slovenia under the European semester

• Take the required steps to build sufficient capital buffers in the banking sector and strongly promote the cleaning of balance sheets so that appropriate lending to productive activities can resume. Obtain fully-fledged third party verification of systemically important banks' stress loan-loss estimates

• Improve the business environment through:• establishing a framework for state-owned enterprises

guaranteeing arms-length management and high standards of corporate governance, and

• improving bankruptcy procedures, in particular in terms of timeliness and efficiency

Short- and long-term impact of fiscal consolidation on the economy

• Consolidation is likely to have negative employment and GDP effects in short run. Multiplier is around 0.3-0.4 for standardised 1% of GDP consolidation package

• In the medium to long run funding costs for the private sector will be lower if sovereign risk is addressed, it leading to positive effects on investment, GDP and employment

• These effects are strengthened by lower government interest payments, creating space for future tax reductions and more growth friendly expenditure

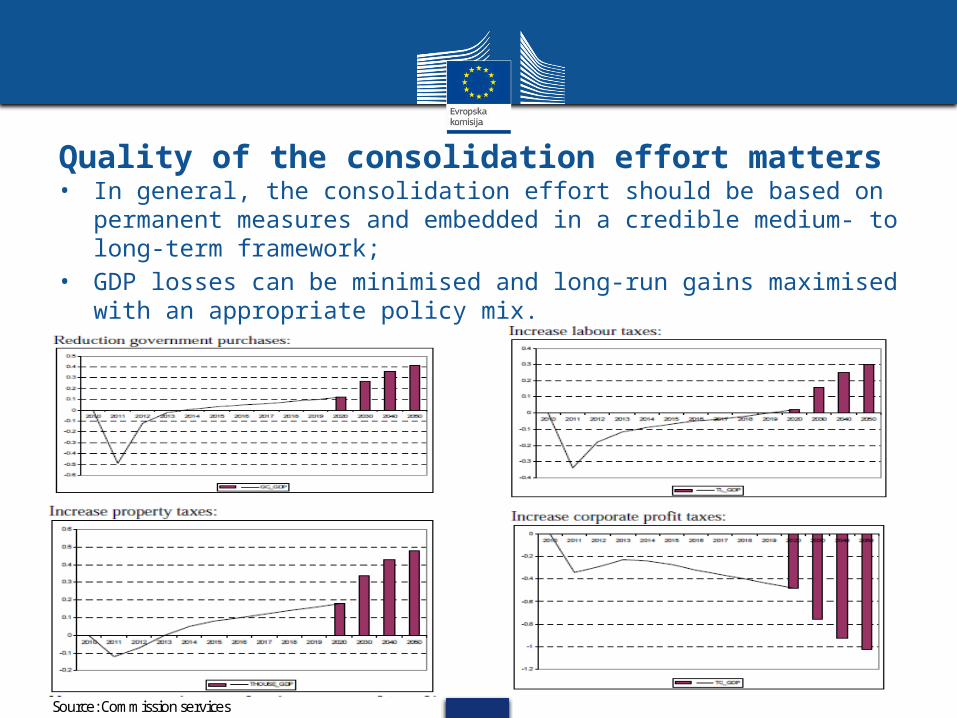

Quality of the consolidation effort matters• In general, the consolidation effort should be based on permanent

measures and embedded in a credible medium- to long-term framework;

• GDP losses can be minimised and long-run gains maximised with an appropriate policy mix.

Source: Commission services

Hvala.