Embed Size (px)

Citation preview

FlexCare Open Enrollment Guide

Open Enrollment 2017: October 31–November 11

Take a closer look!

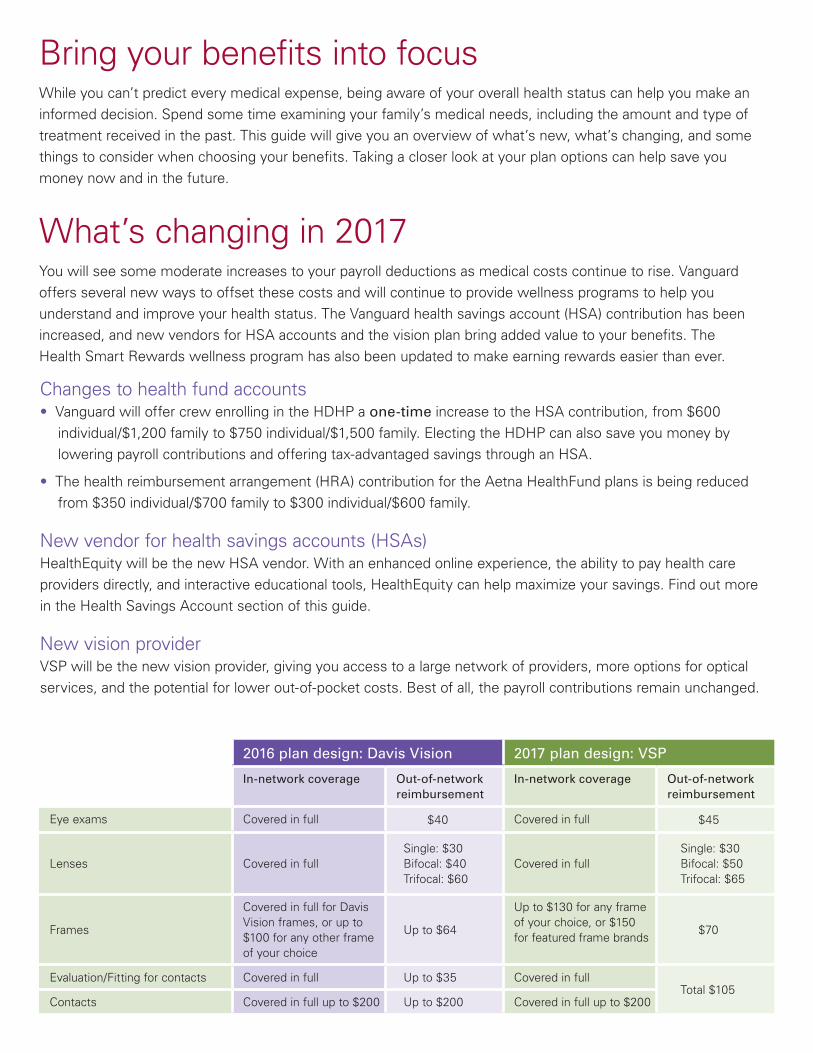

Bring your benefits into focusWhile you can’t predict every medical expense, being aware of your overall health status can help you make an informed decision. Spend some time examining your family’s medical needs, including the amount and type of treatment received in the past. This guide will give you an overview of what’s new, what’s changing, and some things to consider when choosing your benefits. Taking a closer look at your plan options can help save you money now and in the future.

What’s changing in 2017 You will see some moderate increases to your payroll deductions as medical costs continue to rise. Vanguard offers several new ways to offset these costs and will continue to provide wellness programs to help you understand and improve your health status. The Vanguard health savings account (HSA) contribution has been increased, and new vendors for HSA accounts and the vision plan bring added value to your benefits. The Health Smart Rewards wellness program has also been updated to make earning rewards easier than ever.

2016 plan design: Davis Vision 2017 plan design: VSP

In-network coverage Out-of-network reimbursement

In-network coverage Out-of-network reimbursement

Eye exams Covered in full $40 Covered in full $45

Lenses Covered in fullSingle: $30 Bifocal: $40 Trifocal: $60

Covered in fullSingle: $30 Bifocal: $50 Trifocal: $65

Frames

Covered in full for Davis Vision frames, or up to $100 for any other frame of your choice

Up to $64

Up to $130 for any frame of your choice, or $150 for featured frame brands

$70

Evaluation/Fitting for contacts Covered in full Up to $35 Covered in fullTotal $105

Contacts Covered in full up to $200 Up to $200 Covered in full up to $200

Changes to health fund accounts• Vanguard will offer crew enrolling in the HDHP a one-time increase to the HSA contribution, from $600

individual/$1,200 family to $750 individual/$1,500 family. Electing the HDHP can also save you money by lowering payroll contributions and offering tax-advantaged savings through an HSA.

• The health reimbursement arrangement (HRA) contribution for the Aetna HealthFund plans is being reduced from $350 individual/$700 family to $300 individual/$600 family.

New vendor for health savings accounts (HSAs) HealthEquity will be the new HSA vendor. With an enhanced online experience, the ability to pay health care providers directly, and interactive educational tools, HealthEquity can help maximize your savings. Find out more in the Health Savings Account section of this guide.

New vision provider VSP will be the new vision provider, giving you access to a large network of providers, more options for optical services, and the potential for lower out-of-pocket costs. Best of all, the payroll contributions remain unchanged.

2017 Health Smart Rewards wellness program

Health assessment Complete RedBrick Compass™ health assessment $50

Tobacco attestation Complete tobacco attestation $100

Biometric screenings Complete biometric screening $50

Optimal targets Year-over-year improvement

Blood pressure <120/80 $100Improve from at-risk to moderate riskAt-risk: 140–159/90–99Moderate risk: 120–139/80–89

$50

Cholesterol Non-HDL <100 $100 Reduced by 10% $50

Body mass index (BMI) >18.5 and <25 $100 Reduced by 5% $50

Glucose<100 (fasting)

<140 (non-fasting)$100

Improve from at-risk to moderate riskAt-risk: >126 (fasting)/>200 (non-fasting) Moderate risk: 100–125 (fasting)/140–199 (non-fasting)

$50

Note: If you or your covered spouse or domestic partner cannot meet a biometric target or participate in a healthy activity, you may be able to earn the same reward by different means. Contact Crew Central™, and a benefits specialist will work with you (and, if you wish, your doctor) to find other reasonable alternatives that are right for you in light of your health status, and also to determine whether a waiver may be appropriate in your situation.

Enhanced Health Smart Rewards wellness program

For 2017, you and your covered spouse or domestic partner can continue to participate in the Health Smart Rewards wellness program and earn up to $500 each in your health fund. The program has been enhanced to provide additional flexibility so you can receive rewards by simply completing the biometric screening and making incremental improvements in your biometric screening results from 2016 to 2017.

Coverage tier

Medical Dental Vision

Aetna HealthFund HDHP

$950/$1,900 $1,250/$2,500 Standard Enhanced

Crew member (CM) $27 $19 $14 $4 $8 $6.32

CM and spouse/domestic partner (DP) 79 62 48 8 16 11.49

CM and one child 47 35 32 8 15 10.21

CM, spouse/DP, and one child 109 86 62 12 23 15.32

CM, spouse/DP, and two children 138 111 77 15 31 19.16

CM, spouse/DP, and three children 168 136 92 19 38 22.35

CM, spouse/DP, and four or more children 205 167 110 23 45 27.46

CM and two children 77 60 47 11 23 14.04

CM and three children 106 84 61 15 30 17.88

CM and four or more children 146 117 81 19 37 25.54

Your 2017 payroll contributions Vanguard will continue to generously subsidize medical paycheck contributions at an 86% target subsidy rate, compared to the 65%–75% that similar companies pay toward their employees’ health care costs. While biweekly paycheck contributions for medical coverage will increase for both medical plans across coverage tiers, contributions for dental and vision coverage will remain the same. The coverage costs for full-time crew are below.

Note: To view all biweekly contributions, search “crew costs for health benefits” on CrewNet or CrewNet External (crewnet.vanguard.com).

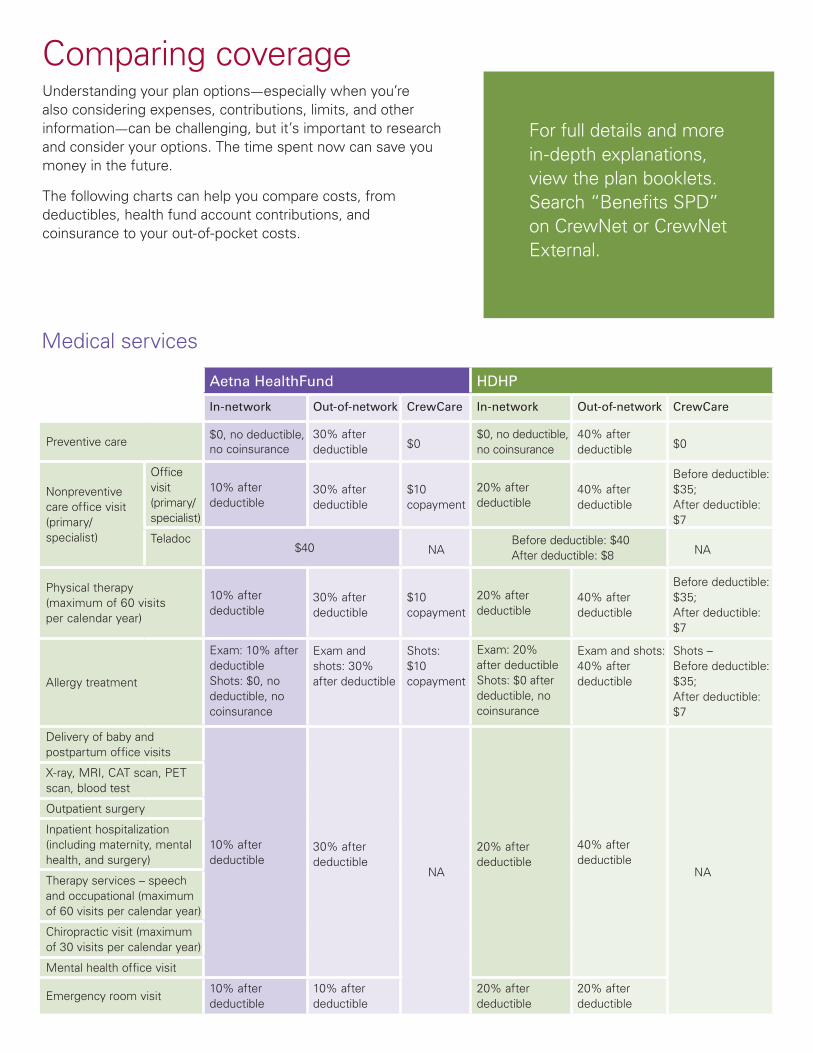

Comparing coverageUnderstanding your plan options—especially when you’re also considering expenses, contributions, limits, and other information—can be challenging, but it’s important to research and consider your options. The time spent now can save you money in the future.

The following charts can help you compare costs, from deductibles, health fund account contributions, and coinsurance to your out-of-pocket costs.

Aetna HealthFund HDHP

In-network Out-of-network CrewCare In-network Out-of-network CrewCare

Preventive care$0, no deductible, no coinsurance

30% after deductible $0

$0, no deductible, no coinsurance

40% after deductible $0

Nonpreventive care office visit (primary/ specialist)

Office visit (primary/specialist)

10% after deductible

30% after deductible

$10 copayment

20% after deductible

40% after deductible

Before deductible: $35; After deductible: $7

Teladoc$40 NA

Before deductible: $40 After deductible: $8 NA

Physical therapy (maximum of 60 visits per calendar year)

10% after deductible

30% after deductible

$10 copayment

20% after deductible

40% after deductible

Before deductible: $35; After deductible: $7

Allergy treatment

Exam: 10% after deductible Shots: $0, no deductible, no coinsurance

Exam and shots: 30% after deductible

Shots: $10 copayment

Exam: 20% after deductible Shots: $0 after deductible, no coinsurance

Exam and shots: 40% after deductible

Shots – Before deductible: $35; After deductible: $7

Delivery of baby and postpartum office visits

10% after deductible

30% after deductible

NA

20% after deductible

40% after deductible

NA

X-ray, MRI, CAT scan, PET scan, blood test

Outpatient surgery

Inpatient hospitalization (including maternity, mental health, and surgery)

Therapy services – speech and occupational (maximum of 60 visits per calendar year)

Chiropractic visit (maximum of 30 visits per calendar year)

Mental health office visit

Emergency room visit10% after deductible

10% after deductible

20% after deductible

20% after deductible

Medical services

For full details and more in-depth explanations, view the plan booklets. Search “Benefits SPD” on CrewNet or CrewNet External.

Prescription drug coverage

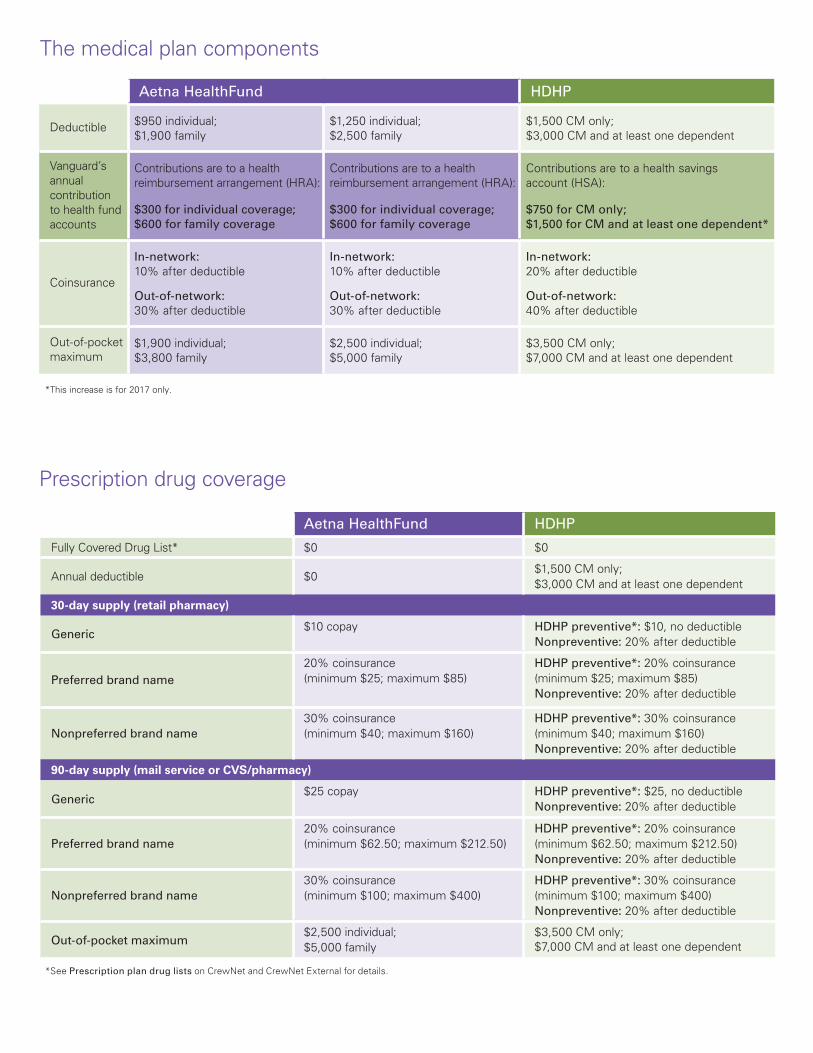

The medical plan components

Aetna HealthFund HDHP

Deductible $950 individual; $1,900 family

$1,250 individual; $2,500 family

$1,500 CM only; $3,000 CM and at least one dependent

Vanguard’s annual contribution to health fund accounts

Contributions are to a health reimbursement arrangement (HRA):

$300 for individual coverage; $600 for family coverage

Contributions are to a health reimbursement arrangement (HRA):

$300 for individual coverage; $600 for family coverage

Contributions are to a health savings account (HSA):

$750 for CM only; $1,500 for CM and at least one dependent*

Coinsurance

In-network: 10% after deductible

Out-of-network: 30% after deductible

In-network: 10% after deductible

Out-of-network: 30% after deductible

In-network: 20% after deductible

Out-of-network: 40% after deductible

Out-of-pocket maximum

$1,900 individual; $3,800 family

$2,500 individual; $5,000 family

$3,500 CM only; $7,000 CM and at least one dependent

Aetna HealthFund HDHP

Fully Covered Drug List* $0 $0

Annual deductible $0$1,500 CM only; $3,000 CM and at least one dependent

30-day supply (retail pharmacy)

Generic$10 copay HDHP preventive*: $10, no deductible

Nonpreventive: 20% after deductible

Preferred brand name20% coinsurance (minimum $25; maximum $85)

HDHP preventive*: 20% coinsurance (minimum $25; maximum $85) Nonpreventive: 20% after deductible

Nonpreferred brand name30% coinsurance (minimum $40; maximum $160)

HDHP preventive*: 30% coinsurance (minimum $40; maximum $160) Nonpreventive: 20% after deductible

90-day supply (mail service or CVS/pharmacy)

Generic$25 copay HDHP preventive*: $25, no deductible

Nonpreventive: 20% after deductible

Preferred brand name20% coinsurance (minimum $62.50; maximum $212.50)

HDHP preventive*: 20% coinsurance (minimum $62.50; maximum $212.50) Nonpreventive: 20% after deductible

Nonpreferred brand name30% coinsurance (minimum $100; maximum $400)

HDHP preventive*: 30% coinsurance (minimum $100; maximum $400) Nonpreventive: 20% after deductible

Out-of-pocket maximum$2,500 individual; $5,000 family

$3,500 CM only; $7,000 CM and at least one dependent

*See Prescription plan drug lists on CrewNet and CrewNet External for details.

*This increase is for 2017 only.

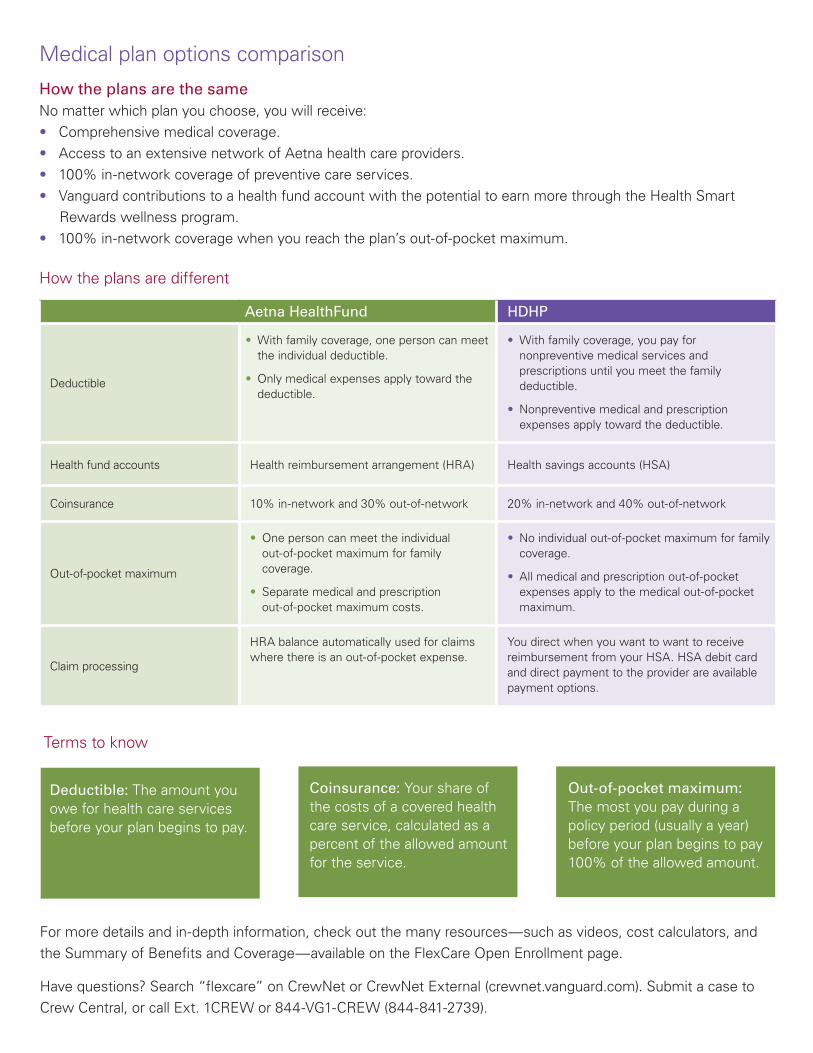

Medical plan options comparison

How the plans are the sameNo matter which plan you choose, you will receive:• Comprehensive medical coverage. • Access to an extensive network of Aetna health care providers.• 100% in-network coverage of preventive care services.• Vanguard contributions to a health fund account with the potential to earn more through the Health Smart Rewards wellness program.• 100% in-network coverage when you reach the plan’s out-of-pocket maximum.

How the plans are different

Aetna HealthFund HDHP

Deductible

• With family coverage, one person can meet the individual deductible.

• Only medical expenses apply toward the deductible.

• With family coverage, you pay for nonpreventive medical services and prescriptions until you meet the family deductible.

• Nonpreventive medical and prescription expenses apply toward the deductible.

Health fund accounts Health reimbursement arrangement (HRA) Health savings accounts (HSA)

Coinsurance 10% in-network and 30% out-of-network 20% in-network and 40% out-of-network

Out-of-pocket maximum

• One person can meet the individual out-of-pocket maximum for family coverage.

• Separate medical and prescription out-of-pocket maximum costs.

• No individual out-of-pocket maximum for family coverage.

• All medical and prescription out-of-pocket expenses apply to the medical out-of-pocket maximum.

Claim processing

HRA balance automatically used for claims where there is an out-of-pocket expense.

You direct when you want to want to receive reimbursement from your HSA. HSA debit card and direct payment to the provider are available payment options.

Coinsurance: Your share of the costs of a covered health care service, calculated as a percent of the allowed amount for the service.

Terms to know

Out-of-pocket maximum: The most you pay during a policy period (usually a year) before your plan begins to pay 100% of the allowed amount.

Deductible: The amount you owe for health care services before your plan begins to pay.

For more details and in-depth information, check out the many resources—such as videos, cost calculators, and the Summary of Benefits and Coverage—available on the FlexCare Open Enrollment page.

Have questions? Search “flexcare” on CrewNet or CrewNet External (crewnet.vanguard.com). Submit a case to Crew Central, or call Ext. 1CREW or 844-VG1-CREW (844-841-2739).

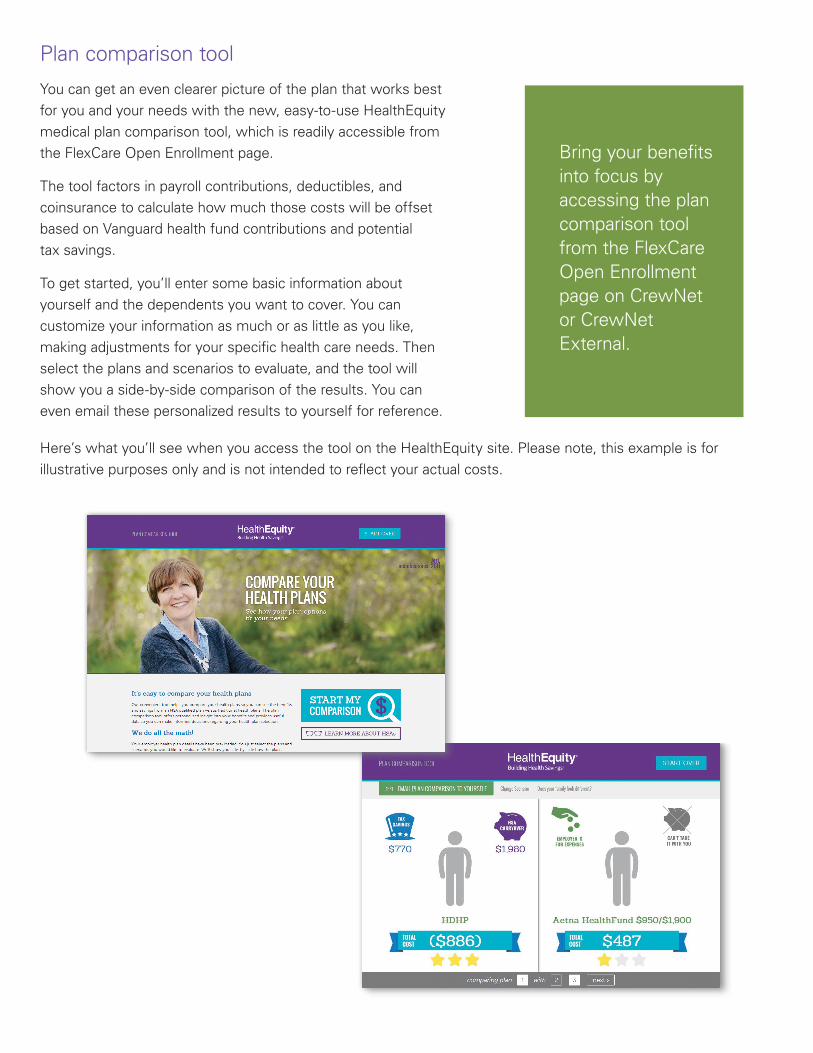

Plan comparison tool

You can get an even clearer picture of the plan that works best for you and your needs with the new, easy-to-use HealthEquity medical plan comparison tool, which is readily accessible from the FlexCare Open Enrollment page.

The tool factors in payroll contributions, deductibles, and coinsurance to calculate how much those costs will be offset based on Vanguard health fund contributions and potential tax savings.

To get started, you’ll enter some basic information about yourself and the dependents you want to cover. You can customize your information as much or as little as you like, making adjustments for your specific health care needs. Then select the plans and scenarios to evaluate, and the tool will show you a side-by-side comparison of the results. You can even email these personalized results to yourself for reference.

Bring your benefits into focus by accessing the plan comparison tool from the FlexCare Open Enrollment page on CrewNet or CrewNet External.

Here’s what you’ll see when you access the tool on the HealthEquity site. Please note, this example is for illustrative purposes only and is not intended to reflect your actual costs.

Individual Family (without a covered spouse/DP)

Family (with a covered spouse/DP)

Total maximum annual HSA contribution limit $3,400 $6,750 $6,750

Empl

oyer

co

ntrib

utio

n Vanguard’s annual contribution (contributed only if you establish your HSA with HealthEquity)

$750 $1,500 $1,500

Health Smart Rewards wellness program (contributed only if you establish your HSA with HealthEquity) $500 $500 $1,000

Your personal contribution limit via payroll deduction $2,150 $4,750 $4,250

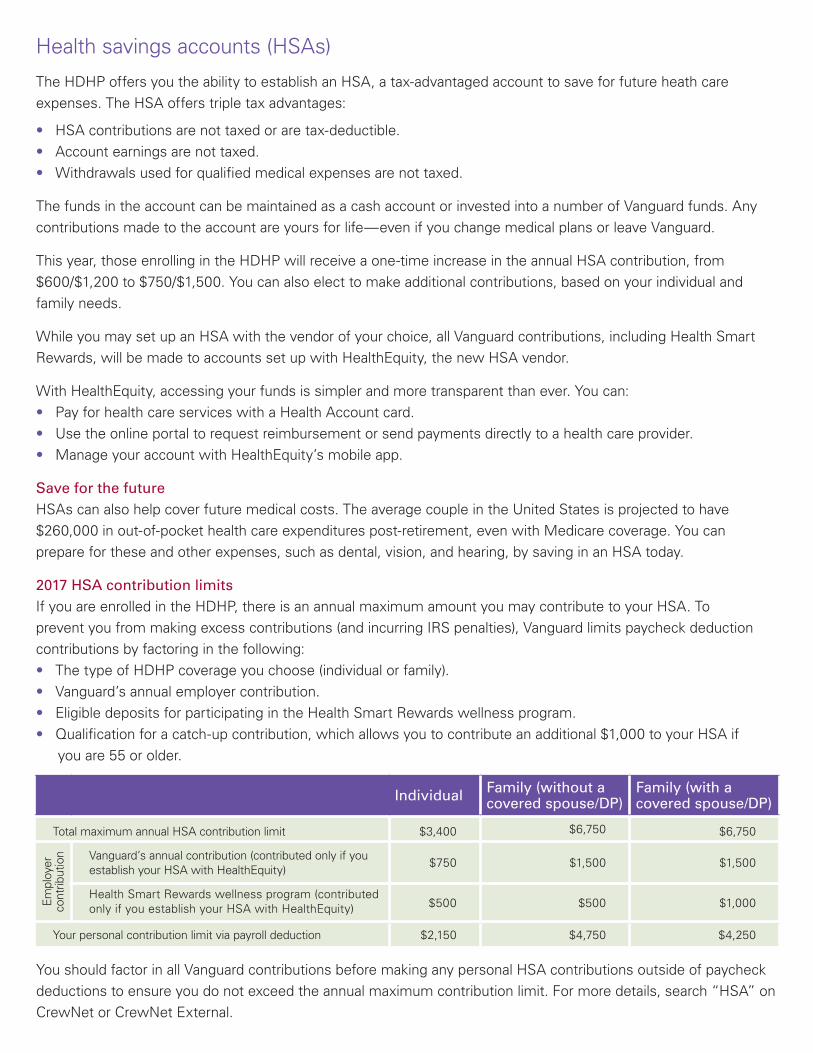

Health savings accounts (HSAs)

The HDHP offers you the ability to establish an HSA, a tax-advantaged account to save for future heath care expenses. The HSA offers triple tax advantages:

• HSA contributions are not taxed or are tax-deductible. • Account earnings are not taxed. • Withdrawals used for qualified medical expenses are not taxed.

The funds in the account can be maintained as a cash account or invested into a number of Vanguard funds. Any contributions made to the account are yours for life—even if you change medical plans or leave Vanguard.

This year, those enrolling in the HDHP will receive a one-time increase in the annual HSA contribution, from $600/$1,200 to $750/$1,500. You can also elect to make additional contributions, based on your individual and family needs.

While you may set up an HSA with the vendor of your choice, all Vanguard contributions, including Health Smart Rewards, will be made to accounts set up with HealthEquity, the new HSA vendor.

With HealthEquity, accessing your funds is simpler and more transparent than ever. You can:• Pay for health care services with a Health Account card. • Use the online portal to request reimbursement or send payments directly to a health care provider. • Manage your account with HealthEquity’s mobile app.

Save for the future HSAs can also help cover future medical costs. The average couple in the United States is projected to have $260,000 in out-of-pocket health care expenditures post-retirement, even with Medicare coverage. You can prepare for these and other expenses, such as dental, vision, and hearing, by saving in an HSA today.

2017 HSA contribution limits If you are enrolled in the HDHP, there is an annual maximum amount you may contribute to your HSA. To prevent you from making excess contributions (and incurring IRS penalties), Vanguard limits paycheck deduction contributions by factoring in the following:• The type of HDHP coverage you choose (individual or family).• Vanguard’s annual employer contribution.• Eligible deposits for participating in the Health Smart Rewards wellness program.• Qualification for a catch-up contribution, which allows you to contribute an additional $1,000 to your HSA if

you are 55 or older.

You should factor in all Vanguard contributions before making any personal HSA contributions outside of paycheck deductions to ensure you do not exceed the annual maximum contribution limit. For more details, search “HSA” on CrewNet or CrewNet External.

Flexible spending accounts (FSAs)

Health care and dependent day care FSAs let you set aside pre-tax dollars to pay for eligible out-of-pocket health care expenses (up to $2,600) and/or day care expenses (up to $5,000). To determine how much you should contribute to an FSA, consider your health fund account balance, which includes Vanguard’s employer contribution and potential Health Smart Rewards, as well as your anticipated eligible out-of-pocket medical, dental, vision, and prescription expenses. Search “FSA” on CrewNet or CrewNet External for more information.

Next steps

• Visit the FlexCare Open Enrollment page on CrewNet or CrewNet External for a closer look at your options.

• Take advantage of plan comparison tools. • Submit your elections in Workday anytime from October 31 through November 11.

You can log in at work through CrewNet or from anywhere via CrewNet External.Your elections will be effective on January 1, and they are final unless you experience a permitted election change.

Note: Under the Affordable Care Act, a Social Security number for each covered dependent is needed when you enroll to satisfy a reporting requirement.

For HDHP enrollees:Elect the limited health care FSA to remain eligible to make and receive HSA contributions. This FSA can be used immediately to pay for dental, vision, and preventive prescription drug expenses, but the plan deductible must be met to receive reimbursement for medical and nonpreventive prescription drug expenses.

For Aetna HealthFund enrollees:In most cases, you should elect a general purpose health care FSA. However, if your spouse is enrolled in a high-deductible health plan, you should consider electing a limited health care FSA so your spouse can remain eligible to make and receive HSA contributions.

Aetna HealthFund participants cannot start using the health care FSA for medical expenses until the HRA balance is depleted. An FSA may benefit you if you expect to have out-of-pocket costs for medical expenses (beyond your HRA balance) or dental, vision, and prescription expenses that are not eligible for HRA use.

Search “flexcare” on CrewNet or CrewNet External.

Use the PayFlex FSA Savings Calculator (available on the FlexCare Open Enrollment page) to estimate how much you can save by setting aside pre-tax funds.

Have questions?Connect with Health Advocate: Use this free, confidential service to speak with an external Personal Health Advocate regarding your health care concerns, insurance issues, and more. Call 855-424-9400 or email [email protected].

Connect with Vanguard: Search “flexcare” on CrewNet or CrewNet External (crewnet.vanguard.com). Submit a case to Crew Central, or call Ext. 1CREW or 844-VG1-CREW (844-841-2739).

Note: This summary provides an overview; further details can be found in the formal plan documents. If there is a conflict between this summary and the formal plan documents, the formal plan documents are the final authority and will govern in all cases.

© 2016 The Vanguard Group, Inc. All rights reserved.

BBBBLKSL 102016