Embed Size (px)

Citation preview

Florida Housing Finance Corporation

Credit Underwriting Report

Smathers Phase Two

RFA 2014‐103 (2014‐306S) / 2013‐526C

State Apartment Incentive Loan Program, ELI Gap, & 4% Non‐Competitive Housing Credits Program

Section A: Report Summary

Section B: SAIL & ELI Gap Loan Special and General Loan Closing Conditions

& Housing Credit Allocation Recommendation and Contingencies

Section C: Supporting Information and Schedules

Prepared by

AmeriNational Community Services, Inc.

Final Report

December 4, 2014

Exhibit A Page 1 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

December 4, 2014

Smathers Phase Two

TABLE OF CONTENTS

Section A

Report Summary Page Recommendation A1‐A8 Overview A9‐A13 Uses of Funds A14‐A17 Operating Pro Forma A18‐A20

Section B

SAIL & ELI Gap Loan Special and General Loan Closing Conditions & B1‐5 Housing Credit Allocation Recommendation and Contingencies B6

Section C

Supporting Information and Schedules Additional Development & Third Party Information C1‐C5 Borrower Information C6‐C13 Guarantor Information C14 Syndicator Information C15 General Contractor Information C16‐C17 Property Management Information C18‐C19

Exhibits

15 Year Pro Forma 1 Description of Features and Amenities 2 1‐5 HC Allocation Calculation 3 1‐2 Completeness and Issues Checklist 4 1‐2

Exhibit A Page 2 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

December 4, 2014

Section A

Report Summary

Exhibit A Page 3 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐1 December 4, 2014

Recommendation AmeriNational Community Services, Inc. (“AmeriNational”) recommends a State Apartment Incentive Loan (“SAIL”) of $1,138,150, an Extremely Low Income (“ELI”) Gap loan of $975,000, and an annual 4% Housing Credits (“HC”) allocation of $1,024,583 to Smathers Phase Two, LLC (“Applicant”) for the construction and permanent phase financing of Smathers Phase Two (“Development”).

Address: City: Zip Code:

County: County Size:

Development Category: Development Type:

Construction Type:

Demographic Commitment: Elderly: Homeless: ELI: Units @ AMI

Farmworker or Commercial Fish Worker: Family: Link: Units

Buildings: Residential ‐ Non‐Residential ‐

Parking: Parking Spaces ‐ Accessible Spaces ‐

Concrete block with reinforced walls and beams supporting post‐tensions concrete slabs

200 Feet North of SW 11th Street

and 100 feet East of SW 30th

Avenue Miami 33135

Miami‐Dade Large

Redevelopment Mid‐Rise with Elevator

DEVELOPMENT & SET‐ASIDESDevelopment Name: Smathers Phase Two

Program Numbers: RFA 2014‐103 2014‐306S 2013‐526C

Gross HC

Rent

$487 $40,908

Yes 14 33%

7

$41 $487 $351 $487 $487

$0 $0

$0

Appraiser

Rents CU Rents

Annual Rental

Income

0.0 1.0 7 462 33% $392 $0

Low

HOME

Rents

High

HOME

Rents

Utility

Allow

RD/HUD

Cont

Rents

Net HC

Rent

Applicant

Rents

Bed

Rooms

Bath

Rooms Units

Square

Feet AMI%

$487 $554 $487 $487 $487 $233,760

$40,908

0.0 1.0 40 462 50% $595 $595 $747 $41

$54 $487 $366 $487 $487 $4871.0 1.0 7 576 33% $420

0.0 1.0 2 462 50% $595 $595

$637 $8091.0 1.0 28 576 50% $637

576 50% $637 $637 $809

$747

$487 $487 $163,632$54 $487 $583 $487

$554 $13,296$41 $0 $554 $540 $536

$13,992$54 $0 $583

$0 $673 $659 $655

$765

$843 $50,580

$673 $64,608

$290,088

$819

0.0 1.0 8 462 60% $714 $0 $0 $41

$582 $559 $5831.0 1.0 2

$0

$687 $711

2.0 2.0 5 864 60% $918 $0

$0 $0 $54 $0 $711 $7101.0 1.0 34 576 60%

$75 $0 $843 $843

133 71,550 $911,772

1 0

82 4 Rental Assistance Units: 82 Set Asides: Program % of Units # of Units % AMI Term (Years)

MMRB 40.0% 52 60% 30

ELI Gap 10.0% 14 33% 30

SAIL 90.0% 119 60% 30

Surtax 100.0% 133 80% 30

Surtax 10.0% 14 33% 30

HOME 3.0% 4 50% 30

HOME 12.0% 16 80% 30

HC 10.0% 14 33% 30

HC 90.0% 119 60% 30

Exhibit A Page 4 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐2 December 4, 2014

Absorption Rate: units per month for months.

Occupancy Rate at Stabilization: Physical Occupancy Economic Occupancy

Occupancy Comments

DDA?: QCT?:

Site Acreage: Density: Flood Zone Designation:

Zoning: Flood Insurance Required?:

Applicant/Borrower:

General Partner 1:

Limited Partner 1:

Guarantor(s):

Developer:

Principal 1

Principal 2

Principal 3

Principal 4

Principal 5

General Contractor 1:

Management Company:

Syndicator:

Bond Issuer:

Architect:

Market Study Provider:

Appraiser:

35 4

T5‐R ‐ Urban Center Zone ‐ Restricted No

DEVELOPMENT TEAM

Smathers Phase Two, LLC % Ownership

Smathers Phase Two Manager, LLC 0.01%

98.0% 97.0%

Senior LIHTC properties report 0‐3% vacancy rates.

Yes No

2.20 60.5 X

Raymond James Tax Credit Funds, Inc. or an affi l iate 99.99%

The Urban Development Group, LLC

Albert Milo, Jr. (Construction Completion only)

Smathers Phase Two, LLC

Smathers Phase Two Manager, LLC

RUDG, LLC

PRH Affordable Investments, LLC

PRH Investments, LLC

Smathers Phase Two Developer, LLC

RUDG, LLC

PRH Affordable Investments, LLC

Jorge M. Perez

The Urban Development Group, LLC

Albert Milo, Jr.

TRG Management Company of Florida

Raymond James Tax Credit Funds, Inc.

Housing Finance Authority of Miami‐Dade County

Fortune Urban Construction, LLC

Modis Architects, LLC

Novogradac & Company, LLP

Novogradac & Company, LLP

PERMANENT FINANCING INFORMATION1st Source 2nd Source 3rd Source 4th Source 5th Source Other

Lender/Grantor CITI/HFAMD FHFC FHFCMiami‐Dade

CountyCity of Miami

Amount $2,835,000 $1,138,150 $975,000 $8,250,000 $698,000

Loan Term 15 30 30 30 30

All In Interest Rate 5.479% 1.0% 0.0% 0.3% 3.0%

Market Rate/Market

Financing LTV22.50% 31.53% 7.74% 65.48% 5.54%

Amortization 35 0 0 0 30

Loan to Cost 11.5% 4.6% 4.0% 33.4% 2.8%

Restricted Market

Financing LTV70.9% 99.33% 24.4% 206.3% 17.5%

Operating/Deficit

Service Reserve$286,817

Debt Service Coverage 1.57 1.48 1.48 1.30 1.30

Period of Operating

Expenses/Deficit

Reserve in Months

5.5

Exhibit A Page 5 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐3 December 4, 2014

Land Value

Deferred Developer Fee $750,087

$2,100,000

Market Rent/Market Financing Stabilized Value $12,600,000

Projected Net Operating Income (NOI) ‐ 15 Year $283,432

Year 15 Pro Forma Income Escalation Rate 2%

Year 15 Pro Forma Expense Escalation Rate 3%

Rent Restricted Market Financing Stablized Value $4,000,000

Projected Net Operating Income (NOI) ‐ Year 1 $285,749

CONSTRUCTION/PERMANENT SOURCES:

Source Lender Construction Permanent Perm Loan/Unit

Bond Structure Tax Exempt "Back to Back" Loan Structure

Housing Credit Syndication Price $1.04

Housing Credit Annual Allocation $1,024,583

Tax Exempt Loan CITI/HFAMD $12,000,000 $2,835,000 $21,316

SAIL FHFC $1,138,150 $1,138,150 $8,558

SAIL ELI GAP FHFC $975,000 $975,000 $7,331

Surtax Miami‐Dade County $8,250,000 $8,250,000 $62,030

HOME City of Miami $698,000 $698,000 $5,248

HC Equity RJTCF $2,439,707 $10,023,766 $75,367

Deferred Developer Fee Developer $2,103,057 $750,087 $5,640

TOTAL $27,603,914 $24,670,003 $185,490

Note: During the construction phase, all subordinate funding will be available and a portion will be drawn to pay down the Borrower Loan until such time as it converts to the Permanent Loan.

Exhibit A Page 6 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐4 December 4, 2014

Changes from the Application:

COMPARISON CRITERIA YES NO

Does the level of experience of the current team equal or exceed that of the team described in the Application?

x

Are all funding sources the same as shown in the Application? 1

Are all local government recommendations/contributions still in place at the level described in the Application?

2

Is the Development feasible with all amenities/features listed in the Application? x

Do the site plans/architectural drawings account for all amenities/features listed in the Application?

x

Does the Applicant have site control at or above the level indicated in the Application? x

Does the Applicant have adequate zoning as indicated in the Application? x

Has the Development been evaluated for feasibility using the total length of set‐aside committed to in the Application?

x

Have the Development costs remained equal to or less than those listed in the Application?

3

Is the Development feasible using the set‐asides committed to in the Application? x

If the Development has committed to serve a special target group (e.g. elderly, large family, etc.), do the development and operating plans contain specific provisions for implementation?

x

HOME ONLY: If points were given for match funds, is the match percentage the same as or greater than that indicated in the Application?

N/A

HC ONLY: Is the rate of syndication the same as or greater than that shown in the Application?

x

Is the Development in all other material respects the same as presented in the Application?

4

The following are explanations of each item checked "No" in the table above:

1. The City of Miami Housing and Commercial Loan Committee approved an allocation of $698,000 of HOME funding for the construction and permanent financing of the Development according to a letter dated July 11, 2014. The Application’s Construction Funding Sources illustrated the $12,000,000 in first mortgage financing would be paid off in its entirety at or prior to completion of the construction / stabilization phase. However, since the Application, a Citi Community Capital (“CITI”) term sheet dated August 27, 2014 illustrates CITI will provide the Housing Finance Authority of Miami‐Dade (“HFAMD” or “Issuer”) a $12,000,000 tax‐exempt direct construction/permanent loan (“Funding Loan”) evidenced by the issuance of tax‐exempt Multifamily Housing Revenue Notes (“MMRN”) issued by the HFAMD at loan closing. HFAMD will in turn provide a tax exempt construction loan to the Applicant (“Borrower Loan”) on a draw down basis for the construction phase financing of

Exhibit A Page 7 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐5 December 4, 2014

the Development. The Borrower Loan will be paid down until such time as it converts to a CITI Permanent Loan.

2. The Applicant provided a Fiscal Year 2014 Surtax Funding Loan Commitment from Miami‐Dade County that illustrated $12,364,571 in Surtax construction and permanent financing of the Development. However, the amount of the Surtax loan has been reduced to $8,250,000 according to a Miami‐Dade County Board of County Commissioners Memorandum dated October 21, 2014. A 2013 Local Government Verification of Contribution of Loan of $160,000 from Miami‐Dade County was provided within the Application; however, according to the Applicant, it will not utilize this funding. Therefore, it was removed from the sources of funds.

3. Total Development Costs increased $607,341 since the Application due to increases in construction costs and developer fee.

4. The Applicant increased the total number of units from 130 to 133 as outlined within this report. Florida Housing staff approved this change on December 2, 2014. The Applicant selected the Development Category: Redevelopment (where 50% or more of the units are new construction) and states the number of rental assistance units is 130 or 100% of the total units. Please refer to Issues and Concerns #1.

Does the Development Team have any FHFC Financed Developments on the Past Due/Non‐Compliance Report? According to the FHFC Asset Management Noncompliance Report dated September 30, 2014, the following noncompliance issues exist for the Development Team:

Emerald Villas (HC 2009‐530C) Physical Inspection per the Initial Review on April 16, 2014 According to the FHFC Past Due Report dated September 30, 2014, no past due issues exist for the Development Team. This recommendation is subject to satisfactory resolution, as determined by Florida Housing, of any outstanding past due items or non‐compliance issues applicable to the Development Team prior to the issuance of the annual HC allocation recommended herein.

Strengths:

1. The Development Team has demonstrated the ability to successfully develop and operate

affordable multifamily rental communities using a variety of different subsidies.

2. The Development will operate 82 or 62% of its 133 total units as Public Housing units that operate under a Consolidated Annual Contributions Contract (“ACC”) between Miami‐Dade County and the U.S. Department of Housing and Urban Development (“HUD”) in which tenants pay rental rates based on 30% of their adjusted monthly income (the “30% ACC Provision”). Rent Subsidies are comprised of utility and operating subsidies paid to a Public Housing development by HUD that are utilized to offset the costs associated with operations that are greater than the rental

Exhibit A Page 8 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐6 December 4, 2014

revenue of the 30% ACC Provision. HUD through PHCD shall pay rent subsidies on an annual basis to the Applicant to achieve “breakeven” operations on 82 of the total 133 units.

3. According to the appraisal, the Development will achieve the maximum allowable net restricted rents on the remaining 51 units set‐aside at or below 50% and 60% of Area Median Income (“AMI”).

Other Considerations:

None Issues and Concerns:

1. The Applicant selected a Development Category of Redevelopment (where 50% or more of the units

are new construction) and wherein 100% of the Development’s units have rental assistance. Subsequently to the Application, the Applicant provided an August 1, 2014 Rental Assistance Letter from HUD that illustrates the development known as Smathers Plaza and its 182 units will receive rental assistance in the form of HUD subsidies under an ACC between the Housing Authority and HUD. According to the RFA, the Application will be held to the number of Rental Assistance (“RA”) units stated in the applicable letter throughout the entire compliance period, subject to Congressional appropriation and continuation of the rental assistance program Mitigant: On November 25, 2014, the Applicant provided a revised letter from HUD illustrating the Development will operate 82 RA units under an ACC between HUD and Miami‐Dade County as reflected within this credit underwriting report. The Development appears to be financially feasible with less than 100% of its units operating with RA.

2. According to Rule Chapter 67.48.0072 F.A.C., in determining whether or not to provide a positive recommendation in connection with a proposed Development, the Credit Underwriter will consider the prior and recent performance history of the Applicant, Developer, any Financial Beneficiary of the Applicant or Developer, and the General Contractor in connection with any other affordable housing development. The performance history shall consider instances involving a foreclosure, deed in lieu of foreclosure, financial arrearage, or other event of material default in connection with any affordable housing development or the documents governing financing or operation of any such development.

Jorge M. Perez provided a Statement of Financial Credit Affairs dated November 20, 2014 for another transaction illustrating he is a principal of special purpose entities of The Related Group that had (1) a foreclosure, deed‐in‐lieu (“DIL”), loan default or payment moratorium, (2) a loan restructuring due to negative cash flow, (3) a principal or interest payment deferred, and/or (4) a loan in arrears for principal, interest, taxes, and insurance premiums due. In addition, Mr. Perez is involved in a pending legal action where there is a material monetary claim (more that than $10K) whereby he is named as a defendant.

Mitigating Factor: The Applicant provided documentation dated November 24, 2014 that illustrates none of the developments in question are affordable housing developments but instead are condominium projects developed by The Related Group. According to the Applicant, at the time of

Exhibit A Page 9 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐7 December 4, 2014

the real estate market collapse The Related Group was developing approximately 8,700 condominium units amongst 20 projects nationwide. AmeriNational estimates these occurrences of loan workouts, financial restructuring, or DIL of condominium projects developed by The Related Group or Jorge M. Perez do not represent a material adverse condition affecting the successful redevelopment of the Development. The one matter of litigation pending where Jorge Perez is named as a defendant is a derivative lawsuit brought by a shareholder of corporation within the ownership structure of a development entity demanding enforcement of note and pledge agreement. There is no reasonable expectation of loss to Jorge Perez by this suit.

Waiver Requests: None Special Conditions:

1. Pursuant to Rule Chapter 67‐48 F.A.C. (the “Rule”), the Development’s operations must satisfy a minimum 1.10 debt service coverage (“DSC”) with all first and second mortgages with Housing Credits and a maximum 1.50 DSC for the SAIL loan including all superior mortgages. The Miami‐Dade County Surtax Program requires the Development’s operations to satisfy an overall maximum 1.30 DSC on all mortgages during year one and a minimum 1.15 DSC in year 15 for Surtax funding with Tax Exempt Bonds. The Surtax Program requires a minimum 20% deferral of Developer Fee. Pursuant to the 1‐ and 15‐year Operating Pro Forma, these requirements have been satisfied.

2. As required by the Federal Fair Housing Act (the “Act”), at least 80% of the total units will be rented to residents that qualify as Elderly pursuant to the Act.

Additional Information:

1. The Development, located in Miami‐Dade County, is not located within a 2.5 mile radius of any

longitude/latitude coordinates for any county on the Restricted Areas Chart of the Non‐Competitive 4% HC Application Instructions.

2. In accordance with RFA 2014‐103, FHFC limits the Total Development Cost (“TDC”) per unit for all Developments categorized by the construction type of the units as indicated by the Applicant in the RFA. The maximum TDC per unit for the construction type specified by the Applicant (mid‐rise, 5‐6 story, concrete) is $221,000 per unit. With a total of 133 units, the maximum TDC for the Development is $29,393,000 (133 units @ $221,000/unit). The TDC as underwritten equals $24,670,003 or $185,489/unit. As such, the Development does not exceed the per unit maximum TDC and is eligible for funding.

Recommendation: AmeriNational recommends a SAIL loan of $1,138,150, an ELI Gap loan of $975,000, and an annual allocation of 4% HC of $1,024,583 to the Applicant for the construction and permanent phase financing of the Development.

Exhibit A Page 10 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐8 December 4, 2014

These recommendations are based upon the assumptions detailed in the Report Summary (Section A), and Supporting Information and Schedules (Section C). In addition, these recommendations are subject to the SAIL & ELI Gap Loan Special and General Conditions and the Housing Credit Allocation Recommendation and Contingencies (Section B). This recommendation is only valid for six months from the date of the report. The reader is cautioned to refer to these sections for complete information. Prepared by: Reviewed by:

Michael Drapkin, Jr. George J. Repity VP – Chief Credit Underwriter Senior Credit Underwriter

Exhibit A Page 11 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐9 December 4, 2014

Overview Construction Financing Sources:

Source LenderApplicant's

Total

Applicant's

Revised Total

Underwriter's

Total

Interest

Rate

Debt Service

During

Construction

MHRN CITI/HFAMD $12,000,000 $12,000,000 $12,000,000 3.854% $320,192

SAIL FHFC $1,138,150 $1,138,150 $1,138,150 1.00% $0

ELI Gap FHFC $975,000 $975,000 $975,000 0.00% $0

Surtax

Miami‐Dade

County $12,364,571 $8,250,000 $8,250,000 0.00% $0

HOME City of Miami $0 $698,000 $698,000 0.00% $0

HC Equity RJTCF $1,916,988 $2,020,453 $2,439,707

Deferred Developer

Fee Developer $0 $2,053,663 $2,103,057

$28,394,709 $27,135,266 $27,603,914 $320,192Total :

Proposed First Mortgage Loan: The Applicant provided an August 27, 2014 LOI that illustrates CITI will provide the HFAMD a $12,000,000 tax‐exempt direct construction/permanent loan (“Funding Loan”) evidenced by the issuance of tax‐exempt Multifamily Housing Revenue Notes issued by the HFAMD at loan closing. HFAMD will in turn provide a tax exempt construction loan to the Applicant (“Borrower Loan”) on a draw down basis for the construction phase financing of the Development. Terms and conditions of the Funding Loan include: a term of 24 months with two 6 month extensions available, and an interest only, variable rate equal to SIFMA (presently at 0.05%) plus a 2.50% spread and a 1.00% cushion required by CITI. AmeriNational added 0.25% for the Issuer Administrative Fee, 0.033% for the Issuer Compliance Monitoring Fee, and 0.021% for the fiscal agent fee to derive the “all‐in” interest rate of 3.854% during the construction phase. Proposed Second Mortgage Loan – SAIL: The Applicant applied to Florida Housing for a $1,138,150 SAIL Program loan under Request for Applications 2014‐103 (“RFA”) for the construction financing of the Development. The SAIL loan term will be 30 years, as requested by the HC syndicator and as permitted by the RFA and the Rule. The SAIL loan shall be non‐amortizing with a 1.00% interest rate over the life of the loan with payments based upon available cash flow as determined by Florida Housing. Annual payments of all applicable fess will be required. SAIL Program loan proceeds may be amongst the sources of funds utilized to pay down the first mortgage Borrower Loan during the construction phase. SAIL loan proceeds shall be disbursed during

Exhibit A Page 12 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐10 December 4, 2014

the construction phase in an amount per construction draw which does not exceed the ratio of the SAIL loan to Total Development Costs, unless approved by the credit underwriter. Proposed Third Mortgage Loan – ELI Gap: The Applicant requested an Extremely Low Income (“ELI”) Gap loan of $975,000 for the construction financing of the Development. The RFA states an Applicant is eligible for “a forgivable loan in the amount of $75,000 for each required ELI set‐aside unit, not to exceed a total of $1,800,000.” Therefore, the Applicant is eligible to receive an ELI Gap loan of up to $1,050,000 for its 14 ELI set‐aside units; however, is limited to its request of $975,000. The ELI Gap loan will have non‐amortizing payments at 0% interest per year over the life of the loan with principal forgivable at maturity provided the units are targeted to ELI Households for the duration of the 30‐year Compliance Period. It shall have a term of 30 years, as requested by the HC syndicator. After 15 years all of the ELI Set‐Aside units may convert to serve residents at or below 60% of AMI. ELI Gap loan proceeds shall be disbursed during the construction phase in an amount per construction draw which does not exceed the ratio of the ELI Gap loan to Total Development Costs, unless approved by the credit underwriter. Proposed Fourth Mortgage Loan ‐ Surtax: Under the Fiscal Year 2014 Consolidated Request for Applications (“RFA”) for Surtax “Gap” funding (Category two), Miami‐Dade County will provide a Surtax loan in an amount not to exceed $8,250,000 for the construction and permanent financing of the proposed Development. Terms and conditions include a 0% interest only rate during the construction phase. Additional terms and conditions are outlined in the Permanent Sources of Funds. Proposed Fifth Mortgage Loan ‐ HOME: Pursuant to a letter dated July 11, 2014, the City of Miami Housing and Commercial Loan Committee will provide $698,000 in HOME Investment Partnership (“HOME”) funds to the Applicant for the construction and permanent financing of the Development. HOME loan proceeds will be used for construction hard costs. Terms and conditions of the HOME loan include a 0% interest only rate during the construction phase. Additional terms and conditions are outlined in the Permanent Sources of Funds. Additional Construction Sources of Funds: According to a syndication LOI dated October 31, 2014, between Raymond James Tax Credit Funds, Inc. (“RJTCF”) and the Applicant, RJTCF will purchase a 99.99% limited member interest in the Applicant at loan closing. The HC allocation will be syndicated at a rate of $1.04 for each $1.00 of tax credits delivered. A total of $1,539,707 (15.4% of total equity available) is to be funded at construction loan closing, which is an amount sufficient to meet the 15% criteria as outlined in the RFA. Total equity installments of $2,439,707 will be available during the construction period. Deferred Developer Fee: Per the CITI LOI, any payment of Developer Fee prior to permanent loan conversion is subject to CITI’s approval. The Applicant will be required to defer $2,103,057 of its total Developer Fee.

Exhibit A Page 13 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐11 December 4, 2014

Permanent Financing Sources:

Source LenderApplicant's

Total

Applicant's

Revised Total

Underwriter's

Total

Interest

Rate

Amortization

Years

Term

Years

Annual

Debt Service

Tax Exempt Loan CITI $0 $2,835,000 $2,835,000 5.479% 35 15 $182,219

SAIL FHFC $1,138,150 $1,138,150 $1,138,150 1.00% 0 30 $11,382

ELI Gap FHFC $975,000 $975,000 $975,000 0.00% 0 30 $0

Surtax

Miami‐Dade

County $12,364,571 $8,250,000 $8,250,000 0.32% 0 30 $26,586

Fifth Mortgage City of Miami $0 $698,000 $698,000 3.00% 30 30 $0

HC Equity RJTCF $9,584,941 $10,102,267 $10,023,766

Deferred Developer

Fee Developer $0 $228,494 $750,087

$24,062,662 $24,226,911 $24,670,003 $220,187Total :

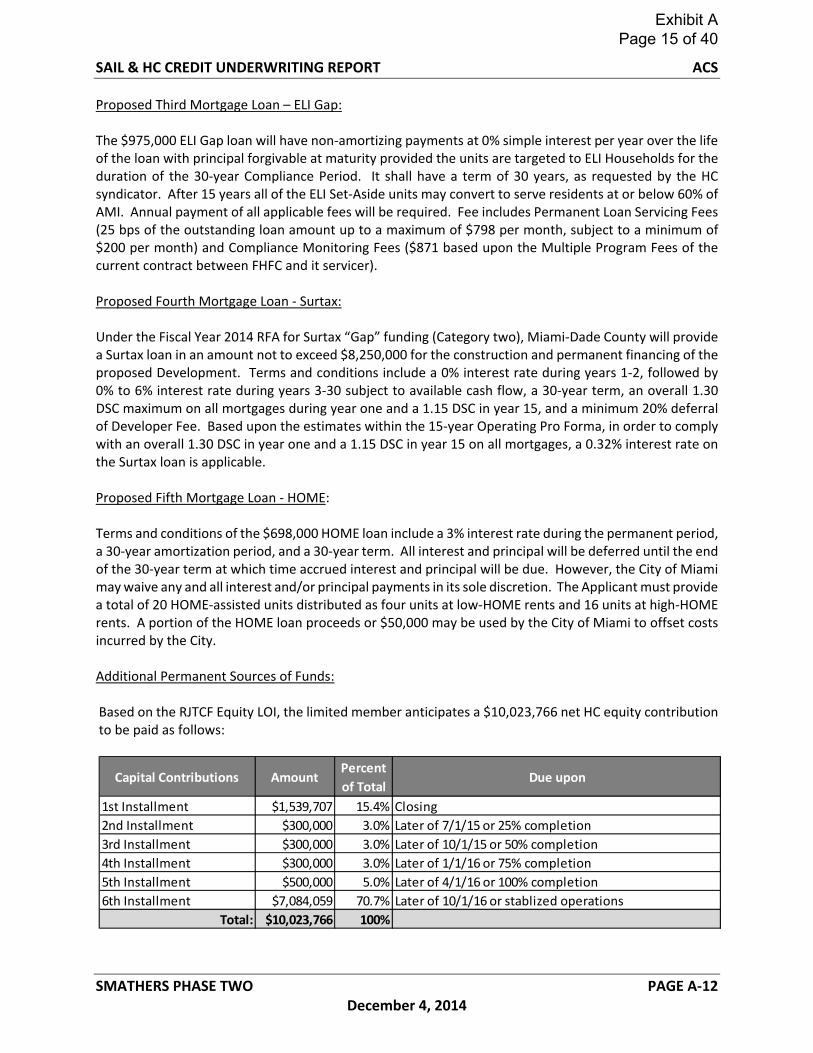

Proposed First Mortgage Loan: According to the CITI LOI, the $12,000,000 Borrower Loan will be paid down with other sources identified herein to $2,835,000 (“Permanent Loan”) or such other amount as determined by CITI during its underwriting performed at permanent loan conversion. The following conditions must be met in order to convert to permanent financing: 1) construction must be complete, 2) the Development must be a minimum of 90% occupied for 90 continuous days, and 3) the Development must meet a minimum 1.31 DSC in order to ensure a 1.15 DSC in year 15 with a loan to value (“LTV”) not to exceed 80% based upon a re‐underwriting of the actual income and expenses in place at the time of conversion. Terms and conditions of the Permanent Loan include a 15‐year term and a 35‐year amortization period. The “all‐in” fixed interest rate used for underwriting purposes is presently estimated at 5.479% and is based upon the sum of the 18‐year maturity “AAA” bond rates as published by the Thompson Municipal Market Monitor plus a 2.20% CITI spread. According to CITI, as of October 29, 2014 the 15‐year maturity rate was 2.55%. AmeriNational added 0.25% for the Issuer Administrative Fee, 0.141% for the Issuer Compliance Monitoring Fee, 0.088% for the fiscal agent fee, and an underwriting cushion of 0.25% to account for possible future rate fluctuations to arrive at the “all‐in” permanent loan rate. Proposed Second Mortgage Loan – SAIL: The Applicant applied to Florida Housing for a $1,138,150 SAIL Program loan under RFA 2014‐103 for the permanent financing of the Development. The SAIL loan term will be 30 years as requested by the HC syndicator and as permitted by the RFA and the Rule. The SAIL loan shall be non‐amortizing with a 1.00% interest rate over the life of the loan with payments based upon available cash flow as determined by Florida Housing. Any unpaid interest will be deferred until cash flow is available. However, at maturity of the SAIL loan, all principal and interest will be due. Annual payments of all applicable fees will be required. Fees include Permanent Loan Servicing Fees (25 bps of the outstanding loan amount up to a maximum of $798 per month, subject to a minimum of $200 per month) and Compliance Monitoring Fees ($871 based upon the Multiple Program Fees of the current contract between FHFC and it servicer).

Exhibit A Page 14 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐12 December 4, 2014

Proposed Third Mortgage Loan – ELI Gap: The $975,000 ELI Gap loan will have non‐amortizing payments at 0% simple interest per year over the life of the loan with principal forgivable at maturity provided the units are targeted to ELI Households for the duration of the 30‐year Compliance Period. It shall have a term of 30 years, as requested by the HC syndicator. After 15 years all of the ELI Set‐Aside units may convert to serve residents at or below 60% of AMI. Annual payment of all applicable fees will be required. Fee includes Permanent Loan Servicing Fees (25 bps of the outstanding loan amount up to a maximum of $798 per month, subject to a minimum of $200 per month) and Compliance Monitoring Fees ($871 based upon the Multiple Program Fees of the current contract between FHFC and it servicer). Proposed Fourth Mortgage Loan ‐ Surtax: Under the Fiscal Year 2014 RFA for Surtax “Gap” funding (Category two), Miami‐Dade County will provide a Surtax loan in an amount not to exceed $8,250,000 for the construction and permanent financing of the proposed Development. Terms and conditions include a 0% interest rate during years 1‐2, followed by 0% to 6% interest rate during years 3‐30 subject to available cash flow, a 30‐year term, an overall 1.30 DSC maximum on all mortgages during year one and a 1.15 DSC in year 15, and a minimum 20% deferral of Developer Fee. Based upon the estimates within the 15‐year Operating Pro Forma, in order to comply with an overall 1.30 DSC in year one and a 1.15 DSC in year 15 on all mortgages, a 0.32% interest rate on the Surtax loan is applicable. Proposed Fifth Mortgage Loan ‐ HOME: Terms and conditions of the $698,000 HOME loan include a 3% interest rate during the permanent period, a 30‐year amortization period, and a 30‐year term. All interest and principal will be deferred until the end of the 30‐year term at which time accrued interest and principal will be due. However, the City of Miami may waive any and all interest and/or principal payments in its sole discretion. The Applicant must provide a total of 20 HOME‐assisted units distributed as four units at low‐HOME rents and 16 units at high‐HOME rents. A portion of the HOME loan proceeds or $50,000 may be used by the City of Miami to offset costs incurred by the City. Additional Permanent Sources of Funds: Based on the RJTCF Equity LOI, the limited member anticipates a $10,023,766 net HC equity contribution to be paid as follows:

Capital Contributions AmountPercent

of Total Due upon

1st Installment $1,539,707 15.4% Closing

2nd Installment $300,000 3.0% Later of 7/1/15 or 25% completion

3rd Installment $300,000 3.0% Later of 10/1/15 or 50% completion

4th Installment $300,000 3.0% Later of 1/1/16 or 75% completion

5th Installment $500,000 5.0% Later of 4/1/16 or 100% completion

6th Installment $7,084,059 70.7% Later of 10/1/16 or stablized operations

Total: $10,023,766 100%

Exhibit A Page 15 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐13 December 4, 2014

Annual Credits Per Syndication Agreement $963,920

Total Credits Per Syndication Agreement $9,639,200

Calculated HC Rate: $1.04

Limited Member Ownership Percentage 99.99%

Proceeds During Construction $2,439,707

Deferred Developer Fee: As indicated in the CITI LOI, any payment of developer fee prior to permanent loan conversion is subject to CITI’s approval. The Applicant will be required to permanently defer $750,087 of the total developer fee after stabilization.

Exhibit A Page 16 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐14 December 4, 2014

Uses of Funds

Applicant CostsRevised

Applicant Costs

Underwriters

Total Costs ‐ CURCost Per Unit

HC Ineligible

Costs ‐ CUR

Demolition $100,000 $0 $15,000 $113 $15,000

New Rental Units $13,305,305 $13,965,000 $13,446,039 $101,098 $405,305

Site Work $0 $0 $815,000 $6,128 $0

Swimming Pool $0 $0 $0 $0 $0

General Conditions $782,600 $878,616 $856,562 $6,440 $0

Overhead $254,800 $292,872 $285,521 $2,147 $0

Profit $782,600 $878,616 $856,562 $6,440 $0

Builder's Risk Insurance $240,407 $108,370 $108,289 $814 $0

Payment and Performance Bonds $148,200 $144,373 $144,204 $1,084 $0

Furniture, Fixture, & Equipment $200,000 $100,000 $100,000 $752 $0

Total Construction Contract/Costs $16,213,912 $16,367,847 $16,627,177 $125,016 $420,305

Hard Cost Contingency $845,710 $834,685 $831,358 $6,251 $0

Fees for LOC used as Construction Surety $0 $0 $0 $0 $0

$17,059,622 $17,202,532 $17,458,535 $131,267 $420,305

CONSTRUCTION COSTS:

Total Construction Costs: Notes to Actual Construction Costs: 1. A Standard Form of Agreement between the Owner and General Contractor where the basis of

payment is a stipulated sum of $16,615,389 (the “Construction Contract”) dated November 21, 2014 was provided. The General Contractor shall achieve substantial completion 458 days from the date of commencement. Retainage shall be ten percent until fifty percent completion of construction and five percent shall be withheld thereafter.

2. The Construction Contract’s schedule of values represents General Contractor’s Fee (consisting of

general requirements, overhead, and profit) is within the maximum 14.00% of actual construction costs, calculated exclusive of insurance bonds, and FF&E.

3. A 5.00% hard cost contingency was utilized by AmeriNational and is supported by the plan and cost

review. 4. The General Contractor will secure a Payment and Performance Bond to secure the Construction

Contract and its cost is included within the Construction Contract’s schedule of values. 5. A Plan and Cost Review (“PCR”) was performed by GLE & Associates, Inc. (“GLE”). The total hard cost

budget of $16,663,089 or $125,286 per unit of the schedule of values is within an acceptable range as compared to similar projects. The costs associated with site work of $815,000 or $3.29 per square foot are appropriate for the scope of work. The costs associated with vertical construction of $13,280,001 or $135.89 per square foot are reasonable for the scope of work. GLE recommends a 5% hard cost contingency. The construction timeline of 458 days appears to be a reasonable duration for the Development provided no unforeseen circumstances occur.

Exhibit A Page 17 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐15 December 4, 2014

GENERAL DEVELOPMENT COSTS: Applicant CostsRevised

Applicant Costs

Underwriters

Total Costs ‐ CURCost Per Unit

HC Ineligible

Costs ‐ CUR

Accounting Fees $40,000 $40,000 $40,000 $301 $0

Appraisal $7,500 $7,500 $6,500 $49 $0

Architect's Fee ‐ Site/Building Design $525,000 $450,000 $379,500 $2,853 $0

Architect's Fee ‐ Supervision $75,000 $0 $37,950 $285 $0

Building Permits $162,500 $139,650 $139,650 $1,050 $0

Engineering Fees $60,000 $0 $0 $0 $0

Environmental Report $5,000 $10,000 $10,000 $75 $0

FHFC Administrative Fees $76,687 $77,718 $82,449 $620 $82,449

FHFC Application Fee $3,000 $3,000 $3,000 $23 $3,000

FHFC Credit Underwriting Fee $20,000 $20,000 $16,886 $127 $16,886

FHFC HC Compliance Fee (HC) $185,000 $135,000 $115,357 $867 $115,357

Lender Inspection Fees / Const Admin $48,000 $30,000 $64,114 $482 $0

Insurance $13,000 $13,300 $13,300 $100 $0

Market Study $7,500 $7,500 $4,000 $30 $0

Marketing and Advertising $28,137 $15,000 $15,000 $113 $15,000

Plan and Cost Review Analysis $15,000 $15,000 $7,500 $56 $0

Property Taxes $0 $34,775 $34,775 $261 $0

Soil Test $5,000 $0 $7,500 $56 $0

Survey $10,000 $10,000 $10,000 $75 $0

Tenant Relocation Costs $325,000 $246,000 $246,000 $1,850 $0

Title Insurance and Recording Fees $279,880 $236,463 $236,463 $1,778 $32,866

Util ity Connection Fees $50,000 $186,200 $159,600 $1,200 $0

Soft Cost Contingency $0 $164,041 $87,302 $656 $0

Other: Private Provider Inspections $0 $66,500 $66,500 $500 $0

Other: Green Building Consultant $0 $40,000 $40,000 $301 $0

Other: Zoning $0 $10,000 $10,000 $75 $0

$1,941,204 $1,957,647 $1,833,346 $13,785 $265,558Total General Development Costs: Notes to the General Development Costs: 1. AmeriNational reflects actual costs for the appraisal, market study, plan and cost review, FHFC

Application and Credit Underwriting Fees. FHFC HC Compliance Fee is based upon the 2014 FHFC Monitoring Fee Chart. FHFC Administrative Fee is based upon 8% of the annual HC recommendation.

2. Architectural Fees were reduced commensurate with the proposal executed by the Applicant with

10% allocated to Architectural Supervision. Engineering services will be provided by the Architect.

3. Lender Inspection/Construction Administration Fees represents estimated costs of construction loan servicing by AmeriNational and costs of construction consultants hired by the CITI, RJTCF, and AmeriNational.

4. The Development is new construction and a geotechnical report was prepared. AmeriNational

estimated the cost which will be verified at or prior to loan closing.

5. Though the Development is new construction, residents will be relocated from an existing, adjacent public housing development. As such, the Applicant will incur tenant relocation costs primarily attributed to moving its residents.

6. A contingency reserve of 5.00% of general development costs was utilized by AmeriNational.

Exhibit A Page 18 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐16 December 4, 2014

Applicant CostsRevised

Applicant Costs

Underwriters

Total Costs ‐ CURCost Per Unit

HC Ineligible

Costs ‐ CUR

Construction Loan Origination Fee $231,392 $160,000 $120,000 $902 $40,000

Construction Loan Interest $850,000 $450,000 $320,192 $2,407 $0

Permanent Loan Origination Fee $30,000 $30,000 $28,350 $213 $28,350

Local HFA Bond Application Fee $0 $0 $1,995 $15 $0

Local HFA Bond Underwriting Fee $0 $0 $14,049 $106 $14,049

Local HFA Bond Trustee Fee $25,000 $15,000 $15,000 $113 $15,000

Local HFA Bond Closing Costs $0 $63,990 $69,600 $523 $12,798

SAIL Commitment Fee $0 $0 $21,132 $159 $0

SAIL Closing Costs $0 $0 $15,000 $113 $0

Misc Loan Underwriting Fee $0 $0 $5,000 $38 $5,000

Reserves ‐ ACC Reserve $0 $176,362 $176,362 $1,326 $176,362

Reserves ‐ Operating Deficit $285,507 $286,817 $286,817 $2,157 $286,817

Reserves ‐ Required by Syndicator $0 $100,000 $100,000 $752 $0

Reserves ‐ Replacement Escrow $0 $39,900 $39,900 $300 $39,900

Financial Advisor Fee $45,000 $40,000 $37,500 $282 $37,500

Legal Fees ‐ Bond Counsel $0 $65,000 $55,000 $414 $16,250

Legal Fees ‐ Borrower's Counsel $122,000 $40,000 $40,000 $301 $40,000

Legal Fees ‐ Lender's Counsel $235,000 $296,000 $296,000 $2,226 $76,500

Other: Permanent Loan Conversion Fee $0 $0 $15,000 $113 $15,000

Other: Syndicator Due Diligence Fees $0 $50,000 $50,000 $376 $0

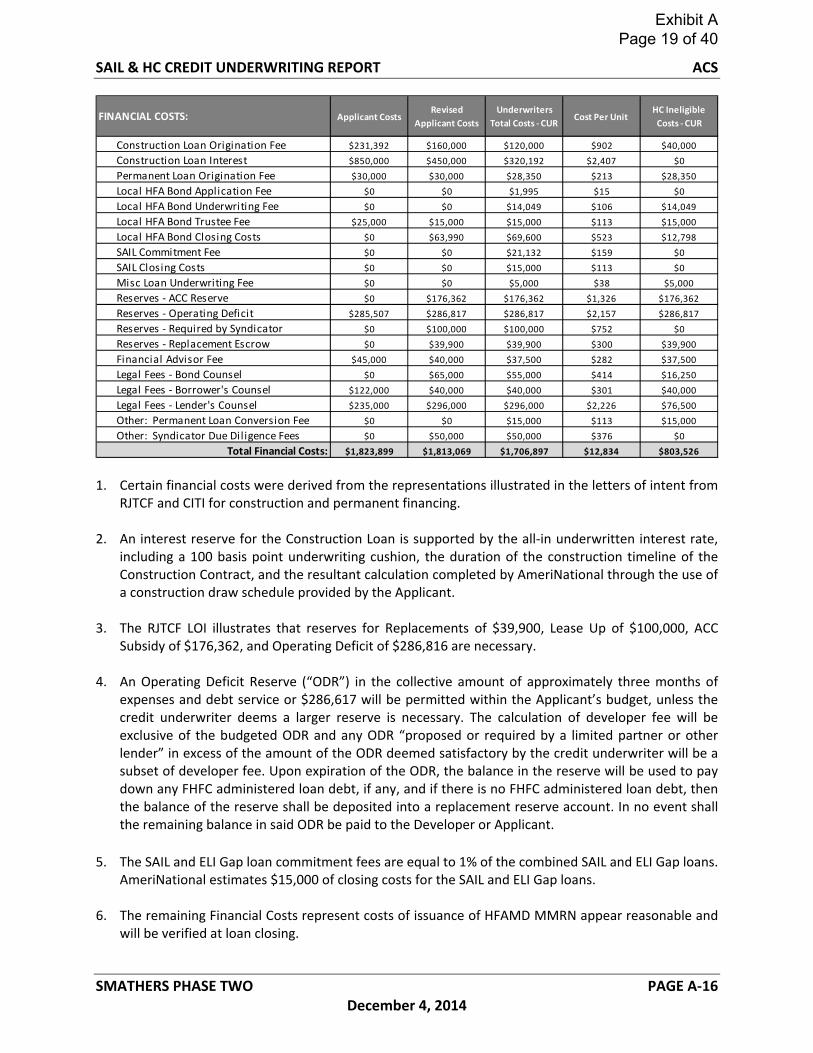

$1,823,899 $1,813,069 $1,706,897 $12,834 $803,526

FINANCIAL COSTS:

Total Financial Costs: 1. Certain financial costs were derived from the representations illustrated in the letters of intent from

RJTCF and CITI for construction and permanent financing.

2. An interest reserve for the Construction Loan is supported by the all‐in underwritten interest rate, including a 100 basis point underwriting cushion, the duration of the construction timeline of the Construction Contract, and the resultant calculation completed by AmeriNational through the use of a construction draw schedule provided by the Applicant.

3. The RJTCF LOI illustrates that reserves for Replacements of $39,900, Lease Up of $100,000, ACC Subsidy of $176,362, and Operating Deficit of $286,816 are necessary.

4. An Operating Deficit Reserve (“ODR”) in the collective amount of approximately three months of

expenses and debt service or $286,617 will be permitted within the Applicant’s budget, unless the credit underwriter deems a larger reserve is necessary. The calculation of developer fee will be exclusive of the budgeted ODR and any ODR “proposed or required by a limited partner or other lender” in excess of the amount of the ODR deemed satisfactory by the credit underwriter will be a subset of developer fee. Upon expiration of the ODR, the balance in the reserve will be used to pay down any FHFC administered loan debt, if any, and if there is no FHFC administered loan debt, then the balance of the reserve shall be deposited into a replacement reserve account. In no event shall the remaining balance in said ODR be paid to the Developer or Applicant.

5. The SAIL and ELI Gap loan commitment fees are equal to 1% of the combined SAIL and ELI Gap loans.

AmeriNational estimates $15,000 of closing costs for the SAIL and ELI Gap loans.

6. The remaining Financial Costs represent costs of issuance of HFAMD MMRN appear reasonable and will be verified at loan closing.

Exhibit A Page 19 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐17 December 4, 2014

Applicant CostsRevised

Applicant Costs

Underwriters

Total Costs ‐ CURCost Per Unit

HC Ineligible

Costs ‐ CUR

$20,824,725 $20,973,248 $20,998,778 $157,886 $1,489,389

Developer Fee $3,237,937 $3,253,661 $3,671,225 $27,603 $0

$3,237,937 $3,253,661 $3,671,225 $27,603 $0

OTHER DEVELOPMENT COSTS

Development Cost Before Developer Fee

and Land Costs

Total Other Development Costs: Notes to the Other Development Costs: 1. Developer Fee is within 18.00% of Total Development Costs before Land and exclusive of reserves as

permitted by the Rule.

Applicant CostsRevised

Applicant Costs

Underwriters

Total Costs ‐ CURCost Per Unit

HC Ineligible

Costs ‐ CUR

Land $0 $0 $0 $0 $0

Land Lease Payment $0 $0 $0 $0 $0

$0 $0 $0 $0 $0

$24,062,662 $24,226,909 $24,670,003 $185,489 $1,489,389

LAND ACQUISITION COSTS

Total Acquisition Costs:

TOTAL DEVELOPMENT COSTS: Notes to Land Acquisition Costs and Total Development Costs: 1. The Applicant provided an undated, draft Ground Lease between Miami‐Dade County (“Landlord”)

and Smathers Phase Two, LLC (“Tenant”) to lease the land of the Development for a 75‐year term at an annual rent payment of $1.00 per year. The Ground Lease does not reflect a capitalized lease payment; however, the tenant agrees to pay the Landlord additional rent in an amount equal to 50% of the available cash flow generated annually from the Development 120 days following the end of each fiscal year. “Available cash flow” is defined in the Ground Lease as revenue from the premises for the previous fiscal year, less all expenses of the premises for the same period, including but not limited to all payments (principal, interest, and reserves) on any debt and the payment of all developer fees. Receipt of a satisfactory, executed Ground Lease is a condition precedent to loan closing as outlined in Section B.

2. An Appraisal performed by Novogradac identifies an “as is” market value of the leasehold interest in

the land of $2,100,000. The lesser of the two values was therefore used for underwriting purposes.

3. Total Development Costs increased $607,341 since the Application due to increases in construction costs and developer fee.

Exhibit A Page 20 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐18 December 4, 2014

OPERATING PRO FORMA

FINANCIAL COSTS: Year 1Year 1

Per Unit

OPERATING PRO FORMA

Gross Potentia l Renta l Income $911,772 $6,855

Other Income $0

Miscel laneous $13,300 $100

Gross Potentia l Income $925,072 $6,955

Less :

Phys ica l Vac. Loss Percentage: 2.00% $18,501 $139

Col lection Loss Percentage: 1.00% $9,251 $70

Total Effective Gross Income $897,320 $6,747

Fixed:

Rea l Estate Taxes $34,457 $259

Insurance $93,100 $700

Variable:

Management Fee Percentage: 6.00% $53,839 $405

General and Adminis trative $63,175 $475

Payrol l Expenses $127,600 $959

Uti l i ties $109,725 $825

Marketing and Advertis ing $9,975 $75

Maintenance and Repairs/Pest Control $39,900 $300

Grounds Maintenance and Landscaping $39,900 $300

Reserve for Replacements $39,900 $300

Total Expenses $611,571 $4,598

Net Operating Income $285,749 $2,148

Debt Service Payments

Firs t Mortgage ‐ CITI $182,219 $1,370

Second Mortgage ‐ SAIL $11,382 $86

Third Mortgage ‐ ELI Gap $0 $0

Fourth Mortgage ‐ Surtax $26,586 $200

Fi fth Mortgage ‐ HOME $0 $0

Other Fees ‐ SAIL & ELI GAP PLS Fees $5,283 $40

Other Fees ‐ SAIL & ELI Gap CM Fees $1,742 $13

Total Debt Service Payments $227,211 $1,656

Cash Flow after Debt Service $58,537 $493

FINANCIAL COSTS: Annual Per Unit

Debt Service Coverage Ratios

DSC ‐ Firs t Mortgage 1.57 1.57

DSC ‐ Second Mortgage 1.48 1.48

DSC ‐ Third Mortgage 1.48 1.48

DSC ‐ Fourth Mortgage 1.30 1.30

DSC ‐ Fi fth Mortgage 1.30 1.30

DSC ‐ Al l Mortgages and Fees 1.26 1.26

Financial Ratios

Operating Expense Ratio 68.2%

Break‐even Economic Occupancy Ratio (a l l debt) 90.7%

INCO

ME:

EXPENSES:

Notes to the Operating Pro Forma and Ratios:

1. The Development will operate 82 of its 133 units as Public Housing units under an ACC with HUD in

which tenants pay rental rates based on 30% of their adjusted monthly income (the “30% ACC

Exhibit A Page 21 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐19 December 4, 2014

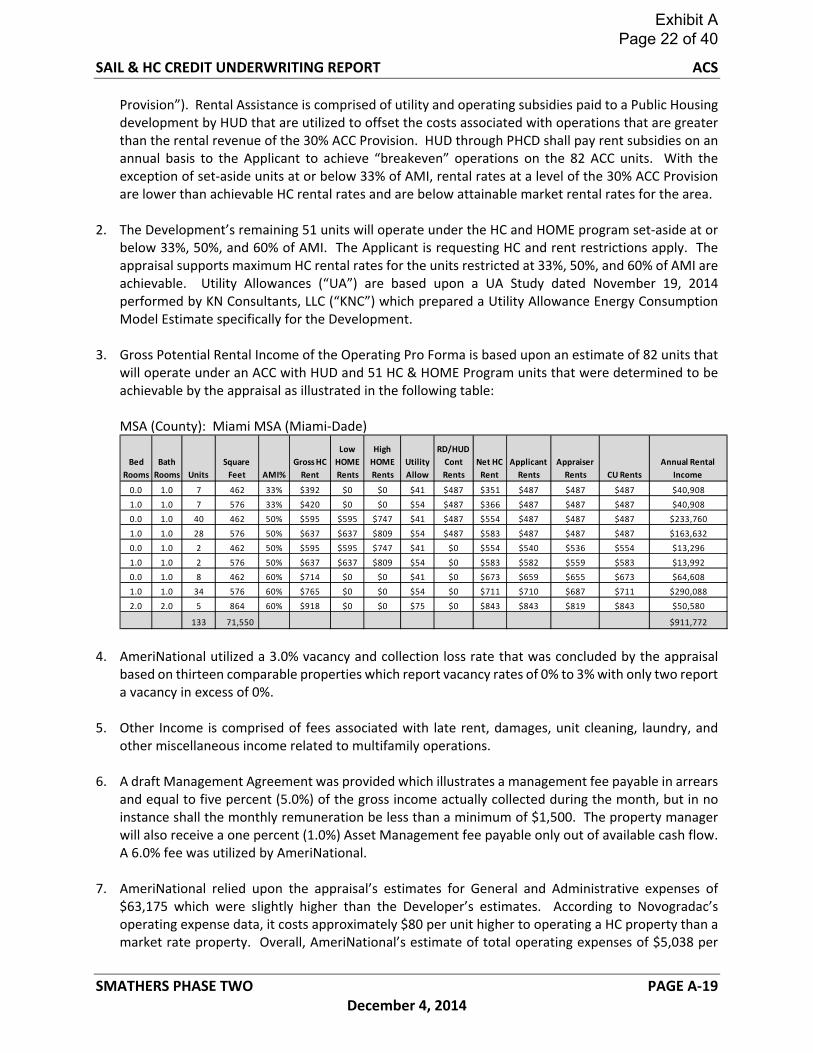

Provision”). Rental Assistance is comprised of utility and operating subsidies paid to a Public Housing development by HUD that are utilized to offset the costs associated with operations that are greater than the rental revenue of the 30% ACC Provision. HUD through PHCD shall pay rent subsidies on an annual basis to the Applicant to achieve “breakeven” operations on the 82 ACC units. With the exception of set‐aside units at or below 33% of AMI, rental rates at a level of the 30% ACC Provision are lower than achievable HC rental rates and are below attainable market rental rates for the area.

2. The Development’s remaining 51 units will operate under the HC and HOME program set‐aside at or below 33%, 50%, and 60% of AMI. The Applicant is requesting HC and rent restrictions apply. The appraisal supports maximum HC rental rates for the units restricted at 33%, 50%, and 60% of AMI are achievable. Utility Allowances (“UA”) are based upon a UA Study dated November 19, 2014 performed by KN Consultants, LLC (“KNC”) which prepared a Utility Allowance Energy Consumption Model Estimate specifically for the Development.

3. Gross Potential Rental Income of the Operating Pro Forma is based upon an estimate of 82 units that will operate under an ACC with HUD and 51 HC & HOME Program units that were determined to be achievable by the appraisal as illustrated in the following table:

MSA (County): Miami MSA (Miami‐Dade)

Gross HC

Rent

$487 $40,908$41 $487 $351 $487 $487

$0 $0

$0

Appraiser

Rents CU Rents

Annual Rental

Income

0.0 1.0 7 462 33% $392 $0

Low

HOME

Rents

High

HOME

Rents

Utility

Allow

RD/HUD

Cont

Rents

Net HC

Rent

Applicant

Rents

Bed

Rooms

Bath

Rooms Units

Square

Feet AMI%

$487 $554 $487 $487 $487 $233,760

$40,908

0.0 1.0 40 462 50% $595 $595 $747 $41

$54 $487 $366 $487 $487 $4871.0 1.0 7 576 33% $420

0.0 1.0 2 462 50% $595 $595

$637 $8091.0 1.0 28 576 50% $637

576 50% $637 $637 $809

$747

$487 $487 $163,632$54 $487 $583 $487

$554 $13,296$41 $0 $554 $540 $536

$13,992$54 $0 $583

$0 $673 $659 $655

$765

$843 $50,580

$673 $64,608

$290,088

$819

0.0 1.0 8 462 60% $714 $0 $0 $41

$582 $559 $5831.0 1.0 2

$0

$687 $711

2.0 2.0 5 864 60% $918 $0

$0 $0 $54 $0 $711 $7101.0 1.0 34 576 60%

$75 $0 $843 $843

133 71,550 $911,772

4. AmeriNational utilized a 3.0% vacancy and collection loss rate that was concluded by the appraisal

based on thirteen comparable properties which report vacancy rates of 0% to 3% with only two report a vacancy in excess of 0%.

5. Other Income is comprised of fees associated with late rent, damages, unit cleaning, laundry, and other miscellaneous income related to multifamily operations.

6. A draft Management Agreement was provided which illustrates a management fee payable in arrears

and equal to five percent (5.0%) of the gross income actually collected during the month, but in no instance shall the monthly remuneration be less than a minimum of $1,500. The property manager will also receive a one percent (1.0%) Asset Management fee payable only out of available cash flow. A 6.0% fee was utilized by AmeriNational.

7. AmeriNational relied upon the appraisal’s estimates for General and Administrative expenses of

$63,175 which were slightly higher than the Developer’s estimates. According to Novogradac’s operating expense data, it costs approximately $80 per unit higher to operating a HC property than a market rate property. Overall, AmeriNational’s estimate of total operating expenses of $5,038 per

Exhibit A Page 22 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE A‐20 December 4, 2014

unit per year is slightly above the Developer’s estimate of $4,694 and within the range of $4,429 to $5,790 of expense comparable properties surveyed by the appraiser.

8. The Development will offer trash removal, sewer, and cold water at no expense to the tenant with

the remaining utility expenses incurred by the tenants. Replacement Reserves of $300 per unit per year are required.

9. The FHFC SAIL loan shall be non‐amortizing and have an interest rate of 1% over the life of the loan.

The ELI GAP loan shall have a 0% interest rate. Other Fees includes annual Permanent Loan Servicing Fee on the SAIL loan and annual Compliance Monitoring Fees for Housing Credits, SAIL, and ELI Gap loans. Other Fees are subject to annual adjustments that shall not exceed 3% of the prior year’s fee.

10. Based upon an estimated Net Operating Income (“NOI”) of $285,749 for the Development’s initial

year of stabilized operations; the first mortgage loan can be supported by operations at a 1.57 Debt Service Coverage (“DSC”). The combined amount of the first mortgage and SAIL loan yields a 1.48 DSC in the initial year of operations in accordance with the Rule. The combined amount of all mortgages and fees yields a 1.26 DSC in the initial year of operations. The DSC requirements of the Rule and Surtax Program outlined in the Special Conditions of Section A have been satisfied.

11. A 15‐year Operating Pro Forma attached hereto as Exhibit 1 reflects rental income increasing at an annual rate of 2% and expenses increasing at an annual rate of 3%

Exhibit A Page 23 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

December 4, 2014

Section B

SAIL & ELI Gap Loan Special and General Loan Closing Conditions & HC Allocation Recommendation

and Contingencies

Exhibit A Page 24 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐1 December 4, 2014

Special Conditions

This recommendation is contingent upon the review and approval of the following items by Florida Housing and the Servicer, at least 30 days prior to real estate loan closing. Failure to submit and to receive approval of these items within this time frame may result in postponement of the loan closing date.

1. An Operating Deficit Reserve (“ODR”) in the collective amount of approximately three months of

expenses and debt service or $286,817 will be permitted within the Applicant’s budget, unless the credit underwriter deems a larger reserve is necessary. The calculation of developer fee will be exclusive of the budgeted ODR and any ODR “proposed or required by a limited partner or other lender” in excess of the amount of the ODR deemed satisfactory by the credit underwriter will be a subset of developer fee. Upon expiration of the ODR, the balance in the reserve will be used to pay down any FHFC administered loan debt, if any, and if there is no FHFC administered loan debt, then the balance of the reserve shall be deposited into a replacement reserve account. In no event shall the remaining balance in said ODR be paid to the Developer or Applicant.

2. Executed HUD evidentiary documentation that outlines ACC contracted rental assistance as outlined within this report.

3. Receipt of a satisfactory executed management plan, management agreement, and ground lease.

4. Receipt and satisfactory review of financial statements dated within 90 days loan closing that comply

with the Rule for RUDG, LLC and Jorge M. Perez.

5. A Proposal for Professional Services dated September 1, 2014 between the Applicant and the architect was provided. However, an executed AIA document of Standard Form of Agreement between Owner and Architect is required to the satisfactory of FHFC, its servicer, and GLE.

6. Receipt of any or all documentation necessary to confirm the Utility Allowance Energy Consumption

Model Estimate is acceptable to the satisfaction of Florida Housing and its servicer, if applicable.

General Conditions

This recommendation is contingent upon the review and approval of the following items by Florida Housing and the Servicer at least 30 days prior to real estate loan closing. Failure to submit and to receive approval of these items within this time frame may result in postponement of the closing date. 1. Borrower is to comply with any and all recommendations noted in the Plan and Cost Review prepared

by GLE.

2. Signed and sealed survey, dated within 90 days of closing, unless otherwise approved by Florida Housing, and its Legal Counsel, based upon the particular circumstances of the transaction. The Survey shall be certified to Florida Housing, and its Legal Counsel, as well as the title insurance company, and shall indicate the legal description, exact boundaries of the Development, easements, utilities, roads, and means of access to public streets, total acreage and flood hazard area and any other requirements of Florida Housing.

Exhibit A Page 25 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐2 December 4, 2014

3. Building permits and any other necessary approvals and permits (e.g., final site plan approval, water management district, Department of Environmental Protection, Army Corps of Engineers, Department of Transportation, etc.). An acceptable alternative to this requirement is receipt and satisfactory review of a letter from the local permitting and approval authority stating that the above referenced permits and approvals will be issued upon receipt of applicable fees (with no other conditions), or evidence of 100% lien‐free completion, if applicable. If a letter is provided, copies of all permits will be required as a condition of the first post‐closing draw.

4. Final sources and uses of funds itemized by source and line item, in a format and in amounts approved by the Servicer. A detailed calculation of the construction interest based on the final draw schedule (see below), documentation of the closing costs, and draft loan closing statement must also be provided. The sources and uses of funds schedule will be attached to the Loan Agreement as the approved development budget.

5. A final construction draw schedule showing itemized sources and uses of funds for each monthly draw. ELI Gap and SAIL loan proceeds shall be disbursed during the construction phase in an amount per Draw that does not exceed the individual ratios of the ELI Gap and SAIL loans, respectively, to the Total Development Cost, unless approved by the Credit Underwriter. The closing draw shall include appropriate backup and ACH wiring instructions.

6. During construction/rehabilitation, the developer is only allowed to draw a maximum of 50% of the total developer fee (developer fee minus acquisition developer fee) during construction/rehabilitation, but in no case more than the payable developer fee, which is determined to be “developer’s overhead”. No more than 35% of “developer’s overhead” during construction/rehabilitation will be allowed to be disbursed at closing. The remainder of the “developer’s overhead” will be disbursed during the construction/rehabilitation on a pro rata basis, based on the percentage of completion of the Development, as approved by FHFC and Servicer. The remaining unpaid developer fee shall be considered attributable to “developer’s profit” and may not be funded until the development has achieved 100% lien‐free completion and retainage has been released.

7. Evidence of general liability, flood (if applicable), builder’s risk and replacement cost hazard insurance (as certificates of occupancy are received) reflecting Florida Housing as Loss Payee/Mortgagee, with coverages, deductibles and amounts satisfactory to Florida Housing.

8. If the development is not 100% lien‐free completed, a 100% Payment and Performance Bond or a Letter of Credit (LOC) in an amount not less than 25% of the construction contract is required in order to secure the construction contract between the GC and the Borrower. In either case, Florida Housing must be listed as co‐obligee. The P&P bonds must be from a company rated at least “A‐“by A.M. Best & Co with a financial size category of at least FSC VI. FHFC, and/or Legal Counsel must approve the source, amount(s), and all terms of the P&P bonds, or LOC. If the LOC option is utilized, the LOC must include “evergreen” language and be in a form satisfactory to the Servicer, Florida Housing, and its Legal Counsel.

9. Architect, Construction Consultant, and Borrower certifications on forms provided by Florida Housing will be required for both design and as‐built with respect to Section 504 of the Rehabilitation Act, Americans with Disabilities Act, and the Federal Fair Housing Act requirements, as applicable.

10. A copy of the Amended and Restated Limited Partnership Agreement (“LPA”) or Operating Agreement (“OA”) reflecting purchase of the HC under terms consistent with the assumptions contained within this Credit Underwriting Report. The LPA or OA shall be in a form and of financial substance satisfactory to Servicer, Florida Housing, and its Legal Counsel.

Exhibit A Page 26 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐3 December 4, 2014

11. Satisfactory resolution of any outstanding past due or non‐compliance issues by closing of the loan(s).

12. Final “as permitted” (signed & sealed) site plans, building plans & specifications. The geotechnical report must be bound within the final plans & specifications.

13. Payment of any outstanding arrearages to the Corporation, its legal counsel, Servicer or any agent or assignee of the Corporation for past due issues applicable to the development team (Applicant or Developer or Principal, Affiliate or Financial Beneficiary, as described in 67‐21.0025(5) and 67‐48.0075(5) F.A.C., of an Applicant or a Developer).

This recommendation is contingent upon the review and approval by Florida Housing, and its Legal Counsel at least 30 days prior to real estate loan closing. Failure to receive approval of these items within this timeframe may result in postponement of the closing date.

1. Documentation of the legal formation and current authority to transact business in Florida for the Borrower, the general partner/principal(s)/manager(s) of the Applicant, the guarantors, and any limited partners of the Applicant.

2. Signed and sealed survey, dated within 90 days of closing, unless otherwise approved by Florida Housing, and its legal counsel, based upon the particular circumstances of the transaction. The Survey shall be certified to Florida Housing and its legal counsel, as well as the title insurance company, and shall indicate the legal description, exact boundaries of the Development, easements, utilities, roads, and means of access to public streets, total acreage and flood hazard area and any other requirements of Florida Housing.

3. An acceptable updated Environmental Audit Report, together with a reliance letter to Florida Housing, prepared within 90 days of Set‐Aside Gap and ELI Supplemental loan closings, unless otherwise approved by Florida Housing, and Legal Counsel, based upon the particular circumstances of the transaction. Borrower to comply with any and all recommendations noted in the Environmental Assessment(s) and Update and the Environmental Review, if applicable.

4. Title insurance pro‐forma or commitment for title insurance with copies of all Schedule B exceptions, in the amount of the ELI Gap and SAIL loan(s) naming Florida Housing as the insured. All endorsements required by Florida Housing shall be provided.

5. Florida Housing and its legal counsel shall review and approve all other lenders closing documents and the limited partnership or other applicable agreement. Florida Housing shall be satisfied in its sole discretion that all legal and program requirements for the Loans have been satisfied.

6. Evidence of general liability, flood (if applicable), builder’s risk, and replacement cost hazard insurance (as certificates of occupancy are received) reflecting Florida Housing as Loss Payee/Mortgagee, in coverage, deductibles and amounts satisfactory to Florida Housing.

7. Receipt of a legal opinion from the Borrower's Legal Counsel acceptable to Florida Housing addressing the following matters:

a. The legal existence and good standing of the Borrower and of any partnership or limited liability company that is the general partner of the Borrower (the "GP") and of any corporation or partnership that is the managing general partner of the GP, and of any corporate guarantor and any manager;

b. Authorization, execution, and delivery by the Borrower and the guarantors, of all Loan documents;

Exhibit A Page 27 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐4 December 4, 2014

c. The loan documents being in full force and effect and enforceable in accordance with their terms, subject to bankruptcy and equitable principles only;

d. The Borrower's and the guarantor's execution, delivery and performance of the loan documents shall not result in a violation of, or conflict with, any judgments, orders, contracts, mortgages, security agreements or leases to which the Borrower is a party or to which the Development is subject to the Borrower’s Partnership Agreement and;

e. Such other matters as Florida Housing or its legal counsel may require.

8. Evidence of compliance with local concurrency laws, if applicable.

9. UCC Searches for the Borrower, its partnerships, as requested by counsel.

10. Such other assignments, affidavits, certificates, financial statements, closing statements and other documents as may be reasonably requested by Florida Housing or its legal counsel in form and substance acceptable to Florida Housing or its legal counsel, in connection with the Loan(s).

11. Any other reasonable conditions established by Florida Housing and its Legal Counsel.

This recommendation is also contingent upon the following additional conditions:

1. Compliance with all provisions of Rule Chapters 67‐21, 67‐48, 67‐53, 67‐60 F.A.C., RFA 2014‐103, Section 42 of the I.R.C., and any other State and Federal requirements.

2. Acceptance by the Borrower and execution of all documents evidencing and securing the ELI Gap and SAIL loan(s) in form and substance satisfactory to Florida Housing, including, but not limited to, the Promissory Note(s), the Loan Agreement(s), the Mortgage and Security Agreement(s), and the Land Use Restriction Agreement(s).

3. All amounts necessary to complete construction or any phased pay‐in of amount necessary to complete construction shall be contingent upon an unconditional obligation, through a Joint Funding Agreement or other mechanism acceptable to Florida Housing, of the entity providing HC Equity payments (and evidence that 100% of such amount is on deposit with such entity at Loan Closing) to pay, regardless of any default under any documents relating to the HC as long as the First Mortgage continues to be funded.

4. If applicable, receipt and satisfactory review of financial statements from all guarantors dated within 90 days of real estate closing.

5. Guarantors to provide the standard Florida Housing Construction Completion Guaranty; to be released upon lien‐free completion as approved by the Servicer.

6. Guarantors are to provide the standard FHFC Operating Deficit Guaranty to be released upon achievement of an 1.15 Debt Service Coverage on the combined permanent first mortgage loan which is the ELI Gap loan & SAIL Loan as determined by FHFC or its agent, 90% occupancy, and 90% of the gross potential rental income, net of utility allowances, if applicable, for a period equal to twelve (12) consecutive months, all as certified by an independent Certified Public Accountant (“CPA”). Notwithstanding the above, the Operating Deficit Guarantee shall not terminate earlier than three years following the final certificate of occupancy.

7. Guarantors are to provide the standard Florida Housing Environmental Indemnity Guaranty.

8. Guarantors are to provide the standard Florida Housing Guaranty of Recourse Obligations.

9. A mortgagee title insurance policy naming Florida Housing as the insured in the amount of the ELI Gap and SAIL loan(s) is to be issued immediately after closing. Any exceptions to the title insurance policy

Exhibit A Page 28 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐5 December 4, 2014

must be acceptable to Florida Housing or its Legal Counsel. All endorsements that are required by Florida Housing are to be issued and the form of the title policy must be approved prior to closing.

10. Property tax and hazard insurance escrow are to be established and maintained by the First Mortgagee or the Servicer. In the event the reserve account is held by the Servicer, the release of funds shall be at Florida Housing’s sole discretion.

11. Replacement Reserves in the amount of $300 per unit per year will be required to be deposited on a monthly basis into a designated escrow account, to be maintained by the First Mortgagee or Florida Housing’s loan servicing agent. However, Applicant has the option to prepay Replacement Reserves. New construction developments shall not be allowed to draw during the first five (5) years or until the establishment of a minimum balance equal to the accumulation of five (5) years of replacement reserves per unit. The reserve shall be adjusted based on a capital needs assessment beginning no later than the 10th year after the first residential building receives a certificate of occupancy, a temporary certificate of occupancy, or is placed in service, whichever is earlier (“Initial Replacement Reserve Date”). A subsequent CNA is required no later than the 15th year after the Initial Replacement Reserve Date and subsequent assessments are required every five years thereafter.

12. Varian, or other construction inspector acceptable for Florida Housing, will act as Florida Housing’s inspector during the construction period.

13. A minimum of 10% retainage holdback on all construction draws until the Development is 50% complete, and 0% retainage thereafter is required. Retainage will not be released until successful completion of construction and issuance of all certificates of occupancy.

14. Satisfactory completion of a pre‐loan closing compliance audit conducted by Florida Housing or Servicer, if applicable.

15. Closing of all the funding sources prior to or simultaneously with the SAIL and ELI Gap loans.

16. Any other reasonable requirements of the Servicer, Florida Housing, or its Legal Counsel

Exhibit A Page 29 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO PAGE B‐6 December 4, 2014

Housing Credit Allocation Recommendation AmeriNational recommends an $1,024,583 annual Housing Credit allocation in the amount of the construction and permanent financing of Smathers Phase Two. Please refer to Exhibit 3 ‐ HC Allocation Calculation for further detail.

Contingencies The HC allocation recommendation is contingent upon the receipt and satisfactory review of the following items by AmeriNational and Florida Housing by the deadline established in the Preliminary HC Allocation. Failure to submit these items within this timeframe may result in forfeiture of the HC Allocation.

1. Closing of the ELI Gap and SAIL loans consistent with the assumptions of this credit underwriting

report.

2. GLE is to act as construction phase inspector for Florida Housing.

3. Purchase of the HC by the Syndicator or its assigns under the terms consistent with the assumptions of this report.

4. Receipt of executed FHFC Fair Housing, Section 504 and ADA as‐built certification forms 122, 127, and 129.

5. Satisfactory resolution of any outstanding past due items or non‐compliance issues .

6. Any other reasonable requirements of AmeriNational or Florida Housing.

Exhibit A Page 30 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO EXHIBIT 1, PAGE 1 December 4, 2014

Exhibit 1 Smathers Phase Two

15 Year Operating Pro Forma FINANCIAL COSTS: Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Year 11 Year 12 Year 13 Year 14 Year 15OPERATING PRO FORMA

Gross Potentia l Rental Income $911,772 $930,007 $948,608 $967,580 $986,931 $1,006,670 $1,026,803 $1,047,339 $1,068,286 $1,089,652 $1,111,445 $1,133,674 $1,156,347 $1,179,474 $1,203,064

Other Income

Anci l lary Income $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Miscel laneous $13,300 $13,566 $13,837 $14,114 $14,396 $14,684 $14,978 $15,278 $15,583 $15,895 $16,213 $16,537 $16,868 $17,205 $17,549

Gross Potentia l Income $925,072 $943,573 $962,445 $981,694 $1,001,328 $1,021,354 $1,041,781 $1,062,617 $1,083,869 $1,105,547 $1,127,658 $1,150,211 $1,173,215 $1,196,679 $1,220,613

Less :

Phys ica l Vac. Loss Percentage: 2.00% $18,501 $18,871 $19,249 $19,634 $20,027 $20,427 $20,836 $21,252 $21,677 $22,111 $22,553 $23,004 $23,464 $23,934 $24,412

Col lection Loss Percentage: 1.00% $9,251 $9,436 $9,624 $9,817 $10,013 $10,214 $10,418 $10,626 $10,839 $11,055 $11,277 $11,502 $11,732 $11,967 $12,206

Total Effective Gross Income $897,320 $915,266 $933,572 $952,243 $971,288 $990,714 $1,010,528 $1,030,738 $1,051,353 $1,072,380 $1,093,828 $1,115,704 $1,138,019 $1,160,779 $1,183,994

Fixed:

Real Estate Taxes $34,457 $35,491 $36,555 $37,652 $38,782 $39,945 $41,143 $42,378 $43,649 $44,959 $46,307 $47,697 $49,127 $50,601 $52,119

Insurance $93,100 $95,893 $98,770 $101,733 $104,785 $107,928 $111,166 $114,501 $117,936 $121,474 $125,119 $128,872 $132,738 $136,720 $140,822

Variable:

Management Fee Percentage: 6.00% $53,839 $54,916 $56,014 $57,135 $58,277 $59,443 $60,632 $61,844 $63,081 $64,343 $65,630 $66,942 $68,281 $69,647 $71,040

General and Administrative $63,175 $65,070 $67,022 $69,033 $71,104 $73,237 $75,434 $77,697 $80,028 $82,429 $84,902 $87,449 $90,072 $92,775 $95,558

Payrol l Expenses $127,600 $131,428 $135,371 $139,432 $143,615 $147,923 $152,361 $156,932 $161,640 $166,489 $171,484 $176,628 $181,927 $187,385 $193,006

Uti l i ties $109,725 $113,017 $116,407 $119,899 $123,496 $127,201 $131,017 $134,948 $138,996 $143,166 $147,461 $151,885 $156,442 $161,135 $165,969

Marketing and Advertis ing $9,975 $10,274 $10,582 $10,900 $11,227 $11,564 $11,911 $12,268 $12,636 $13,015 $13,406 $13,808 $14,222 $14,649 $15,088

Maintenance and Repa irs/Pest Control $39,900 $41,097 $42,330 $43,600 $44,908 $46,255 $47,643 $49,072 $50,544 $52,060 $53,622 $55,231 $56,888 $58,594 $60,352

Grounds Maintenance and Landscaping $39,900 $41,097 $42,330 $43,600 $44,908 $46,255 $47,643 $49,072 $50,544 $52,060 $53,622 $55,231 $56,888 $58,594 $60,352

Reserve for Replacements $39,900 $39,900 $39,900 $39,900 $39,900 $39,900 $39,900 $39,900 $39,900 $39,900 $41,097 $42,330 $43,600 $44,908 $46,255

Total Expenses $611,571 $628,183 $645,282 $662,884 $681,002 $699,652 $718,850 $738,612 $758,955 $779,896 $802,650 $826,073 $850,186 $875,008 $900,562

Net Operating Income $285,749 $287,083 $288,289 $289,359 $290,286 $291,062 $291,678 $292,126 $292,398 $292,484 $291,178 $289,632 $287,833 $285,771 $283,432

Debt Service Payments

Firs t Mortgage ‐ CITI $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219 $182,219

Second Mortgage ‐ SAIL $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382 $11,382

Third Mortgage ‐ ELI Gap $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Fourth Mortgage ‐ Surtax $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586 $26,586

Fi fth Mortgage ‐ HOME $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Al l Other Mortgages ‐ $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

$5,283 $5,245 $5,403 $5,565 $5,732 $5,904 $6,081 $6,263 $6,451 $6,645 $6,844 $7,049 $7,261 $7,479 $7,703

Other Fees ‐ SAIL & ELI Gap CM Fees $1,742 $1,794 $1,848 $1,904 $1,961 $2,019 $2,080 $2,142 $2,207 $2,273 $2,341 $2,411 $2,484 $2,558 $2,635

Tota l Debt Service Payments $227,211 $227,226 $227,437 $227,655 $227,879 $228,110 $228,347 $228,592 $228,844 $229,104 $229,372 $229,647 $229,931 $230,223 $230,524

Cash Flow after Debt Service $58,537 $59,857 $60,852 $61,705 $62,407 $62,952 $63,330 $63,534 $63,554 $63,380 $61,807 $59,984 $57,902 $55,547 $52,908

FINANCIAL COSTS: Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual AnnualDebt Service Coverage Ratios

DSC ‐ Firs t Mortgage 1.57 1.58 1.58 1.59 1.59 1.60 1.60 1.60 1.60 1.61 1.60 1.59 1.58 1.57 1.56

DSC ‐ Second Mortgage 1.48 1.48 1.49 1.49 1.50 1.50 1.51 1.51 1.51 1.51 1.50 1.50 1.49 1.48 1.46

DSC ‐ Third Mortgage 1.48 1.48 1.49 1.49 1.50 1.50 1.51 1.51 1.51 1.51 1.50 1.50 1.49 1.48 1.46

DSC ‐ Fourth Mortgage 1.30 1.30 1.31 1.31 1.32 1.32 1.32 1.33 1.33 1.33 1.32 1.32 1.31 1.30 1.29

DSC ‐ Fi fth Mortgage 1.30 1.30 1.31 1.31 1.32 1.32 1.32 1.33 1.33 1.33 1.32 1.32 1.31 1.30 1.29

DSC ‐ Al l Mortgages and Fees 1.26 1.26 1.27 1.27 1.27 1.28 1.28 1.28 1.28 1.28 1.27 1.26 1.25 1.24 1.23

Financial Ratios

Operating Expense Ratio 68.2% 68.6% 69.1% 69.6% 70.1% 70.6% 71.1% 71.7% 72.2% 72.7% 73.4% 74.0% 74.7% 75.4% 76.1%

Break‐even Economic Occupancy Ratio (a l l debt) 90.7% 90.7% 90.7% 90.7% 90.8% 90.8% 90.9% 91.0% 91.1% 91.3% 91.5% 91.8% 92.1% 92.4% 92.7%

INCOME:

EXPENSES:

Other Fees ‐ SAIL & ELI GAP PLS Fees

Exhibit A Page 31 of 40

SAIL & HC CREDIT UNDERWRITING REPORT ACS

SMATHERS PHASE TWO EXHIBIT 2, PAGE 1 December 4, 2014

Smathers Phase Two RFA 2014‐103 (2014‐306S) / 2013‐526C Description of Features and Amenities

A. The Development will consist of:

133 units located in 1 Mid‐Rise residential building w/elevator. Unit Mix: Fifty‐seven (57) Studio units;

Seventy‐one (71) one bedroom/one bath units; and Five (5) two bedroom/two bath units;

133 Total Units B. The Development must meet all requirements of local, state & federal laws, rules, regulations,

ordinances, orders and codes, Federal Fair Housing Act as implemented by 24 CFR 100, the 2012 Florida Accessibility Code for Building Construction as adopted pursuant to Section 553.503, F.S., Section 504 of the Rehabilitation Act of 1973, and Titles II and III of the Americans with Disabilities Act (“ADA”) of 1990 as implemented by 28 CFR 35, incorporating the most recent amendments, regulations, and rules, as applicable.

C. The Development must provide the following General features:

1. Termite prevention;