Embed Size (px)

Citation preview

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

ForeInvestors ChoiceSM

Variable Annuity with Lifetime Spending AccountSM Option

VA5210 (11-15) 102558FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

NAIC Training

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

ForeInvestors Choice variable annuity

Variable annuities are long-term investments intended for retirement purposes that offer tax-deferral,

professionally managed investment options and flexible payouts. Values will fluctuate with investment

performance, and the annuity may gain or lose value. Charges and fees will also reduce its value.

Optional benefits are not available for purchase outside of a variable annuity and may be elected at an

additional cost. A standard death benefit is included in the base product. Suitability and willingness to

purchase the variable annuity must be considered prior to the potential benefits of any optional features.

Taxable distributions (including certain deemed distributions) are subject to ordinary income taxes, and if

made prior to age 59½, may also be subject to a 10% federal income tax penalty.

2

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 3

ForeInvestors Choice:At a glance

Product Feature ForeInvestors Choice B-Share ForeInvestors Choice C-Share

Contract Fees 1.00% ME&A 1.15% ME&A

Maximum Issue Age 85

Minimum Initial Premium $25,000

CDSC 5-year ( 9 / 8 / 7 / 6 / 5 ) N/A

Annual Maintenance Fee $50 (waived if contract value > $50,000)

Fund Options 94 investment options, including asset allocation funds and alternative investment options

Fixed OptionsFixed Account, DCA-plus,1 and 3-year and 5-year multi-

year guaranteed accounts N/A

Death Benefit Standard death benefit is 100% contract value (Not Return Of Premium)

Optional Death BenefitAvailable for 0.25%.

If contract has positive earnings, the Earnings Protection Benefit pays in excess of contract value to help cover taxes. If contract has negative earnings, it reverts to standard death benefit.

Optional Income BenefitAvailable for 0.50%.

The Lifetime Spending Account option is a variable lifetime withdrawal benefit (VLWB) that efficiently manages asset drawdown to provide a stream of variable income for life.

Additional Benefits2 Nursing Home Waiver and Terminal Illness Waiver N/A

Surrender Charge-Free Partial Withdrawals

Greater of 5% of premiums subject to CDSC or earnings 100% of contract value

1Because Dollar Cost Averaging (DCA) involves continuous investing regardless of fluctuating price levels, your clients should carefully consider their financial ability to continue investing through periods of fluctuating prices. Continuous or periodic investment plans neither assure a profit nor protect against loss in declining markets.2Subject to state availability. All guarantees assume compliance with the benefit rules and are based on the claims-paying ability of Forethought Life Insurance Company.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

ForeInvestors Choice is an innovative variable annuity product that provides retirees with strategies to help address their needs in retirement:

1. Invest for growth: For investors seeking to invest for growth with tax-deferral.

– Tax-deferred investment growth potential through open-architecture investing.

2. Transfer a legacy: For investors concerned with estate planning and tax liability.

– Earnings Protection Benefit (EPB)1 optional death benefit grosses up contract value payable at death by 35% of contract growth to help cover tax liability.

3. Manage income: A new option for investors considering or currently taking income from non-guaranteed sources.

– Lifetime Spending Account1 optional benefit is designed to provide lifetime income protection that automatically calibrates withdrawals to performance to help avoid asset depletion while maximizing income received.

– If investors determine they need income after the contract is issued, the Lifetime Spending Account optional benefit can be added post-issue (provided the benefit is still available for sale).

4

ForeInvestors Choice: A new product to help address critical client needs

1

2

3

1Optional benefit available at an additional costAll guarantees assume compliance with the benefit rules and are based on the claims-paying ability of Forethought Life Insurance Company.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 5

Invest for growthForeInvestors Choice

1

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

Invest for growth:Broad portfolio; diverse sectors, investments objectives

For investors looking for investment flexibility and tax-deferral, ForeInvestors Choice offers:

94 underlying funds

15 fund families

11 asset allocation investment options

10 managed risk investment options

Nine alternative investment options

Six index investment options

Four fixed crediting options (B-Share only), including multi-year guaranteed accounts in three-year or five-year terms

6

1

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 7

Invest for growth:A diverse selection of money managers1

(See the full list of investment options at end of presentation)

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 8

Fixed Account – One-year Fixed Account at a set rate ― rates determined annually at our discretion. – Each contract year, you may transfer the greater of 30% of the contract value in the Fixed Account as of the last

contract anniversary (adjusted for premium payments and transfers) or an amount equal to the largest previous transfer from the Fixed Account.

– Transfer into the Fixed Account can occur at any time except during any six-month period following a transfer out of the Fixed Account.

Multi-year guaranteed account investment options.‒ Rates guaranteed for three- and five-year terms. ‒ Allocations to multi-year guaranteed account options will be limited to 40% of premium/contract value. ‒ Transfers cannot be made from the multi-year guaranteed account during the Guaranteed Period.

DCA-Plus– Enhanced crediting rate for dollar-cost-averaging (DCA) of premium into sub-accounts. – Available in six-month or 12-month intervals.– DCA not available into Fixed Account or multi-year guaranteed account options.

Because Dollar Cost Averaging (DCA) involves continuous investing regardless of fluctuating price levels, your clients should carefully consider their financial ability to continue investing through periods of fluctuating prices. Continuous or periodic investment plans neither assure a profit nor protect against loss in declining markets.

1Invest for growth:Fixed crediting options (available for B-Share only)

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 9

Transfer a LegacyForeInvestors Choice

2

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

Optional death benefit offered for a cost of 0.25%.

Grosses up contract value payable at death by 35% of contract growth to help cover tax liability.

– At death, the Earnings Protection Benefit only provides a benefit if there is positive contract growth, otherwise it reverts to the standard death benefit of 100% contract value (not return of premium). In other words, if there is no gain, the Earnings Protection Benefit provides no benefit.

– If elected at issue, Cumulative Adjusted Premium equals the premium; if elected post-issue Cumulative Adjusted Premium equals contract value at the time of the election.

– Only withdrawals that are in excess of contract growth reduce the Cumulative Adjusted Premium by the amount of the withdrawal that exceeds the contract growth.

– Contract Growth = Contract Value – Cumulative Adjusted Premium.

10

Transfer a legacy: Optional Earnings Protection Benefit (EPB)2

Some annuity products offer tax-deferral but lack tax-sensitivity for transfer to the next generation. ForeInvestors Choice can help meet this need with the optional Earnings Protection Benefit.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 11

Transfer a legacy: Above and beyond contract value2

ForeInvestors Choice with Optional Earnings Protection Benefit1

Current Premium

Contract Value at Death

Contract Growth

Earnings Protection Benefit (35% of Gains)

Total Death Benefit

$100,000 $112,000 $12,000 $4,200 $116,200

1Optional benefit available at an additional costAssumes 6.08% average annual return over two years, which is net of fund expenses; mortality, expense and administration costs and the 0.25% EPB charge. This hypothetical example is for illustrative purposes only. There is no guarantee of future performance. Assumes an initial investment of $100,000 with no additions and no withdrawals.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

The Earnings Protection Benefit optional death benefit guarantees that your beneficiaries will receive the greater of:

– The contract value, or

– Earnings Protection Death Benefit Value, which is contract value plus contract growth multiplied by 35%.

If there is no or negative growth, the Earnings Protection Benefit provides no benefit and the standard death benefit will apply.

The benefit terminates upon annuitization, typically at age 95, unless you annuitize sooner.

The Earnings Protection Benefit is offered at an additional charge of 0.25%. The charge is (1) based on the benefit value; (2) assessed quarterly and deducted from the sub-accounts.

– The client may revoke the rider upon an increase in the rider charge, however the rider cannot be re-elected. Guaranteed maximum cost is 0.50%.

Cumulative Adjusted Premium is increased for subsequent premiums.

Annuity death benefit may be subject to ordinary income tax.

Ownership changes may result in termination of the benefit.

The contract value utilized to determine your death benefit is the contract value upon receipt of due proof of death.

The Earnings Protection Benefit is available through age 80 and subject to a maximum payout at death equal to $1 million plus the contract value upon receipt of proof of death.

Only withdrawals that are in excess of contract growth reduce the Cumulative Adjusted Premium by the amount of the withdrawal that exceeds the contract growth.

12

Earnings Protection Benefit optional death benefit:Additional considerations 2

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 13

Manage incomeForeInvestors Choice

3

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 14

Annuities with Guaranteed Lifetime Withdrawal Benefits (GLWB) provide strong income guarantees and manage longevity and withdrawal risk for an associated cost, but may limit:

L̶ Investment/crediting flexibility and choice.L̶ Opportunity to keep pace with inflation in retirement.

Non-guaranteed income sources (i.e. systematic withdrawals1) offer investment flexibility, growth potential and the opportunity to keep pace with inflation but are subject to:

– Longevity risk L investor risks outliving income.– Withdrawal risk L advisor may not know how to adjust withdrawals over time based on

performance and may over- or underestimate withdrawal amounts.

13Manage income:Today’s income trade-offs

1Taxable distributions (including certain deemed distributions) are subject to ordinary income taxes, and if made prior to age 59 1/2, may also be subject to a 10% federal income tax penalty. Distributions received from a non-qualified contract before the Annuity Commencement Date are taxable to the extent of the income on the contract. Payments from IRAs are taxable in accordance with the normal rules surrounding taxation of payments from an IRA. Early surrender charges may also apply. Withdrawals will reduce the death benefit and any optional guaranteed amounts in an amount more than the actual withdrawal.All guarantees assume compliance with the benefit rules and are based on the claims-paying ability of Forethought Life Insurance Company.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

The Lifetime Spending Account is an optional variable lifetime1 withdrawal benefit that provides a guarantee of lifetime income (versus a guarantee of an amount of lifetime income), a Deferral Bonus and a smoothing feature to help manage income volatility once the client is taking withdrawals.

Optional benefit available for an additional cost of 0.50%.

The client’s income stream and Deferral Bonus will be variable. The Withdrawal Base and Deferral Bonus Base both fluctuate daily (up and down) based on investment performance compared to a 4% annual return target, or Assumed Investment Rate (AIR). This means that exceeding 4% annually will lead to an increase in benefit bases, not meeting 4% annually will result in a decrease in benefit bases and hitting exactly 4% results in no change to benefit bases.

The amount of a client’s Lifetime Annual Payments may be reduced significantly if they experience investment losses prior to beginning Lifetime Annual Payments.

Once the contract reaches the Minimum Contract Value (<$2,500) after age 59 ½, the Withdrawal Base will continue to provide for lifetime withdrawals and be adjusted based on the performance of the underlying investments.

15

Manage income:How the optional Lifetime Spending Account works3

1Assumes compliance with benefit rules.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

Before taking income, ForeInvestors Choice with the Lifetime Spending Account offers:

Open-architecture investing with more than 94 investment options

6% Deferral Bonus– Credited annually to the Withdrawal Base at the end of the contract year until first withdrawal– Based on Deferral Bonus Base upon anniversary, which fluctuates based on investment performance– No cap on number of years income can be deferred, up to Annuity Commencement Date (max age 95)

A variable Withdrawal Base that fluctuates daily up and down based on investment performance– Prior to starting income, the Withdrawal Base is calculated by first adjusting for performance relative to

the 4% Assumed Investment Rate and then adding the Deferral Bonus on anniversaries.

16

Manage income:Lifetime Spending Account in action L before taking income3

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 17

13Manage income:Lifetime Spending Account in action L before taking income

Let’s take a look at how investment performance relative to the 4% Assumed Investment Rate (AIR) affects benefit bases:

Year 1: Annual Net Return is 4%, which means the 4% AIR target was met but not exceeded, so there’s no adjustment to benefit bases from investment performance. Therefore, the Withdrawal Base will only increase by the addition of the Deferral Bonus.

Year 2: Annual Net Return was 14% and exceeds the 4% AIR, which drives an increase in the benefit bases. The Withdrawal Base increases due to investment performance and the addition of the Deferral Bonus.

Year 4: Even though there’s positive Annual Net Return of 2%, the Deferral Bonus Base decreases due to missing the 4% AIR. However, the Withdrawal Base increases due to the addition of the Deferral Bonus.

1Net of operating expenses and ME&A fees; 6.92% average annual net return for years 1-5 This hypothetical example is for illustrative purposes only. There is no guarantee of future performance. Assumes an initial investment of $100,000 with no additions and no excess withdrawals. Contract value is additionally reduced by the Lifetime Spending Account optional benefit charge of 0.50%.

ForeInvestors Choice with Lifetime Spending Account

Annual Net Return1

Deferral Bonus Base

Deferral Bonus Withdrawal Base Contract ValueYear

0 $100,000.00 $100,000.00 $100,000.00

1 4.00% $100,000.00 $6,000.00 $106,000.00 $103,480.00

2 14.00% $109,615.38 $6,576.92 $122,769.23 $117,377.36

3 8.00% $113,831.36 $6,829.88 $134,321.01 $126,133.72

4 2.00% $111,642.30 $6,698.54 $138,436.45 $128,013.11

5 7.00% $114,862.75 $6,891.76 $149,321.57 $136,289.16

Benefit base adjustments

All values are as of the end of the year and may be subject to rounding.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

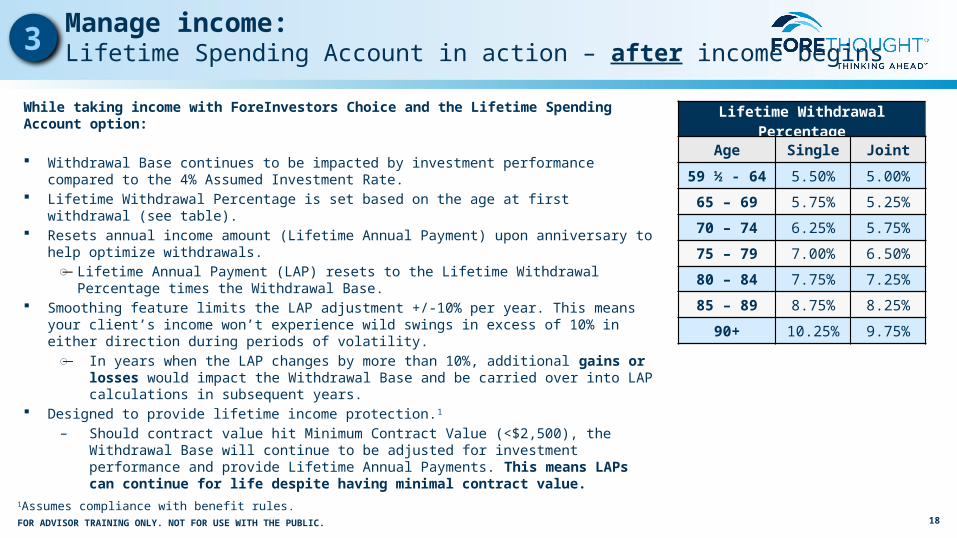

While taking income with ForeInvestors Choice and the Lifetime Spending Account option:

Withdrawal Base continues to be impacted by investment performance compared to the 4% Assumed Investment Rate.

Lifetime Withdrawal Percentage is set based on the age at first withdrawal (see table). Resets annual income amount (Lifetime Annual Payment) upon anniversary to help optimize

withdrawals. L̶ Lifetime Annual Payment (LAP) resets to the Lifetime Withdrawal Percentage times the

Withdrawal Base. Smoothing feature limits the LAP adjustment +/-10% per year. This means your client’s income

won’t experience wild swings in excess of 10% in either direction during periods of volatility.L̶ In years when the LAP changes by more than 10%, additional gains or losses would impact

the Withdrawal Base and be carried over into LAP calculations in subsequent years. Designed to provide lifetime income protection.1

– Should contract value hit Minimum Contract Value (<$2,500), the Withdrawal Base will continue to be adjusted for investment performance and provide Lifetime Annual Payments. This means LAPs can continue for life despite having minimal contract value.

18

Manage income:Lifetime Spending Account in action – after income begins3

Lifetime Withdrawal Percentage

Age Single Joint

59 ½ - 64 5.50% 5.00%

65 – 69 5.75% 5.25%

70 – 74 6.25% 5.75%

75 – 79 7.00% 6.50%

80 – 84 7.75% 7.25%

85 – 89 8.75% 8.25%

90+ 10.25% 9.75%

1Assumes compliance with benefit rules.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 19

13Manage income:Lifetime Spending Account in action – after income begins

1Net of operating expenses and ME&A fees; 5.52% average annual net return for years 5-14.This hypothetical example is for illustrative purposes only. There is no guarantee of future performance. Assumes an initial investment of $100,000 with no additions and no excess withdrawals. All values are as of the end of the year except withdrawals which occur at the beginning of the year and may be subject to rounding. Withdrawals assume a 6.25% Lifetime Withdrawal Percentage. Contract value is additionally reduced by the Lifetime Spending Account optional benefit charge of 0.50%.

Now, let’s focus on Lifetime Annual Payments (LAPs) and the role the smoothing feature plays:

• Year 7: annual net return was 10%, which surpassed the 4% Assumed Investment Rate, so the Withdrawal Base and LAP increased.

• Year 9: The -22% annual net return fully impacts the Withdrawal Base, however, the LAP change is floored at -10% due to the smoothing feature.

• Year 10: The impact on LAP continues due to the prior year’s Withdrawal Base decrease, which is why the LAP decreases despite the +13% annual net return.

• Year 13: The 25% annual net return fully impacts the Withdrawal Base, however, LAP change is capped at +10% due to the smoothing feature.

• Year 14: Again, The impact on LAP continues due to the prior year’s Withdrawal Base increase, which is why the LAP increases despite the -2% annual net return.

ForeInvestors Choice with Lifetime Spending Account

Year AgeAnnual Net

Return1Withdrawal

BaseLifetime Annual Payment (LAP) Withdrawal Contract Value

5 69 7.00% $149,321.57 $9,332.60 $0.00 $136,289.16

6 70 6.50% $152,911.03 $9,556.94 $9,332.60 $134,532.69

7 71 10.00% $161,732.82 $10,108.30 $9,556.94 $136,785.96

8 72 12.00% $174,173.81 $10,885.86 $10,108.30 $141,169.58

9 73 -22.00% $130,630.36 $9,797.28 $10,885.86 $101,113.19

10 74 13.00% $141,934.91 $8,870.93 $9,797.28 $102,671.05

11 75 5.00% $143,299.67 $8,956.23 $8,870.93 $97,997.67

12 76 7.50% $148,122.25 $9,257.64 $8,956.23 $95,240.96

13 77 25.00% $178,031.55 $10,183.40 $9,257.64 $106,941.75

14 78 -2.00% $167,760.50 $10,485.03 $10,183.40 $94,349.06

Lifetime Annual Payments and smoothing feature

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 20

13Manage income:Lifetime Spending Account in action – after income begins

*All guarantees assume compliance with benefit rules1Net of operating expenses and ME&A fees; 4.24% average annual net return for years 23-27.This hypothetical example is for illustrative purposes only. There is no guarantee of future performance. Assumes an initial investment of $100,000 with no additions and no excess withdrawals. All values are as of the end of the year except withdrawals which occur at the beginning of the year and may be subject to rounding. Withdrawals assume a 6.25% Lifetime Withdrawal Percentage. Contract value is additionally reduced by the Lifetime Spending Account optional benefit charge of 0.50%. 2Withdrawals causing contract value to fall below $2,500 will be processed such that a nominal amount of contract value remains to measure investment performance.

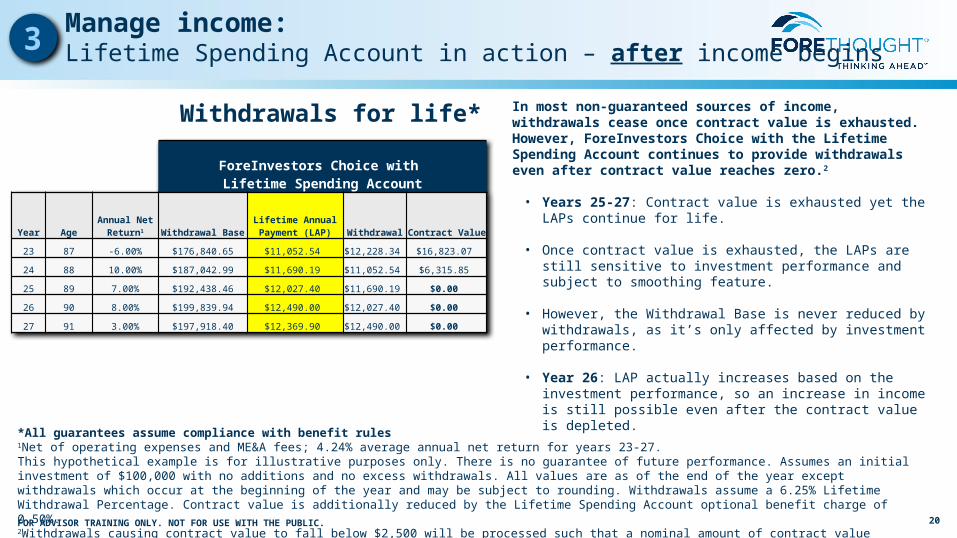

In most non-guaranteed sources of income, withdrawals cease once contract value is exhausted. However, ForeInvestors Choice with the Lifetime Spending Account continues to provide withdrawals even after contract value reaches zero.2

• Years 25-27: Contract value is exhausted yet the LAPs continue for life.

• Once contract value is exhausted, the LAPs are still sensitive to investment performance and subject to smoothing feature.

• However, the Withdrawal Base is never reduced by withdrawals, as it’s only affected by investment performance.

• Year 26: LAP actually increases based on the investment performance, so an increase in income is still possible even after the contract value is depleted.

ForeInvestors Choice with Lifetime Spending Account

Year AgeAnnual Net

Return1 Withdrawal BaseLifetime Annual Payment (LAP) Withdrawal Contract Value

23 87 -6.00% $176,840.65 $11,052.54 $12,228.34 $16,823.07

24 88 10.00% $187,042.99 $11,690.19 $11,052.54 $6,315.85

25 89 7.00% $192,438.46 $12,027.40 $11,690.19 $0.00

26 90 8.00% $199,839.94 $12,490.00 $12,027.40 $0.00

27 91 3.00% $197,918.40 $12,369.90 $12,490.00 $0.00

Withdrawals for life*

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

Lifetime Spending Account option is offered at an additional charge of 0.50%. The charge is (1) based on contract value; (2) assessed quarterly and deducted from the sub-accounts.

– The charge may change upon any contract anniversary. If a fee change is declined, the withdrawal percentage will be decreased by 1% (ex.: 5% to 4%). Guaranteed maximum cost is 1.00%.

Withdrawal Base is a conceptual value used solely for calculating withdrawals under the Lifetime Spending Account, known as Lifetime Annual Payments (LAP). The Withdrawal Base may not be surrendered and has no cash value.

If elected at issue, the initial Withdrawal Base equals premium; if elected post-issue the initial Withdrawal Base equals the contract value at the time of the election.

May be elected through age 85; may be added post-issue. Once elected, the benefit may not be revoked.

Provides a percentage of the Withdrawal Base as a Lifetime Annual Payment.

Percentage is based on age at time of first withdrawal.

Can be for one life or two lives, jointly with a spouse; must be elected at time of rider issuance.

– Withdrawal Percentage for joint income is based on age of the younger spouse.

All Deferral Bonuses are credited annually upon contract anniversary until the time of first withdrawal.

Deferral Bonus is a simple (non-compounding) credit equal to 6% of the Deferral Bonus Base.

21

Lifetime Spending Account optional benefit: Additional considerations3

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

At the Annuity Commencement Date, an additional annuity option is available to allow for continued variable lifetime income. Your client must select the Variable Dollar Amount Annuity Payout Option to continue payments for life.

If electing to receive LAPs under a Systematic Withdrawal Program, the income amounts will automatically adjust to changes in the LAP.

Covered Life changes will result in termination of the benefit.

Subsequent premium payments are subject to Forethought’s discretion and may not be accepted.

Unused Lifetime Annual Payment amounts will not carry to subsequent years.

Withdrawals do not reduce your Withdrawal Base, provided benefit rules are followed.

Withdrawals in excess of the Lifetime Annual Payment for purposes of Required Minimum Distributions related to the contract will not reduce the Withdrawal Base.

The Withdrawal Base will reduce proportionately for all withdrawals prior to the minimum LAP withdrawal age, 59 ½, and those amounts above the LAP benefit, thereby reducing subsequent LAP amounts. Proportionate reductions equal the percentage reduction in the contract value caused by the excess withdrawal and may be greater than dollar-for-dollar.

Withdrawals may be started and stopped, but Deferral Bonuses will cease after the first withdrawal and will not be reinstated.

Prior to age 59½, should your Contract Value fall below the Minimum Contract Value then in effect, your Lifetime Annual Payments will be zero until the Minimum Income Age (59 ½) is attained. Once your Contract Value is reduced below the Minimum Contract Value, any Partial Withdrawals greater than your Lifetime Annual Payments will terminate your rider and result in the contract being liquidated. 22

Lifetime Spending Account optional benefit: Additional considerations (Continued)3

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

Nursing Care Waiver1

Forethought will waive any applicable CDSC charges upon Full Surrender or Partial Withdrawal of the contract value if the Owner or joint Owner (or in the case of non-natural ownership, the Annuitant) is confined to an Approved Nursing Facility, after the Issue Date of the policy and at the recommendation of a physician, for medically necessary reasons, for at least 90 calendar days to a facility that:

– Provides skilled nursing care under the supervision of a Physician; and – Has 24-hour-a-day nursing services by or under the supervision of a registered nurse; and – Keeps a daily medical record of each patient.

This waiver will terminate upon a change made to any beneficial Owner.

Terminal Illness Waiver1

Forethought will waive any applicable CDSC charges upon Full Surrender or Partial Withdrawal of the Contract if the Owner or Joint Owner (or in the case of non-natural ownership, the Annuitant) is diagnosed with a Terminal Illness (life expectancy of 12 months or less).

The Owner or joint Owner (or in the case of non-natural ownership, the Annuitant) must first be diagnosed by a qualifying Physician as having a Terminal Illness after issuance.

The request for a Full Surrender or Partial Withdrawal, together with satisfactory proof of such Terminal Illness, must be provided by notice to Forethought.

Forethought requires the proof of a Terminal Illness to be in writing and, where applicable, attested to by a qualifying Physician. Forethought reserves the right in the Contract to require a secondary medical opinion by a qualifying Physician of its choosing. It will pay for any

such secondary medical opinion. This waiver will terminate upon a change made to any beneficial Owner.

23

ForeInvestors Choice: Additional included benefits (available for B-Share only)

1Subject to state variations. Not available in South Dakota and California.

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 24

Domestic Equity

Large Cap Mid Cap Small Cap

American Century VP Value Fund

American Funds Growth Fund

BlackRock Basic Value V.I. Fund

BlackRock Capital Appreciation V.I. Fund

BlackRock S&P 500 Index V.I. Fund

Calvert VP NASDAQ 100 Index Portfolio

Goldman Sachs U.S. Equity Insights Fund

Invesco V.I. Comstock Fund

Ivy Funds VIP Core Equity

Ivy Funds VIP Value

MFS® Blended Research Core Equity Portfolio

MFS® Growth Series

Putnam VT Investors Fund

American Century VP Capital Appreciation Fund

Calvert VP S&P MidCap 400 Index Portfolio

Goldman Sachs Growth Opportunities Fund

Goldman Sachs Mid Cap Value Fund

Lord Abbett Mid Cap Stock Portfolio

MFS® Mid Cap Growth Series

MFS® Mid Cap Value Portfolio

Oppenheimer Discovery Mid Cap Growth

Fund/VA

Calvert VP Russell 2000 Small Cap Index Portfolio

Goldman Sachs Small Cap Equity Insights Fund

MFS® Blended Research Small Cap Equity Portfolio

Oppenheimer Main Street Small Cap Fund®/VA

Putnam VT Small Cap Value Fund

Growth and Income AB VPS Growth and Income Portfolio

American Century VP Income & Growth Fund

American Funds Blue Chip Income and Growth

Fund

BlackRock Equity Dividend V.I. Fund

Franklin Rising Dividends VIP Fund

Putnam VT Equity Income Fund

International & World Equity

Foreign World Emerging Markets

American Funds International Fund

Calvert VP EAFE International Index Portfolio

Goldman Sachs Strategic International Equity Fund

Ivy Funds VIP International Core Equity

MFS® Research International Portfolio

Oppenheimer International Growth Fund/VA

Putnam VT International Value Fund

Templeton Foreign VIP Fund

American Funds Global Growth Fund

Oppenheimer Global Fund/VA

Franklin Mutual Global Discovery VIP Fund

American Funds New World Fund

ForeInvestors Choice: Equity investment options

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 25

Fixed Income

High Yield BondIntermediate-Term

BondShort Investment

GradeIndex

BlackRock High Yield V.I. Fund

Lord Abbett Series Bond Debenture

Portfolio

American Funds Bond Fund

BlackRock Total Return V.I. Fund

Goldman Sachs Core Fixed

Income Fund

MFS® Total Return Bond Series

PIMCO Total Return Portfolio

Putnam VT Income Fund

Goldman Sachs High Quality

Floating Rate Fund

Lord Abbett Series Fund

Short Duration Income

Portfolio

Calvert VP Investment Grade

Bond Index Portfolio

U.S. Government Intermediate

Non Traditional Bond Multi-Sector Bond

Putnam VT American Government

Income Fund

Goldman Sachs Strategic

Income Fund PIMCO Unconstrained Bond

Portfolio

Franklin Strategic Income VIP Fund

World Bond Emerging Market Bond Money Market

AB VPS Global Bond Portfolio PIMCO Foreign Bond Portfolio (U.S.

Dollar-Hedged) Templeton Global Bond VIP Fund

PIMCO Emerging Markets Bond

Portfolio

Invesco V.I. Money Market Fund

Asset Allocation

Conservative Moderate

Franklin Strategic Income VIP Fund American Funds Asset Allocation Fund

Invesco V.I. Equity and Income Fund

Putnam VT Global Asset Allocation Fund

Tactical Global Goldman Sachs Global Trends Allocation

Fund

PIMCO VIT All Asset Portfolio

PIMCO Global Multi-Asset Managed

Allocation Portfolio

American Funds Capital Income Builder®

BlackRock Global Allocation V.I. Fund

Invesco V.I. Balanced-Risk Allocation Fund

Ivy Funds VIP Asset Strategy

ForeInvestors Choice:Fixed income and asset allocation investment options

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 26

Alternative

Multi-Alternative Domestic Real Estate World Real Estate

Putnam VT Absolute Return 500 Fund Oppenheimer Global Multi-Alternatives Fund/VA

AB VPS Real Estate Investment Portfolio Ivy Funds VIP Real Estate Securities

Franklin Global Real Estate VIP Fund MFS® Global Real Estate Portfolio

Inflation Protection Commodities Utilities

PIMCO Real Return Portfolio PIMCO CommodityRealReturn® Strategy Portfolio MFS® Utilities Series

Managed Risk

Forethought Variable Insurance Trust (FVIT)

FVIT American Funds® Managed Risk Portfolio

FVIT Balanced Managed Risk Portfolio

FVIT BlackRock Global Allocation Managed Risk Portfolio

FVIT Franklin Dividend and Income Managed Risk Portfolio

FVIT Goldman Sachs Dynamic Trends Allocation Portfolio

FVIT Growth Managed Risk Portfolio

FVIT Moderate Growth Managed Risk Portfolio

FVIT PIMCO Tactical Allocation Portfolio

FVIT Select Advisor Managed Risk Portfolio

FVIT Wellington Research Managed Risk Portfolio

ForeInvestors Choice:Managed risk and alternative investment options

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

ForeInvestors Choice is designed to help retirees use their qualified and non-qualified dollars to more effectively plan for and live in retirement with:

Investment flexibility and growth potential.– Open architecture with access to a wide variety of asset classes.– Reintegration of advisor’s role in asset allocation.

Help covering tax liability during wealth transfer ― with the optional Earnings Protection Benefit.

Lifetime income protection ― with the optional Lifetime Spending Account.– Helps take longevity risk out of the equation.– Guards income against volatile market swings.– Simplifies optimal withdrawal rate calculations for advisors.

27

ForeInvestors Choice: Training recap

1

2

3

1Taxable distributions (including certain deemed distributions) are subject to ordinary income taxes, and if made prior to age 59 1/2, may also be subject to a 10% federal income tax penalty. Distributions received from a non-qualified contract before the Annuity Commencement Date are taxable to the extent of the income on the contract. Payments from IRAs are taxable in accordance with the normal rules surrounding taxation of payments from an IRA. Early surrender charges may also apply. Withdrawals will reduce the death benefit and any optional guaranteed amounts in an amount more than the actual withdrawal.All guarantees assume compliance with the benefit rules and are based on the claims-paying ability of Forethought Life Insurance Company..

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC.

All guarantees assume compliance with the benefit rules and are based on the claims-paying ability of Forethought Life Insurance Company.

Optional benefits are subject to state and firm approval and variations.

The ForeInvestors Choice Variable Annuity is available in multiple share classes, which each have different fees and charges as described in the prospectus. Your financial professional’s commission may also differ depending upon the share class selected. You should discuss which share class is right for you with your financial professional based on the available options. Important share class considerations include, but are not limited to, your investment holding period and investment flexibility.

Taxable distributions (including certain deemed distributions) are subject to ordinary income taxes, and if made prior to age 59 1/2, may also be subject to a 10% federal income tax penalty. Distributions received from a non-qualified contract before the Annuity Commencement Date are taxable to the extent of the income on the contract. Payments from IRAs are taxable in accordance with the normal rules surrounding taxation of payments from an IRA. Early surrender charges may also apply. Withdrawals will reduce the death benefit and any optional guaranteed amounts in an amount more than the actual withdrawal.

If you are investing in a variable annuity through a tax-advantaged retirement plan such as an IRA, you will receive no additional tax advantage from a variable annuity. Under these circumstances, you should only consider buying a variable annuity if it makes sense because of the annuity’s other features, such as lifetime income payments and death benefit protection.

This information is intended to provide a basic understanding of the ForeInvestors Choice variable annuities. The information cannot be used or relied upon for the purpose of avoiding IRS penalties. Forethought Life Insurance Company does not provide tax or legal advice. As with all matters of a tax or legal nature, your clients should consult their personal counsel for additional information.

Forethought is Forethought Life Insurance Company and affiliates, subsidiaries of Global Atlantic Financial Group Limited.

ForeInvestors Choice variable annuities are flexible premium variable annuities issued by Forethought Life Insurance Company, and are underwritten and distributed by Forethought Distributors, LLC.

All statements qualified by final prospectus and Contract and are subject to change without notice. In the event of a conflict between this information and that contained in the prospectus and/or contract, the prospectus and contract shall prevail.

All information herein is as of October 27, 2015.

VA5210 (11-15) 102558

28

FOR ADVISOR TRAINING ONLY. NOT FOR USE WITH THE PUBLIC. 29

Module Title: ForeInvestors Choice Variable Annuity

Course ID: FTFORECHOICE

I certify that I have received Forethought’s Product-Specific Training materials. I further certify that I have read about and understand all material features of Forethought’s variable annuity product, and have adequate knowledge of Forethought’s variable annuity product to determine the suitability of the product for my client.

A copy of this course completion certificate should be faxed to Forethought at:

785-286-6105, or emailed to [email protected], Attn: Licensing

Insurance producer’s name (please print)

Insurance producer’s firm name Insurance producer's National Producer Number (NPN) or Social Security Number (SSN)

Insurance producer’s signature Date (mm/dd/yyyy)

Certificate of Product-Specific Training

![CCSDS SM&C State of the Union - American Institute of ... Documents/2010/Merri... · SM&C Working Group 7 year lifetime ... Flight Dynamics (Orbit, Attitude) ... [SLE-SM] Ground Station](https://img.pdfslide.net/doc/110x75/5abba6f97f8b9ad1768cf571/ccsds-smc-state-of-the-union-american-institute-of-documents2010merrismc.jpg)