Embed Size (px)

Citation preview

INDIAN INSTITUTE OF BANKING & FINANCE Risk Management –Module C

Treasury Management

For Institute of Banking Studies, Kayamkulam

21st September 2014

S.Ravindranath, Freelance Consultant

Derivative Products in Treasury

What are derivative products?

OTC and Exchange Traded Derivative Products

Forwards

Options

Futures and Forwards

Forward Rate Agreement

Interest Rate Swaps

Currency Swaps

Other Products

Derivatives

Derivative, as name indicates, is derived from something.

It is normally meant as a hedge against an underlying which is subjected to risk in adverse price movements.

Treasury Products like Foreign Exchange [Currency], Bonds, Equities, Commodities – all have market risk or price fluctuation risk. Derivatives serve the purpose to overcome losses on account of adverse price movements in the underlying.

This is achieved by taking an opposite independent position in a derivative product, such that when there is an adverse market movement in the underlying resulting in loss, the derivative product will have a favourable position, thereby the loss in the underlying will be offset by gain in the derivative product.

Like any other market or product, Derivatives are used not only for hedging [reduce loss on account of adverse market conditions], but also as speculative tools.

OTC and Exchange Traded

OTC – Over The Counter – means derivative products are available directly from banks. Eg: IRS, FRA, Fx Forward, Fx Options, Fx Swaps

Exchange Traded - There are exchanges, where the derivative products are traded and are available. Eg: IRF, CF, Equity Futures, Commodity Futures, Currency Options, Stock Options etc.

Some of the well-known Exchanges are:

International: CME [Chicago Mercantile Exchange], CBOT [Chicago Board of Trade], NYMEX [New York Mercantile Exchange], Euronext.Liffe, Eurex, LME [London Metal Exchange], SGX [Singapore Exchange]

India: NSE [National Stock Exchange of India], BSE [Bombay Stock Exchange], MCX [Multi Commodity Exchange], NCDEX [National Commodity and Derivative Exchange.

OTC 1. Products available in select Banks and financial institutions 2. Flexibility as to amount, period etc. Hence near-total hedge 3. Pricing is flexible, but decided by banks and could be finer or costly 4. Margin, security etc are flexible and decided by banks depending on customer 5. Counter-party Risk 6. Settlement mostly in physical delivery but also squaring up on net settlement 7. Generally used for hedging risk in underlying 8. OTC is highly active in Forex and interest rate products

EXCHANGE TRADED 1. Only in recognised exchanges 2. Available only in standardised size, specific period, specific settlement date. Hence over or under hedge 3. Transparent pricing, based on screen based OM [Order Matching] 4. Standard cash margin, additional margin on MTM basis 5. Exchange is Counterparty 6. Mostly net settlement by way of cash. Physical delivery only in commodity 7. For hedging as well as speculative trading 8. Exchange Traded products more active in stocks, securities and commodities

Difference between OTC and Exchange Traded Products

Forward Exchange

Cash, Tom. Spot and Forwards

Forwards are also one kind of derivative – underlying being firm commitment made for imports, exports or even remittances.

Forward Contract is a firm contract between a Bank and a customer to deliver or take up foreign currency on a future fixed date or future range of time period not exceeding one month, at a fixed rate of exchange.

Hence, essentially Forward Contract is an OTC Product.

A Forward Purchase Contract is concluded by exporters or those customers who are expecting inflow of foreign currency in future [like IT Companies]. Important to note, particularly from examination point of view while solving problems, here Purchase is with reference to banks. Banks will purchase currency at a future date and pay Rupee to Exporters/Others.

Forward Exchange

A Forward Sale Contract is concluded by importers or those customers who are expecting to remit money outside India in future [Say NRIs wishing to take back money from India]. Important to note, particularly from examination point of view while solving problems, here Sale is with reference to banks. Banks will sell currency at a future date and receive Rupee from Importers/Others.

Forward Contract has to be honoured and delivered as per contract terms. However, the contract can either be delivered before the specified date in the contract [early delivery] or can be extended [extension of contract] or cancelled – all subject to payment of costs or settlement of difference, if any.

Forward Exchange markets are very deep, where risks can be covered generally upto 1 year and in rare cases for even longer periods

Some points on Forward Exchange

How does Forward Exchange help and exporter or importer, hedging his risks?

Is Forward Rates a forecast of rates in the future?

Premium and Discount. Forward rates reflect interest rate differentials between the

two countries of the two currencies involved.

Say GBP and USD. Spot 1£= $ 1.6250/55

3m = -11.70/11.60; 6m = - 28.20/27.20

3m GBP LIBOR = 0.56338% 6m GBP LIBOR = 0.70306%

3m USD LIBOR = 0.23460% 6m USD LIBOR = 0.33090%

Roughly 6m fwd 1 £ = $ 1.6220

Currency with higher rate of interest will be at discount and vice versa

However Forward rates between say USD and INR is not a function of interest

rate differential but more on demand and supply

Reason Free Convertibility of major currencies/Partial Convertibility of Rupee

Some points on Forward Exchange

Forward Contracts give flexibility to the entities that look for coverage

without gaps in terms of amount and period.

However, if at the time of delivery of the forward contract, the then prevailing spot rate is favourable, the entity cannot opt for spot rate.

So forward contract helps in hedging currency risk against adverse rate of exchange. However, there could be opportunity loss when the spot rate at the time of forward contract delivery date is better than the contracted rate.

OPTIONS

OPTIONS is not plural of Option.

Where Forward Contracts fail to provide opportunity profit, Options provide that .

In an Options Contract, if the customer taking Options Contract finds that at the time of delivery, the prevailing spot rate is much favourable than the Options Contract price, he/she can avail the spot rate and abandon the Options Contract at no extra cost.

So putting it otherwise, the holder of an Options Contract has the right to exercise the contract ,but no obligation to deliver [In a Forward Contract, the holder of Forward Contract has an obligation to deliver and no right to abandon the contract, unless he pays appropriate charges]

So, are Options always better than Forward Contracts?

Element of Options Premium payable upfront [Forward Contract does not involve

payment of any major charges]

Options v/s Forward Contracts

Forward Contract 1. No charges for booking except profit margin, but extension, early delivery and Cancellation of contract could result in charges 2. Such charges are decided uniformly by FEDAI, transparent and reasonable 3. Delivery at Contracted Rate only. Opportunity Loss 4. OTC market only, with high liquidity even for small amounts and far more market makers 5. One can get any small or big, standard or odd-lot booked 6. Delivery has to be in full, except in Cancellations difference is settled

Options 1. Cash Premium payable upfront, but no charges for abandoning Options Contract 2. Options Premium calculation is complex and generally system generated and not transparent, resulting in possible abnormal pay-out to customers 3. Opportunity to opt for spot rate at the time of maturity exists 4. Generally Exchange Traded, but OTC also exists, with selected market makers 5. Even in OTC market, one may be able to get cover only for big ticket deal and for round amounts. 6. Settlement is done for difference only. Hence leverage is high.

Terms in Options

Strike Price

Expiry Date

Options Premium to Options Writer

Call Options

Put Options

Contract to be specific eg: USD/JPY – USD Call-JPY Put OR USD Put – JPY Call

At the Money

In the Money

Out of the Money

Intrinsic Value and Time Value

American type of Options

European type of Options

Terms in Option explained

Call Options - Right to buy an asset at the strike price, but no obligation

Put Options – Right to sell an assets at the strike price, but no obligation

Strike Price or Exercise Price – Specified price at which the buyer of an Option contract can exercise his/her right to buy [Call] or sell [Put] the asset.

Expiry Date – The last date on which the Option can be exercised

Options Premium to Options Writer – Price to be paid by the buyer of Option to the seller of Option [in both Call and Put Options]

At the Money – An Option with a strike price is equal to the current price of the asset.

In the Money – An Option with strike price more favourable to the buyer than the current market price. Obviously, the premium for this will be high.

Out of the Money – An Option with strike price unfavourable to the buyer than the current market price of the asset. Premium will be low.

Value of an Option – Market price of the Option

American Type of Option – An Option that can be exercised at any time until expiry date.

European Type of Option – An Option that can be exercised only on the expiry date at the specified Expiration time on the Contract. [Nothing to do with Europe]

Intrinsic Value of an Option

• Intrinsic Value of Option – In the case of “In-the-Money” American Style Option, the difference between the strike price and the current market price is the Instrinsic value of the Option. Intrinsic Value is the profit that can be realised immediately on exercising the Option. So this is most likely to be the minimum premium demanded by the seller of the Option, otherwise there will be arbitrage opportunity.

• For a Call Option, Intrinsic Value is the Maximum between 0 and difference between the current market price and the Option Exercise price. If the Spot price is greater than the Strike price, it is positive intrinsic value. If the Spot price is less than the Strike price, the intrinsic value is 0.

• For a Put Option, if the Strike price is greater than the Spot price, it is positive intrinsic value. If the Strike price is less than the Spot price, the intrinsic value is 0.

• Spot price in the above refers to the current market price of the asset.

• For European type of Option, the intrinsic value will only be notional, since the same cannot be exercised and made money, even there is an opportunity, because it can be exercised only at maturity.

Time Value of an Option

• Time Value of an Option – It is the difference between the Option Premium and the Intrinsic Value. Putting it another way, the value of an American Option at any time prior to expiration will be at least equal to its intrinsic value. Actually, since there is time for expiry of the Option, there is every chance that the market price of the Asset may move in favour of the buyer of the Option. So the seller of the Option will factor that too into account and take higher premium. So it would make sense that the price of the Option [premium] will be more than the intrinsic value – the difference being time value.

• Time value reflects what a buyer of Option is willing to pay for the uncertainty of the asset [meaning its chance of appreciating more with passage of time till expiry. The longer the time for expiry, greater will be the time value.

• So, time value of an American Option is the difference between the call premium and the intrinsic value.

• At expiration , a call option is worth the intrinsic value and no time value. If the Market Price is more than Strike Rate, it will give some positive value. Id the Market Price is less than Strike Price, it will be worthless and will not be exercised, so Intrinsic value will be zero.

Illustration for Intrinsic Value

Calls Puts

Exer.Price Sept Oct Nov Sept Oct Nov

120 9 15 21 3 9 14

125 5 13 19 5 11 17

130 4 11 16 7 14 19

Let us say Current Market price of the asset is 126 as on 20th Sept.

Current Market Price is 126. Exercise Price is 120. So Intrinsic Value here is Rs.6, which will be the minimum price [premium] that would be demanded, otherwise one can pay lower premium [say Rs.4] and immediately exercise Call at the Strike Price [of 120] and Sell the Asset in the Market [at Rs.126] and make arbitrage profit of Rs.2 without any effort.

Illustration for Time Value

Strike Price

Intrinsic Value

Sept Oct Nov

120 6 3 9 15

125 1 5 13 18

130 0 4 11 15

Current Market price of the asset is 126 as on 20th Sept.

If you see, Intrinsic Value at Strike Price of 120 when Market Price is 126 is 6; when Strike Price is 125, it is 1 and when Strike Price is higher than the Market Price it 0. At the same time, there is time value of 3,9,15 etc. So for a Strike Price of 120, when the Current Market Price is 126, probably the Option Premium for a Call Option that will expire by September end is likely to be 9; for a Call Option that will expire in October-end it will be 18 and for a Call Option that will expire in November-end, it will be Rs.33. The expectation for the seller of the option is that by November-end the Asset Price may be Rs. 159 or less. For the Buyer of Option, his view may be that it will be more than Rs.159.

Some aspects of OPTIONS

Since buyer of an option [whether it is Put or Call] pays an upfront premium, he will exercise Option at the Strike Price when such rate is better than current market price at that time. His profit [or loss] is net of the upfront premium paid. The potential for unlimited profit exists. If he does not exercise the option, since prevailing market price is more favourable, his loss is limited to the upfront premium paid.

For an Option Writer [OW or Option Seller], say a Bank, he receives upfront premium. If the buyer of the option exercises the option, OW has to necessarily deliver the product for which Options Contract was executed, irrespective of the fact that the current market price is vastly unfavourable to the OW. The net loss, if any, will be net of upfront premium received. An Option Write has no right, but only obligation to perform.

Variations of OPTIONS

Plain Vanilla Options

Complex Options

Range Forwards or Zero-Cost Options

Barrier Options

Embedded Options

• Options are useful in hedging risks in an underlying.

• However, when there are complex options, combining several options or other products bundled in to one, they become highly risky, since the upfront premium may be very high and understanding their intricacies is very difficult. Such Options become highly speculative.

• Options can be both OTC as well as Exchange Traded.

• Options can be in Stocks, Foreign Currency, Interest Rate, Commodities

Range Forward

• Range Forward is a combination of 2 or more Options, used primarily to hedge or mitigate risk. This contract involves taking two opposite positions in Options.

• For example, one can BUY a European type of PUT Option at a specific STRIKE PRICE and also simultaneously SELL a European type CALL option with higher strike price.

• Say, a person wants to sell $ and buy ¥ between 100 and 102

• In the first case he will pay a premium and will be having the right to sell but no obligation. Say, he buys a PUT at 1 $ = ¥ 100 for $ 1 mn.

• In the second case, since he will sell the option, he will get a premium, but the right to take up the call at the given strike price will be with the other person who is buying the Option. [Writing an Option by other than a bank or institution is prevalent more globally, but not in India]. Say, he sells a CALL at 1 $ = ¥ 102 for $ 1 mn.

• The price it wants to lock in will fall in within this range. Either he will exercise the option to sell at 100 or if he sees the price for $/ ¥ is going up, he will wait to sell at higher price for the other party to exercise to buy at higher price of 102 [So either he sells at 100 or at a higher price of 102 – both are okay for him].

• Since he receives premium for writing second Option, it compensates to some extent for the premium he has paid for buying PUT Option. Hence it is often called Zero-cost Options.

Barrier Options

• Barrier Options are exotic option contracts whose value depends on whether or not the price of the underlying asset crosses a certain level during the option's lifetime. Can be CALL or PUT; American style or European style. Barrier Options are cheaper.

• The term barrier option is used to describe options that become operative [known as KNOCK-IN] or become useless [KNOCK-OUT] if the market price of the underlying touches a specified level [Called BARRIER].

• Say, X buys $/¥ Call Option, when current price is at ¥ 90, with knock-in at ¥100 and barrier at ¥110. Depending on the type of contract agreed upon, there can be several variations.

• 1 – Knock-in takes place at 100. During life of the Option Contract, rate also breached 110. On the maturity date [American Option] the rate settled at 103. Option valid for exercising.

• 2 – Knock-in takes place at 100. During life of the Option Contract, rate touched 110. Contract becomes useless.

• 3 – During life of the Option, rate remains constantly below 100. The Option become void.

• 4 - Knock-in agreed at 100. Barrier 110. But Options valid only if during life of the Option Contract, rate also crossed 115, before settling down between 100 and 110.

• Like this, there can be several variations of Barrier Options Contract.

Embedded Options

• An embedded Option is something that is always an inherent part of an underlying. For example, a person depositing money in a term deposit, always has an option to withdraw before maturity – to his advantage and to the disadvantage of the Bank [particularly when interest rates go up] and can reinvest with the same bank at higher rate of interest.

• Similarly, in a Optionally Convertible Bond, an investor has the option at a particular time, to either exercise his option to convert the bond amount into certain amount of shares at a pre-determined price[if the share prices have gone up substantially] or continue to hold the bond till maturity. This clause is embedded.

• So an embedded option is a special condition attached to a security, and in particular, a bond that gives the holder or the issuer the right to perform a specified action at some point in the future.

• In perpetual kind of bonds issued by banks, sometimes there will be an embedded call option to the bank to recall the bond, say after 10/15 years.

• Callable Bonds or Putable Bonds

FUTURES

• Just as Options is not plural for Option; Futures is not plural for future.

• Futures are more like Forwards, which are traded in a recognised Exchange.

• Futures in Exchange Rate, Interest rates, Stock and Stock Index prices are collectively called Financial Futures. Commodities traded in the exchange come under Commodity Futures category.

• Under a futures contact, the seller of futures contract agrees to deliver to the buyer a specified security or currency or a commodity on a specified time and at a fixed price. It is a legally binding contract

• Since all these are traded/made available only in an exchange, the size and delivery period are standardised and prices are transparent.

• Unlike Options where one has to pay Upfront premium, under Futures, one has to pay to the exchange a pre-decided margin and continue to pay margin as and when required as per daily MTM [Marked to Margin]

• Long Position [Buying Base Currency Futures]; Short Position [Selling Base Currency Futures]

Currency Futures - explained

• The example given in the IIBF book explains Currency Futures very clearly. Let us examine that here to understand how it works

• Deal - £/$. Amount 25000 – Importer “XYZ ” agrees to buy £ and deliver $ through an exchange [Buyer unknown] delivery after 2 months. Rate fixed for the Futures deal is 1£ = 1.6650.

• On the maturity date, £ is available in the market at 1.7000. Very important to note, Exchange will not sell £. XYZ has to buy £ from the market at 1.7000 and exchange it for $. This would put XYZ into a loss, since he has to buy the base currency at higher rate than the Futures price [Remember maxim is Buy Low/Sell High]. The Exchange will fix the Spot Rate and work out the difference between the Spot Rate and the contracted Futures Rate and pay the difference. XYZ will actually buy £ from the market. So effectively, XYZ is protected by the movement in the currency rate to a considerable extent.

• What happens if the Spot rate on the delivery date is 1.6000? Here, XYZ has to take delivery at the contracted rate and pay the difference to the Exchange.

Forwards v/s Currency Futures

FORWARDS [FC] CURRENCY FUTURES [CF]

1. It is an OTC product 2. Flexibility in terms of amount, period, rate of exchange etc. 3. Generally no or very low margin requirement . Additional MTM margin not required 4. FC can be pre-delivered or extended or even cancelled, subject to charges 5. Eventually actual delivery at the contracted price is required at the counters of the bank, unless it is cancelled

1. It is an Exchange Traded product 2. Standardised amounts and delivery period. 3. Initial margin needed. Daily review of margin requirement according to MTM which may need to be topped up. 4. CF contract has to be delivered. Extension is possible with charges. One can cancel the effect by booking a fresh opposite contract and square up the transaction. But on the delivery dates, both contracts will be assessed for loss/ profit and differences settled. 5. Settlement is done at the Exchange for the difference only.

Some aspects of Currency Futures [CF] in India

• National Stock Exchange [NSE] offers CF in $, €, £ and ¥ against Rupee.

• Exchange operates for CF on all working days between 9 AM and 5 PM except on Saturdays, Sundays and designated holidays

• For settlement purpose, NSE uses RBI closing reference rates

• For Daily MTM purpose, NSE takes closing price, which is calculated on the basis of the last half an hour weighted average price of such contract or such other price as may be decided by the relevant authority from time to time.

• Settlement date is usually kept such that the spot delivery date coincides with the last international working day for the currency. # [See next slide too]

• Quotes are available for up to one year.

• Other Exchanges providing Currency Futures – MCX-FX, BSE.

• Some banks are permitted to trade in CF thro Exchanges. Clients who cannot deal directly through exchanges, can undertake business through such banks. Banks like SBI provide a platform to deal thro with exchange

• What NSE provides other exchanges provide same with similar features.

Overview of Currency Futures Taken from SBI’s website – Terms based on RBI Guidelines

Deals provided USD/INR, EUR/INR, GBP/INR,JPY/INR. X-ccy CF not permitted

Unit of trading 1 unit. ie: $ 1000, £1000, €1000 and ¥ 100,000

Underlying The exchange rate in INR for USD/EUR/GBP/ JPY

Tick size INR 0.0025

Contract trading cycle 12 month trading cycle.

Final settlement day Last working day of the expiry month - see previous slide marked #

Position limits Clients (per exchange): Maximum USD 10 mn [Long or Short]

Minimum-Initial margin 4% of notional value of the contract.

Settlement Daily : T+ 1 Final : T+ 2

Mode of settlement Cash settled in INR

Daily settlement price (DSP)

Calculated on the basis of last half an hour weighted average price.

Final settlement price (FSP)

RBI reference rate.(Last working day of the month)

Internationally, the terms of different exchanges will be quite different. The above example is just to give you a feel of the various features of Currency Futures.

Interest Rate Futures [IRF]

• Bonds/Securities like G-Secs undergo price/interest rate volatility. When interest rate goes up, price falls and vice versa, thereby exposing the asset to price/interest rate risk .

• IRF is an Interest Rate Derivative, where a fixed interest bearing instrument, as seen above, is an underlying.

• Let us say an investor is holding a bond at a given price [and interest]. When the price of the bond falls in the secondary market [simultaneously interest rate would go up], the investor will lose money on the bond. To hedge this risk he/she may resort to purchasing an IRF.

• An interest rate futures contract is an agreement to buy or sell a debt instrument at a specified future date at a price that is fixed today.

• RBI Definition: Interest Rate Futures means a standardized interest rate derivative contract traded on a recognized stock exchange to buy or sell a notional security or any other interest bearing instrument or an index of such instruments or interest rates at a specified future date, at a price determined at the time of the contract.

•

Interest Rate Futures [IRF]

• First let us see some global IRF products.

• There are short term IRF [up to 1 year – T-Bill Futures] and long term IRF [generally covering 10 years and above – Long Bond Futures]. There can be IRF for the medium term [1 to 10 years] too, but volumes are thin.

• T-Bill Futures are on notional T-Bills and generally settled at maturity on physical delivery basis. In some cases the settlement can be on cash basis for difference

• The underlying for the Long Bond Futures is a notional coupon bearing bond. These contracts are generally settled physically but in some markets they are also cash settled for difference.

• Different Exchanges have different rules and regulations, different product offers [but primarily the basics do not different], different delivery schedules etc. There are wider product offers to choose from. Volumes traded are very high.

Interest Rate Futures – Indian Market

• Interest Rate Futures market is relatively nascent, but volumes are pricking up. SEBI [Securities and Exchange Board of India], the regulator is trying to bring necessary changes to improve the trading volumes, including offering new products and extending the scope to more participants.

• RBI permits for IRF deriving value from the following underlying on the recognised stock exchanges: (i) 91-Day Treasury Bills; (ii) 2-year, 5-year and 10-year coupon bearing notional Government of India security, and (iii) Coupon bearing Government of India security.

• But at present, IRFs in the 3 exchanges are being based on two underlying — the 10-year benchmark government security (G-sec) and the 91-day treasury bill. Bulk of the volumes, however, are seen in the 10-year G-sec.

• IRF are traded in 3 Exchanges, NSE, BSE and MCX-SX.

• Like other Futures, there is initial or up-front margin and extreme loss margin

• There are stipulated trading position limits – separate for FIIs and other Trading Members; separate limits for Long Bond Futures and T-Bill Futures. Similarly there are separate and lower limits for client positions.

•

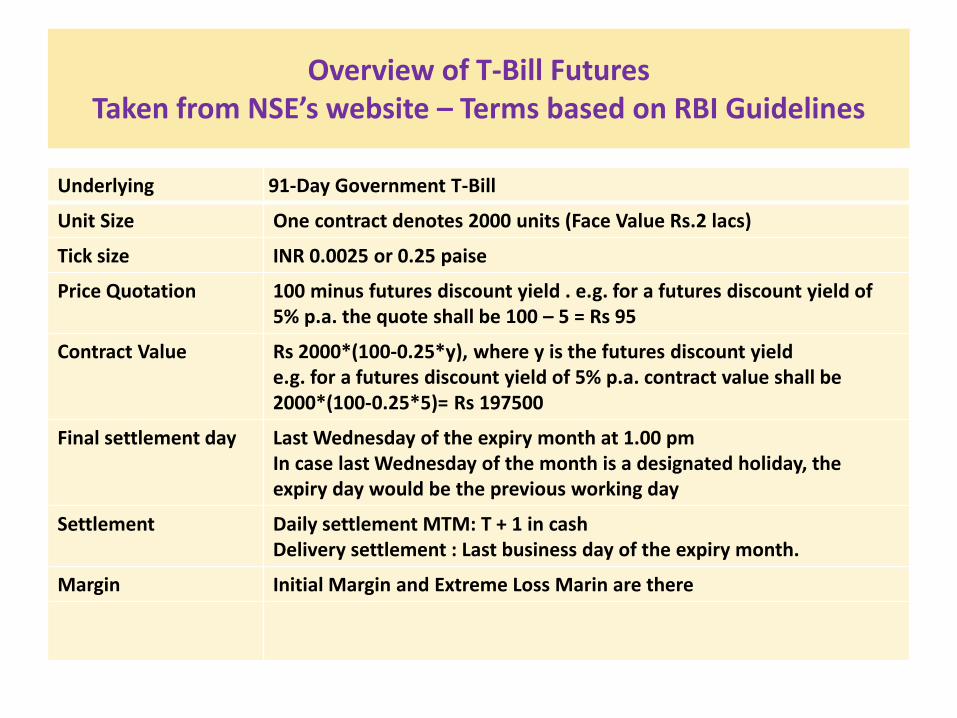

Overview of T-Bill Futures Taken from NSE’s website – Terms based on RBI Guidelines

Underlying 91-Day Government T-Bill

Unit Size One contract denotes 2000 units (Face Value Rs.2 lacs)

Tick size INR 0.0025 or 0.25 paise

Price Quotation 100 minus futures discount yield . e.g. for a futures discount yield of 5% p.a. the quote shall be 100 – 5 = Rs 95

Contract Value Rs 2000*(100-0.25*y), where y is the futures discount yield e.g. for a futures discount yield of 5% p.a. contract value shall be 2000*(100-0.25*5)= Rs 197500

Final settlement day Last Wednesday of the expiry month at 1.00 pm In case last Wednesday of the month is a designated holiday, the expiry day would be the previous working day

Settlement Daily settlement MTM: T + 1 in cash Delivery settlement : Last business day of the expiry month.

Margin Initial Margin and Extreme Loss Marin are there

Overview of Long Bond Futures IRF Taken from NSE’s website – Terms based on RBI Guidelines

2 Underlyings are covered presently

1. Futures contracts based on 8.83% Central Government Security having maturity on November 25, 2023 2. Futures contracts based on 8.40% Central Government Security having maturity on July 28, 2024

Unit Size Rs. 2 lakhs face value of GOI securities equivalent to 2000 units.

Tick size INR 0.0025

Contract Value Quoted price x 2000.

Final settlement day Last Thursday of the month. In case the last Thursday is a trading holiday, the previous trading day shall be the expiry/last trading day

Minimum-Initial margin

4% of notional value of the contract.

Settlement Daily MTM settlement on T+1 in cash based on daily settlement price. Final settlement on T+1 day in cash based on final settlement price

Daily settlement price (DSP)

Volume Weighted Average Futures Price of last half an hour or Theoretical price

Final settlement price (FSP)

Weighted average price of the underlying bond based on the prices during the last two hours of the trading on NDS-OM. If less than 5 trades are executed in the underlying bond during the last two hours of trading, then FIMMDA price shall be used for final settlement

Swaps

• Swap literally means exchange of one for another.

• In forex market, for funding nostro account, which may have been overdrawn, the bank does a simple a swap – buy cash $ [against payment of Rupee] from another bank and simultaneously sell spot $ [against receipt of Rupee] to the same bank. This way the overdraft is plugged. This is also one kind of swap.

• But we shall extend our discussions to a little more complex kinds of swaps – Interest Rate Swaps [IRS] and Currency Swaps.

• They are OTC products – Derivative instruments for managing risks, as well as cost efficiency. Swaps are extensively used by banks, insurance companies, Primary Dealers, Mutual Funds, Corporates etc.

• An Interest Rate Swap is an exchange of interest rate flows of an underlying asset/liability on a notional amount under swap. In this interest flow of one type of asset/liability is exchanged for interest flows of another type of asset/liability. There is no transfer of underlying asset or liability. In a simple IRS, there is exchange of interest flows from a fixed rate bond/Security with interest flows from a floating rate bond/security.

• We shall discuss this with an example in the next few slides.

A case study - IRS Fixed vs Floating

• A Company wants to borrow Rs.50 Crore for a 5-year period at lowest possible cost on say, annual interest payment basis. This Company expects the interest rates to decline.

• Company B also wants to borrow Rs. 50 Crore for 5 years and expects that the interest rates are likely to go up. Having such divergent views is nothing new.

Company A, with better Credit Rating of AA has clear advantage of 2% in Fixed Rate

Company B has better advantage in Floating Rate – only 0.50% higher than Company A.

This comparative advantage positions create an opportunity for arbitrage to each other

Company A Company B

Credit Rating AA B

Can borrow Fixed Rate 9% 11%

Can borrow Floating Rate 364 Day T-Bill Rate + 1% 364 Day T-Bill Rate + 1.50%

Absolute Advantage in both

Comparatively better advantage on Floating basis

How IRS works and helps cost savings

Borrows Pays Borrows Pays 364 Day T-Bill Fixed 9% p.a. Floating Rate + 1.5% Receives Fixed 9.50%

Pays 364 Day T-Bill Rate+ 0.5%

COMPANY A COMPANY B

BANK C

BANK D

COMPANY A COMPANY B

Fixed Rate +0.50% +1.50%

Floating Rate +0.50% -1.00%

Net Gain +1.00% +0.50%

IT’S A WIN-WIN SITUATION

Discussion on the Example

In the previous example, there are a few issues that need observation:

1. The loans of each company with respective banks remains intact and each company may be servicing their interest in the normal course. Banks C and D, may not be even aware of the fact that each customer has entered into an IRS. So the transaction between the two Companies will be on a notional principal. It is quite possible that the loan taken by Company A from Bank C may be for Rs.100 Cr., whereas IRS entered into with Company B will be for Rs.50 Crore only, since Company B has a loan exposure of Rs. 50 Crore. In the case of Company A, the remaining Rs. 50 Crore will be unhedged.

2. It is difficult to get an identical counterpart with similar amount and having contrary views. Therefore, IRS is generally dealt through a third Bank, Bank E, who may be a market-maker [This Bank may offer the quotes for both the Companies from its own large portfolio]. For that a small portion of the profits from both Company A and Company B may be shaved off as commission. So in the given example, the Bank may take 0.15-25% from Company A and 0.20-25% from Company B. Even then both the companies would have benefitted. Here Both Companies may not know each other.

3. Company B will continue to get 9.50% interest from Company B through out the period.

Continued

Discussion on the Example

4. For the first year Company B will pay the prevailing 364-Day Bill plus 0.50%. For the 2nd year, if 364-Day T-Bill rate has changed , Company A will pay 0.50% over the new 364-Day T-Bill rate. This will be repeated for the remaining 3 years. So, if indeed the system rate of interest has declined in the years following, Company A will benefit, since rate of interest on 364-Day T-Bill would have declined and so will be the interest rate that Company A will pay Company B. If, however, interest rates have gone up, then Company A will continue to get 9.50% from Company B, but pay higher interest rates in the subsequent years to Company B, since 364-Day T-Bill rate would have gone up

5. In actual practice, the interest flows are netted out and only difference is paid by one of the Companies to the other.

6. In a Company to Company direct deal, as seen in the example, there is a risk if one of the Company [possibly Company B] defaults or pre-closes its loan, etc. However when the deal is structured through a market-making bank [Bank E], then even if such eventuality happens, the bank will continue to keep its commitment to the remaining Company.

7. The interest stream from both companies should be on the same date. This may be possible on where an intermediary Bank E is involved.

8. I have taken 364-Day T-Bill rate only for understanding. It is not a common benchmark.

How banks too use IRS to hedge its portfolio

• Banks too resort to IRS in a big way to manage Interest Rate risks on account to ALM issues [Deposits are on Fixed Rate basis; Advances are generally on floating rate basis; Short term deposits service long term advances or medium term deposits service short term investment, etc. Hence ALM mismatches both under interest rates as well as time buckets]

• Scenario: Bank A’s 3 year TDR - 9.00%. Inter-Bank Call – 3 year OIS[Overnight Index Swap] of another Bank B - Interest rates tending to fall. So, borrower does not wish to lock in fixed rate. Willing to take floating rate loan linked to call money or MIBOR. Margin 2-2.5%.

• Bank can deploy in call at 7%, which may go down to 6%. Incur Loss OR agree to lend to borrower at MIBOR + 2.5% [9.5%]. If MIBOR too goes to 6%, yield 8.5%.

• Bank chooses to lend to the borrower on the customer’s term at MIBOR + 2.5% [Presently 9.5%]

• Bank A then undertakes OIS for 3 years with Bank B – Receives Fixed at 8.90% and Pays floating O/N MIBOR. [Note: O/N MIBOR will be around average call rates and so I have taken same 7% as MIBOR O/N.]

7.00%

8.90% - 9.00%

Effect of IRS in the example

• How the position will look like for Bank A:

• On Floating Leg: From Borrower - Bank A will receive O/N MIBOR + 2.50% To Bank B – Bank A will pay O/N MIBOR

Inflow to Bank A : 2.50% [“MIBOR from” and “MIBOR to” cancel out,

irrespective of what O/N MIBOR will be – whether it goes up or down]

• On Fixed Leg: From Bank B – Receive 8.90% [Fixed] To Depositor/s of 3 year TDRs – Pay 9.00% [Fixed]

Outflow: 0.10%

• Net Inflow: 2.40% • Costs of CRR/SLR are ignored in this example. A small portion of those costs will

bring down the net inflow to below 2.40%.

Another example

• A Bank are also using IRS to reduce costs on deposits. Here’s how.

• Bank A’s TDR interest rate for 1 year 9.00%; MIBOR/Call 1 year OIS Interest Rate Swap of Bank B –

• Above rate scenario will probably be there in a rising interest scenario.

• Bank A can enter into 1 year OIS with Bank B

• Bank A receives Fixed at 7.95% ; pays MIBOR O/N at 7.00%. [Plus 0.95%]

• Bank A pays Depositor/s of 1 year TDR at 9.00% [ Minus 9.00%]

• Net cost of 1 year TDR to Bank A = - 9.00% + 0.95% = - 8.05%.

• This will continue for some time till interest rises in due course when MIBOR may reach at 7.95%, at which stage there will be no gain from IRS.

Cost on SLR/CRR ignored.

7.95-8.00

7.%

More on IRS

• IRS is therefore generally associated with exchange of Fixed Rate with Floating Rate, vice versa.

• There are, however, cases where IRS exchanges can be between 2 floating rate assets/liabilities. In a floating rate bond, there is a benchmark and the rate of interest will be a mark-up over the benchmark. Eg: 2% over 90-Day T-Bill or LIBOR + 0.75%, 3M NSE-MIBOR + 2%; LIBID – 0.50% [LIBID minus half percent], etc. So, there can be two customer having exposure with different kinds of floating rate exposures, who may like to exchange each other’s interest rate streams. Floating to Floating is also known as BASIS SWAP.

• The benchmark must be credible, widely accepted by the market and generally risk free interest rate. Some of the other Floating Rate Benchmarks are: Commercial Paper Rates, Treasury Bill Rates, 10 Year Benchmark G-Sec rates, NSE-MIBOR Rates, Prime Lending Rates, Bank Rate or any other mutually agreed rates.

• Reset Date is the date when the benchmark rate is refixed for the next period.

LIBOR/LIBID/MIBOR/MIBID

• In the global markets, LIBOR or ICE LIBOR is the most widely accepted benchmark, although in the recent times, LIBOR fraud has come to light.

• ICE LIBOR stands for INTER CONTINENTAL EXCHANGE LONDON INTER BANK OFFERED RATE. LIBOR is widely available in five major currencies: U.S. dollar (USD), Euro (EUR), Pound Sterling (GBP), Japanese Yen (JPY) and Swiss Franc (CHF), covering 7 maturities: overnight, one week, 1, 2, 3, 6 and 12 months. The most commonly quoted rate is the three-month U.S. dollar rate. LIBOR or ICE LIBOR serve as the benchmark reference rate for debt instruments, including government and corporate bonds, mortgages, credit cards, derivatives such as currency and interest swaps, among many other financial products.

• Similar to LIBOR in different markets are TIBOR [Tokyo], SIBOR [Singapore], EURIBOR [European countries] etc.

• NSE-MIBOR and NSE-MIBID are used in India for Rupee products. National Stock Exchange administrates these rates and are available for Overnight [O/N], 3 DAY, 14 DAY, 1 MONTH and 3 MONTH.

Some more market practices

• While NSE-MIBOR is widely used as a benchmark, there are few other benchmarks used for floating rate products in India.

• FIMMDA – Fixed Income, Money Market Derivative Association of India – has standardised market practices for debt market, adopting different benchmarks, like INR-MIBOR, INR-MIFOR, INR-MIOIS, INR-BMK, INR-CMT, etc.

• MIFOR is a combination of LIBOR and forward premium of USD/INR, which is used for foreign currency borrowings swapped into Rupees. This is a proxy used, since forward rates in Indian Rupee is not a function of interest rate differentials, but one of demand and supply, since Rupee is not fully convertible.

• In India, IRS is what we call as plain vanilla type of swaps – very simple to understand and use. However, in the global markets there are large number of variations or combinations, which are widely used by those who are fully familiar with the implications, risks involved etc.

• Indian Banks widely use OIS or Over Night Index Swaps for managing Asset Liability mismatches. Banks pay fixed interest on deposits and generally receive floating rate of interest on advances or investments

An example of MIFOR

MIFOR – Mumbai Inter Bank Forward Offered Rate – a floating benchmark rate.

It’s a combination of 6m USD LIBOR and a 6m USD/INR forward premium [in %

terms]

Market scenario:

• 6m USD LIBOR is 4% [purely hypothetical for this exercise]

• 6m USD/INR premium is 1.67% [Spot USD/INR Rs.60; 6m forward USD/INR Rs.62]

• So 6m MIFOR will be 4.00% + 1.67% = 5.67%

• 5-yr MIFOR Swap = 6.15%-6.25%

Bank A borrows from foreign sources based on 6m LIBOR for 5 years.

A Borrower in India wants Rupee Loan at say 8% [Fixed].

How it will go about?

How will it work out?

• Bank A will borrow USD from foreign Bank for 5 yrs at 6m LIBOR at 4% presently

• Bank A will then undertake a simple USD/INR swap with Bank B for 6m and pay premium of 1.67%. [Sell USD and receive Rupee on Spot basis]

• Then Bank A undertakes a MIFOR Swap with Bank C for 5 years [by agreeing to Pay Fixed 6.25% and Receive 6m MIFOR]

• 6m MIFOR received [5.67%] from Bank C in effect means [6m LIBOR received at 4.00% PLUS 6m USD/INR premium received at 1.67%]

• 6m LIBOR received portion OF MIFOR @ 4.00% will be paid to the foreign bank from where 5-yr USD loan was taken. So it gets cancelled with one another.

• 6m USD/INR premium received portion of MIFOR at 1.67% will be paid to Bank B, which will get cancelled with one another.

• Bank A can now lend USD swapped into INR to a corporate at 8%.

• Paying 6.25% to Bank C and receiving 8.00% from Corporate. Net margin 1.75%.

• Every 6m LIBOR, MIFOR, USD/INR swap etc will be reset, but since whatever may be the rates, they will get evened out – what is received from someone will be paid out to someone else. What will remain constant is 8% inflow from borrower and 6.25% outflow to Ban k C for the full term of 5 years. RESET DATE AND TIME HAS TO BE SAME

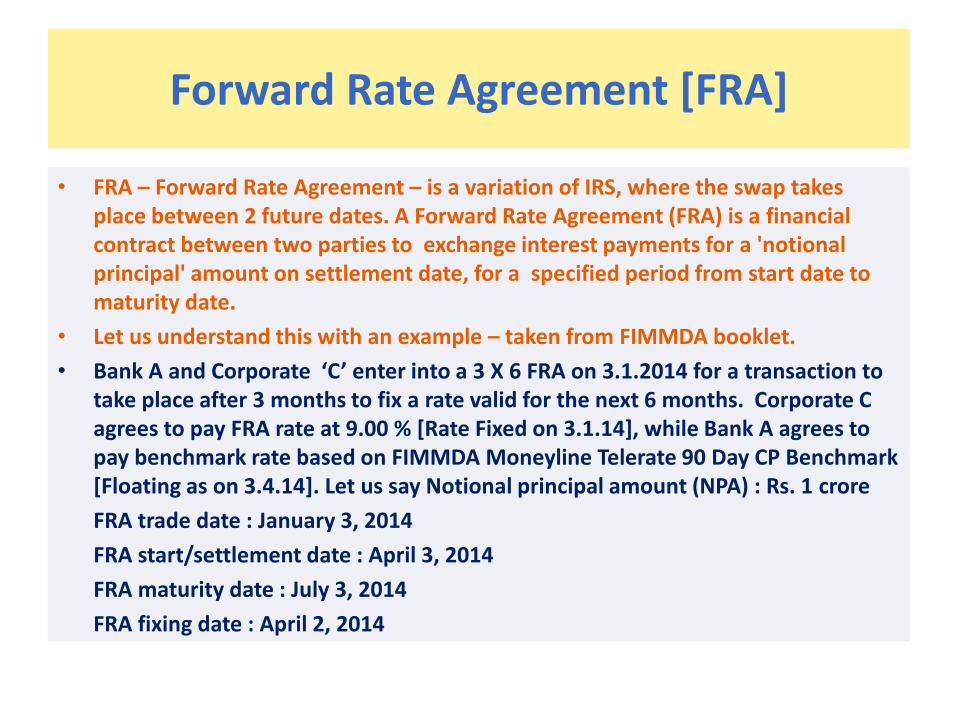

Forward Rate Agreement [FRA]

• FRA – Forward Rate Agreement – is a variation of IRS, where the swap takes place between 2 future dates. A Forward Rate Agreement (FRA) is a financial contract between two parties to exchange interest payments for a 'notional principal' amount on settlement date, for a specified period from start date to maturity date.

• Let us understand this with an example – taken from FIMMDA booklet.

• Bank A and Corporate ‘C’ enter into a 3 X 6 FRA on 3.1.2014 for a transaction to take place after 3 months to fix a rate valid for the next 6 months. Corporate C agrees to pay FRA rate at 9.00 % [Rate Fixed on 3.1.14], while Bank A agrees to pay benchmark rate based on FIMMDA Moneyline Telerate 90 Day CP Benchmark [Floating as on 3.4.14]. Let us say Notional principal amount (NPA) : Rs. 1 crore

FRA trade date : January 3, 2014

FRA start/settlement date : April 3, 2014

FRA maturity date : July 3, 2014

FRA fixing date : April 2, 2014

FRA Example

Assume, FIMMDA Moneyline Telerate 90 Day CP Benchmark on fixing date (April 2,

2014) is 8.50 %. Cash flow calculations are as follows:

Interest payable by X :

{Rs. 1 crore (NPA) x 9 x 91 (April 3 to July 3, 2014)}/ 36500 = Rs. 2,24,384/-

Interest payable by Bank A:

{Rs.1 crore x 8.50 (Benchmark rate) x 91 }/ 36500 = Rs. 2,11,918/-

Therefore, a net interest amount of Rs. 12,466/- is receivable by Bank A

on the maturity date i.e. July 3, 2014. However, the settlement of the amount is to

be done on April 3, 2014 on the discounted value* i.e.

12,466 /{1 + 8.50x 91/36500} = 12466/1.02119 = Rs. 12,207/-

So, X will pay to Bank A Rs. 12,207/- on April 3, 2014.

* PV = FV/(1 + I)ⁿ

Currency Swap [CS]

• A Currency Swap involves exchange of cash flow in one currency with that of another currency or put it another way, it involves exchange of principal and interest in one currency for the same in another currency.

• In cases where currency swap [exchange] is undertaken only for principal amount, it is called Principal only Swap. If only interest streams are exchanged in another currency, it is known as Coupon only Swap.

• Take eg in the booklet. A German Co. can borrow cheaper in its own country, but needs Rupee for investment in India. An Indian Corporate is able to raise fine rate in Rupee, but needs Euro for its European subsidiary. These 2 companies can borrow at best terms in their own currencies and then enter into CS by deciding an interest rate, an agreed upon amount and a common maturity date for the exchange.

• A financial intermediary will step in to facilitate the swap [A swap dealer in Treasury Desk]. Currency Swap is essentially a OTC product

Currency Swap

• Currency Swaps are a series of Forward Contracts, bundled into a single product, in a way.

• Currency swaps are undertaken by large number of Indian corporates with good credit rating, when they borrow in a big way raising ECB [External Commercial Borrowings] for domestic use, as it is far cheaper than borrowing directly in Indian Rupee from banks in India.

• CS helps in lowering of borrowing costs when Companies go cross-border and establish their subsidiaries or make cross-border investments or take up projects. Here again comparative advantage of borrowing in one country over the other becomes the key.

• Let us see this with a hypothetical example in the following slides.

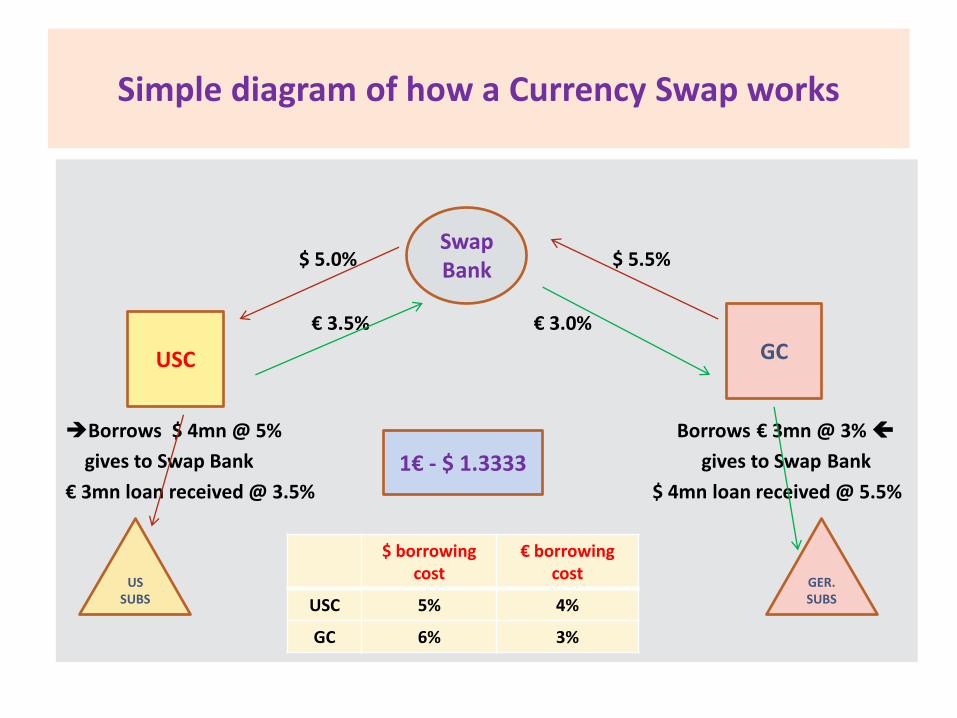

An example of a simple Currency Swap

• A US MNC [Lets call them USC] has a subsidiary in Germany [say USCGS], which it wants to finance with about € 4 million. USC can borrow in Euro Bond Market, but not being so well known will not get good pricing. They can however, get loans at a finer rate locally in $.

• A German MNC [Lets call them GC] also has a subsidiary in USA [say GCUSS] and is facing a similar issue. They are looking to invest in the US subsidiary to the extent of $ 3 million. They have better credit rating locally and can borrow at a cheaper rate than the US MNC subsidiary.

• They both approach a Swap Market Trader, a Bank with their requirements.

• Let us see next how the Currency Swap works for them.

• and convert it into €. But this will expose itself to exchange rate risk. They can borrow € in the Euro bond market, but since they are not as well known in Europe as in USA, they may not get a finer rate than a local German Company with the same kind of rating. But, if they can directly or indirectly with the help of a Swap Market Dealer/Bank find some one, a German MNC with US operations[through a subsidiary] with similar issues and looking to borrow in US market in $, both the entities will benefit. Here comes

• If they can find a German MNC with a mirror-image financing need they may both benefit from a swap.

• If the spot exchange rate is S0($/ €) = $1.30/ €, the U.S. firm needs to find a German firm wanting to finance dollar borrowing in the amount of $52,000,000.

$ borrowing cost € borrowing cost

USC 5% 4%

GC 6% 3%

Simple diagram of how a Currency Swap works

$ 5.0% $ 5.5%

€ 3.5% € 3.0%

Borrows $ 4mn @ 5% Borrows € 3mn @ 3%

gives to Swap Bank gives to Swap Bank

€ 3mn loan received @ 3.5% $ 4mn loan received @ 5.5%

$ borrowing cost

€ borrowing cost

USC 5% 4%

GC 6% 3%

USC GC

Swap Bank

US SUBS

GER. SUBS

1€ - $ 1.3333

Some final thoughts on Risk Management in Treasury products

RBI is constantly monitoring the activities of Treasury with respect to offering products and the level of risk management. Accordingly permission is granted to banks and other users to participate in various risk mitigating measures. However, being very cautious understandably, presently all products are simple plain vanilla kind and complex products are not permitted.

There are strict guidelines and criteria for banks that can offer various products, so that losses on account of plunging in to areas that are not understood, are minimised.

It is essential to understand the implications of any Treasury product, before taking an exposure; otherwise, instead of using derivatives to mitigate risks, the participants may incur colossal losses, as it happened a few years back, when exotic products were offered by some private sector and foreign banks and many corporates who initially made money, lost much more in the later stages.

Before entering into any derivative product the banks and customers enter into a written agreement, called ISDA Master Agreement. This agreement is standardised by INTERNATIONAL SWAP AND DERIVATIVES ASSOCIATION.

Uses of Derivatives

Bank’s Treasury uses Derivatives for own use as well as for customers’ [Corporates] needs, based on guidelines set by RBI.

Options and Futures are more vibrant in Equity Markets, but the banks are not very active [particularly Public Sector Banks] in this segment.

Banks and some of the large Corporates are active in Interest Rate Futures, Interest Rate Swaps, Currency Swaps, Currency Futures, etc – both for managing the risks in own portfolio as well as to fulfil the hedging requirements of the customers.

Final word: Derivatives are useful tools to hedge the risks. Some of the simple derivative products are also useful in trading for profits or to reduce costs. But when they are used indiscriminately with complex structures and without understanding, it is sure trip for disaster.

Noted Financial Wizard and Investor Warren Buffett has stated

“Derivatives are financial weapons of mass destruction, carrying dangers,

that, while now latent, are potentially lethal.” It’s another story that he

himself indulged later on in derivatives and lost a fortune.