Embed Size (px)

Citation preview

FOREIGN INVESTMENT

CAPITAL FLOWS

IN U.S. REAL ESTATE

“U.S. 2016 AND BEYOND”

Overview Review of Past 10-year Trends (As of 4Q 2015)

Update of Recent Trends (As of 3Q 2016)

View of 2016 and Beyond

“Foreign Investment Capital

- U.S. Outlook for 2016”

Article by Tony D. Kamath, MAI, MRICS

Published in CRE Finance World Magazine, Summer

2016 (page 31-34)

Base: Data and published literature as of 1Q 2016

Sources:

Surveys, Data & Opinions

CBRE - “2016 Global Real Estate Market Outlook”

Cushman & Wakefield (C&W) – “Atlas Outlook 2016”

Jones Lang LaSalle (JLL) – “Global Market Perspective, Q1 2016”

RCA – “USA Incoming Cross-Border Capital into Property (Past 5-10 Years)”

AFIRE – Association of Foreign Investors in Real Estate

CRE (Counselors of Real Estate) –”The CRE 2015-16 Top Ten Issues Affecting

Real Estate”

ULI (Urban Land Institute) – “Urban Land”

The Big Picture

U.S. Capital Inflows Historically from Europe, Canada and Japan

Recent 5 years – Sovereign Wealth & Pension Funds

Savings from Canada, China, Singapore and Norway

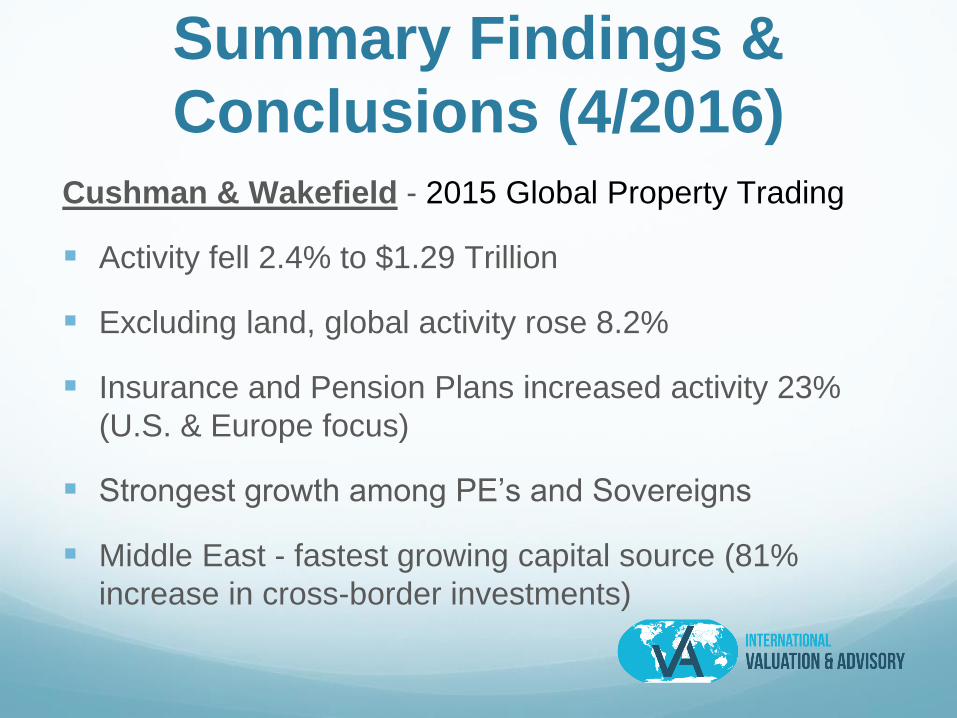

Summary Findings &

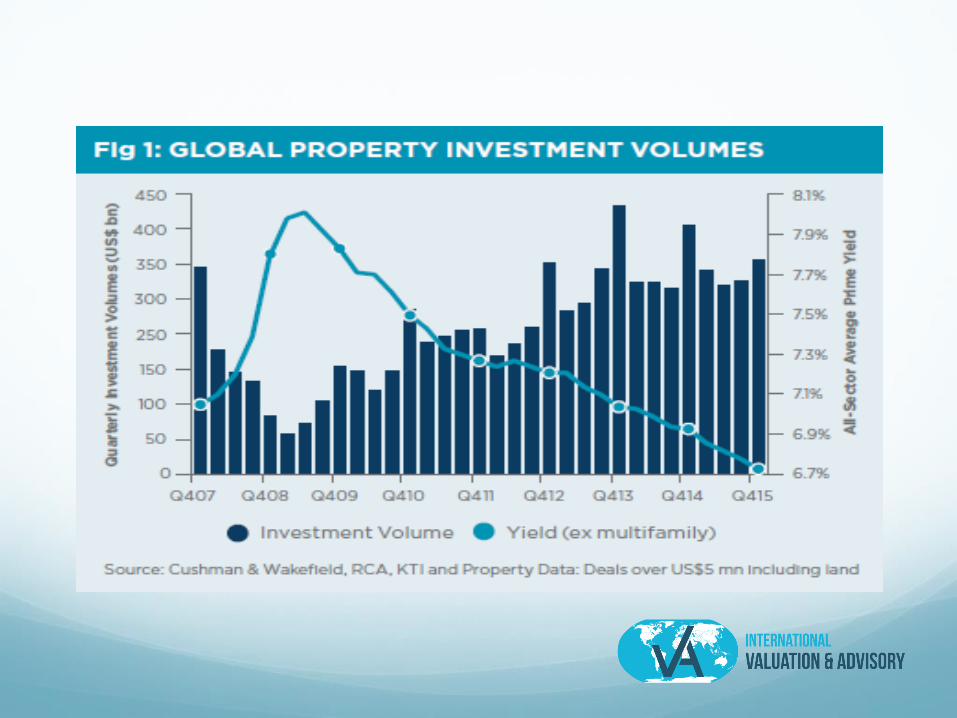

Conclusions (4/2016)Cushman & Wakefield - 2015 Global Property Trading

Activity fell 2.4% to $1.29 Trillion

Excluding land, global activity rose 8.2%

Insurance and Pension Plans increased activity 23%

(U.S. & Europe focus)

Strongest growth among PE’s and Sovereigns

Middle East - fastest growing capital source (81%

increase in cross-border investments)

Summary Findings &

Conclusions (4/2016)Cushman & Wakefield (Cont’d)

Canadian and global funds doubled spending in the

U.S. (70% increase over 2014)

Global funds took 28% of U.S. transactions in 2015

Sources: China, Canada, Norway, Singapore,

Switzerland and Germany

Overseas investors market share increased from 10.0%

to 18.1%

Summary Findings &

Conclusions (Cont’d)CBRE

2016 global activity will remain robust

Pace will slow (- H1 2015 global investment turnover 5X

of H1 2009)

Growth due to

Excess global savings

Low bond yields

Under allocation of real estate in Asia

Summary Findings &

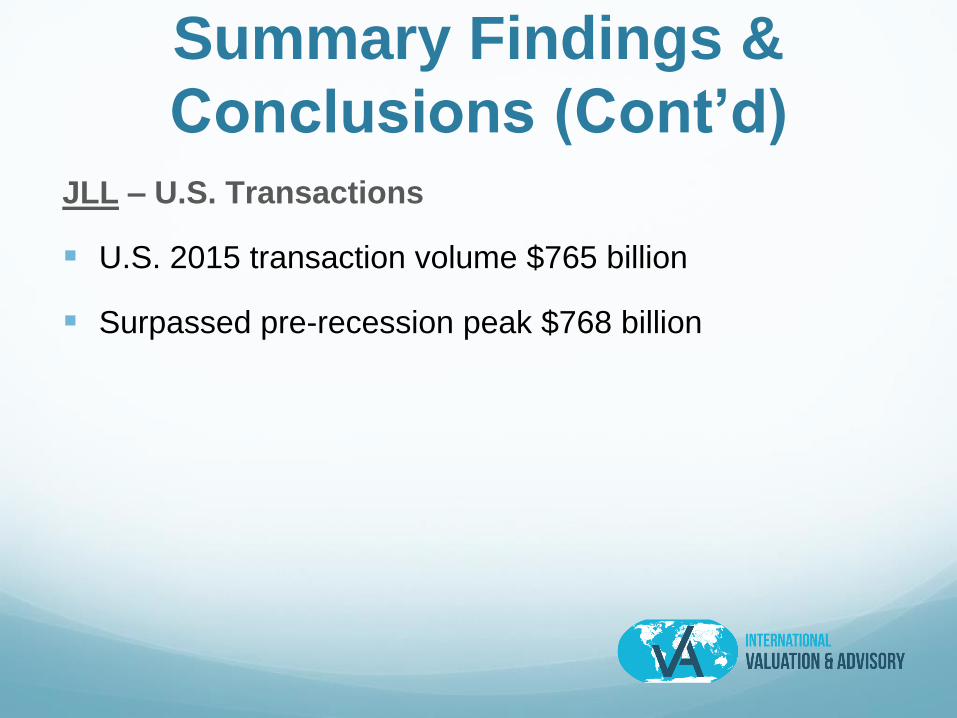

Conclusions (Cont’d)JLL – U.S. Transactions

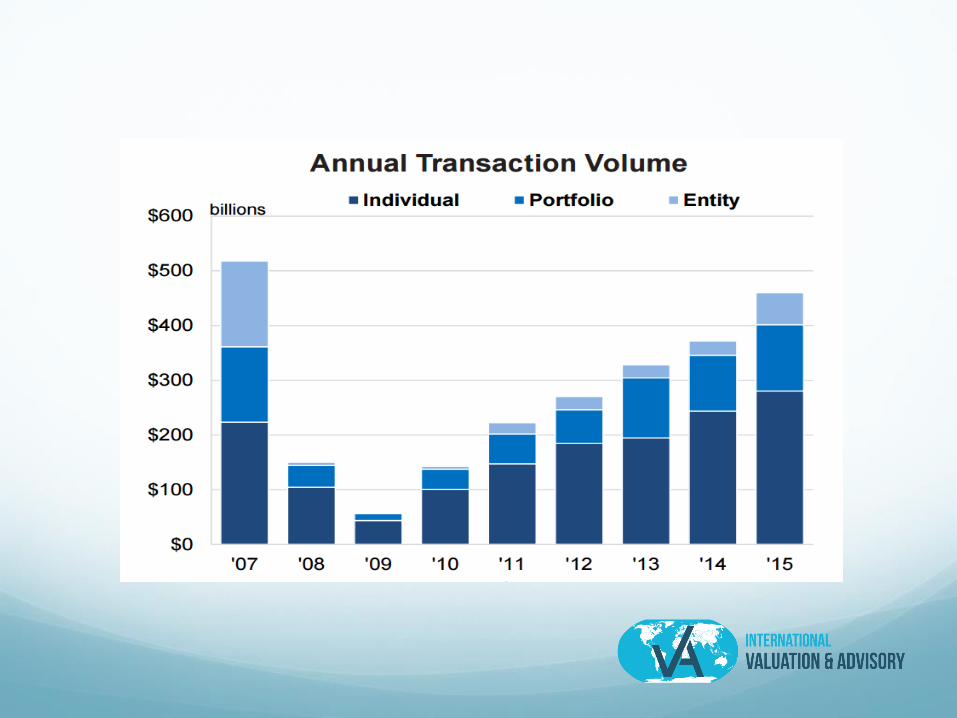

U.S. 2015 transaction volume $765 billion

Surpassed pre-recession peak $768 billion

The Analytics

RCA Data

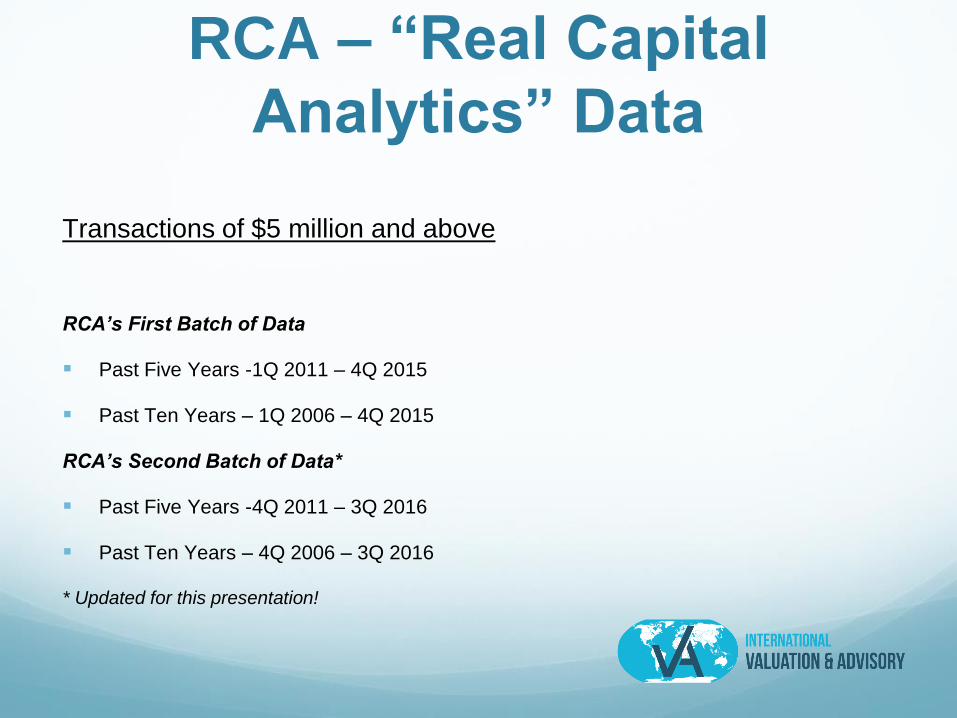

RCA – “Real Capital

Analytics” Data

Transactions of $5 million and above

RCA’s First Batch of Data

Past Five Years -1Q 2011 – 4Q 2015

Past Ten Years – 1Q 2006 – 4Q 2015

RCA’s Second Batch of Data*

Past Five Years -4Q 2011 – 3Q 2016

Past Ten Years – 4Q 2006 – 3Q 2016

* Updated for this presentation!

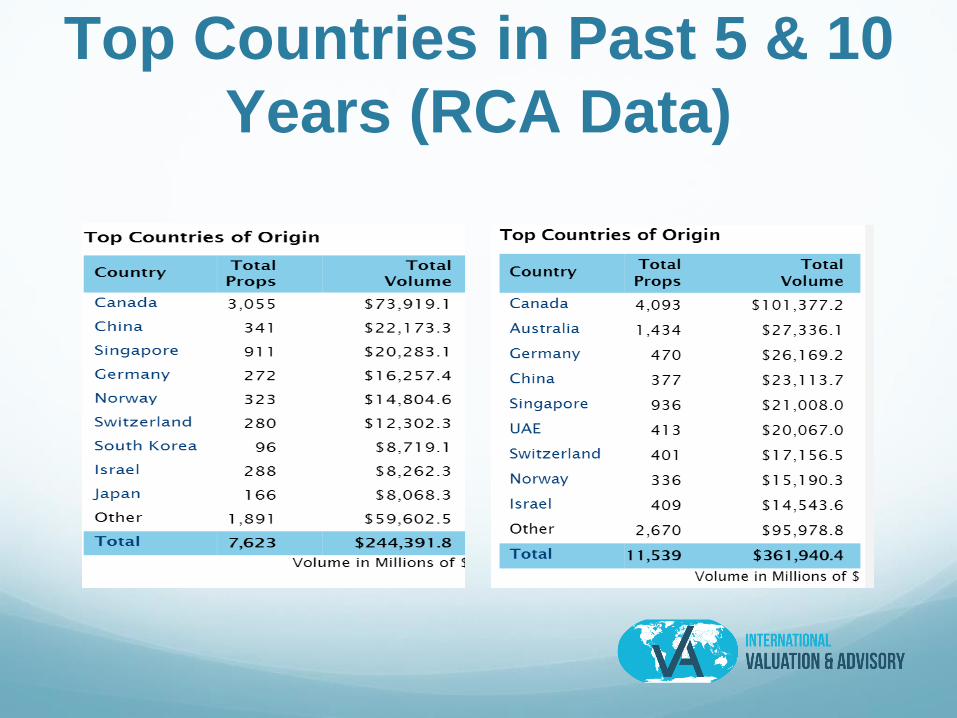

Top Countries in Past 5 & 10

Years (RCA Data)

Top Market Destinations

Past 5 & 10 Years

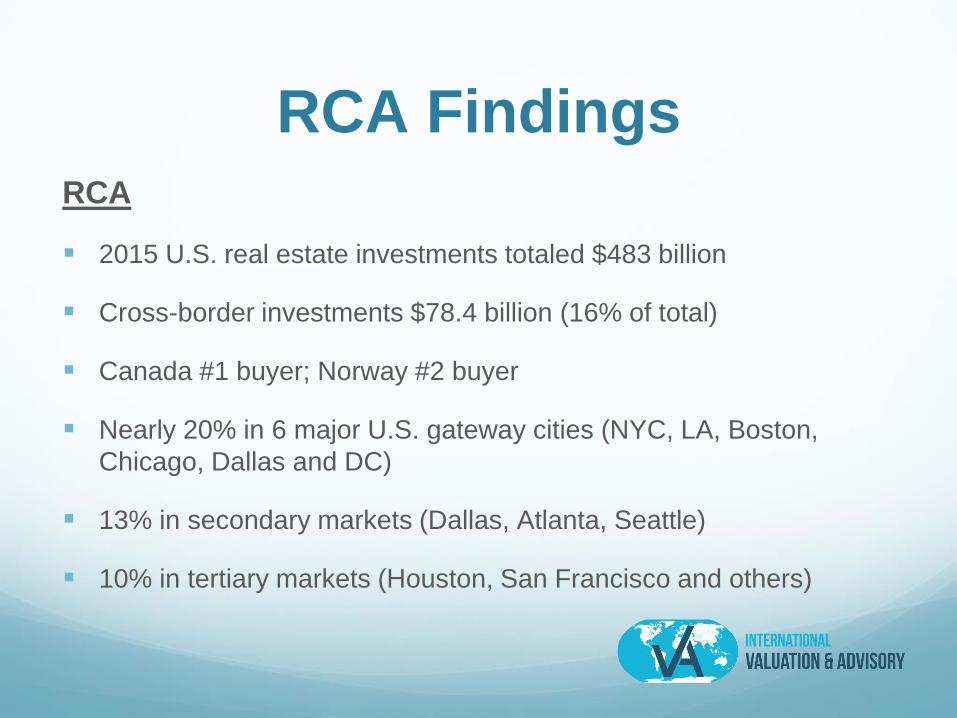

RCA FindingsRCA

2015 U.S. real estate investments totaled $483 billion

Cross-border investments $78.4 billion (16% of total)

Canada #1 buyer; Norway #2 buyer

Nearly 20% in 6 major U.S. gateway cities (NYC, LA, Boston,

Chicago, Dallas and DC)

13% in secondary markets (Dallas, Atlanta, Seattle)

10% in tertiary markets (Houston, San Francisco and others)

RCA Findings (Cont’d)Comparing 2006-2010 to 2011-2015

China, Singapore & Norway from $2.1 billion to $57.3

billion

Canada, Switzerland & Germany, from $41.9 billion to

$102.5 billion

Japan and S. Korea replaced Australia and UAE

Average deal size: $31.37 in 10-year & $32.66 in 5-year

terms

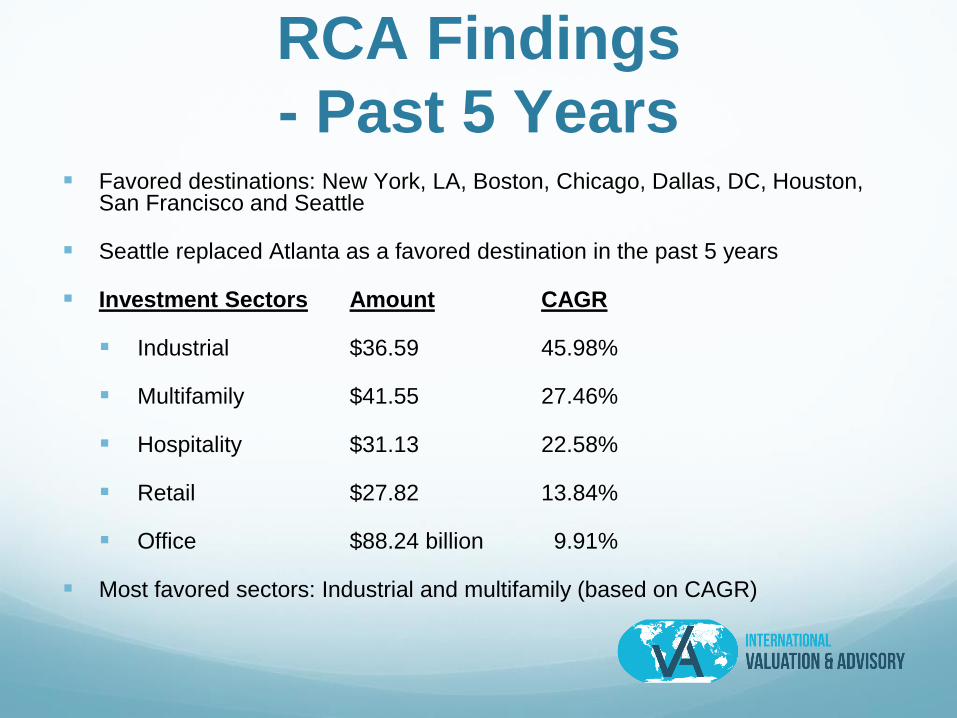

RCA Findings

- Past 5 Years Favored destinations: New York, LA, Boston, Chicago, Dallas, DC, Houston,

San Francisco and Seattle

Seattle replaced Atlanta as a favored destination in the past 5 years

Investment Sectors Amount CAGR

Industrial $36.59 45.98%

Multifamily $41.55 27.46%

Hospitality $31.13 22.58%

Retail $27.82 13.84%

Office $88.24 billion 9.91%

Most favored sectors: Industrial and multifamily (based on CAGR)

Offices - Top Countries

Past 5 & 10 Years

Offices – Top Destinations

Past 5 & 10 Years

Retail - Top Countries

Past 5 & 10 Years

Retail – Top Destinations

Past 5 & 10 Years

Industrial – Top Countries

Past 5 & 10 Years

Industrial - Top Destinations

Past 10 & 5 Years

Apartments – Top Countries

Past 10 & 5 Years

Apartments – Top Destinations

Past 10 & 5 Years

Hotels – Top Countries

Past 10 & 5 Years

Hotels – Top Destinations

Past 10 & 5 Years

Summary Findings &

ConclusionsCRE – Counselors of Real Estate

Funds continue to flow outside the countries to the U.S.

Driven by economies that have:

High savings rate

Shortage of mature financial markets

Shortage of investable assets

Summary Findings &

Conclusions (Cont’d)ULI - Urban Land Institute

Global capital is driven to U.S. property market

By global economic and political uncertainty

Because the U.S. is a safe haven

U.S. – the most stable market

U.S. - the most transparent market

Summary Findings &

Conclusions (Cont’d)AFIRE

Preferred property types

Multi-family

Industrial

Others

Retail

Office

Hotel

The Backdrop

A Mixed Environment

Challenging External

Influences (1Q 2016) Low commodity prices (e.g. oil)

Pressure on domestic budgets

Disinvestment and decreased 2016 capital outflow

Oil producers account for 40% of global savings

Overall glut of savings – cross-border investments

Negative interest rate environment – Japan & Europe

Mixed Global Environment -

Benefits U.S. Real Estate Monetary policies (QE in Europe)

Global economic and political reform agendas

Political developments (Elections in Europe; Brexit)

Lending policies and interest rates

China’s slowing economy – positive for outflow (?)

In 2015 Chinese spent $8.6 billion in U.S. – more

than 4X in 2014

Domestic Environment -

Favors U.S. Real Estate U.S. interest rate decision; effect on 10-year Treasuries

Yields in U.S. commercial real estate; competitive

(“super”) market

FIRPTA (Foreign Investment in Real Estate Property

Act, 1980) reform

Future View

2016 & BeyondCBRE:

U.S. real estate environment to remain positive

Investors have large amount of capital to deploy

Expect moderate yield compression

2016 & Beyond (Cont’d)Cushman & Wakefield:

Investment flows may be better in 2016

Low global interest rates

Global uncertainty & relative strength of U.S.

Strong property & currency markets

Strong supply of debt in U.S. market

4.2% increase in real estate trading volume

2016 & Beyond (Cont’d)AFIRE:

“The investment opportunity is the United States itself.”

Real estate fundamentals are sound

Economy remains strong

Opportunities across all sectors, in gateway and secondary cities

Recent legislation on FIRPTA taxes should provide additional incentives

“In an environment that is regarded both as the safest and most secure in the world, with a strong currency and the best opportunity for capital appreciation, the US is the safest harbor.”

- James A. Fetgatter, CEO of AFIRE

Talking Points

2016 & Beyond…?Debate on U.S. Real Estate Market (1Q, 2016)

Signs of severe downturn?

Is the market ripe for a correction?

Is this a periodic review of portfolios?

Is the market absorbing global uncertainties (e.g.

Brexit)?

2016 & Beyond…(Cont’d)Backdrop: 2015 U.S. Economic Environment (1Q 2016)

2.7 non-farms jobs created

13 million jobs since economic recession

Unemployment rate at 4.9% (in Feb. 2016)

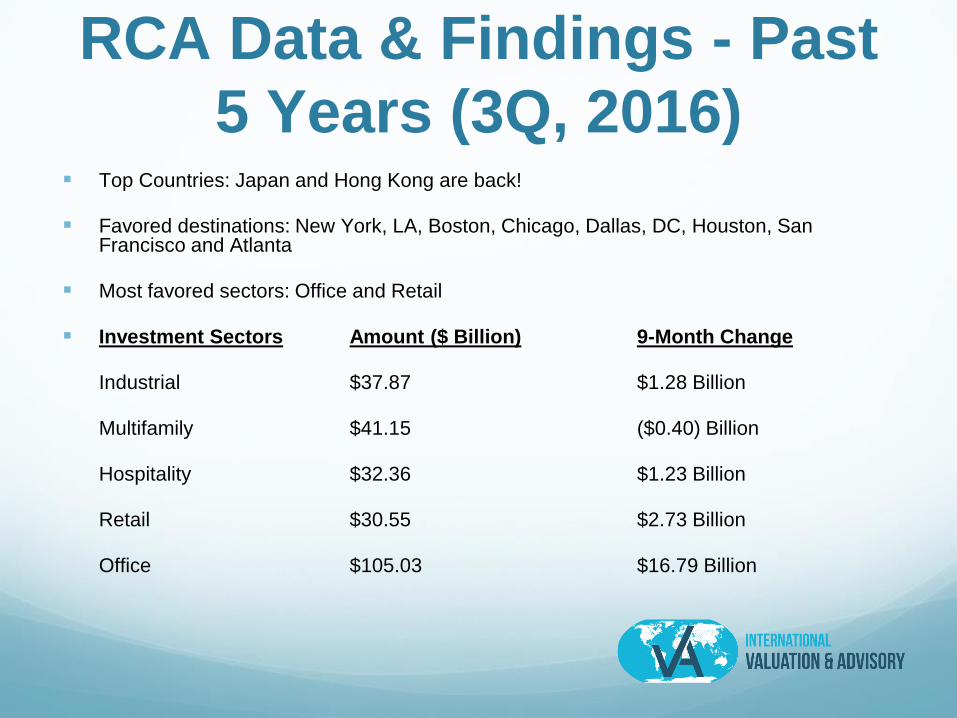

RCA Data & Findings - Past

5 Years (3Q, 2016) Top Countries: Japan and Hong Kong are back!

Favored destinations: New York, LA, Boston, Chicago, Dallas, DC, Houston, San Francisco and Atlanta

Most favored sectors: Office and Retail

Investment Sectors Amount ($ Billion) 9-Month Change

Industrial $37.87 $1.28 Billion

Multifamily $41.15 ($0.40) Billion

Hospitality $32.36 $1.23 Billion

Retail $30.55 $2.73 Billion

Office $105.03 $16.79 Billion

Top Countries

Past 5 & 10 Years (3Q, 2016)

Top Destinations

Past 5 & 10 Years (3Q, 2016)

2016 & Beyond - 3Q 2016Red Flag – Signs of Slowdown

RCA’s Year-over-year Picture

Deal volume in U.S. fell 46% (on Year-over-Year sales

of $25.5 billion)

Single-asset sales down 26% (on sales of $18.8 billion)

Industrial sales down 78%

Hotel (hospitality) sales down 73%

Conclusion Cross-border real estate investing - compelling risk-

return trade-off on long-term capital commitment

Uncertain global socio-economic political changes

(e.g. Brexit)

Unexpected policy changes (e.g., interest rate)

Currency fluctuations and trade competitiveness

Tax environments (e.g., investment incentives)

U.S.: Large, established, stable, transparent market

“In the increasingly unstable global eco-

political atmosphere, foreign investors will

seek more certainty on returns and

reallocate saving surpluses to seek U.S.

growth opportunities.”

- Tony D’Silva Kamath, MAI, MRICS, Principal, International

Valuation & Advisory LLC

Thank You!

Steven Williams, Real Capital Analytics

FENG – Financial Executives Network Group

&

Tom McFarland, Hinduja Group Offices, New York, NY

Tony D. Kamath, MAI, MRICS

Phone: 917-558-1945

International Valuation & Advisory LLC

www.InternationalValuation.com

Note: The opinions expressed in this presentation are the author’s only.