Embed Size (px)

Citation preview

Foreign Tax CreditSome Illustrations

Part of Presentation Paper

At

Chamber of Tax Consultants’ RRC

June 24, 2017

Yogesh Thar

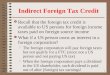

ORDINARY CREDIT V/S FULL CREDIT

3

ORDINARY CREDIT v/s FULL CREDIT

Particulars Ordinary credit method Full credit method

Total income 100 100

Income from COS 20 20

Tax liability in COS (@ 35%) 7 7

Tax liability in COR @ 30%

(without considering credit)30 30

Less: Tax credit available in COR 6* 7

Net liability in COR 24 23

* 30% of 20

UNDERLYING TAX CREDIT

5

UNDERLYING TAX CREDIT

Tax outflow (in COS) Tax outflow for the shareholder (in COR)

Profits before tax 100 Dividend received 70

Tax @ (say) 30% 30 Corporate tax attributable 30

Net taxable profit 70 Dividend gross up 100

Dividend paid (assume entire) 70 Tax @ 40% 40

Tax on dividend @ (say)10% 7 Credit for the underlying tax 30

Credit for tax on dividend paid in COS 7

TAX CREDIT u/s. 91

Overview:

Section 91 provides foreign tax credit to a resident taxpayer in respect offoreign taxes paid on his foreign income earned in a country with which Indiahas not entered into any DTAA.

Computation Mechanism:A x B

OR

A x C

Whichever is lower

Where:

A = Doubly Taxed Income.

B = Indian Rate of Tax

C = Foreign Tax Rate

7

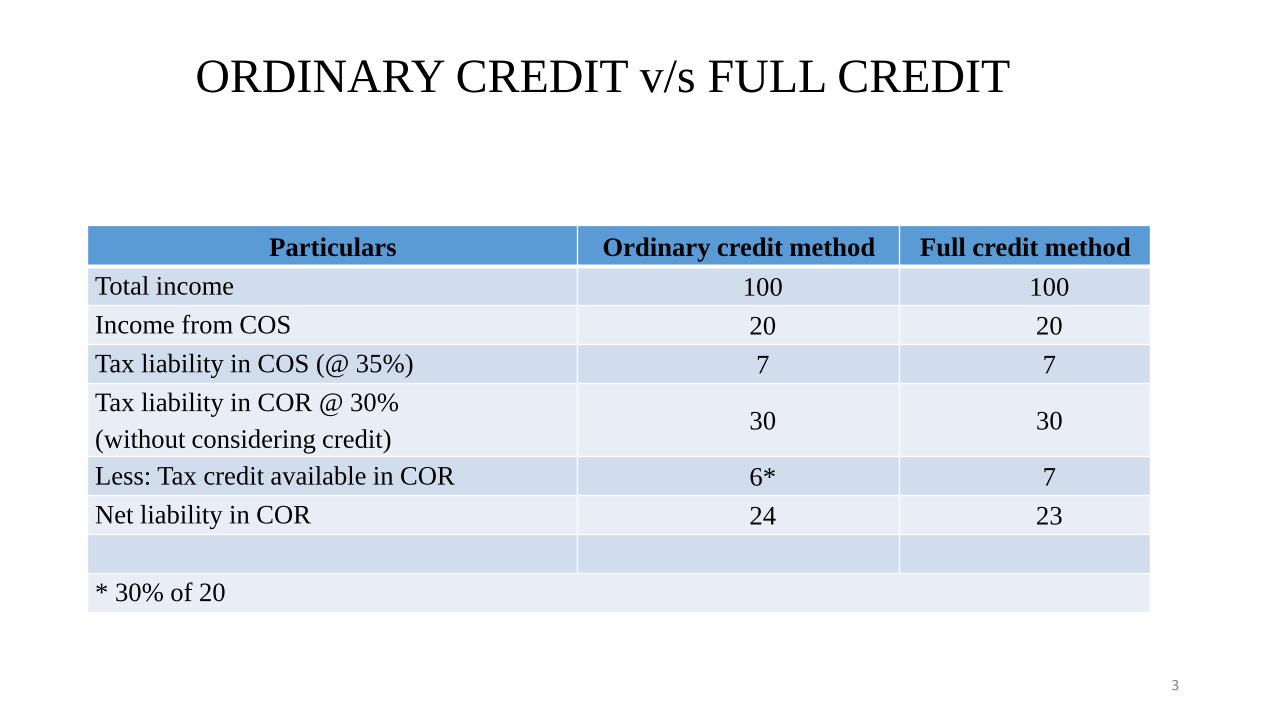

TAX CREDIT U/S 91

Illustration:

8

TAX CREDIT U/S 91 (contd…)

Particulars Amount

(a) Commercial Income earned in Country X by a resident of India USD 100

(b) Taxable income in Country X after all deductions and reliefs under

its domestic law

USD 70

(c) Tax Rate in Country X 30%

(d) Tax paid in Country X ( b x c ) USD 21

(e) Country X income is the only income. With no other Indian Income,

assuming

Fx conversion @ Rs. 65 /USD, Total Income under the Indian law, after

claiming deductions of, say, Rs. 1500 = 6500 – 1500

Rs. 5,000

(f) Tax in India on TI of Rs. 5000 (@ say, 35%) Rs. 1,750

What would be the quantum of FTC available under section 91 of the Act?

Illustration:

Considering that the doubly taxed income is Rs. 5000, because it is also a subject matter of taxationin Country X, and applying the aforesaid formula, the deduction may work out to Rs. 1500, i.e. 5000x 21 / 70. However, the actual tax paid in Country X is only Rs. 1365 (i.e. 21 x 65)! Is this correct? Oris there an issue of interpretation of the term “doubly taxed income”?

9

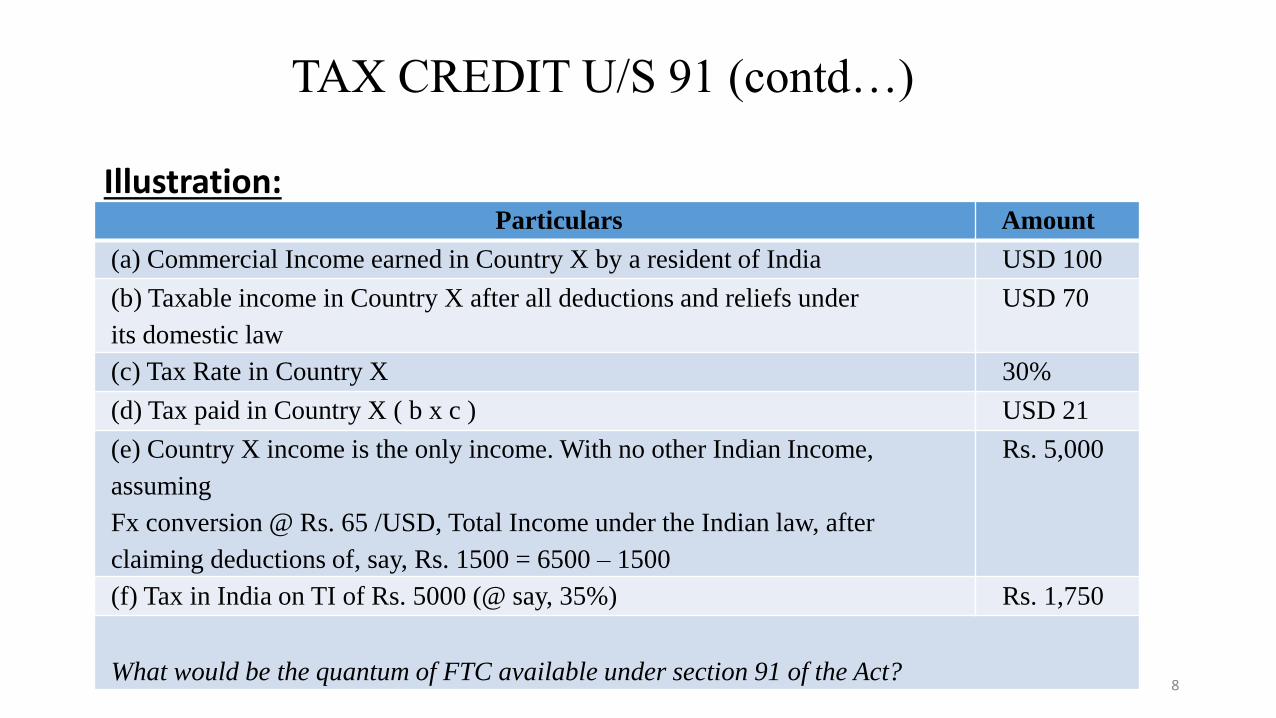

TAX CREDIT U/S 91 (contd…)

Illustration:

Issue:

Whether the doubly taxed income was an amount after claiming weighted deduction u/s. 35B orbefore claiming said deduction?

Solution:

The Hon’ble Madras High Court in the case of CIT v. Best and Crompton Engg. Ltd. (284 ITR 225) hasheld that “income” for the purpose of section 91 would be the income computed in the normalsense before adjustment of deduction u/s 35B.

Considering the said decision, the quantum is worked out as follows:

10

TAX CREDIT U/S 91 (contd…)

Illustration:

11

TAX CREDIT U/S 91 (contd…)

Particulars Amount

(a) Doubly taxed income – being the commercial income USD 100

(b) Tax in Country X USD 21

(c) Tax in India ₹ 1,750

(d) Foreign Tax Rate 21%

(e) India Tax Rate 26.92%

(f) FTC on (a) = (a x d) [(d) being lower than (e)] ₹ 1,365

Branch Profits Tax

Branch Profit Tax – whether tax credit available?• Indian Company (I.Co.) has subsidiary in (say) U.S. (S.Co.)

• I.Co.’s Profits :Rs. 200

• S.Co.’s Profits :Rs. 100

• Indian Tax @ 30% :Rs. 60

• US Tax @ 35% :Rs. 35

• Dividend Paid (100-35) :Rs. 65

• US Tax on Dividend (@15%) :Rs. 9.75

• Indian Tax on US Dividend (@15%) :Rs. 9.75

• Total Indian Tax (60+9.75) :Rs. 69.75

• Less FTC in India (on Dividend) :Rs. 9.75

• Net Tax payable in India :Rs. 60

• Total Tax (US 35+9.75, India 60) :Rs. 104.50

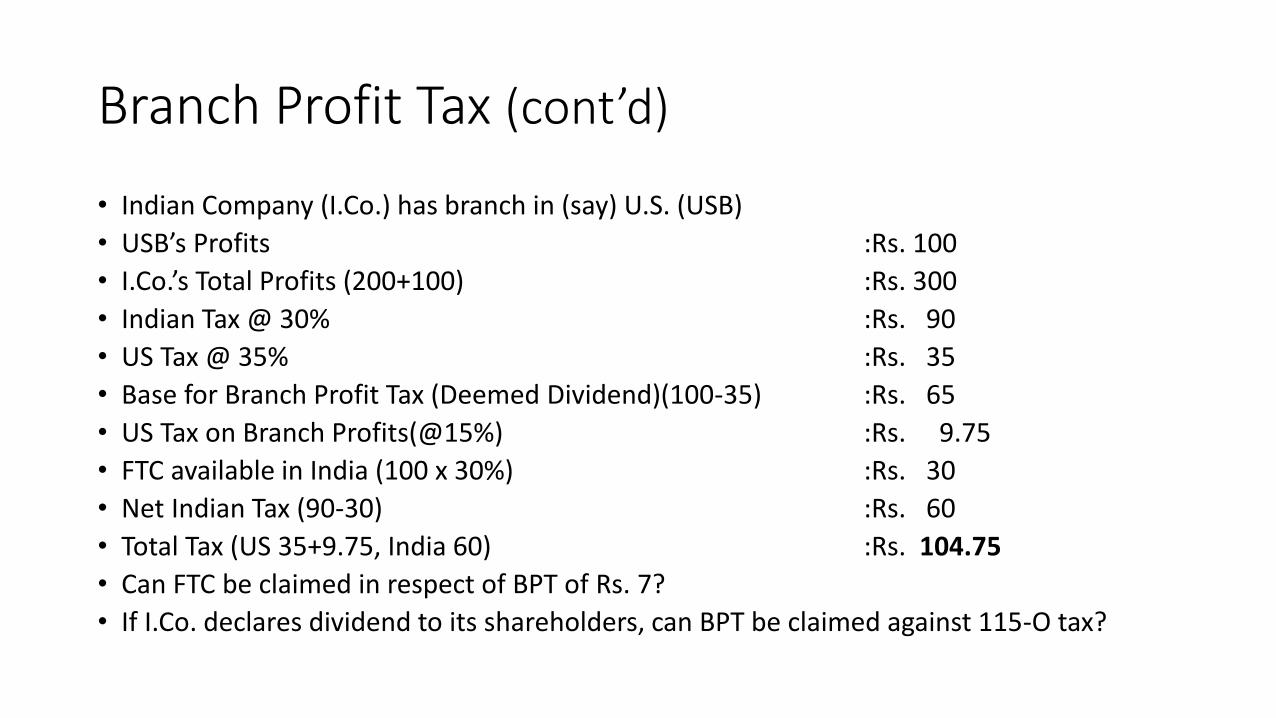

Branch Profit Tax (cont’d)

• Indian Company (I.Co.) has branch in (say) U.S. (USB)

• USB’s Profits :Rs. 100

• I.Co.’s Total Profits (200+100) :Rs. 300

• Indian Tax @ 30% :Rs. 90

• US Tax @ 35% :Rs. 35

• Base for Branch Profit Tax (Deemed Dividend)(100-35) :Rs. 65

• US Tax on Branch Profits(@15%) :Rs. 9.75

• FTC available in India (100 x 30%) :Rs. 30

• Net Indian Tax (90-30) :Rs. 60

• Total Tax (US 35+9.75, India 60) :Rs. 104.75

• Can FTC be claimed in respect of BPT of Rs. 7?

• If I.Co. declares dividend to its shareholders, can BPT be claimed against 115-O tax?

MAT & FTC

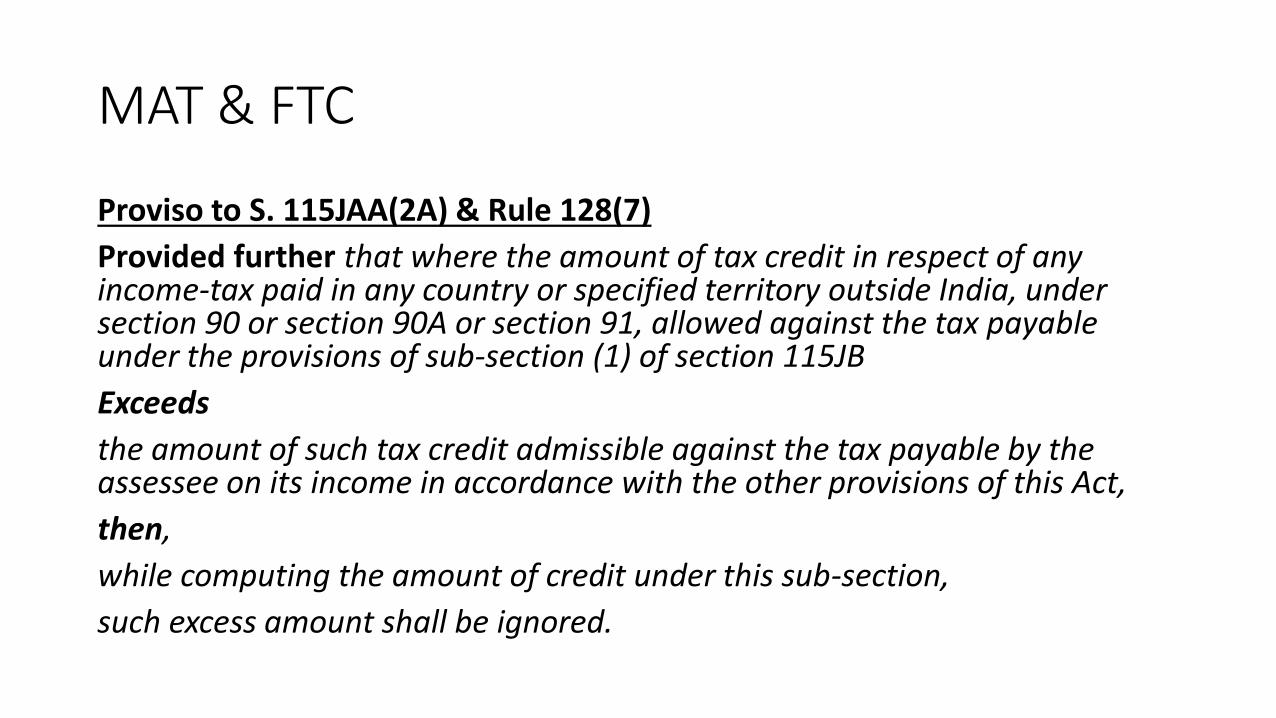

MAT & FTC

Proviso to S. 115JAA(2A) & Rule 128(7)

Provided further that where the amount of tax credit in respect of any income-tax paid in any country or specified territory outside India, under section 90 or section 90A or section 91, allowed against the tax payable under the provisions of sub-section (1) of section 115JB

Exceeds

the amount of such tax credit admissible against the tax payable by the assessee on its income in accordance with the other provisions of this Act,

then,

while computing the amount of credit under this sub-section,

such excess amount shall be ignored.

MAT & FTC (cont’d)

Particulars Book Profits Tax on Book Profits

NormalComputation

Tax on Normal Computation

Dividend from Foreign Subsidiary 100 100 15

Indian Source Income 200 100 30

Total 300 55.50 200 45

Less: FTC (Assume Foreign tax =20) 18.50 15

Net Tax Payable 37.00 30

MAT Credit u/s. 115JAA(2A) 7

Excess MAT Credit (=18.50 – 15 ) 3.50

MAT Credit Allowable ( = 7 – 3.50) 3.50

Rule 128

Source-by-source & Country-by-country Rule

Rule 128(5): Does it override the Act?

Source Country X Income

Country X Income-tax

IndiaIncome

IndiaIncome-tax

S-by-S; C-by-C FTC

Royalty 100 10

Less: Exps 20 80 24 8

Dividend 100 20 100 15 15

Total 200 30 180 39 23

Rate of Tax : 30 / 200= 15%

39 / 180= 21.67%

FTC u/s. 91 = 180 x 15% = 27

Loss due to Rule 128(5):

= 27 - 23 4

Thank you