Embed Size (px)

Citation preview

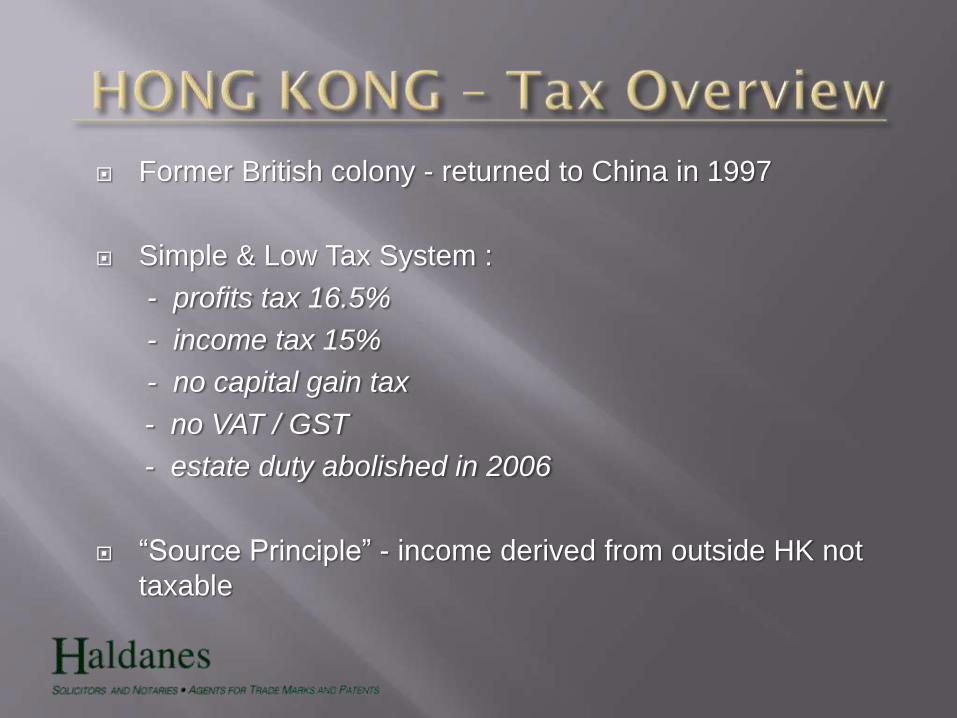

Former British colony - returned to China in 1997

Simple & Low Tax System :

- profits tax 16.5%

- income tax 15%

- no capital gain tax

- no VAT / GST

- estate duty abolished in 2006

“Source Principle” - income derived from outside HK not

taxable

More comprehensive & complicated system

- 26 types of taxes of 7 categories

Higher tax rate

- Enterprise income tax (25% average)

- Individual income tax (5 to 45%)

US crackdown on Swiss banks in 2009 for tax evasion– UBS case

(i) Jeffrey Chernick case

(ii) Roberto Cittadini case

- Hid income using HK shell companies

Problem: Nominee Accounts

Easy to set up nominee & trust accounts - obscure

ownership & control of assets

(i) Tax-avoider/evader - act as director & shareholder

(ii) Engage company secretarial companies - act as

directors & provide nominee shareholders

Legislation: Inland Revenue Ordinance (“IRO”)

Authority: Inland Revenue Department (“IRD”)

General anti-avoidance provision - modeled on

the Australian Tax Acts.

s. 61 IRO - “any transaction, which reduces or

would reduce the amount of tax payable by any

person, is artificial or fictitious; or that any

disposition is not in fact given effect to, the

assessor may disregard any such transaction

or disposition and the person concerned shall

be assessable accordingly”

s. 61A IRO: “any transaction entered into, and that

transaction has the effect of conferring a tax

benefit on a person, and, having regard to all

circumstances of transaction, …..the person did so

for the sole or dominant purpose to obtain a tax

benefit”

Result: IRD can ignore these artificial transactions

& tax accordingly

“Any person who willfully with intent to evade or assist any other person to evade tax, commit acts of tax evasion such as omitting anything in a return which should be included, making any false statement or entry in any return, preparing or maintaining any false books”

Imprisonment / fine

A further fine of 3 times the tax undercharged

Brief Facts

HIT Finance issued debentures (Floating Rate Notes “FRN”) in Luxembourg Stock Exchange

Self-subscription of 2/3 of Luxembourg FRNs

“Round-robin” of funds transfer within the group

HIT claimed interest deduction for issuing FRNs – rejected by IRD for s. 61A “Sole & dominant purpose for tax benefit”

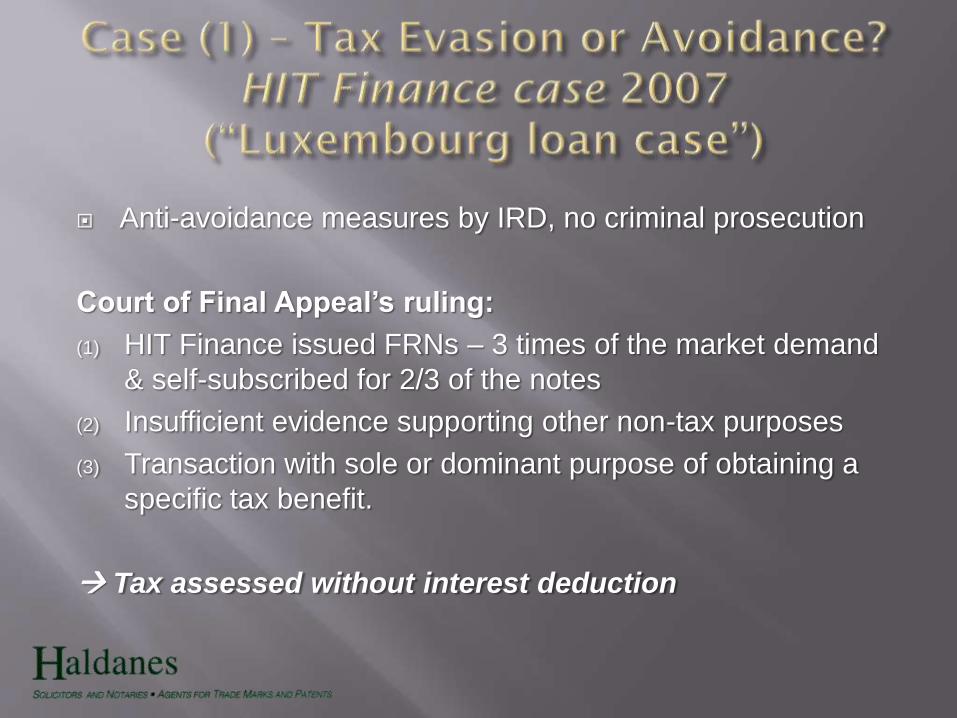

Anti-avoidance measures by IRD, no criminal prosecution

Court of Final Appeal’s ruling:

(1) HIT Finance issued FRNs – 3 times of the market demand

& self-subscribed for 2/3 of the notes

(2) Insufficient evidence supporting other non-tax purposes

(3) Transaction with sole or dominant purpose of obtaining a

specific tax benefit.

Tax assessed without interest deduction

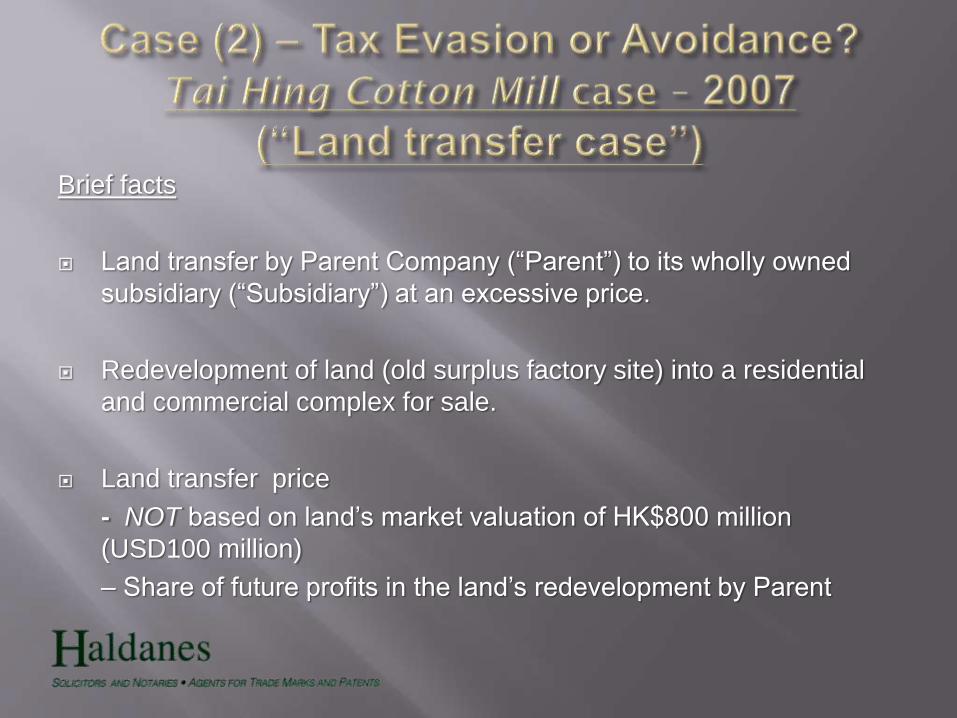

Brief facts

Land transfer by Parent Company (“Parent”) to its wholly owned

subsidiary (“Subsidiary”) at an excessive price.

Redevelopment of land (old surplus factory site) into a residential

and commercial complex for sale.

Land transfer price

- NOT based on land’s market valuation of HK$800 million

(USD100 million)

– Share of future profits in the land’s redevelopment by Parent

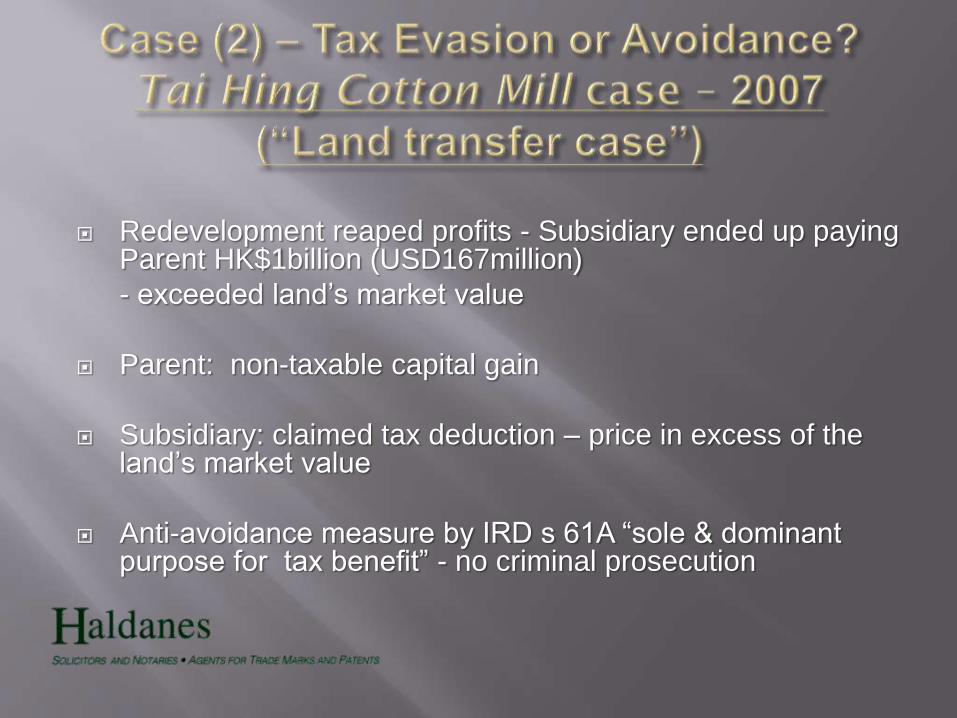

Redevelopment reaped profits - Subsidiary ended up paying Parent HK$1billion (USD167million)

- exceeded land’s market value

Parent: non-taxable capital gain

Subsidiary: claimed tax deduction – price in excess of the land’s market value

Anti-avoidance measure by IRD s 61A “sole & dominant purpose for tax benefit” - no criminal prosecution

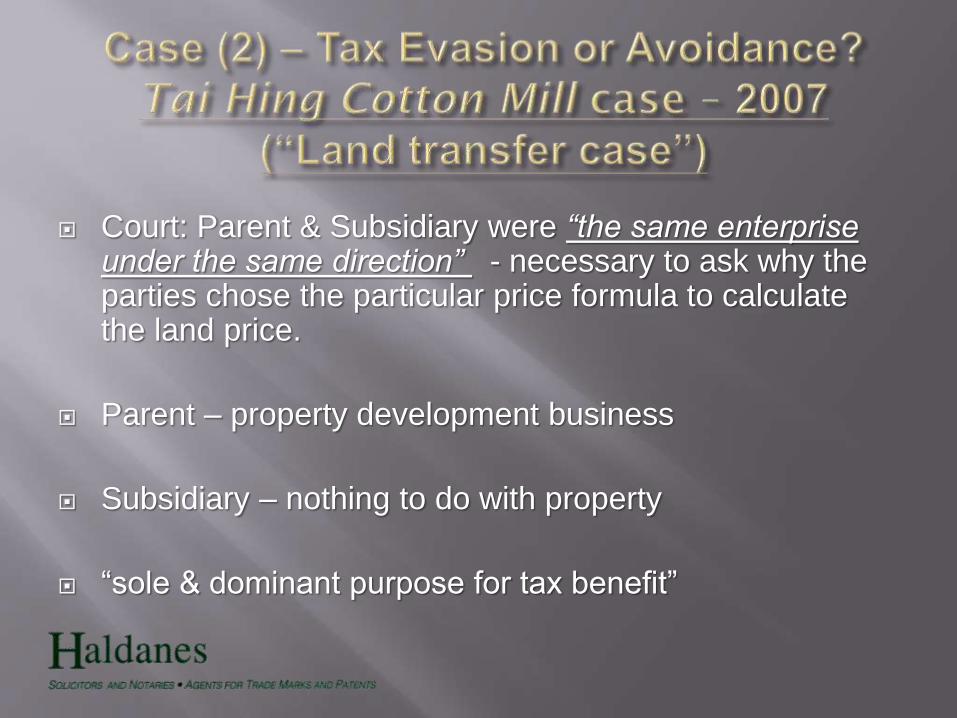

Court: Parent & Subsidiary were “the same enterprise under the same direction” - necessary to ask why the parties chose the particular price formula to calculate the land price.

Parent – property development business

Subsidiary – nothing to do with property

“sole & dominant purpose for tax benefit”

Ms. Pamela Pak – renowned radio talk

show host & celebrity in HK

Criminal prosecution by IRD

Brief Facts

Pak’s radio program income from 1994 to 1997

transferred to a service company owned by Pak

No commercial activity by company

Falsely reported an employee as company’s PR

assistant

False & altered restaurant receipts

Inflated entertainment & employee benefits

Omission of contractual bonus in tax return

IRD prosecuted Pak with 4 charges on tax

evasion / filing fraudulent Profits Tax Returns

Result:

- Imprisonment of 3 months upon guilty plea

- Fine of HK$200,000 (USD 30,000)

Distinction between tax avoidance & tax evasion is not

clear

Wide spectrum:

- full honest disclosure fraudulent concealment

Hallmarks of HK Tax Crimes

(i) fraudulent concealment, esp. with forged documents

(ii) blatant cases of willful concealment criminal

prosecution