Embed Size (px)

Citation preview

Juan Manuel Gers, PhD

FORO MEJORES PRÁCTICAS EN INTERNACIONALIZACIÓN

Medellin, Noviembre 27, 2013

Company Profile

We are a group with more than 32 years experience providing

Consulting Services in Electrical Engineering and associated

areas.

GERS has been involved in the completion of projects of all sizes

and complexity for utilities, industrial and commercial organizations

in four continents over the past three decades.

GERS

COVERAGE

GERS

Estados Unidos - Florida

Colombia - Bogotá

- Barranquilla

- Cali

- Villavicencio

Ecuador - Quito Chile – Santiago de Chile

México - Ciudad de México

FACILITIES

A

ECUADOR

PROJECT MANAGEMENT

MÉXICO

STUDIES

USA

STUDIES

DESIGNS

COLOMBIA

STUDIES

DESIGNS

TESTS &COMMISSIONING

SMART GRIIDS

GENERAL

MANAGEMENT

PRESIDENCY

CHILE

PROJECT MANAGEMENT

ORGANIZATIONAL CHART

Multilateral Banks

creo que deberías resaltar las actividades con organismos multilaterales y el crecimiento de nuevas alianzas internacionales con empresas internacionales, como India, Bangaldesh, Brazil y otras Organismos como World Bank, IDB (InterAmerican Development Bank), USTDA (US Trade and Development Agency) otras entidades privadas US DOIE DOE IFC

Regional Development Banks

UNION EUROPEA

FINANCE INSTITUTIONS

International Alliances

Government Institutions

WORKING OPPORTUNITIES

State license

County occupational license

City occupational license

City certificate of use

Professional Engineer

Minority Certification

Small Business

Company Licensing

GERS

FREE TRADE AGREEMENT

On October 21, 2011, President Obama signed the U.S.-Colombia FTA. “We welcome today’s signing of the FTA, which brings Colombia and the United States one step closer to the entry into force of this historic agreement.

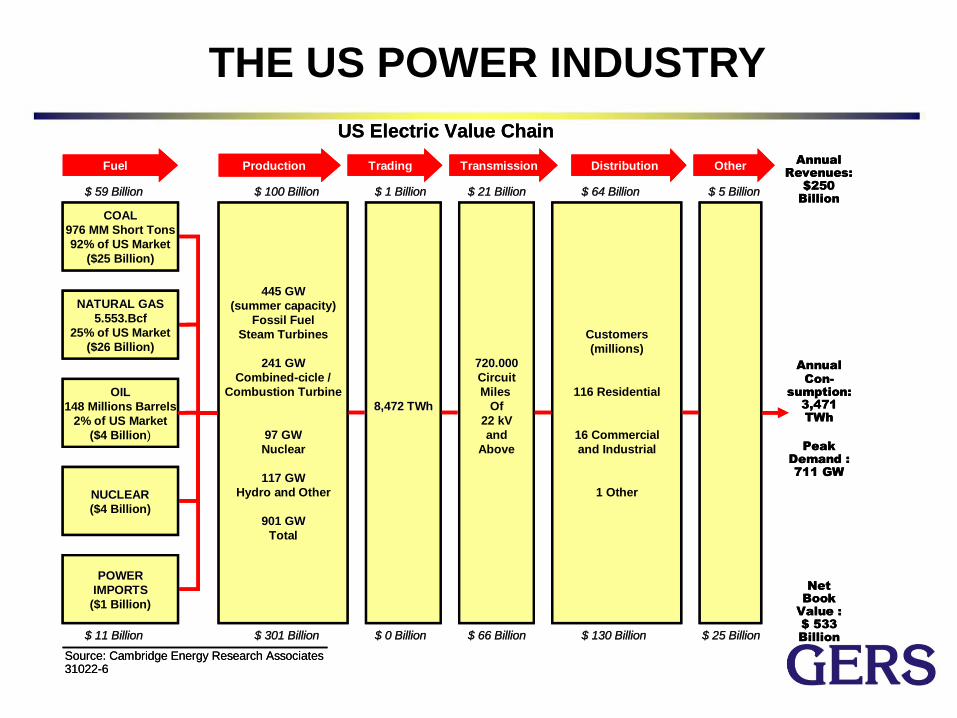

THE US POWER INDUSTRY

COALCOAL

976 MM Short Tons

92% of US Market

($25 Billion)

NATURAL GASNATURAL GAS

5.553.Bcf

25% of US Market

($26 Billion)

OILOIL

148 Millions Barrels

2% of US Market

($4 Billion)

NUCLEARNUCLEAR

($4 Billion)

POWERPOWER

IMPORTSIMPORTS

($1 Billion)

445 GW445 GW

(summer capacity)

Fossil Fuel

Steam Turbines

241 GW241 GW

Combined-cicle /

Combustion Turbine

97 GW97 GW

Nuclear

117 GW117 GW

Hydro and Other

901 GW901 GW

Total

8,472 8,472 TWhTWh

720.000720.000

Circuit

Miles

Of

22 kV

and

Above

CustomersCustomers

(millions)

116 Residential

16 Commercial

and Industrial

1 Other

$ 11 $ 11 BillionBillion $ 301 $ 301 BillionBillion $ 0 $ 0 BillionBillion $ 66 $ 66 BillionBillion $ 130 $ 130 BillionBillion $ 25 $ 25 BillionBillion

$ 59 $ 59 BillionBillion $ 100 $ 100 BillionBillion $ 1 $ 1 BillionBillion $ 21 $ 21 BillionBillion $ 64 $ 64 BillionBillion $ 5 $ 5 BillionBillion

TradingProductionFuel Transmission Distribution OtherAnnual

Revenues:

$250

Billion

Annual

Con-

sumption:

3,471

TWh

Peak

Demand :

711 GW

Net

Book

Value :

$ 533

Billion

Source: Cambridge Energy Research Associates31022-6

US Electric Value Chain

COALCOAL

976 MM Short Tons

92% of US Market

($25 Billion)

NATURAL GASNATURAL GAS

5.553.Bcf

25% of US Market

($26 Billion)

OILOIL

148 Millions Barrels

2% of US Market

($4 Billion)

NUCLEARNUCLEAR

($4 Billion)

POWERPOWER

IMPORTSIMPORTS

($1 Billion)

445 GW445 GW

(summer capacity)

Fossil Fuel

Steam Turbines

241 GW241 GW

Combined-cicle /

Combustion Turbine

97 GW97 GW

Nuclear

117 GW117 GW

Hydro and Other

901 GW901 GW

Total

8,472 8,472 TWhTWh

720.000720.000

Circuit

Miles

Of

22 kV

and

Above

CustomersCustomers

(millions)

116 Residential

16 Commercial

and Industrial

1 Other

$ 11 $ 11 BillionBillion $ 301 $ 301 BillionBillion $ 0 $ 0 BillionBillion $ 66 $ 66 BillionBillion $ 130 $ 130 BillionBillion $ 25 $ 25 BillionBillion

$ 59 $ 59 BillionBillion $ 100 $ 100 BillionBillion $ 1 $ 1 BillionBillion $ 21 $ 21 BillionBillion $ 64 $ 64 BillionBillion $ 5 $ 5 BillionBillion

TradingProductionFuel Transmission Distribution OtherAnnual

Revenues:

$250

Billion

Annual

Con-

sumption:

3,471

TWh

Peak

Demand :

711 GW

Net

Book

Value :

$ 533

Billion

Source: Cambridge Energy Research Associates31022-6

US Electric Value Chain

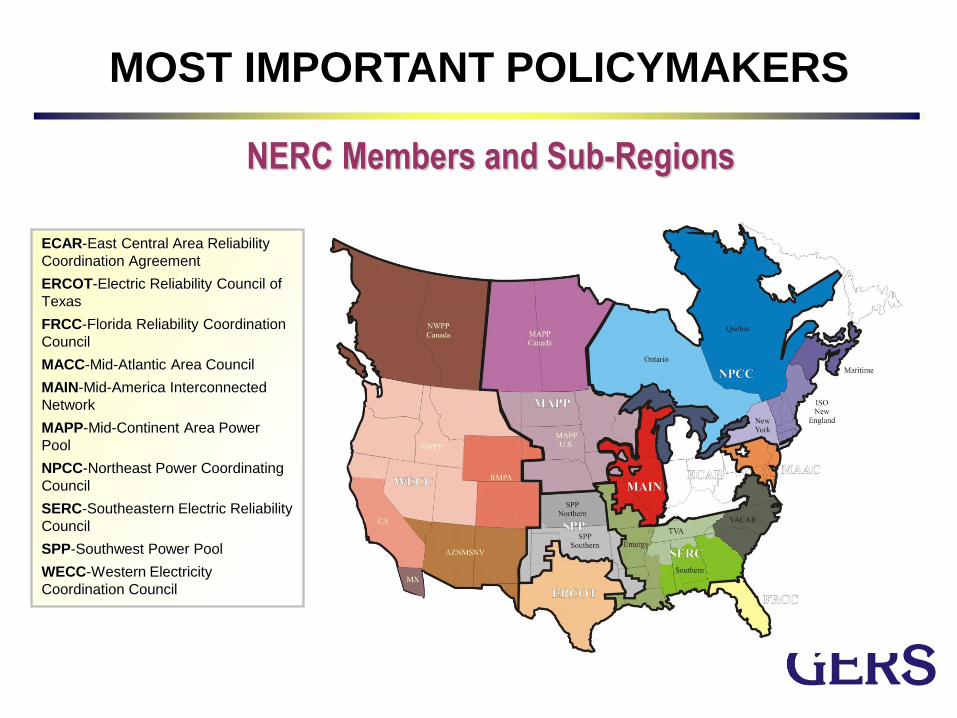

NERC Members and Sub-Regions

ECAR-East Central Area Reliability

Coordination Agreement

ERCOT-Electric Reliability Council of

Texas

FRCC-Florida Reliability Coordination

Council

MACC-Mid-Atlantic Area Council

MAIN-Mid-America Interconnected

Network

MAPP-Mid-Continent Area Power

Pool

NPCC-Northeast Power Coordinating

Council

SERC-Southeastern Electric Reliability

Council

SPP-Southwest Power Pool

WECC-Western Electricity

Coordination Council

MOST IMPORTANT POLICYMAKERS

OVERVIEW OF THE ELECTRIC

INDUSTRY IN THE UNITED STATES

The U.S. electric system

Over 200 million customers participating in an deregulated market

Over 3200 utilities

Over 16,802 generators in commercial operation

Over 155,000 miles of transmission lines (230 kV and above)

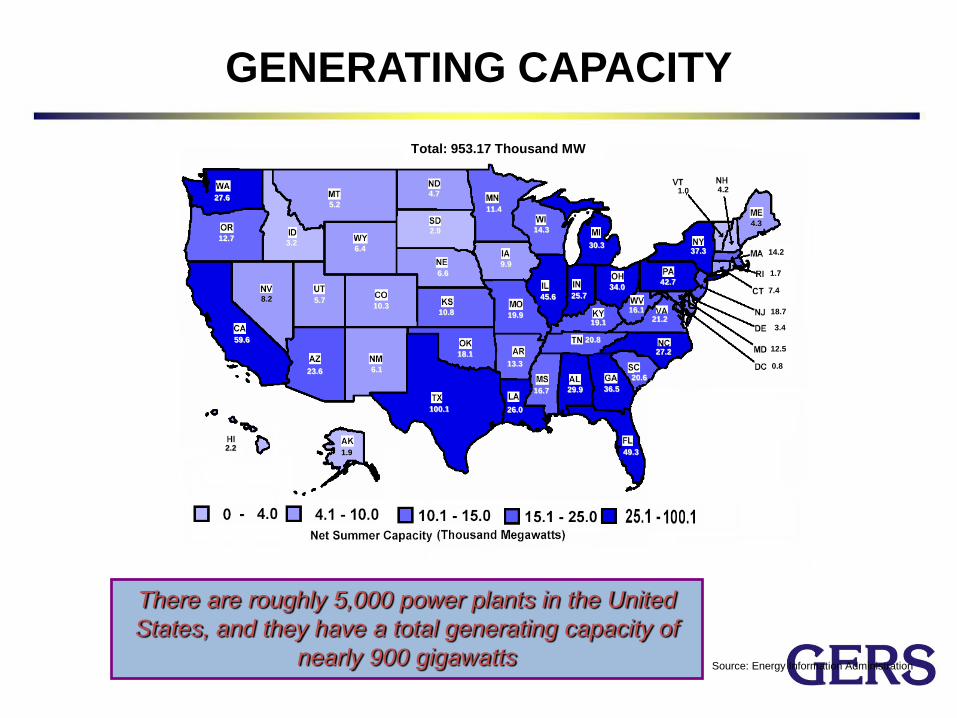

GENERATING CAPACITY

There are roughly 5,000 power plants in the United

States, and they have a total generating capacity of

nearly 900 gigawatts Source: Energy Information Administration

29.9

1.9

23.6 13.3

59.6

10.3

7.4

3.4

0.8

49.3

36.5

2.2

3.2

45.6 25.7

9.9

10.8

19.1

26.0

4.3

12.5

14.2 30.3

11.4

16.7

19.9

5.2

6.6

8.2

4.2

18.7

6.1

37.3

27.2

4.7

34.0

18.1

12.7

42.7 1.7

20.6

2.9

20.8

100.1

5.7

1.0

21.2

27.6

16.1

14.3

6.4

Total: 953.17 Thousand MW

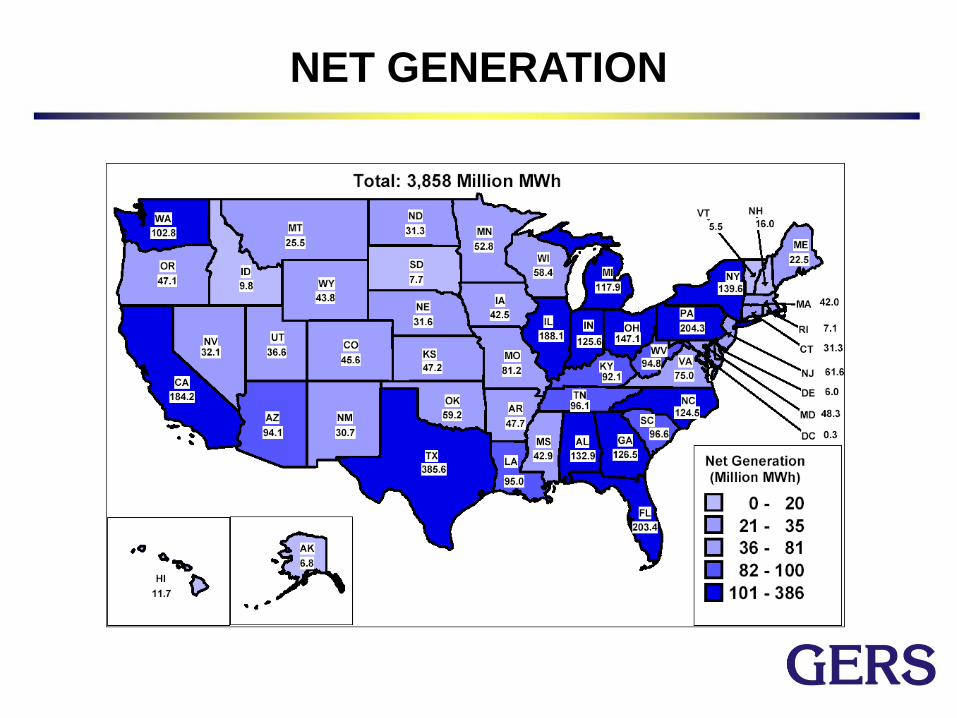

NET GENERATION

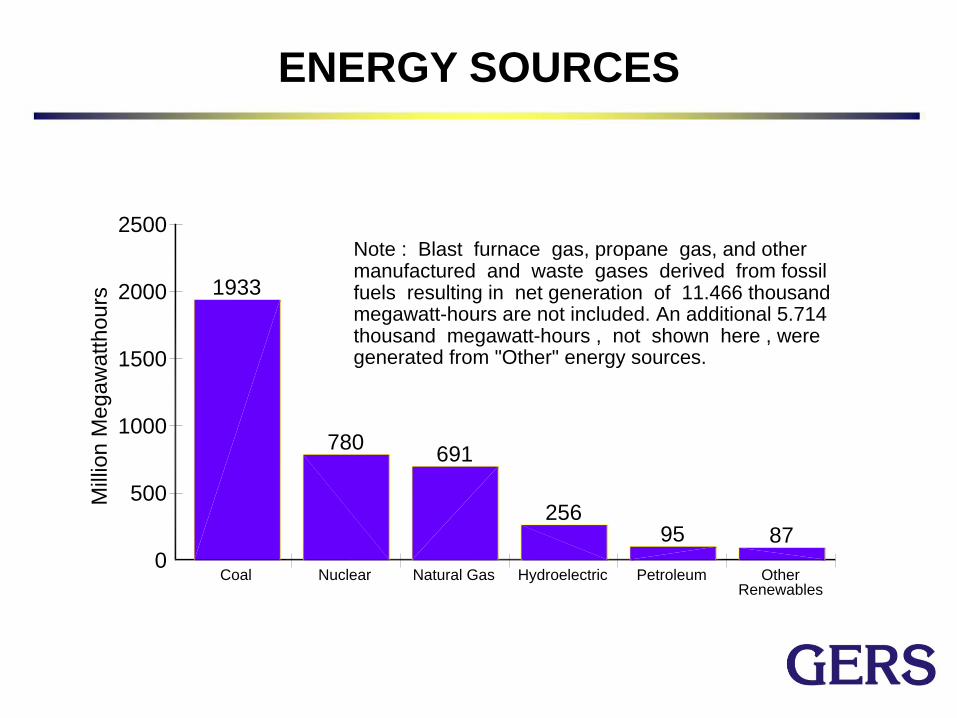

ENERGY SOURCES

1933

780691

25695 87

Coal Nuclear Natural Gas Hydroelectric Petroleum OtherRenewables

2000

2500

1000

500

0

1500

Note : Blast furnace gas, propane gas, and othermanufactured and waste gases derived from fossilfuels resulting in net generation of 11.466 thousand

thousand megawatt-hours , not shown here , were megawatt-hours are not included. An additional 5.714

generated from "Other" energy sources.

Mill

ion

Me

ga

wa

tth

ou

rs

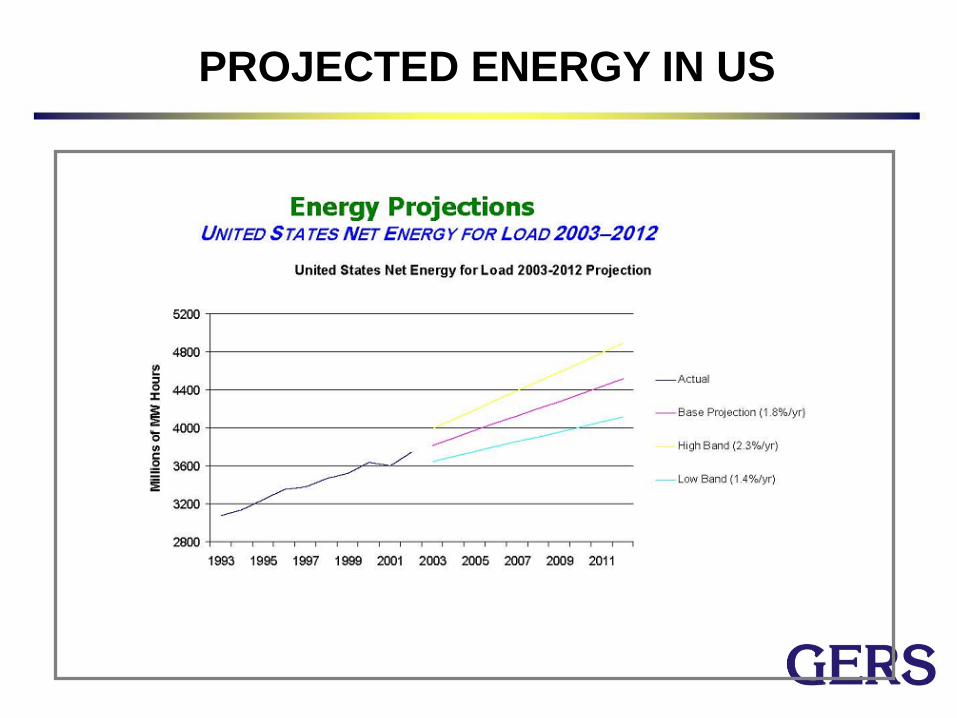

PROJECTED ENERGY IN US

TRANSMISSION SYSTEM INFRASTRUCTURE

U.S. High Voltage Transmission System

Source: NERC

VVoollttaaggee MMiilleess ooff TTrraannssmmiissssiioonn LLiinnee

AACC

230 kV 76,762

345 kV 49,250

500 kV 26,038

765 kV 2,453

Total AC 154,503

DDCC

250-300 kV 930

400 kV 852

450 kV 192

500 kV 1,333

Total DC 3,307

TToottaall AACC ++ DDCC 115577,,881100

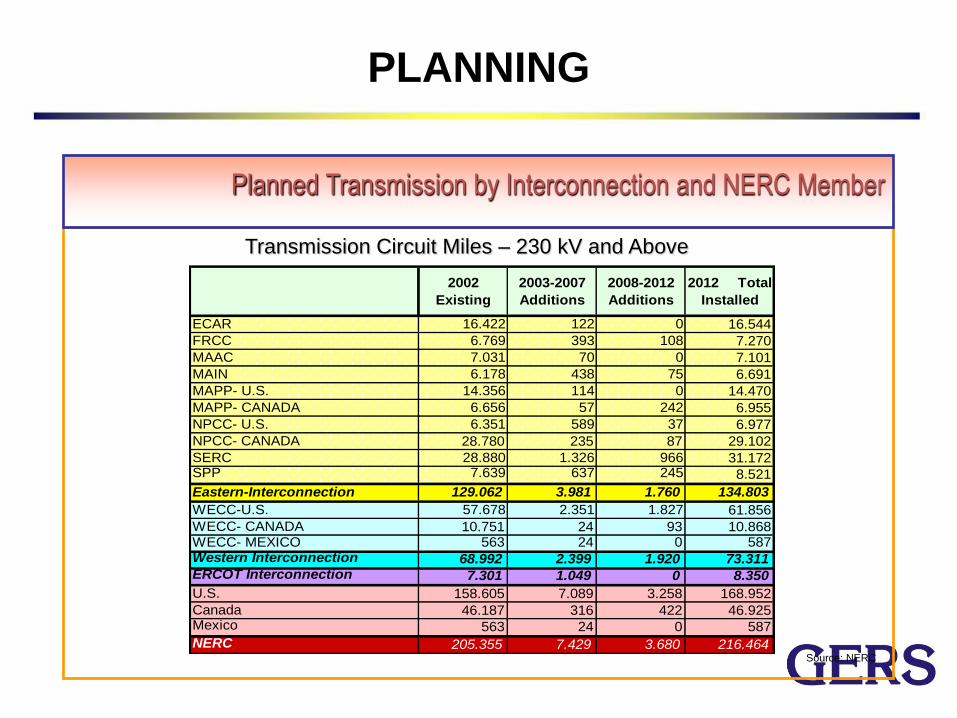

2002

Existing

2003-2007

Additions

2008-2012

Additions

2012 Total

Installed

ECAR 16.422 122 0 16.544

FRCC 6.769 393 108 7.270

MAAC 7.031 70 0 7.101

MAIN 6.178 438 75 6.691

MAPP- U.S. 14.356 114 0 14.470

MAPP- CANADA 6.656 57 242 6.955

NPCC- U.S. 6.351 589 37 6.977

NPCC- CANADA 28.780 235 87 29.102

SERC 28.880 1.326 966 31.172SPP 7.639 637 245 8.521

Eastern-Interconnection 129.062 3.981 1.760 134.803

WECC-U.S. 57.678 2.351 1.827 61.856

WECC- CANADA 10.751 24 93 10.868WECC- MEXICO 563 24 0 587Western Interconnection 68.992 2.399 1.920 73.311ERCOT Interconnection 7.301 1.049 0 8.350

U.S. 158.605 7.089 3.258 168.952

Canada 46.187 316 422 46.925Mexico 563 24 0 587

NERC 205.355 7.429 3.680 216.464

PLANNING

Planned Transmission by Interconnection and NERC Member

Source: NERC

Transmission Circuit Miles – 230 kV and Above

US Map

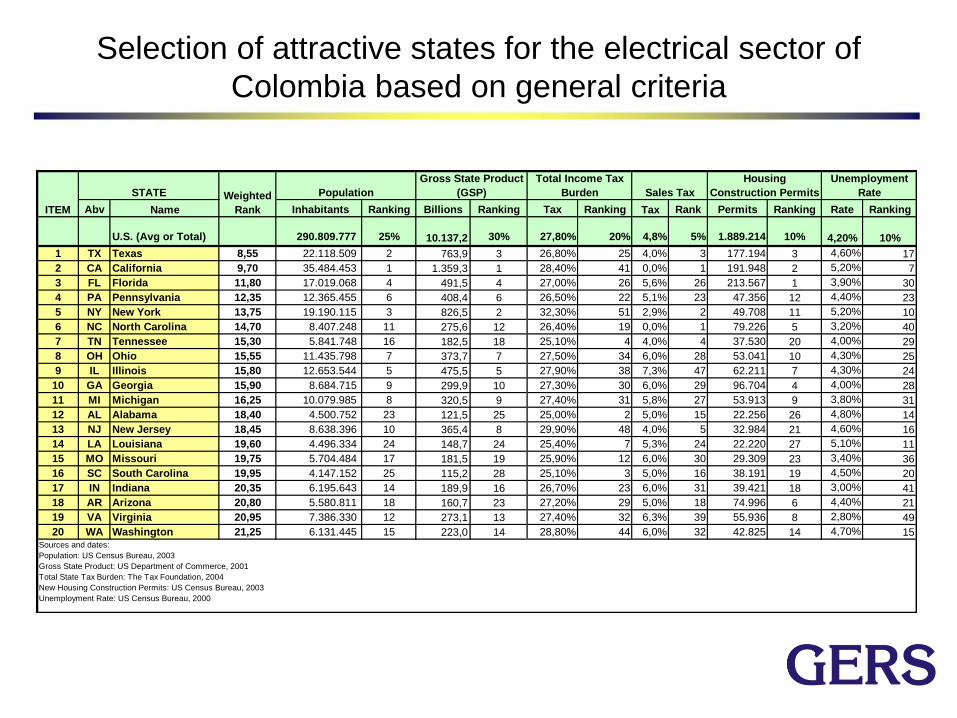

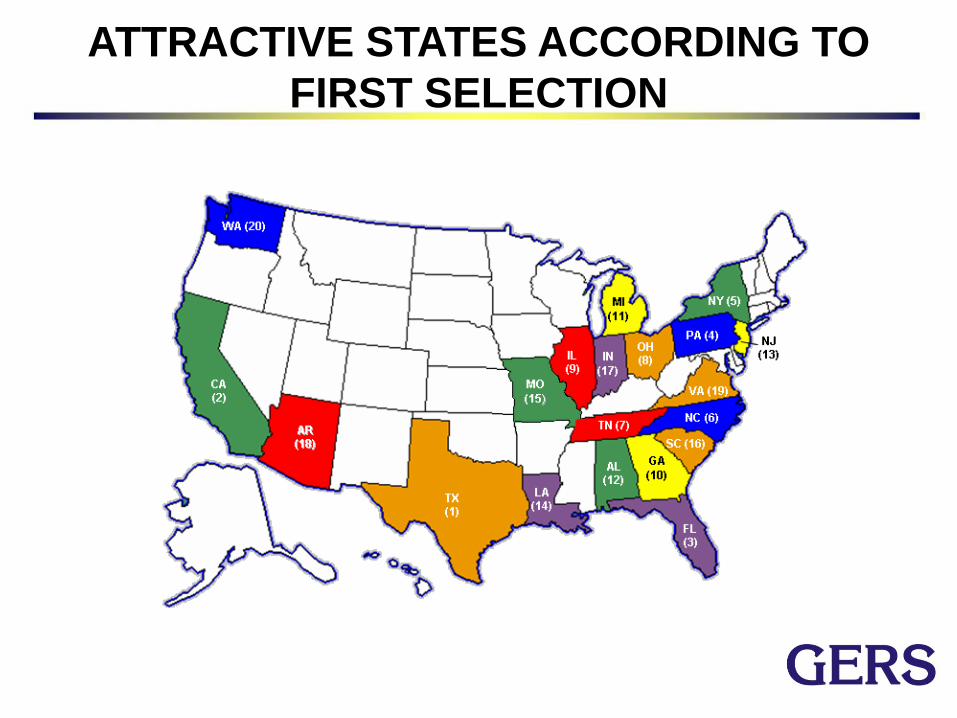

Selection of attractive states for the electrical sector of

Colombia based on general criteria

Abv Name Inhabitants Ranking Billions Ranking Tax Ranking Tax Rank Permits Ranking Rate Ranking

U.S. (Avg or Total) 290.809.777 25% 10.137,2 30% 27,80% 20% 4,8% 5% 1.889.214 10% 4,20% 10%

1 TX Texas 8,55 22.118.509 2 763,9 3 26,80% 25 4,0% 3 177.194 3 4,60% 17

2 CA California 9,70 35.484.453 1 1.359,3 1 28,40% 41 0,0% 1 191.948 2 5,20% 7

3 FL Florida 11,80 17.019.068 4 491,5 4 27,00% 26 5,6% 26 213.567 1 3,90% 30

4 PA Pennsylvania 12,35 12.365.455 6 408,4 6 26,50% 22 5,1% 23 47.356 12 4,40% 23

5 NY New York 13,75 19.190.115 3 826,5 2 32,30% 51 2,9% 2 49.708 11 5,20% 10

6 NC North Carolina 14,70 8.407.248 11 275,6 12 26,40% 19 0,0% 1 79.226 5 3,20% 40

7 TN Tennessee 15,30 5.841.748 16 182,5 18 25,10% 4 4,0% 4 37.530 20 4,00% 29

8 OH Ohio 15,55 11.435.798 7 373,7 7 27,50% 34 6,0% 28 53.041 10 4,30% 25

9 IL Illinois 15,80 12.653.544 5 475,5 5 27,90% 38 7,3% 47 62.211 7 4,30% 24

10 GA Georgia 15,90 8.684.715 9 299,9 10 27,30% 30 6,0% 29 96.704 4 4,00% 28

11 MI Michigan 16,25 10.079.985 8 320,5 9 27,40% 31 5,8% 27 53.913 9 3,80% 31

12 AL Alabama 18,40 4.500.752 23 121,5 25 25,00% 2 5,0% 15 22.256 26 4,80% 14

13 NJ New Jersey 18,45 8.638.396 10 365,4 8 29,90% 48 4,0% 5 32.984 21 4,60% 16

14 LA Louisiana 19,60 4.496.334 24 148,7 24 25,40% 7 5,3% 24 22.220 27 5,10% 11

15 MO Missouri 19,75 5.704.484 17 181,5 19 25,90% 12 6,0% 30 29.309 23 3,40% 36

16 SC South Carolina 19,95 4.147.152 25 115,2 28 25,10% 3 5,0% 16 38.191 19 4,50% 20

17 IN Indiana 20,35 6.195.643 14 189,9 16 26,70% 23 6,0% 31 39.421 18 3,00% 41

18 AR Arizona 20,80 5.580.811 18 160,7 23 27,20% 29 5,0% 18 74.996 6 4,40% 21

19 VA Virginia 20,95 7.386.330 12 273,1 13 27,40% 32 6,3% 39 55.936 8 2,80% 49

20 WA Washington 21,25 6.131.445 15 223,0 14 28,80% 44 6,0% 32 42.825 14 4,70% 15

Housing

Construction PermitsSales Tax

Unemployment

Rate

Sources and dates:

Population: US Census Bureau, 2003

Gross State Product: US Department of Commerce, 2001

Total State Tax Burden: The Tax Foundation, 2004

New Housing Construction Permits: US Census Bureau, 2003

Unemployment Rate: US Census Bureau, 2000

ITEM

Weighted

Rank

STATE

Total Income Tax

BurdenPopulation

Gross State Product

(GSP)

ATTRACTIVE STATES ACCORDING TO

FIRST SELECTION

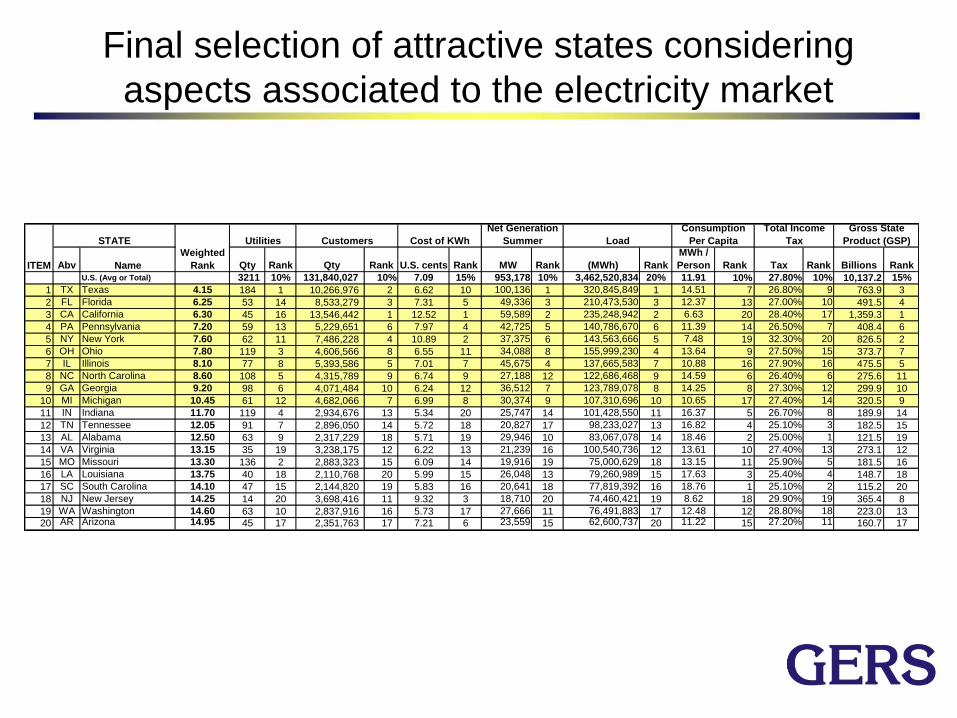

Final selection of attractive states considering

aspects associated to the electricity market

Abv Name Qty Rank Qty Rank U.S. cents Rank MW Rank (MWh) Rank

MWh /

Person Rank Tax Rank Billions Rank

U.S. (Avg or Total) 3211 10% 131,840,027 10% 7.09 15% 953,178 10% 3,462,520,834 20% 11.91 10% 27.80% 10% 10,137.2 15%

1 TX Texas 4.15 184 1 10,266,976 2 6.62 10 100,136 1 320,845,849 1 14.51 7 26.80% 9 763.9 3

2 FL Florida 6.25 53 14 8,533,279 3 7.31 5 49,336 3 210,473,530 3 12.37 13 27.00% 10 491.5 4

3 CA California 6.30 45 16 13,546,442 1 12.52 1 59,589 2 235,248,942 2 6.63 20 28.40% 17 1,359.3 1

4 PA Pennsylvania 7.20 59 13 5,229,651 6 7.97 4 42,725 5 140,786,670 6 11.39 14 26.50% 7 408.4 6

5 NY New York 7.60 62 11 7,486,228 4 10.89 2 37,375 6 143,563,666 5 7.48 19 32.30% 20 826.5 2

6 OH Ohio 7.80 119 3 4,606,566 8 6.55 11 34,088 8 155,999,230 4 13.64 9 27.50% 15 373.7 7

7 IL Illinois 8.10 77 8 5,393,586 5 7.01 7 45,675 4 137,665,583 7 10.88 16 27.90% 16 475.5 5

8 NC North Carolina 8.60 108 5 4,315,789 9 6.74 9 27,188 12 122,686,468 9 14.59 6 26.40% 6 275.6 11

9 GA Georgia 9.20 98 6 4,071,484 10 6.24 12 36,512 7 123,789,078 8 14.25 8 27.30% 12 299.9 10

10 MI Michigan 10.45 61 12 4,682,066 7 6.99 8 30,374 9 107,310,696 10 10.65 17 27.40% 14 320.5 9

11 IN Indiana 11.70 119 4 2,934,676 13 5.34 20 25,747 14 101,428,550 11 16.37 5 26.70% 8 189.9 14

12 TN Tennessee 12.05 91 7 2,896,050 14 5.72 18 20,827 17 98,233,027 13 16.82 4 25.10% 3 182.5 15

13 AL Alabama 12.50 63 9 2,317,229 18 5.71 19 29,946 10 83,067,078 14 18.46 2 25.00% 1 121.5 19

14 VA Virginia 13.15 35 19 3,238,175 12 6.22 13 21,239 16 100,540,736 12 13.61 10 27.40% 13 273.1 12

15 MO Missouri 13.30 136 2 2,883,323 15 6.09 14 19,916 19 75,000,629 18 13.15 11 25.90% 5 181.5 16

16 LA Louisiana 13.75 40 18 2,110,768 20 5.99 15 26,048 13 79,260,989 15 17.63 3 25.40% 4 148.7 18

17 SC South Carolina 14.10 47 15 2,144,820 19 5.83 16 20,641 18 77,819,392 16 18.76 1 25.10% 2 115.2 20

18 NJ New Jersey 14.25 14 20 3,698,416 11 9.32 3 18,710 20 74,460,421 19 8.62 18 29.90% 19 365.4 8

19 WA Washington 14.60 63 10 2,837,916 16 5.73 17 27,666 11 76,491,883 17 12.48 12 28.80% 18 223.0 13

20 AR Arizona 14.95 45 17 2,351,763 17 7.21 6 23,559 15 62,600,737 20 11.22 15 27.20% 11 160.7 17

ITEM

STATE

Total Income

Tax

Gross State

Product (GSP)Utilities Customers Cost of KWh

Weighted

Rank

Load

Net Generation

Summer

Consumption

Per Capita

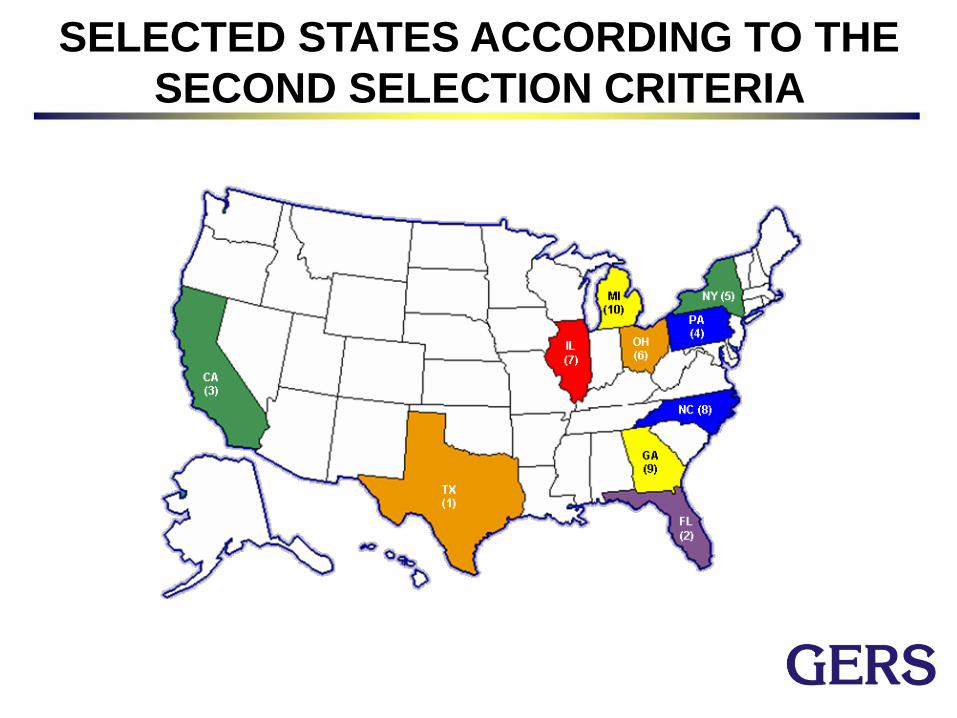

SELECTED STATES ACCORDING TO THE

SECOND SELECTION CRITERIA

WORKING SCHEMES

Joint ventures considering foreign

partnership or cross-border

contracts

Work as a foreign

contractor

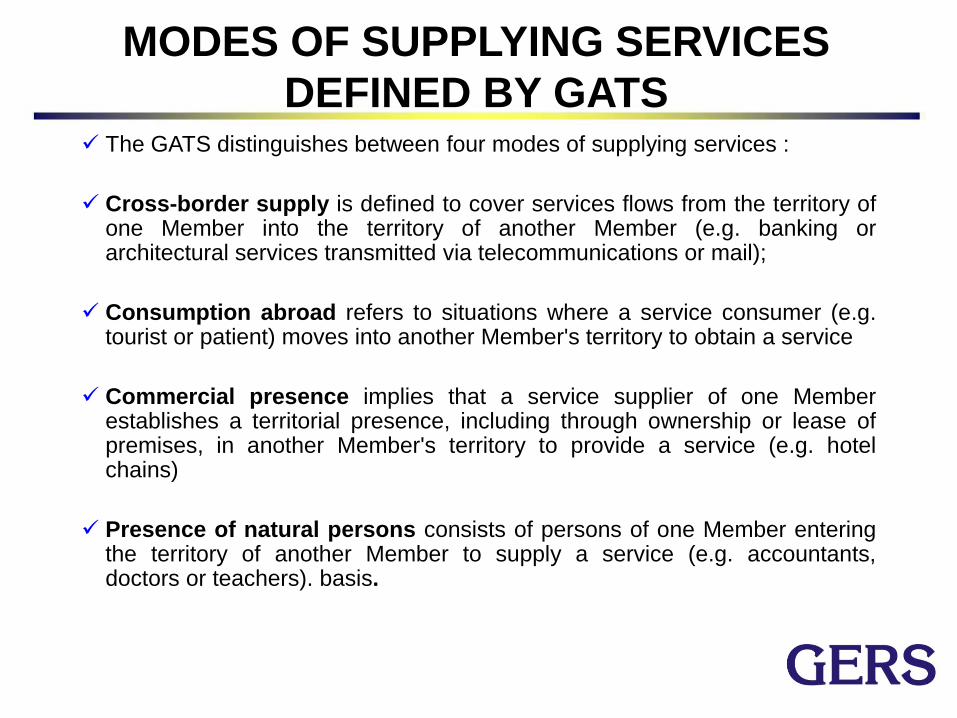

MODES OF SUPPLYING SERVICES

DEFINED BY GATS The GATS distinguishes between four modes of supplying services :

Cross-border supply is defined to cover services flows from the territory of one Member into the territory of another Member (e.g. banking or architectural services transmitted via telecommunications or mail);

Consumption abroad refers to situations where a service consumer (e.g. tourist or patient) moves into another Member's territory to obtain a service

Commercial presence implies that a service supplier of one Member establishes a territorial presence, including through ownership or lease of premises, in another Member's territory to provide a service (e.g. hotel chains)

Presence of natural persons consists of persons of one Member entering the territory of another Member to supply a service (e.g. accountants, doctors or teachers). basis.

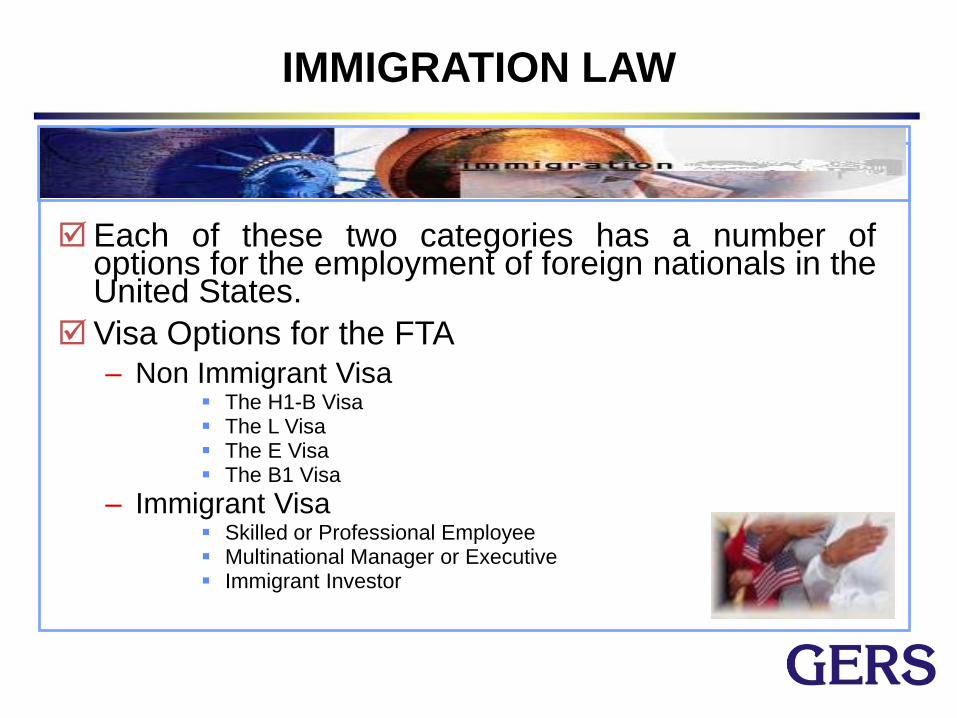

IMMIGRATION LAW

Each of these two categories has a number of options for the employment of foreign nationals in the United States.

Visa Options for the FTA – Non Immigrant Visa

The H1-B Visa The L Visa The E Visa The B1 Visa

– Immigrant Visa Skilled or Professional Employee Multinational Manager or Executive Immigrant Investor

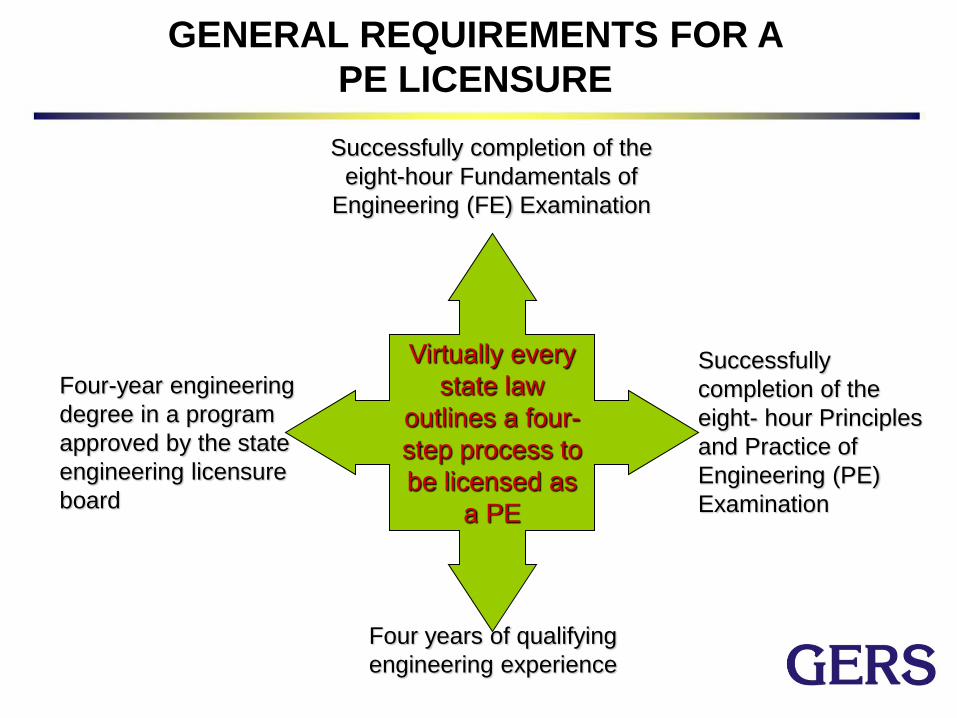

GENERAL REQUIREMENTS FOR A

PE LICENSURE

Virtually every

state law

outlines a four-

step process to

be licensed as

a PE

Four-year engineering

degree in a program

approved by the state

engineering licensure

board

Four years of qualifying

engineering experience

Successfully completion of the

eight-hour Fundamentals of

Engineering (FE) Examination

Successfully

completion of the

eight- hour Principles

and Practice of

Engineering (PE)

Examination

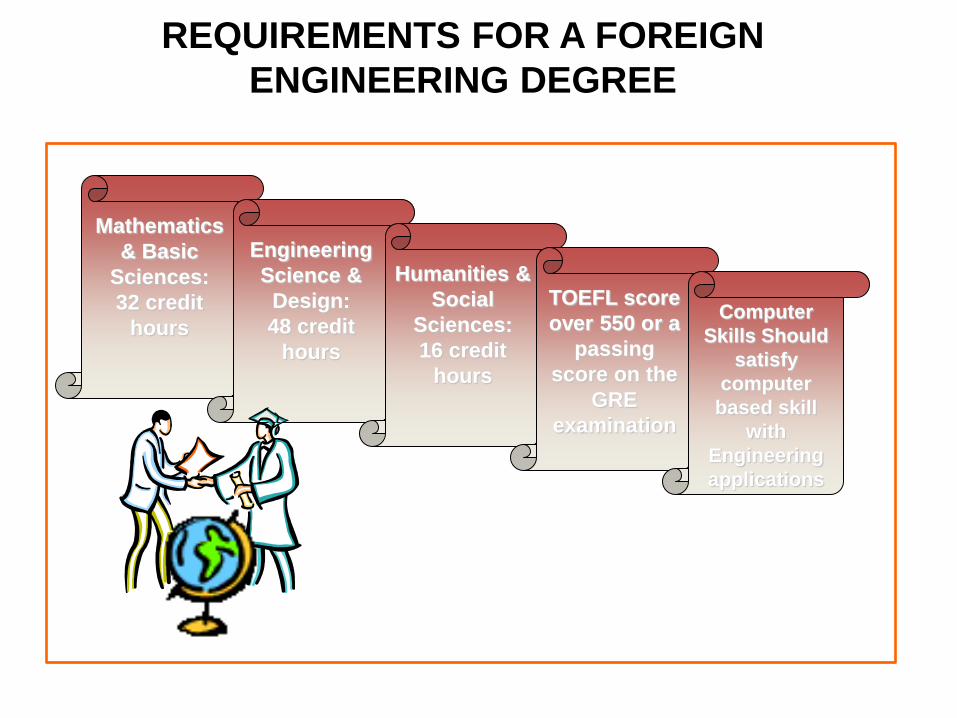

REQUIREMENTS FOR A FOREIGN

ENGINEERING DEGREE

Mathematics

& Basic

Sciences:

32 credit

hours

Engineering

Science &

Design:

48 credit

hours

Humanities &

Social

Sciences:

16 credit

hours

TOEFL score

over 550 or a

passing

score on the

GRE

examination

Computer

Skills Should

satisfy

computer

based skill

with

Engineering

applications

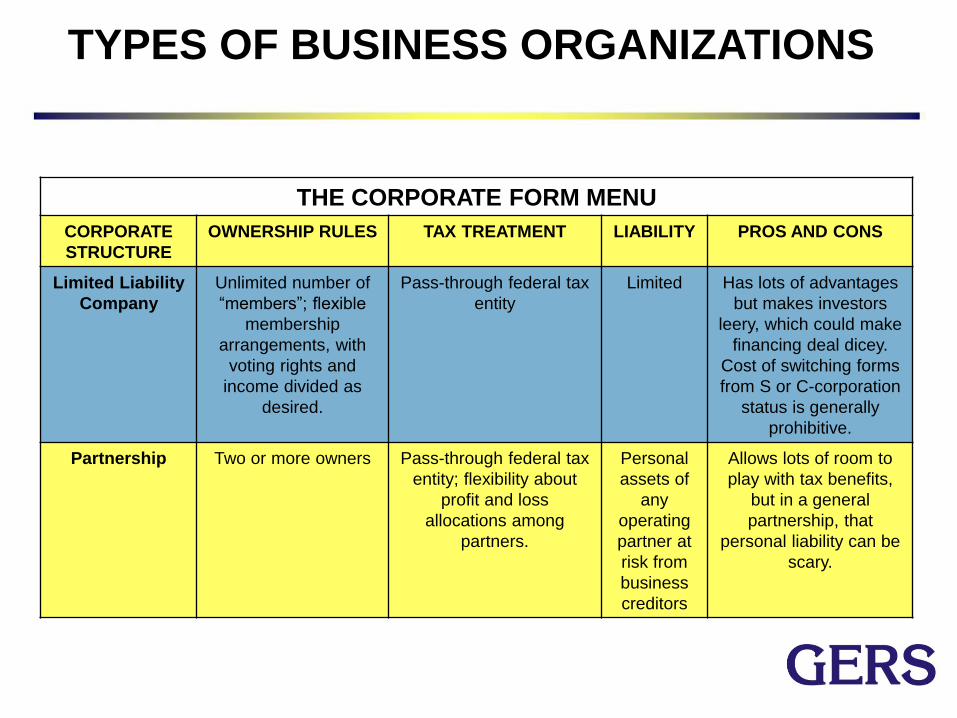

THE CORPORATE FORM MENU

CORPORATE

STRUCTURE

OWNERSHIP RULES TAX TREATMENT LIABILITY PROS AND CONS

Sole

Proprietorship

One owner Pass-through federal tax

entity

Unlimited

personal

liability for

business

debts.

Is easy to set up but

leaves your personal

finances at risk. Plus,

you miss out on all

kinds of business

deductions.

S Corporation Up to 75

shareholders, only

one basic class of

stock; slight flexibility

on voting rights.

Pass-through federal tax

entity

Limited Is easy to set up but

may limit your financing

options later on.

C Corporation Unlimited number of

shareholders; no

limits on stock classes

or voting

arrangements.

Dividend income gets

taxed at the corporate

and shareholder levels;

losses and deductions

stay at the corporate

level.

Limited Can be costly from a

tax perspective but

investor friendly.

TYPES OF BUSINESS ORGANIZATIONS

THE CORPORATE FORM MENU

CORPORATE

STRUCTURE

OWNERSHIP RULES TAX TREATMENT LIABILITY PROS AND CONS

Limited Liability

Company

Unlimited number of

“members”; flexible

membership

arrangements, with

voting rights and

income divided as

desired.

Pass-through federal tax

entity

Limited Has lots of advantages

but makes investors

leery, which could make

financing deal dicey.

Cost of switching forms

from S or C-corporation

status is generally

prohibitive.

Partnership Two or more owners Pass-through federal tax

entity; flexibility about

profit and loss

allocations among

partners.

Personal

assets of

any

operating

partner at

risk from

business

creditors

Allows lots of room to

play with tax benefits,

but in a general

partnership, that

personal liability can be

scary.

TYPES OF BUSINESS ORGANIZATIONS

TYPE OF CUSTOMERS

Customers could be classified in 4 types within the US

electrical sector:

– Federal Government.

– Utilities.

– Contracting Companies and Original Equipment

Manufacturers (OEM’s).

– End Users.

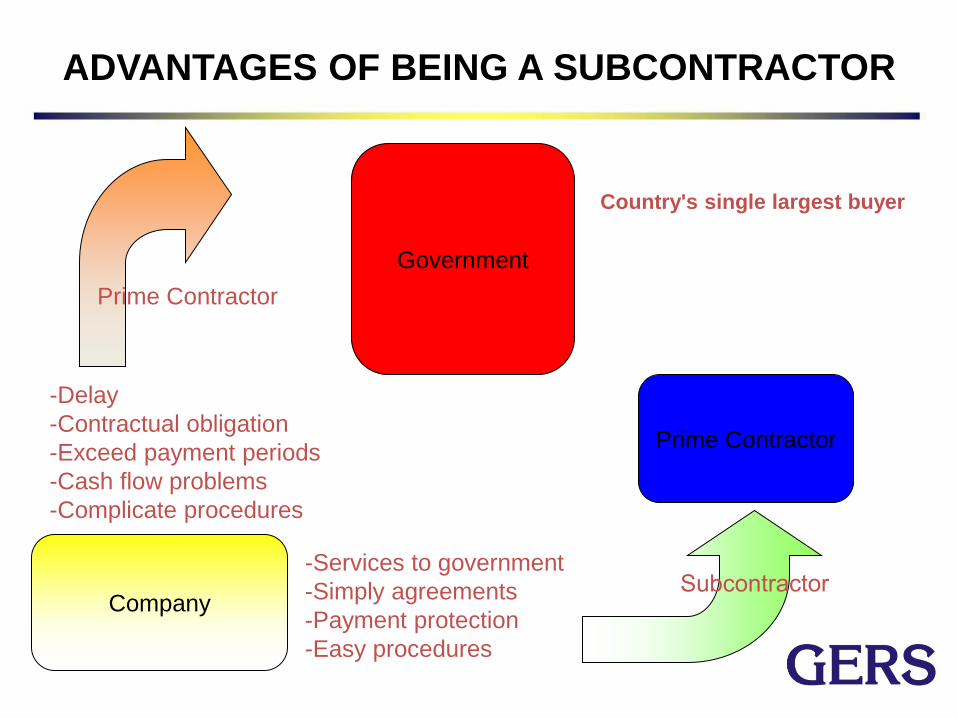

ADVANTAGES OF BEING A SUBCONTRACTOR

Company

Government

Prime Contractor

Prime Contractor

-Delay

-Contractual obligation

-Exceed payment periods

-Cash flow problems

-Complicate procedures

-Services to government

-Simply agreements

-Payment protection

-Easy procedures

Country's single largest buyer

FEDERAL PROCUREMENT

The federal government purchases billions of dollars in goods and

services each year from paperclips to complex space vehicles.

To ensure that small businesses get their fair share, statutory goals

have been established for Federal executive agencies. They are:

23 percent of prime contracts for small businesses

5 percent of prime and subcontracts for small disadvantaged businesses

5 percent of prime and subcontracts for women-owned small businesses

3 percent of prime contracts for Historically Underutilized Business Zone (HUBZone) small businesses

3 percent of prime and subcontracts for service-disabled veteran-owned small businesses.

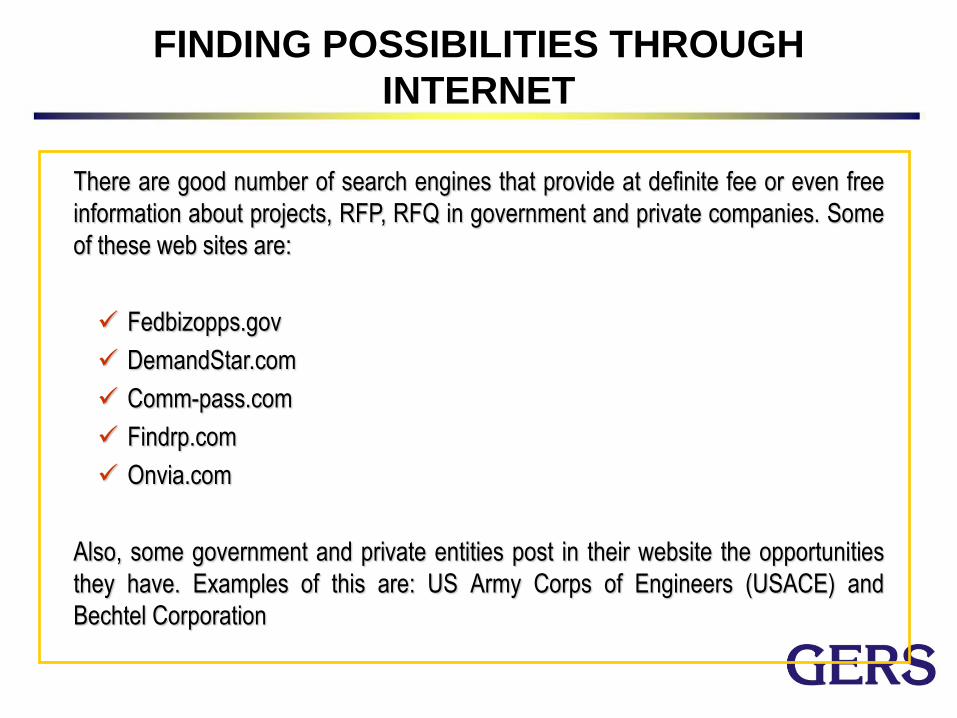

FINDING POSSIBILITIES THROUGH

INTERNET

There are good number of search engines that provide at definite fee or even free

information about projects, RFP, RFQ in government and private companies. Some

of these web sites are:

Fedbizopps.gov

DemandStar.com

Comm-pass.com

Findrp.com

Onvia.com

Also, some government and private entities post in their website the opportunities

they have. Examples of this are: US Army Corps of Engineers (USACE) and

Bechtel Corporation

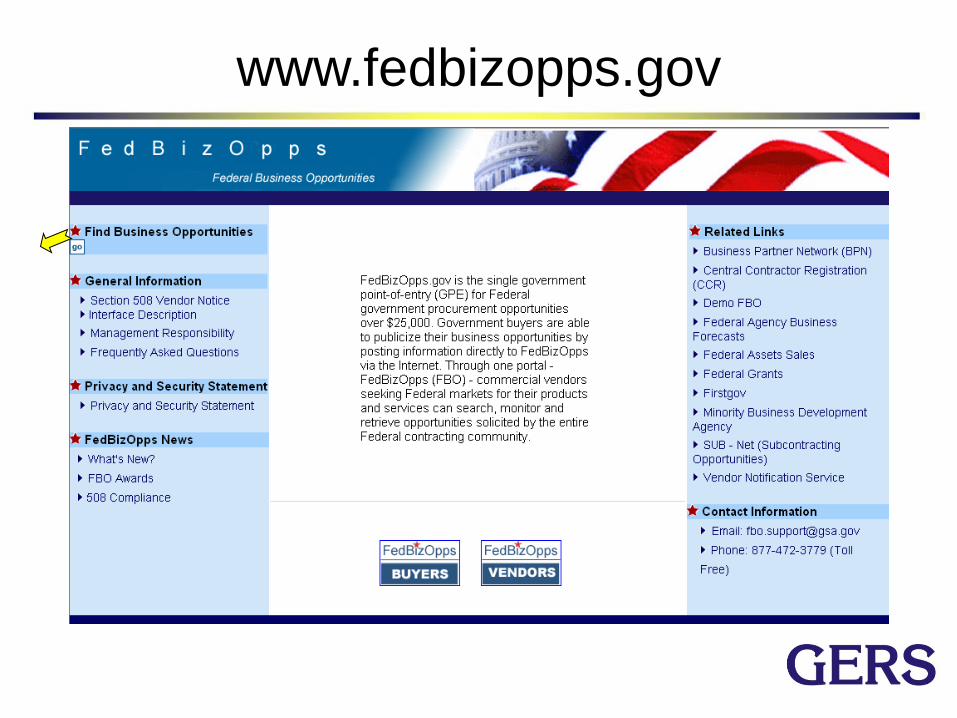

www.fedbizopps.gov

Possibilities of Solar Generating Plants in

New Mexico

SOLAR GENERATION CLASSIFICATION

NEW MEXICO WITHIN THE US

Capital: Santa Fe

Population: 1,984,356

Bordering States: New Mexico borders Texas, Oklahoma,

Colorado, Utah, and Arizona.

New Mexico total area: 315,194 km2

CURRENT PROJECTS

Possibilities in Energy

Efficiency Projects

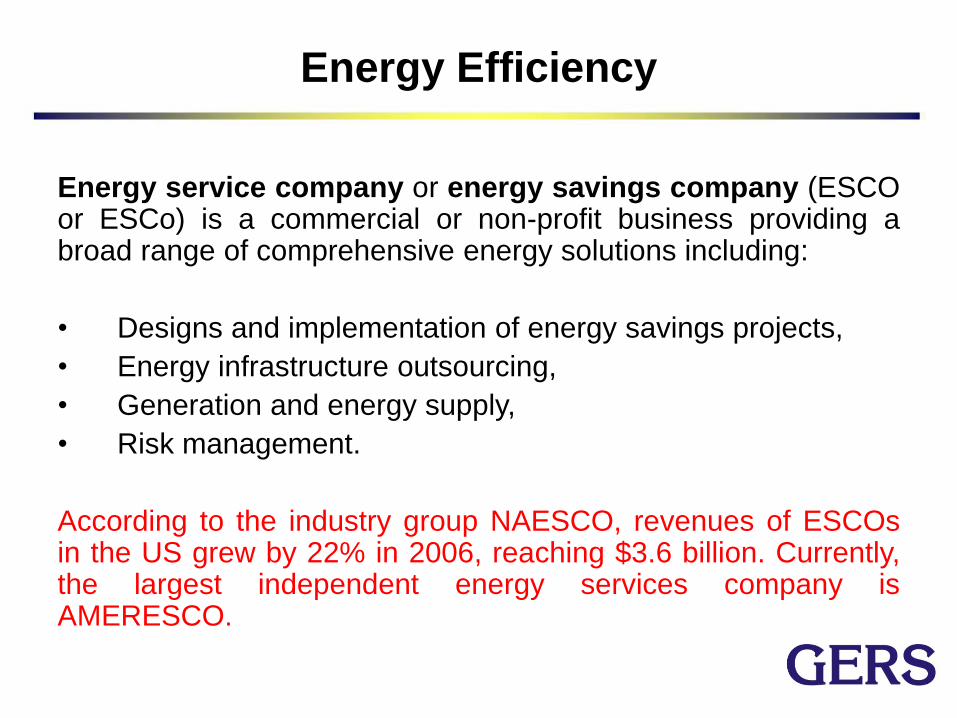

Energy service company or energy savings company (ESCO or ESCo) is a commercial or non-profit business providing a broad range of comprehensive energy solutions including:

• Designs and implementation of energy savings projects,

• Energy infrastructure outsourcing,

• Generation and energy supply,

• Risk management.

According to the industry group NAESCO, revenues of ESCOs in the US grew by 22% in 2006, reaching $3.6 billion. Currently, the largest independent energy services company is AMERESCO.

Energy Efficiency

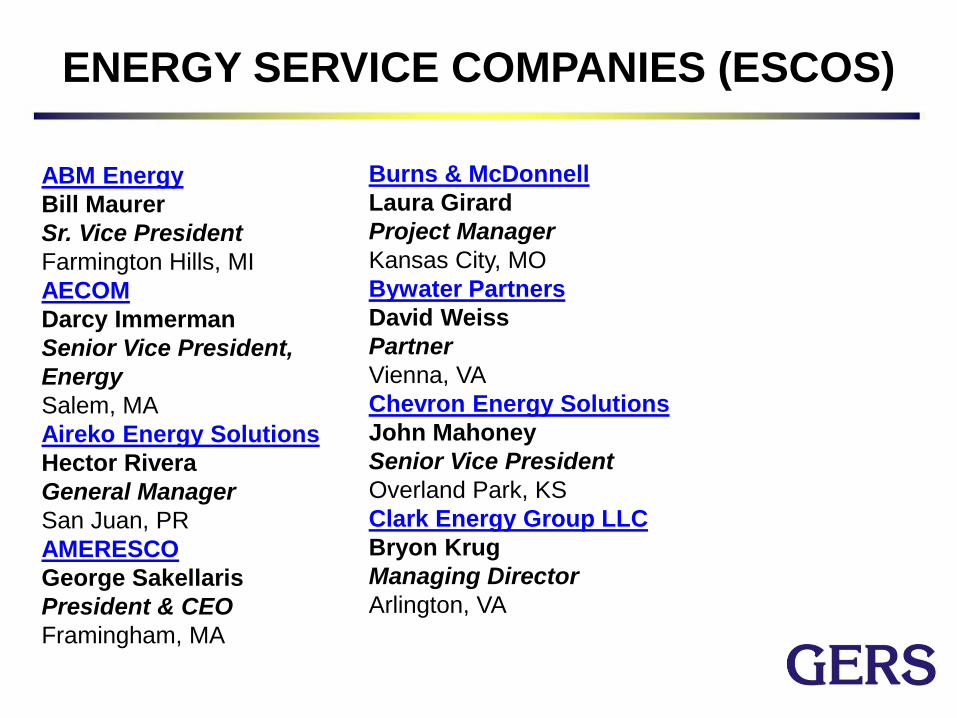

ENERGY SERVICE COMPANIES (ESCOS)

ABM Energy

Bill Maurer

Sr. Vice President

Farmington Hills, MI

AECOM

Darcy Immerman

Senior Vice President,

Energy

Salem, MA

Aireko Energy Solutions

Hector Rivera

General Manager

San Juan, PR

AMERESCO

George Sakellaris

President & CEO

Framingham, MA

Burns & McDonnell

Laura Girard

Project Manager

Kansas City, MO

Bywater Partners

David Weiss

Partner

Vienna, VA

Chevron Energy Solutions

John Mahoney

Senior Vice President

Overland Park, KS

Clark Energy Group LLC

Bryon Krug

Managing Director

Arlington, VA

CONCLUSIONS

The electrical system of the USA presents a giant and well developed infrastructure but presents severe weaknesses and needs important projects. Therefore it offers huge market possibilities for transnational and established companies.

Doing business in the USA is both easy and difficult. It is easy in the sense that there are thousands of opportunities well paid generally. It is difficult though in the sense that penetrating the American market is complicated, high investment is normally required and getting acquainted with the bid process is lengthy.

It is very important to stress that the US offers possibilities in each of the 50 states. From a selection based on economical figures and parameters of the electricity market a total of 10 states were taken: Texas, Florida, California, Pennsylvania, New York, Ohio, Illinois, North Carolina, Georgia and Michigan.