Embed Size (px)

Citation preview

Food Price Monitoring and Analysis10 December 2018

MONTHLY REPORT ON FOOD PRICE TRENDS

BULLETIN#10

GIEWS - Global Information and Early Warning System on Food and Agriculture

KEY MESSAGES ↗ International prices of wheat and maize remained under downward pressure in November, mostly on account of large nearby supplies. For rice, new crop arrivals continued to weigh on export price quotations.

↗ In East Africa, in the Sudan, a further sharp devaluation of the currency triggered a marked increase in the prices of grains, which reached record to near-record highs despite the ongoing harvest.

↗ In Southern Africa, in Zimbabwe, a drop in the value of the country’s currency, as well as a shortage of foreign exchange, curbed imports and underpinned the increases in cereal prices. Elsewhere in the subregion, reduced 2018 harvests pushed the prices of maize to levels above those recorded a year earlier in several countries.

Price warning level: High Moderate [Based on GIEWS analysis]

CONTENTSINTERNATIONAL CEREAL PRICES ............................. 2

DOMESTIC PRICE WARNINGS .................................. 3

WEST AFRICA ........................................................... 6

SOUTHERN AFRICA .................................................. 8

EAST AFRICA .......................................................... 10

EAST ASIA .............................................................. 12

CIS - ASIA AND EUROPE ......................................... 15

CENTRAL AMERICA AND THE CARIBBEAN ............. 18

SOUTH AMERICA ................................................... 19

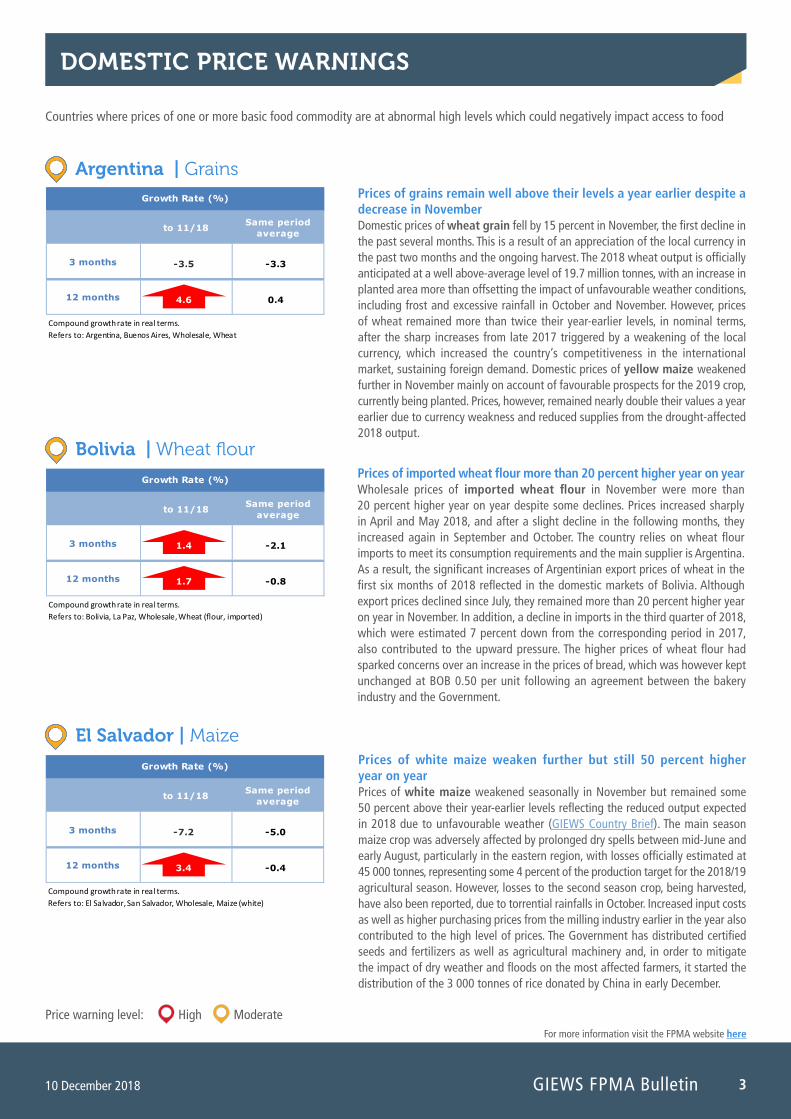

Argentina | Grains

Bolivia | Wheat flour

El Salvador | Maize

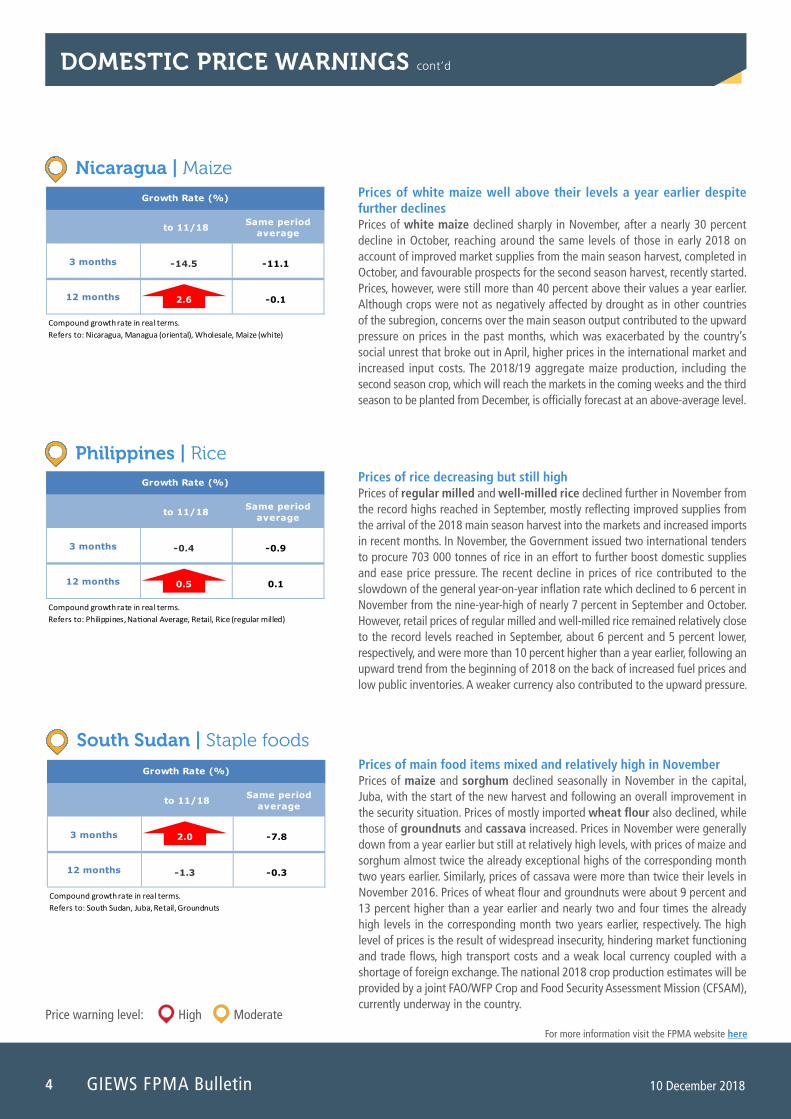

Nicaragua | Maize

Philippines | Rice

South Sudan | Staple foods

Sudan | Staple foods

Zambia | Maize

Zimbabwe | Cereals

Domestic price warnings

Warnings are only included if latest available price data is not older than two months.

2 10 December 2018GIEWS FPMA Bulletin

For more information visit the FPMA website here

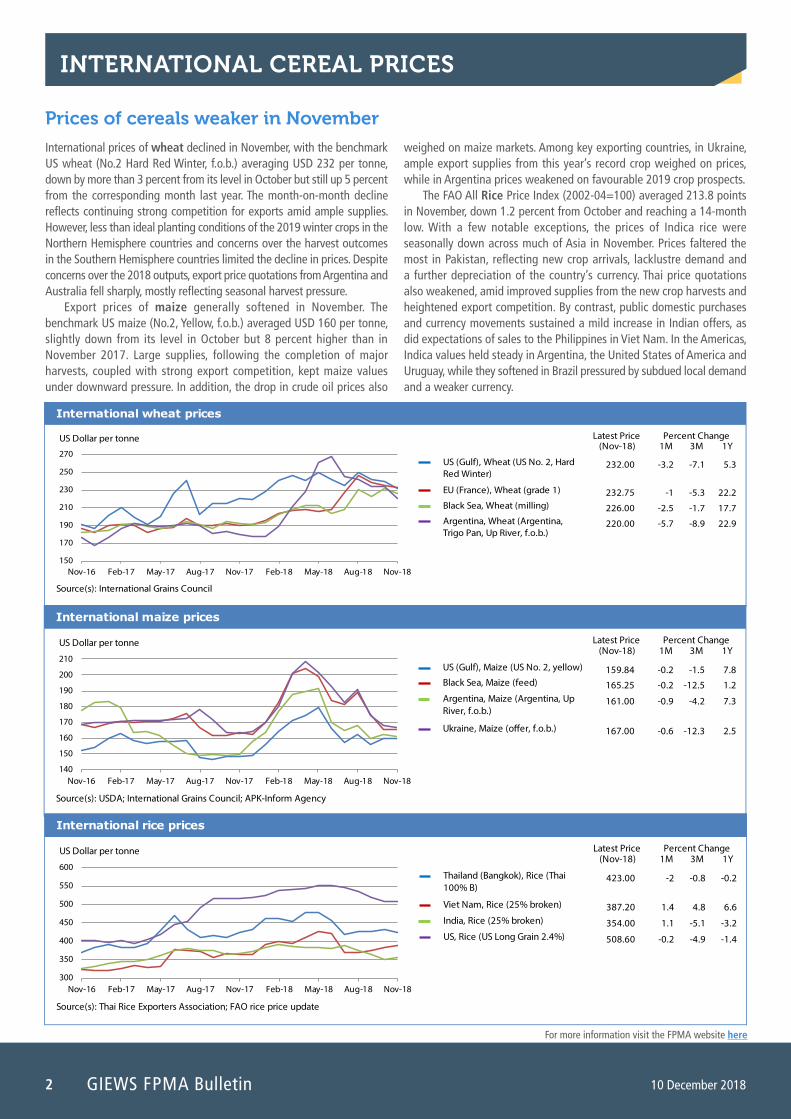

INTERNATIONAL CEREAL PRICES

International prices of wheat declined in November, with the benchmark US wheat (No.2 Hard Red Winter, f.o.b.) averaging USD 232 per tonne, down by more than 3 percent from its level in October but still up 5 percent from the corresponding month last year. The month-on-month decline reflects continuing strong competition for exports amid ample supplies. However, less than ideal planting conditions of the 2019 winter crops in the Northern Hemisphere countries and concerns over the harvest outcomes in the Southern Hemisphere countries limited the decline in prices. Despite concerns over the 2018 outputs, export price quotations from Argentina and Australia fell sharply, mostly reflecting seasonal harvest pressure.

Export prices of maize generally softened in November. The benchmark US maize (No.2, Yellow, f.o.b.) averaged USD 160 per tonne, slightly down from its level in October but 8 percent higher than in November 2017. Large supplies, following the completion of major harvests, coupled with strong export competition, kept maize values under downward pressure. In addition, the drop in crude oil prices also

weighed on maize markets. Among key exporting countries, in Ukraine, ample export supplies from this year’s record crop weighed on prices, while in Argentina prices weakened on favourable 2019 crop prospects.

The FAO All Rice Price Index (2002-04=100) averaged 213.8 points in November, down 1.2 percent from October and reaching a 14-month low. With a few notable exceptions, the prices of Indica rice were seasonally down across much of Asia in November. Prices faltered the most in Pakistan, reflecting new crop arrivals, lacklustre demand and a further depreciation of the country’s currency. Thai price quotations also weakened, amid improved supplies from the new crop harvests and heightened export competition. By contrast, public domestic purchases and currency movements sustained a mild increase in Indian offers, as did expectations of sales to the Philippines in Viet Nam. In the Americas, Indica values held steady in Argentina, the United States of America and Uruguay, while they softened in Brazil pressured by subdued local demand and a weaker currency.

Prices of cereals weaker in November

Latest Price(Nov-18) 1M 3M 1Y

International wheat prices

Percent Change

150

170

190

210

230

250

270

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

US (Gulf), Wheat (US No. 2, Hard Red Winter)

EU (France), Wheat (grade 1)

Black Sea, Wheat (milling)

Argentina, Wheat (Argentina, Trigo Pan, Up River, f.o.b.)

US Dollar per tonne

232.00

232.75

226.00

220.00

-3.2

-1

-2.5

-5.7

-7.1

-5.3

-1.7

-8.9

5.3

22.2

17.7

22.9

Source(s): International Grains Council

Latest Price(Nov-18) 1M 3M 1Y

International maize prices

Percent Change

140

150

160

170

180

190

200

210

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

US (Gulf), Maize (US No. 2, yellow)

Black Sea, Maize (feed)

Argentina, Maize (Argentina, Up River, f.o.b.)

Ukraine, Maize (o�er, f.o.b.)

US Dollar per tonne

159.84

165.25

161.00

167.00

-0.2

-0.2

-0.9

-0.6

-1.5

-12.5

-4.2

-12.3

7.8

1.2

7.3

2.5

Source(s): USDA; International Grains Council; APK-Inform Agency

Latest Price(Nov-18) 1M 3M 1Y

International rice prices

Percent Change

300

350

400

450

500

550

600

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Thailand (Bangkok), Rice (Thai 100% B)

Viet Nam, Rice (25% broken)

India, Rice (25% broken)

US, Rice (US Long Grain 2.4%)

US Dollar per tonne

423.00

387.20

354.00

508.60

-2

1.4

1.1

-0.2

-0.8

4.8

-5.1

-4.9

-0.2

6.6

-3.2

-1.4

Source(s): Thai Rice Exporters Association; FAO rice price update

Price warning level: High Moderate

3

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

DOMESTIC PRICE WARNINGS

Prices of grains remain well above their levels a year earlier despite a decrease in November Domestic prices of wheat grain fell by 15 percent in November, the first decline in the past several months. This is a result of an appreciation of the local currency in the past two months and the ongoing harvest. The 2018 wheat output is officially anticipated at a well above-average level of 19.7 million tonnes, with an increase in planted area more than offsetting the impact of unfavourable weather conditions, including frost and excessive rainfall in October and November. However, prices of wheat remained more than twice their year-earlier levels, in nominal terms, after the sharp increases from late 2017 triggered by a weakening of the local currency, which increased the country’s competitiveness in the international market, sustaining foreign demand. Domestic prices of yellow maize weakened further in November mainly on account of favourable prospects for the 2019 crop, currently being planted. Prices, however, remained nearly double their values a year earlier due to currency weakness and reduced supplies from the drought-affected 2018 output.

Argentina | Grains

Countries where prices of one or more basic food commodity are at abnormal high levels which could negatively impact access to food

El Salvador | Maize

Bolivia | Wheat flour

Prices of white maize weaken further but still 50 percent higher year on year Prices of white maize weakened seasonally in November but remained some 50 percent above their year-earlier levels reflecting the reduced output expected in 2018 due to unfavourable weather (GIEWS Country Brief). The main season maize crop was adversely affected by prolonged dry spells between mid-June and early August, particularly in the eastern region, with losses officially estimated at 45 000 tonnes, representing some 4 percent of the production target for the 2018/19 agricultural season. However, losses to the second season crop, being harvested, have also been reported, due to torrential rainfalls in October. Increased input costs as well as higher purchasing prices from the milling industry earlier in the year also contributed to the high level of prices. The Government has distributed certified seeds and fertilizers as well as agricultural machinery and, in order to mitigate the impact of dry weather and floods on the most affected farmers, it started the distribution of the 3 000 tonnes of rice donated by China in early December.

Prices of imported wheat flour more than 20 percent higher year on year Wholesale prices of imported wheat flour in November were more than 20 percent higher year on year despite some declines. Prices increased sharply in April and May 2018, and after a slight decline in the following months, they increased again in September and October. The country relies on wheat flour imports to meet its consumption requirements and the main supplier is Argentina. As a result, the significant increases of Argentinian export prices of wheat in the first six months of 2018 reflected in the domestic markets of Bolivia. Although export prices declined since July, they remained more than 20 percent higher year on year in November. In addition, a decline in imports in the third quarter of 2018, which were estimated 7 percent down from the corresponding period in 2017, also contributed to the upward pressure. The higher prices of wheat flour had sparked concerns over an increase in the prices of bread, which was however kept unchanged at BOB 0.50 per unit following an agreement between the bakery industry and the Government.

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

4.6

-3.5

Compound growth rate in real terms.Refers to: Argentina, Buenos Aires, Wholesale, Wheat

-3.3

0.4

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

1.7

1.4

Compound growth rate in real terms.Refers to: Bolivia, La Paz, Wholesale, Wheat (flour, imported)

-2.1

-0.8

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

3.4

-7.2

Compound growth rate in real terms.Refers to: El Salvador, San Salvador, Wholesale, Maize (white)

-5.0

-0.4

Price warning level: High Moderate

4 10 December 2018

For more information visit the FPMA website here

GIEWS FPMA Bulletin

DOMESTIC PRICE WARNINGS cont’d

Nicaragua | Maize Prices of white maize well above their levels a year earlier despite further declines Prices of white maize declined sharply in November, after a nearly 30 percent decline in October, reaching around the same levels of those in early 2018 on account of improved market supplies from the main season harvest, completed in October, and favourable prospects for the second season harvest, recently started. Prices, however, were still more than 40 percent above their values a year earlier. Although crops were not as negatively affected by drought as in other countries of the subregion, concerns over the main season output contributed to the upward pressure on prices in the past months, which was exacerbated by the country’s social unrest that broke out in April, higher prices in the international market and increased input costs. The 2018/19 aggregate maize production, including the second season crop, which will reach the markets in the coming weeks and the third season to be planted from December, is officially forecast at an above-average level.

Philippines | RicePrices of rice decreasing but still high Prices of regular milled and well-milled rice declined further in November from the record highs reached in September, mostly reflecting improved supplies from the arrival of the 2018 main season harvest into the markets and increased imports in recent months. In November, the Government issued two international tenders to procure 703 000 tonnes of rice in an effort to further boost domestic supplies and ease price pressure. The recent decline in prices of rice contributed to the slowdown of the general year-on-year inflation rate which declined to 6 percent in November from the nine-year-high of nearly 7 percent in September and October. However, retail prices of regular milled and well-milled rice remained relatively close to the record levels reached in September, about 6 percent and 5 percent lower, respectively, and were more than 10 percent higher than a year earlier, following an upward trend from the beginning of 2018 on the back of increased fuel prices and low public inventories. A weaker currency also contributed to the upward pressure.

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

2.6

-14.5

Compound growth rate in real terms.Refers to: Nicaragua, Managua (oriental), Wholesale, Maize (white)

-11.1

-0.1

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

0.5

-0.4

Compound growth rate in real terms.Refers to: Philippines, National Average, Retail, Rice (regular milled)

-0.9

0.1

South Sudan | Staple foodsPrices of main food items mixed and relatively high in November Prices of maize and sorghum declined seasonally in November in the capital, Juba, with the start of the new harvest and following an overall improvement in the security situation. Prices of mostly imported wheat flour also declined, while those of groundnuts and cassava increased. Prices in November were generally down from a year earlier but still at relatively high levels, with prices of maize and sorghum almost twice the already exceptional highs of the corresponding month two years earlier. Similarly, prices of cassava were more than twice their levels in November 2016. Prices of wheat flour and groundnuts were about 9 percent and 13 percent higher than a year earlier and nearly two and four times the already high levels in the corresponding month two years earlier, respectively. The high level of prices is the result of widespread insecurity, hindering market functioning and trade flows, high transport costs and a weak local currency coupled with a shortage of foreign exchange. The national 2018 crop production estimates will be provided by a joint FAO/WFP Crop and Food Security Assessment Mission (CFSAM), currently underway in the country.

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

-1.3

2.0

Compound growth rate in real terms.Refers to: South Sudan, Juba, Retail, Groundnuts

-7.8

-0.3

5

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

DOMESTIC PRICE WARNINGS cont’d

Price warning level: High Moderate

Sudan | Staple foods Prices of staple foods rise again to record or near-record highs Prices of locally grown sorghum and millet spiked in November and reached record to near-record highs due to a further sharp devaluation of the local currency. Similarly, prices of wheat, mostly imported, increased to record highs in the capital, Khartoum. The Government devaluated the local currency from SDG 17.96 per US dollar to SDG 47.5 per US dollar in early October in an effort to tackle the shortage of foreign exchange. This is part of a number of measures the Government is implementing to address the ongoing economic crisis, which include the removal of import restrictions on 19 selected food items and the introduction of austerity measures such as the elimination of all customs tax exemptions and a reduction in government expenses. In an attempt to curb the recent surge in prices, the Government also announced the reintroduction of the wheat subsidies, which were removed in the 2018 budget. The surge in prices in November comes in spite of the ongoing 2018/19 harvest, which had triggered some declines in September and October. Although crops benefited from favourable precipitation, high prices of agricultural inputs and shortages of fuel and cash have affected farming activities. An ongoing nationwide government-led crop assessment, supported by FAO, will provide detailed production estimates in early 2019.

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

2.8

5.1

Compound growth rate in real terms.Refers to: Sudan, Kadugli, Wholesale, Millet

-0.2

-0.2

Zambia | Maize Prices of maize products on the increase Prices of maize meal products increased in November and were nearly 30 percent above their year-earlier values following sustained increases since August. The seasonal month-on-month gains were amplified by the impact of a sharply reduced 2018 maize output, 23 percent below the five-year average, due to rainfall deficits at the key stage for the crop’s development earlier in the year. This is likely to result in a significant drawdown in national inventories to meet consumption needs. In response to the tighter supply situation, the Government imposed temporary export restrictions to shore-up national availabilities (FPMA Food Policies). On top of the supply pressure, an abrupt depreciation of the local currency in recent months added further inflationary pressure that underpinned prices.

to 11/18 Same periodaverage

3 months

12 months

Growth Rate (%)

1.6

4.9

Compound growth rate in real terms.Refers to: Zambia, National Average, Retail, White roller maize meal

0.9

-0.5

Zimbabwe | Cereals Prices of cereals surged to record levels in October Prices of rice and wheat products increased sharply in October underpinned by foreign exchange shortages that acutely constrained the capacity to import adequate quantities of grains and by a drop in the value of the local currency - bond notes were introduced two years ago to alleviate liquidity constraints - against the US dollar. A new tax on electronic money transactions, widely used in the country, added upward pressure on prices. The reduced access to external supplies of wheat, given the country’s position as a net importer, reportedly curtailed milling operations, which further exerted upward pressure on prices. As of October, prices of wheat flour were double their year-earlier values, following month-on-month increases by up to 90 percent. Similarly, prices of rice rose by comparable rates, but year-on-year variations were not as significant. The recent inflationary pressures amplified seasonal price increases of the main food staple, maize meal, however, prices remained broadly unchanged relative to the previous year on account of adequate domestic supplies. In an effort to curb food prices, the Government responded by suspending import restrictions on basic commodities in late October (FPMA Food Policies).

to 10/18 Same periodaverage

3 months

12 months

Growth Rate (%)

4.7

20.5

Compound growth rate in real terms.Refers to: Zimbabwe, Mash central, Retail, Wheat (flour)

0.0

0.0

GIEWS FPMA Bulletin6 10 December 2018

For more information visit the FPMA website here

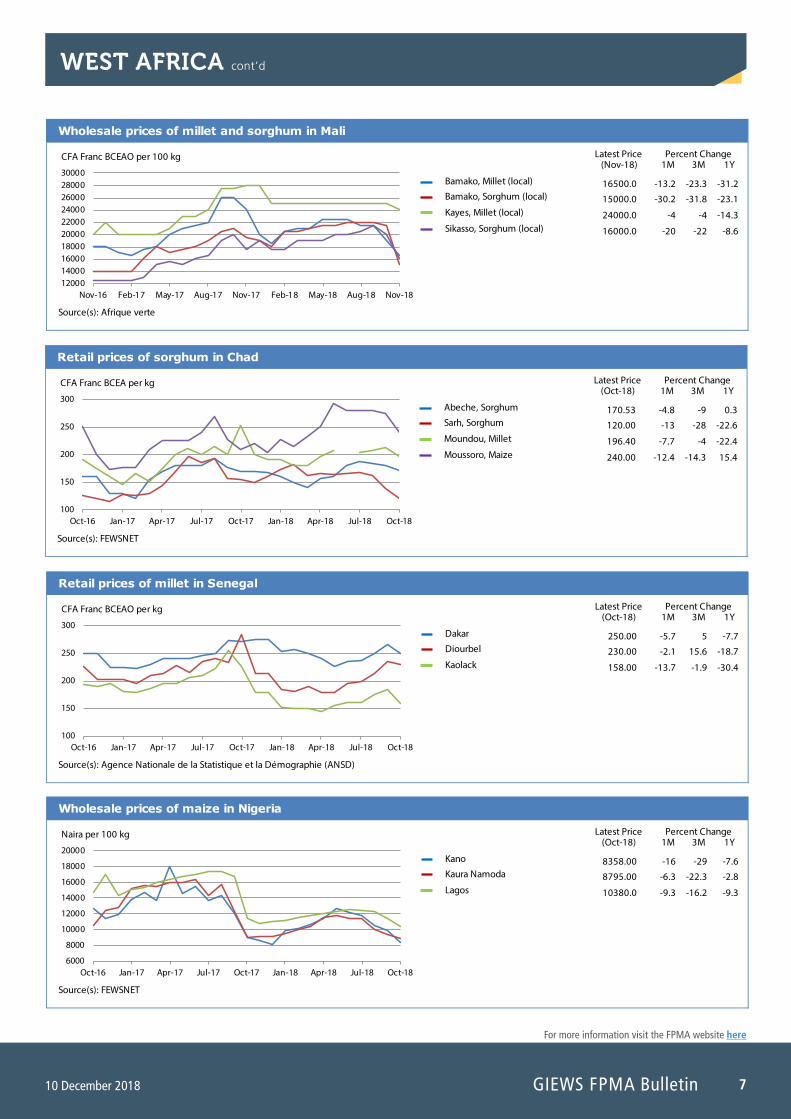

WEST AFRICA

Prices of cereals continue to generally decline in line with seasonal trends In Sahelian countries, prices of coarse grains continued to decline in November reflecting improved supplies from this year’s record harvests, imports and farmers’ destocking. Prices were generally lower than a year earlier with some exceptions, particularly in the northeast of Nigeria and the Lake Chad area, where civil insecurity and armed conflict continued to disrupt market activities. In Burkina Faso, seasonal harvest pressure on prices of millet, sorghum and maize was further compounded by sales at subsidized prices. In Niger, prices of sorghum declined seasonally in November, with imports also contributing to the downward pressure. By contrast, prices of millet generally strengthened, supported by strong domestic demand and pending the bulk of the harvest towards the end of the month. Despite the recent increases, prices remained well below their year-earlier values. In the Diffa Region, however, market supplies remained disrupted in southern parts due to insecurity. In Mali, prices of coarse grains declined significantly in November to levels well below those a year earlier as a result of this year’s bumper harvests and farmers’ destocking. However, in southern areas affected by floods and in northern and central parts where civil insecurity persists, food access was reported to be hampered. In Chad, prices of coarse grains declined in most markets in October and were lower than a year earlier, reflecting

improved market availabilities from this year’s good harvest. However, insecurity in some areas continued to disrupt market activities and access to food. In Senegal, prices of millet generally declined in October with the good 2018 harvest and were significantly down from a year earlier. Prices of imported rice, the most consumed cereal in the country, remained relatively stable, while those of husked rice, locally produced and of higher quality, recorded some increases in October, with the new harvest to begin in November. In coastal countries along the Gulf of Guinea, in Ghana, prices of maize remained stable or declined in November as a result of improved availabilities from the new harvest, while prices of mostly imported rice remained relatively stable. In Togo, prices of maize, the country’s main staple food, stabilized or declined in October following seasonal trends and were above or around their year-earlier levels. Similarly, in Benin, prices of maize declined significantly in most markets in October with the new harvest and were lower than a year earlier. In Nigeria, prices of cereals, maize in particular, declined further in October with the progress of the main 2018 harvest. Prices were well below their levels a year earlier but still relatively high, particularly in the northeast, due to persisting civil conflict, which also triggered some localized food price increases in October.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of millet and sorghum in Burkina Faso

Percent Change

12000140001600018000200002200024000260002800030000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Ouagadougou, Millet (local)

Ouagadougou, Sorghum (local)

Dori, Millet (local)

Fada N'gourma, Sorghum (local)

CFA Franc BCEAO per 100 kg

20000.0

15000.0

23500.0

19000.0

-7

-11.8

-6

0

-13

-25

-13

-9.5

-14.9

-9.1

-13

5.6

Source(s): Afrique verte

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of sorghum in Niger

Percent Change

15000170001900021000230002500027000290003100033000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Agadez

Tillaberi

Zinder

Dosso

CFA Franc BCEAO per 100 kg

23000.0

21000.0

19000.0

18000.0

-2.1

-4.5

-5

-14.3

-8

-4.5

-5

-14.3

-4.2

5

5.6

-10

Source(s): Afrique verte

7

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of millet and sorghum in Mali

Percent Change

12000140001600018000200002200024000260002800030000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Bamako, Millet (local)

Bamako, Sorghum (local)

Kayes, Millet (local)

Sikasso, Sorghum (local)

CFA Franc BCEAO per 100 kg

16500.0

15000.0

24000.0

16000.0

-13.2

-30.2

-4

-20

-23.3

-31.8

-4

-22

-31.2

-23.1

-14.3

-8.6

Source(s): Afrique verte

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of sorghum in Chad

Percent Change

100

150

200

250

300

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Abeche, Sorghum

Sarh, Sorghum

Moundou, Millet

Moussoro, Maize

CFA Franc BCEA per kg

170.53

120.00

196.40

240.00

-4.8

-13

-7.7

-12.4

-9

-28

-4

-14.3

0.3

-22.6

-22.4

15.4

Source(s): FEWSNET

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of millet in Senegal

Percent Change

100

150

200

250

300

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Dakar

Diourbel

Kaolack

CFA Franc BCEAO per kg

250.00

230.00

158.00

-5.7

-2.1

-13.7

5

15.6

-1.9

-7.7

-18.7

-30.4

Source(s): Agence Nationale de la Statistique et la Démographie (ANSD)

Latest Price(Oct-18) 1M 3M 1Y

Wholesale prices of maize in Nigeria

Percent Change

6000

8000

10000

12000

14000

16000

18000

20000

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Kano

Kaura Namoda

Lagos

Naira per 100 kg

8358.00

8795.00

10380.0

-16

-6.3

-9.3

-29

-22.3

-16.2

-7.6

-2.8

-9.3

Source(s): FEWSNET

WEST AFRICA cont’d

GIEWS FPMA Bulletin8 10 December 2018

For more information visit the FPMA website here

SOUTHERN AFRICA

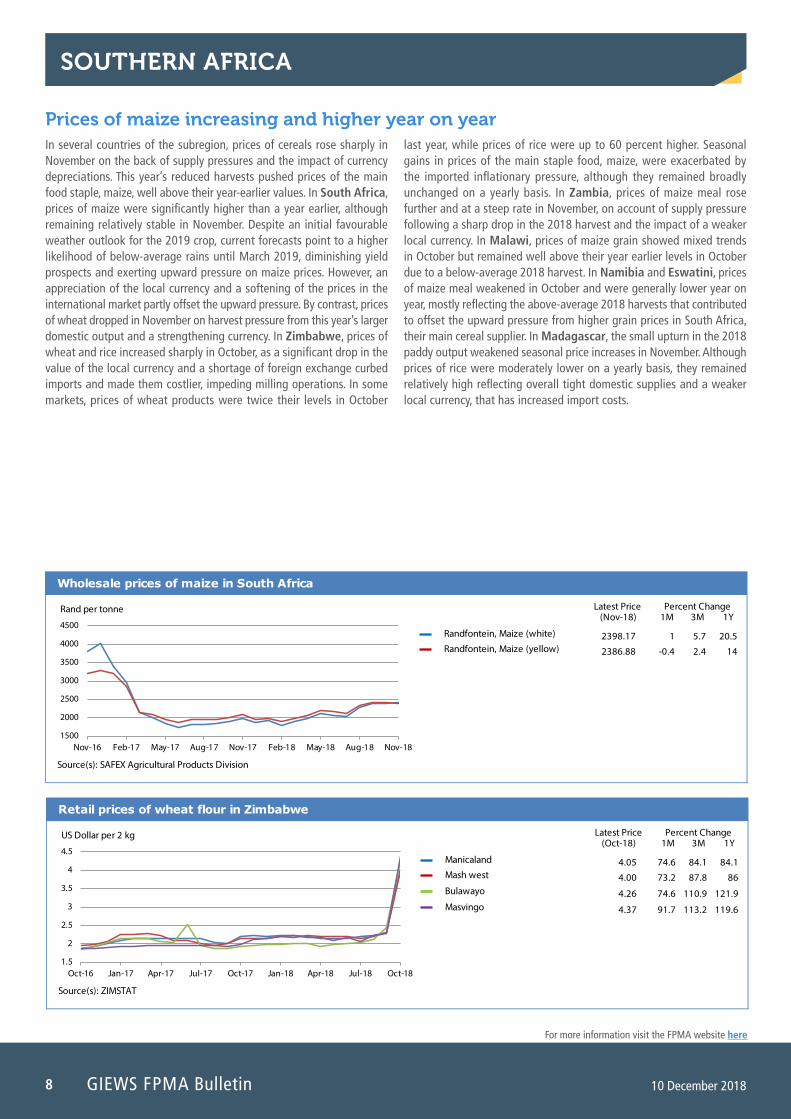

Prices of maize increasing and higher year on year In several countries of the subregion, prices of cereals rose sharply in November on the back of supply pressures and the impact of currency depreciations. This year’s reduced harvests pushed prices of the main food staple, maize, well above their year-earlier values. In South Africa, prices of maize were significantly higher than a year earlier, although remaining relatively stable in November. Despite an initial favourable weather outlook for the 2019 crop, current forecasts point to a higher likelihood of below-average rains until March 2019, diminishing yield prospects and exerting upward pressure on maize prices. However, an appreciation of the local currency and a softening of the prices in the international market partly offset the upward pressure. By contrast, prices of wheat dropped in November on harvest pressure from this year’s larger domestic output and a strengthening currency. In Zimbabwe, prices of wheat and rice increased sharply in October, as a significant drop in the value of the local currency and a shortage of foreign exchange curbed imports and made them costlier, impeding milling operations. In some markets, prices of wheat products were twice their levels in October

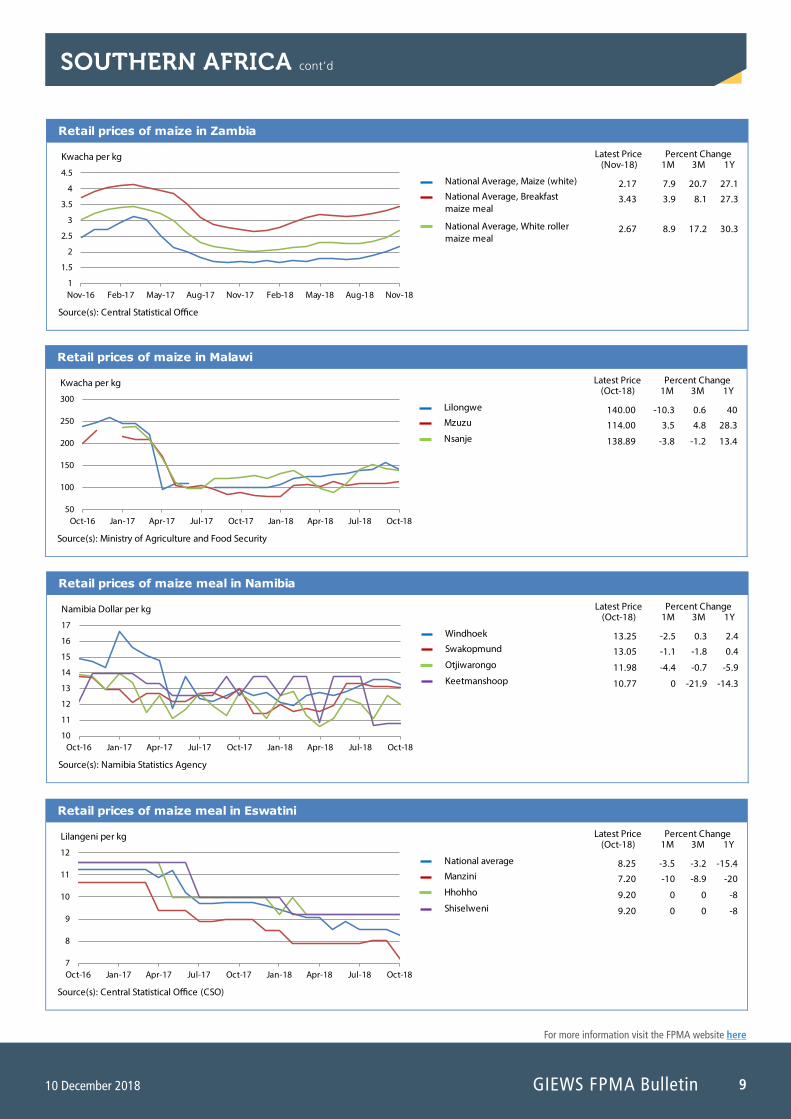

last year, while prices of rice were up to 60 percent higher. Seasonal gains in prices of the main staple food, maize, were exacerbated by the imported inflationary pressure, although they remained broadly unchanged on a yearly basis. In Zambia, prices of maize meal rose further and at a steep rate in November, on account of supply pressure following a sharp drop in the 2018 harvest and the impact of a weaker local currency. In Malawi, prices of maize grain showed mixed trends in October but remained well above their year earlier levels in October due to a below-average 2018 harvest. In Namibia and Eswatini, prices of maize meal weakened in October and were generally lower year on year, mostly reflecting the above-average 2018 harvests that contributed to offset the upward pressure from higher grain prices in South Africa, their main cereal supplier. In Madagascar, the small upturn in the 2018 paddy output weakened seasonal price increases in November. Although prices of rice were moderately lower on a yearly basis, they remained relatively high reflecting overall tight domestic supplies and a weaker local currency, that has increased import costs.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in South Africa

Percent Change

1500

2000

2500

3000

3500

4000

4500

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Randfontein, Maize (white)

Randfontein, Maize (yellow)

Rand per tonne

2398.17

2386.88

1

-0.4

5.7

2.4

20.5

14

Source(s): SAFEX Agricultural Products Division

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of wheat flour in Zimbabwe

Percent Change

1.5

2

2.5

3

3.5

4

4.5

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Manicaland

Mash west

Bulawayo

Masvingo

US Dollar per 2 kg

4.05

4.00

4.26

4.37

74.6

73.2

74.6

91.7

84.1

87.8

110.9

113.2

84.1

86

121.9

119.6

Source(s): ZIMSTAT

9

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of maize in Zambia

Percent Change

1

1.5

2

2.5

3

3.5

4

4.5

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Maize (white)

National Average, Breakfast maize meal

National Average, White roller maize meal

Kwacha per kg

2.17

3.43

2.67

7.9

3.9

8.9

20.7

8.1

17.2

27.1

27.3

30.3

Source(s): Central Statistical O�ce

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of maize in Malawi

Percent Change

50

100

150

200

250

300

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Lilongwe

Mzuzu

Nsanje

Kwacha per kg

140.00

114.00

138.89

-10.3

3.5

-3.8

0.6

4.8

-1.2

40

28.3

13.4

Source(s): Ministry of Agriculture and Food Security

SOUTHERN AFRICA cont’d

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of maize meal in Namibia

Percent Change

10

11

12

13

14

15

16

17

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Windhoek

Swakopmund

Otjiwarongo

Keetmanshoop

Namibia Dollar per kg

13.25

13.05

11.98

10.77

-2.5

-1.1

-4.4

0

0.3

-1.8

-0.7

-21.9

2.4

0.4

-5.9

-14.3

Source(s): Namibia Statistics Agency

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of maize meal in Eswatini

Percent Change

7

8

9

10

11

12

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

National average

Manzini

Hhohho

Shiselweni

Lilangeni per kg

8.25

7.20

9.20

9.20

-3.5

-10

0

0

-3.2

-8.9

0

0

-15.4

-20

-8

-8

Source(s): Central Statistical O�ce (CSO)

GIEWS FPMA Bulletin10 10 December 2018

For more information visit the FPMA website here

EAST AFRICA

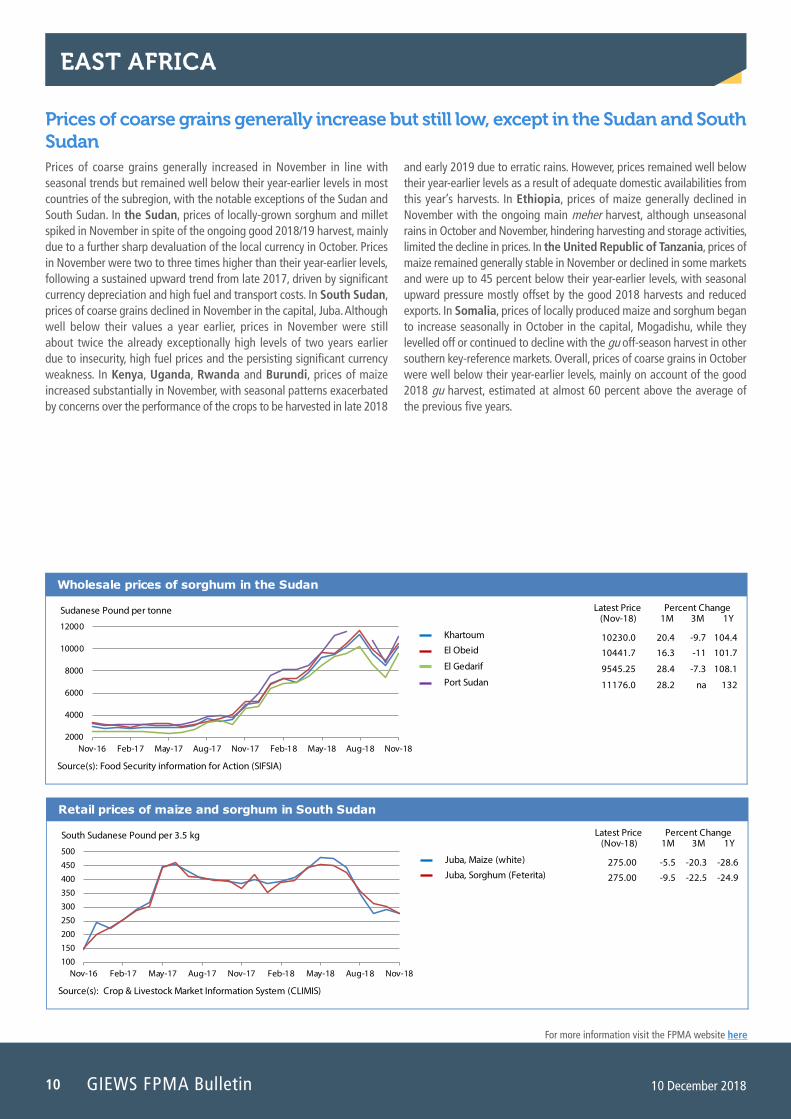

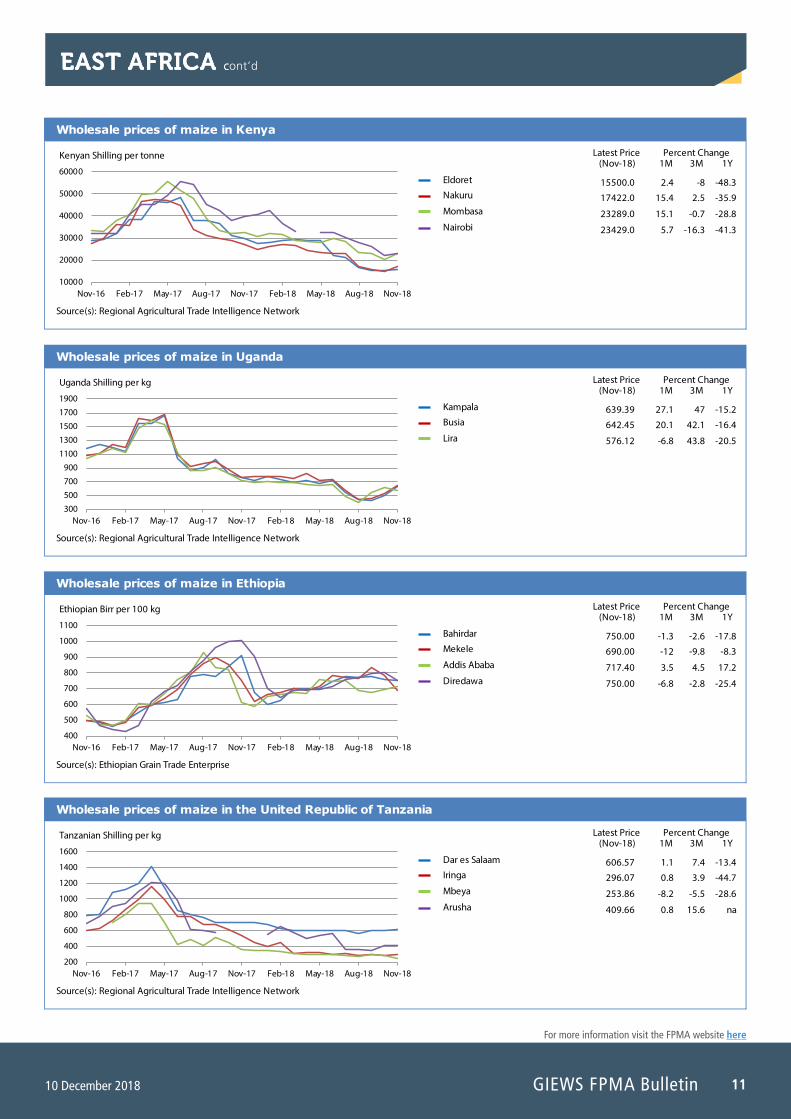

Prices of coarse grains generally increase but still low, except in the Sudan and South Sudan Prices of coarse grains generally increased in November in line with seasonal trends but remained well below their year-earlier levels in most countries of the subregion, with the notable exceptions of the Sudan and South Sudan. In the Sudan, prices of locally-grown sorghum and millet spiked in November in spite of the ongoing good 2018/19 harvest, mainly due to a further sharp devaluation of the local currency in October. Prices in November were two to three times higher than their year-earlier levels, following a sustained upward trend from late 2017, driven by significant currency depreciation and high fuel and transport costs. In South Sudan, prices of coarse grains declined in November in the capital, Juba. Although well below their values a year earlier, prices in November were still about twice the already exceptionally high levels of two years earlier due to insecurity, high fuel prices and the persisting significant currency weakness. In Kenya, Uganda, Rwanda and Burundi, prices of maize increased substantially in November, with seasonal patterns exacerbated by concerns over the performance of the crops to be harvested in late 2018

and early 2019 due to erratic rains. However, prices remained well below their year-earlier levels as a result of adequate domestic availabilities from this year’s harvests. In Ethiopia, prices of maize generally declined in November with the ongoing main meher harvest, although unseasonal rains in October and November, hindering harvesting and storage activities, limited the decline in prices. In the United Republic of Tanzania, prices of maize remained generally stable in November or declined in some markets and were up to 45 percent below their year-earlier levels, with seasonal upward pressure mostly offset by the good 2018 harvests and reduced exports. In Somalia, prices of locally produced maize and sorghum began to increase seasonally in October in the capital, Mogadishu, while they levelled off or continued to decline with the gu off-season harvest in other southern key-reference markets. Overall, prices of coarse grains in October were well below their year-earlier levels, mainly on account of the good 2018 gu harvest, estimated at almost 60 percent above the average of the previous five years.

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of maize and sorghum in South Sudan

Percent Change

100

150

200

250300

350

400

450

500

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Juba, Maize (white)

Juba, Sorghum (Feterita)

South Sudanese Pound per 3.5 kg

275.00

275.00

-5.5

-9.5

-20.3

-22.5

-28.6

-24.9

Source(s): Crop & Livestock Market Information System (CLIMIS)

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of sorghum in the Sudan

Percent Change

2000

4000

6000

8000

10000

12000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Khartoum

El Obeid

El Gedarif

Port Sudan

Sudanese Pound per tonne

10230.0

10441.7

9545.25

11176.0

20.4

16.3

28.4

28.2

-9.7

-11

-7.3

na

104.4

101.7

108.1

132

Source(s): Food Security information for Action (SIFSIA)

11

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

EAST AFRICA cont’dEAST AFRICA c

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in Kenya

Percent Change

10000

20000

30000

40000

50000

60000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Eldoret

Nakuru

Mombasa

Nairobi

Kenyan Shilling per tonne

15500.0

17422.0

23289.0

23429.0

2.4

15.4

15.1

5.7

-8

2.5

-0.7

-16.3

-48.3

-35.9

-28.8

-41.3

Source(s): Regional Agricultural Trade Intelligence Network

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in Uganda

Percent Change

300

500

700

9001100

1300

1500

1700

1900

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Kampala

Busia

Lira

Uganda Shilling per kg

639.39

642.45

576.12

27.1

20.1

-6.8

47

42.1

43.8

-15.2

-16.4

-20.5

Source(s): Regional Agricultural Trade Intelligence Network

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in Ethiopia

Percent Change

400

500

600

700

800

900

1000

1100

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Bahirdar

Mekele

Addis Ababa

Diredawa

Ethiopian Birr per 100 kg

750.00

690.00

717.40

750.00

-1.3

-12

3.5

-6.8

-2.6

-9.8

4.5

-2.8

-17.8

-8.3

17.2

-25.4

Source(s): Ethiopian Grain Trade Enterprise

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in the United Republic of Tanzania

Percent Change

200

400

600

800

1000

1200

1400

1600

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Dar es Salaam

Iringa

Mbeya

Arusha

Tanzanian Shilling per kg

606.57

296.07

253.86

409.66

1.1

0.8

-8.2

0.8

7.4

3.9

-5.5

15.6

-13.4

-44.7

-28.6

na

Source(s): Regional Agricultural Trade Intelligence Network

GIEWS FPMA Bulletin12 10 December 2018

For more information visit the FPMA website here

EAST ASIA

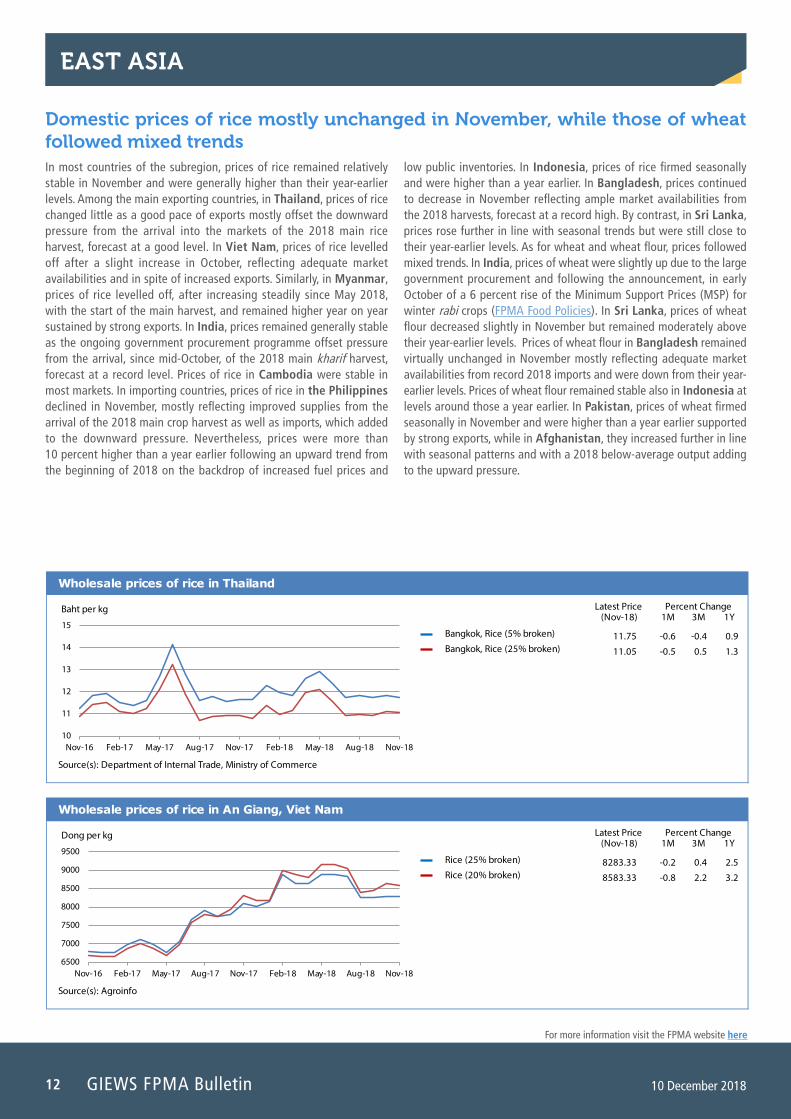

Domestic prices of rice mostly unchanged in November, while those of wheat followed mixed trends In most countries of the subregion, prices of rice remained relatively stable in November and were generally higher than their year-earlier levels. Among the main exporting countries, in Thailand, prices of rice changed little as a good pace of exports mostly offset the downward pressure from the arrival into the markets of the 2018 main rice harvest, forecast at a good level. In Viet Nam, prices of rice levelled off after a slight increase in October, reflecting adequate market availabilities and in spite of increased exports. Similarly, in Myanmar, prices of rice levelled off, after increasing steadily since May 2018, with the start of the main harvest, and remained higher year on year sustained by strong exports. In India, prices remained generally stable as the ongoing government procurement programme offset pressure from the arrival, since mid-October, of the 2018 main kharif harvest, forecast at a record level. Prices of rice in Cambodia were stable in most markets. In importing countries, prices of rice in the Philippines declined in November, mostly reflecting improved supplies from the arrival of the 2018 main crop harvest as well as imports, which added to the downward pressure. Nevertheless, prices were more than 10 percent higher than a year earlier following an upward trend from the beginning of 2018 on the backdrop of increased fuel prices and

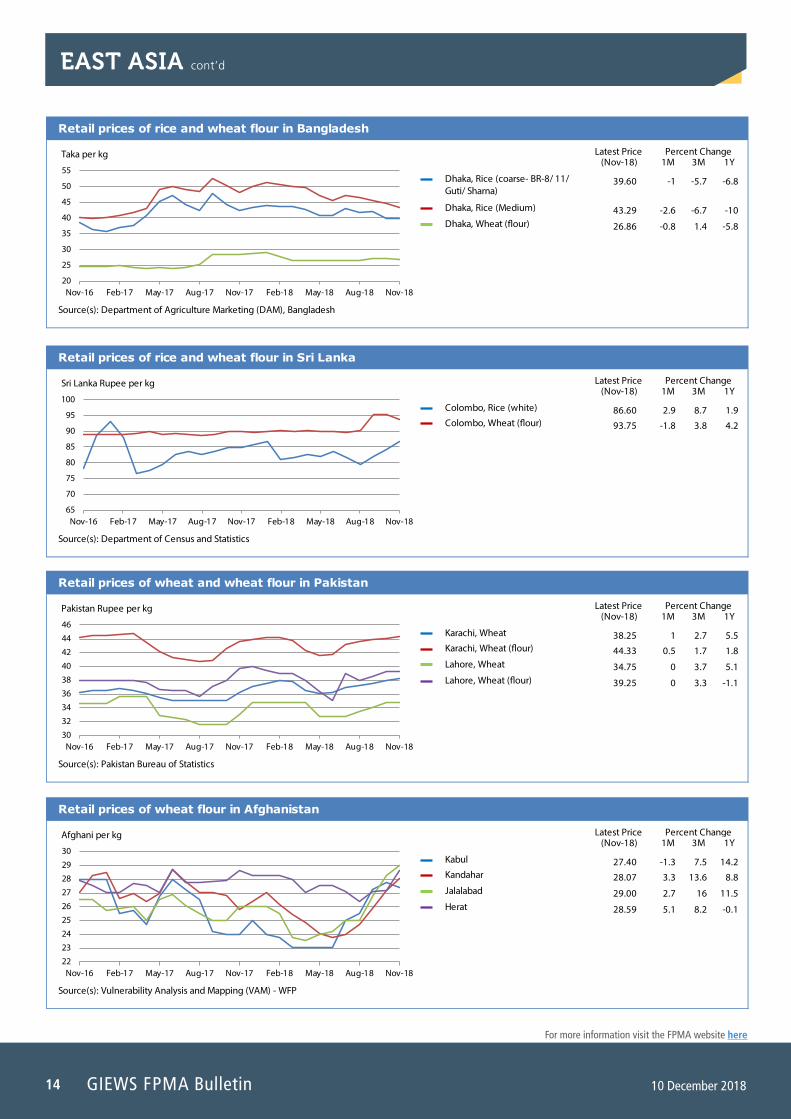

low public inventories. In Indonesia, prices of rice firmed seasonally and were higher than a year earlier. In Bangladesh, prices continued to decrease in November reflecting ample market availabilities from the 2018 harvests, forecast at a record high. By contrast, in Sri Lanka, prices rose further in line with seasonal trends but were still close to their year-earlier levels. As for wheat and wheat flour, prices followed mixed trends. In India, prices of wheat were slightly up due to the large government procurement and following the announcement, in early October of a 6 percent rise of the Minimum Support Prices (MSP) for winter rabi crops (FPMA Food Policies). In Sri Lanka, prices of wheat flour decreased slightly in November but remained moderately above their year-earlier levels. Prices of wheat flour in Bangladesh remained virtually unchanged in November mostly reflecting adequate market availabilities from record 2018 imports and were down from their year-earlier levels. Prices of wheat flour remained stable also in Indonesia at levels around those a year earlier. In Pakistan, prices of wheat firmed seasonally in November and were higher than a year earlier supported by strong exports, while in Afghanistan, they increased further in line with seasonal patterns and with a 2018 below-average output adding to the upward pressure.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of rice in Thailand

Percent Change

10

11

12

13

14

15

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Bangkok, Rice (5% broken)

Bangkok, Rice (25% broken)

Baht per kg

11.75

11.05

-0.6

-0.5

-0.4

0.5

0.9

1.3

Source(s): Department of Internal Trade, Ministry of Commerce

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of rice in An Giang, Viet Nam

Percent Change

6500

7000

7500

8000

8500

9000

9500

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Rice (25% broken)

Rice (20% broken)

Dong per kg

8283.33

8583.33

-0.2

-0.8

0.4

2.2

2.5

3.2

Source(s): Agroinfo

13

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

EAST ASIA cont’d

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of rice in Myanmar

Percent Change

300

350

400

450

500

550

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Yangon, Rice (Emata, EHYV-FQ)

Kyat per kg

521.18 0.1 3.8 14.9

Source(s): E-Trade Myanmar

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of rice in Cambodia

Percent Change

700

900

1100

13001500

1700

1900

2100

2300

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Phnom Penh

Banteay Meanchey

Battambang

Kampong Chhnang

Riel per kg

1800.00

1700.00

1650.00

2167.00

0

-5.6

0

0.7

0

0

-2.9

32.7

5.9

-5.6

10

21.7

Source(s): Cambodia Agricultural Market Information System

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of rice in the Philippines

Percent Change

35

37

39

4143

45

47

49

51

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Rice (regular milled)

National Average, Rice (well milled)

Philippine Peso per kg

43.21

46.78

-4.6

-3.5

0.6

0.7

13.7

10.9

Source(s): Bureau of Agricultural Statistics

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of rice in Indonesia

Percent Change

12500

13000

13500

14000

14500

15000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Rice

Rupiah per kg

14007.0 0.7 1.2 4.3

Source(s): Badan Pusat Statistik (BPS)

GIEWS FPMA Bulletin14 10 December 2018

For more information visit the FPMA website here

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of wheat flour in Afghanistan

Percent Change

22

23

24

2526

27

28

29

30

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Kabul

Kandahar

Jalalabad

Herat

Afghani per kg

27.40

28.07

29.00

28.59

-1.3

3.3

2.7

5.1

7.5

13.6

16

8.2

14.2

8.8

11.5

-0.1

Source(s): Vulnerability Analysis and Mapping (VAM) - WFP

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of rice and wheat flour in Sri Lanka

Percent Change

65

70

75

80

85

90

95

100

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Colombo, Rice (white)

Colombo, Wheat (�our)

Sri Lanka Rupee per kg

86.60

93.75

2.9

-1.8

8.7

3.8

1.9

4.2

Source(s): Department of Census and Statistics

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of rice and wheat flour in Bangladesh

Percent Change

20

25

30

35

40

45

50

55

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Dhaka, Rice (coarse- BR-8/ 11/ Guti/ Sharna)

Dhaka, Rice (Medium)

Dhaka, Wheat (�our)

Taka per kg

39.60

43.29

26.86

-1

-2.6

-0.8

-5.7

-6.7

1.4

-6.8

-10

-5.8

Source(s): Department of Agriculture Marketing (DAM), Bangladesh

EAST ASIA cont’d

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of wheat and wheat flour in Pakistan

Percent Change

30

32

34

3638

40

42

44

46

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Karachi, Wheat

Karachi, Wheat (�our)

Lahore, Wheat

Lahore, Wheat (�our)

Pakistan Rupee per kg

38.25

44.33

34.75

39.25

1

0.5

0

0

2.7

1.7

3.7

3.3

5.5

1.8

5.1

-1.1

Source(s): Pakistan Bureau of Statistics

15

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

CIS - ASIA AND EUROPE

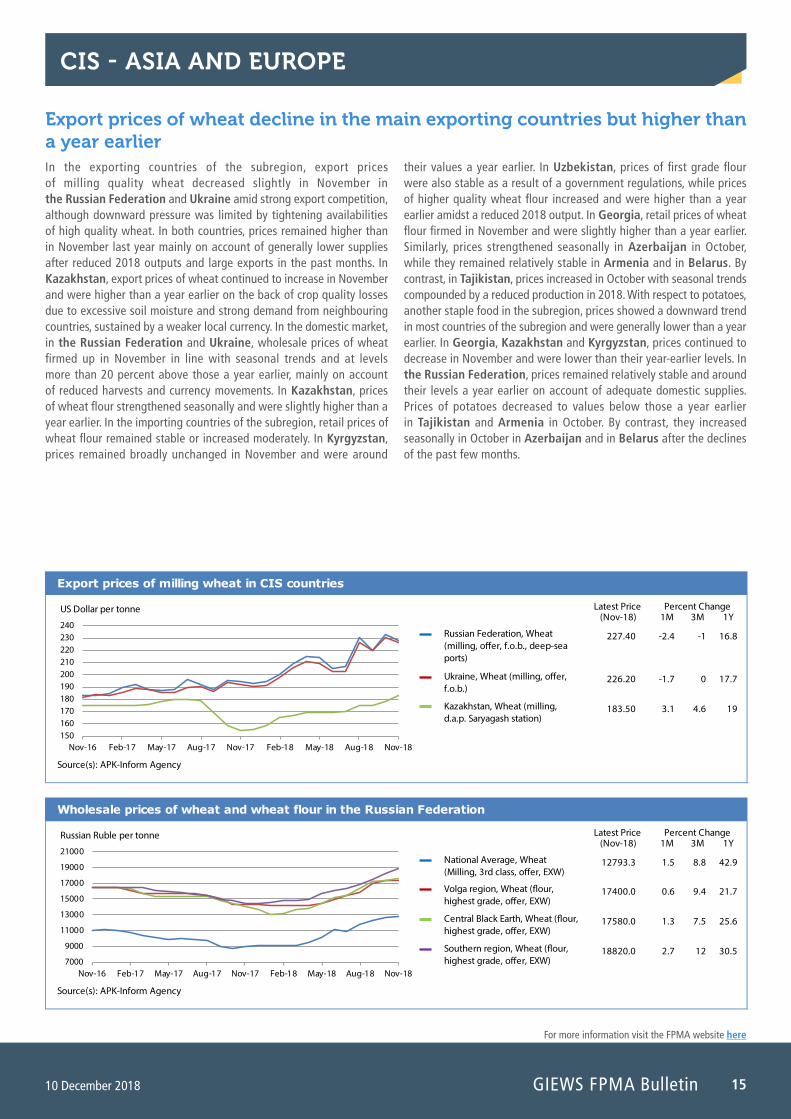

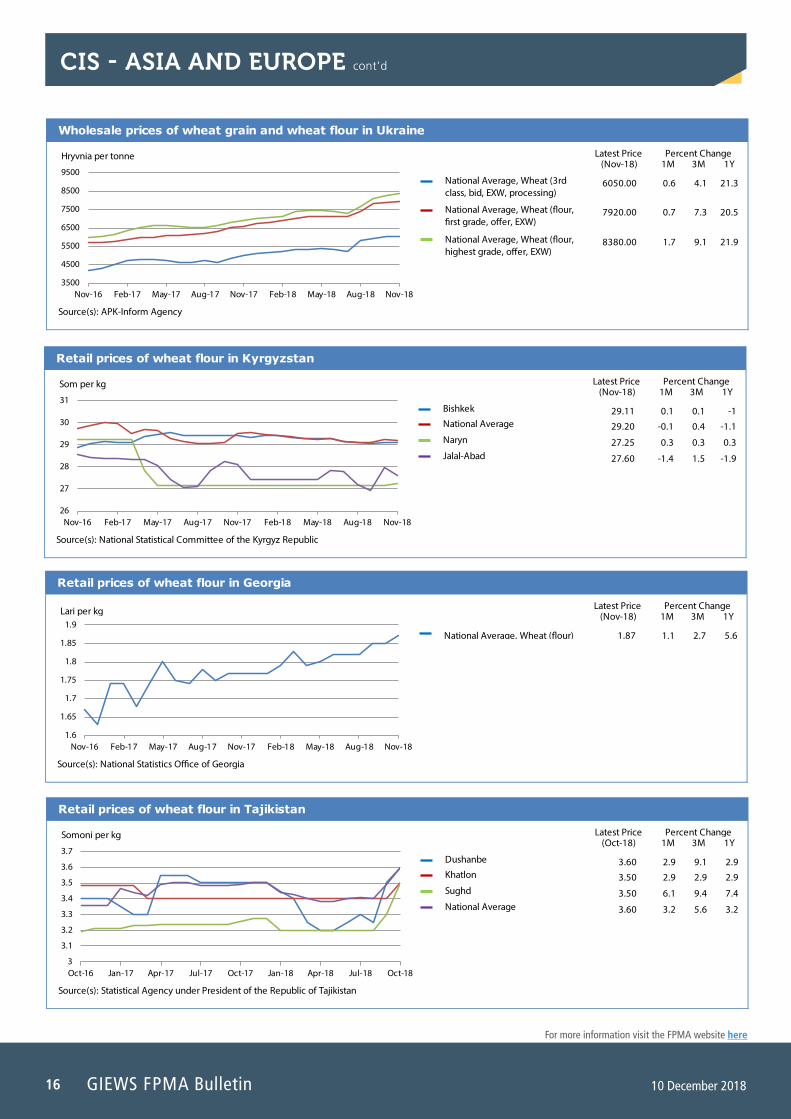

Export prices of wheat decline in the main exporting countries but higher than a year earlier In the exporting countries of the subregion, export prices of milling quality wheat decreased slightly in November in the Russian Federation and Ukraine amid strong export competition, although downward pressure was limited by tightening availabilities of high quality wheat. In both countries, prices remained higher than in November last year mainly on account of generally lower supplies after reduced 2018 outputs and large exports in the past months. In Kazakhstan, export prices of wheat continued to increase in November and were higher than a year earlier on the back of crop quality losses due to excessive soil moisture and strong demand from neighbouring countries, sustained by a weaker local currency. In the domestic market, in the Russian Federation and Ukraine, wholesale prices of wheat firmed up in November in line with seasonal trends and at levels more than 20 percent above those a year earlier, mainly on account of reduced harvests and currency movements. In Kazakhstan, prices of wheat flour strengthened seasonally and were slightly higher than a year earlier. In the importing countries of the subregion, retail prices of wheat flour remained stable or increased moderately. In Kyrgyzstan, prices remained broadly unchanged in November and were around

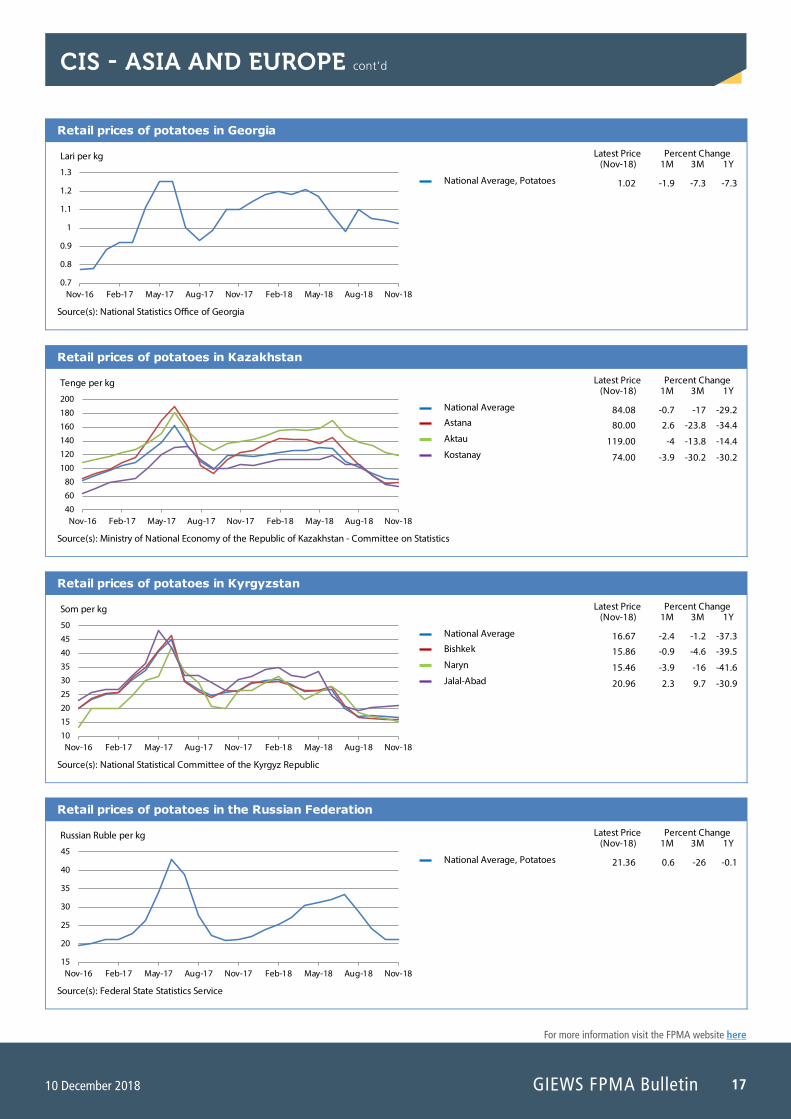

their values a year earlier. In Uzbekistan, prices of first grade flour were also stable as a result of a government regulations, while prices of higher quality wheat flour increased and were higher than a year earlier amidst a reduced 2018 output. In Georgia, retail prices of wheat flour firmed in November and were slightly higher than a year earlier. Similarly, prices strengthened seasonally in Azerbaijan in October, while they remained relatively stable in Armenia and in Belarus. By contrast, in Tajikistan, prices increased in October with seasonal trends compounded by a reduced production in 2018. With respect to potatoes, another staple food in the subregion, prices showed a downward trend in most countries of the subregion and were generally lower than a year earlier. In Georgia, Kazakhstan and Kyrgyzstan, prices continued to decrease in November and were lower than their year-earlier levels. In the Russian Federation, prices remained relatively stable and around their levels a year earlier on account of adequate domestic supplies. Prices of potatoes decreased to values below those a year earlier in Tajikistan and Armenia in October. By contrast, they increased seasonally in October in Azerbaijan and in Belarus after the declines of the past few months.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of wheat and wheat flour in the Russian Federation

Percent Change

7000

9000

11000

13000

15000

17000

19000

21000

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Wheat (Milling, 3rd class, o�er, EXW)

Volga region, Wheat (�our, highest grade, o�er, EXW)

Central Black Earth, Wheat (�our, highest grade, o�er, EXW)

Southern region, Wheat (�our, highest grade, o�er, EXW)

Russian Ruble per tonne

12793.3

17400.0

17580.0

18820.0

1.5

0.6

1.3

2.7

8.8

9.4

7.5

12

42.9

21.7

25.6

30.5

Source(s): APK-Inform Agency

Latest Price(Nov-18) 1M 3M 1Y

Export prices of milling wheat in CIS countries

Percent Change

150160170180190200210220230240

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Russian Federation, Wheat (milling, o�er, f.o.b., deep-sea ports)

Ukraine, Wheat (milling, o�er, f.o.b.)

Kazakhstan, Wheat (milling, d.a.p. Saryagash station)

US Dollar per tonne

227.40

226.20

183.50

-2.4

-1.7

3.1

-1

0

4.6

16.8

17.7

19

Source(s): APK-Inform Agency

GIEWS FPMA Bulletin16 10 December 2018

For more information visit the FPMA website here

CIS - ASIA AND EUROPE cont’d

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of wheat flour in Georgia

Percent Change

1.6

1.65

1.7

1.75

1.8

1.85

1.9

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Wheat (�our)

Lari per kg

1.87 1.1 2.7 5.6

Source(s): National Statistics O�ce of Georgia

Latest Price(Oct-18) 1M 3M 1Y

Retail prices of wheat flour in Tajikistan

Percent Change

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Dushanbe

Khatlon

Sughd

National Average

Somoni per kg

3.60

3.50

3.50

3.60

2.9

2.9

6.1

3.2

9.1

2.9

9.4

5.6

2.9

2.9

7.4

3.2

Source(s): Statistical Agency under President of the Republic of Tajikistan

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of wheat grain and wheat flour in Ukraine

Percent Change

3500

4500

5500

6500

7500

8500

9500

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Wheat (3rd class, bid, EXW, processing)

National Average, Wheat (�our, �rst grade, o�er, EXW)

National Average, Wheat (�our, highest grade, o�er, EXW)

Hryvnia per tonne

6050.00

7920.00

8380.00

0.6

0.7

1.7

4.1

7.3

9.1

21.3

20.5

21.9

Source(s): APK-Inform Agency

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of wheat flour in Kyrgyzstan

Percent Change

26

27

28

29

30

31

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Bishkek

National Average

Naryn

Jalal-Abad

Som per kg

29.11

29.20

27.25

27.60

0.1

-0.1

0.3

-1.4

0.1

0.4

0.3

1.5

-1

-1.1

0.3

-1.9

Source(s): National Statistical Committee of the Kyrgyz Republic

17

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

CIS - ASIA AND EUROPE cont’d

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of potatoes in Georgia

Percent Change

0.7

0.8

0.9

1

1.1

1.2

1.3

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Potatoes

Lari per kg

1.02 -1.9 -7.3 -7.3

Source(s): National Statistics O�ce of Georgia

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of potatoes in Kazakhstan

Percent Change

40

60

80

100120

140

160

180

200

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average

Astana

Aktau

Kostanay

Tenge per kg

84.08

80.00

119.00

74.00

-0.7

2.6

-4

-3.9

-17

-23.8

-13.8

-30.2

-29.2

-34.4

-14.4

-30.2

Source(s): Ministry of National Economy of the Republic of Kazakhstan - Committee on Statistics

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of potatoes in Kyrgyzstan

Percent Change

10

15

20

2530

35

40

45

50

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average

Bishkek

Naryn

Jalal-Abad

Som per kg

16.67

15.86

15.46

20.96

-2.4

-0.9

-3.9

2.3

-1.2

-4.6

-16

9.7

-37.3

-39.5

-41.6

-30.9

Source(s): National Statistical Committee of the Kyrgyz Republic

Latest Price(Nov-18) 1M 3M 1Y

Retail prices of potatoes in the Russian Federation

Percent Change

15

20

25

30

35

40

45

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

National Average, Potatoes

Russian Ruble per kg

21.36 0.6 -26 -0.1

Source(s): Federal State Statistics Service

GIEWS FPMA Bulletin18 10 December 2018

For more information visit the FPMA website here

CENTRAL AMERICA AND THE CARIBBEAN

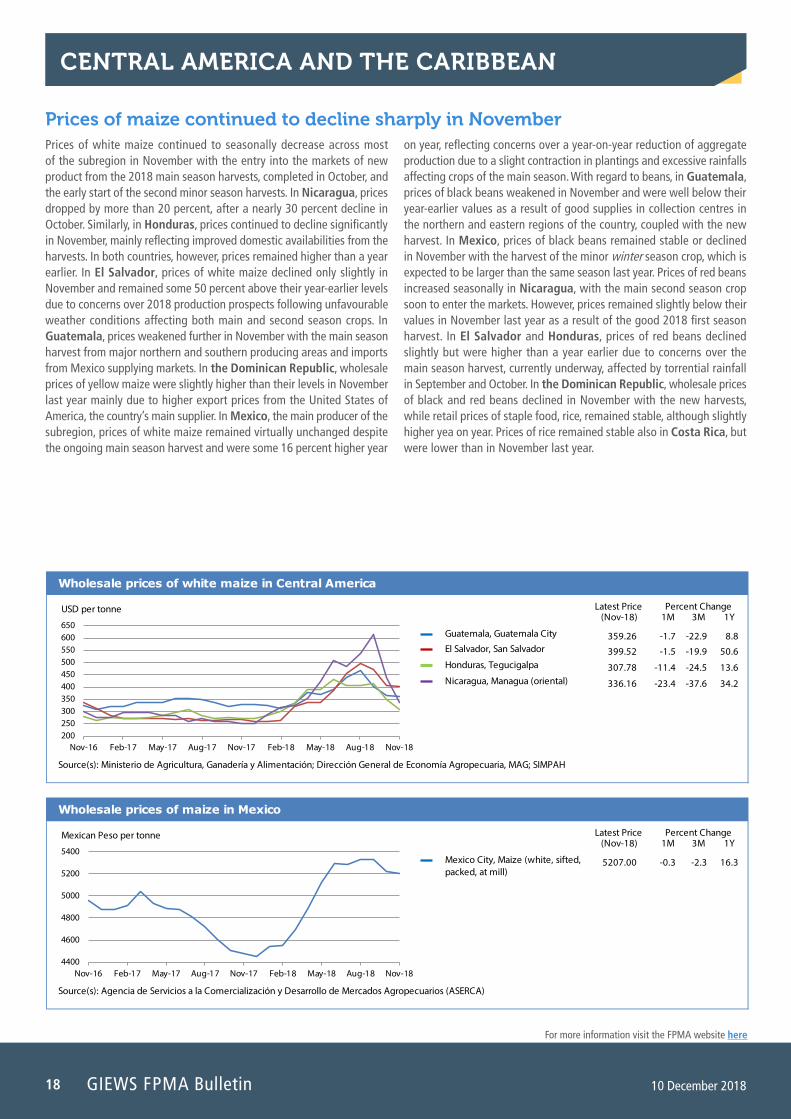

Prices of maize continued to decline sharply in November Prices of white maize continued to seasonally decrease across most of the subregion in November with the entry into the markets of new product from the 2018 main season harvests, completed in October, and the early start of the second minor season harvests. In Nicaragua, prices dropped by more than 20 percent, after a nearly 30 percent decline in October. Similarly, in Honduras, prices continued to decline significantly in November, mainly reflecting improved domestic availabilities from the harvests. In both countries, however, prices remained higher than a year earlier. In El Salvador, prices of white maize declined only slightly in November and remained some 50 percent above their year-earlier levels due to concerns over 2018 production prospects following unfavourable weather conditions affecting both main and second season crops. In Guatemala, prices weakened further in November with the main season harvest from major northern and southern producing areas and imports from Mexico supplying markets. In the Dominican Republic, wholesale prices of yellow maize were slightly higher than their levels in November last year mainly due to higher export prices from the United States of America, the country’s main supplier. In Mexico, the main producer of the subregion, prices of white maize remained virtually unchanged despite the ongoing main season harvest and were some 16 percent higher year

on year, reflecting concerns over a year-on-year reduction of aggregate production due to a slight contraction in plantings and excessive rainfalls affecting crops of the main season. With regard to beans, in Guatemala, prices of black beans weakened in November and were well below their year-earlier values as a result of good supplies in collection centres in the northern and eastern regions of the country, coupled with the new harvest. In Mexico, prices of black beans remained stable or declined in November with the harvest of the minor winter season crop, which is expected to be larger than the same season last year. Prices of red beans increased seasonally in Nicaragua, with the main second season crop soon to enter the markets. However, prices remained slightly below their values in November last year as a result of the good 2018 first season harvest. In El Salvador and Honduras, prices of red beans declined slightly but were higher than a year earlier due to concerns over the main season harvest, currently underway, affected by torrential rainfall in September and October. In the Dominican Republic, wholesale prices of black and red beans declined in November with the new harvests, while retail prices of staple food, rice, remained stable, although slightly higher yea on year. Prices of rice remained stable also in Costa Rica, but were lower than in November last year.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of maize in Mexico

Percent Change

4400

4600

4800

5000

5200

5400

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Mexico City, Maize (white, sifted, packed, at mill)

Mexican Peso per tonne

5207.00 -0.3 -2.3 16.3

Source(s): Agencia de Servicios a la Comercialización y Desarrollo de Mercados Agropecuarios (ASERCA)

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of white maize in Central America

Percent Change

200250300350400450500550600650

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Guatemala, Guatemala City

El Salvador, San Salvador

Honduras, Tegucigalpa

Nicaragua, Managua (oriental)

USD per tonne

359.26

399.52

307.78

336.16

-1.7

-1.5

-11.4

-23.4

-22.9

-19.9

-24.5

-37.6

8.8

50.6

13.6

34.2

Source(s): Ministerio de Agricultura, Ganadería y Alimentación; Dirección General de Economía Agropecuaria, MAG; SIMPAH

19

For more information visit the FPMA website here

10 December 2018 GIEWS FPMA Bulletin

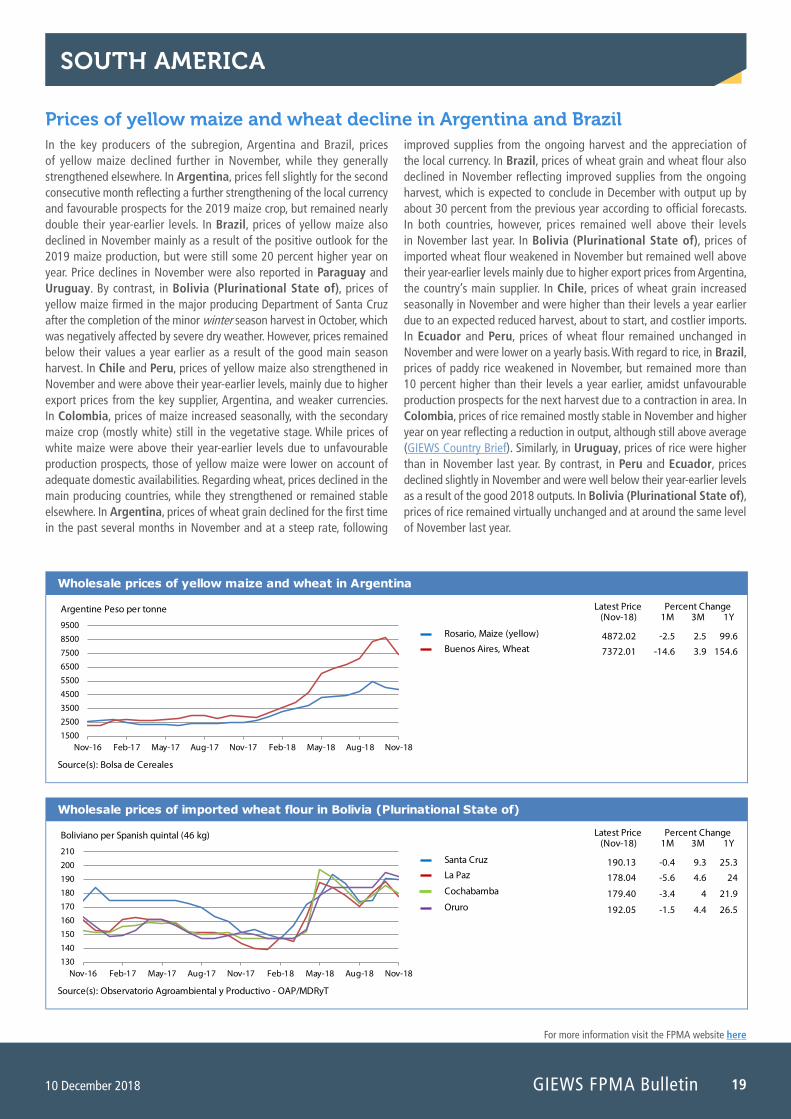

SOUTH AMERICA

Prices of yellow maize and wheat decline in Argentina and Brazil In the key producers of the subregion, Argentina and Brazil, prices of yellow maize declined further in November, while they generally strengthened elsewhere. In Argentina, prices fell slightly for the second consecutive month reflecting a further strengthening of the local currency and favourable prospects for the 2019 maize crop, but remained nearly double their year-earlier levels. In Brazil, prices of yellow maize also declined in November mainly as a result of the positive outlook for the 2019 maize production, but were still some 20 percent higher year on year. Price declines in November were also reported in Paraguay and Uruguay. By contrast, in Bolivia (Plurinational State of), prices of yellow maize firmed in the major producing Department of Santa Cruz after the completion of the minor winter season harvest in October, which was negatively affected by severe dry weather. However, prices remained below their values a year earlier as a result of the good main season harvest. In Chile and Peru, prices of yellow maize also strengthened in November and were above their year-earlier levels, mainly due to higher export prices from the key supplier, Argentina, and weaker currencies. In Colombia, prices of maize increased seasonally, with the secondary maize crop (mostly white) still in the vegetative stage. While prices of white maize were above their year-earlier levels due to unfavourable production prospects, those of yellow maize were lower on account of adequate domestic availabilities. Regarding wheat, prices declined in the main producing countries, while they strengthened or remained stable elsewhere. In Argentina, prices of wheat grain declined for the first time in the past several months in November and at a steep rate, following

improved supplies from the ongoing harvest and the appreciation of the local currency. In Brazil, prices of wheat grain and wheat flour also declined in November reflecting improved supplies from the ongoing harvest, which is expected to conclude in December with output up by about 30 percent from the previous year according to official forecasts. In both countries, however, prices remained well above their levels in November last year. In Bolivia (Plurinational State of), prices of imported wheat flour weakened in November but remained well above their year-earlier levels mainly due to higher export prices from Argentina, the country’s main supplier. In Chile, prices of wheat grain increased seasonally in November and were higher than their levels a year earlier due to an expected reduced harvest, about to start, and costlier imports. In Ecuador and Peru, prices of wheat flour remained unchanged in November and were lower on a yearly basis. With regard to rice, in Brazil, prices of paddy rice weakened in November, but remained more than 10 percent higher than their levels a year earlier, amidst unfavourable production prospects for the next harvest due to a contraction in area. In Colombia, prices of rice remained mostly stable in November and higher year on year reflecting a reduction in output, although still above average (GIEWS Country Brief). Similarly, in Uruguay, prices of rice were higher than in November last year. By contrast, in Peru and Ecuador, prices declined slightly in November and were well below their year-earlier levels as a result of the good 2018 outputs. In Bolivia (Plurinational State of), prices of rice remained virtually unchanged and at around the same level of November last year.

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of yellow maize and wheat in Argentina

Percent Change

1500

2500

3500

45005500

6500

7500

8500

9500

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Rosario, Maize (yellow)

Buenos Aires, Wheat

Argentine Peso per tonne

4872.02

7372.01

-2.5

-14.6

2.5

3.9

99.6

154.6

Source(s): Bolsa de Cereales

Latest Price(Nov-18) 1M 3M 1Y

Wholesale prices of imported wheat flour in Bolivia (Plurinational State of)

Percent Change

130

140

150

160170

180

190

200

210

Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18

Santa Cruz

La Paz

Cochabamba

Oruro

Boliviano per Spanish quintal (46 kg)

190.13

178.04

179.40

192.05

-0.4

-5.6

-3.4

-1.5

9.3

4.6

4

4.4

25.3

24

21.9

26.5

Source(s): Observatorio Agroambiental y Productivo - OAP/MDRyT

This bulletin is prepared by the Food Price Monitoring and Analysis (FPMA) Team of the Global Information and Early Warning System on Food and Agriculture (GIEWS) in the Trade and Markets Division of FAO. It contains latest information and analysis on domestic prices of basic foods mainly in developing countries, complementing FAO analysis on international markets. It provides early warning on high food prices at country level that may negatively affect food security.

This report is based on information available up to early December 2018.

All the data used in the analysis can be found in the FPMA Tool at: www.fao.org/giews/food-prices/tool/public/index.html#/home

For more information visit the FPMA Website at: www.fao.org/giews/food-prices.

Enquiries may be directed to:

GIEWS Food Price Monitoring and Analysis (FPMA) Team

Trade and Markets Division (EST)

Food and Agriculture Organization of the United Nations (FAO)

Viale delle Terme di Caracalla

00153 Rome, Italy

E-mail: [email protected]

The Global Information and Early Warning System on Food and Agriculture (GIEWS) has set up a mailing list to disseminate

its reports.

To subscribe, send an email to FAO’s mail server [email protected]. Leave the subject blank and then put in the first line of

the message the following:

subscribe GIEWSAlertsWorld-L

To unsubscribe from the GIEWSAlertsWorld-L list, put in the first line of the message the following:

unsubscribe GIEWSAlertsWorld-L

The designations employed and the presentation of material in this information product do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations (FAO) concerning the legal or development status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. The mention of specific companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by FAO in preference to others of a similar nature that are not mentioned.

The views expressed in this information product are those of the author(s) and do not necessarily reflect the views or policies of FAO.

© FAO, 2018

Some rights reserved. This work is made available under the Creative Commons Attribution-NonCommercial-ShareAlike 3.0 IGO licence (CC BY-NC-SA 3.0 IGO; https://creativecommons.org/licenses/by-nc-sa/3.0/igo/legalcode).

Under the terms of this licence, this work may be copied, redistributed and adapted for non-commercial purposes, provided that the work is appropriately cited. In any use of this work, there should be no suggestion that FAO endorses any specific organization, products or services. The use of the FAO logo is not permitted. If the work is adapted, then it must be licensed under the same or equivalent Creative Commons license. If a translation of this work is created, it must include the following disclaimer along with the required citation: “This translation was not created by the Food and Agriculture Organization of the United Nations (FAO). FAO is not responsible for the content or accuracy of this translation. The original [Language] edition shall be the authoritative edition.

Disputes arising under the licence that cannot be settled amicably will be resolved by mediation and arbitration as described in Article 8 of the licence except as otherwise provided herein. The applicable mediation rules will be the mediation rules of the World Intellectual Property Organization http://www.wipo.int/amc/en/mediation/rules and any arbitration will be in accordance with the Arbitration Rules of the United Nations Commission on International Trade Law (UNCITRAL).

Third-party materials. Users wishing to reuse material from this work that is attributed to a third party, such as tables, figures or images, are responsible for determining whether permission is needed for that reuse and for obtaining permission from the copyright holder. The risk of claims resulting from infringement of any third-party-owned component in the work rests solely with the user.

Sales, rights and licensing. FAO information products are available on the FAO website (www.fao.org/publications) and can be purchased through publications‑[email protected]. Requests for commercial use should be submitted via: www.fao.org/contact-us/licence-request. Queries regarding rights and licensing should be submitted to: [email protected].

CA2766EN/1/12.18GIEWS FPMA Bulletin | 10 December 2018