Embed Size (px)

Citation preview

Freight Trends and Rail Capacity

Transportation leadership you can trust.

presented topresented to

2008 Ohio Conference on Freight2008 Ohio Conference on FreightToledo, OhioToledo, Ohio

presented bypresented byLance R. GrenzebackLance R. GrenzebackCambridge Systematics, Inc.Cambridge Systematics, Inc.

September 16, 2008September 16, 2008

2

3

Presentation

Freight Transportation and the Economy

Freight Transportation Demand

Rail Freight Transportation Capacity

Authorization Issues

4

Freight Transportation and the Economy

5

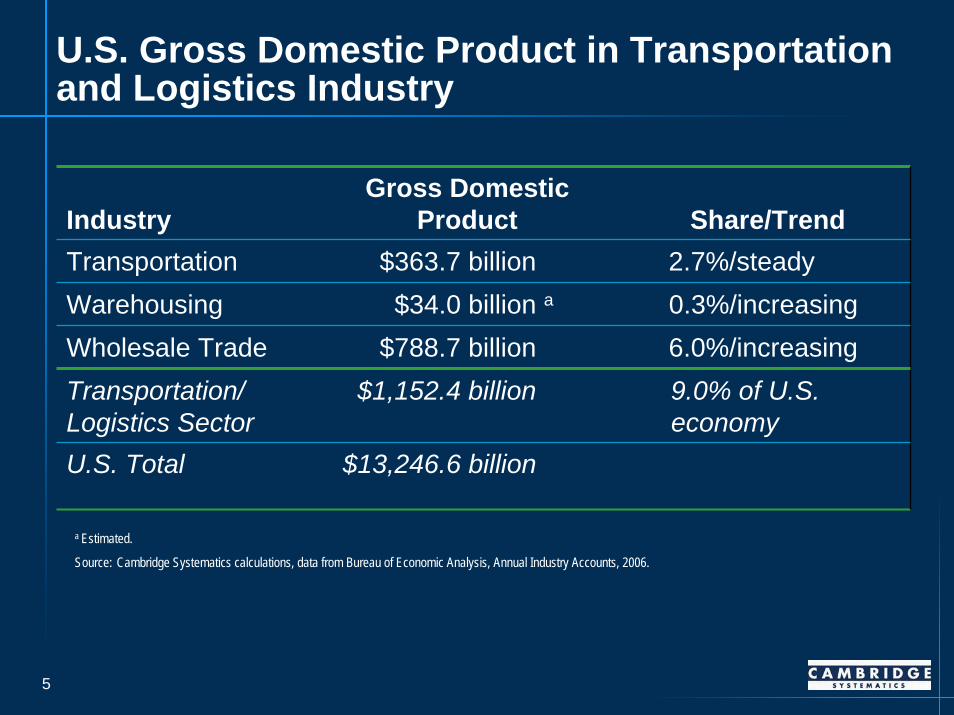

U.S. Gross Domestic Product in Transportation and Logistics Industry

IndustryGross Domestic

Product Share/TrendTransportation $363.7 billion 2.7%/steadyWarehousing $34.0 billion a 0.3%/increasingWholesale Trade $788.7 billion 6.0%/increasingTransportation/ Logistics Sector

$1,152.4 billion 9.0% of U.S.economy

U.S. Total $13,246.6 billion

a Estimated.

Source: Cambridge Systematics calculations, data from Bureau of Economic Analysis, Annual Industry Accounts, 2006.

6

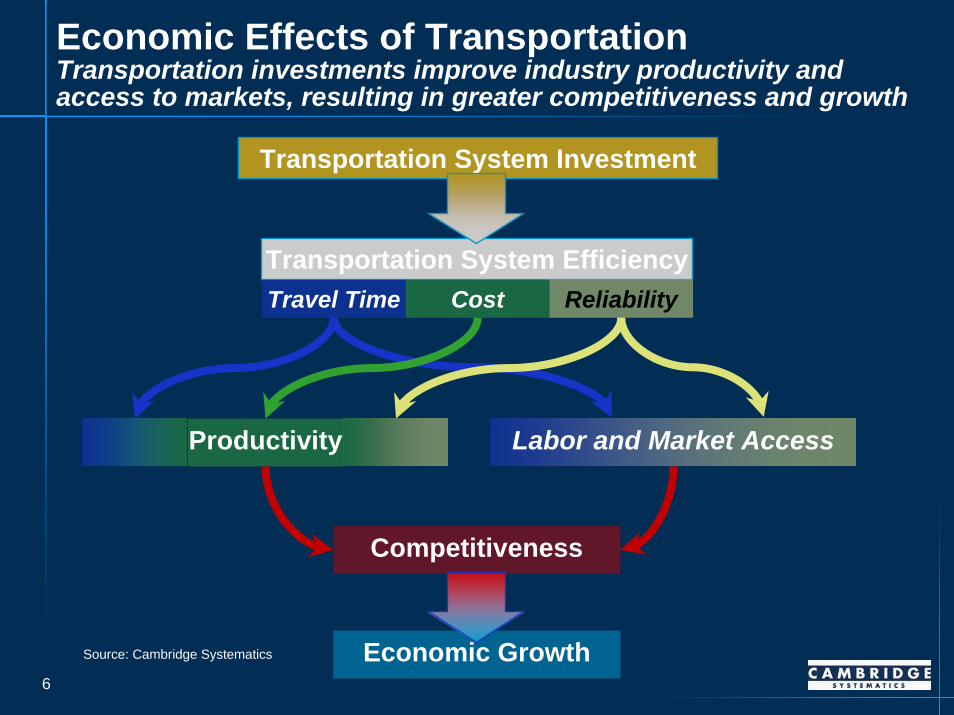

Economic Effects of TransportationTransportation investments improve industry productivity and access to markets, resulting in greater competitiveness and growth

Transportation System Investment

Transportation System EfficiencyTravel Time Cost

Labor and Market Access

Competitiveness

Economic Growth

Reliability

Productivity

Source: Cambridge Systematics

7

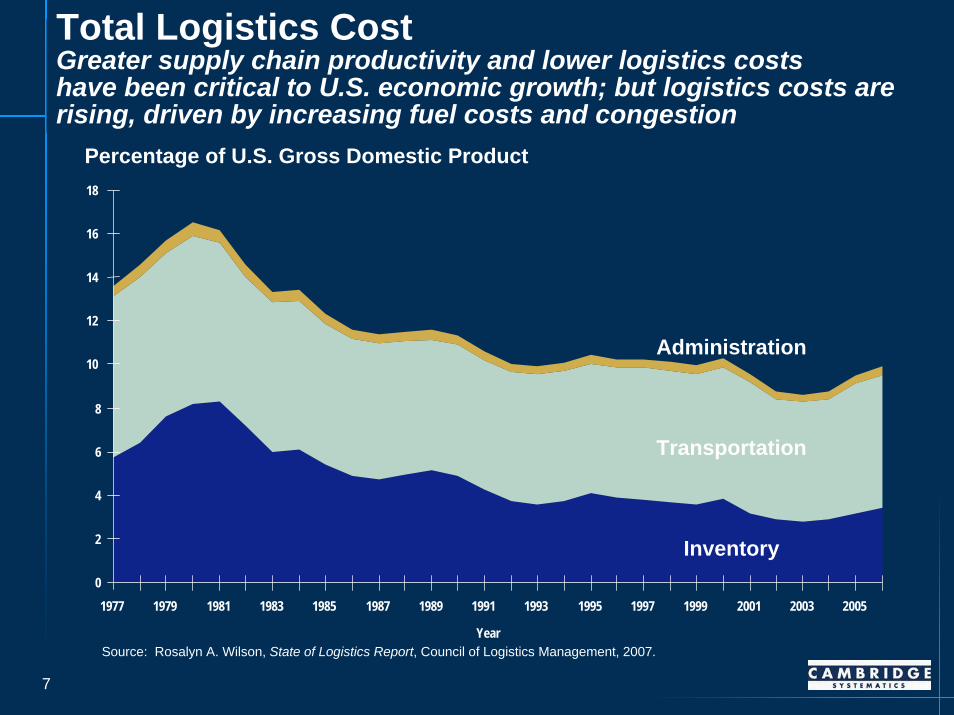

Total Logistics CostGreater supply chain productivity and lower logistics costs have been critical to U.S. economic growth; but logistics costs are rising, driven by increasing fuel costs and congestion

Percentage of U.S. Gross Domestic Product

0

2

4

6

8

10

12

14

16

18

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Administration

Transportation

Inventory

YearSource: Rosalyn A. Wilson, State of Logistics Report, Council of Logistics Management, 2007.

8

Freight Transportation Demand

9

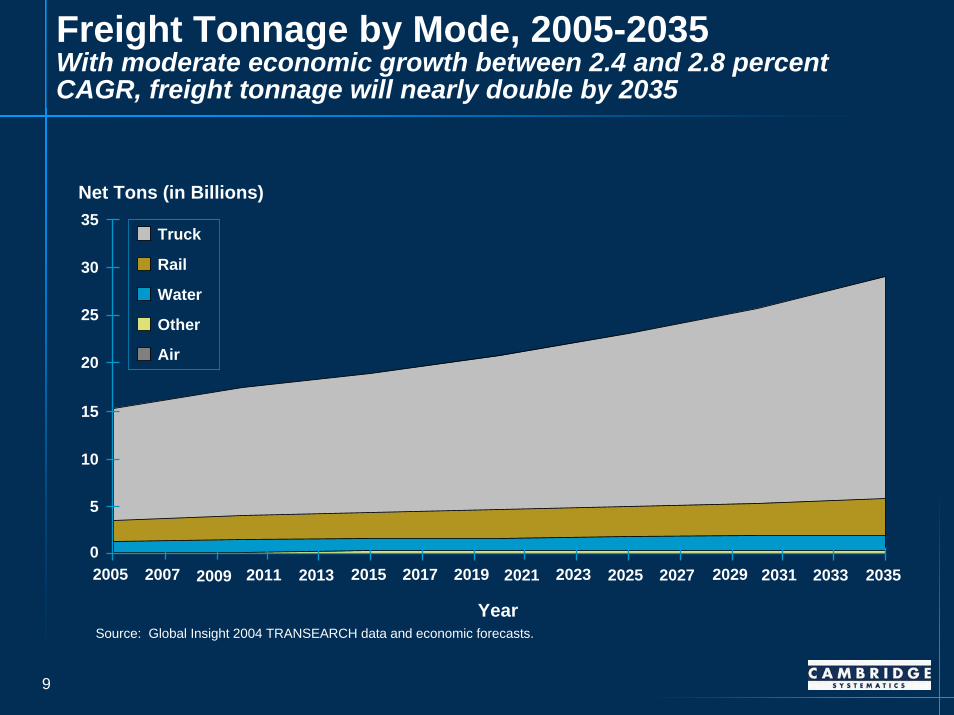

Freight Tonnage by Mode, 2005-2035With moderate economic growth between 2.4 and 2.8 percent CAGR, freight tonnage will nearly double by 2035

Net Tons (in Billions)

Truck

Rail

Water

Other

Air

5

10

15

20

25

30

35

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

Year

0

Source: Global Insight 2004 TRANSEARCH data and economic forecasts.

10

Freight DemandThe four major drivers behind the increasing freight demand are –

Consumption • Growing population: from 300 million to 380 million by 2035

Production• Expanding durable and non-durable goods manufacturing

Trade• Growing imports and exports

Supply Chain Practices• Changing logistics strategies and consumer demands

11

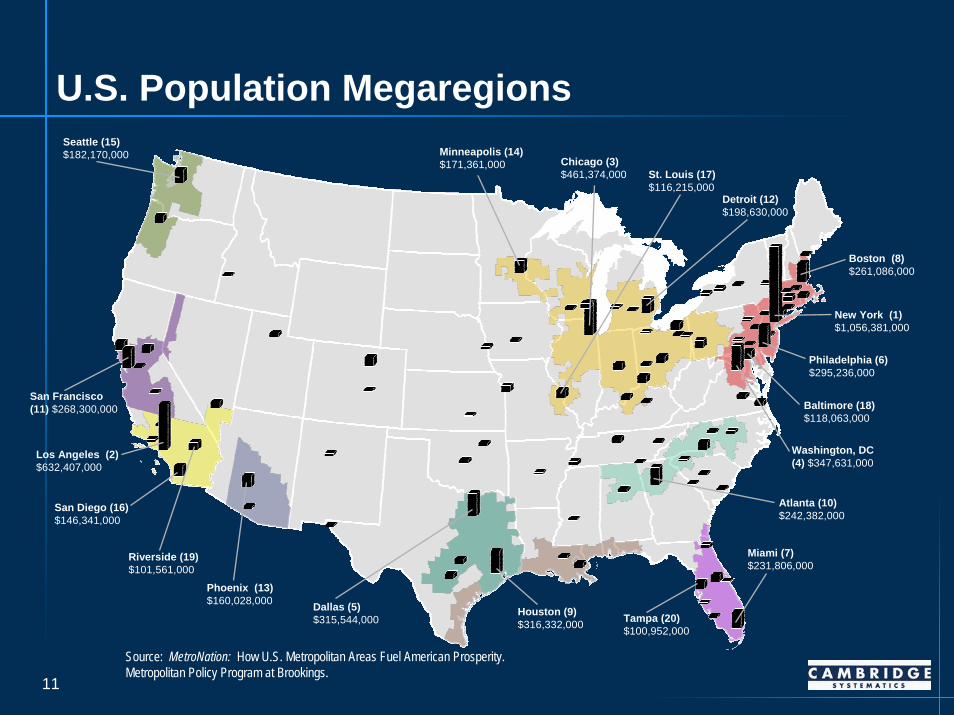

U.S. Population Megaregions

Source: MetroNation: How U.S. Metropolitan Areas Fuel American Prosperity. Metropolitan Policy Program at Brookings.

Seattle (15)$182,170,000

New York (1)$1,056,381,000

Los Angeles (2)$632,407,000

Chicago (3)$461,374,000

Washington, DC (4) $347,631,000

Dallas (5)$315,544,000

Philadelphia (6)$295,236,000

Miami (7) $231,806,000

Boston (8)$261,086,000

Houston (9)$316,332,000

Atlanta (10)$242,382,000

San Francisco (11) $268,300,000

Detroit (12)$198,630,000

Phoenix (13)$160,028,000

Minneapolis (14)$171,361,000

San Diego (16)$146,341,000

St. Louis (17)$116,215,000

Baltimore (18)$118,063,000

Riverside (19)$101,561,000

Tampa (20) $100,952,000

12

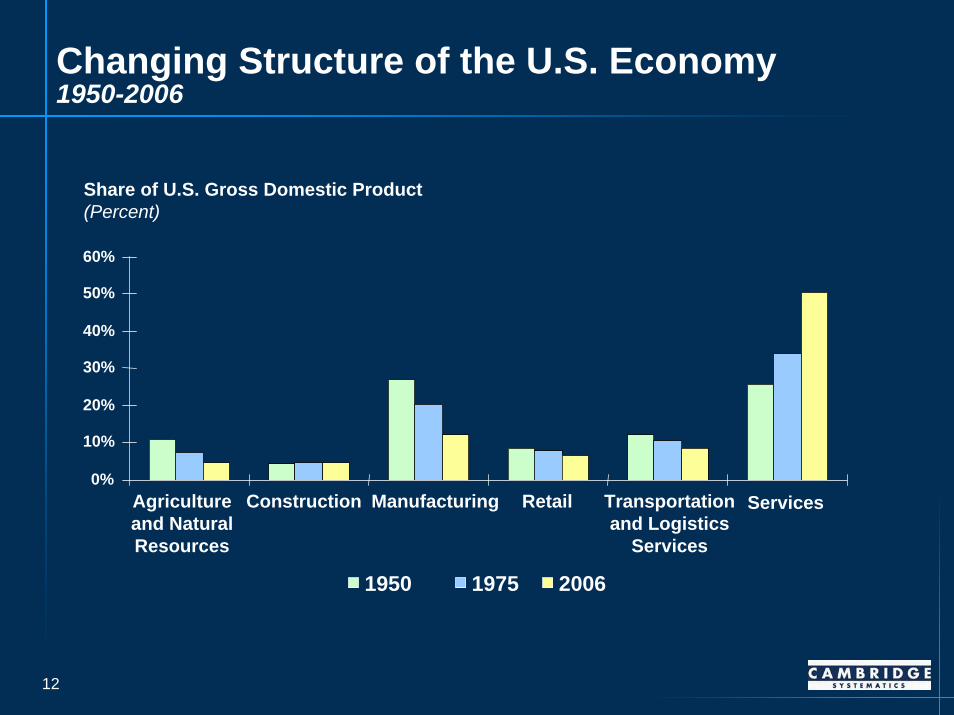

Changing Structure of the U.S. Economy1950-2006

0%

10%

20%

30%

40%

50%

60%

Agriculture and Natural Resources

Construction Manufacturing Retail Transportation and Logistics

Services

Services

Share of U.S. Gross Domestic Product(Percent)

1950 1975 2006

13

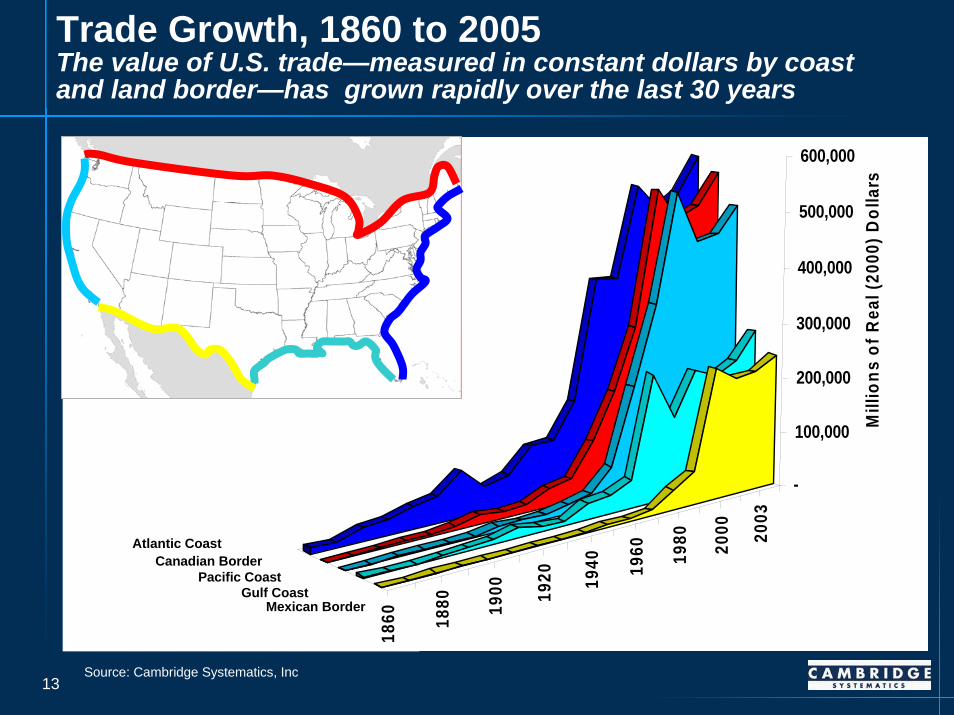

Trade Growth, 1860 to 2005The value of U.S. trade—measured in constant dollars by coast and land border—has grown rapidly over the last 30 years

1860 18

80 1900 19

20 1940 19

60 1980 20

00 2003

-

100,000

200,000

300,000

400,000

500,000

600,000

Mill

ions

of R

eal (

2000

) Dol

lars

Atlantic CoastCanadian Border

Pacific CoastGulf Coast

Mexican Border

Source: Cambridge Systematics, Inc

14

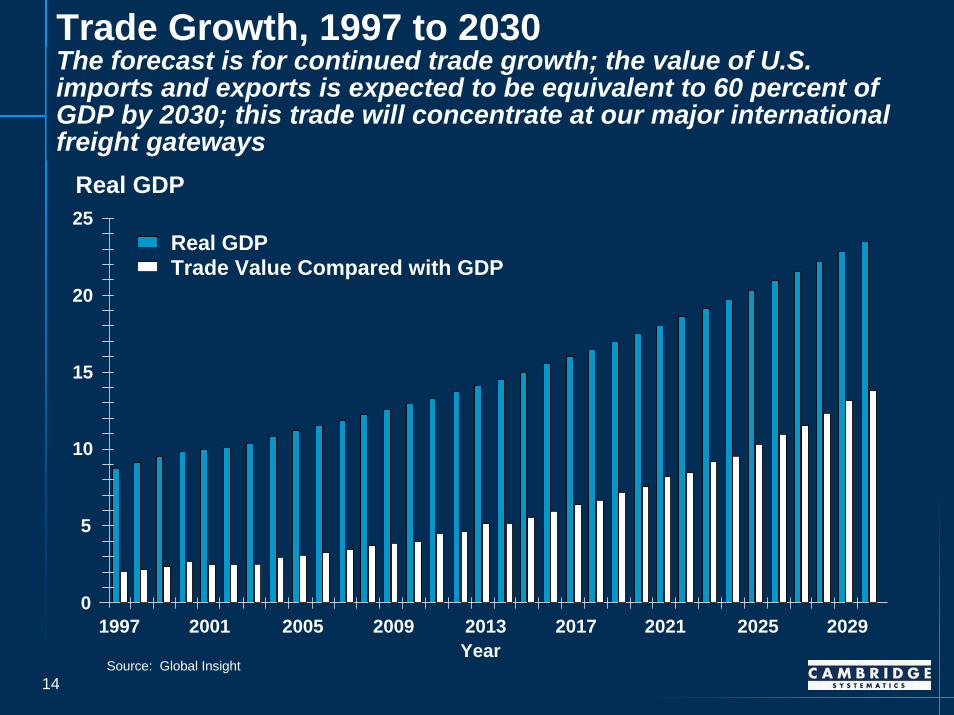

Trade Growth, 1997 to 2030The forecast is for continued trade growth; the value of U.S. imports and exports is expected to be equivalent to 60 percent of GDP by 2030; this trade will concentrate at our major international freight gateways

Real GDP

0

5

10

15

20

25

1997 2001 2005 2009 2013 2017 2021 2025 2029Year

Real GDPTrade Value Compared with GDP

Source: Global Insight

15

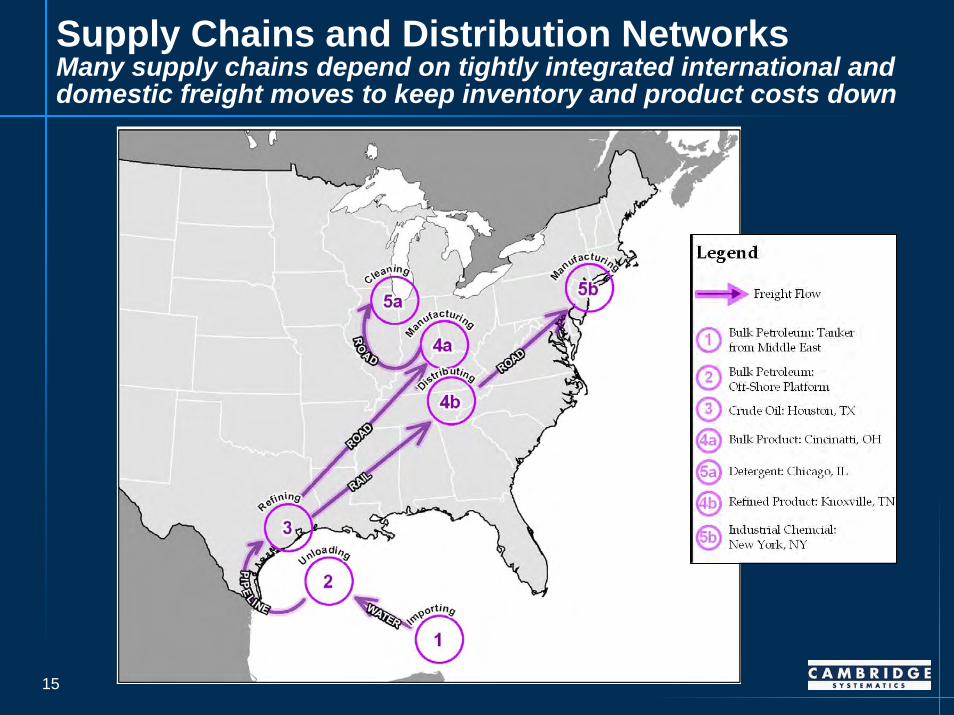

Supply Chains and Distribution NetworksMany supply chains depend on tightly integrated international and domestic freight moves to keep inventory and product costs down

16

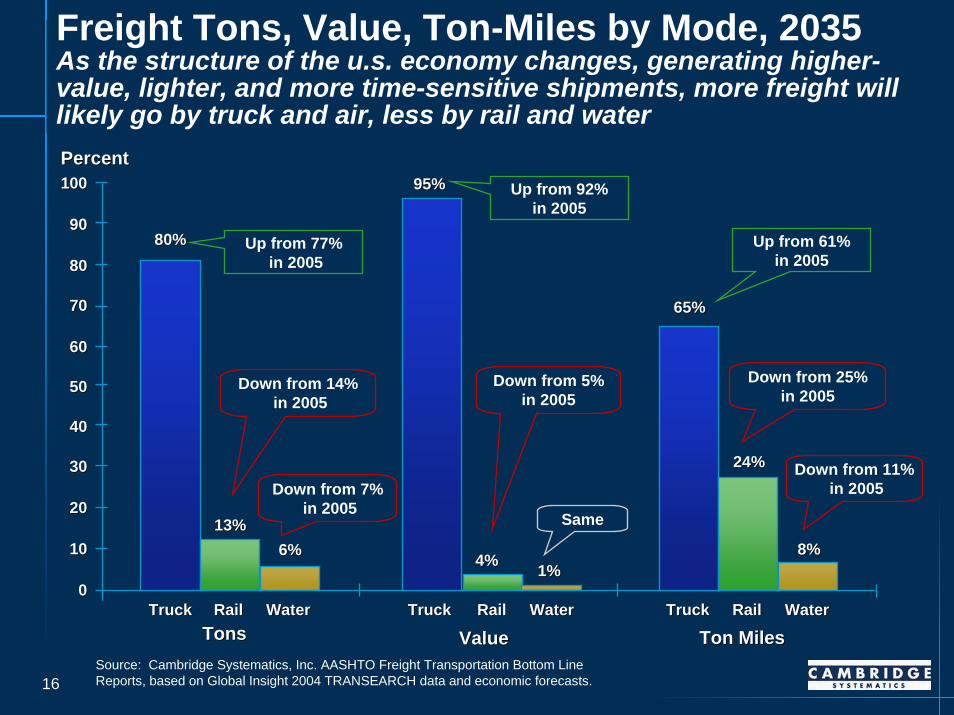

Freight Tons, Value, Ton-Miles by Mode, 2035As the structure of the u.s. economy changes, generating higher-value, lighter, and more time-sensitive shipments, more freight will likely go by truck and air, less by rail and waterPercentPercent100

Up from 77%in 2005

Up from 92% in 2005

Up from 61% in 2005

Down from 14% in 2005

Down from 5% in 2005

Down from 25% in 2005

Same

Down from 11%in 2005

100 95%95%

909080%80%

8080

7070 65%65%

6060

5050

4040

24%24%3030

2020

1010

00

TonsTons ValueValue Ton MilesTon Miles

13%13%

Down from 7%in 2005

6%6% 8%8%4%4%

1%1%

TruckTruck TruckTruck TruckTruckRailRail RailRail RailRailWaterWater WaterWater WaterWater

Source: Cambridge Systematics, Inc. AASHTO Freight Transportation Bottom Line Reports, based on Global Insight 2004 TRANSEARCH data and economic forecasts.

17

Rail Freight Transportation Capacity

18

National Rail Freight Capacity Study

Requested by the National Surface Transportation Policy and Revenue Study Commission

Commissioned by the Association of American Railroads

Prepared by Cambridge Systematics, Inc.

19

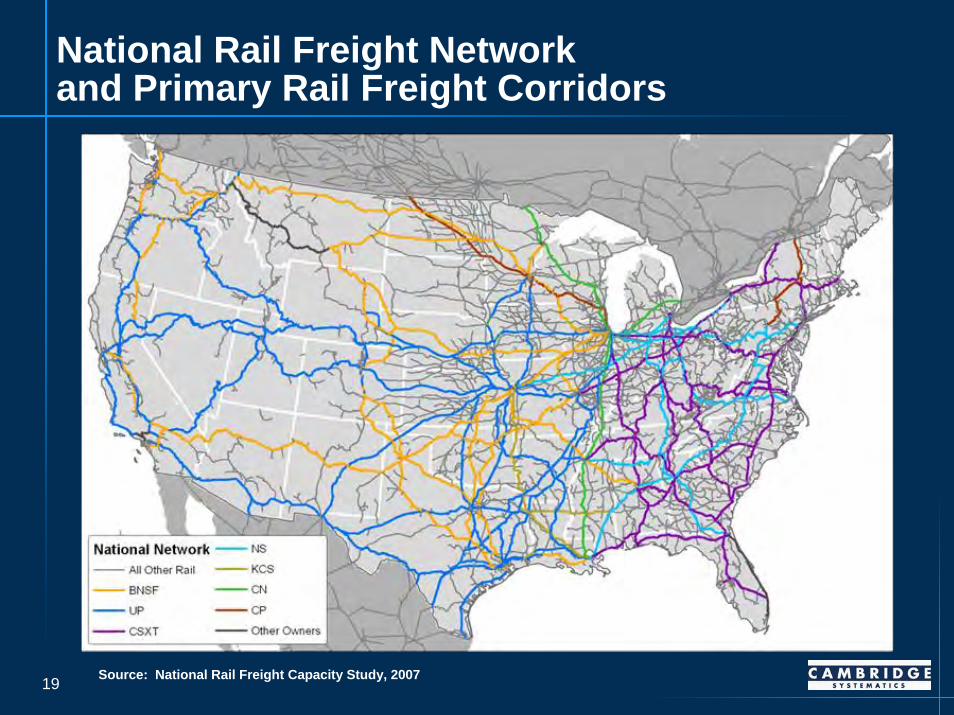

National Rail Freight Networkand Primary Rail Freight Corridors

Source: National Rail Freight Capacity Study, 2007

20

Primary Rail Freight Corridors

Source: National Rail Freight Capacity Study, 2007

21

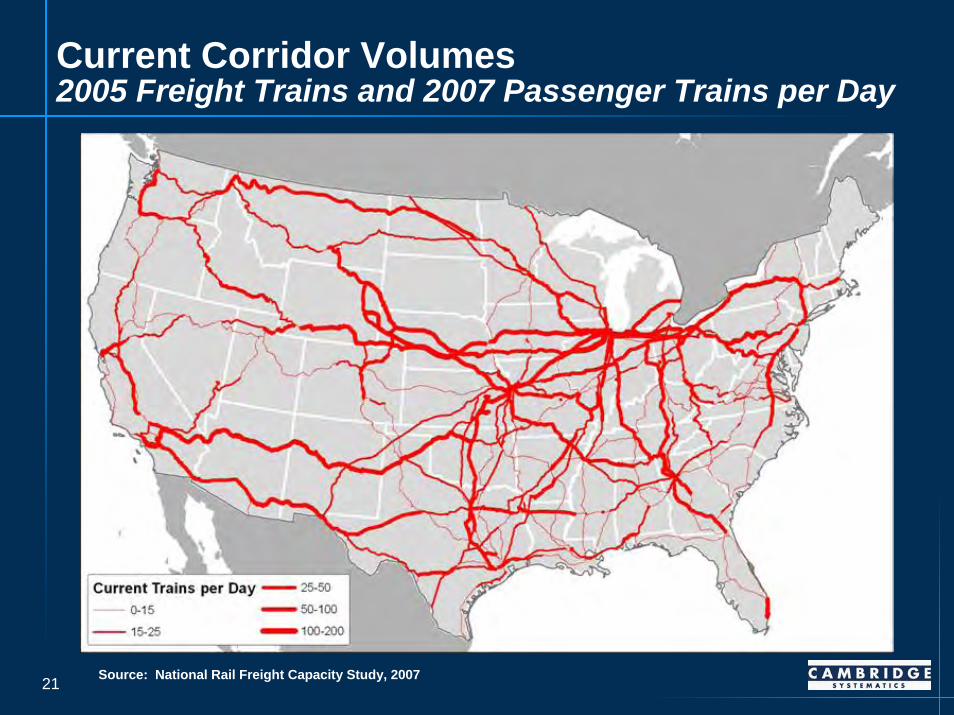

Current Corridor Volumes 2005 Freight Trains and 2007 Passenger Trains per Day

Source: National Rail Freight Capacity Study, 2007

22

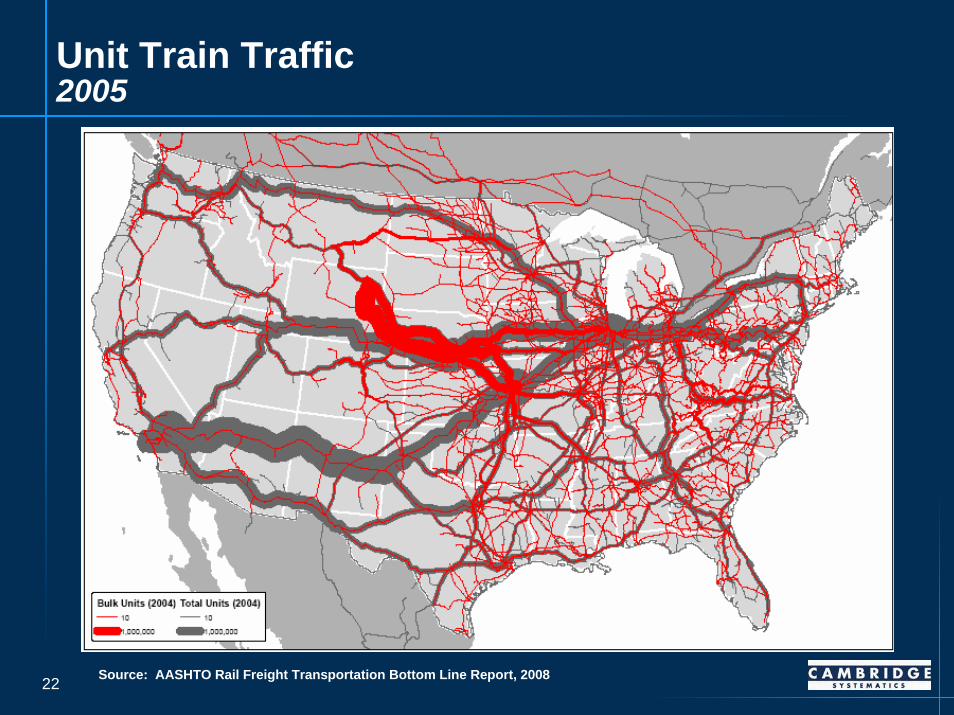

Unit Train Traffic2005

Source: AASHTO Rail Freight Transportation Bottom Line Report, 2008

23

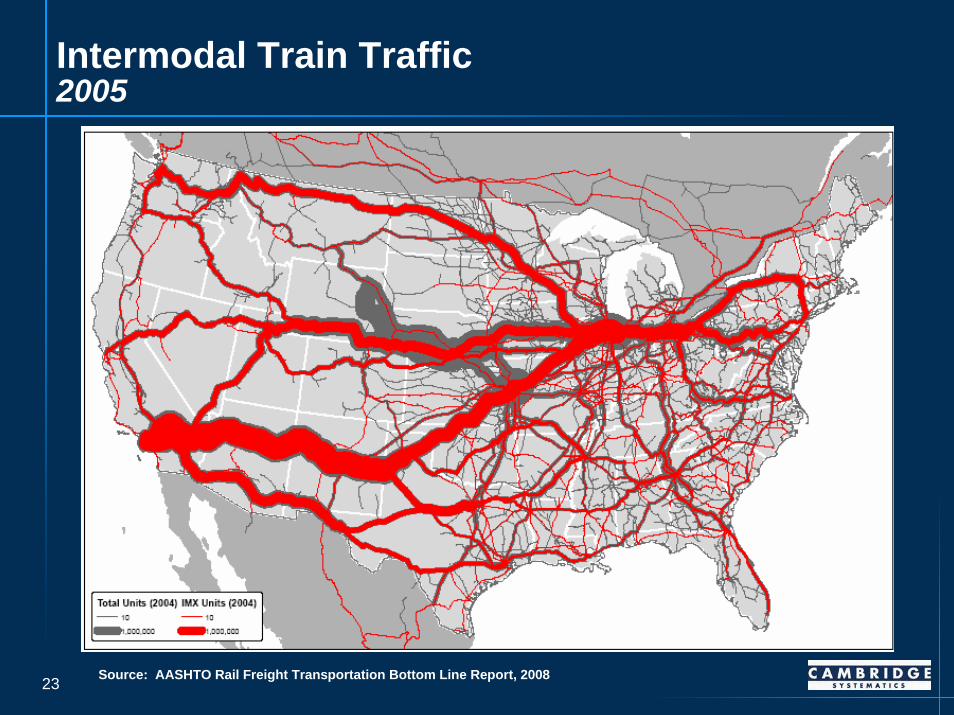

Intermodal Train Traffic2005

Source: AASHTO Rail Freight Transportation Bottom Line Report, 2008

24

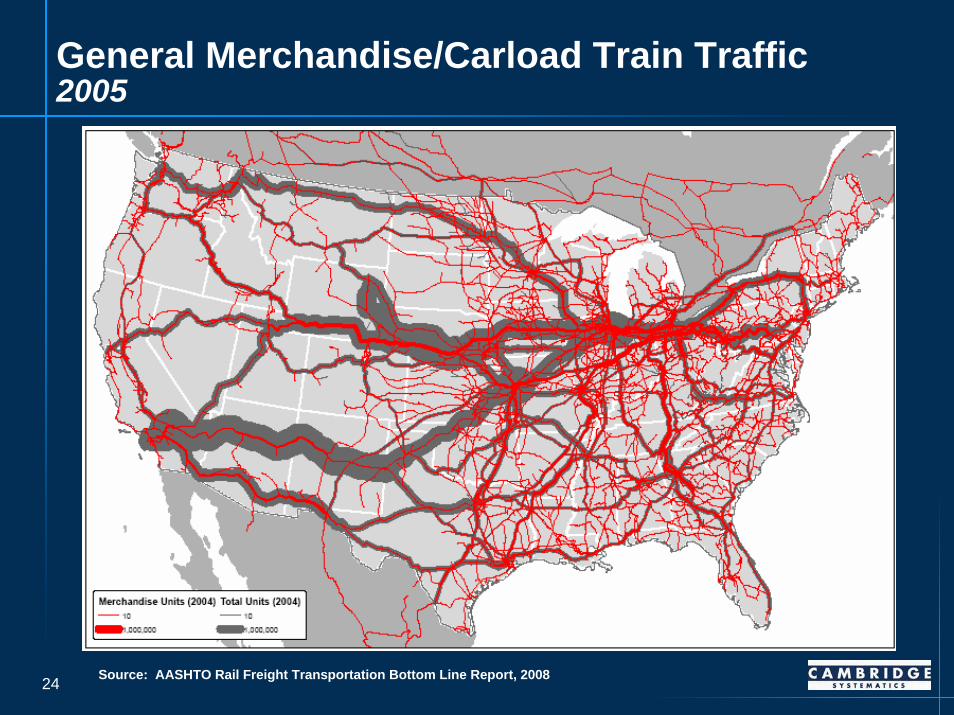

General Merchandise/Carload Train Traffic2005

Source: AASHTO Rail Freight Transportation Bottom Line Report, 2008

25

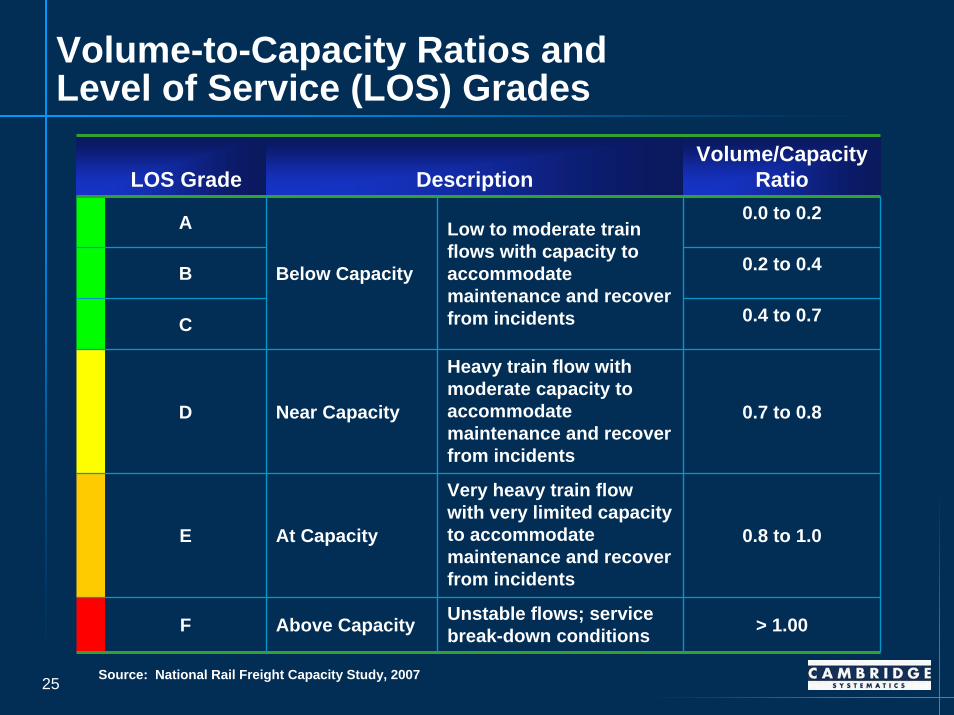

Volume-to-Capacity Ratios and Level of Service (LOS) Grades

LOS Grade DescriptionVolume/Capacity

Ratio

A 0.0 to 0.2

B 0.2 to 0.4

C 0.4 to 0.7

D Near Capacity

Heavy train flow with moderate capacity to accommodate maintenance and recover from incidents

0.7 to 0.8

E At Capacity

Very heavy train flow with very limited capacity to accommodate maintenance and recover from incidents

0.8 to 1.0

F Above Capacity Unstable flows; service break-down conditions > 1.00

Below Capacity

Low to moderate train flows with capacity to accommodate maintenance and recover from incidents

Source: National Rail Freight Capacity Study, 2007

26

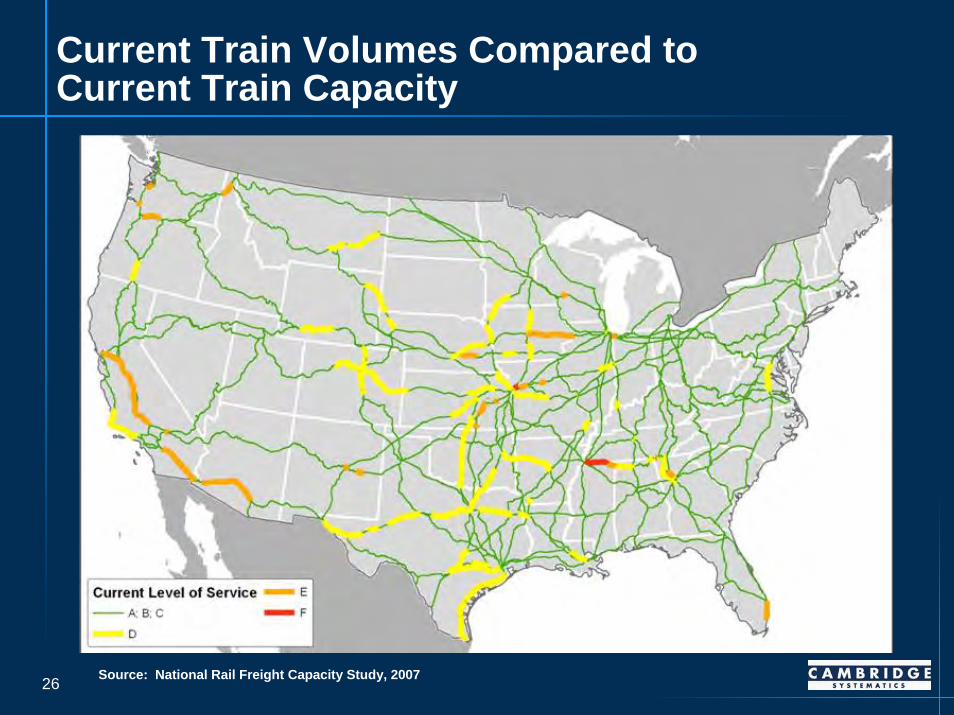

Current Train Volumes Compared to Current Train Capacity

Source: National Rail Freight Capacity Study, 2007

27

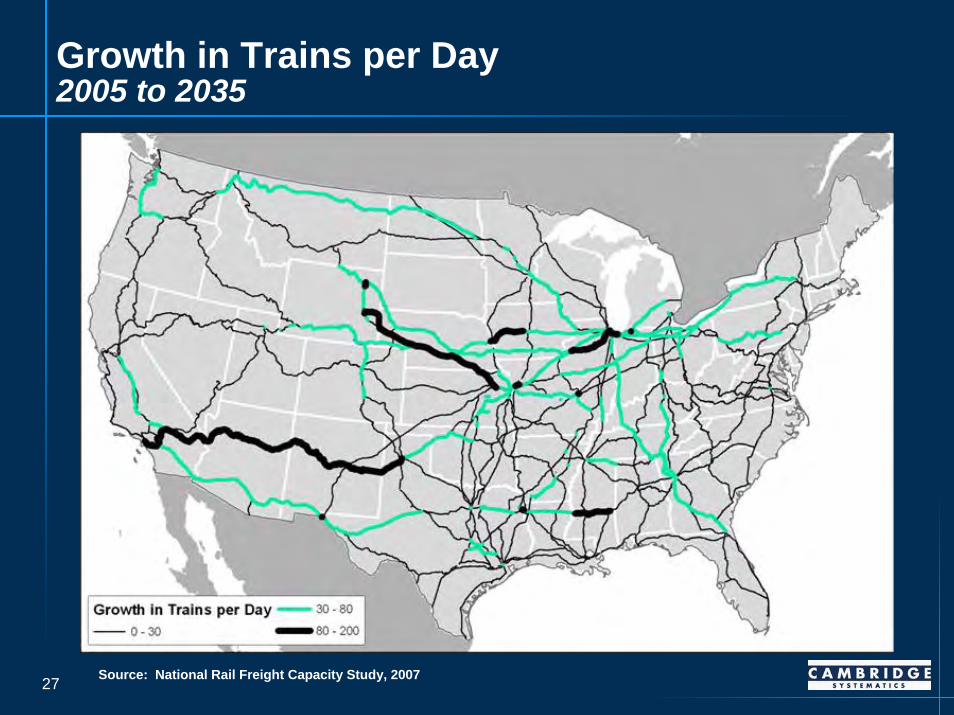

Growth in Trains per Day2005 to 2035

Source: National Rail Freight Capacity Study, 2007

28

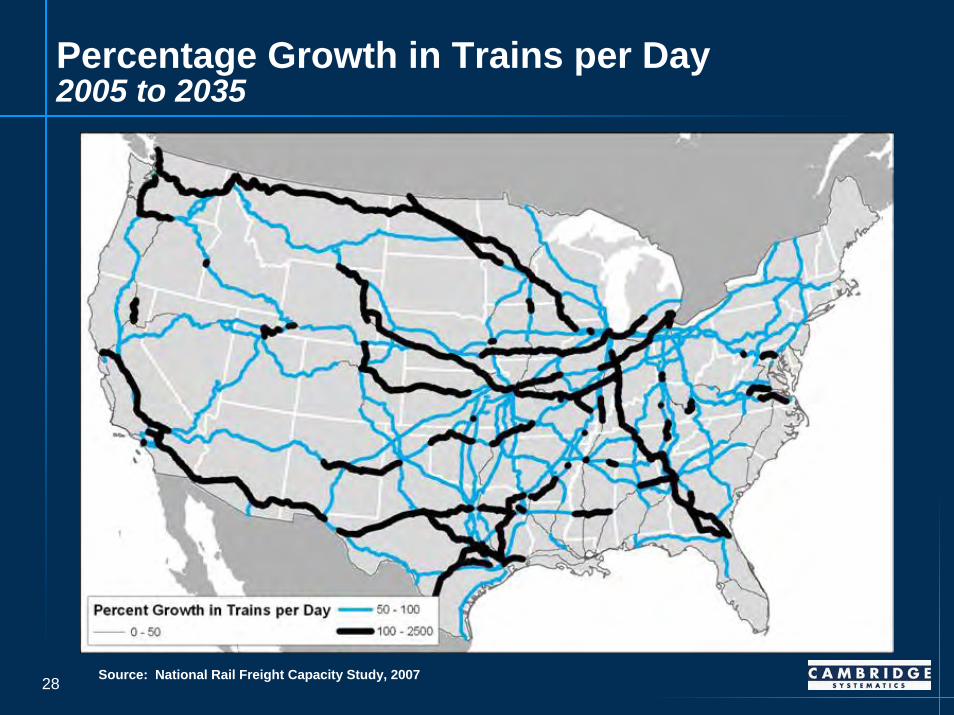

Percentage Growth in Trains per Day2005 to 2035

Source: National Rail Freight Capacity Study, 2007

29

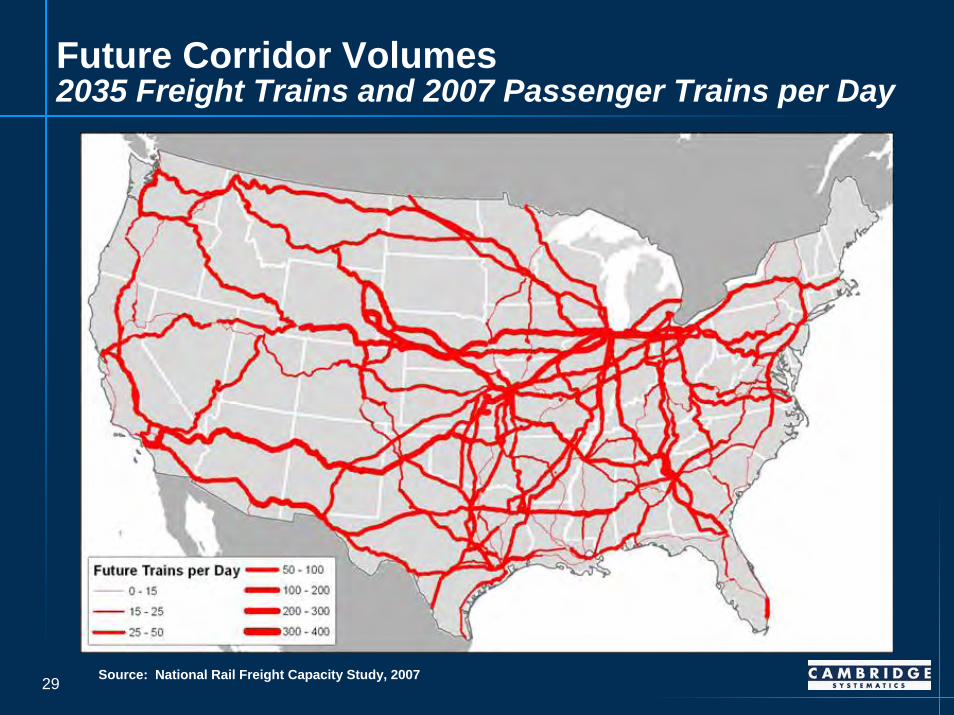

Future Corridor Volumes 2035 Freight Trains and 2007 Passenger Trains per Day

Source: National Rail Freight Capacity Study, 2007

30

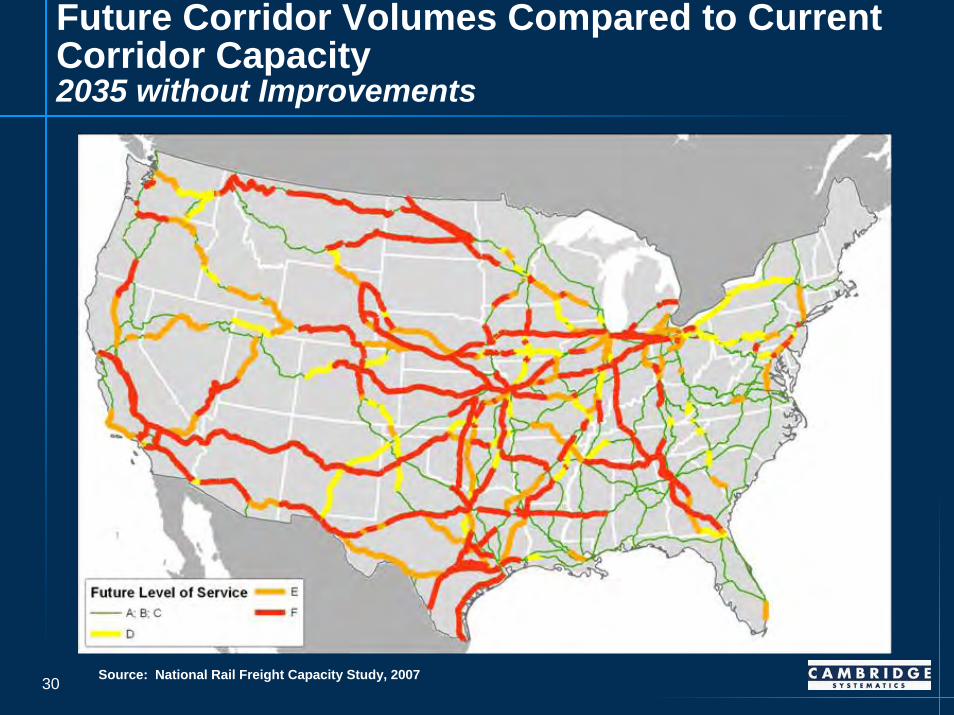

Future Corridor Volumes Compared to Current Corridor Capacity2035 without Improvements

Source: National Rail Freight Capacity Study, 2007

31

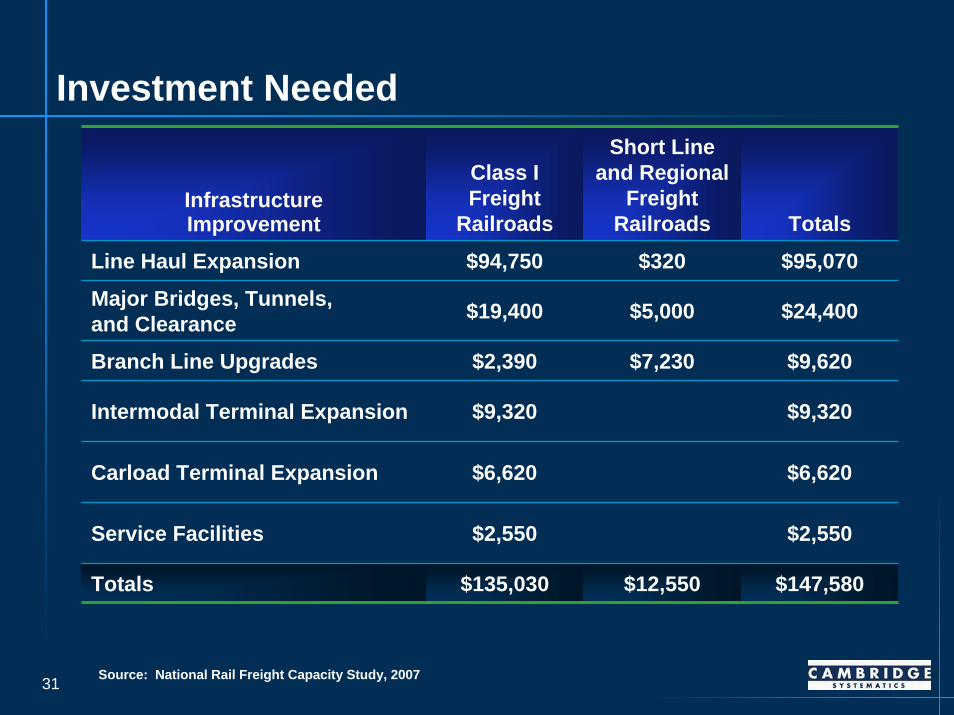

Investment Needed

Infrastructure Improvement

Class IFreight

Railroads

Short Line and Regional

FreightRailroads Totals

Line Haul Expansion $94,750 $320 $95,070

Major Bridges, Tunnels,and Clearance $19,400 $5,000 $24,400

Branch Line Upgrades $2,390 $7,230 $9,620

Intermodal Terminal Expansion $9,320 $9,320

Carload Terminal Expansion $6,620 $6,620

Service Facilities $2,550 $2,550

Totals $135,030 $12,550 $147,580

Source: National Rail Freight Capacity Study, 2007

32

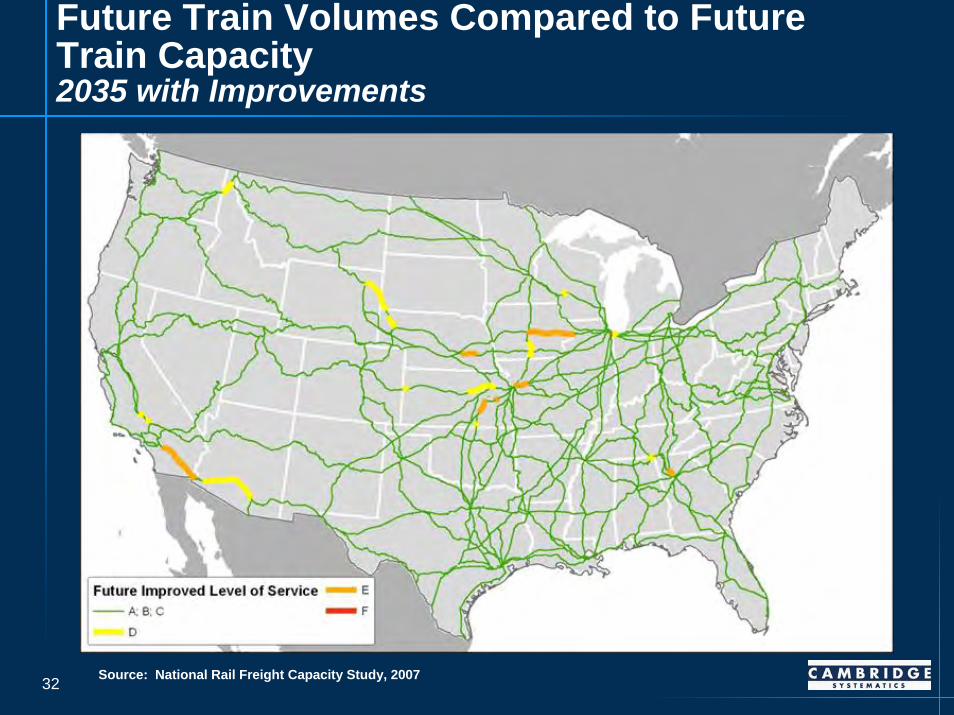

Future Train Volumes Compared to Future Train Capacity2035 with Improvements

Source: National Rail Freight Capacity Study, 2007

33

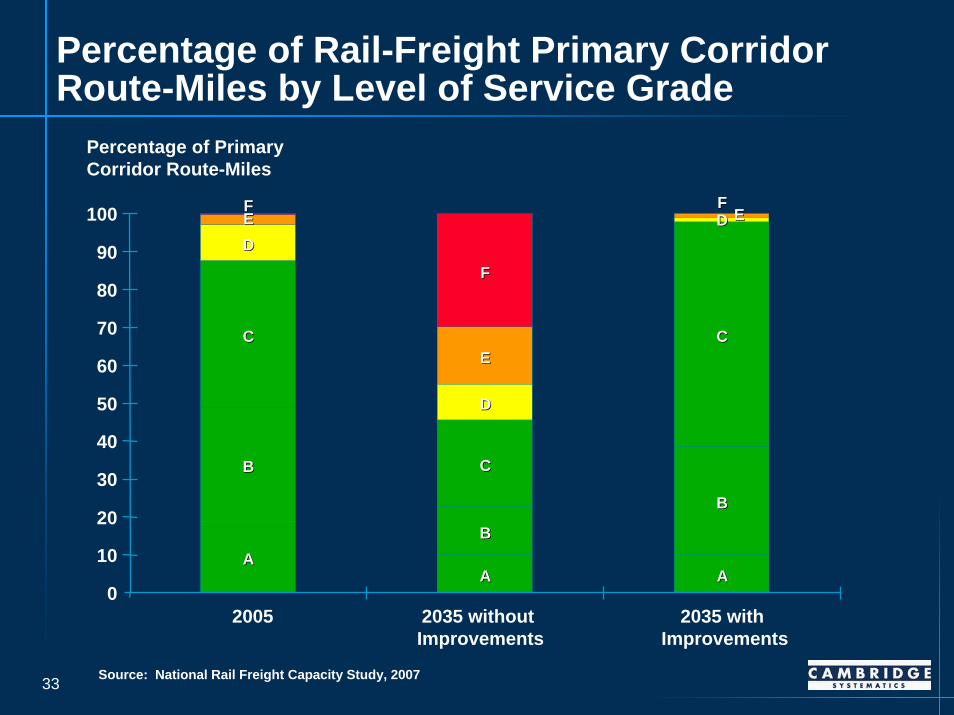

Percentage of Rail-Freight Primary Corridor Route-Miles by Level of Service Grade

Percentage of Primary Corridor Route-Miles

AAAA AA

BB

BB

BB

CC

CC

CC

DD

DD

DDEE

EE

EEFF

FF

FF

0

10

20

30

40

50

60

70

80

90

100

2005 2035 without Improvements

2035 with Improvements

Source: National Rail Freight Capacity Study, 2007

34

Authorization Issues

35

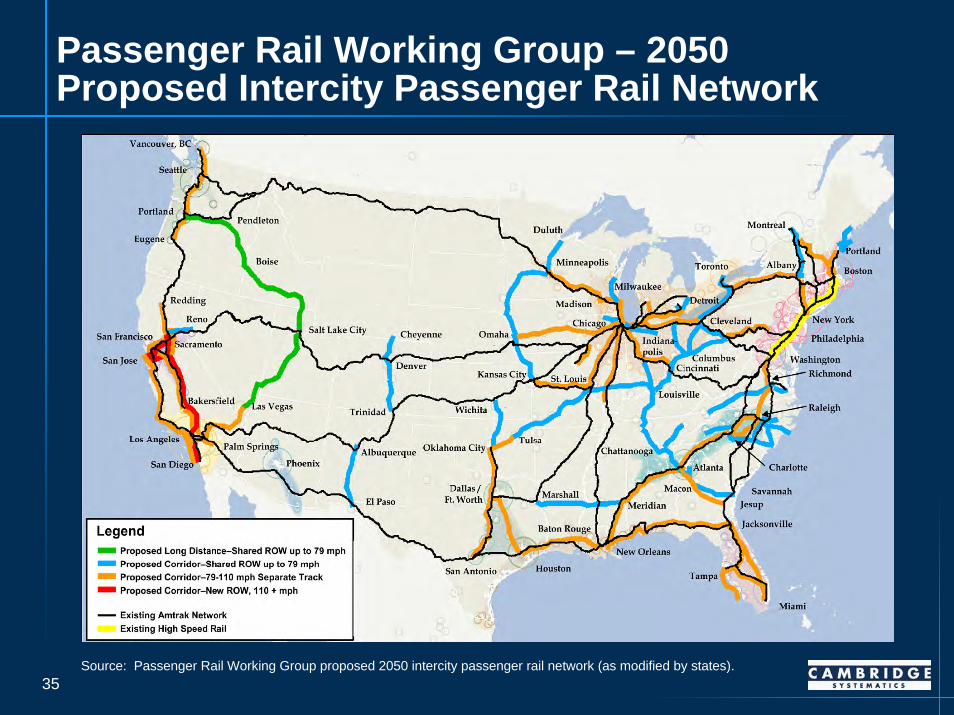

Passenger Rail Working Group – 2050 Proposed Intercity Passenger Rail Network

Source: Passenger Rail Working Group proposed 2050 intercity passenger rail network (as modified by states).

36

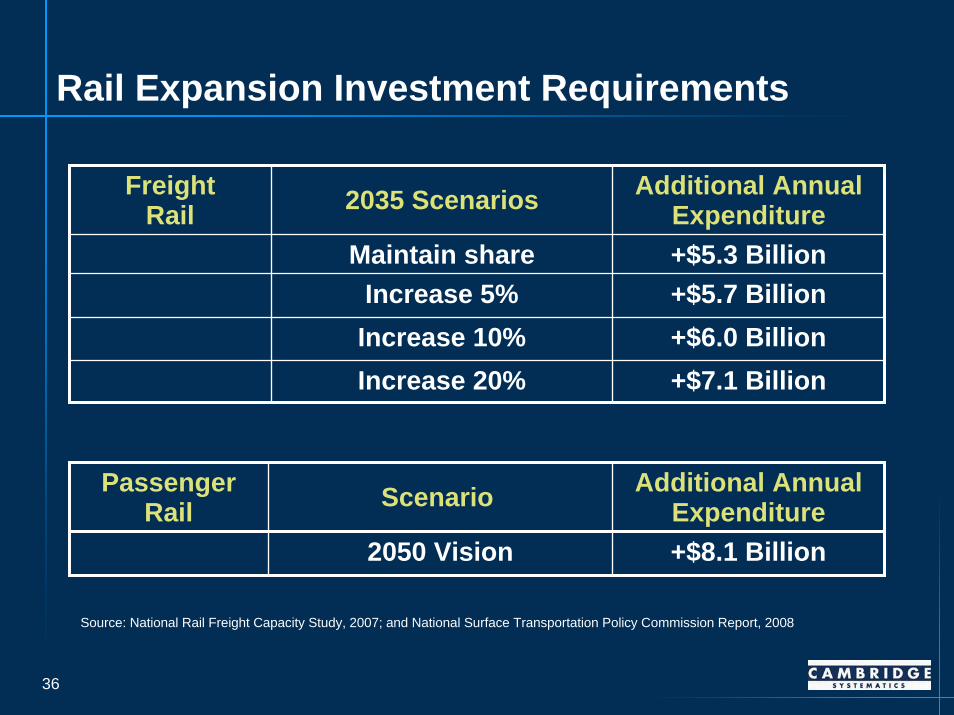

Rail Expansion Investment Requirements

FreightRail 2035 Scenarios Additional Annual

ExpenditureMaintain share +$5.3 Billion

Increase 5% +$5.7 BillionIncrease 10% +$6.0 BillionIncrease 20% +$7.1 Billion

Passenger Rail Scenario Additional Annual

Expenditure2050 Vision +$8.1 Billion

Source: National Rail Freight Capacity Study, 2007; and National Surface Transportation Policy Commission Report, 2008

37

Restructuring Urban Freight Terminals and Services

Consolidated shipments, integrated logistic centers, and inland ports

Gathering and distribution networks

38

Addressing Community and Economic Impacts

Turning up the volume• Grade crossings, noise, vibration, safety and land us

Pricing for volume• Intermodal and bulk• General merchandise/mixed carload

39

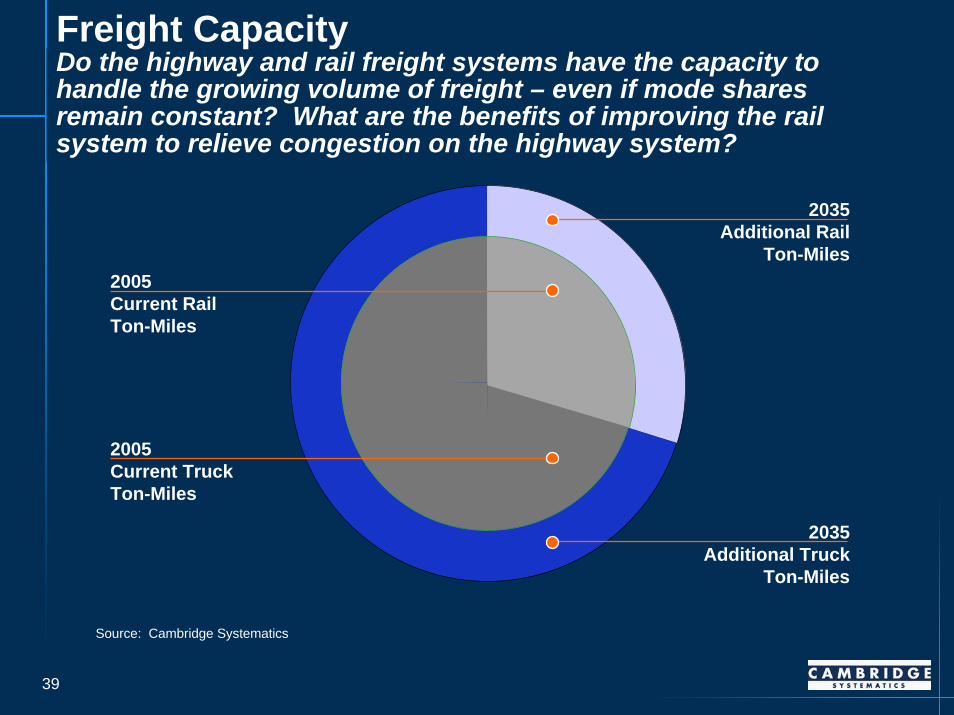

Freight CapacityDo the highway and rail freight systems have the capacity to handle the growing volume of freight – even if mode shares remain constant? What are the benefits of improving the rail system to relieve congestion on the highway system?

2035Additional Rail

Ton-Miles

2035Additional Truck

Ton-Miles

2005Current TruckTon-Miles

2005Current RailTon-Miles

Source: Cambridge Systematics

Freight Trends and Rail Capacity

Transportation leadership you can trust.

presented topresented to

2008 Ohio Conference on Freight2008 Ohio Conference on FreightToledo, OhioToledo, Ohio

presented bypresented byLance R. GrenzebackLance R. GrenzebackCambridge Systematics, Inc.Cambridge Systematics, Inc.

September 16, 2008September 16, 2008