Embed Size (px)

Citation preview

FRM VaR

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

VaR by example

Zvi Wiener VaR example slide 2

Assets

NIS TSAMUD $ Yen

Deposit 1yr. 6% 4,000

Bonds 10yr. 5% 2,000

Credit 3yr. 15% 8,000

Liabilities

NIS TSAMUD $ Yen

Saving 2yr. 4% 1,800

Deposit 1mo. 11% 8,200

Deposit 3mo. L-2% 3,000

Total: (200) 200 4,000 (3,000)

Today L=6%

Zvi Wiener VaR example slide 3

Risk Factors

• USD/NIS exchange rate

• Yen/NIS exchange rate

• Inflation

• Real NIS interest rates (IR, 10 yr., 2 yr.)

• Nominal NIS IR (1mo., 10 yr.)

• USD IR, (1 yr.)

• Yen IR, (Libor 3 mo.)

Zvi Wiener VaR example slide 4

Fair Value

For risk measurement we need not only the

fair value, but the fair value as a function of

risk factors in order to estimate the potential

profit/loss.

300018008200400020008000

Zvi Wiener VaR example slide 5

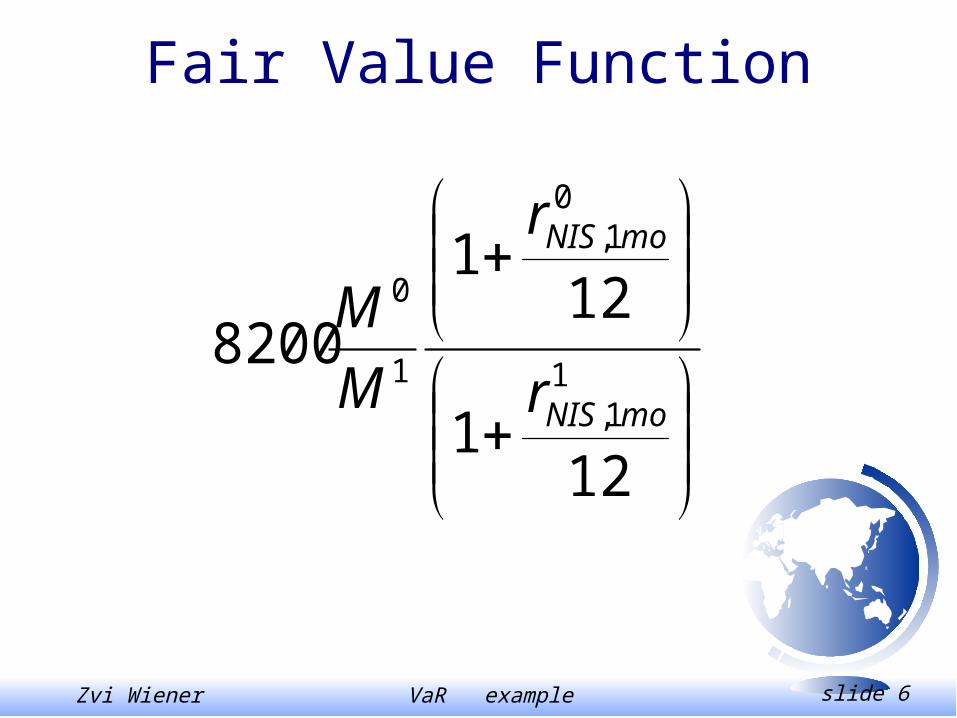

Fair Value Function

313,

303,

1

0

)1(

)1(8000

yNIS

yNIS

r

r

M

M

10110,

10010,

)1(

)1(2000

yreal

yreal

r

r

11$,

01$,

1

0

0

1

1

14000

y

y

r

r

M

M

d

d

Zvi Wiener VaR example slide 6

Fair Value Function

121

121

82001

1,

01,

1

0

moNIS

moNIS

r

r

M

M

Zvi Wiener VaR example slide 7

Fair Value Function

212,

202,

)1(

)1(1800

yreal

yreal

r

r

)02.0(25.01

)02.0(25.013000

11,

01,

1

0

0

1

yY

yY

L

L

M

M

Y

Y

Zvi Wiener VaR example slide 8

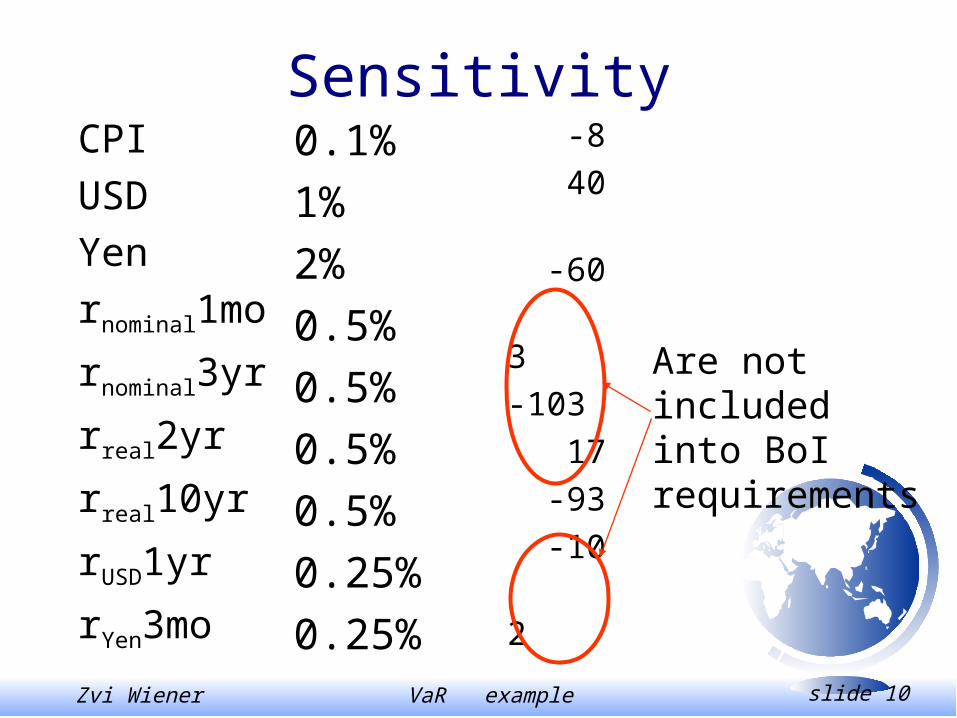

SensitivityCPI

USD

Yen

rnominal1mo

rnominal3yr

rreal2yr

rreal10yr

rUSD1yr

rYen3mo

0.1%

1%

2%

0.5%

0.5%

0.5%

0.5%

0.25%

0.25%

-8

40

-60

3

-103

17

-93

-10

2

Biggest market risk

Significant risk

Significant risk

Zvi Wiener VaR example slide 9

Risky Scenario

2yr 10 yr T

Real r

Zvi Wiener VaR example slide 10

SensitivityCPI

USD

Yen

rnominal1mo

rnominal3yr

rreal2yr

rreal10yr

rUSD1yr

rYen3mo

0.1%

1%

2%

0.5%

0.5%

0.5%

0.5%

0.25%

0.25%

-8

40

-60

3

-103

17

-93

-10

2

Are not includedinto BoI requirements

Zvi Wiener VaR example slide 11

Gradient Vector

Direction of fastest decay (loss).

Take the sensitivity vector and divide it by the

assumed changes in the risk factors.

)()(lim)('

0

xfxfxf

)()(

)('xVxV

xV

Zvi Wiener VaR example slide 12

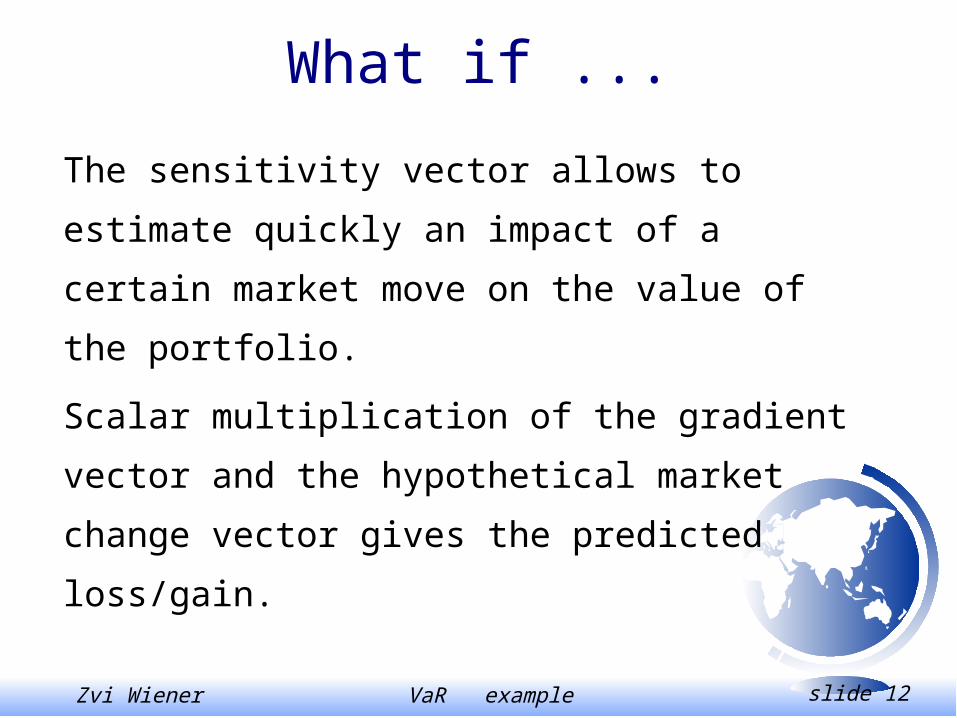

What if ...

The sensitivity vector allows to estimate

quickly an impact of a certain market move

on the value of the portfolio.

Scalar multiplication of the gradient vector

and the hypothetical market change vector

gives the predicted loss/gain.

Zvi Wiener VaR example slide 13

Risk Measurement

• The gradient vector describes my exposure to risk factors

• The distribution of risk factors allows me to estimate the potential loss together with probability of such an event.

• The stress test will describe the response to specific (the most interesting) scenarios.

Zvi Wiener VaR example slide 14

Risk Management

• Swap Dollar Yen

• Two forward contracts

• Quanto option

• FRA (?)

• Fixed - floating swap

Zvi Wiener VaR example slide 15

Duration and IR sensitivity

Zvi Wiener VaR example slide 16

The Yield to Maturity

The yield to maturity of a fixed coupon bond y is given by

n

i

ytTi

iectp1

)()(

Zvi Wiener VaR example slide 17

Macaulay Duration

Definition of duration, assuming t=0.

p

ecTD

n

i

yTii

i

1

Zvi Wiener VaR example slide 18

Macaulay Duration

What is the duration of a zero coupon bond?

T

tt

tT

tt y

CFt

iceBondwtD

11 )1(Pr

1

A weighted sum of times to maturities of each coupon.

Zvi Wiener VaR example slide 19

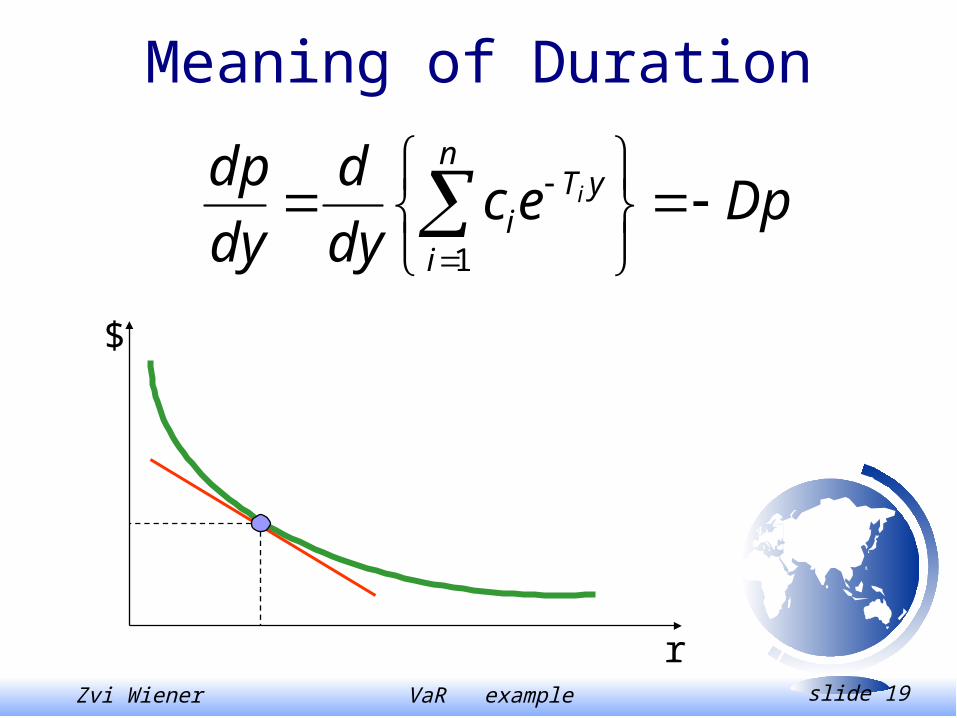

Meaning of Duration

Dpecdy

d

dy

dp n

i

yTi

i

1

r

$

Zvi Wiener VaR example slide 20

Proposition 15.12 TS of IRWith a term structure of IR (note yi), the duration can be expressed as:

Dpecds

d

s

n

i

syTi

ii

01

)(

p

ecTD

n

i

yTii

ii

1

Zvi Wiener VaR example slide 21

Convexity

r

$

2

2

y

pC

Zvi Wiener VaR example slide 22

FRA Forward Rate Agreement

A contract entered at t=0, where the parties (a lender and a borrower) agree to let a certain interest rate R*, act on a prespecified principal, K, over some future time period [S,T].

Assuming continuous compounding we have

at time S: -K

at time T: KeR*(T-S)

Calculate the FRA rate R* which makes PV=0hint: it is equal to forward rate

Zvi Wiener VaR example slide 23

Exercise 15.7Consider a consol bond, i.e. a bond which will forever pay one unit of cash at t=1,2,…

Suppose that the market yield is y - flat. Calculate the price of consol.

Find its duration.

Find an analytical formula for duration.

Compute the convexity of the consol.

Zvi Wiener VaR example slide 24

ALM Duration

• Does NOT work!• Wrong units of measurement• Division by a small number

r

A

ADA

1r

L

LDL

1

r

LA

LAD LA

)(1

Zvi Wiener VaR example slide 25

ALM Duration

A similar problem with measuring yield

r

P

VaR P 1