Embed Size (px)

Citation preview

Report prepared by RSM US LLP in conjunction with the Finance Office Presented by: Dan Schelske, RSM US, LLP January 14, 2019

FY18 Audit Report

EXECUTIVE SUMMARY

Purpose: To receive the findings of the FY18 audit report.

Attached is the PowerPoint presentation of the FY18 audit report of the School District’s auditors, RSM US LLP. Dan Schelske from RSM US LLP will be in attendance at the meeting on Monday, January 14, 2019, to present the audit findings.

Recommendation: It is recommended that the School Board approve the audit report for FY18 and direct the audit to be sent to the Department of Legislative Audit for their approval.

©2015 RSM US LLP. All Rights Reserved.

2

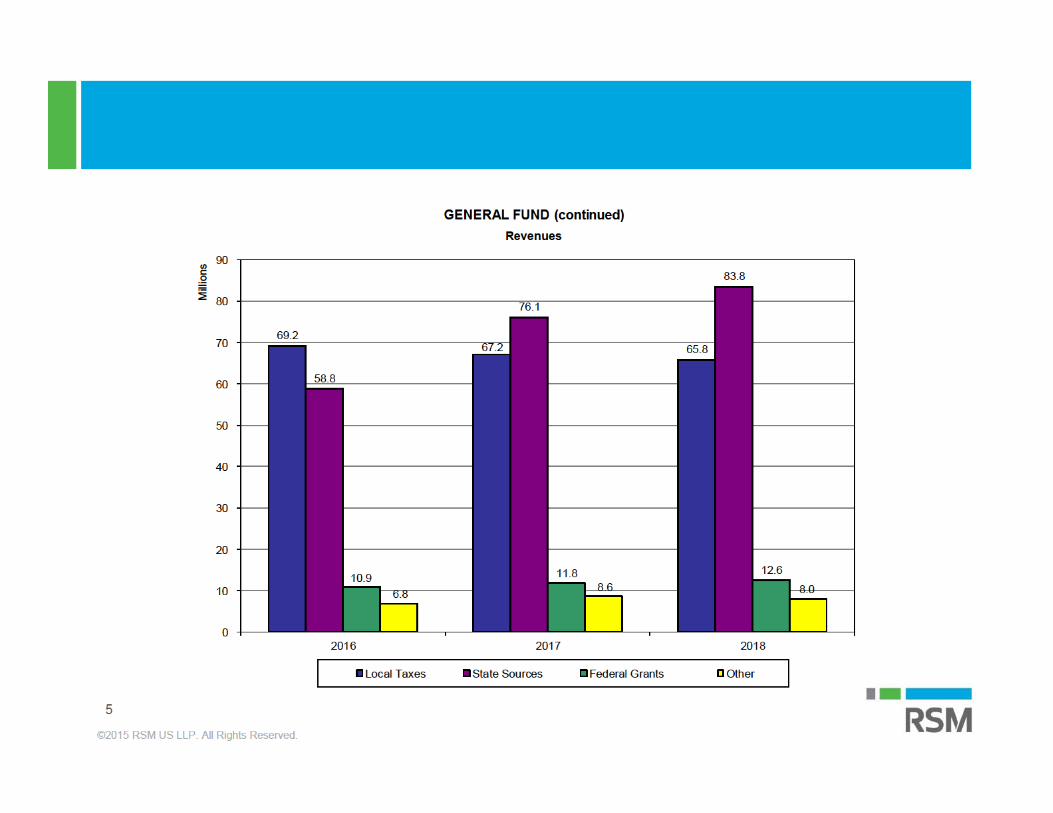

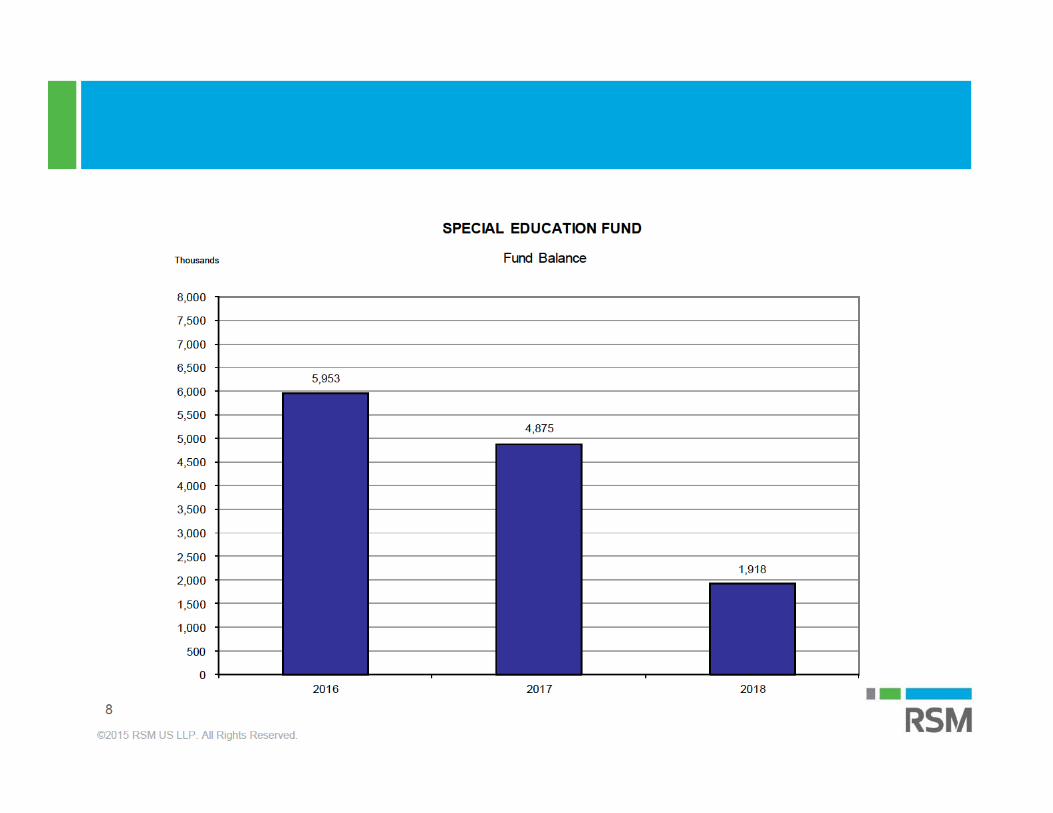

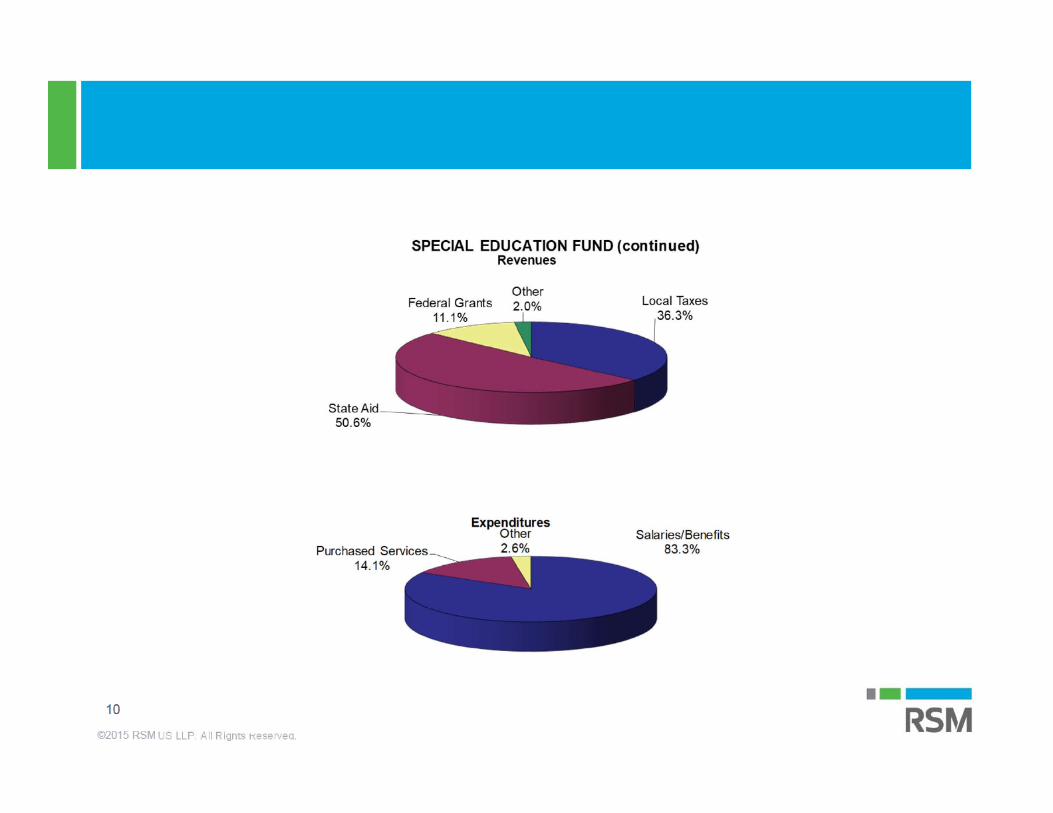

Data portrayed in the attached graphic presentations was derived from the District’s basic financial statements which were audited by RSM US LLP, whose report thereon is expected to be dated in January 2019. The data should be read in conjunction with the District’s basic financial statements and the auditor’s report thereon.

©2015 RSM US LLP. All Rights Reserved.

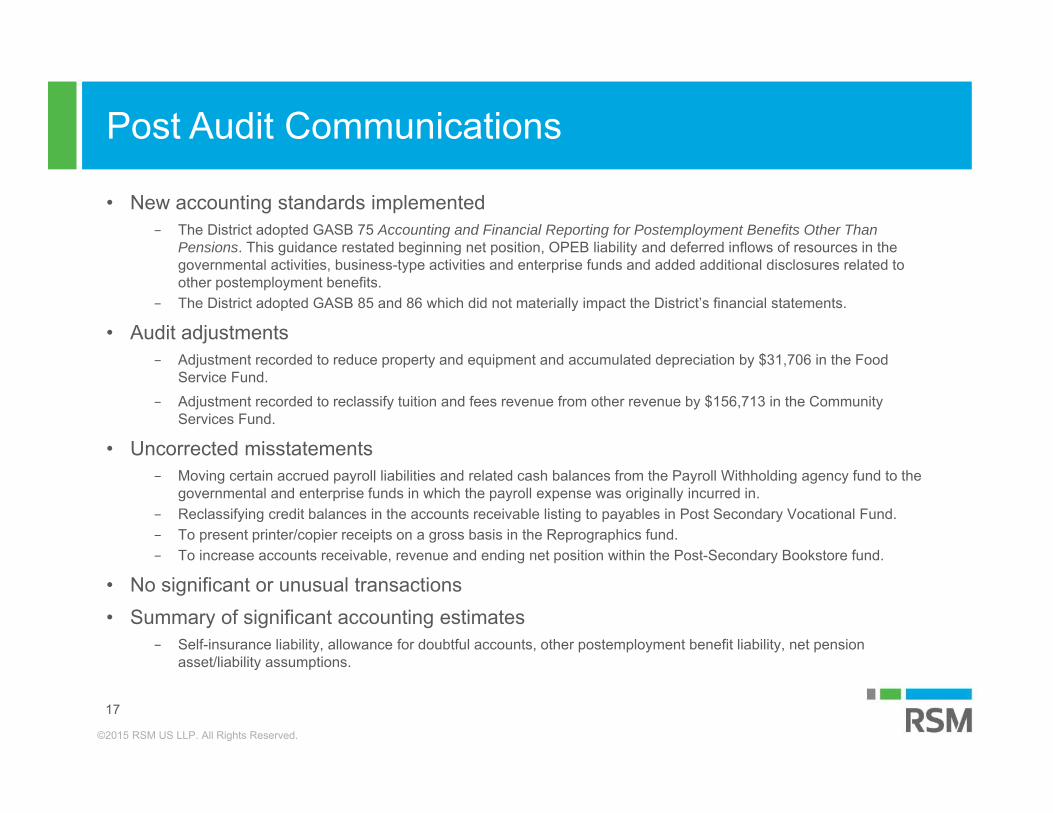

Post Audit Communications

17

• New accounting standards implemented − The District adopted GASB 75 Accounting and Financial Reporting for Postemployment Benefits Other Than

Pensions. This guidance restated beginning net position, OPEB liability and deferred inflows of resources in the governmental activities, business-type activities and enterprise funds and added additional disclosures related to other postemployment benefits.

− The District adopted GASB 85 and 86 which did not materially impact the District’s financial statements.

• Audit adjustments− Adjustment recorded to reduce property and equipment and accumulated depreciation by $31,706 in the Food

Service Fund.− Adjustment recorded to reclassify tuition and fees revenue from other revenue by $156,713 in the Community

Services Fund.

• Uncorrected misstatements− Moving certain accrued payroll liabilities and related cash balances from the Payroll Withholding agency fund to the

governmental and enterprise funds in which the payroll expense was originally incurred in.− Reclassifying credit balances in the accounts receivable listing to payables in Post Secondary Vocational Fund.− To present printer/copier receipts on a gross basis in the Reprographics fund.− To increase accounts receivable, revenue and ending net position within the Post-Secondary Bookstore fund.

• No significant or unusual transactions• Summary of significant accounting estimates

− Self-insurance liability, allowance for doubtful accounts, other postemployment benefit liability, net pension asset/liability assumptions.

©2015 RSM US LLP. All Rights Reserved.

Internal Control / Federal Award Compliance

18

• No material weaknesses in internal control over financial reporting noted.

• A significant deficiency in internal control over financial reporting noted related to the review of purchasing card expenditures at Southeast Technical Institute.

• A federal award compliance issue reported for payroll documentation in the Special Education fund.

• A number of control deficiencies which were separately communicated to management.