Embed Size (px)

Citation preview

1

2nd Berlin Internet Economics Workshop28-29 May 1999

INTERCONNECTION BETWEEN ISPS, CAPACITYCONSTRAINTS AND VERTICAL DIFFERENTIATION

G. DangNguyen, T. PénardENST Bretagne, ICI

Brest - France

Abstract :

In this paper, we study the incentives of Internet Service Providers (ISPs) tointerconnect their networks by means of peering and transit agreements. Wepropose a sequential game-theoretic model where the first stage deals with theinterconnection decisions and the second stage with a vertically differentiatedcompetition on the Internet access services. Formally, we consider a national marketcharacterized by two Internet carriers providing transit and connectivity services andmany symmetric retail ISPs delivering Internet access to end-users. The two carriersare capacity constrained and do not warrant the same level of quality. The ISPsinterconnected to the same backbone, are assumed to provide the same quality ofInternet access and behave like a « club ». The aim of this model is to study theinteractions between the transit agreements of ISPs and their peering agreements.The main result of the paper is that the high quality ISPs have more incentives tomake intra-club peering than inter-club peering whereas the low quality ISPs havemore incentives to make inter-club peering. Moreover, if the size of the high qualityclub rises, the low quality ISPs have a higher probability to peer with each other andwith the high quality ISPs. These theoretic propositions are illustrated by someempirical evidences on the French Internet market.

JEL classifications: L11, L13, L22

Keywords: Interconnection Agreements, Network Externality, Internet Economics

2

I Introduction

Internet is a network of interconnected networks which share a common protocol of datatransmission and routing, named the Internet Protocol (IP). The operator of an IP network is calledan Internet Service Provider (ISP). Noteworthy is the distinction between two categories of ISPs,the wholesale ISPs or Internet carriers and the retail ISPs. The former have backbone infrastructuresand large networks. They provide wholesale access and transit services to other ISPs and privatenetworks, which can resell Internet access. Conversely, a retail ISP sells Internet access only to end-users. However, large national and international ISPs (for example UUNet in the US or FranceTelecom in France) provide both wholesale and access services (integrated ISPs). Modeling ISPcompetition requires therefore to treat differently the wholesale and the retail markets. The customerson the retail market, are more sensitive to the non price dimensions of the access service than on thewholesale market. Wholesaling is rather an homogeneous service, and consists in selling accesscapacities and connectivity. Reselling instead can be seen as a vertically differentiated competitionwhere the differentiation concerns the access quality and the diversity of client services (See Huston[1999]).

Another important specificity of the sector is ISPs’ mutual dependence to provide theirservices. They have to cooperate, because selling Internet access means selling a connectivity withevery Web site and every end-user. This implies a minimum of interconnection agreements betweenISPs to exchange traffic and to reach all the IP networks. The ISPs can use either peeringagreements or customer-provider financial agreements (See Bailey [1997]). The peering is a bilateralor multilateral agreement without any financial compensation. It is free clearing or a Sender KeepsAll agreement : each ISP is paid for by its own customer and receives nothing from theinterconnection services. In a customer-provider agreement instead, one ISP pays to access to thenetwork of the counterpart. The payment is often a capacity-based flat rate. The peering agreementsare dominant between wholesale ISPs and between retail ISPs (horizontal agreements). Vice versa,the interconnection agreements between wholesale ISPs and retail ISPs, are dominated bycustomer-provider contracts : this vertical agreements are also called transit agreements. Such asituation contrasts with the practices in the telecommunication industry, where usage-basedagreements and an accounting rate systems still prevail1.

This paper analyses the link between transit and peering agreements. Indeed, the incentivesof retail ISPs to peer with each other can depend on the choice of their transit providers. As thewholesale ISPs do not warrant the same quality and capacity, the retail ISPs can differentiate theirservices. Do this differentiation stimulate peering agreements ? To answer, we must understand thedifferent motivations of ISPs to refuse peering. Two major reasons can be put forward. First, in aninterconnection agreement, an ISP can be opportunistic and use the network of its peer withoutgiving a reciprocity. For example, it can refuse to reveal some routes to its peers in order to keep

1 The second difference between telecommunication and Internet interconnections is the regulation.Telecommunication sector has a strong public regulation which promotes a fair access policy. For example, thedominant telecommunication operators cannot refuse an interconnection with a small operator and must offer fairconditions in matter of prices and quality. Internet has no such a regulation. Each ISP can refuse to interconnectwith an other ISP, discriminate between ISPs, or impose some restrictive conditions (see Chinoy, B., T. Salao1996).

3

these routes out of congestion or it can reduce its network capacity investments on some routes andtransfers its traffic on the peer routes. However free-riding can be overcome if the ISPs agree toexchange only client traffic (traffic between their own customers) because the risk of opportunismconcerns mainly the traffic with third networks.

The second motivation is more strategic. The ISPs can refuse to exchange client trafficbecause the ISPs might become too close substitute when their networks are locally interconnected.An interconnection agreement increases the network capacity (better optimization of the networkroutes) and improves the quality of access. The consequence is a more intense competition. On thewholesale market, an increase of ISPs capacity is likely to create excess of capacity and pull downprices. On the retail market, an interconnection agreement reduces the difference of quality betweenthe ISPs. Suppose that initially one ISP has a better quality than the other. The upper quality ISP canfear that the lower quality ISP benefit more from the interconnection and increases strongly itsmarket share. Baake and Wichmann [1998] called this effect, the « business stealing effect ».

This competition effect is not specific to Internet interconnection. Matutes and Padilla [1994]exhibited also a substitution effect in the decision of sharing the Automatic Teller Machines Networksin the banking market. When the banks choose the compatibility of their ATM networks, thedepositors are willing to accept lower interest on their deposits because they value a larger ATMnetwork. But the compatible banks become better substitutes for each other and compete in theinterest rate more intensely to attract the rival customers. In the ISP market, we have the same idea.The ISPS customers value better local transmissions and access. They are willing to pay more forthis better quality (network effect). In the following of the paper, we investigate the trade-offbetween the network effect and the competition effect in a two stage game where the retail ISPSdecide first to peer and then compete in a vertical differentiation model à-la Mussa Rosen [1978].

In section 2, we present the model. In section 3, we propose some general propositionswhich are illustrated by some numerical simulations. In section 4, we try to link the theoreticalpropositions with the French Internet market, proceeding to some statistical test on our data.

II) Model of vertical differentiation

2.1 Description of the model

We consider a European country with N symmetric retail ISPs who provide Internet access for end-users. This national Internet market is also characterized by two competing backbones or Internetcarriers, named A and B, who propose transit services to the N ISPs. By signing a financialagreement with one of the carriers, an ISP can obtain a worldwide connectivity and exchangeInternet traffic with all the national ISPs. We suppose that m ISPs have chosen the backbone A and(N-m) the backbone B, with m≤N ; we do not let the possibility of being interconnected with the twocompeting backbone2. Note that the determination of m and even N is outside the scope of themodel. In other words, the market structure is considered as given. We focus on the peering andpricing policy of the two classes of ISPs. 2 If a transit agreement is rather costly, there is no rationale to duplicate the transit agreements. However, anargument for having many transit agreements, is to increase the security and the quality of Internet transmissions.

4

We further assume that the backbone A allows the ISPs to deliver a higher quality service to theirend-users than3 the backbone B : for example, the backbone A has better capacities of transmissionand routing. This quality asymmetry might also arise from the distribution of ISPs on the twobackbones. Indeed, ISPs connected to the same backbone form a « club » characterized by anhomogeneous quality of Internet access. The size of the club might generate positive networkexternality : if this were the case, the number of ISPs belonging to the backbone A should besuperior to N/2. However, we suppose that the two backbones have capacity constraints. Hence thequality of a backbone can suffer from congestion if he provides too many national ISPs with transitservices. Fortunately, the ISPs can reduce the risk of congestion by exchanging directly their trafficthrough peering agreements in a National Internet Exchange (NIX).

If peering concerns two ISPs on the same backbone, it improves the capacity and quality ofthis backbone ; hence it has a positive effect on the quality of service provided by all the ISPs havinga transit agreement with this backbone. If peering concerns two ISPs belonging to differentbackbones, it benefits to the N ISPs, because it reduces the traffic transiting between the backbonesA and B4. The network capacity provided by the two backbones increases and all the ISPs have abetter connection with third networks. However, the benefit is likely to be different for the ISPs ofthe backbone A and those of the backbone B : this asymmetry can play a major role in the decisionof peering, as we will see later. The figure 1 represents the national Internet market described here.

Figure 1 : A stylised Internet market

Backbone A Backbone B

ISP 1 ISP m

NIX

ISP N-m ISP N

USERS

Transitagreement

Peeringagreement

Transitagreement

3 We do not explicit the selection of the Internet carrier. But this decision should depend on the subscription thatthe Internet carriers announce and on their capacity constraints.4 In our model, peering is considered as a public good inside the community of the ISPs connected to the samebackbone. This hypothesis is questionable because peering could have some private benefits for the ISPs. Butwe suppose that the private effects are small compared to the collective effects.

5

The aim of this model is to study the interactions between the transit agreements of ISPs and theirpeering agreements. In particular, we want to address two questions :

• Do ISPs belonging to a high quality backbone tend to have more peering agreements thanthe ISPs of a low quality backbone ?

• Do the ISPs belonging to the same backbone have more incentives to peer with eachother than with the ISPs of other competing backbones ?

For this purpose, we develop a two stage game. In the first stage, the ISPs make theirpeering agreements on the NIX. In the second stage, they compete in price for supplying Internetaccess to end users. The competition is vertically differentiated, with two levels of quality for theISPs, depending on their transit and peering decisions. The club of ISPs connected to the backboneA proposes a high quality access and the club of ISPs on the backbone B a low quality access. Wesuppose that the customers are heterogeneous in their preference for the quality. Each customer ischaracterized by a utility function à la Mussa-Rosen (1978) :

( )U p pθ λθ, = − (1)

where λ is the quality of the Internet access, p is the subscription and θ is the preference for thequality. The users are uniformly distributed on the interval of preference θ ∈[0,1]. An user of type θwill subscribe to an ISP supplying a quality of access λ at a price p if θ > p/λ.

We adopt a strong hypothesis about price setting : ISPs connected to the same backbone donot compete in price, but in other dimensions, like the variety of ancillary services or promotion. Theprice competition occurs only between the two clubs. In a sense, each club agrees to fix a uniqueprice which maximizes its aggregate profit, given the price proposed by the rival club. This clubcompetition determines the share of users who are willing to subscribe to a high quality service andthose who prefer a low quality access. Then, the distribution of the users among the ISPs supplyingthe same quality, results from a non price competition that does not worth being detailed in thispaper.

2.2 The network quality :

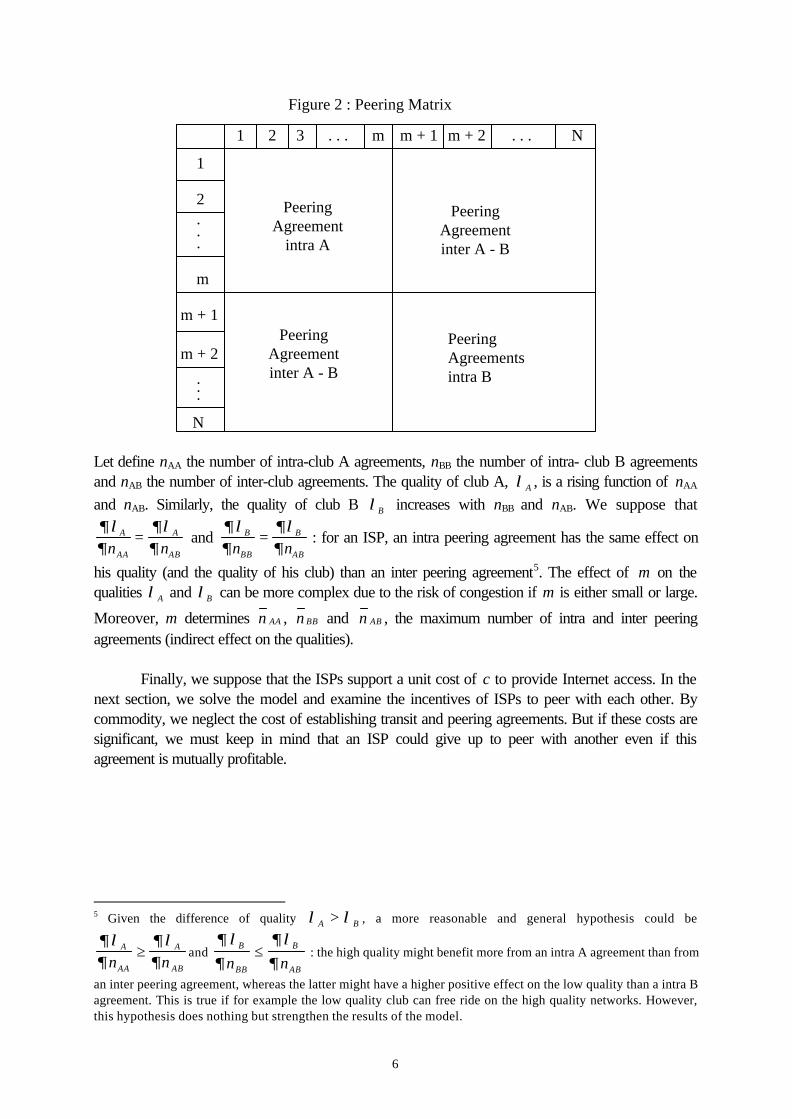

We call λA (respectively λB) the quality of the ISPs on the backbone A (resp. on the backbone B).This quality depends on m , the number of ISPs connected to the backbone A, and on the number ofpeering agreements on the NIX. We distinguish intra peering (between ISPs belonging to the sameclub) and inter-peering (between ISPs of different clubs).

We can count at most ( )

nm m

AA =− 1

2 intra-A peering agreements,

( )( )n

N m N mBB =

− − − 12

intra-B peering agreements and n m N mAB = −( ) inter peering agreement. These agreements aresummarized in a peering matrix of the following form :

6

Figure 2 : Peering Matrix

1 2 3 . . . m m + 1 m + 2 . . . N

1

2...

m

m + 1

m + 2

...

N

PeeringAgreement

intra A

PeeringAgreementinter A - B

PeeringAgreementsintra B

PeeringAgreementinter A - B

Let define nAA the number of intra-club A agreements, nBB the number of intra- club B agreementsand nAB the number of inter-club agreements. The quality of club A, λA , is a rising function of nAA

and nAB. Similarly, the quality of club B λB increases with nBB and nAB. We suppose that∂λ∂

∂λ∂

A

AA

A

ABn n= and

∂λ∂

∂λ∂

B

BB

B

ABn n= : for an ISP, an intra peering agreement has the same effect on

his quality (and the quality of his club) than an inter peering agreement5. The effect of m on thequalities λA and λB can be more complex due to the risk of congestion if m is either small or large.

Moreover, m determines n AA , n BB and n AB , the maximum number of intra and inter peeringagreements (indirect effect on the qualities).

Finally, we suppose that the ISPs support a unit cost of c to provide Internet access. In thenext section, we solve the model and examine the incentives of ISPs to peer with each other. Bycommodity, we neglect the cost of establishing transit and peering agreements. But if these costs aresignificant, we must keep in mind that an ISP could give up to peer with another even if thisagreement is mutually profitable.

5 Given the difference of quality λ λA B> , a more reasonable and general hypothesis could be

∂λ∂

∂λ∂

A

AA

A

ABn n≥ and

∂ λ∂

∂λ∂

B

BB

B

ABn n≤ : the high quality might benefit more from an intra A agreement than from

an inter peering agreement, whereas the latter might have a higher positive effect on the low quality than a intra Bagreement. This is true if for example the low quality club can free ride on the high quality networks. However,this hypothesis does nothing but strengthen the results of the model.

7

III) The Peering Policy

3.1 The price equilibrium

We begin by solving the last stage. Given the quality λA and λB with λ λA B≥ , an end-user ~θ is

indifferent between an ISP of club A and an ISP of club B if

λ θ λ θA A B Bp p~ ~− = − (2)

where pA is the subscription to the high quality ISPs and pB the subscription to the low quality ISPs.The indifferent user

~θ is defined by :~θ =

−−

p pA B

A Bλ λ(3)

If p pA B

A B

−−

>λ λ

1, the high quality ISPs have no subscriber ; all the Internet users prefer subscribing

to the low quality ISPs, because the charges fixed by the high quality ISPs are excessive.Conversely, if p pA B< , the low quality ISPs have no more subscriber because the users can obtain

a better Internet access at a lower price. If 0 1<−−

<p pA B

A Bλ λ, then each club obtains a positive

market share (this is a necessary condition for an equilibrium in a vertical differentiation model). Inthis case, the aggregate demand for the high quality ISPs is equal to :

Dp p

AA B

A B

= −−−

1λ λ

(4)

and the aggregate demand for the low quality ISPs is equal to :

Dp p p

BA B

A B

B

B

=−− −λ λ λ

(5)

The user with a preference θ λ= pB B is indifferent between subscribing to a low quality ISP andnot subscribing at all. The aggregate profits of the ISPS can be written as :

( )

( )

πλ λ

πλ λ λ

A AA B

A B

B BA B

A B

B

B

p cp p

p cp p p

= − −−−

= − −−

−

1

(6)

The equilibrium prices are obtained by maximizing the profit of each club with respect to his ownprice. The best replies are given by :

pp c

pp c

AA B B

BA B A A

A

=− + +

=− + +

λ λ

λ λ λλ

2

2

(7)

8

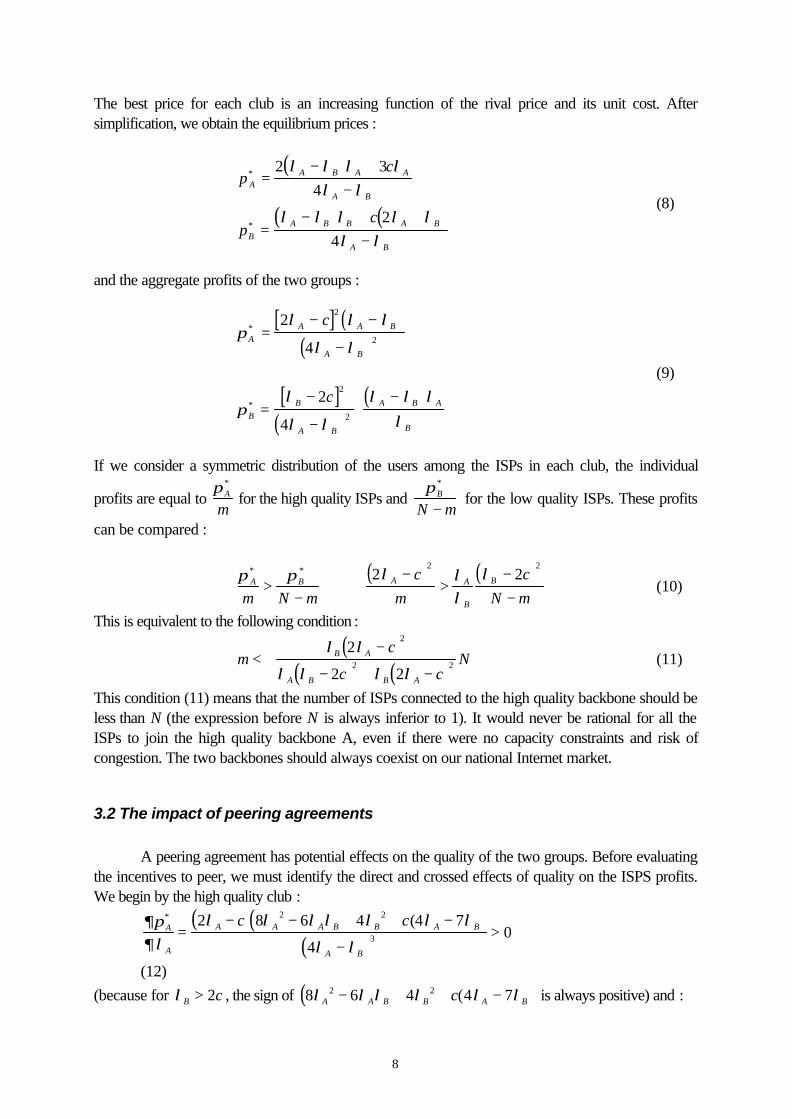

The best price for each club is an increasing function of the rival price and its unit cost. Aftersimplification, we obtain the equilibrium prices :

( )

( ) ( )

pc

pc

AA B A A

A B

BA B B A B

A B

∗

∗

=− +

−

=− + +

−

2 3

4

2

4

λ λ λ λλ λ

λ λ λ λ λλ λ

(8)

and the aggregate profits of the two groups :

[ ] ( )( )

πλ λ λ

λ λA

A A B

A B

c∗ =

− −

−

2

4

2

2

(9)

[ ]( )

( )π

λ

λ λ

λ λ λλB

B

A B

A B A

B

c∗ =

−

−

−2

4

2

2

If we consider a symmetric distribution of the users among the ISPs in each club, the individual

profits are equal to πA

m

∗

for the high quality ISPs and πB

N m

∗

− for the low quality ISPs. These profits

can be compared :

( ) ( )π π λ λλ

λA B A A

B

B

m N m

c

m

c

N m

∗ ∗

>−

⇔−

>−−

2 22 2

(10)

This is equivalent to the following condition :

( )( ) ( )

mc

c cNB A

A B B A

<−

− + −

λ λ

λ λ λ λ

2

2 2

2

2 2 (11)

This condition (11) means that the number of ISPs connected to the high quality backbone should beless than N (the expression before N is always inferior to 1). It would never be rational for all theISPs to join the high quality backbone A, even if there were no capacity constraints and risk ofcongestion. The two backbones should always coexist on our national Internet market.

3.2 The impact of peering agreements

A peering agreement has potential effects on the quality of the two groups. Before evaluatingthe incentives to peer, we must identify the direct and crossed effects of quality on the ISPS profits.We begin by the high quality club :

( )( )( )

∂π∂λ

λ λ λ λ λ λ λ

λ λA

A

A A A B B A B

A B

c c∗

=− − + + −

−>

2 8 6 4 4 7

40

2 2

3

(

(12)

(because for λB c> 2 , the sign of ( )8 6 4 4 72 2λ λ λ λ λ λA A B B A Bc− + + −( is always positive) and :

9

( ) ( )( )

∂π∂λ

λ λ λ

λ λA

B

A A B

A B

c∗

= −− +

−<

2 2

40

2

3 (13)

The club A always increases its profit by improving his quality. Conversely, his profit lessens whenthe quality of the rival group rises. These results are well known in the models of verticaldifferentiation. The profit of the high quality ISPs depends on the degree of differentiation with theservices provided by the low quality ISPs. The higher the differentiation in quality is, the less intensethe price competition is. When the quality of the ISPs B decreases or the quality of the ISPs Aincreases, then the vertical differentiation grows up for the benefit of the high quality group. Now,consider the aggregate profit of the low quality ISPs. By deriving the equilibrium profit with respectto the two levels of quality, we obtain :

( ) ( )( )

∂π∂λ

λ λ λ

λ λB

A

B A B

A B

c∗

=− +

−>

2 2

40

2

3 (14)

and

( ) ( )( )( )

∂π∂λ

λ λ λ λ λ λ λ

λ λ λB

B

A B B A B A A

B A B

c c c c∗

=− − − + − +

−

2 7 4 4 6 8

4

2 2 2

2 3

( )(15)

The low quality ISPs always benefits from a rise of λA because it strengthens the differentiation andlessens the price competition between the ISPs without reducing the quality of group B. Hence thelow quality ISPs can rise their price and their profits6.

The own quality of the ISPs on the backbone B has a more ambiguous impact. An increase of λB

allows the group B to increase his market share. But the price competition is likely to be more

severe. The sign of ∂π∂λ

B

B

∗

should be positive when the value of λB is far from λA and negative when

λB becomes too close to λA . To determine the threshold value of λB below which the impact is still

positive, we analyze the sign of ( )− − + − +λ λ λ λ λB A B A Ac c c2 2 27 4 4 6 8( ) . This quadratic

expression exhibits two roots. One of the roots corresponds to the threshold value and is equal to :

( )λ

λ λ λ λ

λB

A A A A

A

c c c

c=

− + + −

−

2 3 4 44 23

7 4

2 2

(16)

The aggregate profit of ISPs belonging to the backbone B increases with his own quality if and only ifλ λB B< . This threshold value is equal to λ λB A= 4 7/ for c=0 and increases with the high quality

λA and the unit cost. The low quality ISPs are more likely to benefit from an increase of their ownquality when Internet access services are more costly to supply.

6 On the other hand, the rise of λA induces a loss of market share for the club B. However this negative effect is

more than counterbalanced by the positive price effect.

10

Now, we can evaluate the incentives of ISPs to peer with each other by differentiating their

equilibrium profits. First we consider intra-high quality peering which is characterized by ∂λ∂

A

AAn> 0

and ∂λ∂

B

AAn= 0 . The group A increases his own quality by peering with each other, but these

agreements have no effect on the rival quality. The effect on the profit is given by :∂π∂

∂π∂λ

∂λ∂

A

AA

A

A

A

AAn n

∗ ∗

= > 0 (17)

The high quality ISPs should always choose to peer with each other (unless the cost ofinterconnection is too high) and the number of intra agreements would be equal to m(m-1)/2.

In case of inter-group peering, we have ∂λ∂

A

ABn> 0 and

∂λ∂

B

ABn> 0 . Hence, inter-group

peering has a direct effect on the profit of the club A through his own quality and an indirect effectthrough the rival quality. The result is ambiguous :

∂π∂

∂π∂λ

∂λ∂

∂π∂λ

∂λ∂

A

AB

A

A

A

AB

A

B

B

ABn n n

∗ ∗ ∗

= + (18)

The direct effect is positive, because inter-group peering reduces the risk of congestion and improvesthe quality of the group A. But the indirect effect is negative because intergroup peering improvesalso the quality of the rival group and intensifies the price competition. The net effect depends on therespective impact of inter-group peering on each quality. If the low quality group benefits more ofthis kind of agreements, then the group A can refuse to peer with him. Conversely, if the benefits isequally shared between the two groups, then the high quality ISPs have always positive incentives to

peer with their rivals. Formally, if ∂λ∂

∂λ∂

A

AB

B

ABn n= , we have :

( )( ) ( ) ( )( )[ ]∂π

∂λ

λ λλ λ λ λ

∂λ∂

A

AB

A

A B

A B A BA

ABnc

cn

∗

=−

−− − + >

2

42 2 3 03 (19)

Consider now the incentives of group B to peer with the high quality group :

∂π∂

∂π∂λ

∂λ∂

∂π∂λ

∂λ∂

B

AB

B

A

A

AB

B

B

B

ABn n n

∗ ∗ ∗

= + (20)

The indirect effect is always positive : an increase of the high quality benefits to the group B. Thedirect effect is more ambiguous. If the quality λB is initially low, then inter-group peering byimproving this quality is likely to rise the profits of group B. Conversely if the quality is very close toλA , then the direct effect is negative and counterbalances the indirect effect.

Finally, if we analyze intra-group peering, we have ∂λ∂

A

BBn= 0 and :

∂π∂

∂π∂λ

∂λ∂

B

BB

B

B

B

BBn n

∗ ∗

= (21)

11

Similarly the incentives of the low quality ISPs to peer with each other depends on their initial quality.If this quality is superior to the threshold value λB , then the ISPs will refuse any intra peering

agreement. These different results can be summarized in the two following propositions.

Proposition 1 : The m ISPs interconnected to the high quality backbone have alwaysstrong incentives to peer with each other.

Proposition 2 : The (N-m) ISPs interconnected to the low quality backbone will peerwith each other only if the high quality ISPs refuse or restrictintergroup peering agreements.

The proposition 2 results from the fact that given λA and λB , ∂π∂

∂π∂

B

AB

B

BBn n

∗ ∗

> as ∂λ∂

∂λ∂

B

BB

B

ABn n= .

For the club B, an inter peering agreement is more profitable than an intra group peering agreement,

because of the positive indirect effect on the high quality ∂π∂λ

∂λ∂

B

A

A

ABn

∗

> 0 . Hence, the low quality

ISPs should proceed sequentially. First, they should appeal to the high quality ISPs inter peeringagreements. Then they should consider the opportunity of intra peering agreements. Suppose that thetwo clubs convened nAB

* peering agreements such that the club B receives a complete satisfaction

∂π∂

B

ABn

∗

= 0 . As ∂π∂λ

∂λ∂

B

A

A

ABn

∗

> 0 then ∂π∂λ

∂λ∂

B

B

B

AB n nn

AB AB

∗

=

>*

0 and ∂π

∂B AB

BB

nn

∗

<( )*

0 for any nBB. The

club B cannot have intra peering agreement when the club A has accepted all the requested intergroup peering.

We can reformulate the propositions 1 and 2 like that : the high quality ISPs have moreincentives to make intra-group peering than inter-group peering whereas the low quality ISPshave more incentives to make intergroup peering.

We can establish another interesting proposition.

Proposition 3 : If the number of ISPs interconnected to the high quality backboneincreases, then the low quality ISPs will have a higher probability topeer with each other and with the high quality ISPs.

If the number m of high quality ISPs rises, then the number of intra A peering agreement will increaseand the level of quality λA too. Hence, the differentiation between the two club is strengthened andthe threshold value λB below which the low quality club has incentives to make intra peering, rises.

Obviously the incentives to peer with the high quality club increases also with the incentives for intrapeering.

3.3 Simulations

These propositions can be illustrated by some simulations. We consider linear quality functions :

12

( )λ α µA AA ABn n= + +

( )λ α µB BB ABn n= + +' '

The parameters must satisfy α>α’ as the backbone A supplies with a higher quality and a betterconnectivity. µ and µ’ measure the impact of peering agreements on the quality of access. µ can belower than µ’ if the low quality club benefits more of inter-group peering than the high quality club.As the profit of the high quality ISPs always increases with the number of intra peering agreements,all the ISPs on the backbone A have an interest in peering with each other. So we should havenAA=(m-1)m/2. Firstly, we simulate the incentives of the clubs A and B to peer together, given thefollowing initial qualities λ α µA m m= + −( ) /1 2 and λ αB = ' . Then, we simulate the incentives of

low quality ISPs to peer each other, given the following qualities ( )λ α µA ABm m n= + − +( ) / *1 2

and λ α µB ABn= +' ' * (with n N m mAB* ( )< − is the number of inter-club agreements that the ISPs

have convened).We fix α=2, α’=1.5, c=0.1, N=20 and m=10. The maximum number of inter peering agreement isequal to 100. We consider the cases where inter peering has a symmetric impact µ= µ’and anasymmetric impact (µ= µ’).

For µ= µ’=0.05, the two groups have incentives to peer together and the number of inter-group agreements should be equal to 100 (figure 3). For µ=0.05<µ’=0.07, the high quality grouphas no more incentives to peer with the low quality group and there is no inter club peering (figure 4).

Then we consider the incentives of low quality ISPs to peer with each other, when the highquality ISPs has accepted inter-group peering in the symmetric case (µ=0.05, µ’=0.05). The

qualities are equal to ( )λ α µA m m m N m= + − + −( ) / ( )1 2 and λ α µB m N m= + −' ' ( ) with m=10

and N=20. We observe on figure 5 that the profit of low quality ISPs is always decreasing withintra-group peering agreements. The club B should have just inter group peering in this example ofsimulation.

Now, we examine the incentives of low quality ISPs to peer with each other, when the highquality ISPs refuse inter-group peering in the asymmetric case (figure 6). The initial qualities are

20 40 60 80 100

0.2

0.4

0.6

0.8

1

20 40 60 80 100

0.2

0.4

0.6

0.8

Figure 3 : The incentives for inter-clubpeering in the symmetric case µ= µ’=0.05

Figure 4 : The incentives for inter-club peeringin the asymmetric case µ= 0.05 µ’=0.07

Profit of the high quality club

Profit of the low quality club

Profit of the high quality club

Profit of the low quality club

13

λ α µA m m= + −( ) /1 2 and λ αB = ' . The low quality ISPs have interest in limiting the number ofintra-group peering agreements (about 12 agreements on a maximal number of 45)

Finally, we can illustrate the effect of a growing size of the high quality club in the asymmetriccase. The figure 7 shows that the high quality club accepts to have some limited inter peeringagreements (about 19) when the number of high quality ISPs is 15. On figure 8, the optimal numberof intra peering agreements is 24 instead of 12 previously, for a high quality club of twelve ISPs.

To sum up, an Internet access market characterized by two levels of quality (with m highquality ISPs and N-m low quality ISPs) leads to peering matrices with the following properties :

10 20 30 40 50 60 70

1.48

1.52

1.54

1.56

1.58

Figure 7 : The incentives of the high qualityclub for inter peering in the asymmetric case µ=0.05 µ’=0.07 , with m=15

Figure 8 : The incentives of the low quality clubfor intra peering in the asymmetric case µ= 0.05,µ’=0.07 , with m=12

10 20 30 40

0.06

0.08

0.12

0.14

0.16

10 20 30 40

0.04

0.05

0.06

0.07

Figure 5 : The incentives of the low qualityclub for intra peering in the symmetric caseµ= µ’=0.05

Figure 6 : The incentives of the low quality clubfor intra peering in the asymmetric case µ= 0.05µ’=0.07

5 10 15 20 25

0.07

0.08

0.09

Profit of the low quality club

Profit of the high quality club

Profit of the high quality club

Profit of the low quality club

14

i) if low quality ISPs benefit more from inter-group peering than high quality ISPs, then inter-grouppeering should be less frequent than intra low quality peering,ii) if the low quality ISPs benefit as much as the high quality ISPs from inter-group peering, theninter-group peering should be more frequent than intra low quality peeringiii) in any case, intra high quality peering should always be more intense than intra low quality peeringand inter group peering.

IV) Empirical analysis of peering and transit agreements in theFrench Internet market

The aim of this part is to verify some of the conjectures presented in the theoretical part. First, wewould like to categorize the nature of the « clubs » built by the ISPs choosing the same backbone astransit carrier on the French market. Second, we want to investigate how the members of those« clubs » peer and whether the main theoretical result is confirmed : that high quality ISPs will preferto peer with each other, while low quality ISPs would do the same, only if they cannot peer with thehigh quality ones. Finally it is interesting to evaluate the importance of peering in the French context, amarket which is, however, not yet fully developed.

4.1 Data

Peering and transit agreements among ISPs are convened on a voluntary basis, and escape anysupervision from regulatory authorities. Therefore, it is presently impossible to give an exhaustivepicture of those agreements, even if the number of ISPs involved is quite limited. However, somepartial information is provided either by consultancy firms, which specialize in the measure of qualityof transmission on the Internet, or by public institutions which run a public TCP/IP network used byprivate ISPs either as a traffic exchange node or as a backbone. Since at the origin most TCP/IPnetworks were public, private ISPs have long got the habit to peer on to the public network.

In France, the consultancy firm available on the Net at http://www.serveurdedie.com, providesinformation about transit agreements among ISPs, and tests the quality of transport infrastructures todeliver packets from France to the US and vice versa. We are thus able to collect from thisconsultancy firm, the information concerning agreements between ISPs about their transit traffic. Inparticular, we can get the number of in and out going transit traffic that any French ISP identified byserveurdedie.com has signed on. It is thus possible to shape the "clubs" of ISPs put forward by ourtheoretical analysis. We should emphasize however that a single ISP may belong to several clubs.We have constructed, from the information provided by serveurdedie.com, a matrix consisting, asrows, of the ISPs or IP infrastructure owners, and as columns, of the major transit carriers inFrance : Renater, Transpac, Cégétel, UUnet .... We have also added Parix and MAE, two privatenodes of interconnection to which we return later on. The matrix element xij is one if ISP i subscribesto a transit agreement with the carrier j , zero otherwise. This matrix will be called the transitmatrix.

ISPs have also the opportunity to peer with each other, either within or outside the "transit club" towhich they belong. This opportunity is given in particular through the participation to the "SFINX"peering node. SFINX is run by the French public Internet carrier Renater, but it is dedicated topeering between private users, which have to pay for a subscription fee to join SFINX. Although

15

there are also two private peering nodes in France as seen above (MAE-P run by Uunet and Parix,jointly run by Telehouse and France Télécom), SFINX is still the most important peering nodes forIP carriers operating in France. There are altogether 38 ISPs (some of them subsidiaries of largerones) which peer onto the SFINX. Renater publishes regularly the matrix of all peering agreementsconvened between ISPs on to the SFINX7. Contrarily to transit agreements, peering on the SFINXis devoted to exchange direct traffic, namely traffic originated from one partner, and terminating atthe other partner's premise. The peering matrix on SFINX will be the basic data source that we willuse to analyze peering agreements. Like the transit matrix, element x’ij of the square peering matrix isequal to 0, if no peering agreement exists between ISP i and ISP j, and it equals one otherwise.

We have thus two sets of data on the French market. On one hand, those concerning the peeringagreements on the SFINX (the peering matrix). On the other hand, those summarizing the transitagreements between "backbones" and ISPs (the transit matrix). The two sets provide thenecessary information to verify some propositions of the theoretical part.

4.2 Methodology

It is difficult to feature the ISPs, in terms of turnover, range of activities, customers, etc... Some ofthem do not publish their account, and an even more serious drawback is that there are manymergers and acquisitions in this rapidly evolving sector. Therefore, we have not taken too much intoaccount those economic indicators and worked only with the peering and transit agreements. This isequivalent to suppose that all the ISPs are identical from an economic point of view. We will comeback to these features later on, when they will be used to help understanding the results of thestatistical analysis.

The central question is to determine how ISPs gather for this transit agreements, and how theserelate to their peering agreements. We have thus constructed clusters of ISPs, for each matrix,(transit and peering), and have attempted to confirm the theoretical propositions of a link betweentransit behavior and peering behavior. The methods used for this, is a descriptive statistical methodcalled hierarchical ascending clustering, conducted on a multiple correspondence analysis. Aspecialized software package called SPAD has been used for that purpose8. In general, thecorrespondence analysis is particularly suited for comparing the profiles of individuals according tosome qualitative features (e.g. their answer to a questionnaire). Here the individuals of our sample arethe ISPs, while the qualitative features are the agreements they convene, either among each other(peering), or with major backbones (transit)9.

The method provides a synthetic representation of the sample in a two dimensional space, whichgives a minimal transformation of the initial « cloud » of individuals in the multidimensional space. Thelatter has 2*n dimensions, n being the number of transit (respectively, peering) partners that an ISP

7 Note that the ISPs are not compelled to have a peering agreement with all other ISPs subscribers to SFINX.8 An introduction to this type of analysis is provided in Lebart, Morineau, Piron (1996).9 The backbones considered here are : Transpac, Oleane, Uunet, Open Transit, Cegetel, Unisource-Siris, ISDNet,Ebone, Parix, Mae.

16

can have10. This minimal projection uses a special distance called χ2 distance , which has a propertyof « duality »11. This projection helps to reveal the differences between the profiles of individuals.Following this descriptive representation, it is possible to categorize the individuals in clusters, builtup according to a similarity index. Some statistical tests help to pick up the best clustering.

4.3 Results

Transit agreements in France : setting up « clubs » of different quality ?

Here we look at the creation of « clubs » built around the major French backbones. Among theISPs present on the French market, the following have a significant number of transit agreements withothers, and this gives them a prominent position as transit carriers. Those big players are Transpac,Oléane, Uunet, Cegetel and ISDNet, Siris/ Unisource.

Table 1: List of ISPs which have agreed to transport ingoing traffic of other ISPs

Transpac30 agreements

Bull, Francenet, Grolier Int., Imaginet, Infonie, Internext, Transpac, MonacoTel, Microsoft, Euro Info, Pacwan, Satelnet, Infonie, Nordnet, Ornis,Decathlon, Renault, Etsi, Atos, Integra, Monte Carlo Tel, SDV, Ferri,Marcireau, Echo, CGE Online, Rerif, Icor, Macorbur, Cadrus

Uunet France24 agreements :

Francenet, Internext, Oléane, Planetenet, Uunet, Shell, Alto, Alpes Network,Ubisoft, Ornis, Transeo, Renault, Atos, Integra, Cpod, KDD Fr, SDV,Marcireau, CGE Online, Gulliver, Alcatel, Ed du Present, Macorbur, AFP

Cegetel14 agreements :

Asi, Cegetel, Easynet, Infonie, Internext, ISDNet, Worldnet, Infonie, Ubisoft,Cegetel Multimedia, Etsi, Neuronnexion, Proxad, Cadrus

Oléane15 agreements :

Francenet, Nic-France, Oléane, Alpe Networks, Ubisoft, Decathlon, CaissedesDépôts, Ferri, Echo, Wargny, Icor, France Telecom Hebergement, CreditAgricole, Ed. du Présent, Exane

ISDNet9 agreements :

Cybercâble, Netsat, ISDNet, Monaco Tel, Worldnet, Pacwan, Internet Fr,Neuronnexion, Activnet

Unisource/Siris10 agreements :

Asi, Easynet, Ecritel, Imaginet, ISDnet, Siris, GFI, Internet Fr, Matra Grolier,Gulliver

Source : Serveurdedie.com

If all ISPs had only one transit agreement with a backbone carrier, the « clubs » that we are lookingfor, would naturally come out from Table 1. However, as the table shows, most ISPs do not haveone transit agreement only, probably for security reason : they are prepared to pay for a certainredundancy. Hence they belong to at least «two « clubs »12. So it is important to find whether,lacking a pure partition of French ISPs around backbones, some of them exhibit similar profilesconcerning their transit agreements. This may help to distinguish between « high quality » and « low 10 There are 2*n dimensions, because each item of a qualitative data is a dimension. and there are only, for each

partner, two items (agreement =1 or agreement =0). Therefore, there are 2*n possible items.11 It is possible to change the roles of individuals and variables and to represent the variables in a m dimensionalspace, m being the number of individuals. It can be shown that the two representations give the same eigenvaluesand eigenvectors.12 Among the 92 IP networks identified by serveurdedie.com as « operational », more than a half has a transitagreement with backbones other than the six of Table 1.

17

quality » ISPs, in the spirit of the theoretical model. One observations has to be made however.Table 1 reflects the transit agreements for all ISPs and includes in particular the private IP networksof some large companies (Intranets), which need access to the Internet, but have perhaps no interestto extend their connectivity.

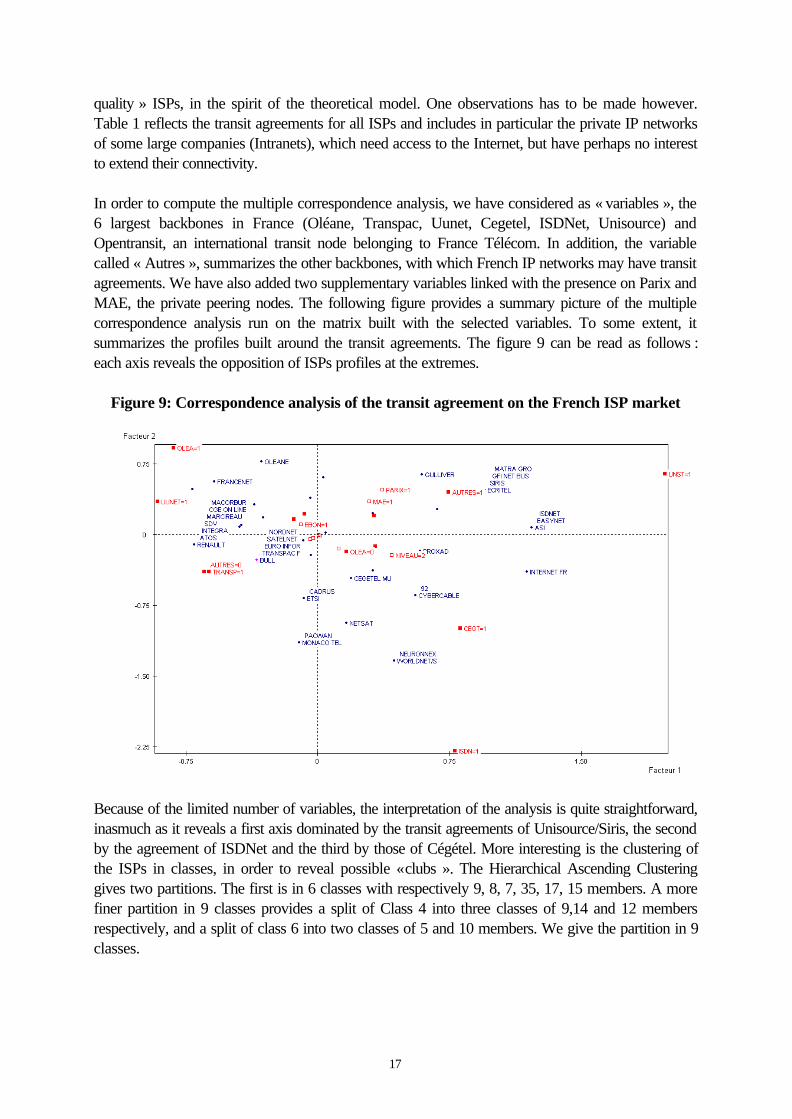

In order to compute the multiple correspondence analysis, we have considered as « variables », the6 largest backbones in France (Oléane, Transpac, Uunet, Cegetel, ISDNet, Unisource) andOpentransit, an international transit node belonging to France Télécom. In addition, the variablecalled « Autres », summarizes the other backbones, with which French IP networks may have transitagreements. We have also added two supplementary variables linked with the presence on Parix andMAE, the private peering nodes. The following figure provides a summary picture of the multiplecorrespondence analysis run on the matrix built with the selected variables. To some extent, itsummarizes the profiles built around the transit agreements. The figure 9 can be read as follows :each axis reveals the opposition of ISPs profiles at the extremes.

Figure 9: Correspondence analysis of the transit agreement on the French ISP market

Because of the limited number of variables, the interpretation of the analysis is quite straightforward,inasmuch as it reveals a first axis dominated by the transit agreements of Unisource/Siris, the secondby the agreement of ISDNet and the third by those of Cégétel. More interesting is the clustering ofthe ISPs in classes, in order to reveal possible « clubs ». The Hierarchical Ascending Clusteringgives two partitions. The first is in 6 classes with respectively 9, 8, 7, 35, 17, 15 members. A morefiner partition in 9 classes provides a split of Class 4 into three classes of 9,14 and 12 membersrespectively, and a split of class 6 into two classes of 5 and 10 members. We give the partition in 9classes.

18

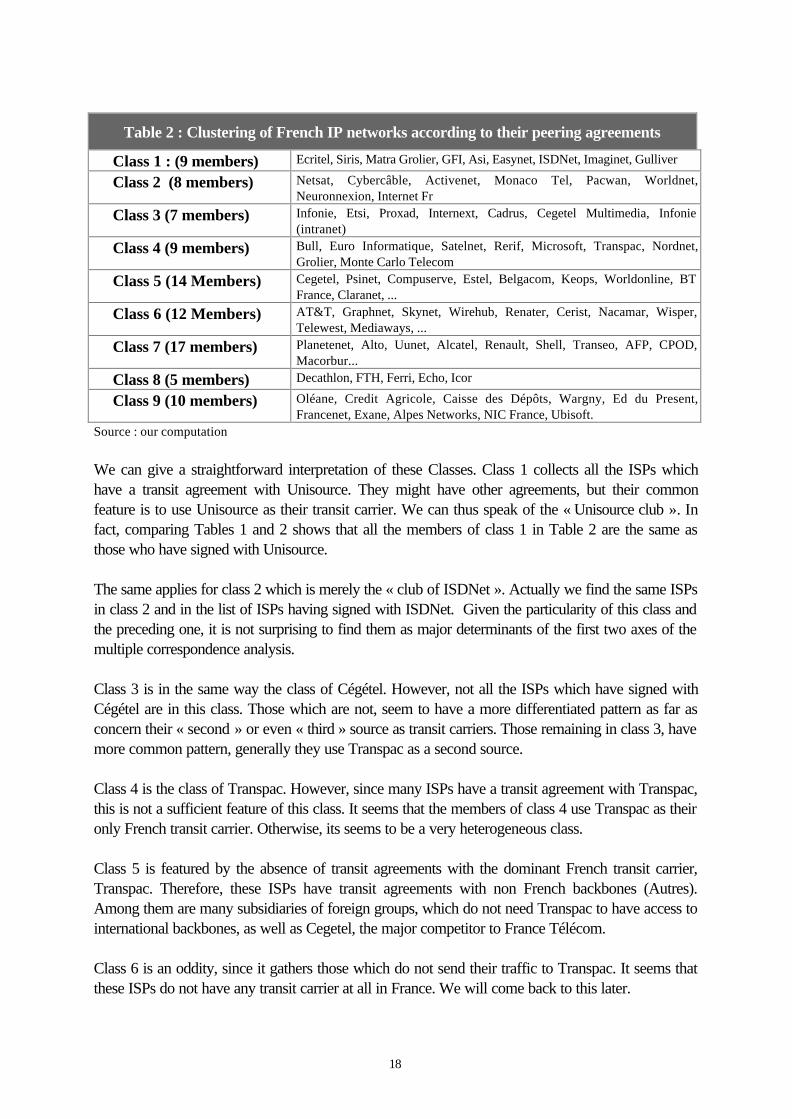

Table 2 : Clustering of French IP networks according to their peering agreements

Class 1 : (9 members) Ecritel, Siris, Matra Grolier, GFI, Asi, Easynet, ISDNet, Imaginet, Gulliver

Class 2 (8 members) Netsat, Cybercâble, Activenet, Monaco Tel, Pacwan, Worldnet,Neuronnexion, Internet Fr

Class 3 (7 members) Infonie, Etsi, Proxad, Internext, Cadrus, Cegetel Multimedia, Infonie(intranet)

Class 4 (9 members) Bull, Euro Informatique, Satelnet, Rerif, Microsoft, Transpac, Nordnet,Grolier, Monte Carlo Telecom

Class 5 (14 Members) Cegetel, Psinet, Compuserve, Estel, Belgacom, Keops, Worldonline, BTFrance, Claranet, ...

Class 6 (12 Members) AT&T, Graphnet, Skynet, Wirehub, Renater, Cerist, Nacamar, Wisper,Telewest, Mediaways, ...

Class 7 (17 members) Planetenet, Alto, Uunet, Alcatel, Renault, Shell, Transeo, AFP, CPOD,Macorbur...

Class 8 (5 members) Decathlon, FTH, Ferri, Echo, Icor

Class 9 (10 members) Oléane, Credit Agricole, Caisse des Dépôts, Wargny, Ed du Present,Francenet, Exane, Alpes Networks, NIC France, Ubisoft.

Source : our computation

We can give a straightforward interpretation of these Classes. Class 1 collects all the ISPs whichhave a transit agreement with Unisource. They might have other agreements, but their commonfeature is to use Unisource as their transit carrier. We can thus speak of the « Unisource club ». Infact, comparing Tables 1 and 2 shows that all the members of class 1 in Table 2 are the same asthose who have signed with Unisource.

The same applies for class 2 which is merely the « club of ISDNet ». Actually we find the same ISPsin class 2 and in the list of ISPs having signed with ISDNet. Given the particularity of this class andthe preceding one, it is not surprising to find them as major determinants of the first two axes of themultiple correspondence analysis.

Class 3 is in the same way the class of Cégétel. However, not all the ISPs which have signed withCégétel are in this class. Those which are not, seem to have a more differentiated pattern as far asconcern their « second » or even « third » source as transit carriers. Those remaining in class 3, havemore common pattern, generally they use Transpac as a second source.

Class 4 is the class of Transpac. However, since many ISPs have a transit agreement with Transpac,this is not a sufficient feature of this class. It seems that the members of class 4 use Transpac as theironly French transit carrier. Otherwise, its seems to be a very heterogeneous class.

Class 5 is featured by the absence of transit agreements with the dominant French transit carrier,Transpac. Therefore, these ISPs have transit agreements with non French backbones (Autres).Among them are many subsidiaries of foreign groups, which do not need Transpac to have access tointernational backbones, as well as Cegetel, the major competitor to France Télécom.

Class 6 is an oddity, since it gathers those which do not send their traffic to Transpac. It seems thatthese ISPs do not have any transit carrier at all in France. We will come back to this later.

19

Class 7 is the « club of Uunet », namely, those ISPs which send their transit traffic to Uunet. Thereare some major multinational firms among them (Shell, Renault, Alcatel, AFP) which use theinternational presence of Uunet to get a better connectivity with the rest of the world.

Class 8 is the small group of ISPs who use both Oléane and Transpac as their transit carriers. Theyare focused on the French market. Finally Class 9 is the exclusive club of Oléane.

Hence, the exercise reveals a certain order in the policy of IP networks, concerning their transitagreements. Some « clubs » are emerging around Unisource/Siris, Cégétel, ISDNet, Oléane,because those backbones have relatively few transit agreements, and such agreements make thosewho sign them quite apart. On the other hand, Transpac and Uunet, which have a more extendedagreement portfolio, will not help very much in defining a « club ». Now a step further in the line ofour theoretical model, is to examine who peers and who does not.

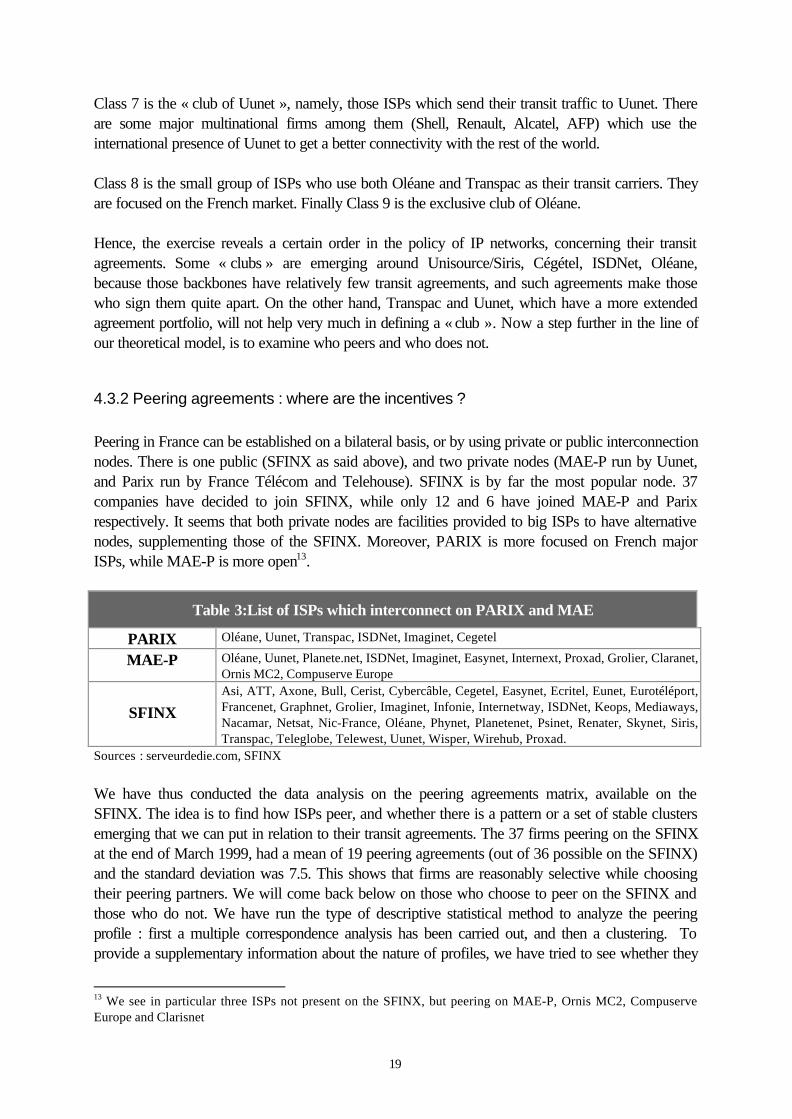

4.3.2 Peering agreements : where are the incentives ?

Peering in France can be established on a bilateral basis, or by using private or public interconnectionnodes. There is one public (SFINX as said above), and two private nodes (MAE-P run by Uunet,and Parix run by France Télécom and Telehouse). SFINX is by far the most popular node. 37companies have decided to join SFINX, while only 12 and 6 have joined MAE-P and Parixrespectively. It seems that both private nodes are facilities provided to big ISPs to have alternativenodes, supplementing those of the SFINX. Moreover, PARIX is more focused on French majorISPs, while MAE-P is more open13.

Table 3:List of ISPs which interconnect on PARIX and MAE

PARIX Oléane, Uunet, Transpac, ISDNet, Imaginet, Cegetel

MAE-P Oléane, Uunet, Planete.net, ISDNet, Imaginet, Easynet, Internext, Proxad, Grolier, Claranet,Ornis MC2, Compuserve Europe

SFINXAsi, ATT, Axone, Bull, Cerist, Cybercâble, Cegetel, Easynet, Ecritel, Eunet, Eurotéléport,Francenet, Graphnet, Grolier, Imaginet, Infonie, Internetway, ISDNet, Keops, Mediaways,Nacamar, Netsat, Nic-France, Oléane, Phynet, Planetenet, Psinet, Renater, Skynet, Siris,Transpac, Teleglobe, Telewest, Uunet, Wisper, Wirehub, Proxad.

Sources : serveurdedie.com, SFINX

We have thus conducted the data analysis on the peering agreements matrix, available on theSFINX. The idea is to find how ISPs peer, and whether there is a pattern or a set of stable clustersemerging that we can put in relation to their transit agreements. The 37 firms peering on the SFINXat the end of March 1999, had a mean of 19 peering agreements (out of 36 possible on the SFINX)and the standard deviation was 7.5. This shows that firms are reasonably selective while choosingtheir peering partners. We will come back below on those who choose to peer on the SFINX andthose who do not. We have run the type of descriptive statistical method to analyze the peeringprofile : first a multiple correspondence analysis has been carried out, and then a clustering. Toprovide a supplementary information about the nature of profiles, we have tried to see whether they

13 We see in particular three ISPs not present on the SFINX, but peering on MAE-P, Ornis MC2, CompuserveEurope and Clarisnet

20

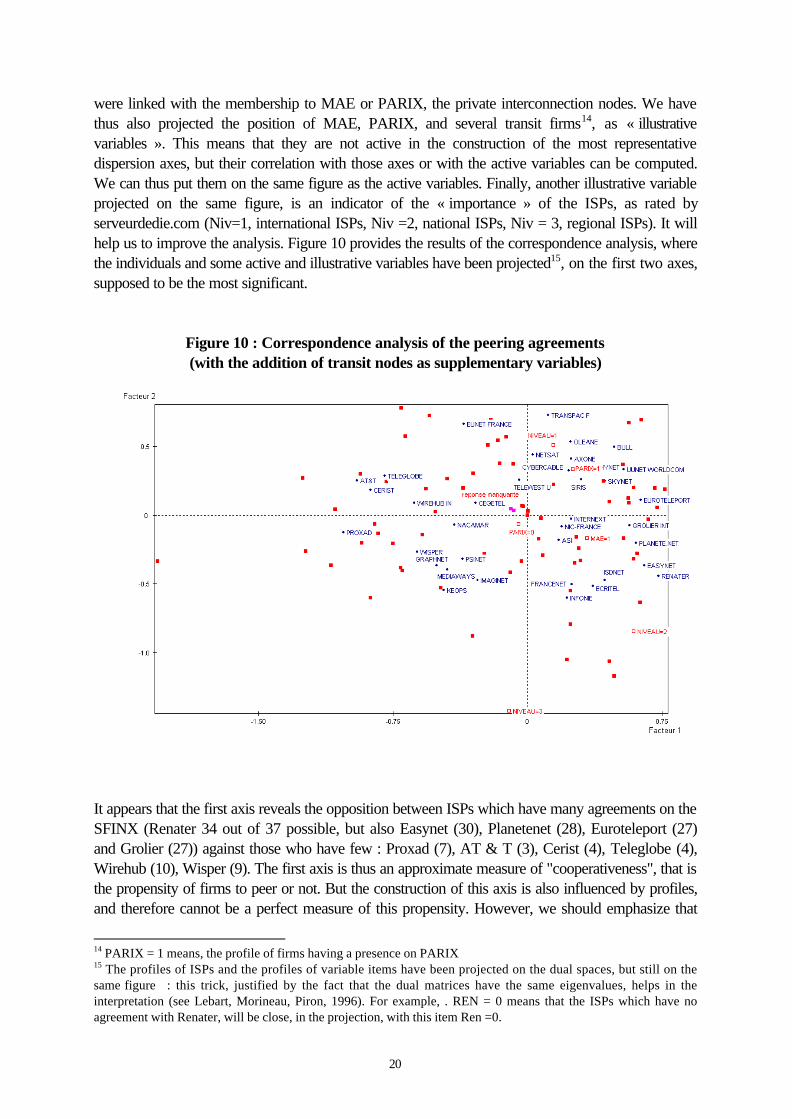

were linked with the membership to MAE or PARIX, the private interconnection nodes. We havethus also projected the position of MAE, PARIX, and several transit firms14, as « illustrativevariables ». This means that they are not active in the construction of the most representativedispersion axes, but their correlation with those axes or with the active variables can be computed.We can thus put them on the same figure as the active variables. Finally, another illustrative variableprojected on the same figure, is an indicator of the « importance » of the ISPs, as rated byserveurdedie.com (Niv=1, international ISPs, Niv =2, national ISPs, Niv = 3, regional ISPs). It willhelp us to improve the analysis. Figure 10 provides the results of the correspondence analysis, wherethe individuals and some active and illustrative variables have been projected15, on the first two axes,supposed to be the most significant.

Figure 10 : Correspondence analysis of the peering agreements(with the addition of transit nodes as supplementary variables)

It appears that the first axis reveals the opposition between ISPs which have many agreements on theSFINX (Renater 34 out of 37 possible, but also Easynet (30), Planetenet (28), Euroteleport (27)and Grolier (27)) against those who have few : Proxad (7), AT & T (3), Cerist (4), Teleglobe (4),Wirehub (10), Wisper (9). The first axis is thus an approximate measure of "cooperativeness", that isthe propensity of firms to peer or not. But the construction of this axis is also influenced by profiles,and therefore cannot be a perfect measure of this propensity. However, we should emphasize that

14 PARIX = 1 means, the profile of firms having a presence on PARIX15 The profiles of ISPs and the profiles of variable items have been projected on the dual spaces, but still on thesame figure : this trick, justified by the fact that the dual matrices have the same eigenvalues, helps in theinterpretation (see Lebart, Morineau, Piron, 1996). For example, . REN = 0 means that the ISPs which have noagreement with Renater, will be close, in the projection, with this item Ren =0.

21

besides Renater, which is the historical public backbone, the ISPs with the largest number of peeringagreements are not the big, vertically integrated ones, like France Telecom or Uunet. They areinstead Easynet, Planetenet and Euroteleport which are of lesser size. This suggests that big ISPs,which are supposed to provide a better quality because they can take benefit of economies of scale,are not very eager to peer with everybody. This is a first indication which goes in the direction of ourtheoretical conclusions.

Another comment should be made on those who do not peer very much. They are foreign ISPs,which are not strongly interested in a presence in France. Cerist is an Algerian research network,while Wirehub and Proxad are small foreign ISPs. AT&T has not yet invested very much in France.So these ISPs come to peer on the SFINX from abroad. Their behavior is perfectly rational and byno means can be interpreted with our theoretical model, which focusses not on foreign ISPs trying tofind counterpart in France through peering agreements, but on the national ISPs, which try toalleviate their capacity constraints through peering with other national ISPs.

The second axis of figure 10 focuses on ISPs with a medium range of peering agreements, and isexhibiting a contrast between Transpac and Eunet France, having seemingly similar profiles on onehand, and Infonie, Keops, Francenet, Imaginet, Ecritel or ISDNet on the other hand, which exhibitan opposite pattern. This means that firms which peer with Transpac or Eunet France (some of themmight be the same), would not peer with Francenet, Infonie, Imaginet or ISDNet, something thatmight not be seen at the first glance, or even through the inspection of the peering matrix. This gives aclue for saying that there may be clusters of ISPs, with well defined peering behavior.

As far as illustrative variables are concerned, we arrive to the following conclusion. The figure 10shows that ISPs peering with Transpac or Eunet will be of international dimension (Niv =1) andmight have another peering agreement on Parix (Parix =1), while those peering with ISDNet wouldrather be of regional or national dimension (Niv =3) and might have a slight preference for MAE asan alternative peering node (MAE = 1). This second category may contain Infonie, Keops,Francenet, Imaginet, Easynet, and the first one will include Transpac, Eunet, Bull, Oléane. Finallyanother opposition, not depicted on the figure, emerges on the third axis, between the variables withfew items (e.g. ISPs which do not peer with Renater, or those on the contrary which peer with AT &T or Wisper). This axis is very much influenced by the oddity of Renater on one hand, or Wisper andAT & T on the other hand.

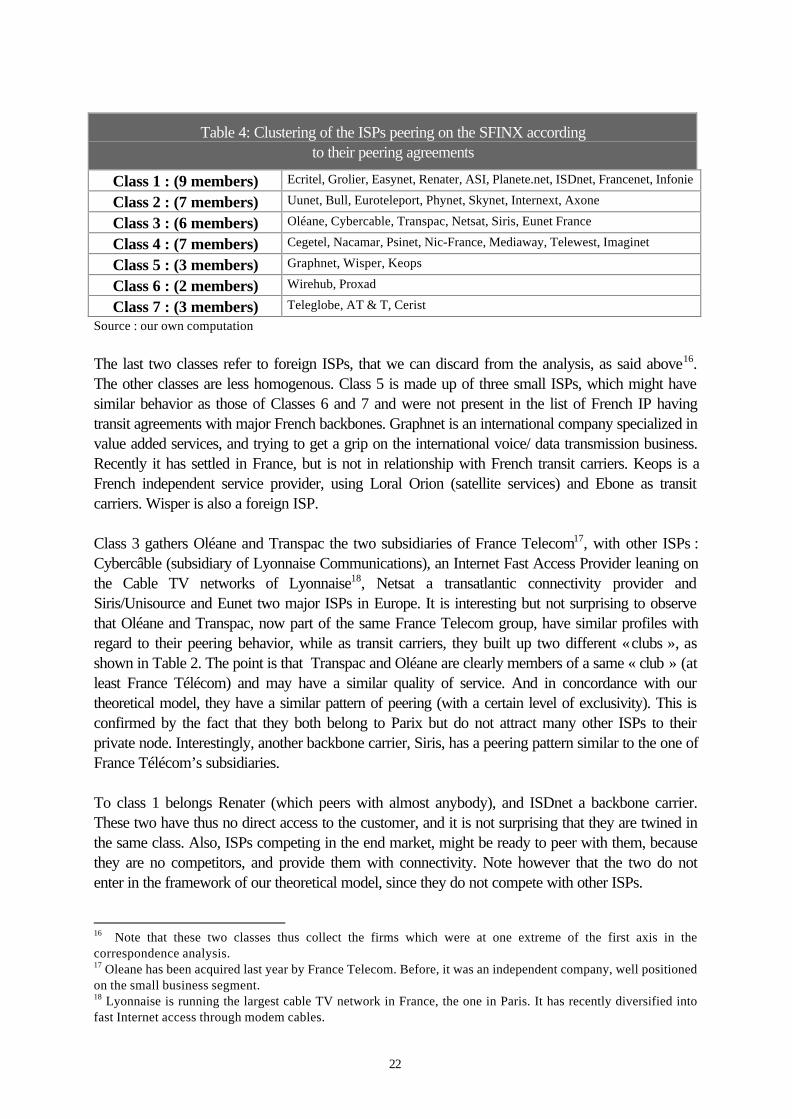

Now, the second step of the data analysis is the clustering of ISPs according to their peering profile.The hierarchical clustering, based upon their peering agreement profiles, will give a partition in 7classes, which is a configuration considered as the information rich. We have the following classes :

22

Table 4: Clustering of the ISPs peering on the SFINX accordingto their peering agreements

Class 1 : (9 members) Ecritel, Grolier, Easynet, Renater, ASI, Planete.net, ISDnet, Francenet, Infonie

Class 2 : (7 members) Uunet, Bull, Euroteleport, Phynet, Skynet, Internext, Axone

Class 3 : (6 members) Oléane, Cybercable, Transpac, Netsat, Siris, Eunet France

Class 4 : (7 members) Cegetel, Nacamar, Psinet, Nic-France, Mediaway, Telewest, Imaginet

Class 5 : (3 members) Graphnet, Wisper, Keops

Class 6 : (2 members) Wirehub, Proxad

Class 7 : (3 members) Teleglobe, AT & T, Cerist

Source : our own computation

The last two classes refer to foreign ISPs, that we can discard from the analysis, as said above16.The other classes are less homogenous. Class 5 is made up of three small ISPs, which might havesimilar behavior as those of Classes 6 and 7 and were not present in the list of French IP havingtransit agreements with major French backbones. Graphnet is an international company specialized invalue added services, and trying to get a grip on the international voice/ data transmission business.Recently it has settled in France, but is not in relationship with French transit carriers. Keops is aFrench independent service provider, using Loral Orion (satellite services) and Ebone as transitcarriers. Wisper is also a foreign ISP.

Class 3 gathers Oléane and Transpac the two subsidiaries of France Telecom17, with other ISPs :Cybercâble (subsidiary of Lyonnaise Communications), an Internet Fast Access Provider leaning onthe Cable TV networks of Lyonnaise18, Netsat a transatlantic connectivity provider andSiris/Unisource and Eunet two major ISPs in Europe. It is interesting but not surprising to observethat Oléane and Transpac, now part of the same France Telecom group, have similar profiles withregard to their peering behavior, while as transit carriers, they built up two different « clubs », asshown in Table 2. The point is that Transpac and Oléane are clearly members of a same « club » (atleast France Télécom) and may have a similar quality of service. And in concordance with ourtheoretical model, they have a similar pattern of peering (with a certain level of exclusivity). This isconfirmed by the fact that they both belong to Parix but do not attract many other ISPs to theirprivate node. Interestingly, another backbone carrier, Siris, has a peering pattern similar to the one ofFrance Télécom’s subsidiaries.

To class 1 belongs Renater (which peers with almost anybody), and ISDnet a backbone carrier.These two have thus no direct access to the customer, and it is not surprising that they are twined inthe same class. Also, ISPs competing in the end market, might be ready to peer with them, becausethey are no competitors, and provide them with connectivity. Note however that the two do notenter in the framework of our theoretical model, since they do not compete with other ISPs.

16 Note that these two classes thus collect the firms which were at one extreme of the first axis in thecorrespondence analysis.17 Oleane has been acquired last year by France Telecom. Before, it was an independent company, well positionedon the small business segment.18 Lyonnaise is running the largest cable TV network in France, the one in Paris. It has recently diversified intofast Internet access through modem cables.

23

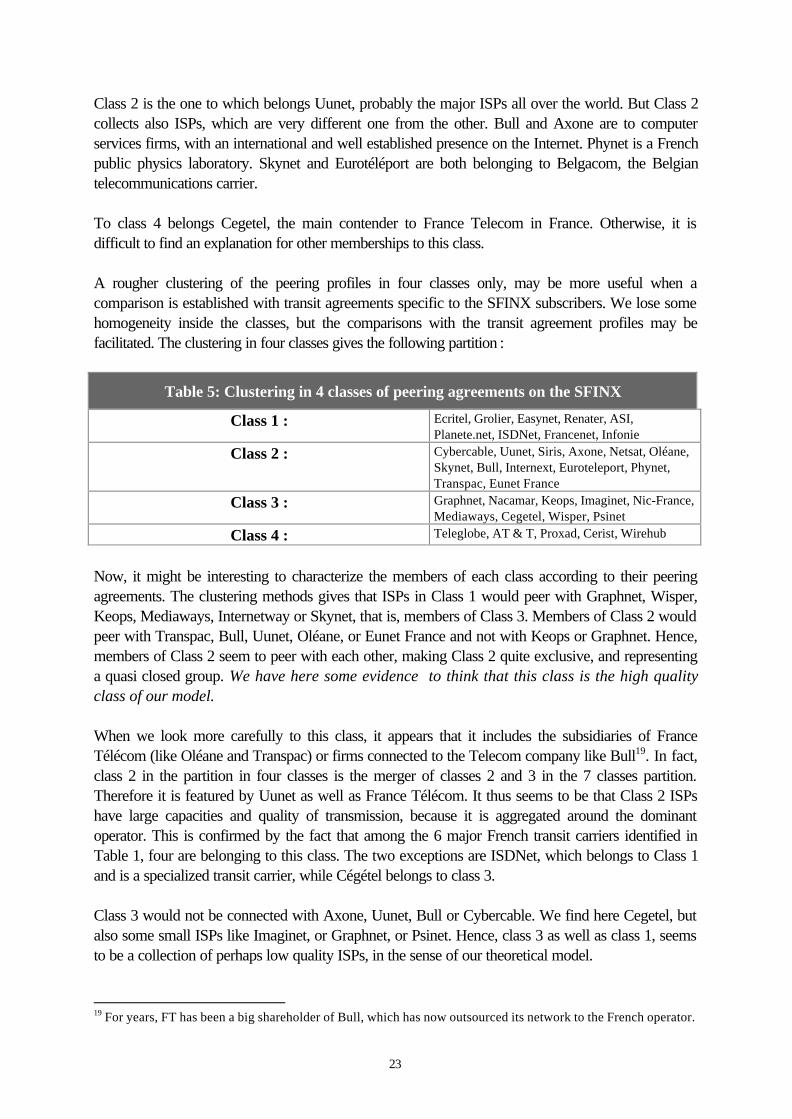

Class 2 is the one to which belongs Uunet, probably the major ISPs all over the world. But Class 2collects also ISPs, which are very different one from the other. Bull and Axone are to computerservices firms, with an international and well established presence on the Internet. Phynet is a Frenchpublic physics laboratory. Skynet and Eurotéléport are both belonging to Belgacom, the Belgiantelecommunications carrier.

To class 4 belongs Cegetel, the main contender to France Telecom in France. Otherwise, it isdifficult to find an explanation for other memberships to this class.

A rougher clustering of the peering profiles in four classes only, may be more useful when acomparison is established with transit agreements specific to the SFINX subscribers. We lose somehomogeneity inside the classes, but the comparisons with the transit agreement profiles may befacilitated. The clustering in four classes gives the following partition :

Table 5: Clustering in 4 classes of peering agreements on the SFINX

Class 1 : Ecritel, Grolier, Easynet, Renater, ASI,Planete.net, ISDNet, Francenet, Infonie

Class 2 : Cybercable, Uunet, Siris, Axone, Netsat, Oléane,Skynet, Bull, Internext, Euroteleport, Phynet,Transpac, Eunet France

Class 3 : Graphnet, Nacamar, Keops, Imaginet, Nic-France,Mediaways, Cegetel, Wisper, Psinet

Class 4 : Teleglobe, AT & T, Proxad, Cerist, Wirehub

Now, it might be interesting to characterize the members of each class according to their peeringagreements. The clustering methods gives that ISPs in Class 1 would peer with Graphnet, Wisper,Keops, Mediaways, Internetway or Skynet, that is, members of Class 3. Members of Class 2 wouldpeer with Transpac, Bull, Uunet, Oléane, or Eunet France and not with Keops or Graphnet. Hence,members of Class 2 seem to peer with each other, making Class 2 quite exclusive, and representinga quasi closed group. We have here some evidence to think that this class is the high qualityclass of our model.

When we look more carefully to this class, it appears that it includes the subsidiaries of FranceTélécom (like Oléane and Transpac) or firms connected to the Telecom company like Bull19. In fact,class 2 in the partition in four classes is the merger of classes 2 and 3 in the 7 classes partition.Therefore it is featured by Uunet as well as France Télécom. It thus seems to be that Class 2 ISPshave large capacities and quality of transmission, because it is aggregated around the dominantoperator. This is confirmed by the fact that among the 6 major French transit carriers identified inTable 1, four are belonging to this class. The two exceptions are ISDNet, which belongs to Class 1and is a specialized transit carrier, while Cégétel belongs to class 3.

Class 3 would not be connected with Axone, Uunet, Bull or Cybercable. We find here Cegetel, butalso some small ISPs like Imaginet, or Graphnet, or Psinet. Hence, class 3 as well as class 1, seemsto be a collection of perhaps low quality ISPs, in the sense of our theoretical model.

19 For years, FT has been a big shareholder of Bull, which has now outsourced its network to the French operator.

24

Class 4 would not peer with Planete.net, Grolier, Ecritel, Uunet, Skynet or Internetway. It is a Classof companies with few requisites on the French market, and with few peering agreements on theSFINX. This is definitely a class of very low quality ISPs, as far as the French market is concerned :members of this class have a low degree of connectivity on the French market.

The statistical analysis on the SFINX peering matrix has brought some evidence that our theoreticalframework gives an insight into the peering behavior of the French ISPs. In order to go further intothe analysis, we have conducted a statistical treatment of the transit agreements of the SFINXmembers only, in order to see whether they are linked with their peering agreements.

4.3.3 Transit agreements of the SFINX subscribers.

If we look to the transit agreement of ISPs who peer on the SFINX, we find a very different picturefrom the whole population of IP networks examined in paragraph 4.3.1. The following table, whichshould be compared to table 1 above, shows a much lower number of such agreements of SFINXmembers with transit carriers.

Table 6 : List of ISPs which are transit carriers of those peering on the SFINX

Transpac 6 : Bull, Grolier, Francenet, Imaginet, Internext, Infonie

Cégétel 5 : ISDNet, Easynet, Internext, ASI, Infonie

Unisource 5 : ISDNet, Imaginet, Easynet, Asi, Ecritel

Oléane 2 : Nic France, Francenet

ISDNet 2 : Cybercâble, Netsat,

Uunet 1 : Francenet

Source : serveurdedie.com

This table needs some comments. First, the sum of transit agreements of the backbones with SFINXmembers listed in table 6 (21) does not reach the total number of SFINX members (37). This meansthat some ISPs of the SFINX use backbones other than those of Table 6. This is probably the casefor foreign ISPs like AT&T or Telewest UK, or Nacamar for example. Conversely major FrenchISPs may rely on Opensource, Ebone or other intercontinental backbones, which do not reach allnational ISPs.

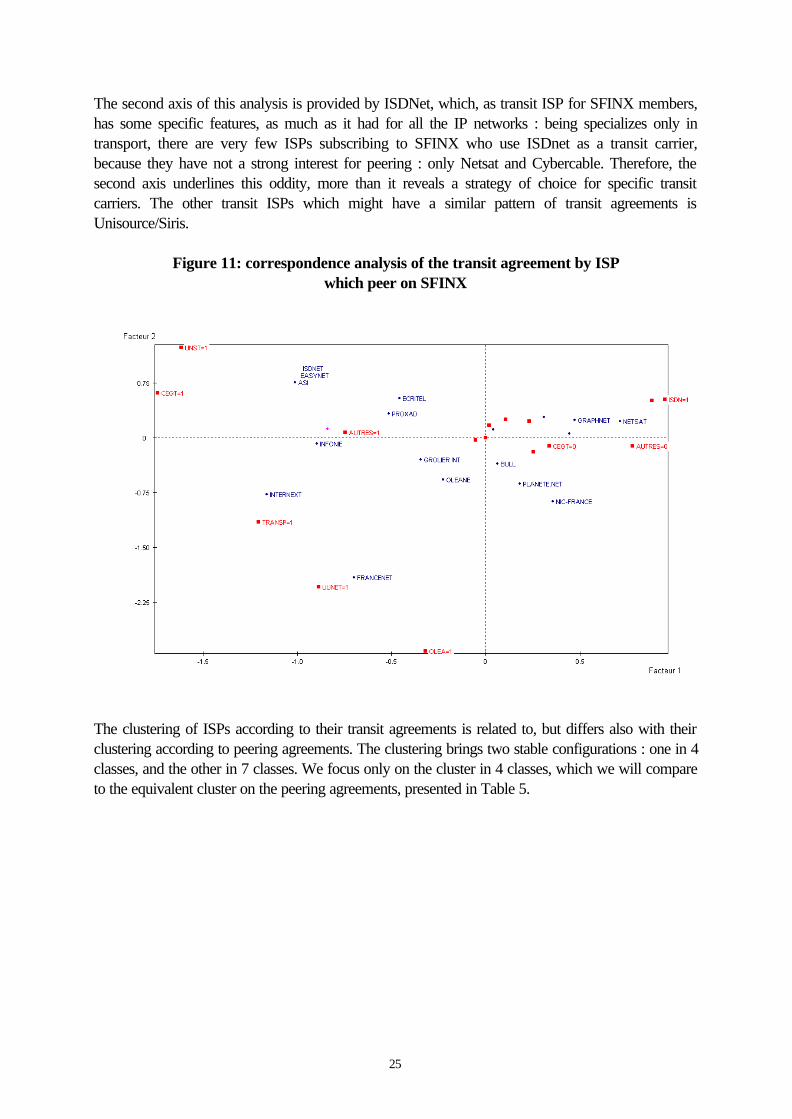

The correspondence analysis run with the transit agreements is quite straightforward, given the lownumber of variables. For example, Cegetel as a transit carrier, has a very specific profile, whichappears on the first axis of figure 11. ISPs who sign an agreement with that transit provider, wouldalso sign with Unisource or ISDNet. The other would prefer Uunet, Oléane or Transpac. Hence, itseems that there are two clubs for transit agreements, agglomerated around two sets of transitcarriers. The first one is built with Cegetel and Unisource as backbones, while the other is built withTranspac, Oléane and Uunet. Our contention, if we follow both our theoretical model and theconclusions of the preceding subsection, is that the first group is made up of « low quality » ISPs,namely ISPs with less connectivity, while those of the second category are those of higher quality.

25

The second axis of this analysis is provided by ISDNet, which, as transit ISP for SFINX members,has some specific features, as much as it had for all the IP networks : being specializes only intransport, there are very few ISPs subscribing to SFINX who use ISDnet as a transit carrier,because they have not a strong interest for peering : only Netsat and Cybercable. Therefore, thesecond axis underlines this oddity, more than it reveals a strategy of choice for specific transitcarriers. The other transit ISPs which might have a similar pattern of transit agreements isUnisource/Siris.

Figure 11: correspondence analysis of the transit agreement by ISPwhich peer on SFINX

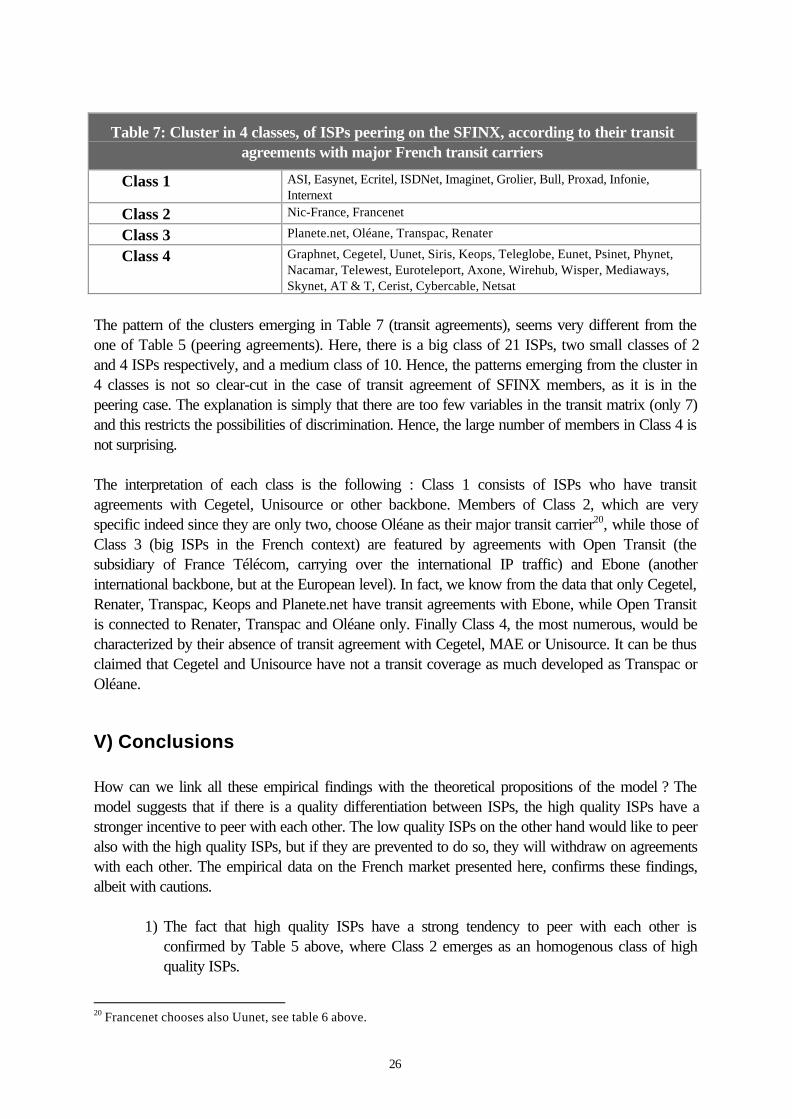

The clustering of ISPs according to their transit agreements is related to, but differs also with theirclustering according to peering agreements. The clustering brings two stable configurations : one in 4classes, and the other in 7 classes. We focus only on the cluster in 4 classes, which we will compareto the equivalent cluster on the peering agreements, presented in Table 5.

26

Table 7: Cluster in 4 classes, of ISPs peering on the SFINX, according to their transitagreements with major French transit carriers

Class 1 ASI, Easynet, Ecritel, ISDNet, Imaginet, Grolier, Bull, Proxad, Infonie,Internext

Class 2 Nic-France, Francenet

Class 3 Planete.net, Oléane, Transpac, Renater

Class 4 Graphnet, Cegetel, Uunet, Siris, Keops, Teleglobe, Eunet, Psinet, Phynet,Nacamar, Telewest, Euroteleport, Axone, Wirehub, Wisper, Mediaways,Skynet, AT & T, Cerist, Cybercable, Netsat

The pattern of the clusters emerging in Table 7 (transit agreements), seems very different from theone of Table 5 (peering agreements). Here, there is a big class of 21 ISPs, two small classes of 2and 4 ISPs respectively, and a medium class of 10. Hence, the patterns emerging from the cluster in4 classes is not so clear-cut in the case of transit agreement of SFINX members, as it is in thepeering case. The explanation is simply that there are too few variables in the transit matrix (only 7)and this restricts the possibilities of discrimination. Hence, the large number of members in Class 4 isnot surprising.

The interpretation of each class is the following : Class 1 consists of ISPs who have transitagreements with Cegetel, Unisource or other backbone. Members of Class 2, which are veryspecific indeed since they are only two, choose Oléane as their major transit carrier20, while those ofClass 3 (big ISPs in the French context) are featured by agreements with Open Transit (thesubsidiary of France Télécom, carrying over the international IP traffic) and Ebone (anotherinternational backbone, but at the European level). In fact, we know from the data that only Cegetel,Renater, Transpac, Keops and Planete.net have transit agreements with Ebone, while Open Transitis connected to Renater, Transpac and Oléane only. Finally Class 4, the most numerous, would becharacterized by their absence of transit agreement with Cegetel, MAE or Unisource. It can be thusclaimed that Cegetel and Unisource have not a transit coverage as much developed as Transpac orOléane.

V) Conclusions

How can we link all these empirical findings with the theoretical propositions of the model ? Themodel suggests that if there is a quality differentiation between ISPs, the high quality ISPs have astronger incentive to peer with each other. The low quality ISPs on the other hand would like to peeralso with the high quality ISPs, but if they are prevented to do so, they will withdraw on agreementswith each other. The empirical data on the French market presented here, confirms these findings,albeit with cautions.

1) The fact that high quality ISPs have a strong tendency to peer with each other isconfirmed by Table 5 above, where Class 2 emerges as an homogenous class of highquality ISPs.

20 Francenet chooses also Uunet, see table 6 above.

27

2) Low quality ISPs will prefer to peer with high quality ISPs, but if this is not possible theywill peer with each other. In the empirical part, we have encountered several times a setof ISPs, that we can consider as « low quality » in the sense that they have limitedcapacities. Their behavior is remarkably homogenous. Among them are Asi, Easynet,Ecritel, Imaginet, Internext, Proxad. They are not well known from the end users, but arestill very active on the Internet. We find them belonging to the same class in table 5(peering agreements) as well as in Table 7 (transit agreements).

3) We have also a cluster of « very low » quality ISPs, at least in the French market. Theseare generally foreign ISPs, which are not looking for a strong connectivity, because theyhave a limited presence on the French market. They peer « on the tiptoes » with FrenchISPs, in order to exchange a traffic to and from France, which is probably a very smallpart of their overall traffic.

Because the market is evolving quickly, and new entry as well as concentration happens quickly allthe empirical conclusions can be considered as provisory. Nonetheless, it appears that the Frenchmarket is a two tiers market, where big ISPs around France Télécom and Uunet, seem to precludeother ISPs to cooperate with them.

28

Bibliography :

Baake, P., T. Wichmann (1998) "On the Economics of Internet Peering", Netnomics.http://www.berlecon.de/tw/peering.pdf.

Bailey, J.P. (1997) "The Economics of Internet Interconnection Agreements", in L. McKnight, J.P.Bailey (Eds.) Internet Economics, Cambridge, MIT Press, 155-168.

Chinoy, B., T. Salao (1996) ``Internet Exchanges : Policy Driven Evolution'', Working Paper.http://ksgwww.harvard.edu/iip/cai/chinsla.htm.

Huston, G. (1999) « Internet, Peering and Settlements», http://www.telstra.net/peerdics/peer.html.

Lebart,L., Morineau, A. & Piron, M., (1996) : Statistique exploratoire multidimensionnelle,Dunod, Paris.

Matutes, C., A Padilla (1994) « Shared ATM networks and banking competition », EuropeanEconomic review 38, 1113-1138.

Mussa M., Rosen S. (1978) « Monopoly and Product Quality », Journal of Economic Theory 18,301-317.

Srinagesh, P. (1997) ``Internet Cost Structures and Interconnection Agreements``, in L. McKnight,J.P. Bailey (Eds.) Internet Economics, Cambridge, MIT Press, 121-154.