Embed Size (px)

Citation preview

Global foreign direct investment: the case of Russia

Laza Kekic - Regional Director, Central and Eastern EuropeEconomist Intelligence Unit

Moscow, July 1st 2003

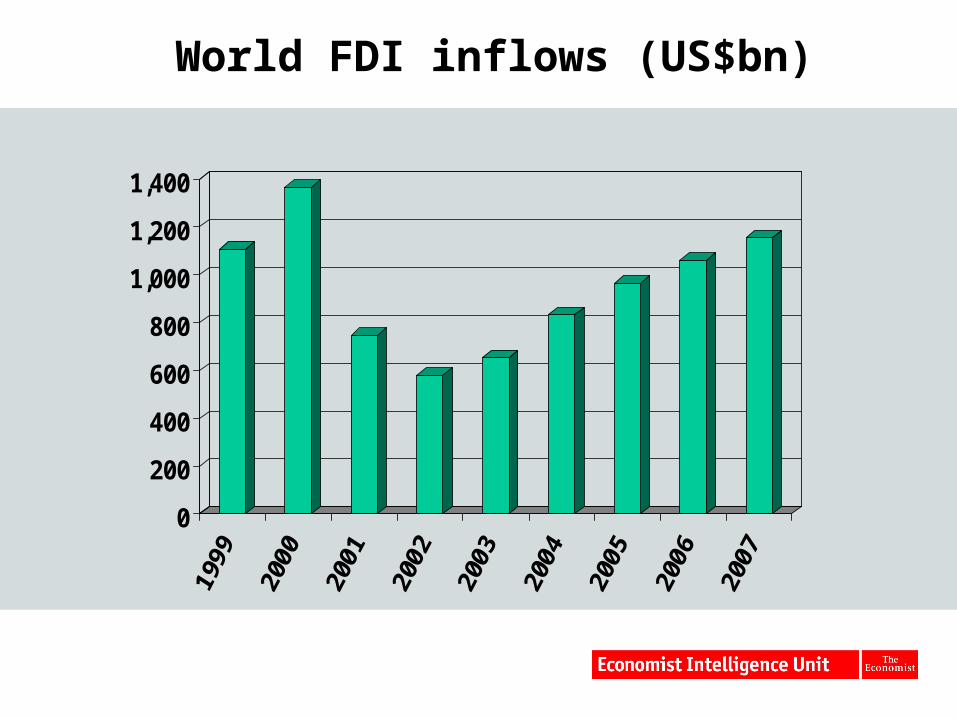

World FDI inflows (US$bn)

0

200

400

600

800

1,000

1,200

1,400

FDI in eastern Europe

FDI into the transition region bucked worldwide trend of stagnant or declining inflows in 2002

Record total of over US$32bn, despite weak OECD growth and difficult financing conditions.

Increased relative attractiveness of the region compared with most other emerging markets;

Further sales of state assets;

Cost-cutting pressures on Western companies

FDI key driver of investment growth, rapid structural change and competitiveness in central

and east European economies

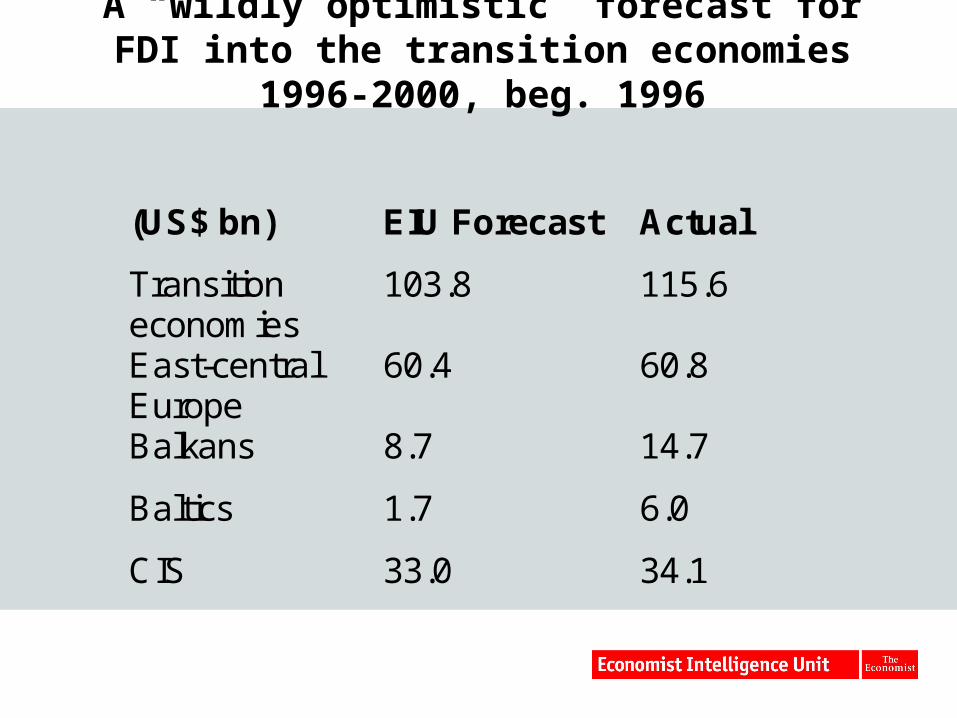

A “wildly optimistic” forecast for FDI into the transition economies 1996-2000, beg. 1996

(US$ bn) EIU Forecast Actual

Transitioneconomies

103.8 115.6

East-centralEurope

60.4 60.8

Balkans 8.7 14.7

Baltics 1.7 6.0

CIS 33.0 34.1

The medium-term future: more of the same

Continued steady increase in inflows Share of Poland, Hungary and Czech Republic in

regional total to decline (to 40% of total) FDI/GDP averages just over 3% of GDP Some CIS energy producers major attraction Catch-up in reforms, performance and FDI by some

previous laggards

FDI inflows into the transition economies (US $m)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1999 2000 2001 2002 2003 2004 2005 2006 2007

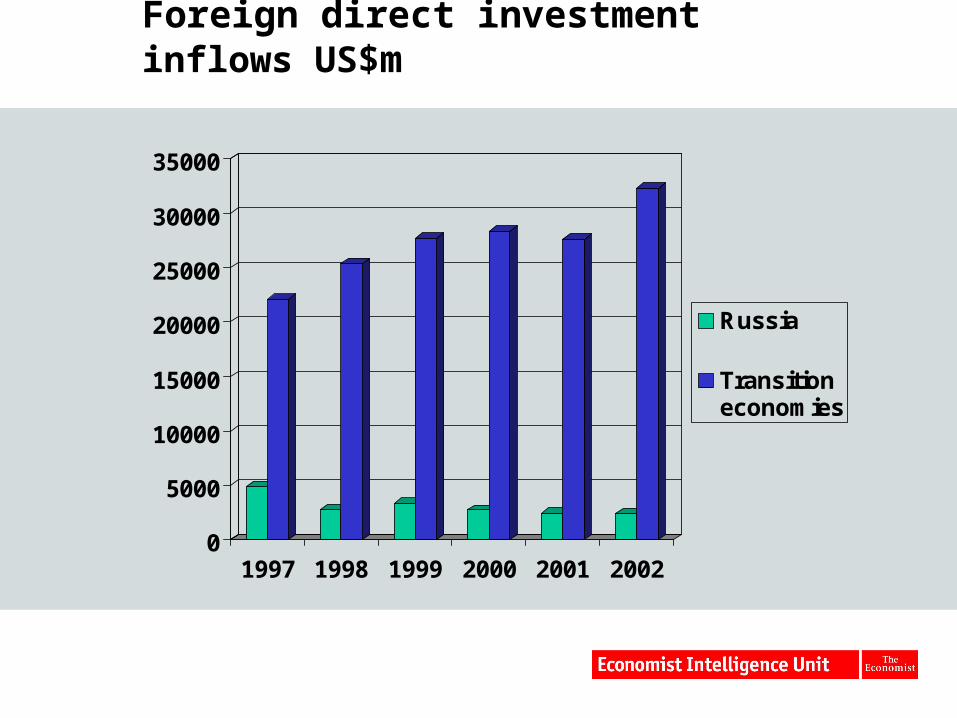

Foreign direct investment inflows US$m

0

5000

10000

15000

20000

25000

30000

35000

1997 1998 1999 2000 2001 2002

Russia

Transitioneconomies

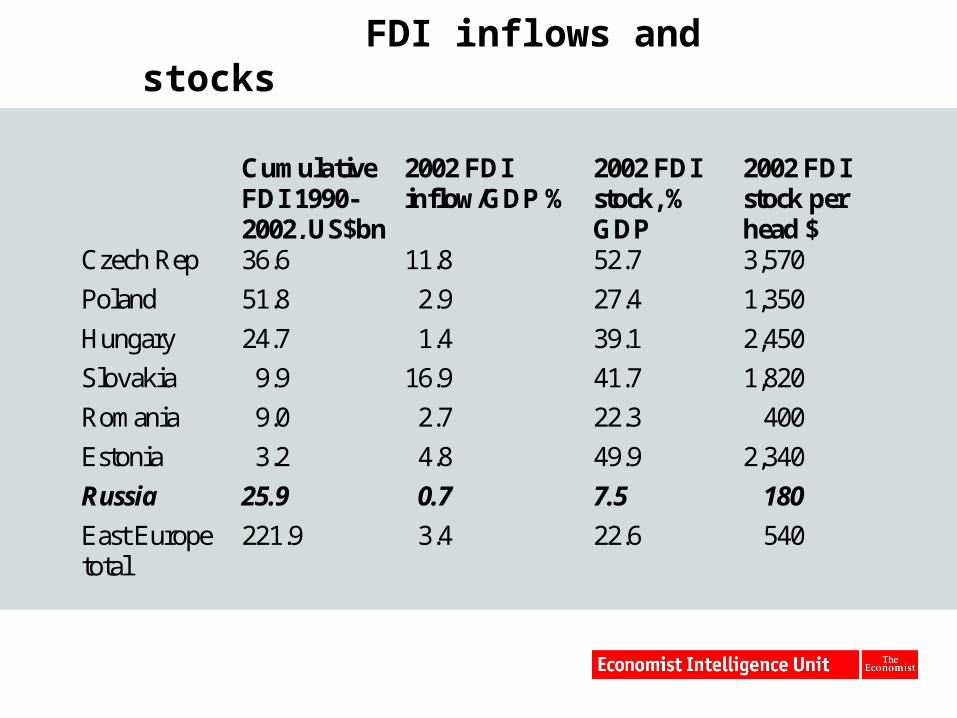

FDI inflows and stocks

CumulativeFDI 1990-2002, US$bn

2002 FDIinflow/GDP %

2002 FDIstock, %GDP

2002 FDIstock perhead $

Czech Rep 36.6 11.8 52.7 3,570

Poland 51.8 2.9 27.4 1,350

Hungary 24.7 1.4 39.1 2,450

Slovakia 9.9 16.9 41.7 1,820

Romania 9.0 2.7 22.3 400

Estonia 3.2 4.8 49.9 2,340

Russia 25.9 0.7 7.5 180

East Europetotal

221.9 3.4 22.6 540

The baseline outlook--getting by

Political stability Putin persists with reforms, although

implementation remains difficult Medium-term external environment is relatively

favourable Macrostability preserved No 2007-08 “succession crisis” Authoritarian trends held in check External debt managed successfully Oil prices remain near US$20 pb

Russia’s long-term growth prospects

Scope for catch-up (+)

Demographics (-)

Skills endowment (mixed)

Geography (-)

Infrastructure (-)

Institutions (-)

Regulation (?)

Macro policies (+)

Max 3.5% growth (if no “Dutch disease”)

0

20

40

60

80

100

120

1989

1991

1993

1995

1997

1999

2001

Real GDP (1989=100)

Russia

Transitionregion

Central Europe

Catch-up prospects

Russia GDP per head (at PPP), 2002: US$7,590

Index, EU-15=100: 29.2

Index, US=100: 20.8

Best-case scenario:

Russia’s catch-up time with long-term growth of GDP per head of 3.5% per year (assumes EU and US growth at 2% per year):

with EU average: 85 years

with US: 108 years

The baseline outlook and growth

Not enough for sustained, very fast growth Long-term growth determinants--Russia has

too many minuses Domestic underpinnings for sustained fast

growth are weak

Hypothesis:

Russia needs massive infusion of foreign capital, technology and management practices to try to break long-term growth bind

Main determinants of FDI

Market size GDP Expected market growth Natural resources endowment Labour costs Distances/proximity to markets Agglomeration effects (FDI clusters) Overall business environment Policy towards FDI Exchange rate variability Regional integration

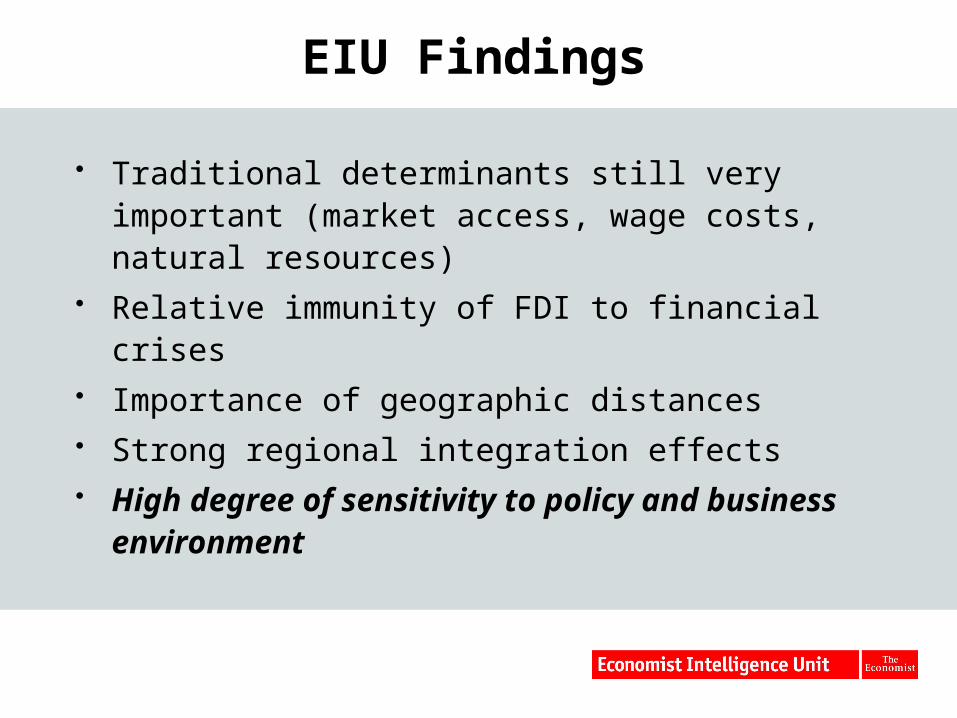

EIU Findings

Traditional determinants still very important (market access, wage costs, natural resources)

Relative immunity of FDI to financial crises Importance of geographic distances Strong regional integration effects High degree of sensitivity to policy and business

environment

EIU business environment rankings model

Model measures the quality or attractiveness of the business environment and its key components

Opportunities for and hindrances to business in 60 countries (over 95% of global FDI and GDP)

Ranking of a country’s overall position and ten categories The model uses quantitative data and forecasts, business

surveys and expert assessment Main criteria used by companies to formulate their global

business strategies and investment location decisions The overall scores (on a 1-10 scale) and rankings are based

on the scores for 70 indicators

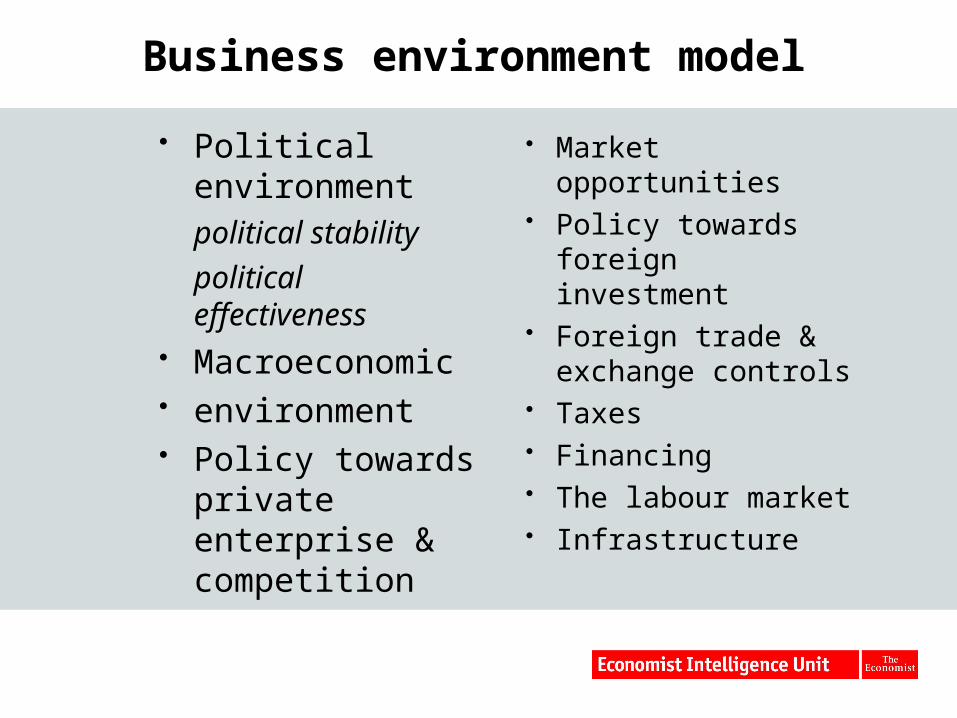

Business environment model

Political environmentpolitical stability

political effectiveness

Macroeconomic environment Policy towards

private enterprise & competition

Market opportunities

Policy towards foreign investment

Foreign trade & exchange controls

Taxes Financing The labour market Infrastructure

Business environment scores and ranks

1998-2002score(out of 10)

Globalrank(out of 60)

2003-2007score(out of 10)

Globalrank(out of 60)

US 8.62 1 8.47 5

…….. ……. …… ….. ….

Hungary 6.69 26 7.12 28

Poland 6.37 32 7.07 29

…….. ……. ……. ……. ……

Russia 4.61 53 5.86 46

….. …… …… …… ……

Nigeria 3.88 59 4.51 60

Russia’s business environment

1998-2002 2003-07 1998-2002 2003-07

Value of index(out of 10)

Value of index(out of 10)

Global rank(out of 60)

Global rank(out of 60)

Overall position 4.61 5.86 53 46

Political environment 3.0 4.3 58 50

Macroeconomicenvironment

4.8 7.3 57 45

Market opportunities 7.2 7.7 12 5

Policy towards privateenterprise

3.3 4.9 55 49

Policy towards FDI 3.3 4.4 59 58

Foreign trade regime 6.1 7.2 41 44

Taxes 4.0 5.5 55 46Financing 3.6 5.1 52 46

The labour market 6.6 7.2 17 12Infrastructure 4.2 5.1 41 40

Russia’s business environment

Comparative strengths Labour market Market opportunities

Comparative weaknesses Institutional ineffectiveness

(bureaucracy, corruption, rule of law) Infrastructure Overall policy towards private enterprise Financial sector

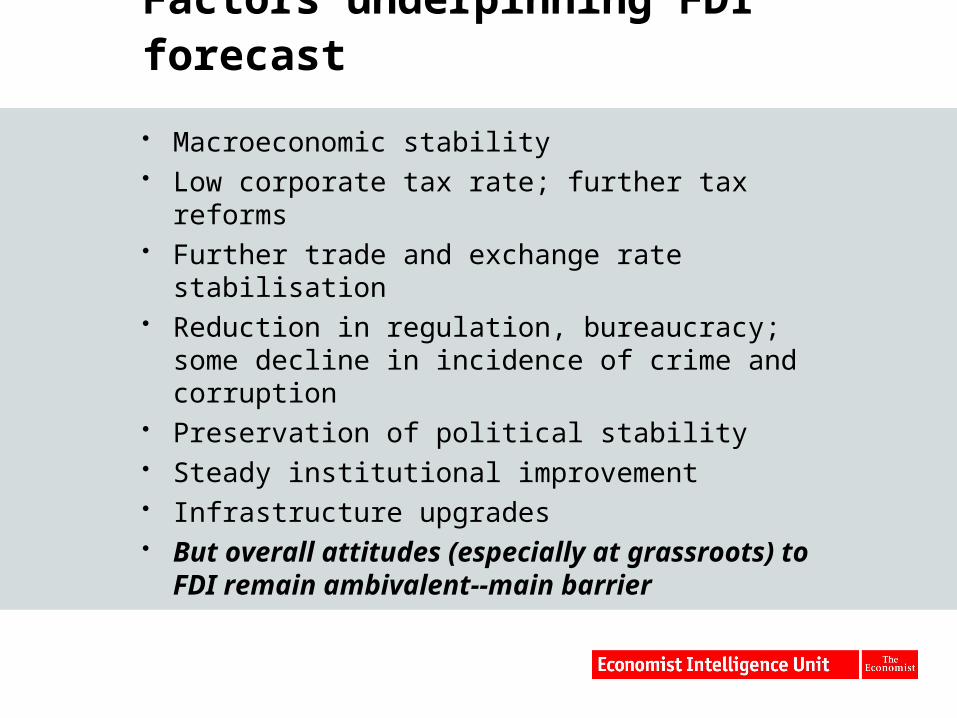

Factors underpinning FDI forecast

Macroeconomic stability Low corporate tax rate; further tax reforms Further trade and exchange rate stabilisation Reduction in regulation, bureaucracy; some

decline in incidence of crime and corruption Preservation of political stability Steady institutional improvement Infrastructure upgrades But overall attitudes (especially at

grassroots) to FDI remain ambivalent--main barrier

Medium-term FDI projection

Expected improvement in overall business environment

with:

Improvement in most areas of the business environment

Maintenance of competitive labour costs

Consistent with average FDI inflow of up to US$10bn per year in 2003-07; about 2% of GDP--but still well below potential and requirements

Some issues for discussion

Could future FDI into Russia be even stronger?

How sensitive to Russo-Western political relations?

FDI and EU membership - how high are the costs of exclusion?

How much does eastern Europe feature in MNE global strategies?

Choosing a regional destination - safe versus risky strategies

![Reforms and growth in transition [EBRD - Working papers] · 2011. 2. 16. · Libor Krkoska and Utku Teksoz, and to Laza Kekic, Colin Lawson, Martin Raiser, Karsten Staehr, Haifeng](https://img.pdfslide.net/doc/110x75/5fe3ecca2c3af44122244b04/reforms-and-growth-in-transition-ebrd-working-papers-2011-2-16-libor-krkoska.jpg)