Embed Size (px)

Citation preview

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 1/19

Global Securities Pakistan Ltd. │ 9th Floor Muhammadi House │ I.I. Chundrigar Road │ Karachi │ Pakistan

www.gslpk.com

Pakistan Equity Research

Initiating Coverage

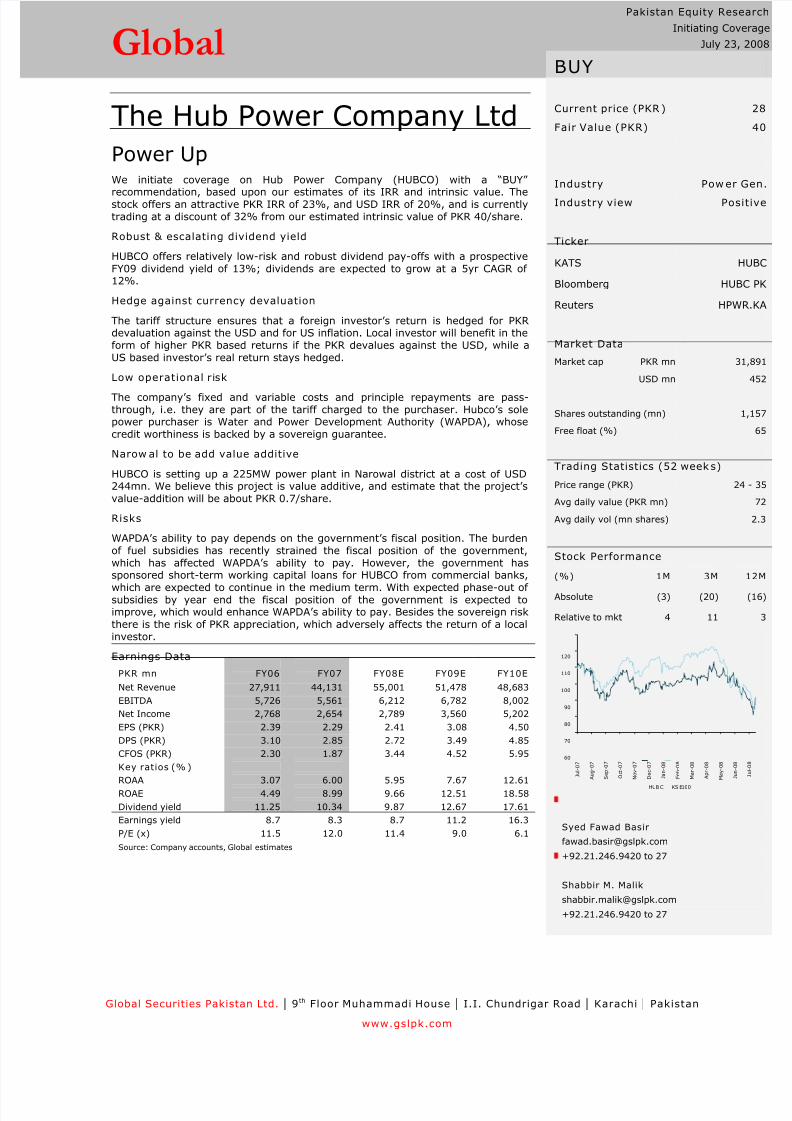

July 23, 2008GlobalBUY

Current price (PKR) 28

Fair Value (PKR) 40

Industry Pow er Gen.Industry view Positive

Ticker

KATS HUBC

Bloomberg HUBC PK

Reuters HPWR.KA

Market Data

Market cap PKR mn 31,891

USD mn 452

Shares outstanding (mn) 1,157

Free float (%) 65

Trading Statistics (52 weeks)

Price range (PKR) 24 - 35

Avg daily value (PKR mn) 72

Avg daily vol (mn shares) 2.3

Stock Performance

(%) 1M 3M 12M

Absolute (3) (20) (16)

Relative to mkt 4 11 3

60

70

80

90

100

110

120

J u l - 0 7

A u g - 0 7

S e p - 0 7

O c t - 0 7

N o v - 0 7

D e c - 0 7

J a n - 0 8

F e b - 0 8

M a r - 0 8

A p r - 0 8

M a y - 0 8

J u n - 0 8

J u l - 0 8

HUB C KS E100

Syed Fawad Basir

+92.21.246.9420 to 27

Shabbir M. Malik

+92.21.246.9420 to 27

The Hub Power Company Ltd

Power UpWe initiate coverage on Hub Power Company (HUBCO) with a “BUY”

recommendation, based upon our estimates of its IRR and intrinsic value. Thestock offers an attractive PKR IRR of 23%, and USD IRR of 20%, and is currently

trading at a discount of 32% from our estimated intrinsic value of PKR 40/share.

Robust & escalating dividend yield

HUBCO offers relatively low-risk and robust dividend pay-offs with a prospective

FY09 dividend yield of 13%; dividends are expected to grow at a 5yr CAGR of 12%.

Hedge against currency devaluation

The tariff structure ensures that a foreign investor’s return is hedged for PKRdevaluation against the USD and for US inflation. Local investor will benefit in the

form of higher PKR based returns if the PKR devalues against the USD, while a

US based investor’s real return stays hedged.

Low operational risk

The company’s fixed and variable costs and principle repayments are pass-

through, i.e. they are part of the tariff charged to the purchaser. Hubco’s solepower purchaser is Water and Power Development Authority (WAPDA), whose

credit worthiness is backed by a sovereign guarantee.

Narow al to be add value additive

HUBCO is setting up a 225MW power plant in Narowal district at a cost of USD244mn. We believe this project is value additive, and estimate that the project’s

value-addition will be about PKR 0.7/share.

Risks

WAPDA’s ability to pay depends on the government’s fiscal position. The burden

of fuel subsidies has recently strained the fiscal position of the government,

which has affected WAPDA’s ability to pay. However, the government hassponsored short-term working capital loans for HUBCO from commercial banks,

which are expected to continue in the medium term. With expected phase-out of

subsidies by year end the fiscal position of the government is expected toimprove, which would enhance WAPDA’s ability to pay. Besides the sovereign risk

there is the risk of PKR appreciation, which adversely affects the return of a local

investor.

Earnings Data

PKR mn FY06 FY07 FY08E FY09E FY10E

Net Revenue 27,911 44,131 55,001 51,478 48,683

EBITDA 5,726 5,561 6,212 6,782 8,002

Net Income 2,768 2,654 2,789 3,560 5,202

EPS (PKR) 2.39 2.29 2.41 3.08 4.50

DPS (PKR) 3.10 2.85 2.72 3.49 4.85

CFOS (PKR) 2.30 1.87 3.44 4.52 5.95

Key ratios (% )

ROAA 3.07 6.00 5.95 7.67 12.61

ROAE 4.49 8.99 9.66 12.51 18.58

Dividend yield 11.25 10.34 9.87 12.67 17.61

Earnings yield 8.7 8.3 8.7 11.2 16.3

P/E (x) 11.5 12.0 11.4 9.0 6.1

Source: Company accounts, Global estimates

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 2/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 1

This page has been left blank

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 3/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 2

Table of Contents

Investment case ........................................................................................ 4 Valuation snapshot .................................................................................. 5 Risk factors ............................................................................................ 6 Structure................................................................................................7 Industry overview ................................................................................... 9 Company overview ................................................................................ 13 Narowal project..................................................................................... 13 Financial Statements.............................................................................. 14

Glossary.................................................................................................. 16

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 4/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 3

This page has been left blank

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 5/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 4

Investment case

Dividend yield

HUBCO is expected to shine in an unfavorable macro-economic environment,courtesy of its Power Purchase Agreement (PPA) with WAPDA as per which the

investor receives relatively low-risk payoffs. Dividend yield for FY08 is expected

to be 13% and is projected to grow at a 5yr CAGR of 12%, primarily due to ascalable trend in its agreed tariff with WAPDA and devaluation of the PKR.

Enticing I RR

At current price the stock offers an attractive USD IRR of 20% and a PKR IRR of

23%. Our estimated PKR required rate of return, based on CAPM, is 16.7%.

Low operational risk

The company’s variable and fixed costs and loan repayments are pass-through

items, i.e. HUBCO charges WAPDA for them in its tariff. Variable costs includethe cost of fuel used in power generation, while fixed costs include operating and

maintenance cost, interest expense and insurance. HUBCO’s margins are not

vulnerable to volatility in oil prices, since its fuel bill is a pass-through item andpaid for by WAPDA.

Tariff hedged for PKR devaluation and US inflation

The tariff is indexed with the PKR/USD exchange rate and offers a pre-

determined real USD return. Local investor gains in the form of higher PKRdividends if the PKR devalues against the USD, while a US based investor’s

return is hedged for exchange rate movements and US inflation.

No taxes

HUBCO does not pay any corporate tax, as it enjoys a tax holiday for theduration of the PPA, expiring in CY27.

New project to be value additive

The company is setting up a new 225MW power project in Narrowal which would

be value additive based on our analysis. The project offers a real USD IRR of

15% and is expected to add PKR 0.70/share to the intrinsic value of HUBCO’sexisting project.

Figure 1: Expected DPS and Dividend Y ield FY08-27

-

5

10

15

20

25

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

F Y 1 2

F Y 1 3

F Y 1 4

F Y 1 5

F Y 1 6

F Y 1 7

F Y 1 8

F Y 1 9

F Y 2 0

F Y 2 1

F Y 2 2

F Y 2 3

F Y 2 4

F Y 2 5

F Y 2 6

F Y 2 7

-

10

20

30

40

50

60

70

80

90

100

DPS (LHS) Dividend y ie ld (RHS)

PKR/share %

Source: Global Estimates

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 6/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 5

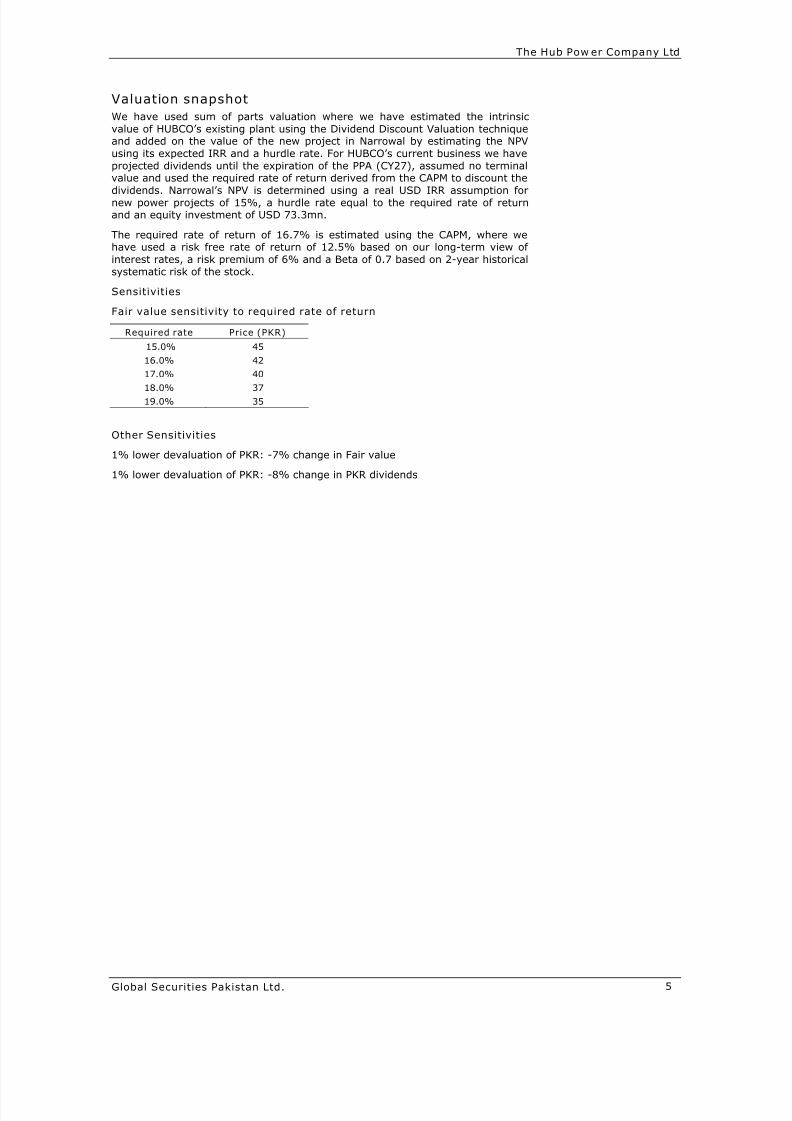

Valuation snapshot

We have used sum of parts valuation where we have estimated the intrinsic

value of HUBCO’s existing plant using the Dividend Discount Valuation techniqueand added on the value of the new project in Narrowal by estimating the NPV

using its expected IRR and a hurdle rate. For HUBCO’s current business we have

projected dividends until the expiration of the PPA (CY27), assumed no terminalvalue and used the required rate of return derived from the CAPM to discount the

dividends. Narrowal’s NPV is determined using a real USD IRR assumption fornew power projects of 15%, a hurdle rate equal to the required rate of returnand an equity investment of USD 73.3mn.

The required rate of return of 16.7% is estimated using the CAPM, where wehave used a risk free rate of return of 12.5% based on our long-term view of

interest rates, a risk premium of 6% and a Beta of 0.7 based on 2-year historical

systematic risk of the stock.

Sensitivities

Fair value sensitivity to required rate of return

Other Sensitivities

1% lower devaluation of PKR: -7% change in Fair value

1% lower devaluation of PKR: -8% change in PKR dividends

Required rate Price (PKR)

15.0% 45

16.0% 42

17.0% 4018.0% 37

19.0% 35

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 7/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 6

Risk factors

WAP DA’s financial position

WAPDA is HUBCO’s sole customer; the payments made by WAPDA besides

compensating for non-fuel costs are used to make payments to Pakistan State

Oil (PSO) for the supply of furnace oil used to run the plant. Due to financial

strains in WAPDA and limited fiscal space of the government, payments to bemade to HUBCO have been delayed and as a result HUBCO has had to borrow

money from banks to maintain fuel supply. These loans are effectively owed bythe government, but are booked on HUBCO’s balance sheet. Principal

repayments and interest expense of these working capital loans are pass through

items and should neither affect the profitability of the company, nor, in ouropinion, its dividend pay-out.

Appreciation in PKR

This is a tangible risk for local investors since HUBCO’s dividends are based on

real USD return, which in PKR terms fluctuate with the exchange rate. The trendin the economy’s trade deficit however suggests that a PKR appreciation is

unlikely in the near-term.

Key Assumptions

ProjectionsUS inflation: 2.60%

PKR devaluation against the USD: 2.20%

Discount Rate

Risk Free Rate: 12.5%

Market Risk Premium: 6%

Beta: 0.7

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 8/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 7

Structure

HUBCO’s bond like characteristics

To understand HUBCO’s pay-offs consider a 30 year semi-annual amortizing

bond maturing in FY27. The repayment structure of the bond is such that the

bulk of the principal re-payments are towards the back-end of the loan term. The

bond holder essentially gets a half-yearly interest income and a partial re-payment of the principal; as the bond nears maturity the principal repayment

increases. Like all bonds the inherent risk of the instrument is lower than equity,because 1) the payments and their schedule are pre-determined and 2) the

amount borrowed is protected by collateral or a sovereign guarantee. As per the

PPA, HUBCO’s equity holder is entitled to pre-determined dividends composed of invested capital and a return on capital whose payment is guaranteed by the

government.

Like any bond HUBCO is not risk free. Return on capital invested can vary

depending on variances between actual expenses incurred in operation and

planned expenses agreed upon by HUBCO’s shareholders and WAPDA in the PPA.In addition PKR based returns may vary depending on the exchange rate of USD

vs. PKR. Although unlikely, the government may back down from its sovereign

guarantee if it is faced with a fiscal crunch.

Tariff compositionAs per the PPA, Hub Power’s tariff is composed of Energy Purchase Price (EPP)

and Capacity Purchase Price (CPP).

Figure 2: HUBCO’S Incom e Statement

EP P: Fuel Cost + Variable Cost

CPP: Fixed Cost + Project Company Equity+Revenue

Principle Repayments +Interest Expense

-

Operating Costs Fuel Cost+ Variable Cost+ Fixed Cost

=

Operating Profit PCE + Principle Repayment + Interest Expense

+

Other Income Interest Income (I)

=

EBITDA PCE + Principle Repayments + I + Interest Exp

-

Non Cash Charges Depreciation + Amortization (D)

-

EBIT PCE + Principle repayment-D + I + Int. Exp.

-

Financial charges Interest expense

-

PAT PCE + Principle repayment-D+I

Source: Global analysis

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 9/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 8

EP P

The EPP incorporates two elements of the cost structure which are fuel cost and

the variable operating and maintaining costs. Fuel cost is linked to the capacity

utilization and the market price of furnace oil. Variable operating andmaintenance costs, within a prescribed limit agreed in the PPA, are pass through

costs.

CPPCPP is composed of a scalable component and a non-scalable component. The

company’s fixed costs excluding depreciation are in the scalable portion of theCPP. They are scalable because they are indexed for PKR devaluation and US

inflation. The CPP section also includes the Project Company Equity (PCE) which

is the return the investors get on the project as per PPA. PCE is escalated in sync

with US inflation and the Pak rupee devaluation. Interest expense and principalrepayments against outstanding loan make up the non-scalable component of

CPP.

PPA

The agreement with WAPDA determines the principles under which the plant is

operated and the tariff arrangements. Under the agreement WAPDA may instruct

HUBCO to generate and deliver electricity into the Grid up to the available NetCapacity of the plant. Tariff payments will be made by WAPDA whether or not

the power is dispatched, provided that it is available for dispatch. If HUBCO failsto meet WAPDA’s generation demands, it will incur penalties payable to WAPDA.

Bonuses are paid by WAPDA for generation in excess of 65% capacity utilization

of the plant.

Figure 4: CPP

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY07 FY08 FY09 FY10 FY11

Escalable Non-Escalable

PKR mn

Source: Global analysis

Figure 3: EPP

37,025

46,935

42,595

38,457 37,601

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

FY07 FY08 FY09 FY10 FY11

PKR mn

Source: Global analysis

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 10/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 9

Industry overview

Pow er demand

Demand for electricity consumption in Pakistan has been growing at an averagerate of 9.5% over the past four years. The rise in demand for power in recent

years came on the back of higher GDP growth (5 yr CAGR of 7%), increasing

rural electrification, commercialization and industrialization. Pakistan has a totalinstalled electricity generation capacity of 19,566 MW, which produced more than

93,621 GWh of electricity in FY08. Currently, there is a peak time power shortfall

of 4,000 MW and the government plans to alleviate the deficit by encouragingprivate investment in the sector, which would add about 2,200 MW over the next

year.

Pow er supply

The current installed capacity is 19,566MW which is theoretically enough to meet

peak load demand. However, due to inadequate fuel supplies thermal plants,which account for 65% of the country’s total generation capacity, are not able to

generate at optimum utilization level. As a result in May’08 the power deficit

reached a peak of 4,000MW. The government has planned extra efforts in FY09to ensure adequate fuel supply for power plants so that the utilization and load

factors can improve. Further, in order to meet the growing demand more power

plants are being encouraged to increase capacity and to reduce the power deficit.The government is actively pursuing new investments in all types of plants, be it

thermal or hydro. It held bidding for setting up six independent power projects to

generate 2,200MW electricity on a fast track basis by Apr09. In addition it has

allocated PKR 76.2bn for investment in the power sector in FY09.

Figure 5: Demand-Supply FY08-12 Figure 6: Planned additions

-

5,000

10,000

15,000

20,000

25,000

FY08 FY09 FY10 FY11 FY12

Demand Supply

MW

Hydel 3%

IPP 40%

Thermal 57%

Hydel Thermal IPP's Source: Economic Survey FY08 Source: Economic Survey FY08

Figure 7: Pow er Generation Plan Figure 8: Installed Capacity

-

10,000

20,000

30,000

40,000

50,000

60,000

FY08 FY10 FY15 FY20 FY25 FY30

Nuclear Hydel Coal Renewable Oil Gas

MW

-

2,000

4,000

6,000

8,000

10,000

12,000

WAPDA IPP's Nuclear KESC

FY07 FY08

MW

Source: Economic Survey FY08 Source: Economic Survey FY08

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 11/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 10

Thermal Pow er

WAPDA operates the majority of thermal power plants in Pakistan, with over

5,000 MW of installed capacity in its control. The Guddu plant is the largest plant

operated by WAPDA, with a capacity of 1,650 MW. In recent years, growth inPakistan’s thermal power generation has come primarily from new Independent

Power Producers (IPPs), some of which have been funded by foreign investors.

The two largest IPP’s in Pakistan are Kot Addu Power Company (1,600MW) and

HUBCO (1,200MW). The government policy is currently focused on setting upthermal power plants (both oil & gas): 90% of foreign investment in the power

sector is directed towards thermal power. Thermal power plants are relativelycheap to install and have a short set-up time compared to hydro power units,

which is why the government is favoring them to overcome the current power

crisis. Thermal plants have high operating costs since they rely on expensive fuel

such as furnace oil, coal and natural gas.

Hydro Pow er

Hydro power plants involve huge capital outlays and take longer to set-up

compared to thermal plants. They have, however, one of the lowest operating

costs which translate into cheaper power and lower stress on the trade balance.The prospects of installation of Hydro projects continue to be marginalized due to

the incessant political disagreement on the setup of such projects.

Hydroelectric power represents a third of Pakistan’s power source and has a

potential of approximately 41,722 MW, most of which lies in the North WestFrontier Province, Northern Areas, Azad Jammu and Kashmir and Punjab. WAPDA

controls the country’s major hydroelectric plants, the largest being the Tarbela

plant with an installed capacity of 3,046MW. Additional hydroelectric plants inoperation include Mangla with 1,000MW, Warsak 240MW and Chashma 184MW.

Although Pakistan has plans to develop additional hydroelectric generating

capacity, infrastructure constraints such as access roads in mountainous regionsand resettlement costs of affected populations have stalled the progress. In spite

of constraints Eden Enterprises is going ahead with its Suki Kinari 655MW

hydropower project. Construction is expected to begin in 2009, with the plantcoming online in 2011. The importance of this project is great as it is expected to

provide several hundred MW of additional hydroelectric power capacity to the

national grid. Apart from this the Private Power and Infrastructure Board (PPIB)is currently reviewing six additional hydropower projects for the Swat River.

Figure 9: Existing Thermal Capacity vs Expected Capacity by Jun’14

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Existing Capacity Expected Capacity

MW

Source: WAPDA

Figure 10: Installed vs P otential Hydel Capacity

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

NWFP Punjab AJK Northern Areas

Installed Potential

MW

Source: PPIB

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 12/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 11

Alternative pow er sources

Pakistan possesses immense potential to harness solar and wind energy. The

Government of Pakistan is now emphasizing on the acquisition of power through

alternate energy resources and is planning to add 500 MW in the next 5 yearsthrough alternate sources. Feasibility studies are also under way for producing of

over 1,000 MW of energy through the use of solid waste and coal. Government

of Pakistan is putting greater emphasis on Renewable Energy and has set a

target of 2,700MW or 10% of the energy mix from renewable energy by 2015.

Wind energy

The potential of power generation through wind should not be underestimated in

spite of having considerable start up cost. Planet Energy Ltd has signed a MoUwith Gold-wind Science and Technology for purchase of wind turbines for its

planned 50MW wind farm with the option of increasing it to 150MW.

Nuclear

Pakistan has a small nuclear power program, with 425 MW capacity, but plans to

increase this substantially. In Pakistan, nuclear power makes a small contributionto total energy production and requirements, supplying only 2.4% of the

country's electricity. In 2005 an Energy Security Plan was adopted by the

government, calling for a huge increase in generating capacity by 2030. Itincludes plans for lifting nuclear capacity by 8,800MW, of which 900MW will be

added by 2015 and a further 1,500MW by 2020.

Figure 11: Nuclear Generation

0

50

100

150

200

250

300

350

Kanupp Chasnupp-1 Chasnupp-2*

MWe

Source: PNRA, *Expected to come online in Feb10

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 13/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 12

WAPDA

WAPDA is the cornerstone of Pakistan’s power sector. Since its establishment in

1958, the company has implemented a number of major infrastructure projectsfor the generation, transmission and distribution of Pakistan’s electricity supply.

Today, it employs 137,000 people, has a customer base of over 10 million, and is

at the center of the restructuring of Pakistan’s power sector. To streamlineoperations the state-owned giant has been divided into 14 new companies. An

experienced private sector management has been put in place to enhanceoperational efficiencies and improve its financial position.

The new streamlined organization is comprised of nine distribution companies,four generation companies, and a national transmission and dispatch company

that buys and sells electricity from generators to suppliers. With the company’s

successful restructuring under its belt, the government is now moving forwardwith its privatization plans.

NEPRA

NEPRA has been created to introduce transparent and judicious economic

regulation, based on sound commercial principals, to the electric power sector of Pakistan. NEPRA's main responsibilities are to:

• Issue Licenses for generation, transmission and distribution of electric

power • Establish and enforce Standards to ensure quality and safety of

operation and supply of electric power to consumers

• Approve investment and power acquisition programs of the utility

companies

• Determine Tariffs for generation, transmission and distribution of electric power

NEPRA regulates the electric power sector to promote a competitive structure forthe industry and to ensure the coordinated, reliable and adequate supply of

electric power in the future. By law, NEPRA is mandated to ensure that the

interests of the investor and the customer are protected through judicious

decisions based on transparent commercial principals and that the sector moves

towards a competitive environment.

Figure 12: WAPDA Electricity Generation

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY07 FY08

Hydro Thermal

GWh

Source: Pepco

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 14/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 13

Company overview

The development of the Hub Power Project began when the Government

requested sponsors led by Xenel Industries of Saudi Arabia to present proposalsfor a 1,292 MW plant.

In 1991, HUBCO was incorporated in Pakistan as a limited liability company for

the purpose of implementing the project. During the three years that followed, a

series of agreements were negotiated between HUBCO and the Government of Pakistan and certain of its institutions, the construction consortium and NationalPower. It was on the basis of these agreements that long-term finance was

raised without direct guarantees from the Government.

Debt syndication was completed during the last quarter of 1994 and by the end

of the year, the full financing, including equity was in place. This was the singlelargest issue of domestic shares at one time. Financial closure was finally

achieved in Jan95.

Plant details

HUBCO consists of four generating units each rated at 323MW gross output, withan oil-fired single re-heat boiler, two cylinder condensing steam turbines directly

coupled to a hydrogen cooled generator. The design net available output is

exported to WAPDA's national grid via the power station's 500kv switchyard.Both the plant configuration and the steam conditions represent conventional

design based on proven technology. HUBCO is one of the most efficient oil fired

thermal plant in Pakistan and can provide 8% of country's electricity demand.The plant is operated in such a way that it is available at a short notice during

high demand period and can switch to flexible operations during low demand

periods. Hubco holds 21% of the total installed capacity of IPP’s.

Narowal project

The Hub Power Company Limited is setting up a combined cycle power plantbased on reciprocating engines technology with a total project cost of

USD 244.3mn and having an installed capacity of 225MW at Narowal district,

Punjab. The government has approved formal request and the tariff structurehas also been agreed upon with NEPRA. The plant will be powered by 11, 18

cylinder V-configuration four stroke engines which will run on Residual Fuel Oil.

The plant is expected to contribute to the national grid by the end of Mar10.

The project cost will be financed by 30% equity which comes to USD 73.3mn and70% debt worth USD 171mn. The plant will have the ability to run on High speed

diesel oil as an alternative fuel source. 100% generation from the plant would be

supplied to the National Transmission and Dispatch Company Ltd (NTDC).

Figure 13: HUBCO’s Shareholding Pattern Figure14: Planned Additions

AICL

1%

MCB Bank Ltd

5%

Fauji

Foundation18%

NBP

3%

Mitsui &

Company

4%

HBL Treasury

3%

State Life

Insurance3%

Xenel

Industries Ltd

26%

National Power

Intl37%

Others

79%

Hubco

21%

Others Hubco Source: Company accounts Source: PPIB

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 15/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 14

Financial Statements

Income Statement

PKR mn FY06 FY07 FY08E FY09E FY10E

Net Sales 27,911 44,131 55,001 51,478 48,683

Operating costsFuel Cost 20,238 36,259 46,487 42,100 37,940

0&M cost 1,253 1,688 1,651 1,877 1,982

Insurance 413 369 367 400 400

Gen & Admin 281 253 284 319 359

Sub Total 22,185 38,570 48,789 44,697 40,681

EBITDA 5,726 5,561 6,212 6,782 8,002

Depreciation & Amortization 1,649 1,650 1,653 1,662 1,672

EBIT 4,078 3,911 4,560 5,119 6,330

Financing cost 1,577 1,417 1,889 1,603 1,189

Other income 268 161 118 44 61

EBT 2,768 2,654 2,789 3,560 5,202

Taxation - - - - -

Recurring Net Profit 2,768 2,654 2,789 3,560 5,202

Extraordinary Items - - - - -Net Profit 2,768 2,654 2,789 3,560 5,202

Source: Company accounts, Global estimates

Balance Sheet

PKR mn FY06 FY07 FY08E FY09E FY10E

Current Assets

Inventory of fuel oil 1,891 2,564 1,479 1,263 1,138

Trade debts 2,938 7,937 15,000 12,000 8,000

Advances and prepayments 1,401 1,269 873 774 733

Cash and bank balances 3,363 743 350 438 567

Sub Total 9,594 12,513 17,703 14,475 10,438

Non Current assets

PPE 33,319 31,857 30,393 28,948 27,498

Intangibles 5 5 5 6 6

Stores and spares 592 613 691 598 544

Long term deposits 4 6 - - -

Sub Total 33,921 32,481 31,089 29,552 28,049

Total assets 43,515 44,994 48,792 44,026 38,486

Liabilities

Non current

Long term loans 9,250 8,271 7,303 6,329 5,355

Deferred liability-gratuity 15 18 - - -

Sub Total 9,265 8,290 7,303 6,329 5,355

Current liabilities

Current maturity long term loan 979 979 974 974 974

Short term loan - 2,090 6,500 4,000 400

Trade and other payables 2,591 3,938 4,378 3,788 3,448

Interest on long term loans 695 645 943 723 511

Sub Total 4,265 7,652 12,796 9,485 5,333

Total Liabilities 13,530 15,941 20,098 15,814 10,689

Share Capital and reserve

Issued subscribed and paid-up 11,572 11,572 11,572 11,572 11,572

Un-appropriated profit 18,414 17,481 17,122 16,641 16,226

Total equity 29,985 29,052 28,694 28,212 27,797

Total equity and liabilities 43,515 44,994 48,792 44,026 38,486

Source: Company accounts, Global estimates

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 16/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 15

Cash Flow Statement

PKR mn FY06 FY07 FY08E FY09E FY10E

PAT 2,768 2,654 2,789 3,560 5,202

Depreciation & Amortization 1,659 1,663 1,653 1,662 1,672

Change in current assets (1,310) (5,539) (5,582) 3,315 4,166Change in current liabilities (455) 3,390 5,125 (3,311) (4,152)

Cash from operations 2,663 2,168 3,985 5,227 6,889

CAPEX (44) (199) (190) (218) (223)

Stores & spares (30) (20) (78) 93 54

Change in long term deposits 158 (2) 6 - -

Cash from investing 84 (221) (261) (125) (169)

Long term borrowing (979) (979) (968) (974) (974)

Dividends paid (4,443) (3,589) (3,148) (4,042) (5,617)

Cash from financing (5,422) (4,568) (4,116) (5,015) (6,590)

Change in Cash (2,675) (2,620) (392) 87 129Beg Cash 6,038 3,363 743 350 438

End Cash 3,363 743 350 438 567

Source: Company accounts, Global estimates

Key ratios

FY06 FY07 FY 08E FY09E FY10E

Margins (% )

EBITDA margin 20.5 12.6 11.3 13.2 16.4

Profitability (% )

ROAA 3.07 6.00 5.95 7.67 12.61

ROAE 4.49 8.99 9.66 12.51 18.58

Leverage (x)

Debt to equity 34.11 39.03 51.50 40.06 24.21

Valuation

Dividend yield (%) 11.25 10.34 9.87 12.67 17.61

Dividend payout (%) 130 124 113 114 108

Earnings yield (%) 8.7 8.3 8.7 11.2 16.3

P/E (x) 11.5 12.0 11.4 9.0 6.1

BVS (x) 2.59 2.51 2.48 2.44 2.40

P/B (x) 10.6 11.0 11.1 11.3 11.5

EV/EBITDA (x) 8.4 8.6 7.7 7.1 6.0

Source: Company accounts, Global estimates

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 17/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 16

Glossary

HUBCO: The Hub Power Company Ltd

WAPDA: Water and Power Development Authority

NEPRA: National Electric Power Regulatory Authority

PEPCO: Pakistan Electric Power Company

PPIB: Private Power and Infrastructure Board

PNRA: Pakistan Nuclear Regulatory Authority

PPA: Power Purchase Agreement

EPP: Energy Purchase Price

CPP: Capacity Purchase Price

IPP: Independent Power Producers

MW: Mega-Watts

GWh: Giga watt hours

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 18/19

The Hub Pow er Company Ltd

Global Securities Pakistan Ltd. 17

Analyst certification

Each research analyst primarily responsible for the content of this research

report, in whole or in part, certifies that with respect to each security or issuer

that the analyst covered in this report: (1) all of the views expressed accuratelyreflect his or her personal views about those securities or issuers; and (2) no

part of his or her compensation was, is, or will be, directly or indirectly, related

to the specific recommendations or views expressed by that research analyst in

the research report.

8/8/2019 Global - HUBCO - Jul08

http://slidepdf.com/reader/full/global-hubco-jul08 19/19

Global Securities Pakistan Ltd., Head Office: 9 th Floor Muhammadi House, I .I. Chundrigar Road, Karachi, Pakistan, Phone: +9221 2469420; Stock Exchange Office: 720 Karachi Stock Exchange, Stock Exchange Road, Karachi, +9221 2443880.

This report has been prepared by Global Securities Pakistan Limited for distribution only under such circumstances as may be permitted byapplicable law, including the following:

This report is intended solely for distribution to professional and business customers of Global Securities Pakistan Limited. It is not intended fordistribution to non-professional or private investors. The report has no regard to the specific investment objectives, financial situation or particularneeds of any specific recipient. The report is published solely for informational purposes and is not to be construed as a solicitation or an offer tobuy or sell any security or options thereon. The report is based on information obtained from sources believed to be reliable but is not guaranteedas being accurate, nor is it a complete statement or summary of the securities, markets or developments referred to in the report. The reportshould not be regarded by recipients as a substitute for the exercise of their own judgment. Any opinions expressed herein are subject to changewithout notice. Global Securities Pakistan Limited, and/or its directors, officers and employees may have or have had interests or positions ortraded or acted as market-maker in the relevant securities. Furthermore, they may have or have had a relationship with or may provide or haveprovided corporate finance or other services to or serve or have served as directors of the relevant Company. Global Securities Limited accept noliability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this report. Additional information will be madeavailable on request.

© Copyright reserved. No part of this report may be reproduced or distributed in any manner without the written permission of Global SecuritiesPakistan Limited. Global Securities Pakistan Limited specifically prohibits the re-distribution of this report, via the Internet or otherwise, to non-professional or private investors and accepts no liability whatsoever for the actions of third parties in this respect.

![Tp4 portugues jul08[1]](https://img.pdfslide.net/doc/110x75/55d57b75bb61eb685b8b45e0/tp4-portugues-jul081.jpg)

![Final Girc Hubco[1]](https://img.pdfslide.net/doc/110x75/577d2fce1a28ab4e1eb2bd45/final-girc-hubco1.jpg)

![Tp2 portugues jul08[1]](https://img.pdfslide.net/doc/110x75/5590ce431a28ab02398b45c5/tp2-portugues-jul081.jpg)

![Tp5 portugues jul08[1]](https://img.pdfslide.net/doc/110x75/558347cad8b42a8f548b4b8e/tp5-portugues-jul081.jpg)

![Tp3 portugues jul08[1]](https://img.pdfslide.net/doc/110x75/5588c0d9d8b42ad9448b45b6/tp3-portugues-jul081.jpg)

![Tp6 portugues jul08[1]](https://img.pdfslide.net/doc/110x75/55736119d8b42a40208b4835/tp6-portugues-jul081.jpg)