Embed Size (px)

Citation preview

03.12.2015

1

Global industry trends - penetrating future growth markets and entering new segments

Dr Peter Hackel, CFO

Not allowed for further usewithout permission

2

Agenda

Synergy potential and Neodent’s environment

Current industry trends

Our responses to these market trends

Financial performance & Outlook 2015

Questions & answers

Intro Deck

03.12.2015

2

Synergy potential and Neodent’senvironment

4

Who makes where?

Andover (USA):Implant productionPREMIUM

Arlington (USA)CADCAM millingPREMIUM & VALUE

Curitiba (BR)Neodent implant productionVALUECADCAM millingPREMIUM & VALUE

Malmö (S)Regenerative productsPREMIUM

Markkleeberg (D)Etkon CADCAM millingPREMIUM & VALUEVilleret (CH)

Implant productionPREMIUM

Tokyo (JP)[under construction]Etkon CADCAM millingPREMIUM & VALUE

03.12.2015

3

5

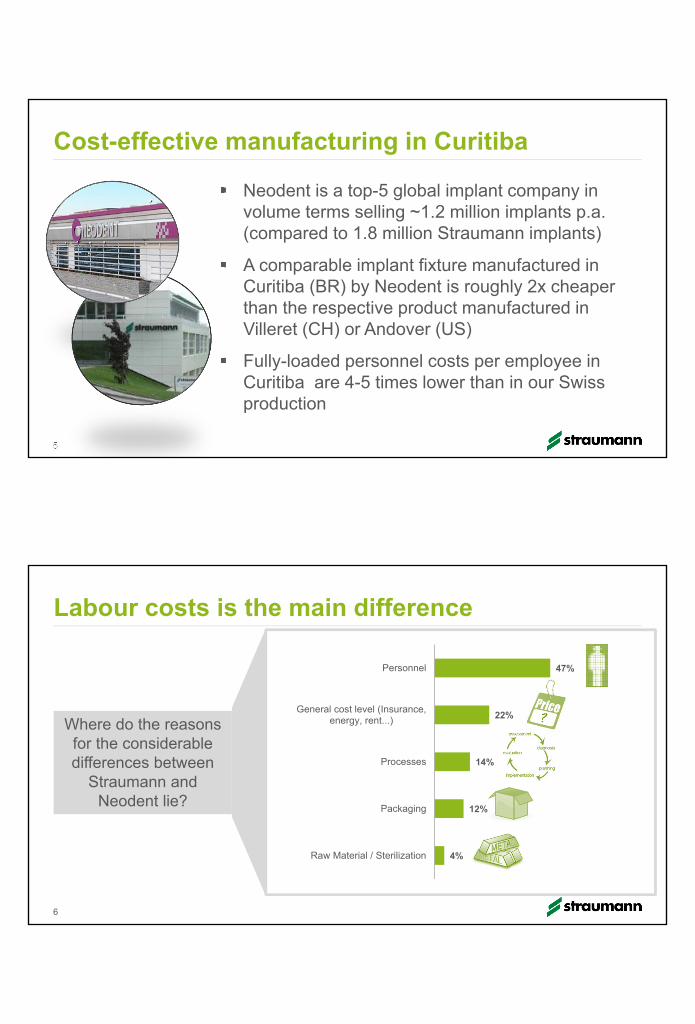

Neodent is a top-5 global implant company in volume terms selling ~1.2 million implants p.a. (compared to 1.8 million Straumann implants)

A comparable implant fixture manufactured in Curitiba (BR) by Neodent is roughly 2x cheaper than the respective product manufactured in Villeret (CH) or Andover (US)

Fully-loaded personnel costs per employee in Curitiba are 4-5 times lower than in our Swiss production

Cost-effective manufacturing in Curitiba

6

Labour costs is the main difference

Where do the reasons for the considerable differences between

Straumann and Neodent lie?

4%

12%

14%

22%

47%

Raw Material / Sterilization

Packaging

Processes

General cost level (Insurance,energy, rent...)

Personnel

03.12.2015

4

7

Continuous productivity improvements in our premium implant production

80

100

120

140

2011 2012 2013 2014 2015

Ind

exed

to

100

in

201

1

Volume and gross margin development in the premium implant production

Sales Volume COGSVilleret +Andover

8

Devaluation of the BRL lowers Neodent’s contribution – natural hedge mitigates the situation

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2010 2011 2012 2013 2014 2015BRLCHF USDCHF

-52%

0.266

0.57310.2%

89.8%

Revenue

9.8%

90.2%

OPEX & COGS

BRL other Group currencies

2015: Complete takeover

2012: 49% stake

03.12.2015

5

9

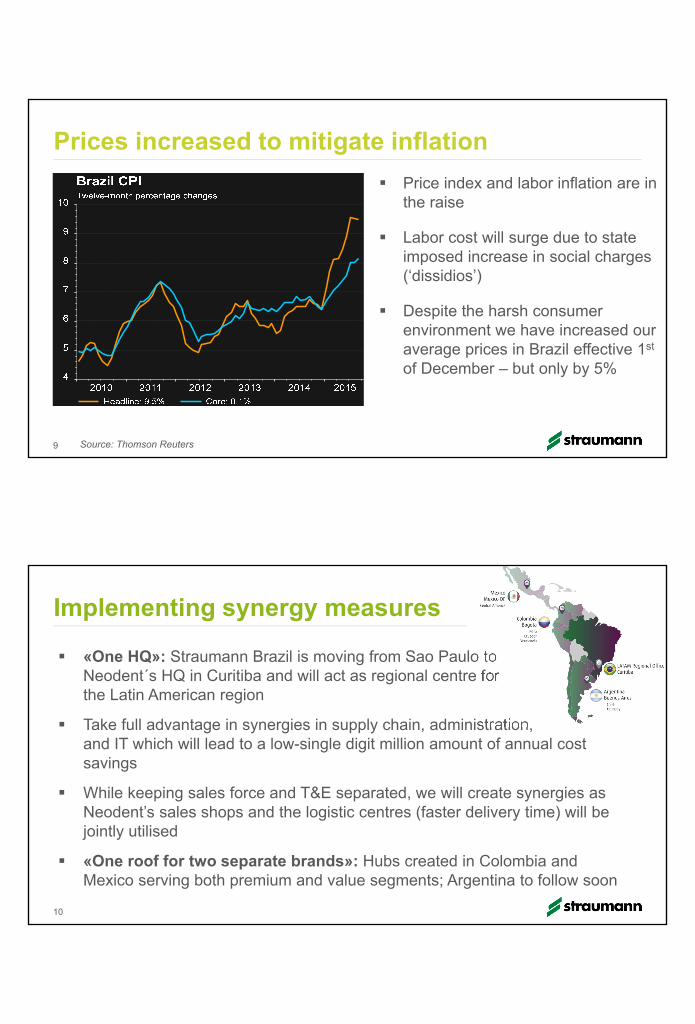

Price index and labor inflation are in the raise

Labor cost will surge due to state imposed increase in social charges (‘dissidios’)

Despite the harsh consumer environment we have increased our average prices in Brazil effective 1st

of December – but only by 5%

Prices increased to mitigate inflation

Source: Thomson Reuters

10

«One HQ»: Straumann Brazil is moving from Sao Paulo to Neodent´s HQ in Curitiba and will act as regional centre for the Latin American region

Take full advantage in synergies in supply chain, administration, and IT which will lead to a low-single digit million amount of annual cost savings

While keeping sales force and T&E separated, we will create synergies as Neodent’s sales shops and the logistic centres (faster delivery time) will be jointly utilised

«One roof for two separate brands»: Hubs created in Colombia and Mexico serving both premium and value segments; Argentina to follow soon

Implementing synergy measures

03.12.2015

6

11

Neodent has strong reputation for customer focus and service; perceived as a ‘high quality company’ by Brazilian dentists

Strong on education; associated with ILAPEO, one of the world´s largest implant training centers

Strong home market and platform for expansion into other LATAM markets

Cost-efficient, modern production in Curitiba

Platform to drive value strategy internationally

Complementary product portfolio

Straumann & Neodent – from strength to strength

Current industry trends

03.12.2015

7

Current dental implant market trends

Industry consolidation

Value products getting more accepted

Future growth markets are outside the traditional implant markets

Digitalisation of treatment workflows andtraditional manufacturing processes

Patients’ expectations have increased and customer base is more heterogenous

1

2

3

4

513

Pure playersPremium Value/Local

Medical device companies

Dental product manufacturers

Dental Wholesaler

14

2010: A fragmented tooth replacement market

>300 smaller/local players

1

03.12.2015

8

1

24%

20%

10%

13%

7%

26%

17

Competitive landscape has changed

Others

Global dental implant & abutment market worth~CHF 3.5bn (2014 pro-forma)

Based on iData, MRG and Straumann estimates. Zimmer-Biomet 3i acquisition pending antitrust clearance.

1

03.12.2015

9

40%

2014

The value segement has gained importance

1 Please note that market size has been influenced by high volatility in exchange rates2 Based on Straumann bottom-up estimation.. 18

2003 2008

Premium segment (incl. Straumann)

Value- und Discount segment (incl. Neodent)

~ 25% ~ 30%

~ 75%~ 70% ~60%

Market shares development per segment (in value terms)1,2

Market size est. CHF 1.3-1.6bn

Market size est. CHF 3.5bn

Market size est. CHF 3.3-3.6bn

2

Market structure and dynamics in high-growth markets vary considerably from traditional markets

19

3

0%

100%

Europe Asia Pacific North America Latin America

Discount Value Premium

Source: Straumann estimates

03.12.2015

10

Large potential to unlock in underpenetrated markets

Source: Straumann estimates

20

3

Implant market size in 2014 (volume)

Switzerland

Austria

Sweden

Netherlands

Canada

Australia

India

Colombia

Mexico

Japan

Spain

China

France

Russia

Israel

Turkey

Argentina

United Kingdom

<250k implants 250-1000k implants >1000k implants

United States

Brazil

South Korea

Germany

Italy

20

2 examples how digitalisation has transformedindustries

21

Photography

Media

4

03.12.2015

11

Dentistry is in a period of technologicalupheaval

22

Impression

Manufacturing

Casting and polishing Milling centre Laser sintering

Polyethylene Impression Intra-oral scanner Local scan and milling in the dental practice

4

24

Many of our new product solutions are driven by end-customer needs 5

03.12.2015

12

25

Patients’ expectations have changed...

Today Trend

Data based on Straumann poll conducted by GfK Healthcare

5

max

min

Buying groups (GPO)

Dental service organisations

(DSO)

... and the customer face has become multidimensional

Dental Laboratory

Surgeon

General practices

Patient

All-in-one multi-

disciplinary practices

Solo-practitioners

Dental chains

Solo-practitioners

5

26

03.12.2015

13

Clearchoice is one of our first DSO customer

The ClearChoice network provides innovative dental implant care across the United States. Each ClearChoice Center is owned and operated by licensed and experienced dental experts, providing all-in-one treatment facilities. Each center is equipped with modern technology (f.e. 3D CAT Scan technology) with on-site lab support. Over 30,000 Americans trust ClearChoice for dental implants.

5

The ClearChoice nationwide network has now 32 centers

27

Bupa insurance exemplifies this trend

Bupa was founded in 1947 in the UK and has become a leading global health and care company, which offers health insurance, medical subscription, care homes, retirement and care villages, primary care, diagnostic and wellness centres, hospitals and dental clinics in 190 countries.

‘Sanitas Dental’ (segment of Bupa) and his affiliate network has a global presence of nearly 400 dental practices

5

28

03.12.2015

14

Our responses to these market trends

Straumann’s growth strategy

Adr

essa

ble

mar

ket

Accelerate and expand in

underpenetrated markets

Total solution provider

Fortify innovation and technology leadership

Offer state-of-the-art digital and milling

solutions

Expand geographicalreach

Less-invasive, fast-healing, to metal-free ceramic

implant solutions

Access untapped segments & indications

Offer root-to-tooth solution for all

indications both for the premium and value

segment

30

03.12.2015

15

Addressing the value segment with various pricepoints

Introduction of Neodent brand in the US and selective markets in Europe

Implant price range in Europe1

€400

€100

€200 SLA

Roxolid

SLActive

PURE

Roxolid

SLATitanium

Acqua

Smart

CM

Neoporos

NeoporosCM

1 Example applying German reference prices: Please note that prices may vary from country to country31

32

Competing with attractively-priced Straumann solutions

Example applying German reference prices 1 Calculation does not consider dentist service fees and dental technician

labour share

Proven Titantium SLA implant € 179

Economically pricedVariobase product

family € 69+ +CADCAM bridge or single full-contoured crown for € 59 per

unit

Artifical tooth forslightly more than € 3001

03.12.2015

16

In the US example, implant list prices from Premium companies range between USD 250-450, Value from 100-250, while discount generally below the 100-dollar mark. These price bands vary by country depending on the overall PPP level and dental fee structure.

Addressing the value segment with other brands

33

Develop a regional/global value segment while at the same time minimizing the cannibalization risk

Offer different price points to decision makers

Enlarge distribution network and fasten market entry into fast growing markets

Greater flexibility when dealing with servicing organisationsor tenders

Combining scale, local and global expertise

Leverage cost-efficient manufacturing footprint

Drivers for multi-brands in the sector

34

03.12.2015

17

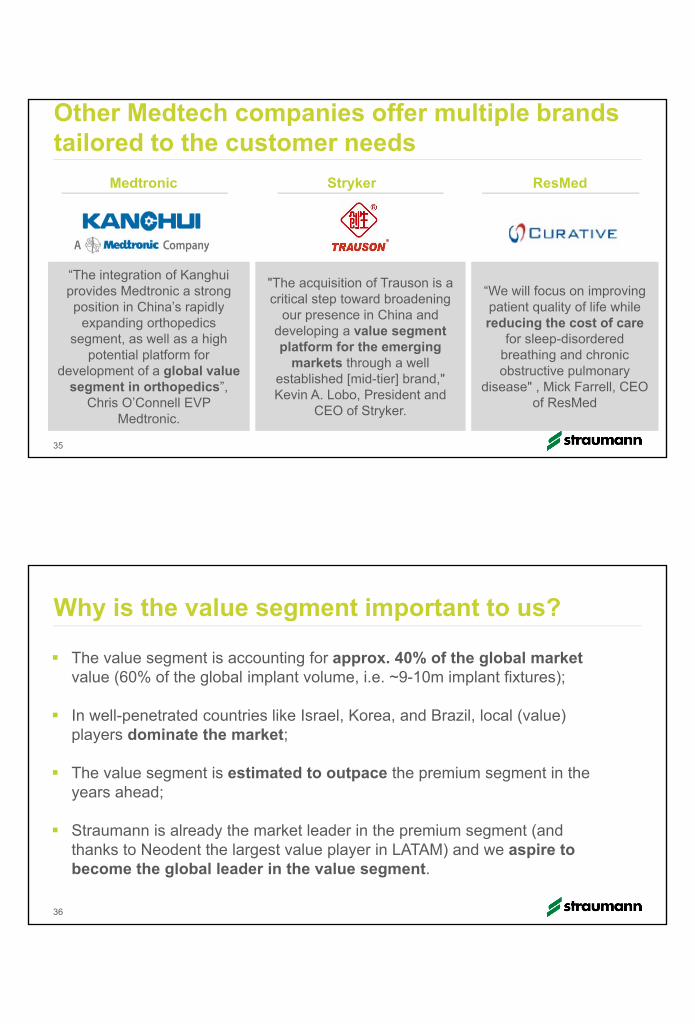

Other Medtech companies offer multiple brandstailored to the customer needs

Medtronic Stryker

35

"The acquisition of Trauson is a critical step toward broadening

our presence in China and developing a value segment platform for the emerging

markets through a well established [mid-tier] brand," Kevin A. Lobo, President and

CEO of Stryker.

“The integration of Kanghuiprovides Medtronic a strong position in China’s rapidly

expanding orthopedics segment, as well as a high

potential platform for development of a global value

segment in orthopedics”, Chris O’Connell EVP

Medtronic.

ResMed

“We will focus on improving patient quality of life while reducing the cost of care

for sleep-disordered breathing and chronic obstructive pulmonary

disease" , Mick Farrell, CEO of ResMed

Why is the value segment important to us?

The value segment is accounting for approx. 40% of the global market value (60% of the global implant volume, i.e. ~9-10m implant fixtures);

In well-penetrated countries like Israel, Korea, and Brazil, local (value) players dominate the market;

The value segment is estimated to outpace the premium segment in the years ahead;

Straumann is already the market leader in the premium segment (and thanks to Neodent the largest value player in LATAM) and we aspire to become the global leader in the value segment.

36

03.12.2015

18

37

Instradent expands its global presence

Availablity of Neodent products through:

Own subsidiaries, Instradent and 3rd party distributors

Future roll-outs

Neodent’s comprehensive implant portfoliocomplements well...

Drive Alvim Titamax Titamax Ex WS FacilityZygo-matico

NeoPoros Acqua NeoPoros Acqua NeoPoros Acqua NeoPoros Acqua NeoPoros NeoPoros Acqua NeoPoros

Main product for the international market

(60% volume)

Main products for the domestic

market (2/3 share)

38

03.12.2015

19

...with the Straumann implant lines

39

Tissue Level 4mm short implant Bone Level Bone Level TaperedPURE

Monotype

SLA SLActive SLActive SLA SLActive SLA SLActive ZLA

Titanium

Roxolid

Ceramic

‘Workhorse’ implant

Minimal invasive

Ideal for the aesthetic zone

More primary stability

Metal-free & improved aesthetics

ILAP

EO

Joined forces to exploit the full potential

Conservative, well-documented treatments

Progressive, immediate function protocols

BLT

Pro- Arch

Occupied by peers

ITI

ProArch

BLTPremium

Value

TissueLevel

BoneLevel

Drive Acqua

To4Zygoma

Alvim

Titamax

40

03.12.2015

20

1'060

0 500 1000 1500 2000

Fully tapered

Apically tapered

Parallel walled

Fully tapered

Apically tapered

Parallel walled

Tissue Level

Bone Level

STMN share Potential to grow Lower priced tapered implants

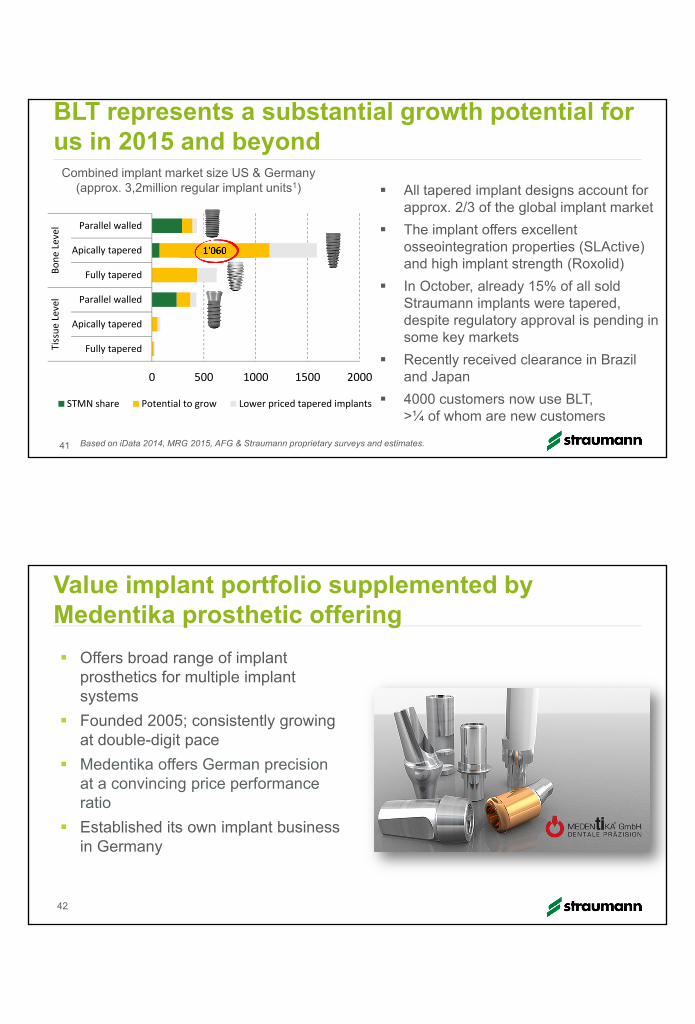

All tapered implant designs account for approx. 2/3 of the global implant market

The implant offers excellent osseointegration properties (SLActive) and high implant strength (Roxolid)

In October, already 15% of all sold Straumann implants were tapered, despite regulatory approval is pending in some key markets

Recently received clearance in Brazil and Japan

4000 customers now use BLT, >¼ of whom are new customers

BLT represents a substantial growth potential for us in 2015 and beyond

Combined implant market size US & Germany (approx. 3,2million regular implant units1)

Based on iData 2014, MRG 2015, AFG & Straumann proprietary surveys and estimates. 41

42

Value implant portfolio supplemented by Medentika prosthetic offering

Offers broad range of implant prosthetics for multiple implant systems

Founded 2005; consistently growing at double-digit pace

Medentika offers German precisionat a convincing price performanceratio

Established its own implant business in Germany

03.12.2015

21

43

Potential identified to expand our position across indications and segments

Stock abutments

Customized abutments

CA

DC

AM

m

illin

g sy

stem

s

Dental implants

DV

T /

3D

ra

dio

logy

Sur

gica

l pla

nnin

g &

dril

l gu

ides

Global market size ~CHF 7bnShare of the Straumann Group

Bon

e &

tiss

ue

rege

nera

tion

CADCAM manu--factured prosthetics

Sca

nner

s

Conventionally manufactured prosthetics on

implants (crowns, bridges, bars)

1 CARES Scan&Shape as an additional Service for GP and DL, mainly for non digitally equipped customers

Our current digital offering...

44

GPDental lab

3rd party intra-oral scanners

1Desktop Scan

Centralized milling

Equipment business supplemented by various consumables ranging from ceramic materials through to implant bars & bridges

Scan&ShapeService1

03.12.2015

22

1 CARES Scan&Shape as an additional Service for GP and DL, mainly for non digitally equipped customers

...and what we are aiming for

45

GPDental lab

3rd party intra-oral scanners

Intra-oral scanning

1Desktop Scan

Centralized millingIn-lab milling Chairside solution

Equipment business supplemented by various consumables ranging from ceramic materials through to implant bars & bridges

Scan&ShapeService1

1 CARES Scan&Shape as an additional Service for GP and DL, mainly for non digitally equipped customers* LMR = limited market release in EU. Further rollout pending regulatory approval in the respective markets

With the following timelines

46

3rd party intra-oral scanners

Intra-oral scanning

1Desktop Scan

Centralized millingIn-lab milling Chairside solution

Equipment business supplemented by various consumables ranging from ceramic materials through to implant bars & bridges

Scan&ShapeService1

GPDental lab

03.12.2015

23

Financial performance & Outlook 2015

48 Organic growth – i.e. excluding the effects of acquisitions, divestitures and currency exchange rates . Main competitors incl. Nobel Biocare, Zimmer Dental, Biomet 3i, Dentsply Implants based on company and SEC reports, as well as management comments

Revitalized topline and raise in profitability

22.3%

17.3%14.9%

18.2%20.9%

24.0%

0%

10%

20%

30%

0

100

200

2010 2011 2012 2013 2014 H1 2015

Operating profits

Operating income Exceptionals Underlying EBIT margin

in CHF million 2010 2011 2012 2013 2014 9M 2015 5y CAGR

Revenue in CHF 737.6 693.6 686.4 679.9 710.3 585.3 ‐1%

growth in %

Organic revenue growth 2.5 4.1 ‐1.0 1.2 6.4 8.6 3.6

Acquisiton / Divesture 2.1 0.0 ‐0.6 ‐0.8 0.0 9.5 1.7

Total l.c. growth 4.6 4.1 ‐1.6 0.4 6.4 18.1 5.3

FX effect ‐4.4 ‐10.1 0.5 ‐1.3 ‐1.9 ‐6.3 ‐3.9

Total revenue growth (in CHF) 0.2 ‐6.0 ‐1.1 ‐0.9 4.5 11.8 1.4

4.0%3.2%

‐1.0%

1.2%

6.4%

8.6%

0.2%

2.5%

‐0.9%0.1%

2.4%

4.6%

2010 2011 2012 2013 2014 9M 2015

Organic growth vs. main peers

Organic revenue growth Organic growth main competitors

03.12.2015

24

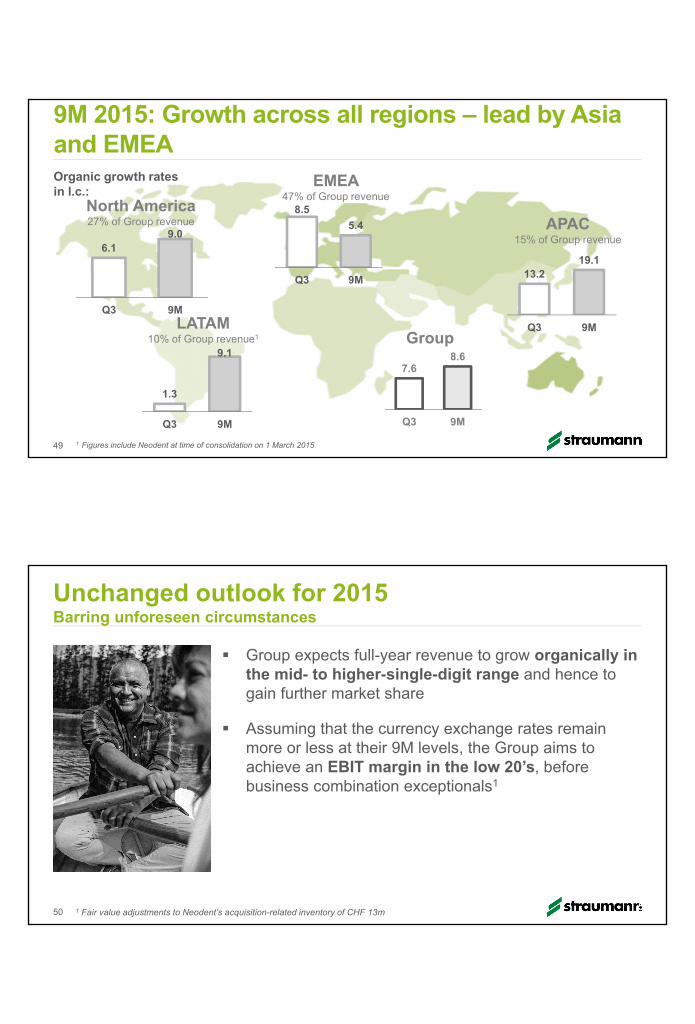

North America27% of Group revenue

49

Organic growth rates in l.c.:

9M 2015: Growth across all regions – lead by Asia and EMEA

6.19.0

Q3 9M

1.3

9.1

Q3 9M

LATAM 10% of Group revenue1

8.5

5.4

Q3 9M

EMEA 47% of Group revenue

13.219.1

Q3 9M

APAC15% of Group revenue

7.68.6

Q3 9M

Group

1 Figures include Neodent at time of consolidation on 1 March 2015

50

Group expects full-year revenue to grow organically in the mid- to higher-single-digit range and hence to gain further market share

Assuming that the currency exchange rates remain more or less at their 9M levels, the Group aims to achieve an EBIT margin in the low 20’s, before business combination exceptionals1

Unchanged outlook for 2015Barring unforeseen circumstances

501 Fair value adjustments to Neodent’s acquisition-related inventory of CHF 13m

03.12.2015

25

Questions & answers