Embed Size (px)

Citation preview

- 4

V,r1{.=

• -

•• -

- -UNITED STATES DISTRICT COURT ir'c,41,

DISTRICT OF MASSACHUSETTS

c 7 FTHOMAS P. GORMAN, BARRETT HERRIOTT, ) No.

LYMAN, ALBERT HALEGOUA, RONALD )CFFNER and FRED COHEN, On Behalf of ) CLASS ACTION Themselves and All Others Similarly )Situated, )

) CLASS ACTION COMPLAINT FORPlaintiffs, ) VIOLATION OF THE FEDERAL

) SECURITIES LAWSvs.

SYSTEMSOFT CORPORATION, ROBERT F. )ANGELO, WILLIAM J. O'CONNELL, PAUL ) 7' MJ. PEDEVILLANC, ROBERT N. GOLDMAN, ) - -THOMAS W. HIGGINS, RUSSELL BLAIR, )JONATHAN L. JOSEPH, W. FRANK KING, )DAVID SOMMERS, DAVID J. McNEFF and )COOPERS & LYBRAND LLP, )

)Defendants. ) Plaintiffs Demand.A (.1;- ) Trial By Jury

-

-

TABLE OF CONTENTS

Page

INTRODUCTION AND OVERVIEW 1

JURISDICTION AND VENUE 20

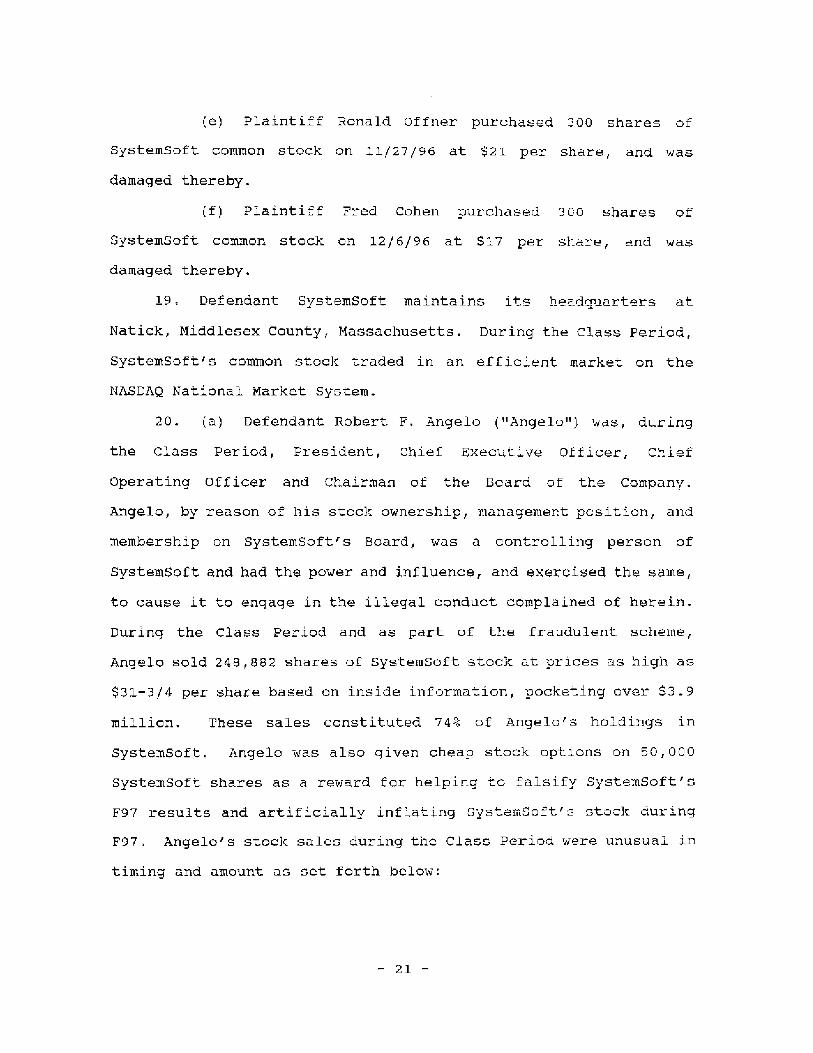

THE PARTIES 20

SCIENTER ALLEGATIONS 32

Actual Knowledge 32

Motive And Opportunity ' 38

DEFENDANTS' FRAUDULENT SCHEME AND COURSE OF BUSINESS . . . 38

STATUTORY SAFE HARBOR 39

BACKGROUND TO THE CLASS PERIOD 40

FALSE AND MISLEADING STATEMENTS ISSUED DURING THE CLASSPERIOD 40

SYSTEMSOFT'S FALSE FINANCIAL REPORTING DURING THE CLASSPERIOD 86

Digital Equipment Revenue 87

Distributor Revenue Recognition 89

COOPERS & LYBRAND'S PARTICIPATION IN THE FRAUD 93

INSIDER SELLING 103

FIRST CLAIM FOR RELIEFFor Violation Of §10(b) Of The Exchange Act AndRule 10b-5 Against All Defendants 108

SECOND CLAIM FOR RELIEFFor Violation Of S20(a) Of The Exchange ActAgainst Defendants Angelo and SystemSoft 110

CLASS ACTION ALLEGATIONS 111

BASIS OF ALLEGATIONS 113

PRAYER FOR RELIEF 113

JURY DEMAND 114

_ _

INTRODUCTION AND OVERVIEW

1. This is an action on behalf of purchasers of the stock of

SystemSoft Corporation ("SystemSoft" or the "Company") between

1/25/96 and 3/3/97 (the "Class Period"), complaining of a

fraudulent scheme L and course of business that operated as a fraud

and deceit on purchasers of SystemSoft stock. The defendants are

SystemSoft and its top officers and directors (the "SystemSoft

Defendants") and SystemSoft's outside auditor and accounting firm

(collectively the "Defendants").

2. SystemSoft went public in 8/94 at $2.75 per share l with

annual revenues of only about $9-$10 million. However, after

SystemSoft went public, its stock was a poor performer, as the

Company sold only a few software products for use almost

exclusively in laptop computers, which limited the commercial

market for its products and its prospects for significant

profitable growth. Sy late 95, analysts became critical of

SystemSoft's growth rate and its failure to introduce new products.

SystemSoft's top insiders were upset over this criticism and

determined to overcome it by pushing SystemSoft's stock to much

higher prices so they could sell off large amounts of their

SystemSoft stock at much higher -- and more profitable -- prices.

Thus, in 1/96, SystemSoft, with great fanfare, announced the

development of a new "call-avoidance" software product called

SystemWizardm ("SystemWizard"), which would be used in both desktop

and laptop PCs and supposedly had the ability to quickly analyze

All per share amounts in this Complaint are adjusted forSystemSoft's 2-for-1 stock split effective 7/17/96, unlessotherwise stated.

-1-

and determine the cause of a PC malfunction and advise the user how

to remedy it -- thus avoiding for both PC users and PC

manufacturers the frustration and expense of calls to the PC

manufacturers' technical service centers. SystemSoft told

investors that this new SystemWizard product addressed a huge

potential market, because attempting to obtain help from the

technical assistance centers of PC manufacturers often required

frustrating and expensive telephone calls involving long periods

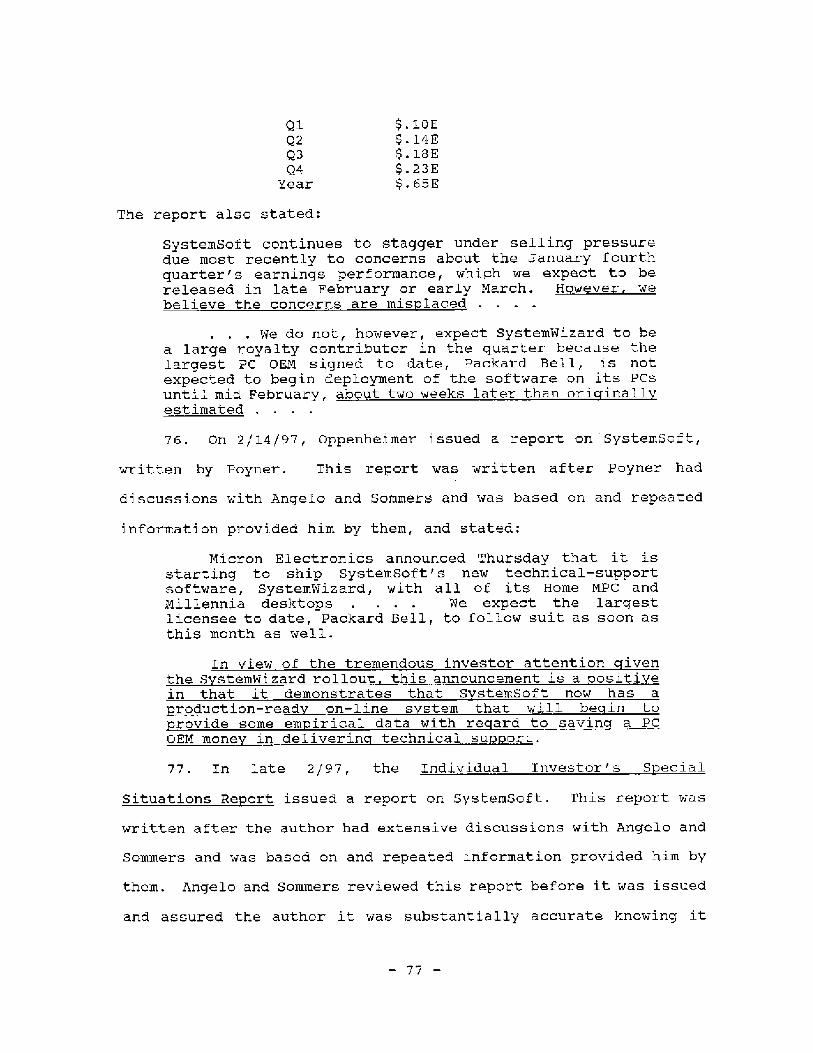

spent on "hold," as well as service charges of $30 per more per

call on which charge PC manufacturers still lost money. Thus,

reducing these service calls would benefit both PC users and

manufacturers.

3. In the event SystemWizard was unable to identify and

remedy the cause of the malfunction, SystemWizard also was to

enable the PC user to be connected quickly to the PC manufacturers'

technical service center with its analysis of the problem, thus

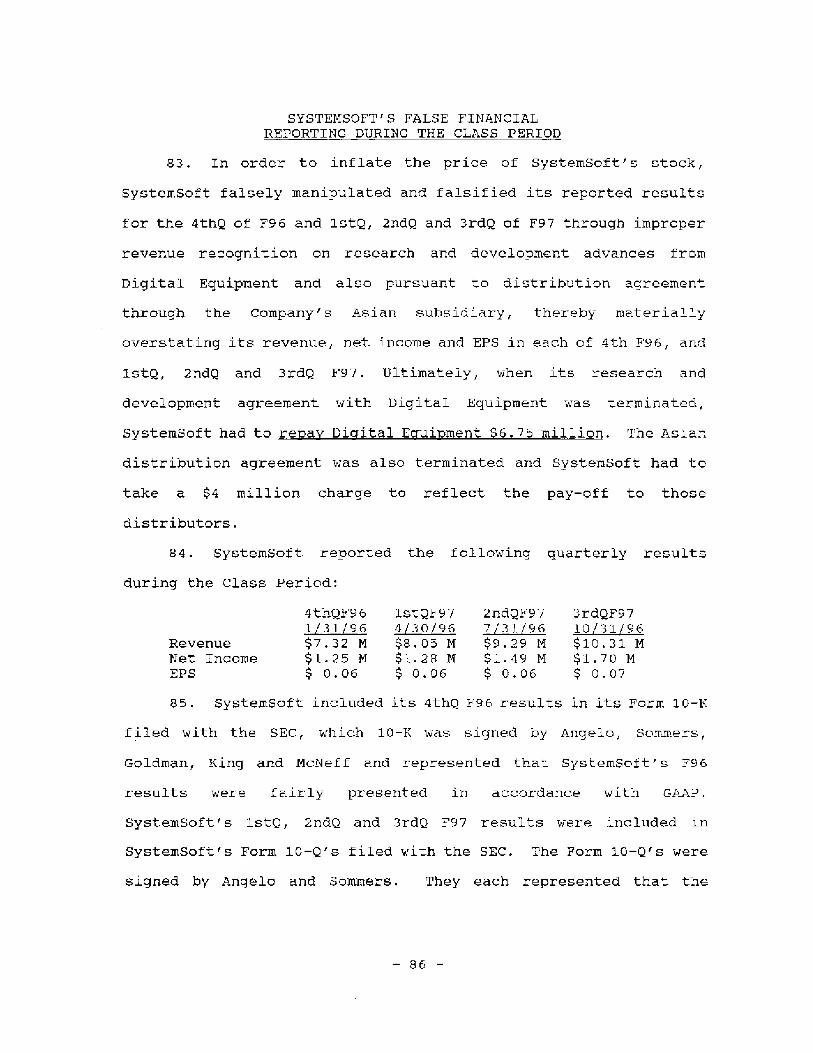

greatly facilitating the users' receipt of technical assistance.

According to SystemSoft, because its SystemWizard product would be

incorporated by major PC manufacturers into desktop PCs, as well as

laptops, this new product would access a huge market five times

larger than SvstemSoft's existing market, would be SystemSoft's

breakthrough/flagship product and would, in combination with

continued strong demand for SystemSoft's core product line, lead to

tremendous revenue and earnings per share ("EPS") growth for

systemSoft of 40%-60% over the next several years and specifically

a doubling of the size of the Company by the end of fiscal 97

("F97"), i.e., 1/31/97, with revenues and EPS of $90 million and

$.65, respectively.

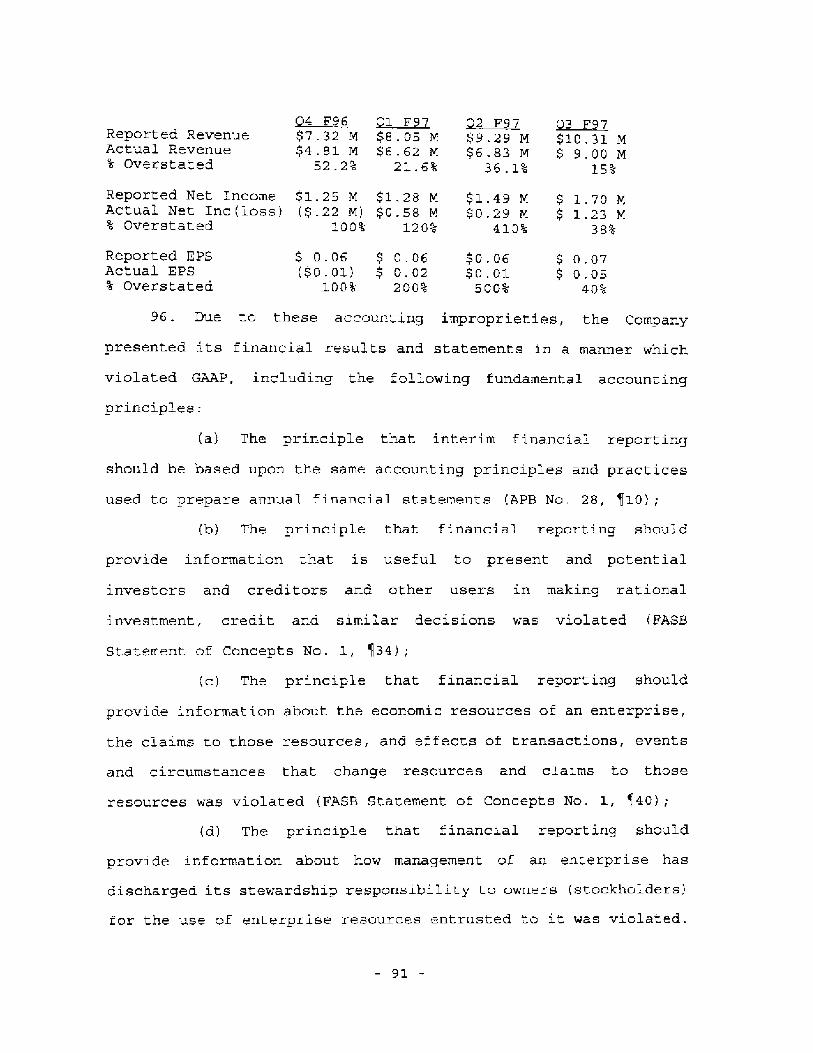

-2-

4. When SystemWizard was announced, SystemSoft stated that

with the financial backing and marketing assistance of Digital

Equipment, SystemWizard would be ready for evaluation by PC OEMs by

mid-96, initial shipments would occur early in the 4th c of F96

ending 1/31/96, with volume shipments to begin in F97. SystemSoft

falsely represented in 1/96 that SystemWizard would reduce calls to

technical support by 30%, even though its internal research showed

only a 10% reduction in calls. SystemSoft also said it expected

most major PC Original Equipment Manufacturers ("OEMs") to license

and deploy SystemWizard. As SystemWizard was being developed in

F96, SystemSoft represented the "development effort . . . is

Yielding very strong support from its OEM customers," and that

SystemSoft would charge a royalty fee of at least $5 per unit.2

When SystemWizard was formally introduced in 6/96, SystemSoft

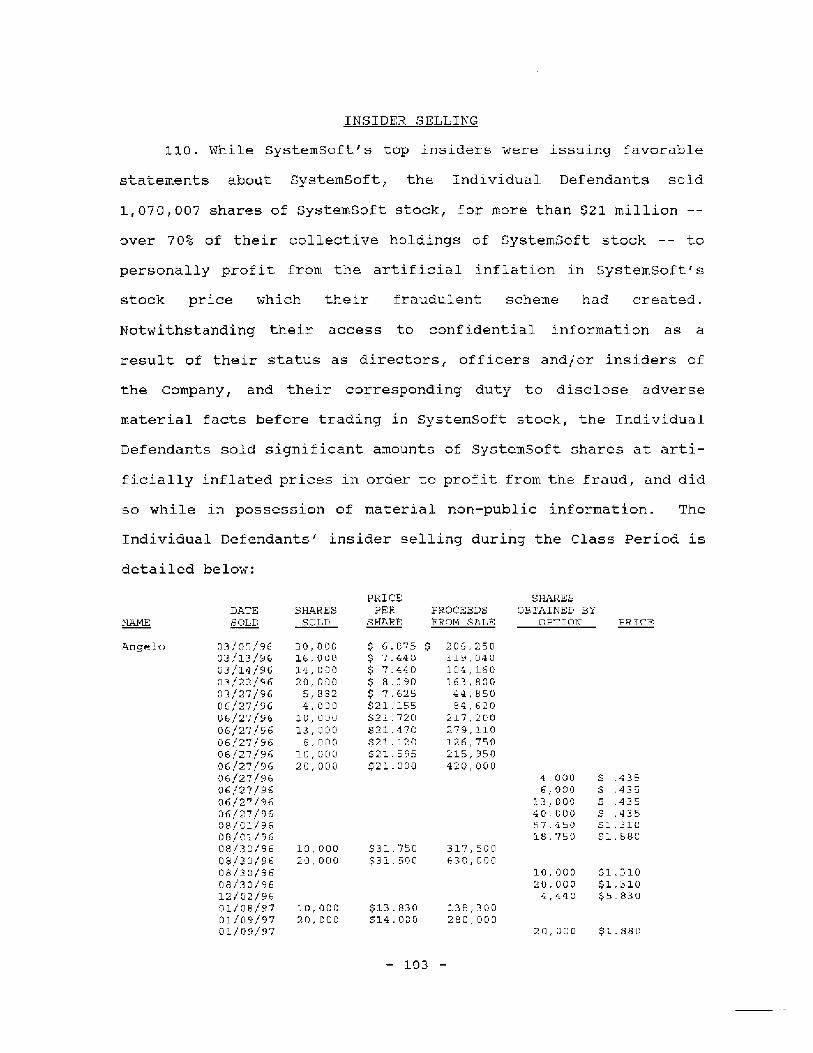

stated it had "firm commitments" from a number of PC CEMs for

"eight million units" in the next 12 months, which would generate

approximately $50 million in revenue. During the summer and fall

of 96, SystemSoft represented that in evaluations by major PC

manufacturers, SystemWizard got an "A+ from all," was "coming out

with flying colors," the product was "blowing SvstenSoft away," had

"tremendous upside" and this was the "best feeling that

[SystemSoft] ever had about a product." SystemSoft also told

investors that its new SystemWizard contracts translated into "many

millions of units" and "several million dollars of new revenue."

SystemSoft was also very positive about its new Universal Serial

Bus ("USB") product which it announced in 8196, stating that the

2 Here, as elsewhere, emphasis is has been added unlessotherwise noted.

- 3 -

product was doing very well, it had a number of companies that

would be ordering the product, and it expected the product to "take

the world by storm," generating significant F98 revenues. During

this period, SystemSoft continued to reassure investors that its

"base business is flourishing," where it was "getting faster growth

than expected" and, as a result, its PC card business would grow by

505-60% over the next two years. And, as SystemSoft reported

sequential revenue and EPS growth throughout the Class Period,

which results were audited and certified and/or reviewed and

approved by its accountants, it attributed its "record growth" and

"record results" to "customer acceptance of our products" and the

"continued accqptance of SvstemSoft's technologies by a growing

customer base." As a result of this barrage of extremely favorable

information about SystemSoft and its new SystemWizard and USB

products, SystemSoft's stock was a fantastic performer, rocketing

from $4-3/8 in mid-1/96 to a Class Period high of $36-1/2 in 9/96.

5. However, when SystemSoft reported slightly lower revenues

than anticipated for its 3rdQ F97, i.e., the three months ended

10/31/96, and announced a large contract for SystemWizard with

Packard Bell, but at lower per unit prices, SystemSoft's stock

declined. However, SystemSoft's stock continued to trade at

artificially inflated levels as the Company continued to forecast

strong F98 EPS ($.65) and unveiled a new product -- its USB

software suite, which it represented was a "huge market oppor-

tunity" for SystemSoft. Nevertheless, the decline accelerated in

12/96 and 1/97 when rumors circulated that SystemSoft's 4thQ F97

results would fall short of expectations, due to weakening demand

for SystemSoft's core products and delays in the deployment of

- 4 -

SystemWizard by major PC OEMs. Although SystemSoft denied that

there were any significant problems with the Company or delays with

its new SystemWizard product and insisted that the pricing of the

Packard Bell contract was misunderstood by analysts and not a

negative development and that major deployments of SystemWizard

would occur in the near future, SystemSoft's stock ultimately fell

to S17-5/8 on 3/3/97. Then, after the close of trading on 3/3/97,

SystemSoft shocked the market by revealing that SystemWizard was,

in fact, encountering significant delays in deployment, that

shipments of SystemSoft's core CardWizard product to IBM had been

delayed and, as a result, SystemSoft's revenue and EPS growth

during F98 would be significantly lower than earlier forecast.

SystemSoft's stock collapsed on this revelation, immediately

falling to $11-1/8 and then to $7-5/8 by 3/19/97, as the market

digested the implications of these adverse developments. The

3/4/97 one-day SystemSoft stock decline of 37% on volume of 6.1

million shares was the largest one-day price decline on the largest

one-day stock trading volume in SystemSoft's history as a public

company!

6. While SystemSoft's insiders continued to attempt to

support SystemSoft's stock during 97 by assuring investors and

analysts that SystemWizard was still making good progress with

major PC OEMs, and that SystemSoft would still achieve profitable

growth throughout F98 to end 1/31/90, in fact, SystemSoft's results

stagnated, due to slowing growth of SystemSott's core business and

a lack of significant revenues from SystemWizard or USB. It was

revealed that during the Class Period, Digital Equipment had

cancelled its SystemWizard contract with SystemSoft and as a

-5-

result, SystemSoft had to pay back approximately $7 million to

Digital Equipment. Promised announcements of major OEM adoption of

or deployment of SystemWizard were delayed or never occurred.

Rather than the strong growth forecast during the Class Period for

SystemSoft during F98, due to the success of SystemWizard and

continued strong demand for SystemSoft's core CardWizard products,

in fact, symSr-, ft suffered a hideous F98. SystemSoft achieved

revenues of only about $39-$40 million, while it suffered a large

loss. The "doubling" of the Company forecasted during the Class

Period for F98, i.e., revenue of $90 million and EPS of $.65, never

occurred.

7. In discussions with analysts on 2/6198, Robert F. Angelo

admitted to being in "mortal shock" over these "embarrassing"

developments, i.e., SystemSoft's large operating loss and multi-

million dollar write-offs, and said that SystemSoft had suspended

hiring indefinitely and would, at best, breakeven in following

quarters. Angelo also said "We're writing-off [$12-$14 million]

many, many things that just had no value." He admitted that the

USB business was being spun-off as "the cost of doing USB business

continues to outweigh the short-term benefits* and that SystemSoft

was receiving no payment for the business and was writing-off its

investment in it. As to systemWizard, Angelo admitted SystemSoft

did not even know what its "installed base" of that product was,

was no longer even tracking that, and that "SystemWizard revenue

continued to experience "very long" implementation cycles which

"pushes revenue out" and even "two new wins . . . unfortunately

didn't carry a lot of revenue with them." When Angelo admitted

that these huge losses wiped out all SystemSoft's retained earnings

-6-

and "obviously put that into a large loss," one analyst erupted,

saying "so . . . you guys have . . never made a nickel at the end

of the day when you add it all up," to which Angelo said, "I agree

with you." When asked if the current write-downs related to

questions raised about SystemSoft's accounting in a Forbes article

a year earlier, Paul J. Pedevillano said, "No, it wasn't related to

that article."

S. SystemSoft's stock has never recovered from the bungled

development and unsuccessful launch of the SysterWizard product,

the termination of the Digital Equipment/SystemWizard contract, and

softening in demand for its core products, including CardWizard.

As a result, SystemSoft's stock fell to as low as $3 per share in

F98. The USB product was spun-off and a charge recorded to reflect

non-recoverable costs associated with USB. Defendant Robert

Angelo, President, Chief Executive and Operating Officer and

Chairman of the Board, was ultimately removed from overseeing

SystemSeft's day-to-day operations. The Boston Business Journal

reported this change of leadership at SystemSoft:

Deborah Besemer, who was named president and chiefoperating officer, has taken over day-to-day operations at SystemSoft. .

The move is . . an attempt to stabilizeSystemSoft's stock price . . . . Analysts have beencritical about the company . . . since SystemWizard hasyet to generate its expected revenue. . .

Aaron Edelheit, an analyst with New York-basedIndividual Investment Group, said the main problem withSystemWizard has been a lack of support from the majorplayers in the computer industry, such as Dell computerCorp. of Austin, Texas, and Compaq Computer Corp. ofHouston.

Edelheit said prolonged product testing, andallowing computer makers to have the product for free,may continue to depress SystemWizard's revenue figures

-7--

into 1998. . . . "The problem is no one's paving for ISystemWizardl."

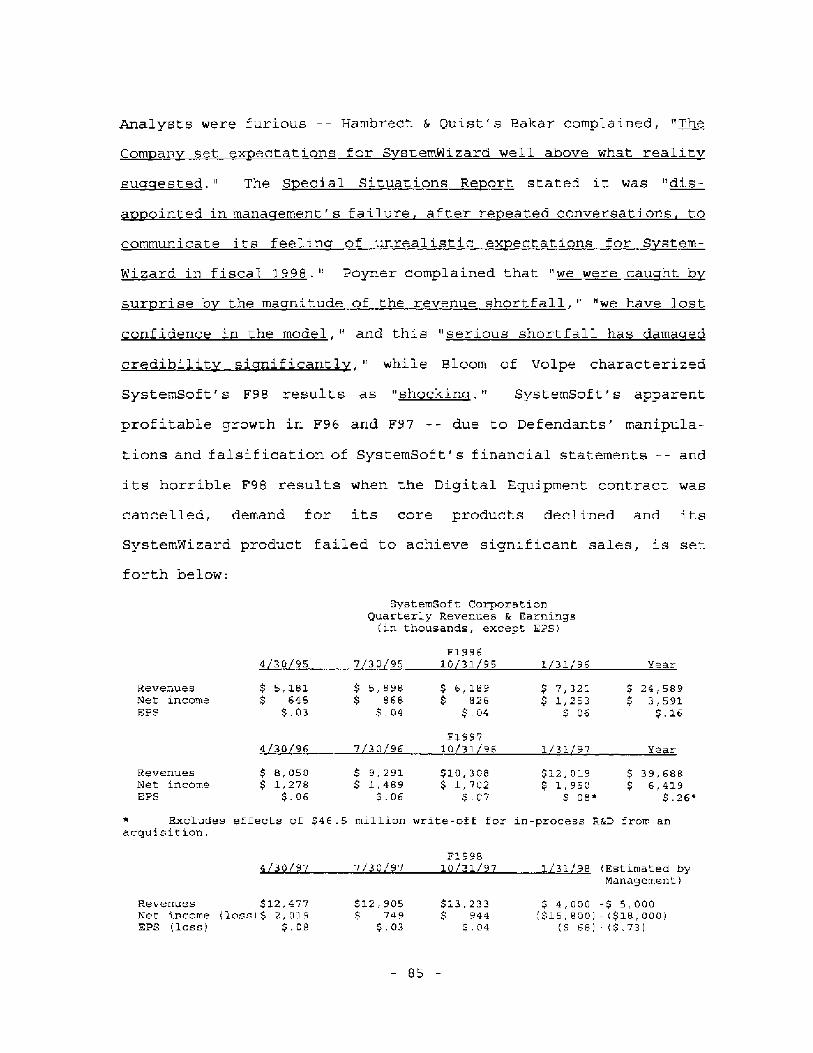

9. Analysts were furious about the deception practiced on

them, complaining, "The Company set expectations for SystemWizard

well above what reality suggested," they were "disappointed in

management's failure, after repeated conversations, to communicate

its feeling of unrealistic expectations for SystemWizard in fiscal

1998," that they "were caught by surprise by the magnitude of the

revenue shortfall," they "hardl lost confidence in the model," and

this "serious shortfall has damaged credibility significantly,"

while characterizing SystemSoft's F98 results as "shocking."

10. Public investors who invested based on SystemSoft's

representations about the successful development and launch of

SystemWizard, continuing strong demand for systemSoft's core

products and its forecasts of strong growth in 1'98-F99, and thus

paid as high as $36-1/2 per share for SystemSoft's stock during the

Class Period, have suffered millions in damages. However,

SystemSoft's insiders who knew the truth about the delays in the

development and deployment of SystemWizard and its limited

potential, the softening demand for SystemSoft's core products and

SystemSoft's serious problems with Digital Equipment and the

inevitable cancellation of that contract, did not fare nearly so

poorly. Before the startling revelations of 3/3/97 occurred, and

SystemSoft's stock price collapsed, SystemSoft insiders --

defendants Angelo, O'Connell, Pedevillano, Goldman, Higgins, Blair,

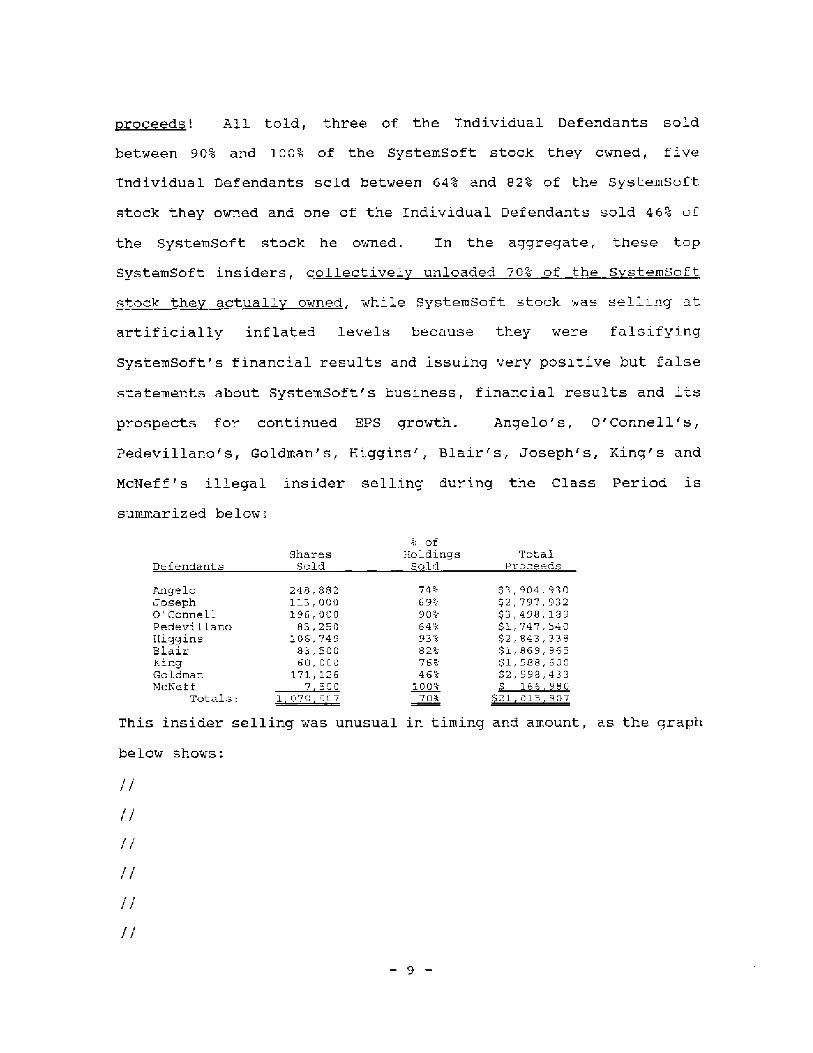

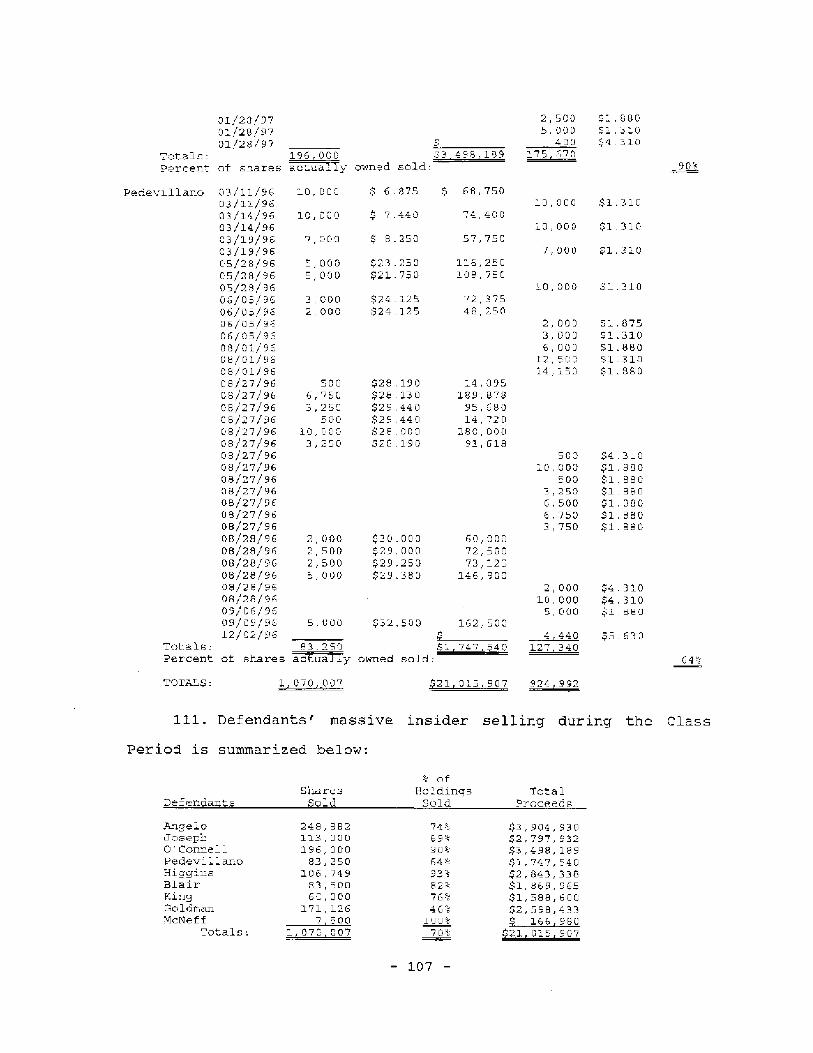

Joseph, King and McNeff unloaded 1,070,007 shares of their

SystemSoft stock at artificially inflated prices as high as $34-1/8

per share, pocketing over $21 million in illegal insider tradinq

-8-

proceeds! All told, three of the Individual Defendants sold

between 90% and 100% of the SystemSoft stock they owned, five

Individual Defendants sold between 64% and 82% of the SystemSoft

stock they owned and one of the Individual Defendants sold 46% of

the SystemSoft stock he owned. In the aggregate, these top

SystemSoft insiders, collectively unloaded 70% of the SystemSoft

stock they actually owned, while SysterSoft stock was selling at

artificially inflated levels because they were falsifying

SystemSoft's financial results and issuing very positive but false

statements about SystemSoft's business, financial results and its

prospects for continued EPS growth. Angelo's, O'Connell's,

Pedevillano's, Goldman's, Higgins', Blair's, Joseph's, King's and

McNeff's illegal insider selling during the Class Period is

summarized below:

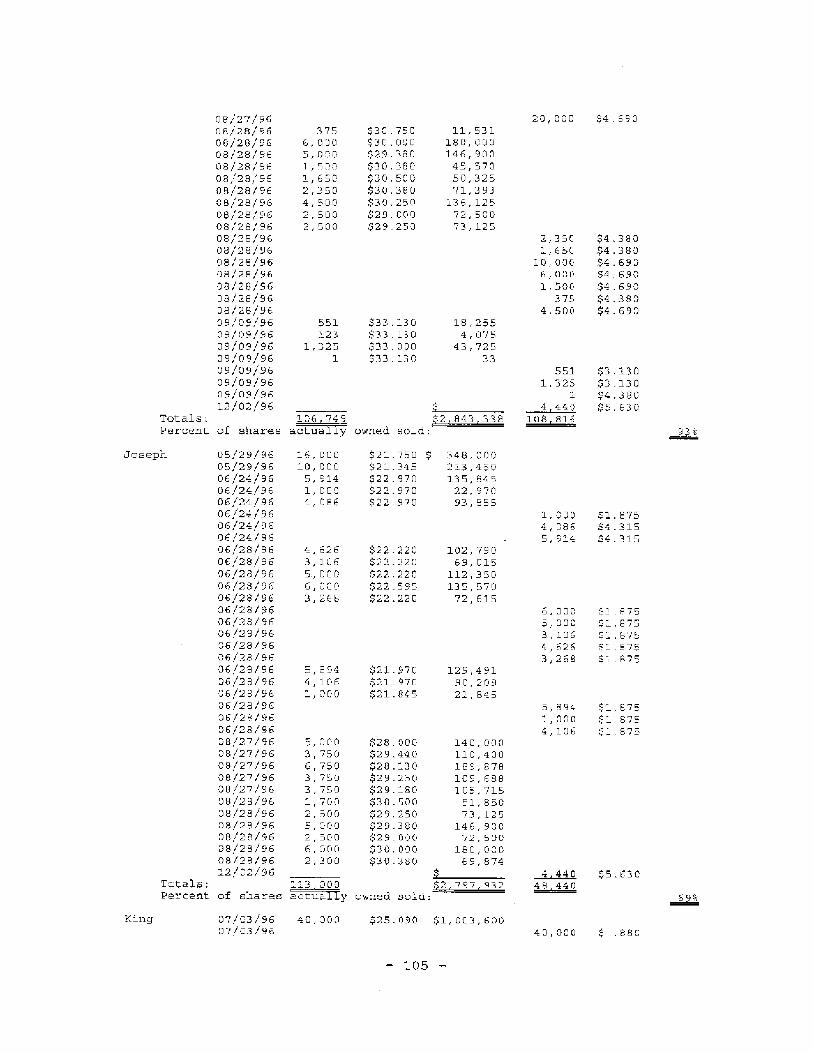

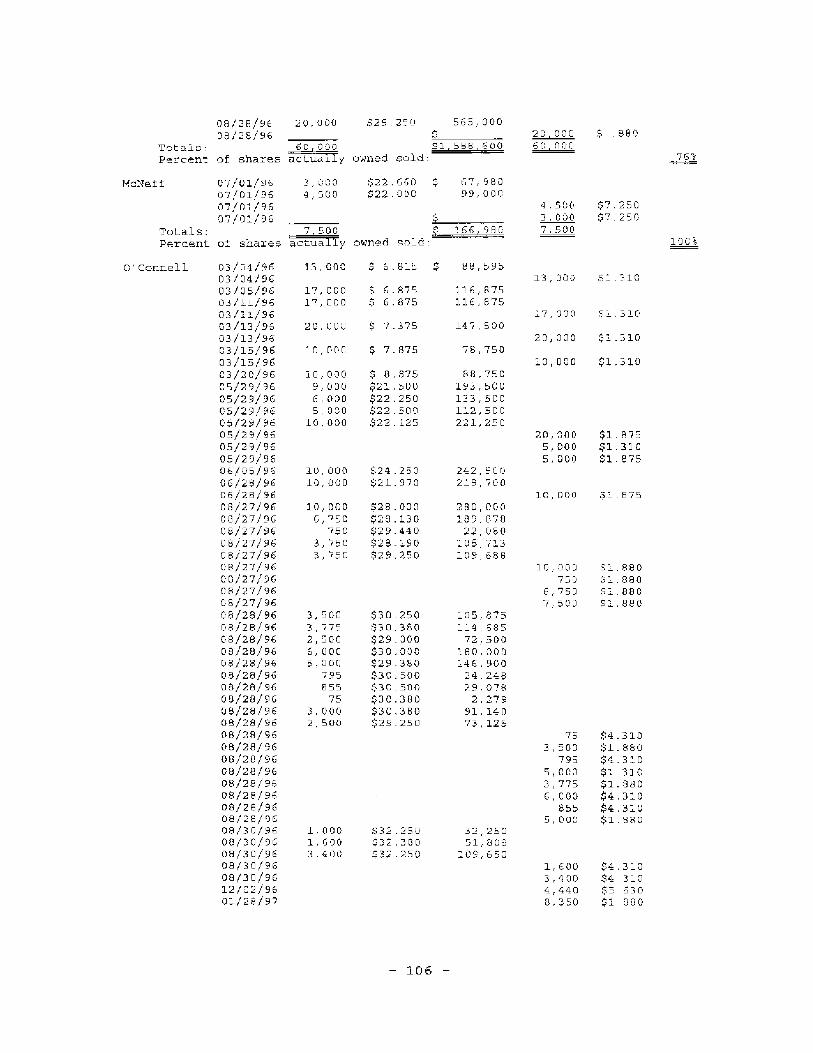

of

Shares Holdings TotalDefendants Sold Sold Proceeds

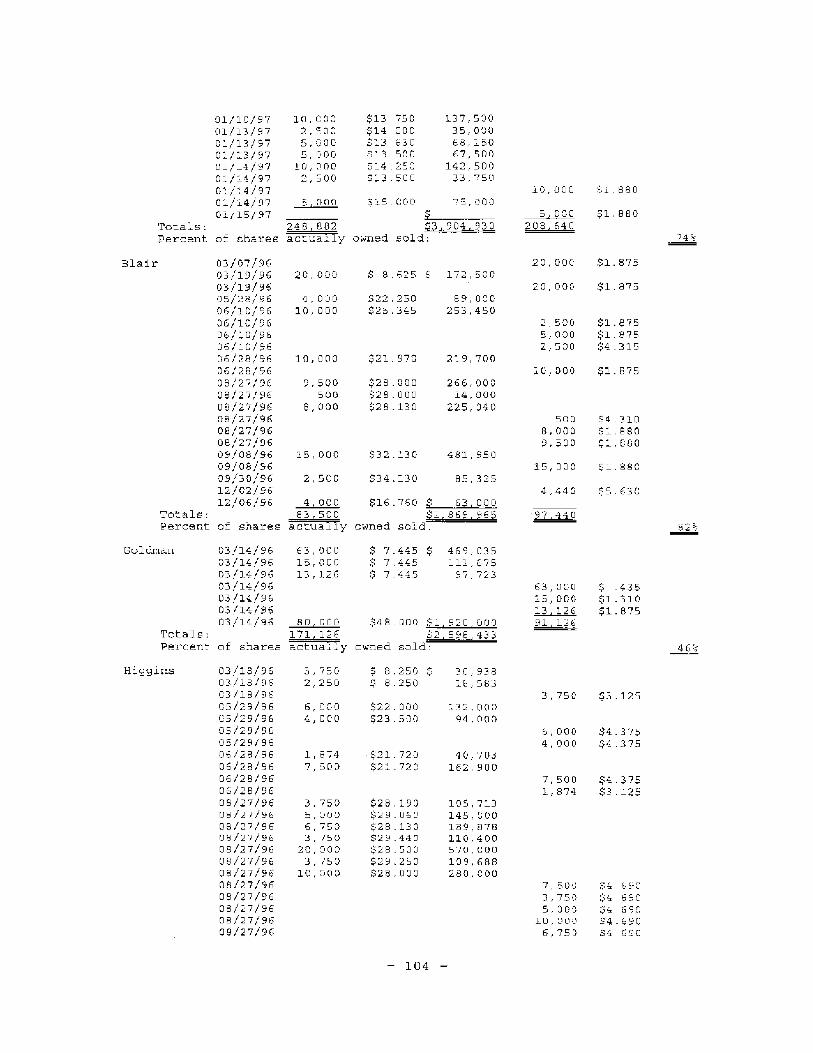

Angelo 245,882 74% $3,904,930Joseph 113,000 69% $2,797,932O'Connell 195,000 90% $3,495,189Pedevillano 83,250 64% $1,747,540Eiggins :06,749 93% $2,843,338Blair 83,500 82% $1,869,965King 60,000 $1,588,60CGoldman 171,125 45" $2,598,433MeNeff 7,300 100% '4 166,980

Totals: 1,070,007 70s $21,015,907

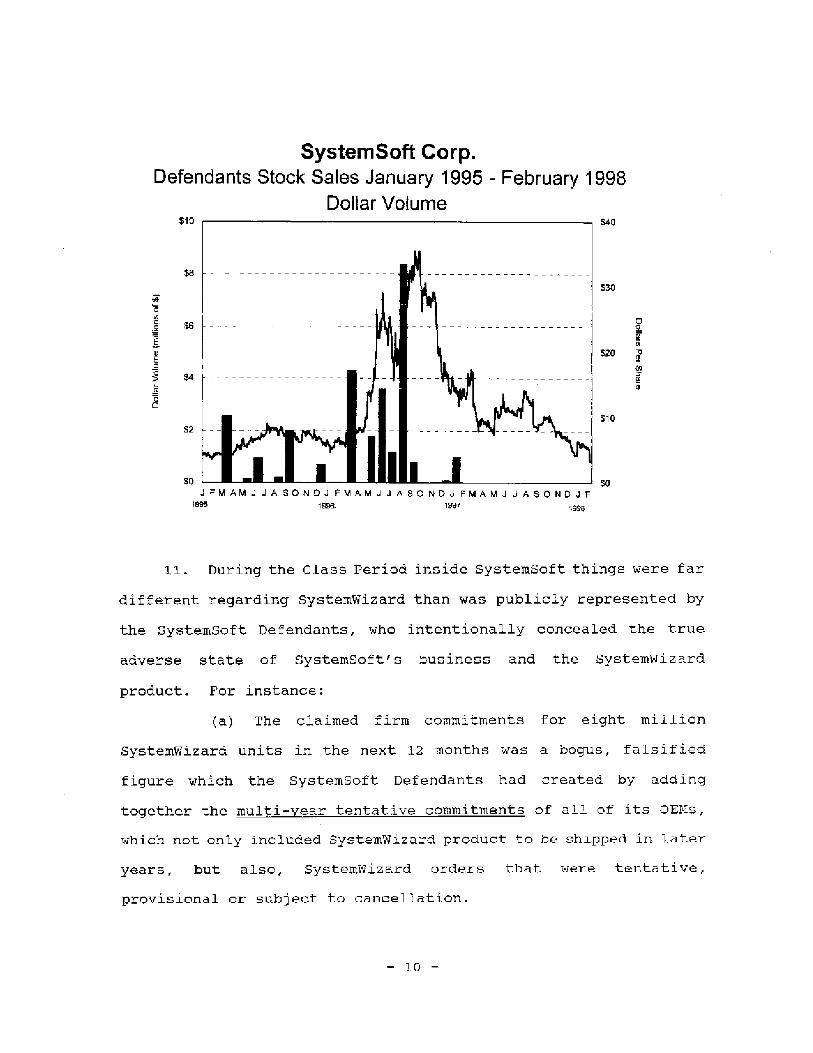

This insider selling was unusual in timing and amount, as the graph

below shows:

//

//

//

//

//

1/

-9-

SystemSoft Corp.Defendants Stock Sales January 1995 - February 1998

Dollar Volume$10 $40

$B $30

aF

1$20

a $4

4Pmr $10$2 -

Iiiml I I 1 J FM AM ... J ASONDJ FMAMJ J ASO NDJ FMAMJJASONDJF

less 1E913 1897 199t3

11. During the Class Period inside SystemSoft things were far

different regarding SystemWizard than was publicly represented by

the SystemSoft Defendants, who intentionally concealed the true

adverse state of SystemSoft's business and the SystemWizard

product. For instance:

(a) The claimed firm commitments for eight million

SystemWizard units in the next 12 months was a bogus, falsified

figure which the SystemSoft Defendants had created by adding

together the multi-year tentative commitments of all of its OEMs,

which not only included SystemWizard product to be shipped in later

years, but also, SystemWizard orders that were tentative,

provisional or subject to cancellation.

- 10 -

(b) The technical service call centers of IBM, Hewlett-

Packard, Compaq and Digital Equipment were all profitable and these

OEMs had little, if any, interest in undercutting their existing

profitable technical service center business by a product like

SystemWizard. This was especially true with respect to Digital

Equipment which, through its Multi-Vendor Technical Services Unit,

provided technical service operations for itself and other large PC

OEMs (including Compaq) and which unit was a highly profitable part

of Digital Equipment's business.

(c) By the spring of 96, SystemSoft had been informed by

Dell and Toshiba that these PC OEMs saw no end-user demand for a

SystemWizard-type product and told SystemSoft that its proposed $5-

$6 per unit pricing was "obscene" and would not result in

deployment of the product with them.

(d) SystemSoft had been told by several PC OEMs,

including Dell, that configuring the necessary server operations at

the OEMs' technical service centers for SystemWizard to work was

far too expensive, complicated and time-consuming for them to

undertake. In order for SystemWizard to work it was necessary for

the PC OEMs to "build a case" for each potential PC malfunction, an

enormously time-consuming and expensive task which could not be

justified in light of the existing technical service centers'

capability to deal with these problems.

(e) That the attempt to deploy SystemWizard at Packard-

Bell was failing and suffering long delays because Packard-Bell's

technical service center was a cheap, skeletal operation where

Packard-Bell had not accumulated in useable form in data base of

prior customer complaints about its PCs and the solutions utilized

- 11 -

and thus, Packard-Bell found it impossible to create a "knowledge

base" of its PC products in its SystemWizard server which was

indispensable to the deployment of SystemWizard in a workable

fashion.

(f) SysterSoft had originally justified the development

and marketing of SystemWizard using an assumed $12 per unit price.

However, by the spring of 96, SystemSoft was aware that competitive

pressures meant that it would not be able to charge more than $5

per unit, which greatly reduced the profitability of the product

line. However, even this fragile pricing structure was destroyed

in mid-96, when a competitor named CyberMedia told PC OEMs of its

new product, known as "First Aid 95," which would perform the same

functions as SystemWizard and that CyberMedia was willing to give

First Aid 95 to OEMs for free and attempt to make money on the

product by selling it to end users. The SystemSoft Defendants knew

this marketing approach from CyberMedia for an equivalent product

doomed SystemWizard. As a result, by the fall of 96, SystemSoft

was reduced to telling OEMs that it would give the SystenWizard

product to them for lengthy free trials and that if the PC OEM

liked the product and saved money as a result of that, SystemSoft

would then try to negotiate a price for the product going forward.

However, PC OEMs, including Dell, refused even to accept that offer

from SystemSoft as that offer would still require the PC OEM to

invest large amounts to create the "knowledge base" necessary for

the SystemWizard server at the PC OEMs' technical service center to

perform its required functions, which investment PC OEMs were very

reluctant to make. Thus, by the fall of 96, SystemWizard had

- 12 -

become a product that SystemSoft literally could not even give

away!

(g) SystemSoft's relationship with Digital Equipment

regarding SystemWizard soured early on. While Digital Equipment

was originally interested in the SystemWizard technology, by the

spring of 96, SystemSoft was chronically delinquent in providing

Digital Equipment with engineering and other documentation Digital

Equipment demanded as necessary to monitor the development of

SystemWizard. This failure created increasing tension between

Digital Equipment and SystemSoft. The deterioration of the

relationship accelerated during 96, as a dispute between SystemSoft

and Digital Equipment over the type of SystemWizard server to be

created for Digital Equipment's Multi-Vendor Service Technical

Services Unit escalated. Because of the unique nature of its

Multi-Vendor Technical Services Unit, Digital Equipment demanded a

specialized type of SystemWizard server different from that

SystemSoft was designing and developing for other PC OEMs, which

specialized SystemWizard server SystemSoft declined to develop

because of the expense and complexity of doing so. SystemSoft's

conduct in this regard, combined with Digital Equipment's growing

realization that SystemWizard, if successful, could undermine its

highly profitable Multi-Vendor Technical Services Unit operation so

soured the SystemSoft/Digital Equipment relationship that, by the

fall of 96, the SystemSoft Defendants knew that Digital Equipment

would never deploy SystemWizard and would terminate its

SystemWizard contract with SystemSoft in the near future.

12. Each of the positive statements about SystemSoft's

business during the Class Period was materially false and

- 13 -

misleading when issued. Defendants also failed to disclose, inter

alia, the following adverse information which was then known only

to Defendants due to their access to internal SystemSoft data and

disclosure of which was required to be made to make the statements

made not misleading:

(a) SystemSoft had hurried the announcement of

SvstemWizard t s development in early 96 in order to blunt criticisms

of its slow pace in developing new products and, at the time of

that announcement, in fact, SystemSoft had not completed sufficient

product development or market analysis to be able to state that

"the first products are scheduled to ship to system manufacturers

in the second quarter of 1996" or that SystemSoft would be able "to

rapidly bring this new category of call avoidance software to

market";

(b) Based upon communications with PC OEMs, the

SystemSoft Defendants knew that the market potential for

SystemWizard was nowhere near as large as represented and that most

of the large OEMs were satisfied with the status quo because

service calls gave them a chance to sell additional product to

users and were actually generating profits for them;

(c) Based upon communications with PC OEMs, the

SystemSoft Defendants knew that PC OEMs did not have anywhere near

the level of interest in deploying SystemWizard as SystemSoft was

representing and that the most important, major PC OEMs,

Compaq, Dell, Gateway and IBM, were extremely dubious about and

reluctant to license the product, and SystemSoft was only able to

service the OEM agreements it did have by agreeing to barter

transactions wherein SystemSoft would agree to accept old Pc

- 14 -

equipment in exchange for SystemWizard and by promising positions

at SystemSoft to OEM employees, including those at DEC, Hewlett-

Packard and Packard Bell;

(d) Based on marketing studies and other evaluations of

the SystemWizard product they had made, the SystemSoft Defendants

knew that there was no possibility that PC OEMs would ever pay $5

or $6 per SystemWizard unit in large volume transactions and thus

the revenue and profit potential of the SystemWizard product was

actually far less than SystemSoft was forecasting;

(e) SystemSoft did not have firm commitments from PC

OEMs to order eight million SystemWizard units in the next 12

months and, in fact, had agreed to provide millions of units to PC

OEMs for free to evaluate or test consumer reaction or on a

deferred pay basis;

(f) Due to the difficulties PC OEMs were encountering in

integrating SystemWizard into their PC products and establishing

necessary technical arrangements to accept and process service

calls from SystemWizard, the SystemSoft Defendants knew that volume

deployment of SystemWizard by PC OEMs would be materially delayed

even with those PC manufacturers that had agreed to utilize the

product. They knew that as a result SystemSoft's revenue from

SystemWizard during F98 would be far less than what was being

forecasted;

(g) None of the PC OEMs who had purportedly agreed to

utilize SystemWizard were actually firmly committed to purchase any

specific quantity of the product, but rather, only to accept

shipments for evaluation and, in fact, during such evaluation

process the OEMs were expressing considerable dissatisfaction with

- 15 -

the product, both in terms of its technical capabilities and its

cost benefit justification;

(h) Because SystemWizard was achieving extremely limited

success with PC OEMs, this product was not vastly expanding

SystemSoft's potential marketplace by opening up deskto p computers

to it. Defendants knew that, in fact, SystemSoft remained a

company dependent upon selling its products into the smaller and

slower-growing mobile or laptop part of the computer industry and

thus did not have the prospects for revenue and BPS growth being

represented;

(i) SystemSoft was not, in fact, achieving consistent

strong quarterly revenue and EPS growth as represented; but rather,

its revenues were stagnating and it was concealing the stagnation,

falsifying and manipulating its financial results by improperly

recording revenue from its Digital EguipmentiSystemWizard

development contract and from its Asian distributor and

restructuring its agreement with Intel to accelerate payments (and

revenue) from later quarters to show revenue and BPS growth during

the Class Period;

(j) SystemSoft's streak of record quarterly revenues and

BPS was not the result of the strong demand for or broad customer

acceptance of its core products as represented; but rather, was due

to the deliberate falsification of SystemSoft's financial results

by improperly recording revenue on its Digital Equipment/

SystemWizard contract and on shipments to its Asian distributor, as

detailed in T583-97;

(k) SystemSoft's revenues and EPS for the 4thQ F96 and

the lstQ, 2ndQ and 3rdQ F97 were each artificially inflated and

- 16 -

falsified due to the manipulation of SystemSoft's accounting by

improperly recording revenue on the Digital Equipment/SystemWizard

contract and on shipments to its Asian distributor, as detailed in

¶TB3-97;

(1) SystemSoft was having significant disagreements with

Digital Equipment about the development of and potential for

SvstemWizard and that product's commercial success and it was very

likely Digital Equipment would cancel its SystemWizard development

and marketing contract with SystemSoft, thus triggering a multi-

million dollar liability of SystemSoft to Digital Equipment;

(m) SystemSoft's USB software product was not ahead of

the competition, had created little, if any, customer interest and

virtually no sales, would produce little, if any, revenue in F98,

and would likely have to be sold or spun-off, creating a signifi-

cant write-down of SystemSoft's investment in that product;

(n) Demand for SystemSoft's core products, especially

CardWizard, was softening such that Defendants knew that the rate

of growth in sales of that product would decline dramatically in

the coming months in part because IBM would not order any

CardWizard products until well into F98;

(o) SystemSoft was improperly capitalizing development

costs for SystemWizard and its USE software, as it did not have any

adequate basis to believe, forecast or estimate that it would

recover those costs in the reasonably foreseeable future from sales

of the SystemWizard product at profitable prices; and

(p) As a result of the foregoing negative factors which

were negatively impacting SystemSoft's business, the SystemSoft

Defendants actually knew that the forecasts of strong revenue and

- 17 -

EPS growth during F98 due to continued strong growth and

SystemSoft's core product line, plus accelerating sales of

SystemWizard, were false when made as those forecasted results were

unachieveable.

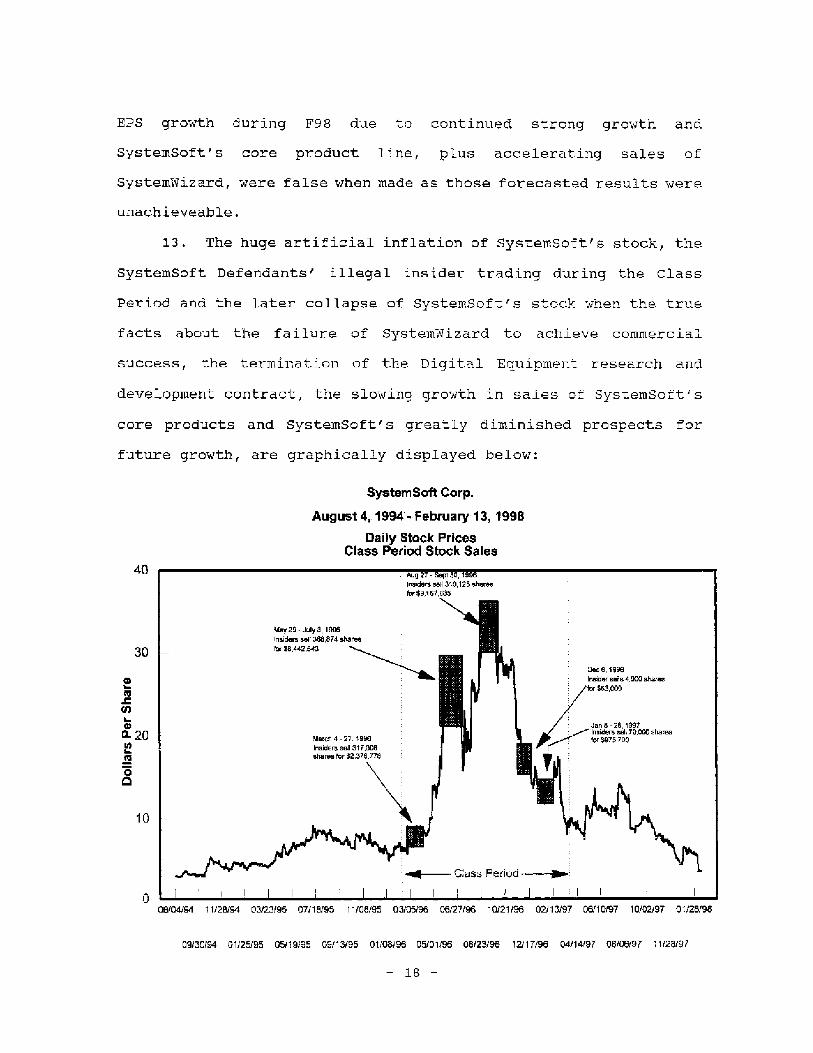

13. The huge artificial inflation of SystemSoft's stock, the

SystemSoft Defendants' illegal insider trading during the Class

Period and the later collapse of SystemSoft's stock when the true

facts about the failure of SystemWizard to achieve commercial

success, the termination of the Digital Equipment research and

development contract, the slowing growth in sales of SystemSoft's

core products and SystemSoft's greatly diminished prospects for

future growth, are graphically displayed below:

System Soft Corp.

August 4,1994 - February 13, 1998

Daily Stock PricesClass Period Stock Sales

40 . Aug 27 - Sept 30, 1996Inas:Jars sefi 3%125 shamsfor S5,187.085

May 29 - July 3, 1096insiders selr 388,874 shame

30 — for S8,442,643

Dee 8, 190SInsider seas 4.005 sharesfor 58.3.886

Cl,

Jan 8 - 28, 1997

el- 20 Mar& 4-27 1£196r..........„.„.n ;noistmeloi070.000 shares

Insiders sell 317,008 .

shares Ter $2,378.778 y

0

10 —

• -40— ss Per bci

0 1'I 1 1 1 I' 1 1 :1 1 1 1 + 1 1 1 1 • 1 1

08/04/94 11/2/94 03/23/95 07/18/95 11/08/95 03/05/95 06/27/96 10/21/96 02113/97 06/10/97 10102197 01/28/98

09130194 01125195 05/19(95 09/13195 0108/96 05/01/96 08/23196 12/17/96 04/14/97 08106/97 11/28197

- 18 -

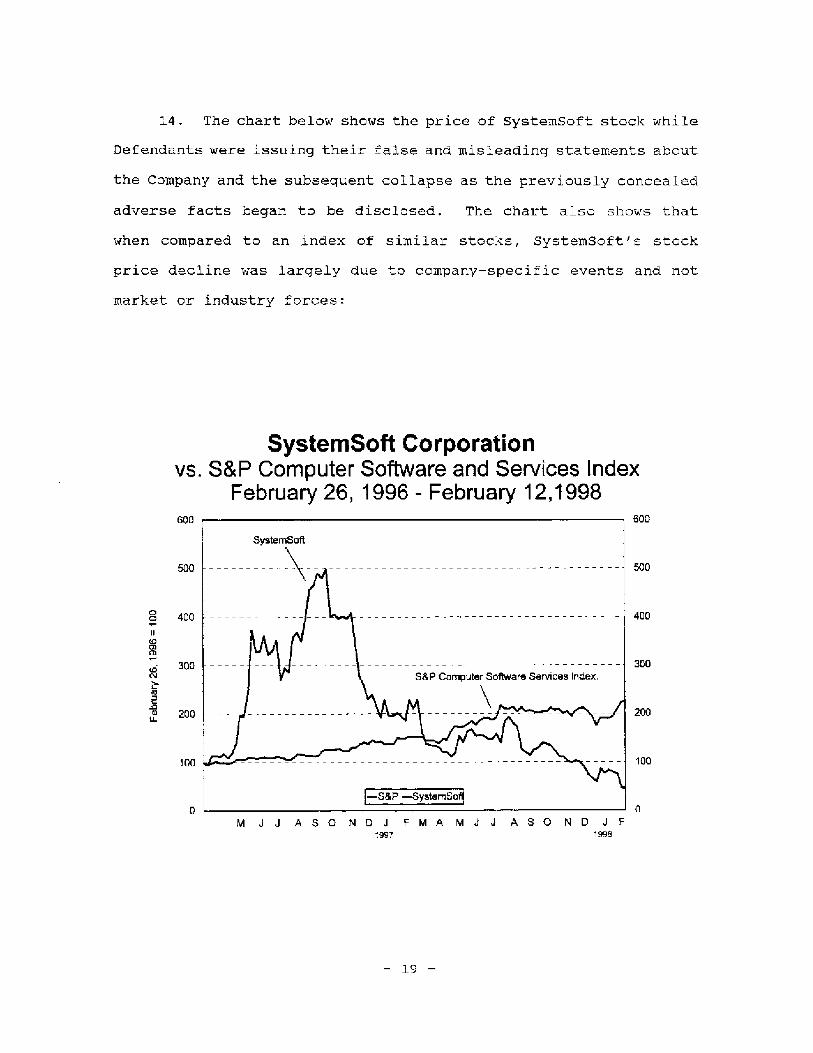

14. The chart below shows the price of SystemSoft stook while

Defendants were issuing their false and misleading statements about

the Company and the subsequent collapse as the previously concealed

adverse facts began to be disclosed. The chart also shows that

when compared to an index of similar stocks, SystemSoft's stock

price decline was largely due to company-specific events and not

market or industry forces:

SystemSoft Corporationvs. S&P Computer Software and Services Index

February 26 1996 - February 12,1998

600 600

SystemSoft

500 500

ao 400 400

a)6 300 300

S&P Computer Software Services Index.QC;

1) 200 200

100 100

1—S&P --SystemSol

0 0J J ASO NDJ FMA MJ J ASO ND J5

1997 1998

— 19 —

JURISDICTION AND VENUE

15. The claims asserted herein arise under §510(b) and 20(a)

of the Securities Exchange Act of 1934 ("Exchange Act"), 15 U.S.C.

SS78j(b) and 78t(a), and Rule 10b-5, 17 C.F.R. S240.10b-5.

16. Jurisdiction is conferred by §27 of the Exchange Act, 15

U.S.C. 578aa, and 28 U.S.C. §1331.

17. Venue is proper in this District pursuant to §27 of the

Exchange Act, and 28 U.S.C. §1391(b). SystemSoft is headquartered

in this District. The false and misleading statements were made or

issued from this District and most of the Individual Defendants

live here. Thus, most of the acts and transactions giving rise to

the violations of law complained of occurred in this District.

THE PARTIES

18. (a) Plaintiff Thomas P. Gorman purchased 2,000 shares of

SystemSoft common stock on 5/3/96 at $27.67 per share, and was

damaged thereby.

(b) Plaintiff Barrett Herriott purchased 400 shares of

SystemSoft common stock on 12/23/96 at $14.94 per share, 100 shares

on 1/22/97 at $12.61 per share and 300 shares on 1/22/97 at $11.46

per share, and was damaged thereby.

(c) Plaintiff Lori Lyman purchased 300 shares of

SystemSoft common stock on 1/16/97 at $14.52 per share, and was

damaged thereby.

(d) Plaintiff Albert Halegoua purchased 6,000 shares of

SystemSoft common stock on 3/29/96 at $7.69 per share, 1,400 shares

on 6/19196 at $24.50 per share, 1,000 shares on 10/8/96 at 529.50

per share, 1,500 shares on 12/10/96 at $18-1/8 per share and 1,000

shares on 1/24/97 at $14-1/4 per share, and was damaged thereby.

- 20 -

(e) Plaintiff Ronald Offner purchased 300 shares of

SystemSoft common stock on 11/27/96 at $21 per share, and was

damaged thereby.

(f) Plaintiff Fred Cohen purchased 300 shares of

SystemSoft common stock on 12/6/96 at $17 per share, and was

damaged thereby.

19. Defendant SystemSoft maintains its headquarters

Natick, Middlesex County, Massachusetts. During the Class Period,

SystemSoft's common stock traded in an efficient market on the

NASDAQ National Market System.

20. (a) Defendant Robert F. Angelo ("Angelo") was, during

the Class Period, President, Chief Executive Officer, Chief

Operating Officer and Chairman of the Board of the Company.

Angelo, by reason of his stock ownership, management position, and

membership on SystemSoft's Board, was a controlling person of

SystemSoft and had the power and influence, and exercised the same,

to cause it to engage in the illegal conduct complained of herein.

During the Class Period and as part of the fraudulent scheme,

Angelo sold 248,882 shares of SystemSoft stock at prices as high as

$31-3/4 per share based on inside information, pocketing over $3.9

million. These sales constituted 74% of Angelo's holdings in

SystemSoft. Angelo was also given cheap stock options on 50,000

SystemSoft shares as a reward for helping to falsify SystemSoft's

F97 results and artificially inflating SystemSoft's stock during

F97. Angelo's stock sales during the Class Period were unusual in

timing and amount as set forth below:

- 21 -

SystemSoft Corp.Defendant R. Angelo Class Period Sales

$1400 $40

$1200

^$1000

$800

$3$2:21'6 $600

n_ $400 116 $10

$200

$0 $0FMAMJJASONDJFMAMJJA3ONCIJFMAMJJASONDJF

1995 is 197 1 NS

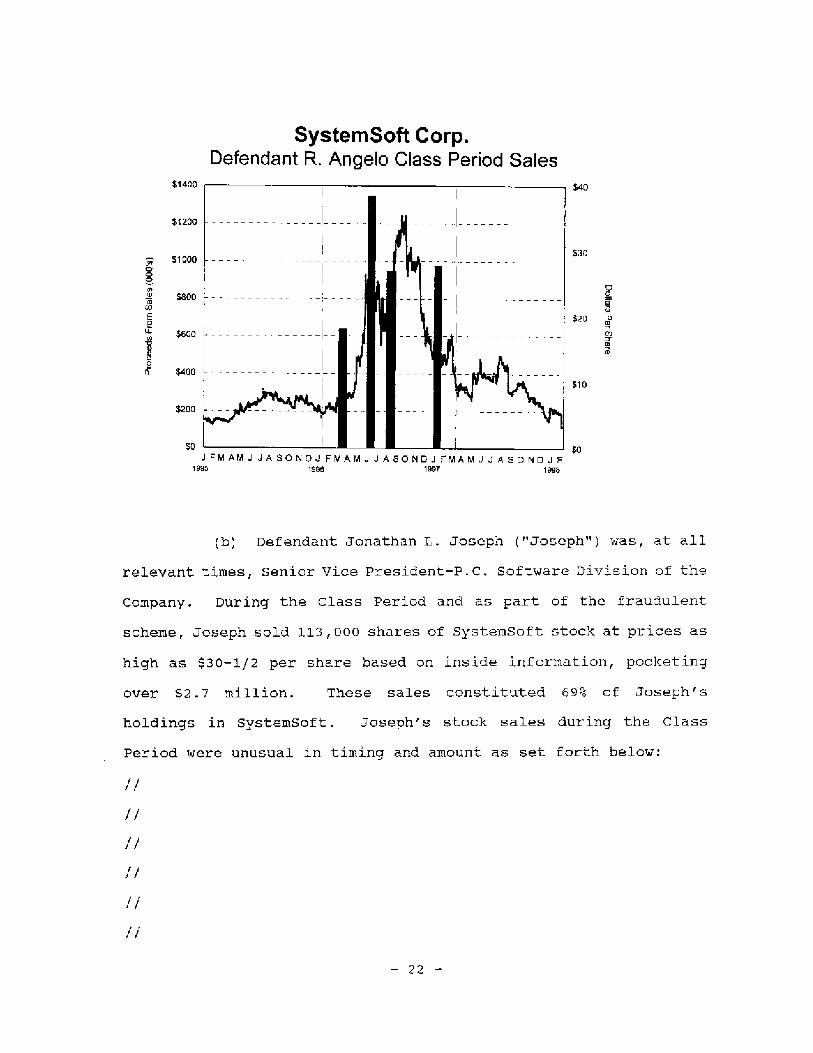

(b) Defendant Jonathan L. Joseph ("Joseph") was, at all

relevant times, Senior Vice President-P.C. Software Division of the

Company. During the Class Period and as part of the fraudulent

scheme, Joseph sold 113,000 shares of Systemsoft stock at prices as

high as $30-1/2 per share based on inside information, pocketing

over $2.7 million. These sales constituted 69% of Joseph's

holdings in SystemSoft. Joseph's stock sales during the Class

Period were unusual in timing and amount as set forth below;

//

I-

II

//

//

- 22 -

SystemSoft Corp.Defendant J. Joseph Class Period Sales

$1400 $40

$1200

$30$1000

0a"

hiss441‘[141j(if\v1 $20 -,vu

$800

1 J $400

lip.444N $1 0

•

$200

so .1 FMAMJ JASONDJ FMAMJJ ASONDJ FlulAMJ J ASO NO.IF

1995 19943 :997 1998

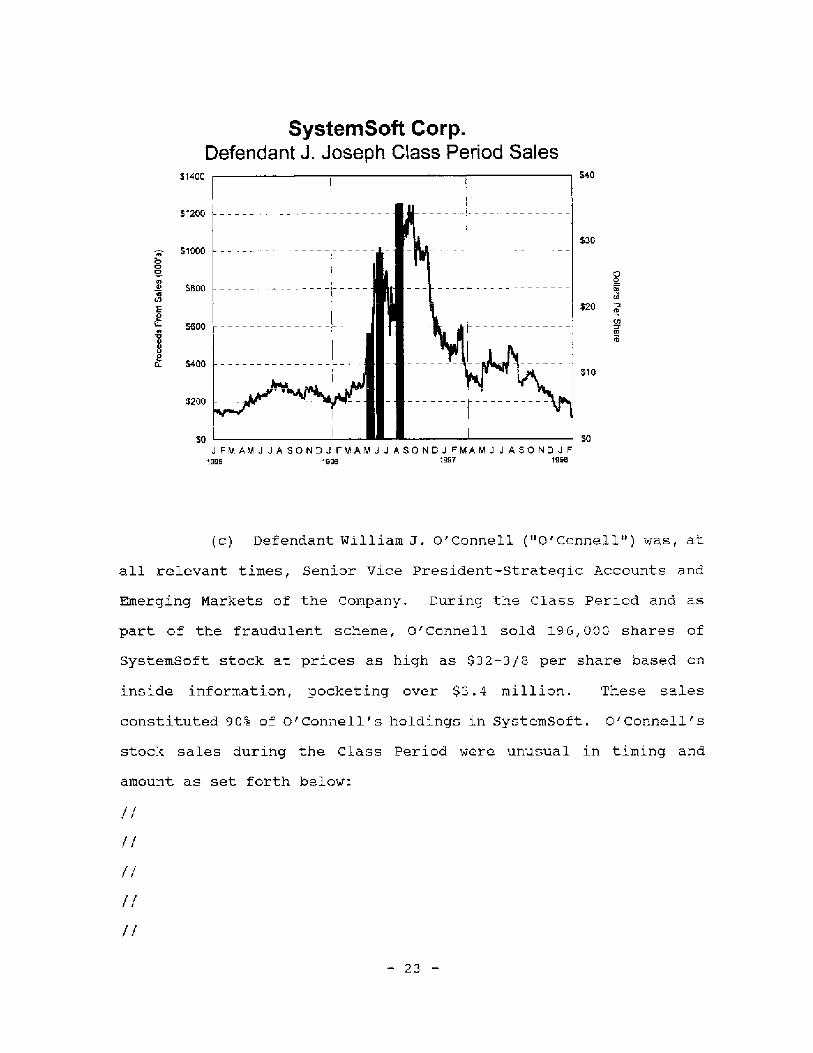

(c) Defendant William J. O'Connell ("O'Connell") was, at

all relevant times, Senior Vice President-Strategic Accounts and

Emerging Markets of the Company. During the Class Period and as

part of the fraudulent scheme, o'connell sold 196,000 shares of

SystemSoft stock at prices as high as $32-3/8 per share based on

inside information, pocketing over $3.4 million. These sales

constituted 90% of O'Connell's holdings in SystemSoft. O'Connell's

stock sales during the Class Period were unusual in timing and

amount as set forth below:

//

//

//

//

//

- 23 -

SystemSoft Corp.Defendant W. O'Connell Class Period Sales

12000 $40

$1500 $30

8

1-1

4141441P1 It'

a $1000 h $20

3

$500 $10

$0 $0JFMAMJJASONDJFMAMJJASONDJFMAMJ.,ASONDJF

10E+5 1g96 'S97 1998

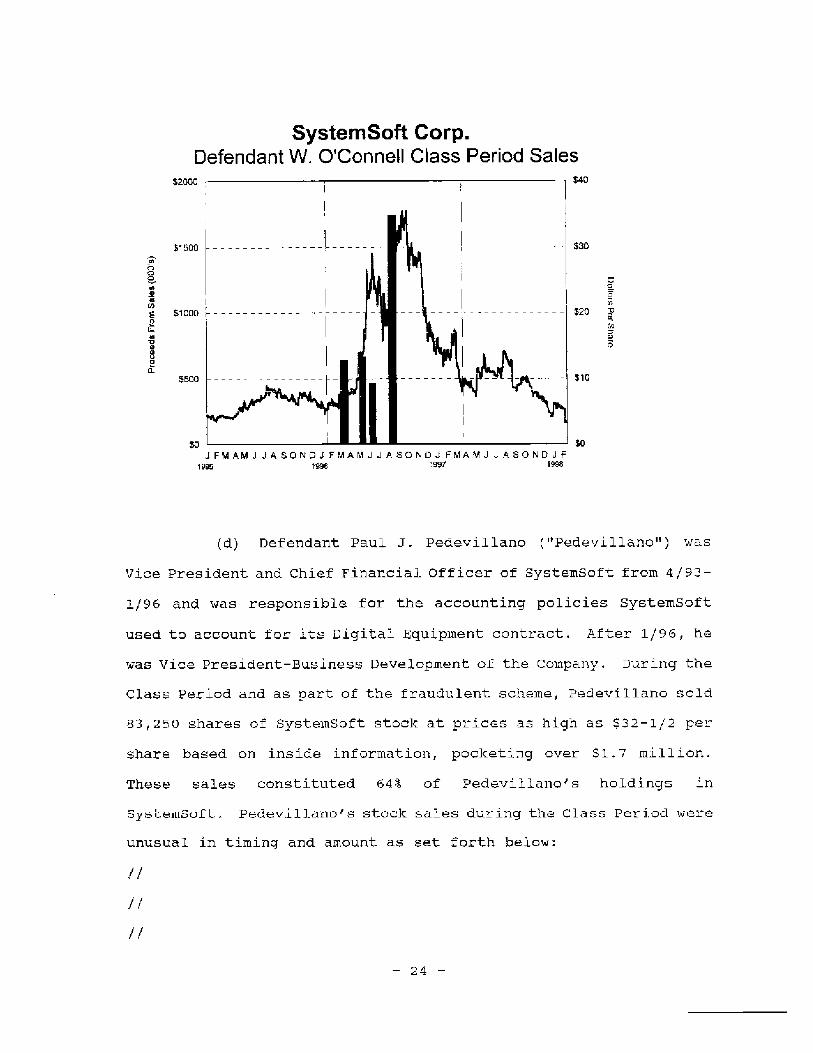

(d) Defendant Paul J. Pedevillano ("Pedevillano") was

Vice President and Chief Financial Officer of SystemSoft from 4/93-

1/96 and was responsible for the accounting policies SystemSoft

used to account for its Digital Equipment contract. After 1/96, he

was Vice President-Business Development of the Company. During the

Class Period and as part of the fraudulent scheme, Pedevillano sold

83,250 shares of SystemSoft stock at prices as high as $32-1/2 per

share based on inside information, pocketing over $1.7 million.

These sales constituted 64% of Pedeviliano's holdings in

SystemSoft- Pedevillano's stock sales during the Class Period were

unusual in timing and amount as set forth below:

//

//

//

- 24 -

SystemSoft Corp.Defendant P. Pedevillano Class Period Sales

$1200 $40

$1000

$30

$1300

@ae $80u $20IL

$400 \i/11\t44(16411111A. $10$200 wir jp,"4/14,10,

$0 II $0JFMAMJ.,ASONDJFMAMJJASONDJFMAMJJASONDJF

199S 1998 t997 1998

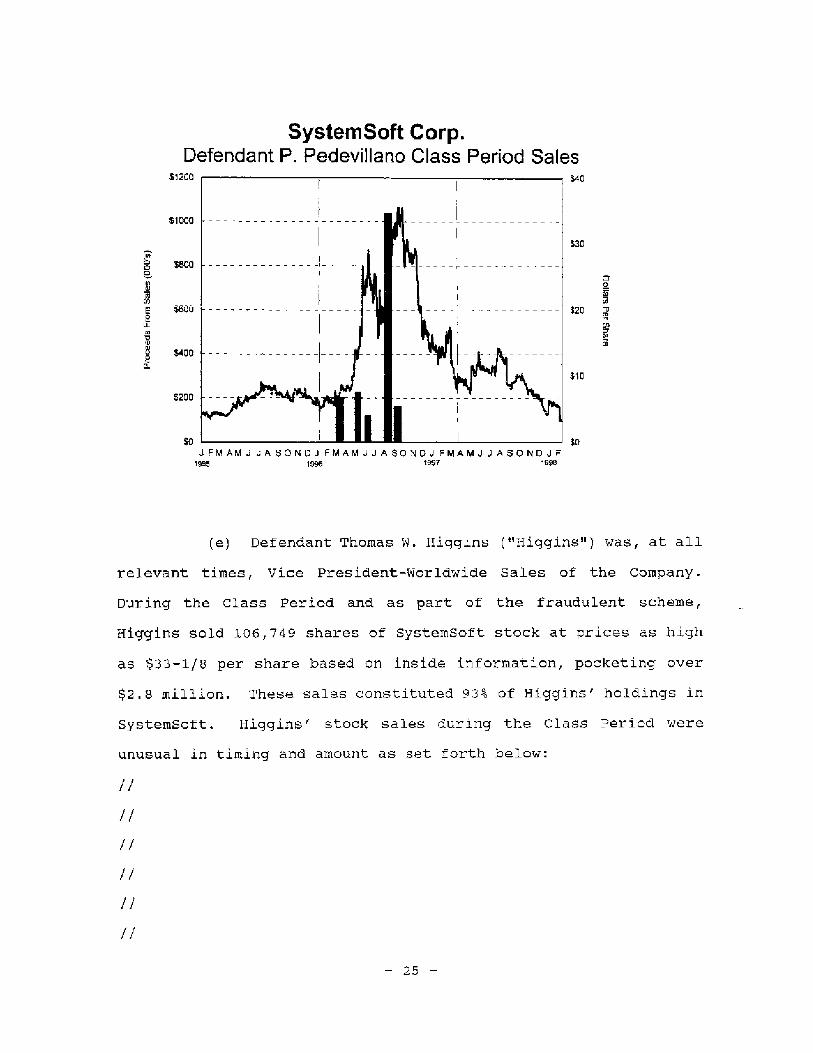

(e) Defendant Thomas W. Higgins ("Higgins") was, at all

relevant times, Vice President-Worldwide Sales of the Company.

During the Class Period and as part of the fraudulent scheme,

Higgins sold 106,749 shares of SystemSoft stock at prices as high

as $33-1/8 per share based on inside information, pocketing over

$2.8 million. These sales constituted 93% of Higgins' holdings in

SystemSoft. Higgins' stock sales during the Class Period were

unusual in timing and amount as set forth below:

//

//

//

//

//

//

- 25 -

SystemSoft Corp.Defendant T. Higgins Class Period Sales

$2500 $40

$2000 I-$30

$1500 Crg_

TO

$202

$1000 ro

$10

$500 I — -

$0 $0,FMAMJ JA SON01 FPAAMJ J ASONDJ FMAMJ .1 A SONDJ F

1995 toe 1997 1999

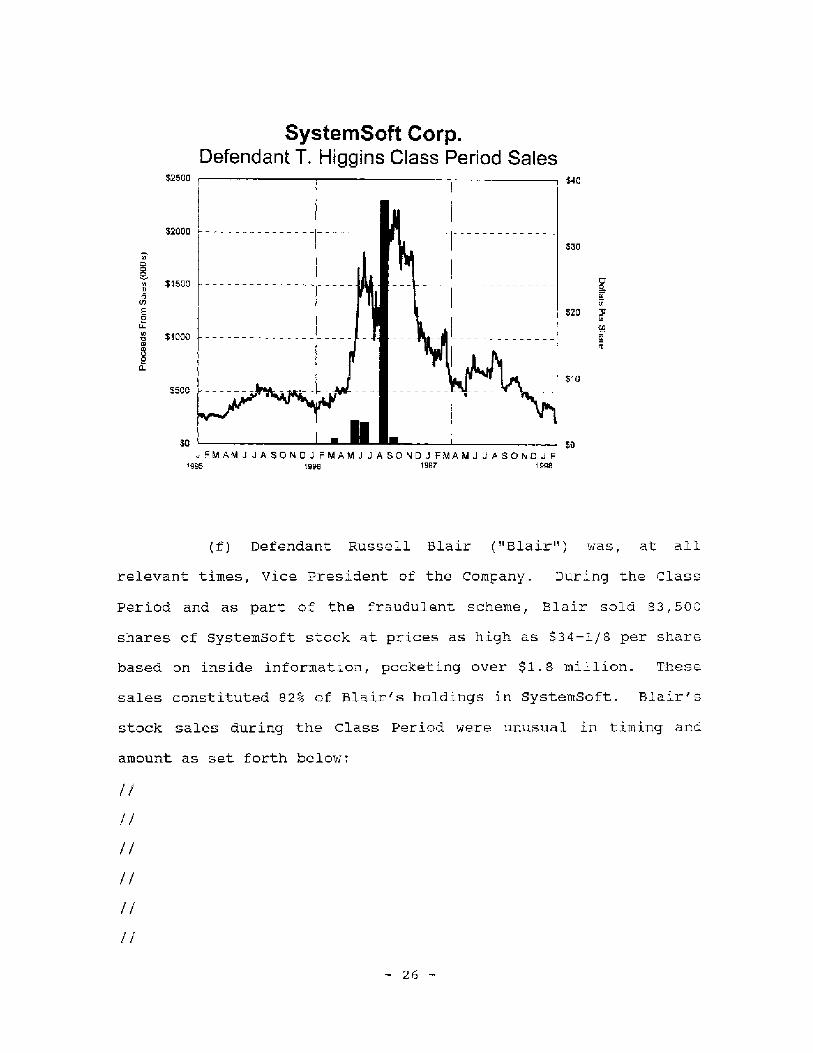

(f) Defendant Russell Blair ("Blair") was, at all

relevant times, Vice President of the Company. During the Class

Period and as part of the fraudulent scheme, Blair sold 83,500

shares of SystemSoft stock at prices as high as S34-1/8 per share

based on inside information, pocketing over $1.8 million. These

sales constituted 82% of Blair's holdings in SystemSoft. Blair's

stock sales during the Class Period were unusual in timing and

amount as set forth below:

1/

//

//

I-

1/

//

- 26 -

SystemSoft Corp.Defendant R. Blair Class Period Sales

$6,00 $40

$500 -

$3C

$400

a

E $:300 - $20 T,

5$200

-11111 111111111,111411\vol S 10$100

L ..I FM AM.) JASONDJ FMANI,J .1 A SONDJ FMAMJJ ASONDJ F

1995 1996 1997 1L

(g) Defendant David Sommers ("Sommers") was, at all

relevant times, Vice President-Finance, Treasurer and Chief

Financial Officer of the Company. During the Class Period, Sommers

did not sell any shares of SystemSoft stock because he owned no

shares outright and during the Class Period had almost no vested

stock options he was able to exercise and sell. However, Sommers

was paid a cash bonus for helping to falsify SystemSoft's F97

results and artificially inflate its stock price.

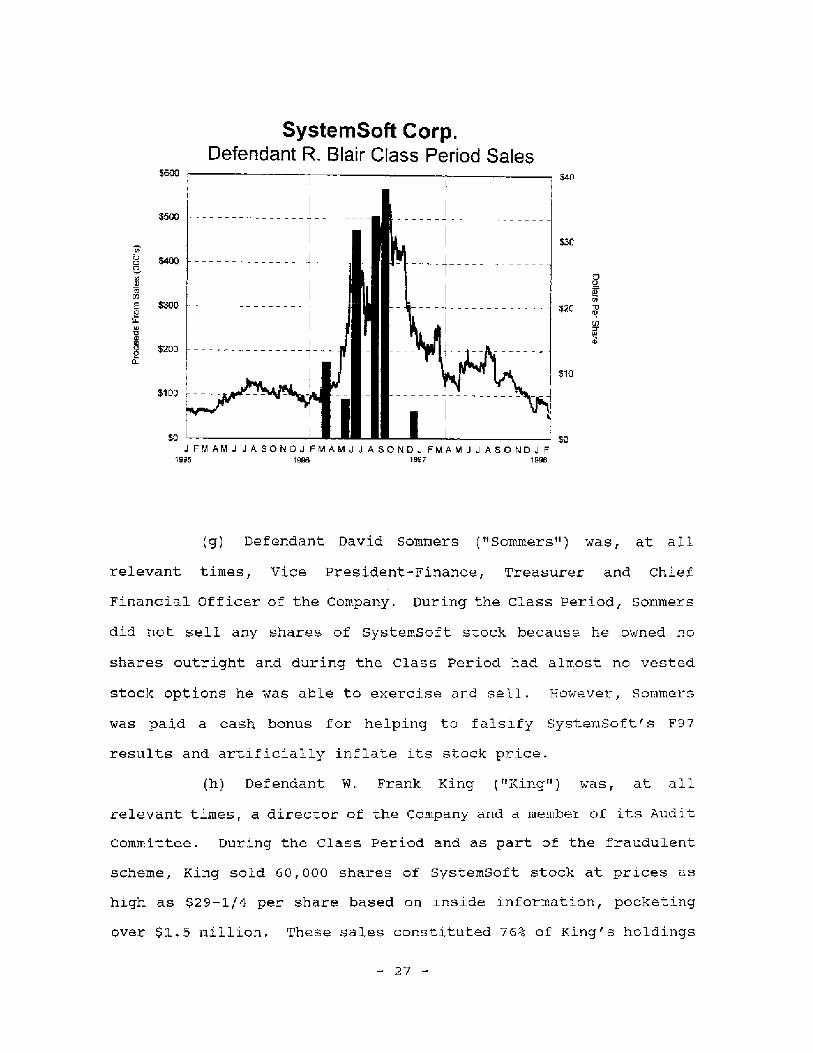

(h) Defendant W. Frank King ("King") was, at all

relevant times, a director of the Company and a member of its Audit

Committee. During the Class Period and as part of the fraudulent

scheme, King sold 60,000 shares of SystemSoft stock at prices as

high as $29-1/4 per share based on inside information, pocketing

over $1.5 million. These sales constituted 76% of King's holdings

- 27 -

in SystemSoft. King's stock sales during the class Period were

unusual in timing and amount as set forth below:

SystemSoft Corp.Defendant F. King Class Period Sales

$1200 $40

$/000

$30

8 Um r

'4 3

E $600 $20 -0

$400 1- \\SI $10

$200

SD $0JFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJF

1995 199e 1997 1998

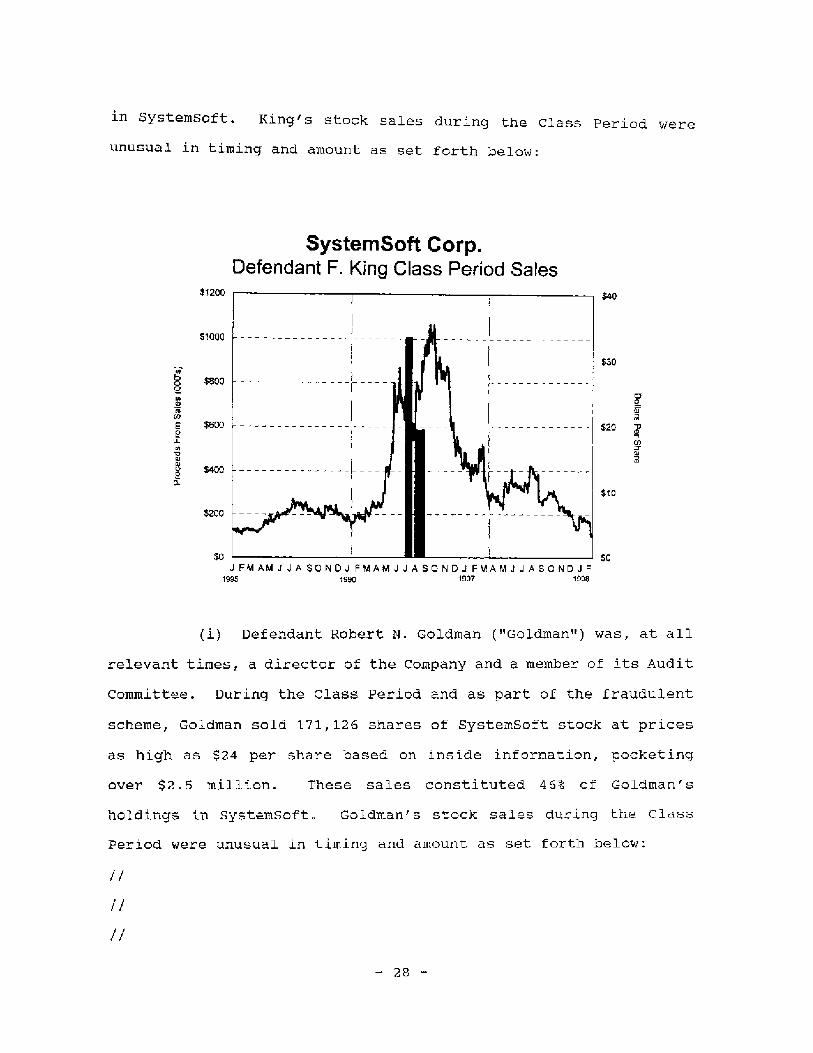

(i) Defendant Robert N. Goldman ("Goldman") was, at all

relevant times, a director of the Company and a member of its Audit

Committee. During the Class Period and as part of the fraudulent

scheme, Goldman sold 171,126 shares of SystemSoft stock at prices

as high as $24 per share based on inside information, pocketing

over $2.5 million. These sales constituted 46% of Goldman's

holdings in SystemSoft. Goldman's stock sales during the Class

Period were unusual in timing and amount as set forth below:

//

//

//

- 28 -

SystemSoft Corp.Defendant R. Goldman Class Period Sales

$3000 $40

$2500-

1111\kitseivakiNtill $30$2on 0

$15W $20 ;

$1000 L

$10

$500

$0 $0JFMAMJJASONJELIFMANIJJASONDJFMAMJIASONDJF

1995 19E6 1997

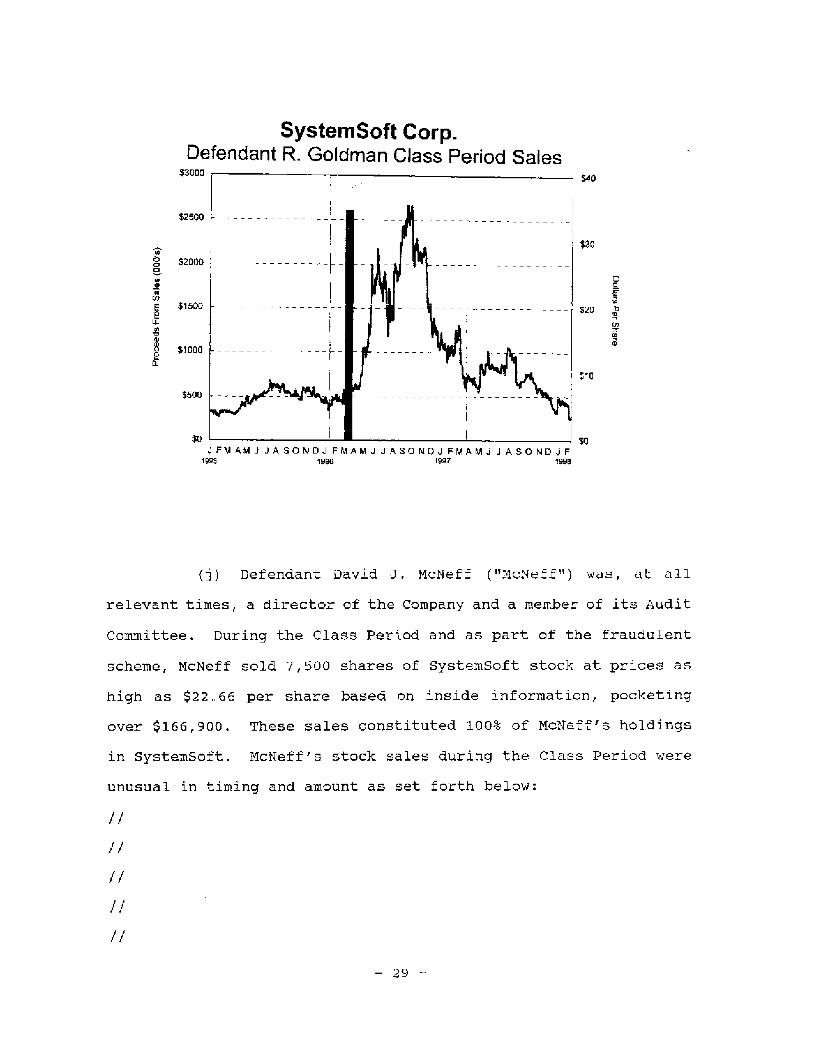

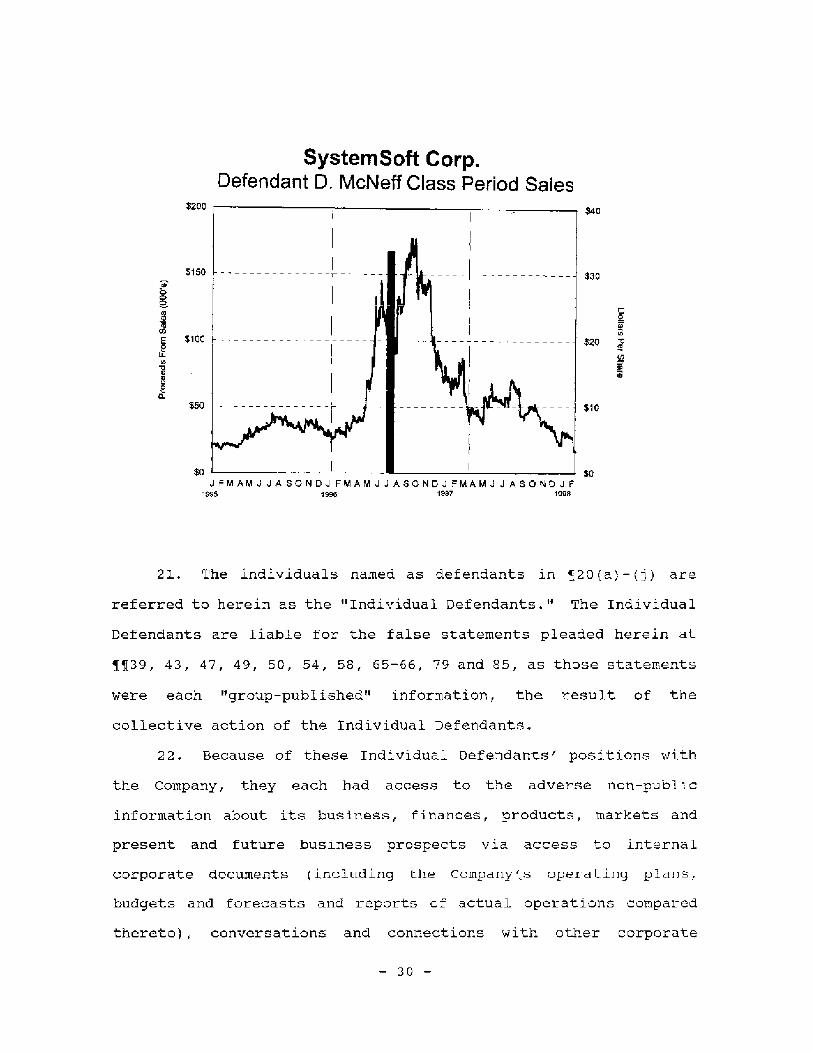

(j) Defendant David J. McNeff ("McNeff") was, at all

relevant times, a director of the Company and a member of its Audit

Committee. During the Class Period and as part of the fraudulent

scheme, McNeff sold 7,500 shares of SystemSoft stock at prices as

high as $22.66 per share based on inside information, pocketing

over $166,900. These sales constituted 100% of MoNeff's holdings

in SystemSoft. McNeff's stock sales during the Class Period were

unusual in timing and amount as set forth below:

//

//

//

//

//

- 29 -

System Soft Corp.Defendant D. McNeff Class Period Sales

$200 $40

$150

_

$39I

a

$100 - 320 -0ti7

- $10

So sa.1 FMAMJ JA SONDJ FMAMJJASONDJFMAMJ JASONDJF

lase 19s7

21. The individuals named as defendants in 4:20(a)-(j) are

referred to herein as the "Individual Defendants." The Individual

Defendants are liable for the false statements pleaded herein at

11139, 43, 47, 49, 50, 54, 58, 65-66, 79 and 85, as those statements

were each "group-published" information, the result of the

collective action of the Individual Defendants.

22. Because of these Individual Defendants' positions with

the Company, they each had access to the adverse non-public

information about its business, finances, products, markets and

present and future business prospects via access to internal

corporate documents (including the Company's operating plans,

budgets and forecasts and reports of actual operations compared

thereto), conversations and connections with other corporate

— 30 —

officers and employees, attendance at management and/or Board of

Directors' meetings and committees thereof and via reports and

other information provided to them in connection therewith.

23. SystemSoft's Board had an Audit Committee which oversaw

the accounting and financial functions of the Company and consulted

with and reviewed the services provided by the Company's indepen-

dent auditors It met four times during 797. Goldman, King and

McNeff were the members of the Audit Committee.

24. The Individual Defendants, because of their positions

with the Company, controlled and/or possessed the power and autho-

rity to control the contents of its quarterly and annual reports,

press releases and presentations to securities analysts, which

information was conveyed through the analysts to the investing

public. Each of these defendants was provided with copies of the

Company's reports and press releases alleged herein to be mislead-

ing prior to or shortly after their issuance and had the ability

and opportunity to prevent their issuance or cause them to be

corrected. Because of their positions and access to material

non-public information each of these defendants knew that the

adverse facts specified herein had not been disclosed to and were

being concealed from the public and that the positive represen-

tations which were being made were then materially false and

misleading. Despite their duty not to sell their SystemSoft stock

under such circumstances, these defendants nonetheless did so.

25. Defendant Coopers & Lybrand LLP ("Coopers & Lybrand") is

a firm of certified public accountants. Coopers & Lybrand was

engaged by Systemsoft to provide independent accounting, business

consulting and auditing services to SystemSoft and gave SystemSoft

- 31 -

accounting advice and consultation regarding SystemSoft's annual

and quarterly reports which were filed with the SEC and publicly

distributed. Coopers & Lybrand consented to its unqualified

opinions on SystemSoft's F96 financial statements being included in

SystemSoft's F96 Report on Form 10-K and Annual Report to

Shareholders. Coopers & Lybrand directly participated in and

worked with SystemSoft to develop the bogus rationales for

SystemSoft's accounting practices for the Digital Equipment

contract, knowing that there was no reasonable basis for these

accounting practices. As a result, Coopers & Lybrand was not

independent with respect to auditing or reviewing SystemSoft's

financial statements or opining thereon, as Coopers & Lybrand was,

in effect, auditing its own work and had a stake in justifying the

correctness of accounting practices that enabled SystemSoft to

inflate its net income and EPS during the Class Period and its

underlying justifications that Coopers & Lybrand had helped create.

Coopers & Lybrand rendered false opinions on SystemSoft's F96

financial statements for the year ended 1/31/96. Coopers & Lybrand

also reviewed SystemSoft's financial results for each of the

interim quarters of F97, ended 4/31/96, 7/30/96 and 10/31/96 and

approved all these interim financial statements as filed with the

SEC and distributed to the public, knowing of their falsity.

SCIENTER ALLEGATIONS

Actual Knowledge

26. Angelo, Joseph, O'Connell, Pedevillano, Higgins, Blair

and Sommers were the top operating officers of SystemSoft. They

had daily contact with each other, as these individuals ran

SystemSoft's business on a daily basis as hands-on managers, having

- 32 -

constant contact with each other to discuss and deal with the most

important issues facing SystemSoft's business, i.e., the

development, marketing and sales of SystemWizard, SystemSoft's

Digital Equipment relationship and sales of its core products,

especially CardWizard.

27. Defendants King, Goldman and McNeff were each directors

and members of the Audit Committee of SystemSoft. These defendants

were much more involved in the management of SystemSoft than would

ordinarily have been the case with outside directors. SystemSoft

had a small Board of Directors which consisted only of these three

defendants, plus Angelo, and thus the Board was very small and

operated as a cohesive group. In addition, because SystemSoft's

business was small, these three directors were in a position to and

in fact did oversee its operations on an ongoing basis. As such,

these directors were intimately familiar with the details of the

Digital Equipment contract and the decision not to disclose the

complete terms of that contract to the public or file it as an

exhibit to SystemSoft's major SEC filings during the Class Period.

As members of the Audit Committee they also participated in the

deliberate decision which was made to misaccount for the Digital

Equipment contract by having SystemSoft recognize millions in

revenue from that contract during F96/F97, even though under the

terms of that contract, no such revenue could properly be

recognized. Similarly, these three defendants, as intimately

involved directors and members of the Audit Committee, were aware

of the problems that SystemSoft was having with its Asian

distributor and that termination of that distributor was inevitable

- 33 -

and would result in the delayed recognition of millions of dollars

of uncollectible accounts receivable.

28. Also, because of their active roles as members of the

small and intimately involved Board of Directors, these three

defendants were aware that the SystemWizard product had been

announced prematurely by the Company and that the product did not

have anywhere near the market potential the Company w as

representing it had. Further, they knew from reports they received

as directors that deployment of the product, even by those PC OEMs

that had ordered it, would be materially delayed and that it was

extremely unlikely that any of the major PC OEMs would ever order

the product in large volumes or deploy in on a full-scale basis.

29. Because of their top executive positions with SystemSoft

and involvement in the day-to-day management of its business,

defendants Angelo, Joseph, O'Connell, Pedevillano, Higgins, Blair,

King, Goldman, McNeff and Sommers each actually knew the adverse

non-public information about the delay in development and

deployment of SystemWizard, the Company's most important new

product, softening demand for its core products, including

CardWizard, the failure of the Digital Equipment partnership, the

falsifying of SystenSoft's financial results and its poor future

revenue and EPS prospects from internal corporate documents and

conversations with other corporate officers and employees and their

attendance at management and Board meetings.

30. Because vastly increased sales of SystemWizard and US8

products, continued strong growth in sales of CardWizard and

continuation of the Digital Equipment relationship were

indispensable to SystemSoft meeting its internally budgeted and

- 34 -

publicly forecast F97 revenue and EPS, each of the Individual

Defendants focused on and constantly monitored each of these key

factors affecting SystemSoft's business.

31. SystemSoft desperately needed to generate additional

revenue in order to keep its supposed streak of quarterly revenue

and EPS growth intact. However, demand for its core products was

softening and therefore the rate of growth in revenue of

products was not sufficient to enable SystemSoft to achieve revenue

and EPS growth on that basis alone. Moreover, any significant

revenue from SystemWizard was far oft in the future, due to the

delays in deployment of that product which were occurring with the

OEMs that had ordered it and the lack of significant revenue

prospects from major OEMs that were decidedly uninterested in the

product. Thus, in order to keep its apparent record of revenue and

EPS growth intact until it could try to supplement its revenues and

EPS with SystemWizard revenues, SystemSoft's insiders decided to

record and report as revenue payments made to SystemSoft by Digital

Equipment under the SystemSoft/Digital Equipment SystemWizard

contract. However, under the terms of the SystemSoft/Digital

Equipment contract, the payments being made by Digital Equipment

were, in effect, loans or advances to SystemSoft and not true

revenues which could be recorded or reported as such, as Digital

Equipment had the right to terminate the relationship and elect not

to utilize SystemWizard in its product line, in which case,

SystemSoft was obligated to repay all of the advances or loans that

Digital Equipment had made to it to date. Knowing that a detailed

analysis of the Digital Equipment/SystemSoft SystemWizard contract

would reveal these terns and the impropriety of SystemSoft's

- 35 -

accounting treatment for that contract, SystemSoft's directors and

officers decided not to include that contract as an exhibit with

SvstemSoft's SEC filings in F96 or E97, even though this was, as

SvstemSoft itself admitted, a material or important contract to

SystemSoft. Coopers & Lybrand, which was intimately involved in

this decision and approved of it, was aware that recognizing

revenue on this contract was improper and that it would be

necessary to conceal the true terms of this contract from the

public and the SEC in order to facilitate their misaccounting for

the contract.

32. The Digital Equipment/SystemSoft relationship was an

extremely important one to SystemSoft. While Intel Corporation had

also agreed to fund part of the development costs of SystemWizard,

Intel was a very large stockholder in SystemSoft and thus its

investment in developing that product was considered much less of

an endorsement of the technology and market potential of that

product than was the agreement of Digital Equipment to help fund

the development of the product, as Digital Equipment was an

independent entity, as well as a potentially large customer for the

product. The Digital Equipment relationship thus gave SystemSoft

not only a substantial public relations coup, but also provided for

it the opportunity to boost its reported revenues by including

Digital Equipment payments to it under the development contract as

current period revenue and also to boost the credibility of the

product when it was completed and ready to ship by ftaving a large

sophisticated computer OEM like Digital Equipment elect to purchase

the product and deploy it.

- 36 -

33. Thus, SystemSoft's corporate Board and top management was

extremely focused on the state of the relationship between

SystemSoft and Digital Equipment and the status of Digital

Equipment's attitude about committing to order and deploy the

SystemWizard product. This was a matter of constant attention and

frequent discussions among SystemSoft's corporate Board and top

managers. As a result, these individuals were kept apprised of the

current status of the Digital Equipment/SystemSoft relationship

throughout F96 and F97, and were aware of the serious deterioration

of that relationship during F97, and knew that it was most unlikely

that Digital Equipment would ever order SystemWizard in volume or

deploy the product and it was most likely that Digital Equipment

would terminate its relationship with SystemSoft in the near term.

Termination of the Digital Equipment/SystemSoft relationship would

be an extremely negative development for SystemSoft, as it would

require SystemSoft to repay some $7 million to Digital Equipment.

The repayment would have a material adverse impact on SystemSoft's

financial results going forward and the termination of the

relationship would indicate that Digital Equipment did not have

confidence in the commercial potential of the product and indeed

was not going to order or deploy it. SystemSoft's corporate Board

and managers determined to withhold this adverse information from

the marketplace, both to conceal from the securities markets this

very negative financial development for SystemSoft and to conceal

from the commercial or product market this very negative

development for the future of SystemWizard. As a result, even

after the Digital Equipment/SystemSoft relationship was formally

terminated in late 2/97, they deliberately concealed this

- 37 -

information. When they did disclose it several weeks later, they

buried the news in a footnote in SystemSoft's Management Discussion

and Analysis section of SystemSoft's F97 Annual Report, published

well after the Class Period ended.

Motive And Opportunity

34. In addition to having actual knowledge of the falsity of

their statements, each of the Defendants had the motive and the

opportunity to perpetrate the fraudulent scheme and course of

business described herein. During 94-95, SystemSoft was operating

in an industry in which smaller niche companies like SystemSoft

were at a competitive disadvantage and to survive SystemSoft was

attempting to grow rapidly. Rapid growth would create a larger

company, justify larger salaries to SystemSoft's corporate

management and push up its stock price, adding millions to their

wealth, based on their actual stock ownership and stock options.

35. Their motive to engage in this conduct included a desire

to attempt to continue SystemSoft's apparent record of sequential

quarterly revenue and EPS growth, to manipulate and artificially

inflate the price of SystemSoft's stock, to enhance the value of

their holdings of SystemSoft stock and/or options to purchase

SystemSoft stock, and permit SystemSoft's insiders to sell off

large portions of their SystemSoft stock at inflated prices.

DEFENDANTS' FRAUDULENT SCHEMEAND COURSE OF BUSINESS

36. Each of the Defendants is liable for making false state-

ments and as a participant in a fraudulent scheme and course of

business that operated as a fraud or deceit on purchasers of

SystemSoft stock, including the making of false and misleading

- 38 -

statements and/or concealing material, adverse facts. The

fraudulent scheme and course of business: (i) deceived the

investing public regarding SystemSoft's products and business; (ii)

deceived the commercial markets regarding SystemSoft's success with

its products; (iii) artificially inflated the price of SystemSoft

stock; (iv) caused plaintiffs and other members of the Class to

purchase SvstemSoft stock at inflated prices; and (v) permitted

certain defendants to dispose of 1,070,007 shares of SystemSoft

stock, pocketing over $21 million in illegal insider-trading

profits.

STATUTORY SAFE HARBOR

37. The statutory safe harbor provided for forward-looking

statements under certain circumstances does not apply to any of the

allegedly false forward-looking statements pleaded in this

Complaint because the statutory safe harbor does not apply to

SystemSoft's financial statements and because none of the

particular oral forward-looking statements pleaded herein were

identified as a "forward-looking statement" when made. None of the

written forward-looking statements made were identified as forward-

looking statements. Nor was it stated as to either type of

forward-looking statement that actual results "could differ

materially from those projected." Nor did meaningful cautionary

statements identifying important factors that could cause actual

results to differ materially from those in the forward-looking

statements accompany those forward-looking statenents. In any

event, each of the forward-looking statements alleged herein was

authorized by an executive officer of SystemSoft, and was actually

known by each of the Individual Defendants to be false when made.

- 39 -

BACKGROUND TO THE CLASS PERIOD

38. SystemSoft was a very small company that went public in

8/94 at $2.75 per share with annual revenues of only about $9-$10

million. After SystemSoft went public, its stock was only a modest

performer, as the Company sold only a few products for use almost

exclusively in laptop computers which limited its prospects for

significant profitable growth. By late 95, anal ysts were critical

of SystemSoft's rate of growth and its inability successfully to

develop and introduce new products. As D.F. Carey of Rodman &

Renshaw wrote on 11/29/95 in downgrading the stock after SystemSoft

reported disappointing 3rdQ F96 revenue growth:

rWle feel that revenue growth sequentially during Ql-O3 has not reflected the perceived potential of the company's products. . . [lit now appears that the company is struggling to meet estimates, and that revenue and earnings upside is doubtful. . . Revenues from newproducts are further off than expected. Much of the excitement about SystemSoft has been related to new products under development. However, it is now clear that we must relate our investment decisions to the current core products . . . .

SystemSoft's top insiders were upset over this negative perception

and were determined to overcome it and push SystemSoft's stock to

much higher prices. Thus, in early 96, SystemSoft announced the

development of a new product -- a new "call-avoidance" software

product called SystemWizard.

FALSE AND MISLEADING STATEMENTSISSUED DURING THE CLASS PERIOD

39. On 01/25/96, SystemSoft issued a press release entiticd

and stating:

SYSTEMSOFT TO RECEIVE FUNDING SUPPORT FROM INTEL ANDDIGITAL TO DEVELOP PRODUCTS THAT WILL AUTOMATICALLYIDENTIFY AND RESOLVE THE MOST COMMON PROBLEM FACED BYPERSONAL COMPUTER USERS; SYSTEM-WIDE PROBLEM RESOLU-

- 40 -

TION/CALL AVOIDANCE SOFTWARE WILL SIGNIFICANTLY REDUCECUSTOMER SUPPORT COSTS

* * *

Intel and Digital Equipment Corp. will provide SystemSoftwith up to several million dollars in funding,intellectual property and development assistance toaccelerate development of this new category of PCsoftware to be known as "Call Avoidance" products.SystemSoft will market and license products resultingfrom this alliance. It is estimated that productsresulting from this development effort could reduce thenumber of calls received by PC manufacturers' technicalsupport organizations by 30 percent, representing apotential annual industry-wide cost savings of more than$1 billion.

The first products are scheduled to ship to systemmanufacturers in the second quarter of 1996. The firstPCs to include problem resolution/call avoidance softwareare expected to be available during the fourth quarter ofthis year.

* * *

Digital's MCS Division which serves as the technicalsupport call center for a wide variety of OEMs includingMicrosoft, Compaq, Dell and NEC Technologies will providemarketing support for SystemSoft products developed underthis agreement. . . . To speed portions of SystemSoft'sdevelopment, Digital will also provide intellectualproperty and software associated with secure remotecommunications.

The release quoted Angelo as saying:

Digital [is] providing world-class resources that willenable SystemSoft to rapidly bring this new category ofcall avoidance software to market.

40. On 1/30/96, subsequent to the 1/25/96 press release,

SystemSoft held a conference call for securities analysts, money

and portfolio managers, institutional investors, large SystemSoft

shareholders, brokers and stock traders to discuss SystemSoft's new

SystemWizard product. During the call, Angelo made presentations

and answered questions. During the call -- and in follow-up

- 41 -

conversations with participants -- he directly disseminated

important information to the market by stating:

• SystemSoft's market research and evaluation revealed apotentially huge market for SystemWizard as this product wouldbe incorporated into desktop PCs as well as laptop computers,which would vastly expand SystemSoft's market penetration andprovide huge revenue growth for SystemSoft going forward.

• SystemSoft had determined that a royalty fee ofapproximately $5-$7 per SystemWizard unit was reasonable andcould be achieved.

• SystemSoft's development partnership with DigitalEquipment for SystemWizard would work very well and SystemSoftexpected that Digital Equipment would be utilizingSystemWizard.

• Because PC OEMs were losing significant amounts of moneyon the technical service calls being received by theirtechnical service centers, there was an enormous market demandfor SystemWizard with these PC manufacturers, as deployment ofSystemWizard would significantly reduce the number of servicecalls and thus provide a significant financial benefit to thePC OEMs.

41. On 1/31/96, Rodman & Renshaw issued a report on

SystemSoft, written by D.F. Carey, which was based on and repeated

information provided Carey in the 1/30/96 conference call and in

follow-up conversations with Angelo. The report stated:

SYSF held a mid-day conference call yesterday to furtheroutline the implications of its agreement with DEC andINTC to develop Call Avoidance software. This softwarerepresents potential cost savings of over $1 billion peryear to the PC industry.

Call Avoidance software would help PC manufacturersrecover technical support expenses. DEC provides techni-cal support to major OEMs such as Compaq, Microsoft,Dell, and NEC technologies through its MCS (MultiCustomer Support) Division. SystemSoft managementindicated a target of 20% cost reduction, which couldtranslate to $33 million in savings for Compaq.

* * *

SYSF expects revenues from the new product by 04fiscal 1997. When asked, management acknowledged plansto ship Call Avoidance software during third or fourthquarter of fiscal 1997 with revenues to follow.

- 42 -

42. On 2/27/96, systemSoft announced that its 4thQ F96

results would be better than expected. Angelo was interviewed by

Dow Jones and stated:

"Our base business is flourishing, getting faster growththan expected" . . Angelo told Dow Jones.

* * *

Angelo said the company this year will likely continue growing at the 50% to 60% rate, it has experienced over the last six years, based on itsexisting core businesses, which serve the mobile computer and hand-held devices market. Angelo further predictedthat SystemSoft's entry into the desktop PC market with a new product it is introducing this fall will bring additional revenue that would "double the company," in fiscal 1998.

43. On 2/28/96, SystemSoft reported 4thQ F96 revenues and EPS

of $7.3 million and $.06, respectively. The release was headlined

and stated:

SYSTEMSOFT ACHIEVES RECORD GROWTH FOR FOURTH QUARTER ANDYEAR END 1996

* * *

With the development of call avoidance software,SystemSoft will, for the first time, be marketing value-added products to desktop computer manufacturers. Thus, with call avoidance software, SystemSoft will begin to address a systems market that is five times the size of its current market.

* * *

During the fourth quarter, SystemSoft announced thecompletion of agreements with Intel Corporation andDigital Equipment to speed the development of CallAvoidance Software.

44. On 2/28/96, SystemSoft held a conference call for

securities analysts, money and portfolio managers, institutional

investors, large SystemSoft shareholders, brokers and stock traders

to discuss SystemSoft's business and its prospects. During the

call, Angelo made presentations and answered questions. During the

- 43 -

call -- and in follow-up conversations with participants -- Angelo

directly disseminated important information to the market by

stating:

• Demand for SystemSoft's core CardWizard productscontinued to be extremely strong and would continue so for theforeseeable future.

• SystemSoft was continuing to achieve increased marketpenetration with its core products and, as a result,SystemSoft expected extremely strong revenue growth of 50%-60%from its core product line during the next two fiscal years.

• SystemSoft was extremely pleased with its performance inthe most recent quarter and its increasing revenue and EPSreflected the continued strong demand for its core products inthe marketplace and broad customer acceptance of itstechnology.

• SystemSoft was making very good progress in developingSystemWizard and was "on track" to ship product later in F97and to achieve accelerated volume shipments in F98, whichwould generate millions in new revenue for SystemSoft.

• SystemSoft's market research and evaluation revealed apotentially huge market for SystemWizard as this product wouldbe incorporated into desktop PCs as well as laptop computers,which would vastly expand SystemSoft's market penetration andprovide huge revenue growth for SystemSoft going forward.

• SystemSoft had determined that a royalty fee ofapproximately $5-$7 per SystemWizard unit was reasonable andcould be achieved.

• SystemSoft's partnership with Digital Equipment forSystemWizard was working very well and SystemSoft expectedthat Digital Equipment would be utilizing SystemWizard.

• SystemSoft was in negotiations with every major PCmanufacturer regarding the deployment of SystemWizard and,based upon the state of those negotiations, was confident thatin each quarter going forward it would be able to make anannouncement that one or two major OEMs had accepted and woulddeploy the SystemWizard product.

• SystemWizard was in evaluation at virtually every majorPC manufacturer and was receiving extremely good reviews fromevery PC OEM, which increased SystemSoft's confidence for thesuccess of the product.

• Based on discussions with PC OEMs, SystemSoft anticipatedinitial volume deployment of the SystemWizard product in 1/97or 2/97.

- 44 -

• Due to continuing strong demand for its core products, aswell as the favorable reaction of PC OEMs to SystemWizard,SystemSoft was forecasting 40%-60% growth for the next severalyears.

45. On 2/29/96, Rodman & Renshaw issued a report on

SystemScft written by Carey, which was based on and repeated

information provided in the 2/28/96 conference call and in follow-

up conversations with Angelo. The report stated:

-- Outlook on SYSF's upcoming Call Avoidance softwareproduct remains positive. In an agreement announcedJanuary 25, SYSF will receive $8 million from DigitalEquipment and Intel to develop Call Avoidance software.The company anticipates product announcements in April orMay, followed by delivery of product in July or August.During the conference call, management alluded to thepossibility of signing two OEM agreements with major PCmanufacturers at the end of Q1 or the beginning of Q2fiscal 1997. . .

Management was forthcoming with expected revenue growthfor their core business. The company anticipates PC Cardand system level software revenue growth of 50%-60% overthe next 1-2 years.

46. On 2/29/96, Hambrecht & Quist issued a report on

SystemSoft, written by Todd Bakar, which was based on and repeated

information provided in the 2/28/96 conference call and follow-up

conversations with Angelo. The report stated:

SystemWizard, the Largest Opportunity of the Future:

A Rapidly Growing Need: It is projected that more than200 million cans will be placed to technical supportcenters in 1996, costing the PC industry nearly $4billion. As a specific example, Compaq is believed tonow encounter more than 25,000 technical support callsper day at an average cost of approximately $25 per call.These figures would equate to more than $150 million inannual technical support costs for Compaq alone. Hence,while many problems will not be automatically fixed, evena 10% or 20% reduction in the number of calls wouldtranslate into significant cost savings even for acompany of Compaq's size. SystemSoft plans on charging these various OEMs a per unit royalty of $5 to $12 basedupon a number of considerations including volume. Given the potential cost savings, this royalty appears reasonable. .

- 45 -

SystemWizard Will Roll out in 1996, but is a 1997 Oppor-tunity: . . . The company has already begun demon-strating the product to potential OEM partners includingsome of the major PC vendors. The company is targetingat least two large OEM customers by mid-year withdeliveries beginning in the July/August time frame. .[I]t remains difficult to forecast the actual revenuecontribution in fiscal 1998 (calendar 1997). At thistime, we are conservatively adding approximately $10million to our revenue forecast for SystemWizard.However, it is important to highlight that a successfullaunch and adoption of this technology could translateinto revenues dramatically larger . . than we areinitially projecting.

47. In 3/96, SystemSoft issued its F96 Annual Report which

included a letter signed by Angelo, that stated:

SystemSoft -- with the backing of Intel and DigitalEquipment -- is developing SystemWizard, our call-avoidance product that builds on the previous success ofour CardWizard product. SystemWizard uses expert systemtechnology to automatically diagnose and fix the most common problems that plagpe PC users so they do not need to pick up the phone to call for support.

* * *

SystemSoft has grown 50-60 percent annually byfocusing solely on the mobile computer market. With thedevelopment of S ystemWizard, SystemSoft will, for thefirst time, dramatically expand its market, offering thisadvanced product to the broader desktop computer market.Unit shipments in the desktop PC market are expected to exceed 50 million in 1996 -- a market that is five times larger than the mobile PC market that SystemSoft currently addresses.

48. On 4/30/96 SystemSoft's CEO Angelo appeared at the

Hambrecht & Quist Technology Conference in San Francisco. In a

formal presentation and in break-out sessions, he told the

assembled security analysts, money and portfolio managers,

institutional investors, brokers and stock traders:

• Demand for SystemSoft's core CardWizard productscontinued to be extremely strong and would continue so for theforeseeable future.

• SystemSoft was continuing to achieve increased marketpenetration with its core products and, as a result,

- 46 -

SystemSoft expected extremely strong revenue growth of 5096-60%from its core product line during the next two fiscal years.

• SystemSoft was making very good progress in developingSystemWizard and was "on track" to ship product later in F97and to achieve accelerated volume shipments in F98, whichwould generate millions in new revenue for SystemSoft.

• SystemSoft's market research and evaluation revealed apotentially huge market for SystemWizard as this product wouldbe incorporated into desktop PCs as well as laptop computers,which would vastly expand SystemSoft's market penetration andprovide huge revenue growth for SystemSoft going forward-

• SystemSoft had determined that a royalty fee ofapproximately $5-$7 per SystemWizard unit was reasonable andcould be achieved.

• SystemSoft's development partnership with DigitalEquipment for SystemWizard was working very well andSystemSoft expected that Digital Equipment would be utilizingSystemWizard.