Embed Size (px)

Citation preview

1

GOVERNMENT OF KARNATAKA

KARNATAKA PRE-UNIVERSITY EDUCATION EXAMINATION BOARD

II YEAR PUC EXAMINATION MARCH-2018

SCHEME OF VALUATION

Subject Code: 30 Subject: ACCOUNTANCY (NS)

Question No.

SECTION-A Marks allotted

1. State any two causes of depreciation. Ans: Causes of depreciation:-

1. Constant use/Wear and Tear. 2. Passage of time/Lapse of time.

3. Obsolescence. 4. Permanent fall in market price. 5. Abnormal factors (Any two, one mark each)

1+1

2. What is partnership Deed? Ans: When the partnership agreement is written and signed by all the partners and is duly stamped according to the Stamp Act, it is called ‘Partnership Deed’ or ‘Articles of Partnership’

2

3. What is goodwill? Ans: Goodwill is the value of good name/reputation of business which attracts more customers and helps the firm to earn more profits.

2

4. Give the journal entry to close revaluation account when there is profit

Ans: Revaluation A/c Dr. To Partners capital A/c (Being profit on revaluation transferred to partners capital accounts)

2

5.

2

2

What is Realisation account?

Ans: Realisation account is an account prepared at the time of dissolution of a firm to ascertain the profit/loss on the realization

of assets and payment of liabilities. 6. What do you mean by issue of shares at premium?

Ans: If issue price is more than the face value of shares, it is called issue of shares at premium.

2

7. Give the meaning of Interim dividend. Ans: Interim dividend is the dividend declared by the company in between two Annual General Meetings in anticipation of profits.

2

8. List out any two techniques of Financial Statement Analysis. Ans: Techniques of Financial Statement Analys 1.Comparative Statements 2.Common size statemen 3.Trend Analysis 4.Ratio Analysis 5.Cash flow Statements (any two,onemark each)

1+1

9.

Give any two examples of non-profit organizations. Ans: Examples of non-profit organizations are:-

1. Schools and colleges 2. Hospitals 3. Sports clubs 4. Charitable institutions 5. Libraries etc., (any two,one mark each)

1+1

10 Mention any two types of information. Ans: Types of information are:-

1. Strategic Information 2. Tactical Information 3. Operational Information 4. Statutory Information (any two,one mark each)

1+1

3

Scecton-B 11. Calculation of Interest on Shiva’s drawings

SL NO DATE AMT(Rs) O/S PERIOD PRODUCT 1 01/05/2016 5,000 11 55,000

2 31/08/2016 7,000 7 49,000 3 31/12/2016 3,000 3 9,000

4 01/02/2017 4,000 2 8,000

TOTAL PRODUCT 1,21,000 Intereston Shiva’s drawings=Total productXRateX1/12

=1,21,000X

X

= Rs.1,210

Int on Shiva’s Drawings= Rs. 1,210 ( One marks for formula and four marks for calculation)

12. Old Profit Sharing Ratio = 4:3:2 New Profit Sharing Ratio = 5:3 Gain Ratio = New profit sharing ratio – Old profit sharing ratio ( I mark)

G.R of Suchit =

-

=

=

( 1.5 marks)

G.R. of Chandru =

-

=

=

( 1.5 marks)

Gain Ratio of Suchit&Chandru = 21:11 (1 mark )

4

13. Raja’ s Capital Account

Dr. Cr. Particulars Rs` Particulars `Rs

To Drawings A/C

To Raja;s Executors A/C(trf)

20,000

1,20,500

By balance b/d

By P & L Suspense A/c

(80000x

x

)

By Int on Capital A/C

(100000x

x

)

By SalaryA/C(1000x9)

1,00,000

24,000

7,500

9,000

1,40,500 1,40,500

(5 marks)

14. Journal entries in the books of Jagadeesh Co. Ltd

Date Particular L/F Debit(Rs) Credit(Rs)

1 2 3 4

Bank A/C (10000x2) Dr To 12% Debentures Application A/C (Being Application money received)

20,000

20,000

50,000

50,000

20,000

20,000

30,000 20,000

50,000

12% Debentures Application A/C Dr To 12% Debentures A/C (Being application money transfrred)

12% Debentures Allotment A/C Dr To 12%Debentures A/C To Securities Premium A/C (Being Allotment money due and discount on debentures adjusted )

Bank A/C Dr To 12% Debenture Allotment A/C (Being Allotment money received)

( simple entries one mark and compound entry two marks i,e 3+2=5marks)

5

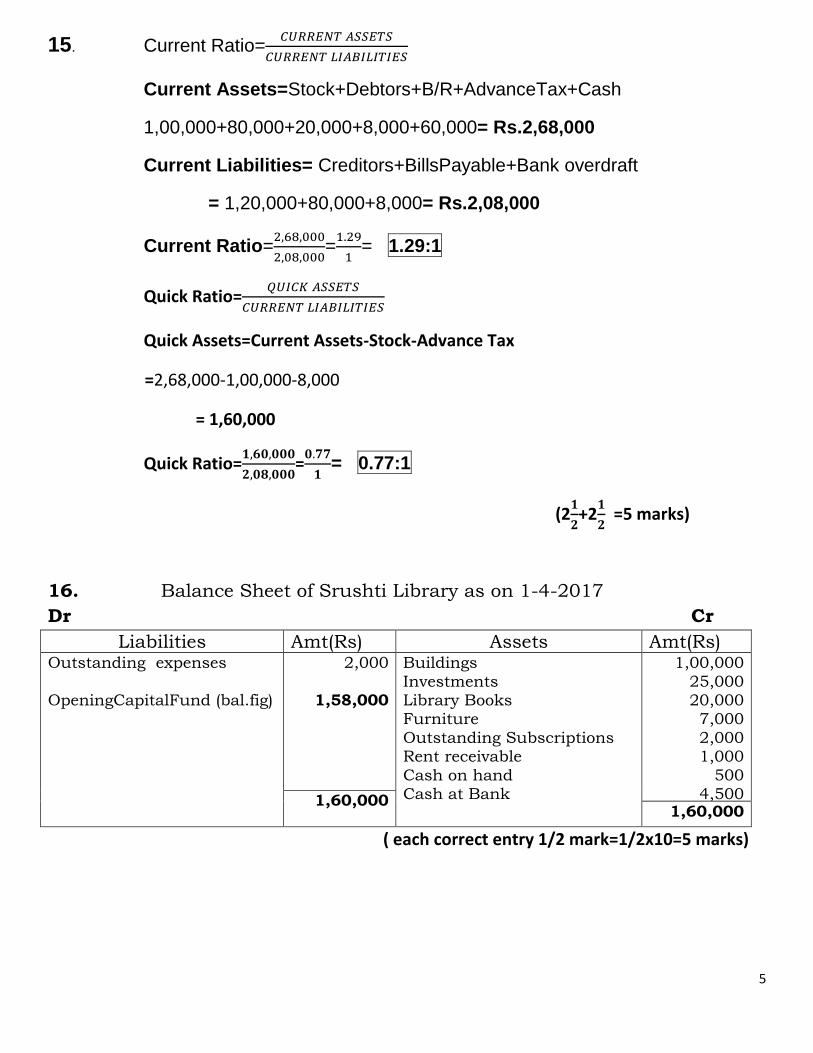

15. Current Ratio=

Current Assets=Stock+Debtors+B/R+AdvanceTax+Cash

1,00,000+80,000+20,000+8,000+60,000= Rs.2,68,000

Current Liabilities= Creditors+BillsPayable+Bank overdraft

= 1,20,000+80,000+8,000= Rs.2,08,000

Current Ratio=

=

= 1.29:1

Quick Ratio=

Quick Assets=Current Assets-Stock-Advance Tax

=2,68,000-1,00,000-8,000

= 1,60,000

Quick Ratio=

=

= 0.77:1

(2

+2

=5 marks)

16. Balance Sheet of Srushti Library as on 1-4-2017

Dr Cr

Liabilities Amt(Rs) Assets Amt(Rs) Outstanding expenses

OpeningCapitalFund (bal.fig)

2,000

1,58,000

160000

Buildings

Investments Library Books Furniture

Outstanding Subscriptions Rent receivable

Cash on hand Cash at Bank

1,00,000

25,000 20,000 7,000

2,000 1,000

500 4,500

160000

1,60,000 1,60,000

( each correct entry 1/2 mark=1/2x10=5 marks)

6

17.Qualities of information:

1.Accurate 2.Complete 3.Reliable 4. Timely 5.Up-to-date

(Explain the above points in brief-3+2 marks)

Section-C

18. Calculation of Profit or Loss on Sale of Machinne A

Cost of the Machinery as on 1-4-2014

Rs.1,20,000

Less Depreciation upto31/03/2015 12,000

Depreciation upto 31/12/2015(9months) 9,000 Rs. 21,000

Book Value of Machine A as on 31-12-2015

Rs. 99,000

Less:- Sale proceeds of Machine A Rs. 84,000

Loss on Sale of Machine A Rs. 15,000

7

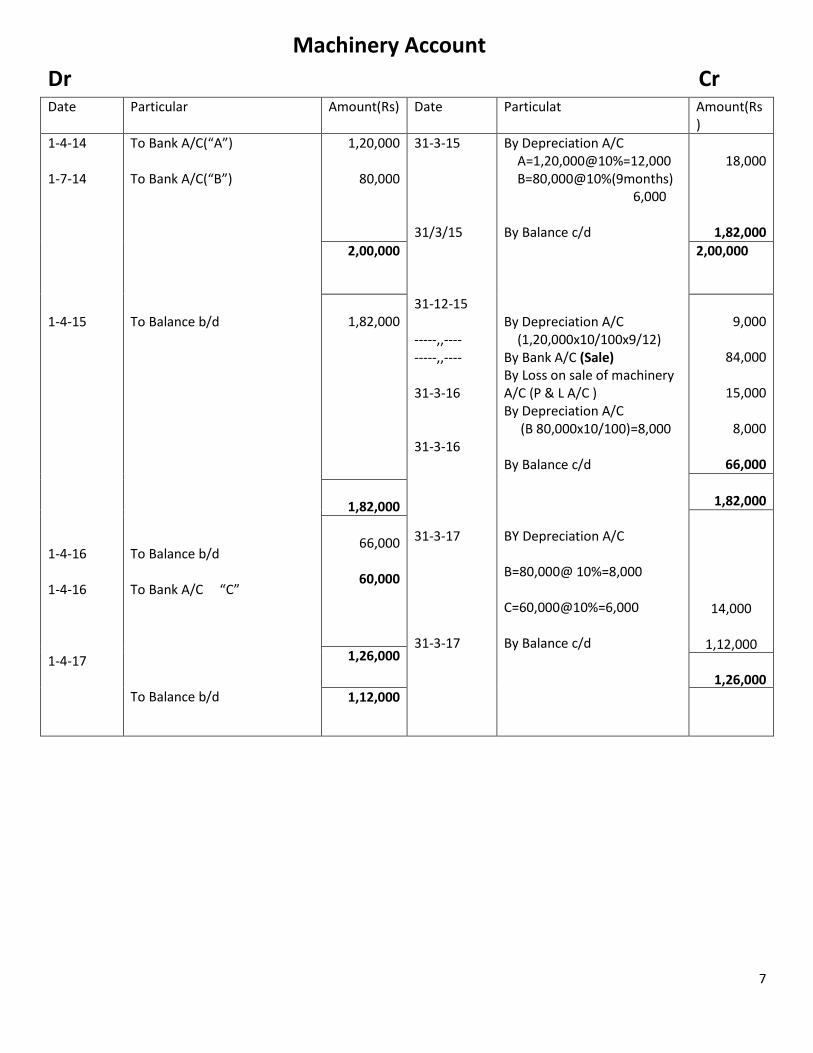

Machinery Account

Dr Cr Date Particular Amount(Rs) Date Particulat Amount(Rs

)

1-4-14 1-7-14 1-4-15 1-4-16 1-4-16 1-4-17

To Bank A/C(“A”) To Bank A/C(“B”) To Balance b/d To Balance b/d To Bank A/C “C” To Balance b/d

1,20,000

80,000

31-3-15 31/3/15 31-12-15 -----,,---- -----,,---- 31-3-16 31-3-16 31-3-17 31-3-17

By Depreciation A/C A=1,20,000@10%=12,000 B=80,000@10%(9months) 6,000 By Balance c/d By Depreciation A/C (1,20,000x10/100x9/12) By Bank A/C (Sale) By Loss on sale of machinery A/C (P & L A/C ) By Depreciation A/C (B 80,000x10/100)=8,000 By Balance c/d BY Depreciation A/C B=80,000@ 10%=8,000 C=60,000@10%=6,000 By Balance c/d

18,000

1,82,000

2,00,000

2,00,000

1,82,000

9,000

84,000

15,000

8,000

66,000

1,82,000

1,82,000

14,000

1,12,000

1,12,000

66,000

60,000

1,26,000 1,26,000

1,12,000

8

Dr Depreciation A/C Cr

Date Particular Amount(Rs) Date Particular Amount(Rs)

31-3-15 31-12-15 31-03-16 31-3-17

To Machinery A/C To Machinery A/C To Machinery A/C To Machinery A/C

18,000 18,000

9,000 8,000

17,000 14,000

14,000

31-3-15 31-3-16 31-3-17

By P & L A/C (Trf) By P & L A/C (Trf) By P & L A/C (Trf)

18,000 18,000

17,000

17,000

14,000 14,000

2+8+4=14

19. Revaluation A/C

Dr Cr

Particular Amount(Rs) Particular Amount (Rs)

To Machinery(80000x10/100)

,, Furniture (40000x10/100)

,, P D D(40000x5/100)

,, O/S Salary

‘’ Partners Capital A/C

Sujata’s Cap A/c(16000x3/5)= 9600

Sanjota’s cap A/c(16000x2/5)=6400

,

8,000

4,000

2,000

2,000

16,000

By Building

,, Investment(50000-40000)

22,000

10,000

32,000 32,000

Capital Account Partners

Dr Cr

Particular Sujata Sanjota Sangeeta Particular Sujata Sanjota Sangeeta

To P & L A/C

To Bank A/C(G/W)

,, balance c/d

6,000

12,000

1,53,600

4,000

8,000

1,02,400

60,000

By Balance B/D

,, Reserve Fund

,, Revaluation A/C

,, Goodwill (3:2)

,, Bank A/C

1,20,000

30,000

9,600

12,000

80,000

20,000

6,400

8,000

60,000

1,71,600 1,14,400 60,000 1,71,600 1,14,400 60,000

9

Balance Sheet of the new firm as on 1-4-2016 Liabilities Amount(Rs) Assets Amount(Rs)

Creditors

Bills Payable

O/S salary

Capital Accounts

Sujata 153600

Sanjota 102400

Sangeeta 60000

1,00,000

50,000

2,000

3,16,000

Cash (40000+60000+20000-20000)

Stock

Debtors 40000

Less: PDD 2000

Furniture 40000

Less: Depreciation 4000

Machinery 80000

Less: Depreciation 8000

Buildings 100000

Add: Appreciation 22000

Investments(40000+1000)

1,00,000

50,000

38,000

36,000

72,000

1,22,000

50,000

36000

4,68,000 4,68,000

(4+5+5=14)

10

20. Realisation Account

Dr Cr

Particular Rs ` Particular Rs

To Investments

,, Bills Receivable

,, Debtors

,, Stock

,, Machinery

,, Furniture

,, Buildings

,, Cash/Bank A/C

( Creditors & B/P paid))

,, Cash/Bank A/C

(Dissolution exp paid)

10,000

10,000

25,000

10,000

10,000

10,000

20,000

30,000

1,000

_____________

1,26,000

By Creditors

,, Bills Payable

,, Cash/Bank A/C

Bills Receivable 7500

Debtors(25000-2500) 22500

Stock(10000-1000) 9000

Machinery(10000+500) 10500

Buildings 15000

,, Rashmi’s Capital A/C

(Furniture taken over)

,, Rahul,s Capital A/C

(Investments taken over)

By Partners Capital A/C

Rashmi (21500x3/5)= 12900

Rahul (21500x2/5) 8600

10,000

20,000

64,500

5,000

5,000

21,500

____________

1,26,000

Capital Accounts of Partners

Dr Cr

Particular Rashmi

Rahul

Particular

Rashmi

Rahul

To Realisation A/C (asset taken over)

To Realisation A/C

(Net Losses)

,, Cash/Bank A/C

(Ultimate Balance

Paid)

5,000

12,900

18,100

5,000

8,600

10,400

By Balance b/d

,, Reserve Fund

30,000

6,000

20,000

4,000

36,000 24,000 36,000 24,S000

11

Cash/Bank A/c

Dr Cr

Particular Rs Particular Rs

To Balance b/d

,, Realisation A/c (Assets realized)

5,000

64,500

By Realisation A/C(Liabilities Paid)

,, Realisation A/C (Dissolution

Expenses paid)

,, Rashmi’S Loan A/C

,, Rashmi’s Capital A/C

,, Rahul’s Capital A/C

30,000

1,000

10,000

18,100

10,400

69,500 69,500

(7+3+4=14marks)

21. Journal entries in the books of Vijayalaxmi Co .Ltd

Date Particular L/F Debit(Rs) Credit(Rs)

1 2 3 4 5 6

Bank A/C(10000x2) Dr To Equity Shares Application A/C (Being Application Money received)

20,000

20,000

50,000

50,000

20,000

20,000

20,000

20,000

30,000 20,000

50,000

20,000

20,000

Equity Shares Application A/C Dr To Equity Share Capital A/C (Being Application money transferred)

Equity Share Allotment A/C(10000x5) Dr To Equity Share Capital A/C(10000x3) To Securities Premium A/C(10000x2) (Being Allotment money due including premium)

Bank A/C(10000x5) Dr To Equity Share Allotment A/C (Being Allotment money received including premium)

Equity Share First Call A/c(10000x2) Dr To Equity Share Capital A/C (Being first call money due)

Bank A/C(10000x2) Dr To Equity Share First Call A/C (Being first call money received)

12

7 8 9 10 11

Equity Share Final Call A/C(10000x3) Dr To Equity Share Capital A/C (Being final call money due)

30,000

28,500

5,000

3,500 1,500

2,000

30,000

28,500

3,500 1,500

5,000

2,000

Bank A/C(9500x3) Dr To Equity Share Final Call A/c (Being Final Call Money received except 500 shares)

Equity Share Capital A/C(500x10) Dr To Forfeited Shares A/C(500x7) ,, Equity Share Final A/C(500x3) (Being Forfeiture of 500 shares)

Bank A/C(500x7) Dr Forfeited Shares A/C Dr To Equity Shares Capital A/C (Being Re-issue of forfeited shares at discount)

Forfeited Shares A/C Dr To Capital Reserve A/C (Being balance in F S a/c transferred to Capital Reserve A/c)

(simple entries one mark and compound entries two marks i,e 8+6=14marks)

22. Shobha Trading Co. Ltd

Balance Sheet as at March31,2014

Equity and Liabilities Notes Amount(Rs)

Shareholders’ funds Share Capital Reserves and Surplus Non-Current Liabilities Long- term borrowings Current Liabilities Short-borrowings Trade Payables Other current liabilities Short-term provisions

1 2

3

4

5 6

2,00,000

62,326

50,000

42,500

56,924

TOTAL 4,11,750

Assets Non-current assets Fixed Assets Tangible Assets Intangible Assets(goodwill)

7

1,80,250 62,500

13

Current Assets Investments Inventories Trade receivables Cash and cash Equivalents Short-term loans and advances

8 9

10

22,500 80,000 66,500

TOTAL 4,11,750

Shobha Trading Co. Ltd

Statement of Profit and Loss for the year ended March 31, 2014

Particulars Notes Rs

Income Revenue from operations Less:Returns Revenue from operations(gross) Less:Excise Duty Revenue from operations(net) Other Income

2,75,000

2,75,000

2,75,000

nil Total Revenue from operation(A) 2,75,000

Expenses Purchases of stock-in-trade Changes in trade(17500-22500) (opening inventory less closing inventory) Employee benefit expenses Finance costs Depreciation and Amortisation expenses Other expenses

11 12 13 14

85,000 (5,000)

33,500

5,000 7,250

37,500

Total Expenses (B) 1,63,250 Profit befor Tax (A-B) 1,11,750

Tax expense:- Current tax

33,525

Profit for the year 78,225

14

Note 1-Share Capital

Particulars Amount(Rs) Amount(Rs)

Equity share capital of Rs. 10 each 2,00,000 Total 2,00,000

Note 2-Reserves and Surplus

Particulars Amount(Rs) Amount(Rs) General Reserve Add:Transferred from surplus Closing balance Surplus:-Opening balance Add:-Surplus from statement of P & L Amount available for appropriations Appropriations Less: (i)Proposed dividend(200000x10/100) :(ii)DDT @16.995% :(iii) Amount transferred to General Reserve Closing balance

2,500 2,500

5,000 78,225

83225 20,000 3399 2500 25,899

5,000

57,326

Total Reserves and Surplus 62,326

Note 3-Long-term borrowings

Particulars Amount(Rs) Amount(Rs)

10% Debentures 50,000 Total 50,000

Note 4-Short-term borrowings

Particulars Amount(Rs) Amount(Rs) Total Nil

Note 5-Other current liabilities

Particulars Amount(Rs) Amount(Rs)

Total Nil

15

Note 6-Short term provisions

Particulars Amount(Rs) Amount(Rs)

Proposed dividend DDT Provision for tax

20,000 3,399

33,525

Total 56,924

Note 7-Fixed Assets

Particulars Gross Block(Rs)

Depreciation(Rs) Net Block(Rs)

Tangible Assests Plant & Machinery Furniture Buildings

50,000 92,500 45,000

5,000

2,250

45,000 92,500 42,750

Sub Total 1,87,500 7,250 1,80,250

Intangible Assets Goodwill

62,500

-

62,500

Sub Total 62,500

-

62,500

Total 2,50,000 7,250 2,42,750

Note 8-Trade Receivables

Particulars Amount(Rs) Amount(Rs) Trade Receivables 80,000

Total 80,000

Note 9-Cash and cash equivalents

Particulars Amount(Rs) Amount(Rs)

Fixed Deposits Cash in hand and at bank

35,000 31,500

Total 66,500

Note 10-Short term loans and advances

Particulars Amount(Rs) Amount(Rs) Total Nil

16

Note 11-Employee benefit expenses

Particulars Amount(Rs) Amount(Rs)

Salaries Staff welfare expenses

27,500 6,000

Total 33,500

Note 12-Finance Costs

Particulars Amount(Rs) Amount(Rs)

Interest on Debentures 5,000 Total 5,000

Note 13-Depreciation and Amortisationa expenses

Particulars Amount(Rs) Amount(Rs) Depreciation on Tangible assets( as per note no 7) 7,250

Total 7,250

Note 14-Other expenses

Particulars Amount(Rs) Amount(Rs) Office Rent Rates & Taxes

25,000 12,500

Total 37,500

(Working Note 5 statement of P/L A/C 5 Balance Sheet 4 Marks.)

23. Sangolli Raytanna Co., Ltd

Comparative Balance Sheet as on 31-3-2015 &31-3-2016

Particulars 31-3-15(Rs) 31-3-16(Rs) Increase or Increase or

Decrease(Rs) Decrease(%)

I. Equity & Liabilities

1. Shareholders Fund:

Share Capital (Eqity+Pref) Reserves & Surplus

5,50,000 10,50,000 5,00,000 90.91

3,00,000 4,00,000 1,00,000 33.33

Total Shareholders Fund(A) 8,50,000 14,50,000 6,00,000 70.59

2. Non Current liabilities

Long-term loans 1,00,000 2,50,000 1,50,000 150.00

17

Liabilities side 8 marks and Assets side 6 marks (8+6=14 marks)

Total Non-Current Liabilities(B) 3

1,00,000 2,50,000 1,50,000 150.00

3.Current Liabilities

a. Trade payables 50,000 1,50,000 1,00,000 200.00

Total Current Liabilities ( C ) 50,000 1,50,000 1,00,000 200.00

Total Equity & Liabilities (A+B+C) 10,00,000 18,50,000 8,50,000 85.00 Assets

II. Assets

I. Non-Current Assets(Fixed Assets)

a. Tangible Assets

Fixed Assets Investments

5,00,000 2,00,000

10,00,000 2,50,000

5,00,000 50,000

100.00 25.00

Total Non-Current Assets(A) 7,00,000 12,50,000 5,50,000 78.57

2. Current Assets:

Inventory 2,25,000 3,25,000 1,00,000 44.44 Trade Receivables Cash & Cash equivalents

50,000 25,000

2,00,000 75,000

1,50,000 50,000

300.00 200.00

Total Current Assets (B) 3,00,000 6,00,000 3,00,000 100.00

Total Assets (A+B) 10,00,000 18,50,000 8,50,000 85.00

18

24. In the books of Anvita Education Society, Bangalore

Dr Income & Expenditure A/C for the Year Ending 31-3-2017 Cr

Expenditure Amt(Rs) Incomes Amt(Rs)

To Audit Fees 2500 Add: Current year o/S 2500 5000 Less: Last Year o/s 2500 ,, Rent ,,, Stationery & Postage ,, Salary ,, Functions ,, Depreciation On Furniture

“ excess of Income over Expenditure

2,500 1,800

250

8,000 1,050

250 8,950

By Subscriptions 20500 Less: Last year o/s 1000 19500 Add:Current Year o/s 2000 21500 Less: received in advance 1500 ,, Donations(2500x1/2) ,, Interest on Govt Bonds 850 Add:-O/S 700

20,000

1,250

1,550

2,2800 22,800

Balance Sheet as on 31-3-2017

Liabilities Amt(Rs) Assets Amt(Rs) Outstanding Audit Fees Subscriptions received in advance Capital Fund

Opening Balance 36400 Add: Donations 1250 Surplus 8950

2,500 1,500

46,600

Cash in hand Maps & Charts 1600 Add: Purchases 3400 5% Govt Bonds Furniture 3250 Less: Depreciation 250 O/S Subscriptions O/S Interest on Govt Bonds

8,900

5,000 31,000

3,000 2,000

700

50,600 50,600

(8+6 marks=14 marks)

19

Section-D

(Practicle oriented Questions)

25. (a)Interest on Capital: - No partner is entitled for any interest on capital

(b)Interest on Drawings: -No interest to be charged on drawings (c)Interest on partners loan: - 6% p. a. interest is allowed on partners loan (d)Distribution of profits or Loss: - Equal distribution of profits or Loss (e)Salary to partner: - No partner is entitled for any salary

( each correct answer one marks 1x5=5 marks)

26.

Dr. Executor’s Loan A/c Cr.

Date Particulars Amount Date Particulars Amount 31-03-2016 To Bank 60,000 01-04-2015 By X’s Capital A/c 1,00,000

31-03-2016 To Balance c/d 50,000 31-03-2016 By Interest@10% 10,000 1,10,000 1,10,000

31-03-2017 To Bank 55,000 01-04-2016 By Balance b/d 50,000 31-03-2017 By Interest@10% 5,000

55,000 5,500

(2

+2

=5 marks)

27.a) Revenue b)Capital c)Revenue d)Capital e)Capital

( each correct answer one mark 1x5=5 marks)

----------------------------------------END------------------------------------------------

20

21

22