Embed Size (px)

Citation preview

GP CME

GP business models – time for a change?

Outline of Session

• General practice overview

• Traditional business model

• What are new GPs looking for?

• Drivers and barriers to change

• The future business model?

General practice – the evolution

10 years ago NOW

Revenue streams 60% - 70% from

patients

60% - 70% from

Government

Sale value: solo practice with

2,000 patients

$ little value $ little value

Sale value: 5 solo practices

amalgamating into one single

business of 10,000 patients

Not done $1million+

Business Structure Solo or group practice cost-

sharing (associateship)

Single business model

becoming more common

Rooms Converted house IFHC developments becoming

more common

Revenue generators All income generated by GP

consultation interaction

Various income streams and

capitation allows for income

generation by other staff

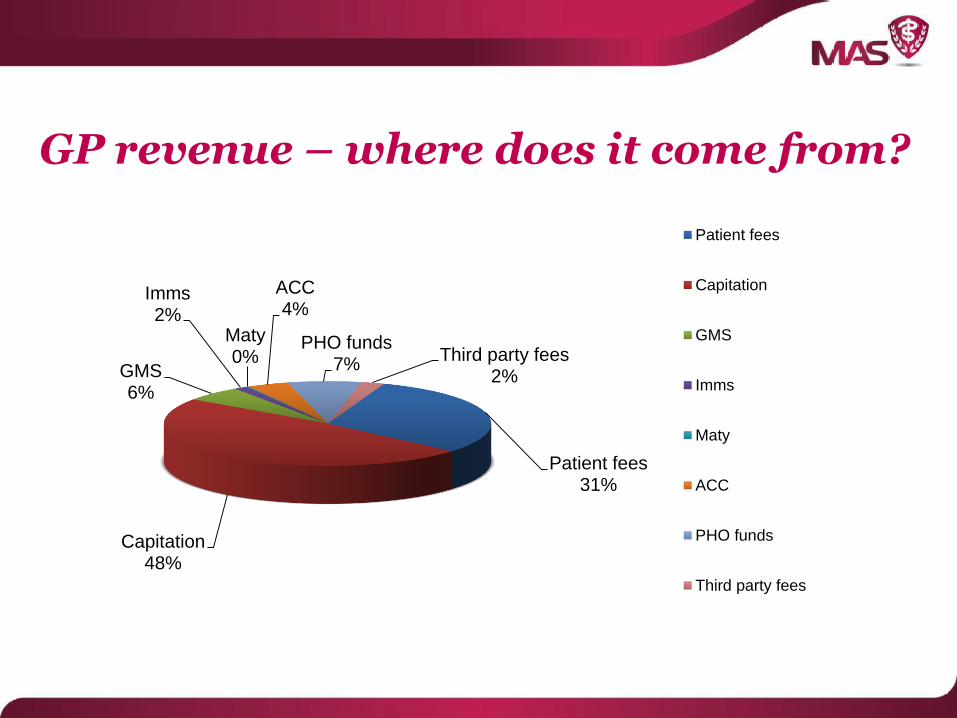

GP revenue – where does it come from?

Patient fees31%

Capitation48%

GMS6%

Imms2%

Maty0%

ACC4%

PHO funds7%

Third party fees2%

Patient fees

Capitation

GMS

Imms

Maty

ACC

PHO funds

Third party fees

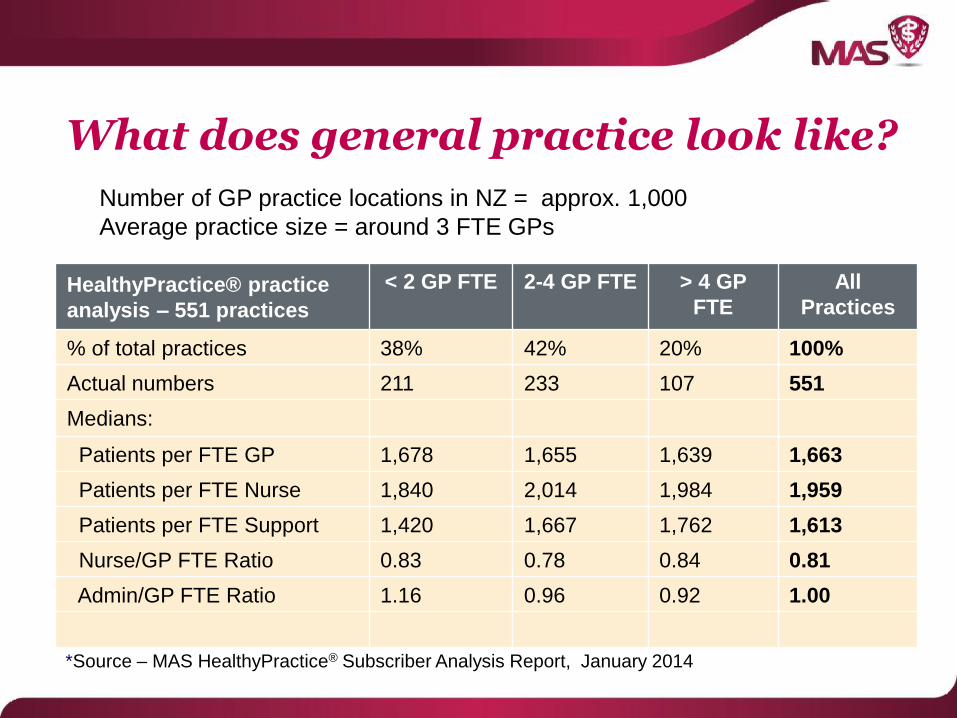

HealthyPractice® practice

analysis – 551 practices

< 2 GP FTE 2-4 GP FTE > 4 GP

FTE

All

Practices

% of total practices 38% 42% 20% 100%

Actual numbers 211 233 107 551

Medians:

Patients per FTE GP 1,678 1,655 1,639 1,663

Patients per FTE Nurse 1,840 2,014 1,984 1,959

Patients per FTE Support 1,420 1,667 1,762 1,613

Nurse/GP FTE Ratio 0.83 0.78 0.84 0.81

Admin/GP FTE Ratio 1.16 0.96 0.92 1.00

What does general practice look like?

Number of GP practice locations in NZ = approx. 1,000

Average practice size = around 3 FTE GPs

*Source – MAS HealthyPractice® Subscriber Analysis Report, January 2014

What does general practice look like?

• Ownership models have expanded. In addition to privately owned (GP and ‘corporate’) there are now PHO, MSO, DHB, Community Trust, Iwi and other ownership models

• Private ownership (‘non-corporate’) generally still cost sharing arrangements

• Practice ownership (patient goodwill) at individual GP level

• Management role shared (GPs/Practice Manager/ some staff)

Cost Sharing Business Model

Cost sharing group practice is still dominant e.g.

• Each GP retains business ownership (their practice goodwill) and receives their revenue streams related to their practice. Group fixed assets are owned equally.

• Capitation funds are received directly by individual GP (with/without internal clawbacks) or internal GMS/notional capitation.

• Group practice employs staff, manages the costs and some group practice revenue and levies GP owners with share of net expenses.

Cost Sharing

Cost Sharing revenue streams

To Individual GP practice• Patients consult fees

• GMS (casuals)

• Capitation (actual or internal GMS)

• ACC

• Prescriptions (no consults)

• Maternity

• Internal clawbacks*

• GP registrar revenue*

• Nurse consult fees*

• Immunisations*

* Some practices

Cost Sharing revenue streams

To Group Practice• Nurse consult fees*

• Immunisations*

• Capitation* (with internal GMS to GP)

• GP registrar revenue*

• PHO projects*

* Some practices

Generally group practice revenue goes to offset group practice

costs and net costs are levied to each GP practice.

Cost sharing benefits/concerns

Benefits

• Individual fee for service model means GP take home income reflects personal consultation activity and/or their enrolled patient base

• Allows more independence of working practice

Concerns

• Difficult and complex to fairly allocate costs and reward for care of chronic illness patients, elderly or psychiatric

• Tensions between what’s better for individual GP and the group practice

• More difficult for group practice governance and compliance

• More difficult for ownership succession planning

What are new GPs looking for?

Increased interest in business ownership but:

• Generally younger GPs lack business management knowledge and the desire to obtain it – they want to be a clinician first and foremost.

• Lack of desire to operate their ‘own’ business as owner, manager and clinician.

• Generally they require more flexible working arrangements, work/life balance and collegial support.

Barriers to business model change

• Fee for service (pre-capitation) mindsets of current

owners

• New entrants to group practice accept current model to

buy in – start ups no longer an option?

• Perceived financial ‘winners & losers’ and uncertainty to

change from status quo

• GP’s often unskilled in business governance and group

decision making

• Lack of time to fully consider ownership issues and

future planning

Drivers for change to business model

• Capitated funding and proactive population health management

• Less direct revenue from GP/patient consult

• Group practice quality standards

• Increased compliance and administration

• GP stress/work-life balance requirements

• Succession planning

• Business and management skill needs

• Better financial returns to owners

Future business model

Future business model?

• A single business owning all fixed assets and goodwill

• Patients would continue to see their preferred GP but all ‘contracts’ would be with the practice company.

• A clear separation between clinical remuneration and return on investment for business ownership i.e. company profits.

• Financial risk (and return) is held at the group company level.

• Better ability to manage compliance and quality within a single business.

• Simpler internal accounting and financial management. All revenue is received and all expenses are paid by the group practice entity.

• Clear governance and management structure with less potential conflicts.

How to get there

1. Determine the total value of all the fixed assets and goodwill – what is total value if the group practice was sold

2. Each GP/practice to sell their practice into the group in return for (equal) shareholding. If practices unequal in value then equalisation valuation model to be determined in conjunction with transfer

3. Determine remuneration model for GP working owners

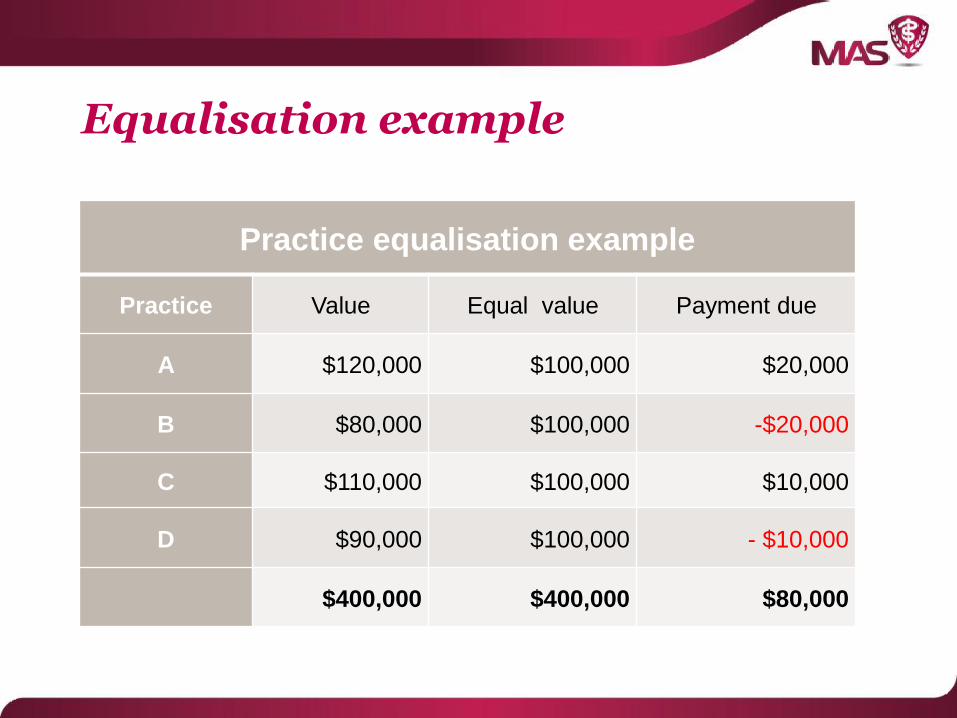

Equalisation example

Practice equalisation example

Practice Value Equal value Payment due

A $120,000 $100,000 $20,000

B $80,000 $100,000 -$20,000

C $110,000 $100,000 $10,000

D $90,000 $100,000 - $10,000

$400,000 $400,000 $80,000

GP remuneration – salary/benefits

MAS survey – December 2013Median employee salary range $181,000-$190,000

ASMS/DHB MECA – Specialist scale• 13-step salary scale range (40-hour week) as from 1 October 2013 is $150,500 to

$209,000 with 30% ‘protected’ non-clinical time.

• Benefits include:

- Annual leave of 6 weeks (in addition to 11 days public holidays)

- 2 weeks CME leave including reimbursement of costs of $16,000 p.a.

- Time and half for after hours roster

- 3 months sick leave prior to review

- Subsidised superannuation/KiwiSaver (6%).

Benefits add significant value to the salary package value

GP remuneration - commission

MAS survey – December 2013

• Now less common – only 17% paid commission (38% hourly rate, 37% sessional, 7% salary)

• Median commission 55% (urban) 60% (rural)

(most - 85%, included capitation – notional or actual)

• Traditional fee for service model – still as relevant?

• More complex with capitation and % of what revenue? e.g. non-consult scripts, GP/nurse, ACC etc.

• Income reflects productivity/activity (consult) level but doesn’t encourage services to be provided by competent lower cost providers e.g. practice nurses.

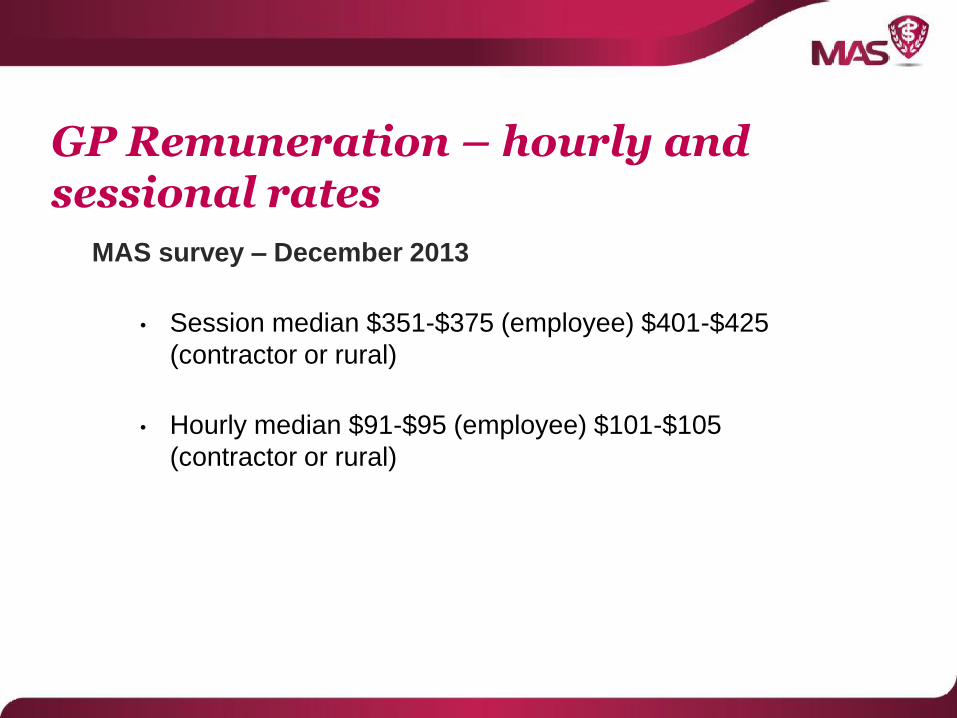

GP Remuneration – hourly and sessional rates

MAS survey – December 2013

• Session median $351-$375 (employee) $401-$425

(contractor or rural)

• Hourly median $91-$95 (employee) $101-$105

(contractor or rural)

Single business model

Possible benefits for the practice/business manager:

• Clearer governance and direction from owners

• No more complex internal cost sharing arrangements

• Focus switches to group practice performance as financial impact (profits/losses) is on all principals

• Ability to manage all revenue opportunities and profit, not just costs

• Should encourage more proactive health management, better use of lower cost nurse providers, clinics, education and self-management of some health conditions

• Should encourage better teamwork, consistency, group standards and group practice compliance

Resources and contacts

Contacts Shaun Phelan

MAS Business Advisory Manager

Telephone 0800 800 627

MAS HealthyPractice® website healthypractice.co.nz

MAS risk and investment mas.co.nz