Embed Size (px)

Citation preview

G-24 Discussion Paper Series

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT

UNITED NATIONS

CENTER FORINTERNATIONALDEVELOPMENTHARVARD UNIVERSITY

Growth After the Asian Crisis:What Remains of the East Asian Model?

Jomo K.S.

No. 10, March 2001

G-24 Discussion Paper Series

Research papers for the Intergovernmental Group of Twenty-Fouron International Monetary Affairs

UNITED NATIONSNew York and Geneva, March 2001

CENTER FOR INTERNATIONAL DEVELOPMENTHARVARD UNIVERSITY

UNITED NATIONS CONFERENCE ONTRADE AND DEVELOPMENT

Note

Symbols of United Nations documents are composed of capitalletters combined with figures. Mention of such a symbol indicates areference to a United Nations document.

*

* *

The views expressed in this Series are those of the authors anddo not necessarily reflect the views of the UNCTAD secretariat. Thedesignations employed and the presentation of the material do notimply the expression of any opinion whatsoever on the part of theSecretariat of the United Nations concerning the legal status of anycountry, territory, city or area, or of its authorities, or concerning thedelimitation of its frontiers or boundaries.

*

* *

Material in this publication may be freely quoted; acknowl-edgement, however, is requested (including reference to the documentnumber). It would be appreciated if a copy of the publicationcontaining the quotation were sent to the Editorial Assistant,Macroeconomic and Development Policies Branch, Division onGlobalization and Development Strategies, UNCTAD, Palais desNations, CH-1211 Geneva 10.

UNCTAD/GDS/MDPB/G24/10

UNITED NATIONS PUBLICATION

Copyright © United Nations, 2001All rights reserved

iiiGrowth After the Asian Crisis: What Remains of the East Asian Model?

PREFACE

The G-24 Discussion Paper Series is a collection of research papers preparedunder the UNCTAD Project of Technical Support to the Intergovernmental Group ofTwenty-Four on International Monetary Affairs (G-24). The G-24 was established in1971 with a view to increasing the analytical capacity and the negotiating strength of thedeveloping countries in discussions and negotiations in the international financialinstitutions. The G-24 is the only formal developing-country grouping within the IMFand the World Bank. Its meetings are open to all developing countries.

The G-24 Project, which is administered by UNCTAD’s Macroeconomic andDevelopment Policies Branch, aims at enhancing the understanding of policy makers indeveloping countries of the complex issues in the international monetary and financialsystem, and at raising awareness outside developing countries of the need to introduce adevelopment dimension into the discussion of international financial and institutionalreform.

The research carried out under the project is coordinated by Professor Dani Rodrik,John F. Kennedy School of Government, Harvard University. The research papers arediscussed among experts and policy makers at the meetings of the G-24 Technical Group,and provide inputs to the meetings of the G-24 Ministers and Deputies in their preparationsfor negotiations and discussions in the framework of the IMF’s International Monetaryand Financial Committee (formerly Interim Committee) and the Joint IMF/IBRDDevelopment Committee, as well as in other forums. Previously, the research papers forthe G-24 were published by UNCTAD in the collection International Monetary andFinancial Issues for the 1990s. Between 1992 and 1999 more than 80 papers werepublished in 11 volumes of this collection, covering a wide range of monetary and financialissues of major interest to developing countries. Since the beginning of 2000 the studiesare published jointly by UNCTAD and the Center for International Development atHarvard University in the G-24 Discussion Paper Series.

The Project of Technical Support to the G-24 receives generous financial supportfrom the International Development Research Centre of Canada and the Governments ofDenmark and the Netherlands, as well as contributions from the countries participatingin the meetings of the G-24.

GROWTH AFTER THE ASIAN CRISIS:WHAT REMAINS OF THE EAST ASIAN MODEL?

Jomo K.S.

University of Malaya, Kuala Lumpur, Malaysia

G-24 Discussion Paper No. 10

March 2001

viiGrowth After the Asian Crisis: What Remains of the East Asian Model?

Abstract

This paper focuses on the prospects for sustained development in the four East Asianeconomies most adversely affected by the crises of 1997/98. These include all three second-tierSouth-East Asian newly industrializing countries (NICs) – Indonesia, Malaysia and Thailand –as well as the Republic of Korea, the most adversely affected of the first-generation newlyindustrialized economies (NIEs). The first section critically examines the East Asian modelpresented by the World Bank’s “East Asian Miracle” (1993). The study emphasizes the varietyof East Asian experiences. The three second-tier South-East Asian experiences are shown to bequite distinct from, and inferior to, those of the first-generation NIEs, especially the Republic ofKorea and Taiwan Province of China.

The circumstances leading to the onset of the East Asian crises of 1997/98 are then reviewedto assess whether and how the East Asian “models” may have contributed to the crises.Macroeconomic indicators in Malaysia and the three most crisis-affected economies – i.e.Indonesia, the Republic of Korea and Thailand – are reviewed to establish that, despite somemisdemeanours, the crises cannot be attributed to macroeconomic profligacy. After reviewingthe causes of these crises, the role of international financial liberalization and the reversal ofcapital inflows are emphasized. Nevertheless, the trend towards further financial liberalizationcontinues. Malaysia is shown to have been less exposed as a result of restrictions on foreignborrowings as well as stricter bank regulations, but more vulnerable owing to the greater roleof capital markets compared to the other three economies in the region. The role of the IMF andfinancial market expectations in exacerbating the crises is also considered.

The emerging discussion begins by asserting that economic recovery in East Asia since1999 – especially in Malaysia and the Republic of Korea – has been principally due to successfulreflationary measures, both fiscal and monetary. The main institutional reforms currently claimedas urgent to protect the four affected economies from future crises and to return them to theirprevious high growth paths are critically assessed. It is argued that the emphasis by the IMFand the financial media on corporate governance reforms has been misguided and that suchreforms are not really necessary for recovery. Instead of the Anglo-American-inspired reformscurrently proposed, reforms should create new conditions for further “catching-up” throughoutthe region. Although the prospects for reform of the international financial system remain dim,a reform agenda in the interests of the South is outlined.

Globalization, including international financial liberalization, has reduced the scope forselective interventions so crucial to the catching-up achieved during the East Asian miracleyears. However, the process has been uneven and far from smooth, leaving considerable roomfor similar initiatives more appropriate to new circumstances. In any case, it is unlikely thatglobalization will ever succeed in fully transforming all other national economic systems alongAnglo-American lines. The emerging hybrid systems have not really advanced late developmentefforts. There is an urgent need to understand better the full implications of globalization andliberalization in different circumstances so as to identify the remaining scope for nationaldevelopmental initiatives.

ixGrowth After the Asian Crisis: What Remains of the East Asian Model?

Table of contents

Page

Preface ........................................................................................................................................... iii

Abstract .......................................................................................................................................... vii

I. Introduction ............................................................................................................................. 1

II. The East Asian Miracle .......................................................................................................... 2

III. East Asian differences ............................................................................................................ 6

A. South East Asia’s ersatzness ............................................................................................... 8B. South-East Asian weaknesses ........................................................................................... 10

IV. The East Asian débâcle ......................................................................................................... 11

A. Crisis and contagion ......................................................................................................... 12B. From miracle to débâcle ................................................................................................... 12C. Consequences of financial liberalization .......................................................................... 14D. Crises of a new type .......................................................................................................... 16E. Reversible capital flows .................................................................................................... 17F. Financial liberalization ..................................................................................................... 21G. The role of IMF ................................................................................................................ 23H. The roots of crises: a summary ......................................................................................... 25

V. Reforms and recovery ........................................................................................................... 26

A. International reform for the better? .................................................................................. 26B. Macroeconomic recovery ................................................................................................. 27C. Reform of corporate governance ...................................................................................... 30D. New international financial architecture .......................................................................... 32

VI. Reforming East Asia for sustainable development ............................................................ 34

A. Exchange rate appreciation and growing imports ............................................................ 34B. FDI slowdown................................................................................................................... 35C. Slow technological progress ............................................................................................. 36D. New investment policies in South East Asia .................................................................... 37

VII. Prospects ................................................................................................................................ 42

VIII. Concluding remarks ............................................................................................................ 43

Notes .......................................................................................................................................... 46

References .......................................................................................................................................... 48

Appendix .......................................................................................................................................... 51

1Growth After the Asian Crisis: What Remains of the East Asian Model?

I. Introduction

From the 1980s, and especially in the early andmid-1990s, there was growing international recog-nition of the sustained rapid economic growth,structural change and industrialization of the EastAsian region. There has also been a tendency to seeEast Asia as much more of an economically inte-grated region than it actually is, and a correspondingtendency to see economic progress in the region asbeing similar in origin and nature. Terms such as the“Far East”, “Asia-Pacific”, “Pacific Asia”, “EastAsia”, “yen bloc”, “flying geese”, “tigers”, “mini-dragons”, and so on, have tended to encourage thisperception of the region as far more economicallyintegrated and similar than it actually is.

The World Bank (1993) argued that of the eighthighly performing (East) Asian economies (HPAEs)identified in its study, The East Asian Miracle,1 threeSouth-East HPAEs – namely Indonesia, Malaysia andThailand – provided the preferred models for emu-lation by other developing countries. Yoshihara

(1988) had earlier argued that South-East Asianeconomies were characterized by ersatz capitalismbecause of the compromised and inferior role of theirstates, their discriminatory treatment of ethnic Chi-nese and their failure to develop better technologicalcapabilities. Jomo et al. (1997) criticized the WorldBank’s claims that the South-East Asian highly per-forming economies were superior models foremulation, pointing to various differences suggest-ing the inferiority of South East Asia’s economicachievements.

The East Asian currency and financial crises of1997/8 radically transformed international percep-tions and opinion about the East Asian experiences,with earlier praise quickly changing into severe con-demnation. This was most obvious with regard tothe issue of business government relations, whichhad previously been characterized as key to the EastAsian success story. Instead, these often intimate re-lations have since been denounced as “crony capi-talism” responsible for the onset as well as theseverity of the crisis (Backman, 1999; Clifford andEngardio, 2000). Various accounts (Jomo, 1998;

GROWTH AFTER THE ASIAN CRISIS: WHATREMAINS OF THE EAST ASIAN MODEL?*

Jomo K.S.

* I am very grateful to Dani Rodrik for his flexible and consultative approach, to Liew San Yee for his research assistance, andto Din Merican for his editorial suggestions, as well as to Chang Ha-Joon, Chin Kok Fay, Joseph Lim, Pasuk Phongpaichit, ShinJang-Sup and You Jong-Il for their help with tracking down references and materials. Needless to say, the usual caveats apply.

2 G-24 Discussion Paper Series, No. 10

Furman and Stiglitz, 1998; Radelet and Sachs, 1998a;Krugman, 1999a; Bhagwati, 1998) have since char-acterized the crises as the consequence of interna-tional financial liberalization and related increasesin easily reversible international capital flows. Theseaccounts have also emphasized the role of the Inter-national Monetary Fund (IMF), particularly its policyprescriptions and conditionalities in exacerbating thecrises.

This paper will focus on the four East Asianeconomies most adversely affected by the crises of1997/98. These include all three second-tier South-East Asian newly industrializing countries (NICs):Indonesia, Malaysia and Thailand, as well as theRepublic of Korea – the most adversely affected first-generation newly industrialized economy. The nextsection of this paper will critically examine the so-called East Asian model, especially as presented bythe World Bank (1993). The third section will thenemphasize the variety of East Asian experiences(Perkins, 1994). The second-tier South-East Asianexperiences will then be shown to be distinct fromand inferior to those of the first-generation newlyindustrialized economies (NIEs), especially the Re-public of Korea and Taiwan Province of China(elaborated in Jomo, 2001b, 2001c). The fourth sec-tion will review the circumstances leading to the onsetof the East Asian crises of 1997/98, and examinewhether and how the East Asian “models” may havecontributed to the crises.

The fifth section will begin with a brief reviewof the reflationary Keynesian policies leading tomacroeconomic recovery since 1999. The section willthen draw on the preceding analyses to critically as-sess the main institutional reforms currently beingclaimed as necessary to protect the four crisis-af-fected economies from future crises and to returnthem to their previous high growth paths. This willmainly dwell on discussions of the need for reformof corporate governance as well as the internationalfinancial architecture. The sixth section considers theimplications of pre-crisis developments and morerecent challenges. In particular, it reviews some ex-change rate dilemmas, the slowdown of regionalforeign direct investment (FDI), limited technologi-cal capabilities and new investment promotionstrategies. The penultimate section reviews the pros-pects for sustainable development in the region inlight of the foregoing, while the concluding remarksconsider the likelihood of convergence – and the vi-ability of distinct development models – in the faceof continued globalization and Anglo-American in-spired liberalization.

II. The East Asian Miracle2

The most important and influential documentwhich attempted to explain the rapid growth, struc-tural change and industrialization of much of EastAsia in the last three decades or more has been TheEast Asian Miracle study (EAM) published by theWorld Bank in 1993. As is now well-known (Wade,1996), the World Bank did not commission the studyon its own volition, and with the East Asian finan-cial crisis since mid-1997 there are many in the Bankwho would now wish to disown the study. In fact, itappears that the study was undertaken by the Bankat the behest of Shiratori, the Japanese ExecutiveDirector or government representative on the Bank’sboard. Shiratori had pointed out the region’s rapidgrowth and structural change in sharp contrast to theBank’s poor experience with structural adjustmentprogrammes (SAPs) in Latin America, Africa andother parts of the world, and with the transitions itwas trying to engineer in Eastern Europe. The SAPsand transitions had generally turned out to be veryproblematic, even causing severe recessions in sev-eral of these economies and, at best, rather slow andunimpressive growth rates elsewhere. Shiratori sug-gested that the Bank should learn and draw lessonsfrom the experiences of East Asia where, by the early1990s, more than half a dozen countries had grownat average rates exceeding 6 per cent per annum forat least a quarter of a century. Shiratori offered theJapanese government funding for such a study, whichthe Bank then undertook.

In EAM, the World Bank identified eight high-performing Asian economies: Japan; the fourfirst-generation NIEs or NICs, dragons or tigers,namely the Republic of Korea, Taiwan Province ofChina, Hong Kong (China) and Singapore; and thethree second-generation South-East Asian NICs,namely Malaysia, Indonesia and Thailand. Interest-ingly, China was left out, perhaps because the Chineseexperience would upset the Bank’s analysis and con-clusions in very fundamental ways. EAM recognizesthat the likelihood of eight relatively contiguouseconomies growing so rapidly for such a sustainedperiod of time is less than one in 60,000. Yet, it doesnot acknowledge the significance of geography –unlike the later 1997 Emerging Asia (EA) study ledby the Harvard Institute of International Develop-ment (HIID) for the Asian Development Bank(ADB).

With the publication and release of EAM, theBank seemed to be shifting its position from the sort

3Growth After the Asian Crisis: What Remains of the East Asian Model?

of neo-liberalism, or the extreme economic liberal-ism of the 1980s, to acknowledging an importantdevelopmental role for the state in the 1990s. EAMappeared to have had something to do with this shift.This impression has been reflected in other Bankactivities and publications, especially the 1997 WorldDevelopment Report which seemed to advocate ef-fective, rather than minimalist, states (World Bank,1997).

In EAM, the Bank identified at least six typesof state interventions, which it saw as having beenvery important for East Asian development. It ap-proved of the first four, deemed to be functionalinterventions, but was more sceptical of the last two,deemed to be strategic interventions. Functional in-terventions are said to compensate for marketfailures, and are hence necessary and less distortingof markets, while strategic interventions are consid-ered to be more market-distorting. The two types ofstrategic interventions considered are in the areas offinance, specifically what it calls directed (i.e. sub-sidized) credit, and international trade, while the fourfunctional interventions the Bank approved of are:

(i) Ensuring macroeconomic discipline and macro-economic balances;

(ii) Providing physical and social infrastructure;

(iii) Providing good governance more generally; and

(iv) Raising savings and investment rates.

It is very important to compare what has actu-ally happened in East Asia with the way the WorldBank has presented this. Beginning with the impor-tance of macroeconomic discipline, there is very littledispute that maintaining macroeconomic balanceshas been important in East Asia. But what the Bankconsiders to be the acceptable parameters of macr-oeconomic discipline may be disputed. One finds,for instance, that inflation was generally kept under20 per cent in the HPAEs, but it was certainly notalways kept below 10 per cent in all the economies.In other words, single-digit inflation was neither apolicy priority nor always ensured in some East Asiancountries during their high growth periods.

Similarly, when considering other macroeco-nomic balances such as the fiscal balance and thecurrent account of the balance of payments, one findsthat the balances were not always strictly maintainedin the way the Fund and the Bank now seem to re-quire of much of the developing world. Malaysia andThailand have had relatively high current accountdeficits throughout the 1990s, while other countries

with much lower deficits were not spared the recentcurrency attacks and massive depreciation.

On physical and social infrastructure, until the1980s, the Bank would probably have gone alongwith what the East Asians have done. However, sincethe 1980s, the Bank has increasingly seemed to rec-ommend privatization and private provision ofphysical infrastructure. With the exception of HongKong (China), most physical infrastructure in EastAsia has been provided by governments until fairlyrecently, when there have been the beginnings ofprivatization in the provision of physical infrastruc-ture, which has become the basis for powerful privatemonopolies associated with “crony capitalism”.

The role of government has been extremelyimportant in providing so-called social infrastructureand services in East Asia. In some of its other docu-ments, the Bank seems to acknowledge this, butnonetheless it recommends a more modest role forgovernment in the provision of social infrastructure.For instance, the Bank recommends universal andfree primary education, but does not recommend thesubsidization of education beyond the primary level,when the “user/consumer” (student) should bear thefull costs of education as far as the World Bank isconcerned. This would have had very serious conse-quences in terms of human resource development, ifone contrasts that recommendation with the actualexperience of East Asia. To give some sense of howimportant government support for education has beenbeyond the primary level, in the Republic of Koreatoday over 40 per cent of young people attend uni-versities. Thailand has a percentage of close to 20 percent, Indonesia has 10 per cent, and most of the first-generation East Asian NIEs have well over 25 percent, generally over 30 per cent.

The notion of good governance is somewhatambiguous and often used rather tautologically. Whenthings are going well, it is assumed that there mustbe good governance, and conversely if things are notgoing well. So one does not really have much of anexplanation of good economic performance by sim-ply invoking good governance, although it is widelytouted these days, sometimes ad nauseum. There have,however, been important efforts to try to understandthe factors contributing to good governance. In thisregard, the 1997 World Development Report has beenimportant and useful. It seems from the East Asianexperience that what was called “strong government”(in Gunnar Myrdal’s sense) has been an importantnotion, though one often misunderstood and wronglyassociated with authoritarian government.

4 G-24 Discussion Paper Series, No. 10

What is called “embedded autonomy” has be-come a useful way to try to understand what theconditions of good governance are. Here, embedded-ness refers to the institutional capacity and capabilityof the governments concerned to effectively providethe coordination necessary for rapid capital accumu-lation and economic transformation. Autonomy isprimarily understood to be from “vested interests”,“special interest groups”, “distribution coalitions”and “rent seekers” who, in more favourable or con-ducive circumstances, would be able to influencepublic policy to their own advantage. Embedded au-tonomy is therefore considered to have been verycrucial in ensuring that regimes in East Asia couldeffectively serve as developmental states.

The role of the state in encouraging savings andpromoting investments is also generally accepted.However, much of East Asia’s large savings is actu-ally comprised of corporate or firm savings, ratherthan just household savings. Household savings inEast Asia are not spectacularly higher than in therest of the world, except in Malaysia and Singapore.The difference in Malaysia and Singapore is due tothe mandatory or forced savings schemes introducedin the late colonial period and the relatively high pro-portion of the working class or wage owners as aproportion of the labour force. The latter is particu-larly true in the case of Singapore, but is also notinsignificant in the case of Malaysia. The significanceof coerced savings should be noted because of thepopular view that the high savings and investmentrates in the region exist because East Asians are cul-turally, if not congenitally, thrifty.

The large contribution of high corporate sav-ings implies that firms have often been able to enjoyvery high profit rates due to government interven-tions, subsidies, tax breaks and other incentives forparticular types of investments favoured by the gov-ernments, enabling the firms concerned to enjoyhigher “rents”. But more important is that attractiveconditions (e.g. tax incentives and other induce-ments), largely created by governments, have inducedhigh rates of reinvestment of the huge profits of firms.How have such high rates of reinvestment been se-cured? In some East Asian countries they have beenassured by the very strict controls on foreign ex-change outflows. Capital flight was made verydifficult in certain East Asian economies, especiallyin the Republic of Korea and Taiwan Province ofChina, during their high growth periods. High levelsof reinvestment have also been successfully inducedby structuring laws so that reinvestment of profits is

subject to little or no tax, or by offering other incen-tives to undertake state-favoured investments.

In pursuing these supposedly functional inter-ventions, the East Asian governments were not justmarket-conforming, but instead played importantroles, which have been more than simply market-augmenting, as suggested by EAM. On the morecontroversial, so-called strategic interventions in fi-nance and international trade, the Bank almostgrudgingly concedes that financial interventions havebeen important and successful in East Asia, particu-larly in North East Asia – i.e. in Japan, the Republicof Korea and Taiwan Province of China. However,the Bank implies that nobody else is capable of suc-cessfully pursuing the types of policies that the NorthEast Asians successfully implemented, because statecapabilities in North East Asia have been almostunique and are non-replicable.

Creating the conditions for attracting invest-ment, both domestic private investment as well asforeign investment, has had much more to do withreforming incentives and governance more generallyto attract particular types of investments to generatespecific sources of economic growth, rather than lib-eralizing financial markets as such. South-East Asiangovernments, notably Singapore and Malaysia, haveespecially sought to attract FDI into areas where in-digenous industrial capabilities were not expectedto become internationally competitive. Venture capi-tal markets, rather than the usual stock markets, tendto be more supportive of developing new industrialand technological capabilities.

Attracting FDI should, however, be distin-guished from capital account liberalization. Chile,which has been very FDI-friendly, has imposed fairlyonerous obstacles on easy exit, probably limitingcapital inflows, especially of a short-term nature.Capital account liberalization has come under re-newed consideration, following the East Asianfinancial crisis, since mid-1997, precipitated by aneventually successful currency attack on the over-valued Thai baht, and greatly exacerbated by herd-like panicky withdrawals from the entire South-EastAsian region, inducing currency and stock marketcollapses (Jomo, 1998). Those who control finan-cial assets usually enjoy disproportionate politicalinfluence in most contemporary economies, andespecially in developing ones. Hence, liberalizingfinancial markets alone, without sufficient induce-ments for a not easily reversed and sustained netinflow of portfolio investments, may well causegreater outflows rather than inflows.

5Growth After the Asian Crisis: What Remains of the East Asian Model?

Why did the Bank give a positive evaluation offinancial interventions in North East Asia despitetheir clear violation of market norms? A few ana-lysts might suggest that the evidence offers no otherpossible conclusion, but most observers would dis-pute this, especially given the ongoing problems ofthe beleaguered Japanese financial system. Anotherexplanation is the influence and unorthodox neo-classical analysis of Joseph Stiglitz, the principalauthor of this part of EAM. The more cynical mightpoint out that the study was funded by the JapaneseMinistry of Finance, and it is hardly likely that theWorld Bank would bite the hand which feeds it bynegatively evaluating the Ministry’s record. Therehas been significant historical rivalry between theFinance Ministry and the bureaucratically weakerMinistry of International Trade and Industry (MITI).Hence, some observers suggest that it is not surpris-ing that the Bank study did not criticize the role ofthe Ministry of Finance of Japan, but was less sym-pathetic to MITI and international trade-relatedindustrial policy.

The evaluation in EAM of the record of Japan’sMITI and its counterparts elsewhere in the region ismore predictable, arguing that government interven-tions have been trade-distorting and, more impor-tantly, generally unsuccessful in East Asia, with someminor exceptions. However, contrary to the impres-sion given by the study, the governments of Japan,the Republic of Korea and Taiwan Province of Chinadid pursue import substituting industrialization poli-cies from the 1950s, but soon also pursued export-orientation so as to ensure that their industries quicklybecame internationally competitive by requiring arapid switch from import substitution to export-orientation.

In many cases, infant industries were generallyprovided with effective protection conditional onexport promotion, which had the effect of forcingthe firms and industries concerned to quickly becomeinternationally competitive. By giving firms protec-tion for certain periods, depending on the product,and by also requiring that they begin exporting cer-tain shares of output within similarly specifiedperiods, strict discipline was imposed on the firmsin return for the temporary trade protection they en-joyed. Quantitatively, such policies forced firms topush down their own production costs as quickly aspossible, for example by trying to achieve greatereconomies of scale and accelerating progress uplearning curves. Requiring exports has also meantthat producers had to achieve international qualitystandards quickly, which technologically imposed

pressures on progress in terms of products as well asprocesses. With strict discipline imposed, but alsosome flexibility in enforcement, many firms man-aged to rapidly achieve international competitiveness.

Thus, the East Asian miracle was characterizedas principally due to export-led growth. But, whileexports tend to rise with trade liberalization in theshort term, imports also tend to rise strongly, espe-cially if the domestic currency appreciates in realterms. Thus, trade liberalization is inclined to limitor only weakly supplement domestic effective de-mand. Hence, while increased international trade mayenhance growth, the added stimulus tends to be muchless than presumed by proponents of trade liberali-zation. Despite efficiency gains from trade liberali-zation, increased exports do not necessarily ensurestronger domestic economic growth.

EAM and its supporting studies have impliedand argued that South East Asia began to take offafter it reversed such trade interventions. Hence, themid-1980s are portrayed by the Bank as a period ofeconomic liberalization and deregulation leading toeconomic recovery and rapid growth and industri-alization. The facts are more complicated (Jomo etal., 1997; Jomo 2001b). There certainly was somederegulation during this period, but there also wassome new private sector-oriented regulation, moreappropriate to the new industrial policy priorities ofthe governments of Indonesia, Malaysia, Singaporeand Thailand.

Given international trends and pressures inrecent years, trade liberalization has become increas-ingly irresistible, and hence inevitable. But bypro-actively accelerating the apparently inevitable,some advantage may be regained by deliberatesequencing and timing of trade liberalization. Un-fortunately, many trade policy instruments have beenexcluded by recent trends in international trade gov-ernance and are no longer available as options forgovernments. For example, local content require-ments were phased out with the conclusion of theUruguay Round of negotiations under the GeneralAgreement on Tariffs and Trade (GATT). However,despite considerable diminution, there still remainssome scope for trade policy initiatives in support ofindustrial policy.

It is instructive to consider some of the impor-tant differences among the East Asian economies,particularly whether all of East Asia has been pro-ceeding inexorably in the same basic direction in asimilar manner. Although the Bank does not really

6 G-24 Discussion Paper Series, No. 10

extol an East Asian model as such, the Bank studyhas often been read as offering one, or perhaps twovariants. However, more generally, as suggested ear-lier, there has been much talk about East Asia in thesingular, as constituting a flock of “flying geese” oreven a “yen bloc”. Many observers even speak ofgeneric East Asian models, approaches or ways ofdoing things. In response to the financial crisis sincemid-1997, as sentiment on East Asia has turned sour,there have been similar broad-brushed sweeping gen-eralizations about East Asian “crony capitalism”.

III. East Asian differences

While many lessons may certainly be drawnfrom the East Asian experience, they are far fromconstituting a single model. Some of the major dif-ferences in East Asia are themselves very instructive.In the case of the role of FDI, one finds tremendouscontrasts, especially between South East Asia andthe rest of East Asia. In the case of Singapore, FDIhas constituted about a quarter of gross domesticcapital formation. In the case of Malaysia, the pro-portion has been about 15 per cent. At the other endof the spectrum, in the case of Japan and the Repub-lic of Korea, the percentage has long been below 2 percent. Some of the other countries fall between thesetwo extremes, with very few near the mean for de-veloping countries of around 5 per cent. Thosemost successful in developing industrial capacitiesand capabilities in East Asia – namely Japan, theRepublic of Korea and Taiwan Province of China –have hardly depended on FDI, which has only playeda relatively small role.

The far greater importance of FDI in South EastAsia has been due to a variety of reasons, which havenot been entirely economic. One of the reasons forthe major role of FDI in Singapore and Malaysia ispolitical. After Singapore seceded from Malaysia in1965, the Lee Kuan Yew government decided that toensure its own survival, it would be best to attractforeign investment in massive quantities to Singapore,so that the major foreign powers would quickly de-velop a stake in the survival of the Singapore regime.Of course, this preference was subsequently justi-fied in terms of improving access to the technologyfrontier. In other words, political considerations havebeen a very important reason for attracting, evenprivileging, foreign investment in Singapore.

In the case of Malaysia, the country has longhad ethnic rivalries and an ethnic affirmative action

policy. This may have incited some policy makers totry to limit ethnic Chinese control over the economyby encouraging FDI so as to reduce proportionatelysuch control. Again, one finds a political motivationfor the important role of FDI in Malaysia. Singaporeand Malaysia are exceptions, which need to be ex-plained politically, rather than simply by economicconsiderations.

Clearly, there is considerable diversity in therole and performance of public investments, includ-ing state-owned enterprises (SOEs), in East Asia,including within South East Asia. In Japan, HongKong (China) and the Republic of Korea, state-owned enterprises are hardly important today, buthistorically were so in Japan at the end of the nine-teenth century and in the twentieth century beforethe Second World War. Conversely, however, morerecently one finds that state-owned enterprises havebeen extremely important in Singapore and TaiwanProvince of China; this is partly explained by politicalfactors, but there are also economic considerations.Very importantly, the performance of these enter-prises has also been quite impressive.

In the case of Singapore, for instance, the singlelargest foreign investor – i.e. the biggest Singaporeanfirm investing abroad – has been the GovernmentInvestment Corporation. For quite a number of yearsin the 1990s, the average rate of return for its invest-ments was higher than for all major financialinvestment firms in the City of London as well as onWall Street. Such SOE success poses a challenge forthose who insist that state-owned enterprises arebound to fail because of property rights and princi-pal-agent arguments.

There is also tremendous diversity in the roleof industrial and technology policies in East Asia.One extreme, of course, is Hong Kong (China), wherethere is relatively little industrial policy, althoughmore than most opponents of industrial policy careto admit. It is far more detailed and sophisticated inJapan and the Republic of Korea at the other end ofthe spectrum. In the Republic of Korea, industrialpolicy is largely oriented towards the chaebols,whereas in Taiwan Province of China, much moreemphasis is given to medium-sized and relativelysmaller enterprises. There have also been differentorientations, emphases and instruments in industrialpolicy in the region. For example, the role of tradepolicy has been very important in almost all econo-mies in the region except Hong Kong (China) andSingapore, while financial policy has been impor-tant in all the countries, including Singapore, but

7Growth After the Asian Crisis: What Remains of the East Asian Model?

again with the exception of Hong Kong (China).Since the latter’s reversion to China in mid-1997,there have been many indications of the possible in-troduction of an industrial policy for the territory,presumably in line with its new status and China’senvisaged role for the de-industrialized financial cen-tre. There have also been very important differencesin the role of technology policy in the region.

As noted earlier, the World Bank recommendsthat the rest of the developing world emulate SouthEast rather than North East Asia. There are very im-portant differences between North East Asia andSouth East Asia underlying the Bank’s recommen-dations. These differences oblige us to recognize theachievement of the first-tier East Asian NIEs (includ-ing Singapore) – rather than the transformation ofthe second-tier South-East Asian NICs – as far moreimpressive and superior in terms of economic per-formance.

Despite the much greater resource wealth ofSouth East Asia, one finds that growth performancehas been superior in North East Asia over the longterm. Over the period studied by the Bank – i.e. fromthe 1960s until the early 1990s – the average growthrate in the former was in the region of about 8 percent, compared to about 6 per cent for the latter. A2 per cent difference, compounded over a period ofa quarter century or more, adds up to a lot. Very im-portantly also, population growth, except in HongKong (China) owing to immigration from China andperhaps Singapore, has been much lower in theformer compared to the latter. The immigration intoHong Kong (China) and Singapore involves a veryhigh proportion of people in the labour force, thusraising the average labour utilization rate. Politicalfactors have also ensured far more equitable distri-bution of economic welfare than would otherwisehave been the case in the first-tier NIEs, whereas suchconsiderations have been less influential in the sec-ond-tier South-East Asian NICs, except perhaps forMalaysia due to its ethnic “social contact”.

Hence, the improvements in per capita incomeand economic welfare have been much more signifi-cant in North East Asia, compared to South East Asia(with the exception of Singapore), despite the rela-tive resource wealth of the latter. In other words, whatSouth East Asia has achieved has been less impres-sive in some critical ways. Drawing from thiscontrast, one could argue that resource wealth is nota blessing but a curse insofar as it postpones the im-perative to industrialize.

As noted earlier, North East Asia has generallyhad a much more sophisticated and effective indus-trial policy compared to South East Asia. Thisaccounts, in no small way, for the very importantdifferences in industrial and technological capabili-ties between North East and South East Asia. Also,industrialization in the latter is still primarily drivenby FDI, whereas industrialization in the former isprimarily an indigenous phenomenon.

It is now generally recognized that Japan andthe first-generation NIEs began to industrialize in thevery specific economic and political conditions of aparticular cold war historical conjuncture. North EastAsia grew rapidly in the immediate post-war periodunder a “security umbrella” provided by the Ameri-cans, especially after the cold war began. Besidessubsidizing military expenditure and providing gen-erous aid, the Americans were anxious for them to“succeed” economically in order to be show-casedas attractive alternatives to those under communistrule or influence. Hence, the Americans were quitehappy to tolerate trade, finance, investment, intel-lectual property and other policies violatinglaissez-faire market or neo-liberal economic normsthat they are now strongly opposed to, especiallyfollowing the end of the cold war. These favourableconditions are simply not available to others, andhence their experiences are said to be almost impos-sible to emulate.

In arguing why other developing countriesshould not imitate the first-generation East AsianNIEs, it is now often argued that their state capabili-ties are almost unique and virtually impossible forany other regimes to emulate. The more cultural ex-planations suggest that this has something to do withthe East Asian Confucian legacy of meritocracy.However, it is important to remember that the sup-posedly Confucian Kuomintang government ofTaiwan was the same regime driven out of mainlandChina by the communists because of its incredibleincompetence and corruption. One could say the sameof the Rhee regime in South Korea in the 1950s, aswell as of the Chun, Roh and Kim Young Sam re-gimes in the 1980s and 1990s. Japan has hardly beenscandal-free in recent years, and most observerswould trace recently disclosed abuses to the natureof post-war Japanese political economy. The supe-rior policy-making and implementation capabilitiesof the North-East Asian decision makers was, at leastuntil recently, widely acknowledged, but this, in it-self, does not prove the existence of thoroughlycompetent and incorruptible policy makers.

8 G-24 Discussion Paper Series, No. 10

There is also the claim that East Asia cannot beemulated owing to its very different initial conditions.Such differences are real, but often exaggerated.There is no doubt that Japan and the first-tier EastAsian NIEs are now distinguished by high levels ofeducation. However, the level of literacy in SouthKorea in 1950 was lower than the literacy rate incontemporary Ethiopia (which has one of the lowestrates in Africa today); thus the level of educationachieved by contemporary Koreans reflects the tre-mendous investments consecrated to developinghuman resources in East Asia in the post-war pe-riod, as the region then was generally not veryadvanced despite, or perhaps even because of, its(elitist) Confucian legacy. But by the end of the1960s, literacy rates had gone up greatly for the first-generation East Asian NIEs after enormous resourceshad been poured into education in the preceding twodecades.

In discussing initial conditions, some fortuitouscircumstances must also be considered. Japan, SouthKorea and Taiwan Province of China all had rela-tively virtuous American-sponsored land reformsshortly after the end of the war (Hsiao, 1996). In Ja-pan, there also was significant redistribution of othernon-land assets, most notably of the pre-war andwartime zaibatsu industrial conglomerates. Much ofthe motivation for such re-distributive reforms was,of course, anti-communist, i.e. to undermine andminimize support for the communists by those de-siring asset redistribution.

The implications of asset redistribution in Ja-pan were considerable. Ironically, the Americanswere not uninfluenced by the left, partly because ofthe nature of the wartime anti-Axis alliance and thenature of the most influential scholarships available(Tsuru, 1993). During the post-war American occu-pation of Japan, it was widely presumed that thezaibatsu “military industrial complex” had been re-sponsible for the militarization of pre-war Japan. Sothe Americans decided to dismantle the zaibatsu, andforcibly broke family control over them, selling offthe assets in interesting ways with important conse-quences. To ensure popular acceptance of this policy,preference was first given to employees, and then tolocal communities – thus developing worker andcommunity stakes in the companies and the basis forwhat is now called a stakeholder economy. Thus, thestakeholder economy was created by deliberatelyre-distributive policies that have had many conse-quences now considered to be peculiarly Japanese.Similarly, many now acknowledge the influence ofthe “human relations” school of industrial relations

on the post-war development of guaranteed life-longemployment and the seniority wage system, both ofwhich have effectively developed a strong employeecommitment to the fate of their firm. There are nu-merous other ostensibly typically Japanese features,many of which were not inherited from the Edo pe-riod or even developed autochthonously during theMeiji period; quite a few are actually relatively re-cent innovations, with rather virtuous consequences.

There are important lessons to be drawn fromEast Asia, but clearly there is no single East Asianmodel as such, and most certainly not one that canaccommodate all the different experiences of SouthEast Asia. Considering the historicity of the devel-opment experiences, it does not make much sensefor any other country to think in terms of trying toemulate any particular economy in the South Eastregion or, for that matter, East Asia more generally.There are many reasons why most will find it impos-sible to imitate any other country even if they wantedto. But even in drawing lessons, it will be importantto recognize the distinctive nature of the South-EastAsian experiences.

A. South East Asia’s ersatzness

There is considerable evidence that the threeSouth-East Asian economies of Indonesia, Malaysiaand Thailand have some common characteristics andpolicies that distinguish them from the other high-growth economies of East Asian (Jomo et al., 1997).Most importantly, the region’s high growth econo-mies have relied heavily on FDI to develop most oftheir internationally competitive industrial capabili-ties; government interventions have also been morecompromised by considerations besides economicgrowth and late industrialization, especially redistri-bution and rent capture. Consequently, industrialpolicy has also varied in nature, quality and effec-tiveness. Yet, it will be shown that the South-EastAsian economies would not have achieved so muchwithout selective government interventions, includ-ing industrial policy.

The conditions contributing to, and the natureof, industrialization in Indonesia, Malaysia, Singa-pore and Thailand have been quite distinct (Jomo. etal, 1997; Jomo, 2001b). The inclusion of these econo-mies as four of the eight HPAEs identified by theWorld Bank (1993) has encouraged comparison withthe record of Japan and the three of the other fourfirst-generation or first-tier East Asian newly indus-

9Growth After the Asian Crisis: What Remains of the East Asian Model?

trializing economies (NIEs): Hong Kong (China), theRepublic of Korea and Taiwan Province of China.Comparisons with other countries in South East Asiaand elsewhere are also shown in some chapters below.

South-East Asian industrialization has been farmore dominated by foreign capital (Jomo et al., 1997;Jomo, 2001b), and has, as a consequence, fewer in-dustrial and technological capabilities that may beconsidered indigenous or under national control. Theefficacy of industrial policy has thus emerged as theprimary determinant of the ability of different na-tional economies to take advantage of transnationalcapital’s relocation of productive capacities in theregion. The distinct nature of the South-East Asianeconomies and experiences (Jomo et al., 1997; Jomo,2001b) offers valuable insights into various indus-trial policy instruments, the circumstances in whichthese may work, as well as the importance of relativelyuncompromised, competent and effective state capaci-ties in ensuring desirable industrial policy outcomes.

South-East Asia’s development experienceshave been almost as diverse as those of the otherfour HPAEs identified by the World Bank (1993).South-East Asian high-performing economies havegenerally been less successful in developing indig-enous industrial and technological capabilities forvarious reasons (Jomo et al., 1997); this seems to bepartly due to the greater reliance on FDI in the re-gion for political as well as other reasons. South EastAsia’s industrialization is also less impressive in otherrespects, probably as a result of its greater naturalresource wealth and consequently weaker impera-tive to industrialize (ADB, 1997).

Industrial policy has been less elaborate, effi-cient and effective in the three South-East Asiansecond-tier NICs – Indonesia, Malaysia and Thai-land, as compared to Japan and the first-tier EastAsian NIEs, except for Hong Kong (China) but in-cluding Singapore. This is partly because stateintervention in South East Asia has been far moreabused, and hence, often seriously compromised bypolitically influential business interests. Yet, it wouldbe a mistake to “throw the baby out with the bathwater” by condemning all industrial policy in theregion. Despite various abuses and other weaknessesin implementation, some industrial policy has beencrucial to South East Asia’s rapid economic growth,structural change and late industrialization (Jomo etal., 1997).

Before the currency and financial crises of 1997/98, the South-East Asian second-tier NICs were be-

ing celebrated by the World Bank and others as thenew models for other developing countries to emu-late. In its influential 1993 publication, The EastAsian Miracle, the Bank argued that the eight HPAEs– Hong Kong (China), Japan, Republic of Korea,Singapore, Taiwan Province of China; Indonesia,Malaysia and Thailand – had achieved sustained andequitable export-led high growth and rapid industri-alization.

The Bank and others suggested that owing tothe first five HPAEs’ various exceptional character-istics, the last three South-East HPAEs were the mostappropriate examples for other developing countriesto follow. Implicit in this recommendation was theclaim that the achievements of Indonesia, Malaysiaand Thailand were similar to and comparable withthe other HPAEs in terms of growth, structural changeand industrialization. Their industrialization recordshave been significantly different from and inferiorto those of the other HPAEs, especially Japan, theRepublic of Korea, Singapore and Taiwan Provinceof China (Jomo et al., 1997; Jomo, 2001b).

Closer examination suggests that the experi-ences of Indonesia, Malaysia and Thailand, as wellas Hong Kong (China) and Singapore, more closelyapproximated the neo-classical, export-led, growthmodel than those of Japan, the Republic of Koreaand Taiwan Province of China. The latter appear tohave promoted exports very actively while also pro-tecting domestic markets, at least temporarily, todevelop domestic industrial and technological capa-bilities in order to compete internationally. Thisstrategy of temporary effective protection conditionalupon export promotion (EPconEP) can hardly beequated with trade liberalization. Recent criticisms(Baer et al., 1999) of attempts by an earlier genera-tion (for example, Ian Little, Jagdish Bhagwati, AnneKrueger) to accommodate the North-East AsianEPconEP experience within their fundamentalist freetrade advocacy paradigm, have exposed the intellec-tual sophistry of neo-classical trade economists intrying to explain away the North-East Asian successin requiring export promotion as a condition for tem-porary (national) market protection.

Besides more modest growth as well as indus-trialization, the South-East HPAEs (includingSingapore) were much more reliant upon FDI com-pared to Japan, the Republic of Korea and TaiwanProvince of China. The much greater South-EastAsian dependence on FDI raises disturbing questionsabout the actual nature of industrial and technologi-cal capacities and capabilities in these economies,

10 G-24 Discussion Paper Series, No. 10

especially in their most dynamic and export-orientedsectors. This, in turn, raises concerns about thesustainability of their growth and industrializationprocesses, especially if they are later deemed lessattractive as sites for further FDI, for example as moreattractive alternative locations become available.

B. South-East Asian weaknesses

In recent years, there has been growing recog-nition of major structural and systemic differencesamong the eight HPAEs studied by the World Bank(1993). Of these, Indonesia, Malaysia and Thailandhave been increasingly grouped as second-tier orsecond-generation South-East Asian NICs, with char-acteristics quite different from the others, and ofcourse, even among themselves. It has been arguedthat industrial policy or selective state interventionhas, for various reasons, been of much poorer qual-ity and less effective in these economies. Instead,there have been other state interventions motivatedby less developmental considerations, especially inIndonesia and Malaysia (Jomo et al., 1997). It ap-pears that such interventions bear some of theresponsibility for the vulnerability of the second-tierSouth-East Asian NICs to the factors that precipi-tated the mid-1997 financial crisis in the region.

A longer-term view of the crisis would, ofcourse, have to recognize the vulnerability of exist-ing financial systems to such “exogenous” shocks.The central banks in the region clearly fell short ofthe new challenges faced (Hamilton-Hart and Jomo,2001). National-level central banking faced a newsituation with the new international monetary sys-tem that emerged after abandonment by the UnitedStates of the Bretton Woods framework in 1971.Further international financial liberalization from the1980s on added to the new problems for the nationalmonetary authorities precisely when the role of gov-ernment in economic affairs was coming undergreater pressures for economic liberalization. Thefailure of institutional and regulatory reform to riseto new challenges posed by the changing interna-tional as well as domestic situations has to beacknowledged.

It would be erroneous to view the crises as dueto “crony capitalism” or to some similar failure ofthe policy and institutional framework supporting theaccelerated development of industrial capacities andcapabilities in the region. Yet, it would be equallyfallacious to regard the concerned economies as in-

nocent bystanders bearing no responsibility whatso-ever for what was happening. Instead, the region’svulnerability to crisis was due to inappropriate andeven irresponsible earlier policies, with importantadverse macroeconomic implications.

While official efforts to accelerate industrialtechnological progress in Indonesia, Malaysia andThailand have increased, at least since the late 1980s,the South-East Asian trio remained well behind theRepublic of Korea, Taiwan Province of China andSingapore. Domestic political priorities have oftenneglected technology policies, while policy initia-tives have also been constrained by the weakcommitments of the governments concerned. Thedominant position of foreign firms in the most dy-namic manufacturing sectors has also served as amajor deterrent to more pro-active technology de-velopment efforts. All too often, technology policieshave not been sensitive enough to sector- or indus-try-specific conditions. More worryingly, the scopefor discretionary policies has become more con-strained as global regulatory frameworks areincreasingly defined by international organizationswith enforcement capacities, as well as effectivelycoordinated and articulated investor demands. None-theless, there still is much scope and potential forinformed technology policies in the region.

With accelerated globalization and economicintegration in the past decade, the international in-vestment environment, especially in the East Asianregion, has changed considerably. Taking into con-sideration the fresh constraints imposed by newinternational regulations and commitments, as wellas the more sophisticated industries in some of theseeconomies, investment policy reform was alreadyoccurring before the 1997/98 crises. However, thecrises and its aftermath, including the conditionalitiesimposed by IMF on Indonesia and Thailand for emer-gency credit facilities, have also introduced newconstraints. Attracting new “green-field” investmentsto restore and sustain growth as well as structuralchange is all the more urgent as so much recent FDIin the region has involved mergers and acquisitions.

Most accounts of the East Asian miracle haveemphasized the key contributions of educational ef-forts in raising the quality of human resourcesthroughout the region. However, once again, the ac-tual South-East Asian record in this regard has fallenwell short of the other HPAEs (Booth, 1999). Withthe exception of Singapore, educational achieve-ments in South-East Asia, including in the South-EastAsian trio, have been grossly inferior to those in the

11Growth After the Asian Crisis: What Remains of the East Asian Model?

other HPAEs. While the region’s earlier achievementsin extending primary and lower secondary school-ing have probably contributed to rapid its growth andlabour-intensive industrialization, these limited edu-cational gains may well serve as fetters to furtherprogress. (Ironically, the country with the highestshare of tertiary education in the region – the Philip-pines – has not had a particularly impressive economicgrowth record for a complex variety of reasons.)There is now considerable cause for concern thatrapid structural change, industrialization and produc-tivity gains may not be achievable in the future owingto the region’s poor educational efforts. Such find-ings and comparisons compel a reconsideration ofthe facile World Bank policy recommendation thatgovernments should concentrate on enhancing hu-man resources, but only subsidize primary schooling.

Comparing the South-East Asian trio with theRepublic of Korea and Taiwan Province of China, itis now quite clear that the latter two economies notonly achieved far more in terms of growth, industri-alization and structural change, but that incomeinequality in them has been significantly lower aswell (Jomo, 1999). While their better economic per-formance was probably due to more effectivegovernment interventions, especially selective indus-trial policy, lower inequality was probably due tosignificant asset (especially land) redistribution be-fore the high growth period, i.e. more equitable“initial conditions”. However, there is also troublingevidence that economic liberalization in recent yearsmay well have exacerbated inequalities in both EastAsian groups.

Evidence from other developing countries(Ganuza et al., 2000) suggests that more equitablegrowth has been achieved elsewhere with policymixes combining three elements: first, avoiding amacroeconomic mix of real exchange rate apprecia-tion and high domestic interest rates; second, developingand maintaining flexible systems of well targeted ex-port incentives; third, having appropriate prudentialfinancial regulation as well as capital controls to containthe negative consequences of capital flow surges.

IV. The East Asian débâcle

Although there has been considerable workcritical of the East Asian record and potential, noneactually anticipated the East Asian débâcle of 1997/98 (Krugman, 1994). Although some of the weak-nesses identified in the literature did make the region

economically vulnerable, none of the critical writ-ing seriously addressed one crucial implication ofthe greater role of foreign capital in South East Asia,in particular with regard to international financialliberalization, which became more pronounced in the1990s. As previously noted (Jomo, 1998), dominanceof manufacturing activities – especially the most tech-nologically sophisticated and dynamic ones – by foreigntransnationals subordinated domestic industrial capi-tal in the region, allowing finance capital, bothdomestic and foreign, to become more influential.

In fact, financial capital developed a complexsymbiotic relationship with politically influentialrentiers, now dubbed “cronies” in the aftermath of1997/98. Although threatened by the full implica-tions of international financial liberalization, South-East Asian financial interests were quick to identifyand secure new possibilities of capturing rents fromarbitrage as well as other opportunities offered bygradual international financial integration. In theseand other ways (Gomez and Jomo, 1999; Khan,2000), transnational dominance of South-East Asianindustrialization facilitated the ascendance and con-solidation of financial interests and politically influ-ential rentiers.

This increasingly powerful alliance was prima-rily responsible for promoting financial liberalizationin the region, both externally and internally. How-ever, insofar as the interests of domestic financialcapital did not entirely coincide with internationalfinance capital, the process of international finan-cial liberalization was partial. The processes werealso necessarily uneven, considering the variety ofdifferent interests involved and their varying lobby-ing strengths in different parts of the region.

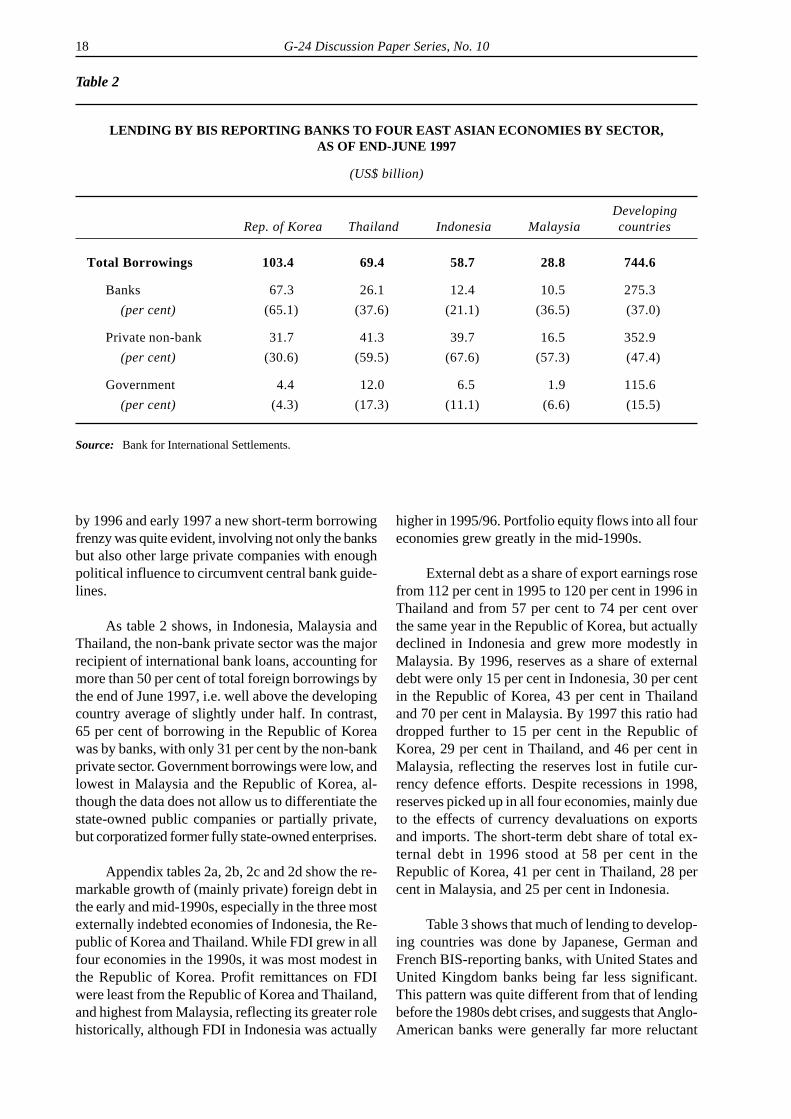

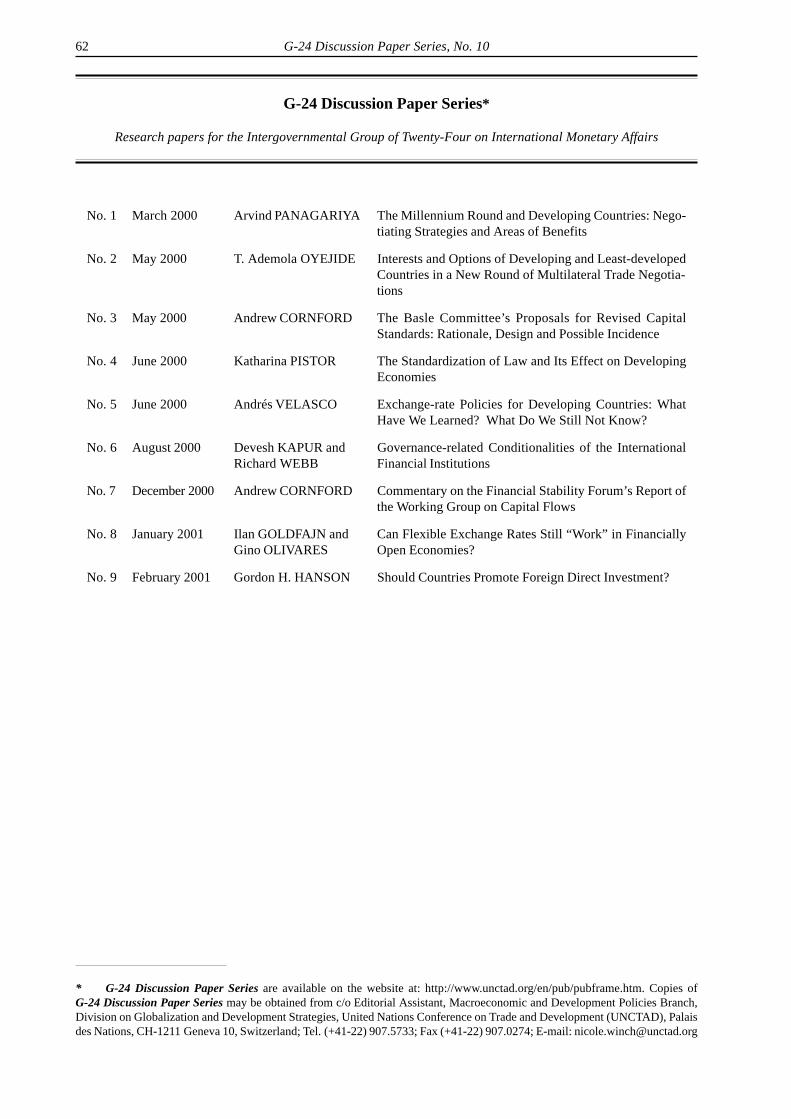

History too was not irrelevant. For example, thebanking crisis in Malaysia in the late 1980s servedto ensure a prudential regulatory framework whichchecked the process from becoming as in Thailand,where caution was thrown to the wind as early ex-ternal liberalization measures succeeded in securingcapital inflows. Yet, in both countries such flows werewanted to finance current account deficits, princi-pally due to service account deficits (mainly forimported financial services as well as investmentincome payments abroad) and growing imports forconsumption, speculative activity in regional stockmarkets, and output of non-tradeables, mainly in theproperty (real estate) sector. There is little evidencethat such capital inflows contributed significantly toaccelerating the pace of economic growth, especiallyof the tradeable sectors of the economy. Instead, it is

12 G-24 Discussion Paper Series, No. 10

likely that they contributed greatly to the asset pricebubbles, whose inevitable deflation was acceleratedby the advent of the crisis, with its devastating eco-nomic, social and political consequences.

A. Crisis and contagion

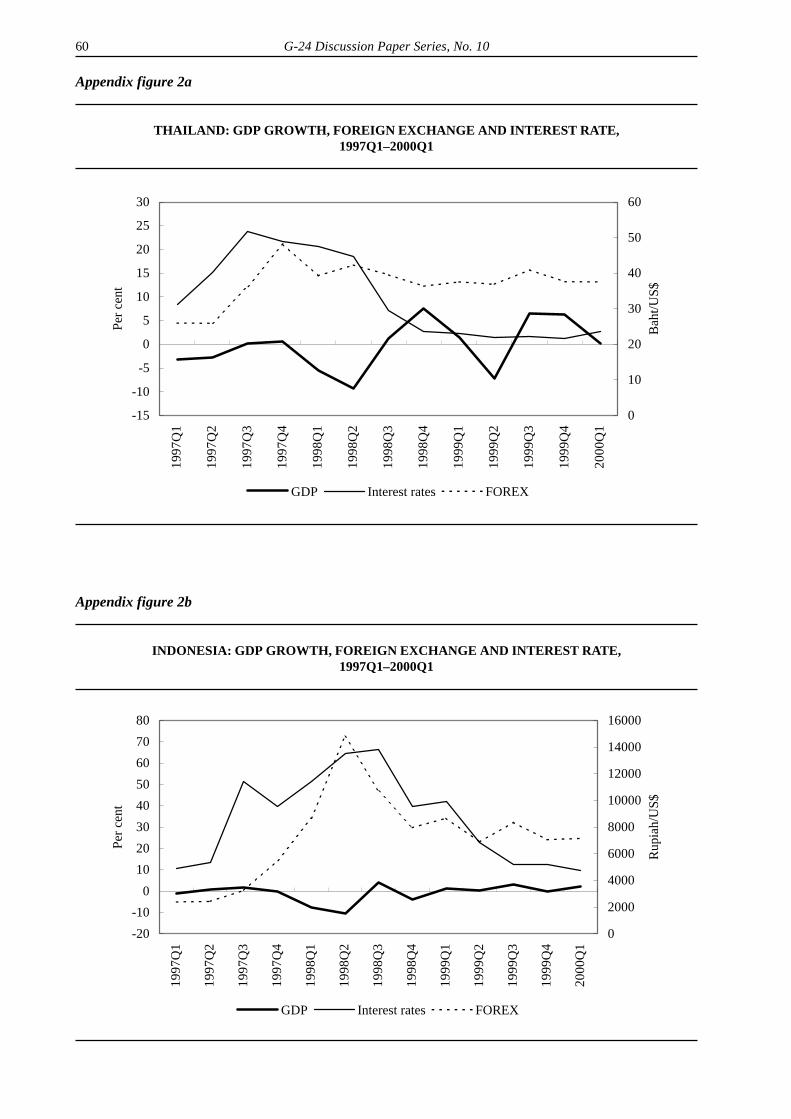

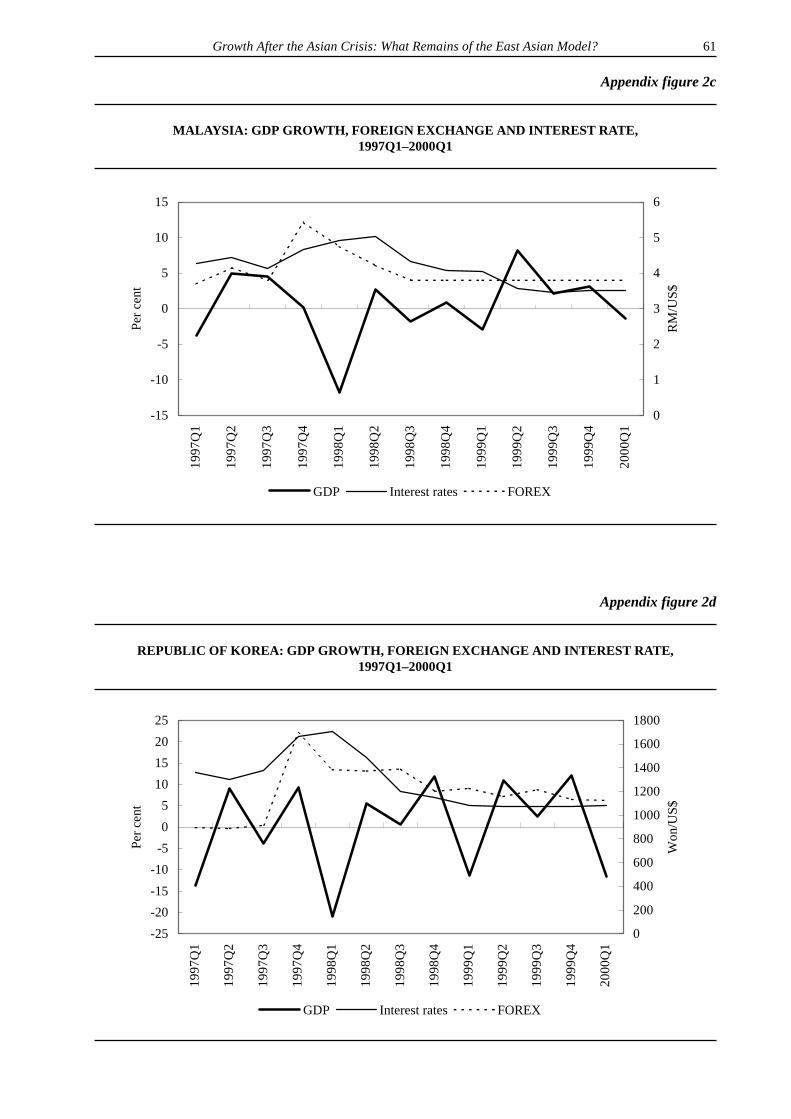

After months of international speculative at-tacks on the Thai baht, the Bank of Thailand let itscurrency float from 2 July 1997, allowing it to dropsuddenly. By mid-July 1997, the currencies of Indo-nesia, Malaysia and the Philippines had also fallenprecipitously after being floated, with their stockmarket price indices following suit. In the followingmonths, currencies and stock markets throughout theregion came under pressure as easily reversible short-term capital inflows took flight in herd-like fashion.In November 1997, despite the Republic of Korea’srather different economic structure, the won too hadcollapsed after withdrawal of official support. Mostother economies in East Asia were also under con-siderable pressure, either directly (e.g. the attack onthe Hong Kong dollar) or indirectly (e.g. due to thedesire to maintain competitive cost advantage againstthe devalued currencies of South-East Asian export-ers).

Contrary to the impression conveyed mainly bythe business media as well as by IMF, there is stillno consensus on how to understand and characterizethe crisis. One manifestation of this has been thedebates between IMF and its various critics over theappropriateness of its negotiated programmes in In-donesia, the Republic of Korea, and Thailand. Whilepolicy debates have understandably captured the mostattention, especially with the public at large, the EastAsian crises have also challenged previously ac-cepted international economic theories.

However, contrary to the popular impressionpromoted by the Western-dominated financial me-dia of “crony capitalism” as the main culprit, mostserious analysts now agree that the crisis began es-sentially as a currency crisis of a new type, differentfrom those previously identified with either fiscalprofligacy or macroeconomic in-discipline. A grow-ing number also seem to agree that the crisis startedoff as a currency crisis and quickly became a moregeneralized financial crisis, before impacting on thereal economy because of reduced liquidity in the fi-nancial system and the consequences of inappropriateofficial policy and ill-informed herd-like market re-sponses.3

B. From miracle to débâcle

Rapid economic growth and structural change,mainly associated with export-led industrializationin the region, can generally be traced back to the mid-1980s. Then, devaluation of the currencies of all threeSouth-East HPAEs as well as selective deregulationof onerous rules helped to create attractive condi-tions for the relocation of production facilities inthese countries and elsewhere in South East Asia andChina. This was especially attractive for Japan andthe first-tier or first-generation NIEs – Hong Kong(China), the Republic of Korea, Singapore and Tai-wan Province of China – most of which experiencedcurrency appreciations, tight labour markets andhigher production costs. This sustained export-ori-ented industrialization well into the 1990s, and wasaccompanied by the growth of other manufacturing,services and construction activities.

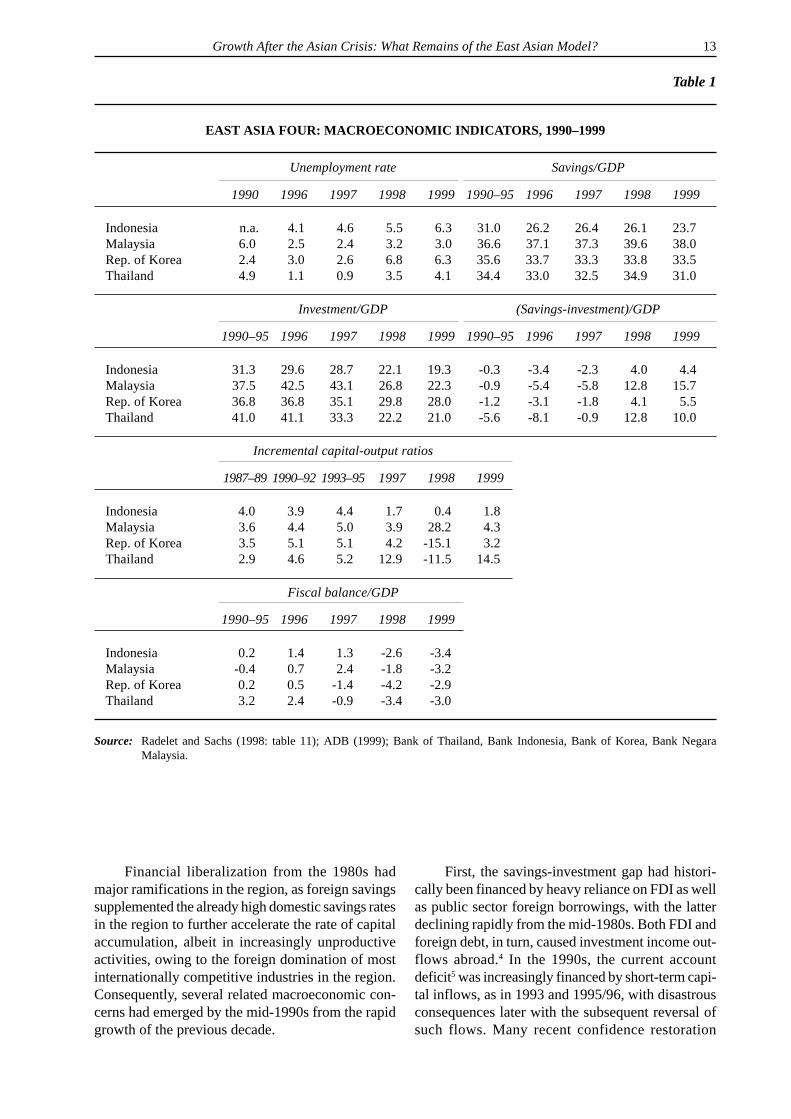

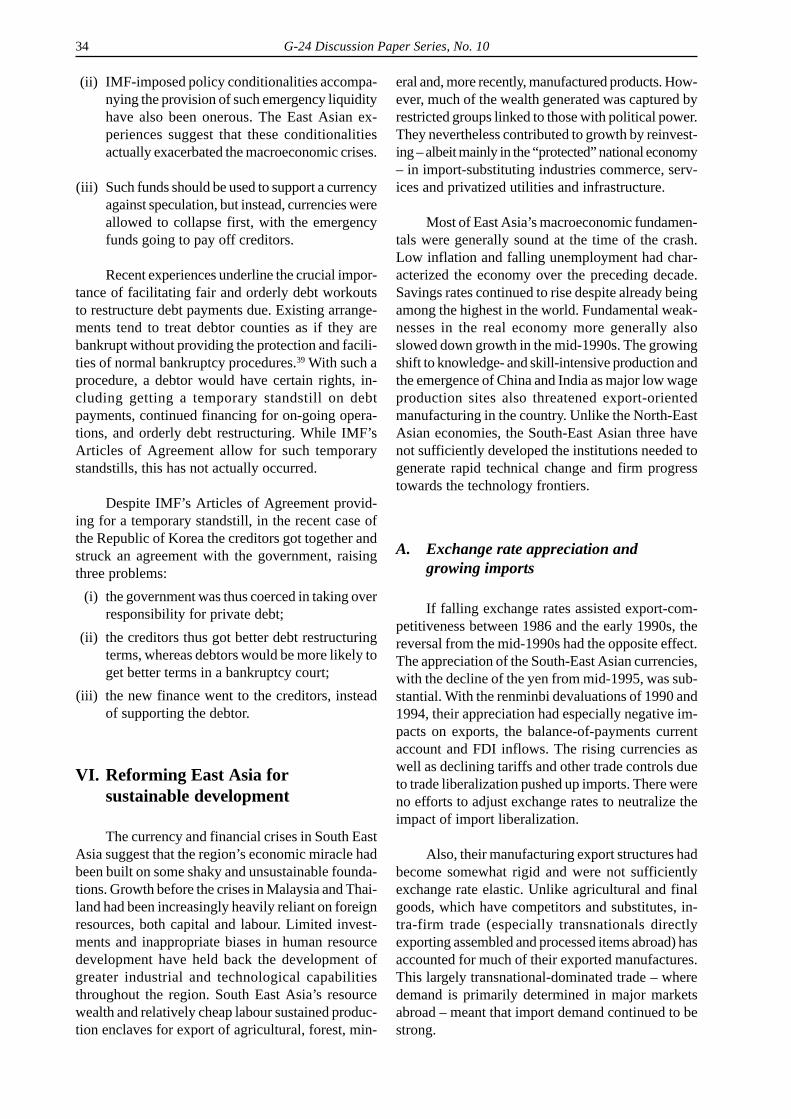

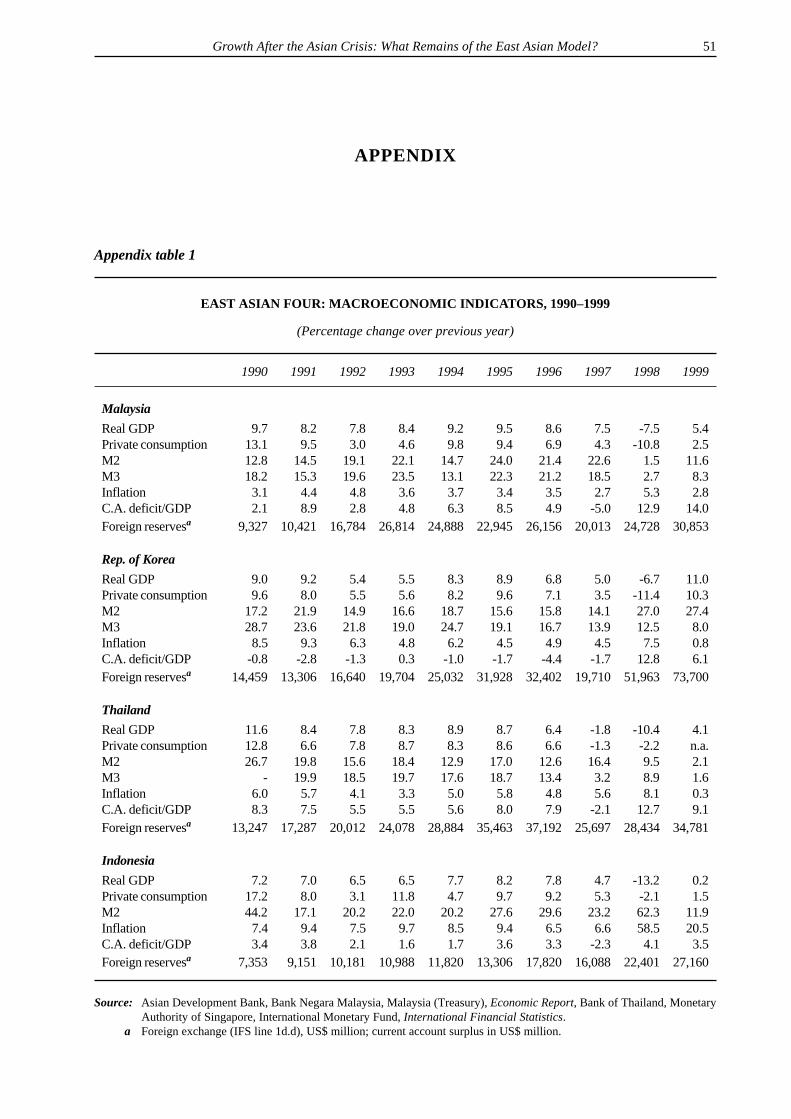

High growth was sustained for about a decade,during much of which fiscal surpluses were main-tained, monetary expansion was not excessive andinflation was generally under control (see Appendixtable 1). Table 1 shows various summary macroeco-nomic indicators for the 1990s, with greater atten-tion to the period from 1996. Prior to 1997, thesavings and investment rates were high and rising inall three South-East Asian economies. Foreign sav-ings supplemented high domestic savings in all foureconomies, especially in Thailand and Malaysia.Unemployment was low, while fiscal balances gen-erally remained positive up to 1997/98.

This is not to suggest, however, that the funda-mentals were all alright in East Asia (Rasiah, 2001).As table 1 shows, the incremental capital-output ratio(ICOR) rose in all three South-East Asian economiesduring the 1990s before 1997, with increase greatestin Thailand and least in Indonesia. The rising ICORsuggests declining returns to new investments be-fore the crisis. Export-led growth had been followedby a construction and property boom, fuelled by fi-nancial systems favouring such “short-termist” in-vestments – involving loans with collateral, whichbankers like – over more productive, but also seem-ingly more risky investments in manufacturing andagriculture. The exaggerated expansion of investmentin such non-tradeables exacerbated their current ac-count deficits. Although widespread in East Asia,for various reasons, the property-finance nexus wasparticularly strong in Thailand, which made it muchmore vulnerable to the inevitable bursting of the bub-ble (Jomo, 1998; Pasuk and Baker, 2000).

13Growth After the Asian Crisis: What Remains of the East Asian Model?

Financial liberalization from the 1980s hadmajor ramifications in the region, as foreign savingssupplemented the already high domestic savings ratesin the region to further accelerate the rate of capitalaccumulation, albeit in increasingly unproductiveactivities, owing to the foreign domination of mostinternationally competitive industries in the region.Consequently, several related macroeconomic con-cerns had emerged by the mid-1990s from the rapidgrowth of the previous decade.

First, the savings-investment gap had histori-cally been financed by heavy reliance on FDI as wellas public sector foreign borrowings, with the latterdeclining rapidly from the mid-1980s. Both FDI andforeign debt, in turn, caused investment income out-flows abroad.4 In the 1990s, the current accountdeficit5 was increasingly financed by short-term capi-tal inflows, as in 1993 and 1995/96, with disastrousconsequences later with the subsequent reversal ofsuch flows. Many recent confidence restoration

Table 1

EAST ASIA FOUR: MACROECONOMIC INDICATORS, 1990–1999

Unemployment rate Savings/GDP

1990 1996 1997 1998 1999 1990–95 1996 1997 1998 1999

Indonesia n.a. 4.1 4.6 5.5 6.3 31.0 26.2 26.4 26.1 23.7Malaysia 6.0 2.5 2.4 3.2 3.0 36.6 37.1 37.3 39.6 38.0Rep. of Korea 2.4 3.0 2.6 6.8 6.3 35.6 33.7 33.3 33.8 33.5Thailand 4.9 1.1 0.9 3.5 4.1 34.4 33.0 32.5 34.9 31.0

Investment/GDP (Savings-investment)/GDP

1990–95 1996 1997 1998 1999 1990–95 1996 1997 1998 1999

Indonesia 31.3 29.6 28.7 22.1 19.3 -0.3 -3.4 -2.3 4.0 4.4Malaysia 37.5 42.5 43.1 26.8 22.3 -0.9 -5.4 -5.8 12.8 15.7Rep. of Korea 36.8 36.8 35.1 29.8 28.0 -1.2 -3.1 -1.8 4.1 5.5Thailand 41.0 41.1 33.3 22.2 21.0 -5.6 -8.1 -0.9 12.8 10.0

Incremental capital-output ratios

1987–89 1990–92 1993–95 1997 1998 1999

Indonesia 4.0 3.9 4.4 1.7 0.4 1.8Malaysia 3.6 4.4 5.0 3.9 28.2 4.3Rep. of Korea 3.5 5.1 5.1 4.2 -15.1 3.2Thailand 2.9 4.6 5.2 12.9 -11.5 14.5

Fiscal balance/GDP

1990–95 1996 1997 1998 1999

Indonesia 0.2 1.4 1.3 -2.6 -3.4Malaysia -0.4 0.7 2.4 -1.8 -3.2Rep. of Korea 0.2 0.5 -1.4 -4.2 -2.9Thailand 3.2 2.4 -0.9 -3.4 -3.0

Source: Radelet and Sachs (1998: table 11); ADB (1999); Bank of Thailand, Bank Indonesia, Bank of Korea, Bank NegaraMalaysia.

14 G-24 Discussion Paper Series, No. 10

measures seek to induce such short-term inflows onceagain, but they cannot be relied upon to address theunderlying problem in the medium to long term. Al-though always in the minority, foreign portfolioinvestments increasingly influenced the stock mar-kets in the region in the 1990s. With incompleteinformation exacerbated by limited transparency,their regional presence, the biased nature of fundmanagers’ incentives and remuneration and theshort-termism of their investment horizons, foreignfinancial institutions were much more prone to herdbehaviour, and thus contributed most decisively toregional contagion.

Second, there was an explosion of private sec-tor debt in the 1990s, especially from abroad, notleast because of the efforts of “debt-pushers” keento secure higher returns from the fast-growing re-gion.6 Commercial banks’ foreign liabilities alsoincreased quickly as the ratio of loans to GNP roserapidly during the period.

Overinvestment of investible funds, especiallyfrom abroad, in non-tradeables only made thingsworse, especially on the current account. Only a smallproportion of commercial banks and other lendingagencies went to manufacturing and other productiveactivities. This share is likely to have been even smallerwith foreign borrowings, most of which was collater-alized with assets such as real property and stock.7

Thus, much of the inflow of foreign savingsactually contributed to asset price inflation, mainlyinvolving real estate and share prices. Insofar as suchinvestments did not increase the production of trade-ables, they actually exacerbated the current accountdeficit, rather than alleviated it – as they were thoughtto be doing. This, in turn, worsened the problem of“currency mismatch”, with borrowings in US dol-lars invested in activities not generating foreignexchange.

As a high proportion of these foreign borrow-ings were short-term in nature and deployed tofinance medium- to long-term projects, a “term mis-match” problem also arose. According to the Bankfor International Settlements (BIS) (Asian Wall StreetJournal, 6 January 1998), well over half of the foreignborrowings by commercial banks were short-term innature: in Malaysia 56 per cent, in Thailand 66 percent, in Indonesia 59 per cent, and in the Republic ofKorea 68 per cent.

More generally, the foreign exchange risks ofinvestments generally increased, raising the vulner-

ability of these economies to the maintenance of cur-rency pegs to the US dollar.8 The pegs encouraged agreat deal of un-hedged borrowing by an influentialconstituency with a strong stake in defending the pegsregardless of their adverse consequences for theeconomy. Owing to foreign domination of export-oriented industries in South East Asia, unlike in NorthEast Asia, there was no strong domestic export-ori-ented industrial community to lobby for floating ordepreciation of the South-East Asian currencies de-spite the obvious adverse consequences of the pegsfor international cost competitiveness. Instead, afterpegging their currencies to the US dollar, from theearly 1990s and especially from the mid-1990s, mostSouth-East Asian central banks resisted downwardadjustments to their exchange rates, which wouldhave reduced, if not averted some of the more dis-ruptive consequences of the 1997/98 currency col-lapses.9 Yet, it is also now generally agreed that the1997/98 East Asian crises saw tremendous “over-shooting” in exchange rate adjustments well in ex-cess of expected “corrections”.

It is generally agreed that the affected South-East Asian economies were characterized by thefollowing key fundamentals:

(i) viability of domestic financial systems;10

(ii) domestic output and export responsiveness tonominal devaluations;11

(iii) sustainability of current account deficits;12

(iv) high savings rates and robust public finances.

C. Consequences of financial liberalization

In Kaminsky and Reinhart’s (1996) study of71 balance-of-payments (BoP) crises and 25 bank-ing crises during the period 1970–1995, there wereonly three banking crises associated with the 25 BoPcrises during 1970–1979. However, there were 22banking crises which coincided with 46 BoP crisesover 1980–1995, which the authors attribute to the1980s financial liberalization, with a private lendingboom culminating in a banking crisis, and then acurrency one. Montes (1998) attributes the South-East Asian currency crisis to the “twin liberali-zations” of domestic financial systems and openingof the capital account. Financial liberalization in-duced new behaviour in financial systems, notably:

(i) domestic financial institutions had greater flex-ibility in offering interest rates to secure fundsdomestically and in bidding for foreign funds;

15Growth After the Asian Crisis: What Remains of the East Asian Model?

(ii) they became less reliant on lending to the gov-ernment;

(iii) regulations, such as credit allocation rules andceilings, were reduced;

(iv) greater domestic competition meant that ascend-ance depended on expanding lending portfolios,often at the expense of prudence.

Looking at 57 countries during the 1970–1996period, Carleton et al. (2000) find that inflationarymacroeconomic policies and small foreign reservesstocks reliably predicted currency collapses. Theyargue that since the probability of Indonesia, Malay-sia, the Republic of Korea and Thailand experiencinga currency collapse in 1997 was about 20 per cent,and all four currencies (and economies) collapsed –rather than just one, as expected – financial conta-gion is a better explanation than weak domesticfundamentals.