Embed Size (px)

Citation preview

���� ����� ��������� ����

GUIDE ���� �������

����� ��������� ��������� ��� ��������� ��. 205

NAIC Guide to Compliance

with State Audit Requirements

2010

Accounting & Reporting

Accountants, members of the insurance industry and

educators will find relevant information about statutory

accounting practices and procedures.

Consumer Information

Consumers, educators and members of the insurance

industry will find important answers to common questions

in guides about auto, home, health and life insurance.

Financial Regulation

Accountants, financial analysts and lawyers will find

handbooks, compliance guides and reports on financial

analysis, state audit requirements and receiverships.

Legal

State laws, regulations and guidelines apply to members

of the legal and insurance industries.

NAIC Activities

Insurance industry members will find directories,

newsletters and reports affecting NAIC members.

Special Studies

Accountants, educators, financial analysts, members of

the insurance industry, lawyers and statisticians will find

relevant products on a variety of special topics.

Statistical Reports

Insurance industry data directed at regulators, educators,

financial analysts, insurance industry members, lawyers

and statisticians.

Supplementary Products

Accountants, educators, financial analysts, insurers,

lawyers and statisticians will find guidelines, handbooks,

surveys and NAIC positions on a wide variety of issues.

Securities Valuation Office

Provides insurers with portfolio values and procedures

for complying with NAIC reporting requirements.

White Papers

Accountants, members of the insurance industry and

educators will find relevant information on a variety of

insurance topics.

© 2010 National Association of Insurance Commissioners. All rights reserved.

ISBN: 978-1-59917-352-8

Printed in the United States of America

No part of this book may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic or

mechanical, including photocopying, recording, or any storage or retrieval system, without written permission from the NAIC.

The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of

regulators, insurers and researchers by providing detailed and comprehensive insurance information. The NAIC

offers a wide range of publications in the following categories:

For more information about NAIC publications, view our online catalog at:

http://store.naic.org

NAIC Central Office

2301 McGee Street, Suite 800

Kansas City, MO 64108-2662

816.842.3600

NAIC Securities Valuation Office

48 Wall Street, 6th Floor

New York, NY 10005-2906

212.398.9000

NAIC Executive Office

444 North Capitol Street NW, Suite 701

Washington, DC 20001

202.471.3990

The following companion product provides additional information on the same or similar subject matter. Many

customers who purchase the NAIC’s Guide to Compliance with State Audit Requirements also purchase the

following product:

Companion Products

Annual Financial Reporting Model Regulation (Model Audit Rule)

Improves the surveillance of the financial condition of insurers by requiring

1) annual audit of financial statements; 2) communication of internal control-

related matters noted in an audit; and 3) management's report of internal

control over financial reporting. Commonly referred to as the Model Audit Rule.

Includes updates through April 2010 (Update #91).

International orders must be prepaid, including shipping charges. Please contact an NAIC Customer Service Representative, Monday - Friday, 8:30 am - 5 pm CT.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

The NAIC has prepared this publication to assist insurers, certified public accountants, and other interested parties in complying with various state filing requirements for annual audited financial reports. These filing requirements generally provide for, among other things, specific information concerning the filing and content of audited financial reports and other related letters and reports with the state insurance department. All of the guidelines in this area have recently been significantly changed and this publication has been created to summarize these new requirements. On June 11, 2006, the NAIC membership voted to approve amendments to the Annual Financial Reporting Model Regulation (#205), commonly known as the Model Audit Rule. The purpose of this regulation is to improve a state’s surveillance of the financial condition of insurers by requiring an independent annual audit of the financial statements by Certified Public Accountants. Significant elements of this regulation are required as an accreditation standard and have been since the creation of the standards. The amendments adopted in 2006 were the result of nearly three years of continued research and discussion by financial regulators, members of industry, public accountants and representatives from trade associations. The revisions deal with primarily three areas: auditor independence, corporate governance and internal control over financial reporting. The critical new requirements associated with these revisions became effective beginning January 1, 2010 and have now been adopted by virtually all member states. Citations providing reference to each state’s statute or regulation containing the relevant provisions have been provided within the publication. The publication summarizes requirements placed on insurers and their external auditors by the Model Audit Rule and compares and contrasts the requirements included within the NAIC Model to those ultimately adopted by each NAIC member state. The summaries contained herein are not intended to be all-inclusive and should not be relied on solely in determining state-specific requirements. Where a question exists with respect to any requirement, the state’s statute or regulation should be reviewed and, where necessary, the state insurance department should be contacted. Every effort has been made to ensure the contents of this publication are complete and factually correct, but the NAIC makes no warranty as to the completeness or correctness of the information provided. All responsibility for compliance with individual state insurance codes rests solely with the insurance company and its independent auditor.

© 2010 National Association of Insurance Commissioners

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

TABLE OF CONTENTS

Alabama .............................................................................................................................. 1 Alaska ................................................................................................................................. 5 Arizona................................................................................................................................ 9 Arkansas.............................................................................................................................13 California ...........................................................................................................................17 Colorado.............................................................................................................................21 Connecticut ........................................................................................................................25 Delaware ............................................................................................................................29 District of Columbia ..........................................................................................................33 Florida ................................................................................................................................37 Georgia...............................................................................................................................41 Hawaii ................................................................................................................................45 Idaho ..................................................................................................................................49 Illinois ................................................................................................................................53 Indiana................................................................................................................................57 Iowa....................................................................................................................................61 Kansas ................................................................................................................................65 Kentucky............................................................................................................................69 Louisiana............................................................................................................................73 Maine .................................................................................................................................77 Maryland............................................................................................................................81 Massachusetts ....................................................................................................................85 Michigan ............................................................................................................................89 Minnesota...........................................................................................................................93 Mississippi .........................................................................................................................97 Missouri ...........................................................................................................................101 Montana ...........................................................................................................................105 Nebraska ..........................................................................................................................109 Nevada .............................................................................................................................113 New Hampshire ...............................................................................................................117 New Jersey .......................................................................................................................121 New Mexico.....................................................................................................................125

© 2010 National Association of Insurance Commissioners i

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

ii © 2010 National Association of Insurance Commissioners

TABLE OF CONTENTS

New York.........................................................................................................................129 North Carolina .................................................................................................................133 North Dakota....................................................................................................................137 Ohio..................................................................................................................................141 Oklahoma.........................................................................................................................145 Oregon..............................................................................................................................149 Pennsylvania ....................................................................................................................153 Puerto Rico.......................................................................................................................157 Rhode Island ....................................................................................................................161 South Carolina .................................................................................................................165 South Dakota....................................................................................................................169 Tennessee.........................................................................................................................173 Texas ................................................................................................................................177 Utah..................................................................................................................................181 Vermont ...........................................................................................................................185 Virginia ............................................................................................................................189 Washington ......................................................................................................................193 West Virginia ...................................................................................................................197 Wisconsin.........................................................................................................................201 Wyoming..........................................................................................................................205

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 1

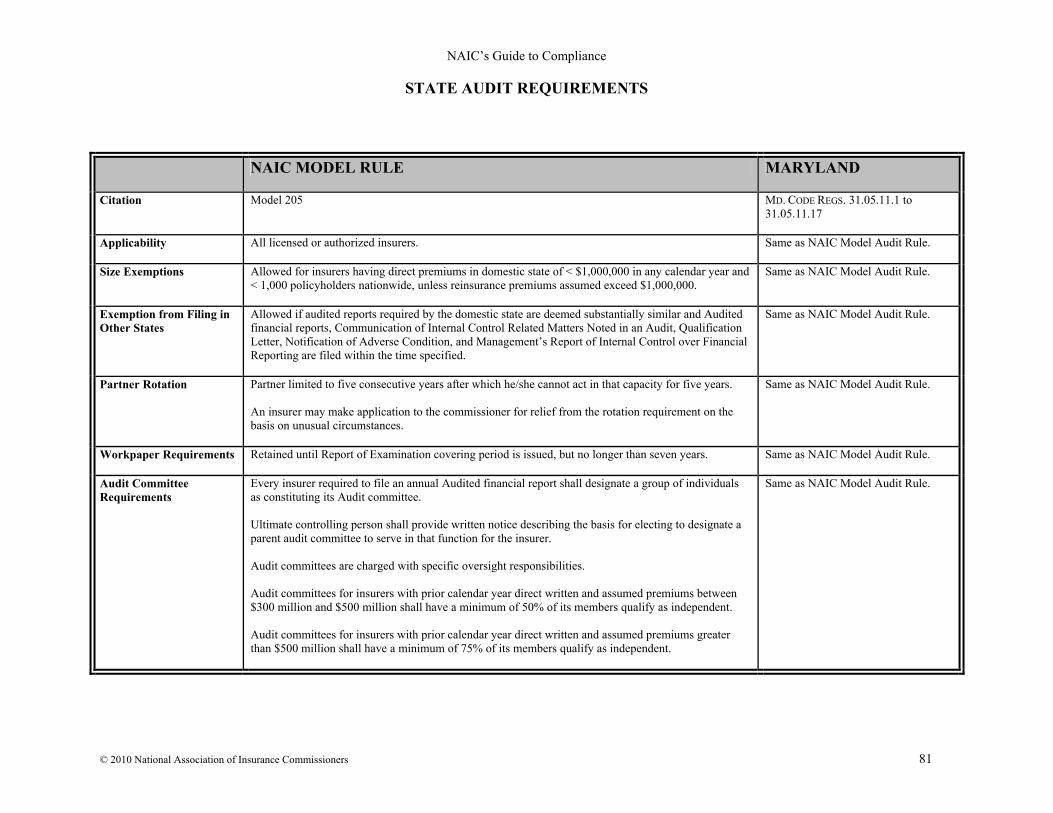

NAIC MODEL RULE ALABAMA

Citation Model 205 ALA. ADMIN. CODE R. 482-1-141.01 to 482-1-141.20

Applicability All licensed or authorized insurers.

All licensed insurers.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years.

Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 2

NAIC MODEL RULE

ALABAMA

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

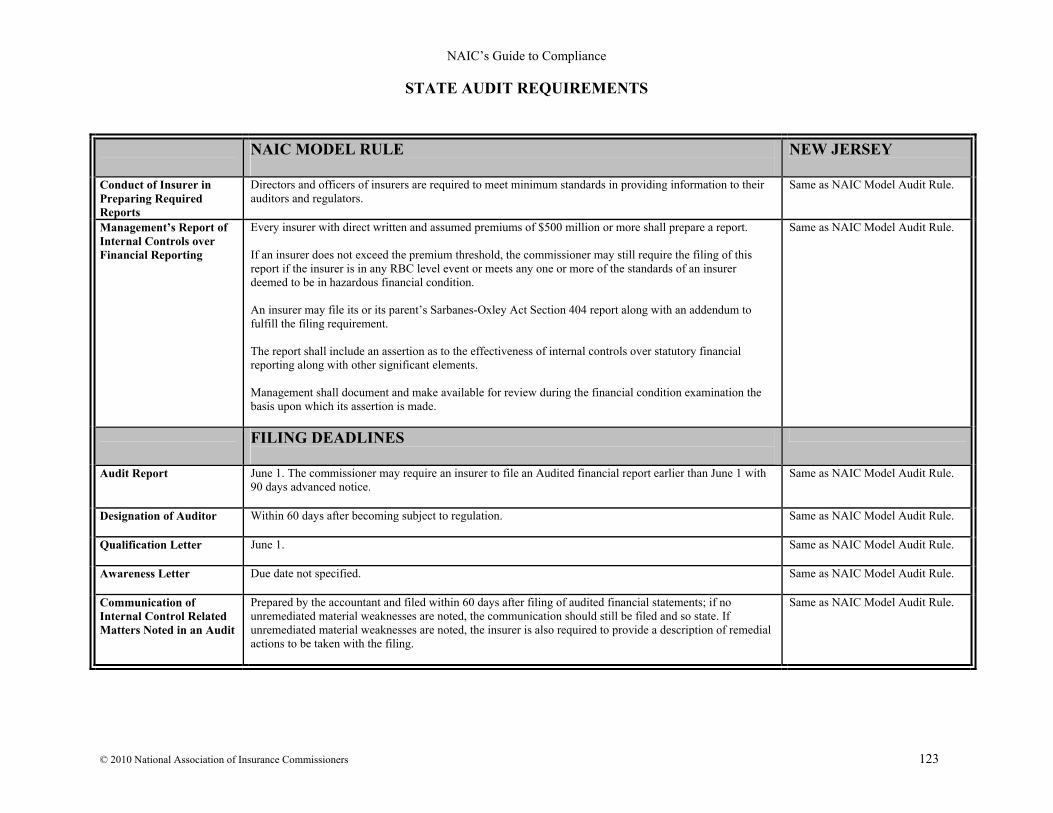

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

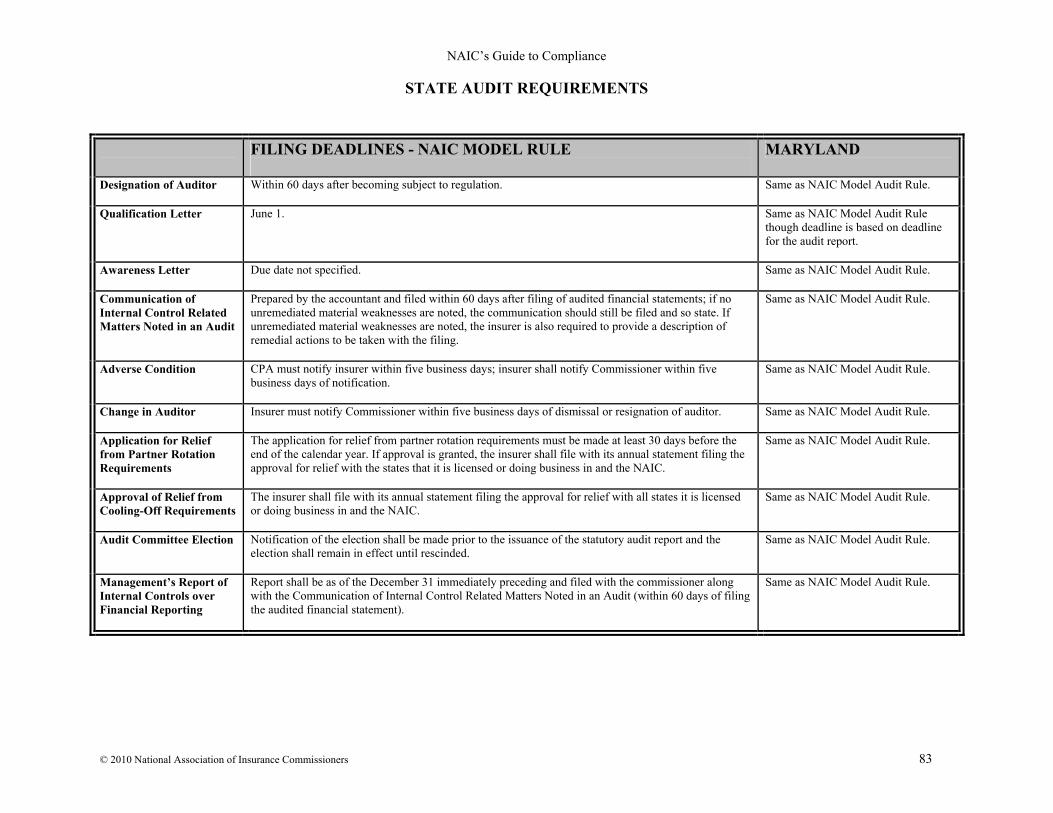

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation.

Same as NAIC Model Audit Rule.

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 3

FILING DEADLINES - NAIC MODEL RULE

ALABAMA

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 4

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

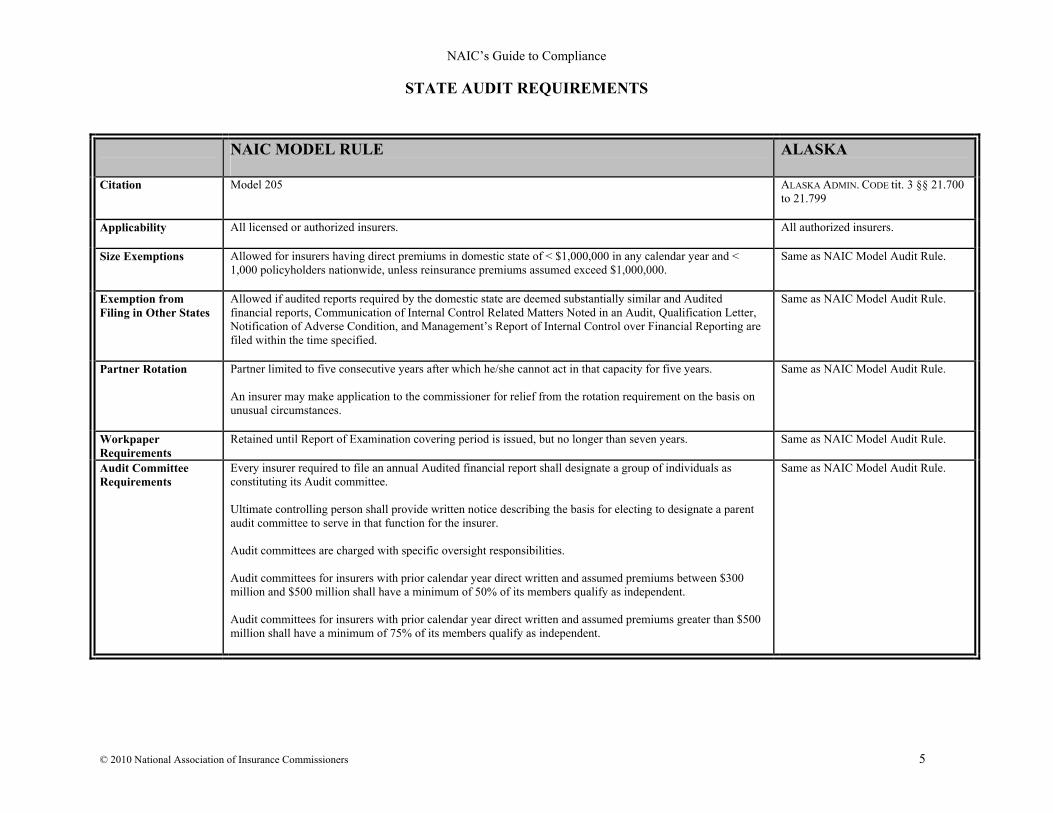

© 2010 National Association of Insurance Commissioners 5

NAIC MODEL RULE

ALASKA

Citation Model 205

ALASKA ADMIN. CODE tit. 3 §§ 21.700 to 21.799

Applicability All licensed or authorized insurers.

All authorized insurers.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements

Retained until Report of Examination covering period is issued, but no longer than seven years. Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 6

NAIC MODEL RULE

ALASKA

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

AS 21.09.200(i) refers to the management report in internal control over financial reporting. This section is effective 12/31/2010. Regulations are currently in the process of adoption. Per NAIC Model Audit Rule Sec. 17 G, this reporting starts with the reporting period ending 12/31/2010.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor

Within 60 days after becoming subject to regulation. Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 7

FILING DEADLINES - NAIC MODEL RULE

ALASKA

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election

Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Effective 12/31/2010.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 8

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 9

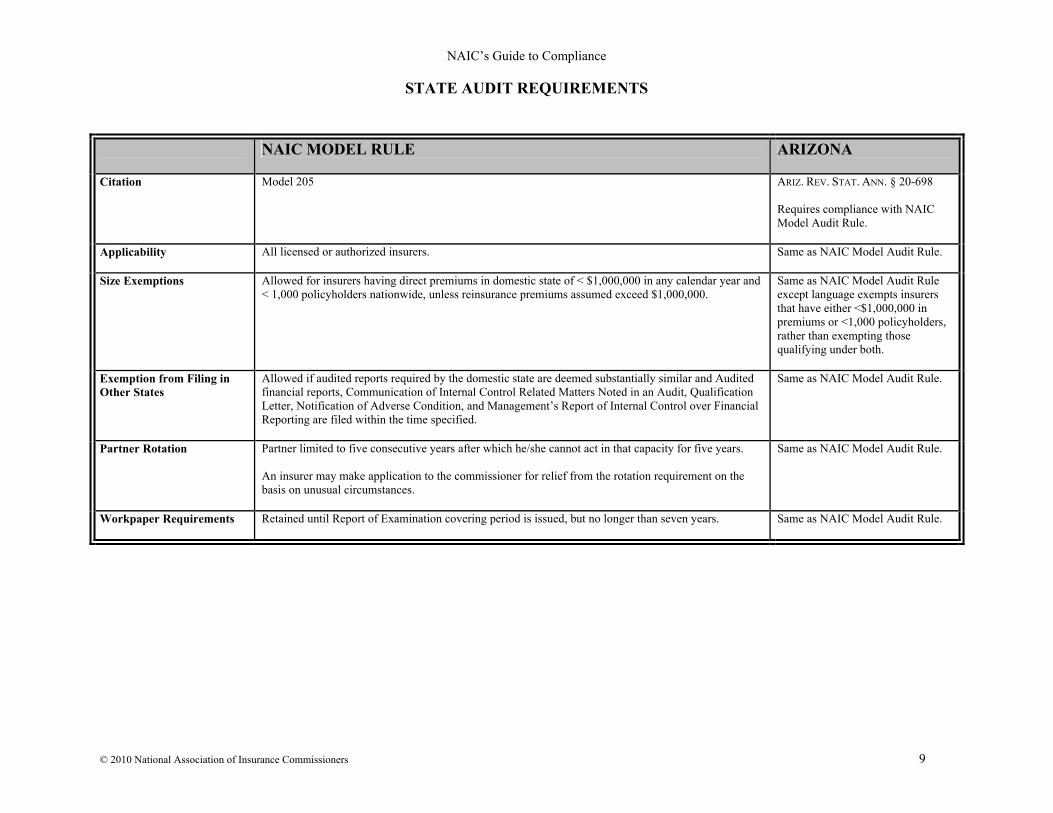

NAIC MODEL RULE ARIZONA

Citation Model 205 ARIZ. REV. STAT. ANN. § 20-698 Requires compliance with NAIC Model Audit Rule.

Applicability All licensed or authorized insurers. Same as NAIC Model Audit Rule.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule except language exempts insurers that have either <$1,000,000 in premiums or <1,000 policyholders, rather than exempting those qualifying under both.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years. Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 10

NAIC MODEL RULE

ARIZONA

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 11

NAIC MODEL RULE

ARIZONA

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation. Same as NAIC Model Audit Rule.

Qualification Letter June 1. Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified. Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor. Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 12

FILING DEADLINES - NAIC MODEL RULE

ARIZONA

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 13

NAIC MODEL RULE ARKANSAS

Citation Model 205 25 ARK. CODE INS. R. §§ 1-19

Applicability All licensed or authorized insurers. Same as NAIC Model Audit Rule.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years. Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 14

NAIC MODEL RULE

ARKANSAS

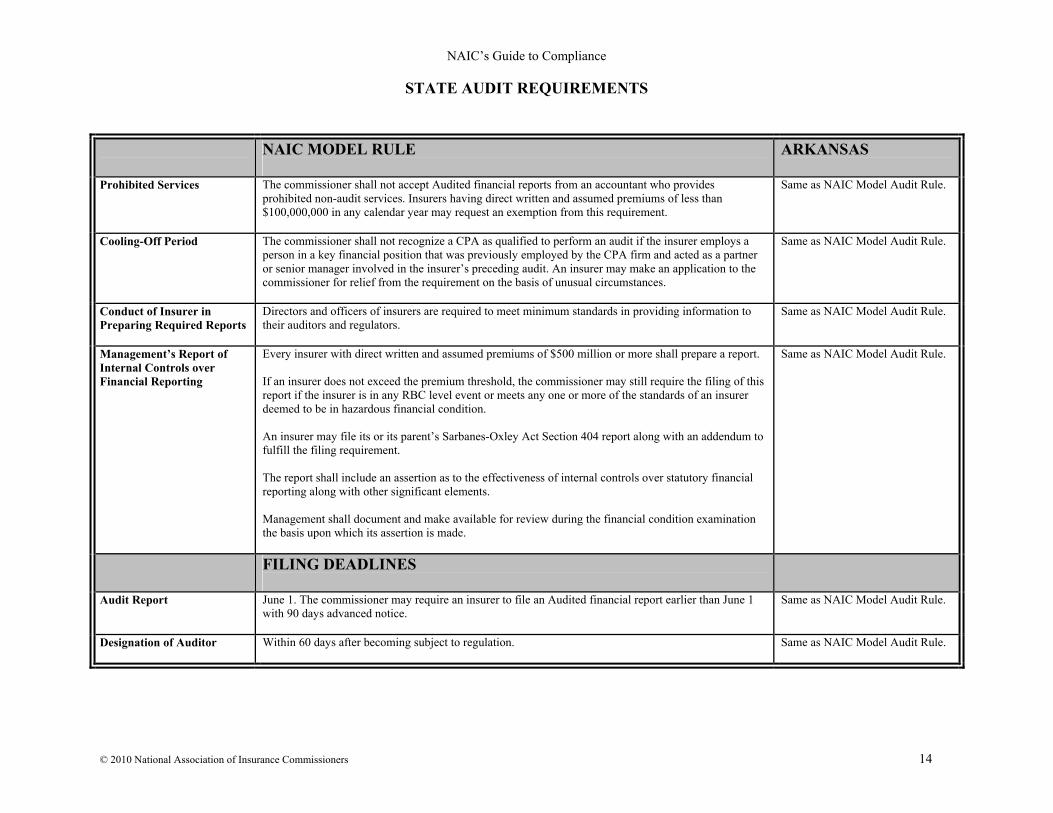

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation. Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 15

FILING DEADLINES - NAIC MODEL RULE

ARKANSAS

Qualification Letter June 1. Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified. Same as NAIC Model Audit Rule except that it states the awareness letter must be filed simultaneously with the designation of auditor.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor. Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 16

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 17

NAIC MODEL RULE CALIFORNIA

Citation Model 205

CAL. CODE. REGS. tit. 10, §§ 2309.2 to 2309.20

Applicability All licensed or authorized insurers. All insurers doing business in California subject to ICS 900.2 requirements.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Allowed for insurers having direct premiums of < $1,000,000 and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Not addressed.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 18

NAIC MODEL RULE

CALIFORNIA

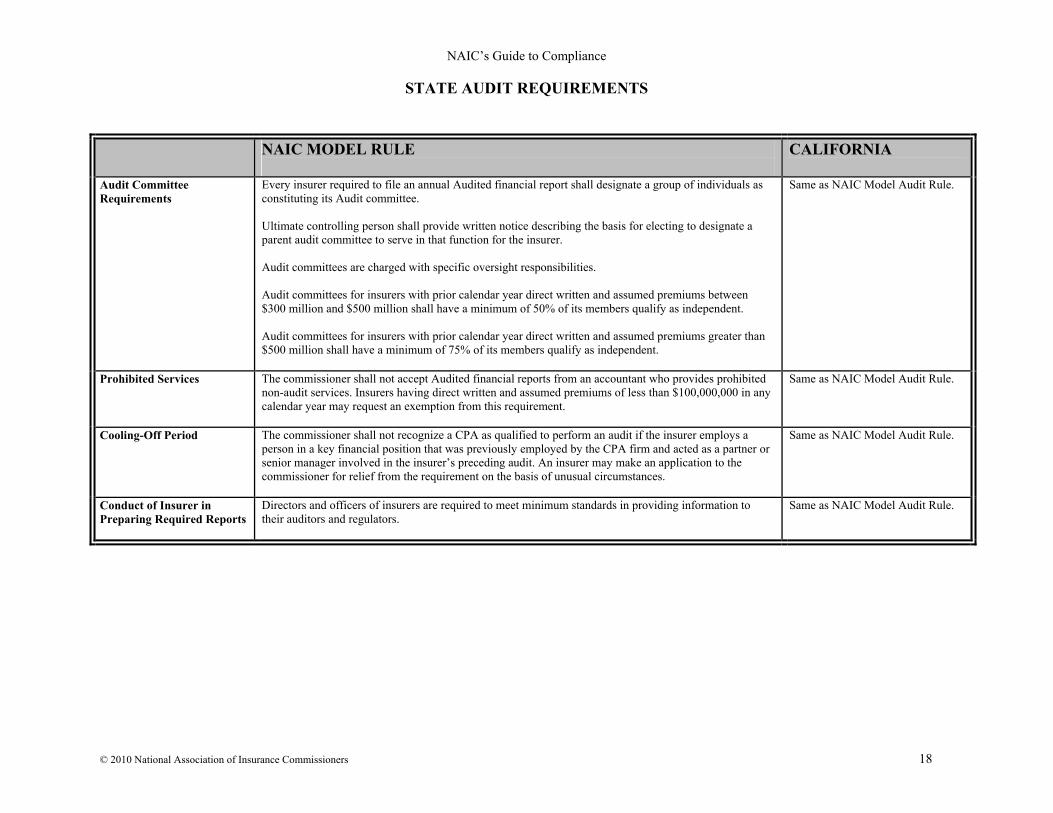

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 19

NAIC MODEL RULE

CALIFORNIA

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation.

Same as NAIC Model Audit Rule.

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 20

FILING DEADLINES - NAIC MODEL RULE

CALIFORNIA

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 21

NAIC MODEL RULE COLORADO

Citation Model 205 3 COLO. CODE REGS. 3-1-4

Applicability All licensed or authorized insurers. Same as NAIC Model Audit Rule.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years. Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 22

NAIC MODEL RULE

COLORADO

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation. Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 23

FILING DEADLINES - NAIC MODEL RULE

COLORADO

Qualification Letter June 1. Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified. Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor. Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 24

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 25

NAIC MODEL RULE CONNECTICUT

Citation Model 205

CONN. AGENCIES REGS. §§ 38a-54-1 to 38a-54-14

Applicability All licensed or authorized insurers.

All licensed insurers.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years.

Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 26

NAIC MODEL RULE

CONNECTICUT

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 27

FILING DEADLINES - NAIC MODEL RULE

CONNECTICUT

Designation of Auditor Within 60 days after becoming subject to regulation.

Same as NAIC Model Audit Rule.

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 28

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 29

NAIC MODEL RULE DELAWARE

Citation Model 205

301 DEL. CODE REGS. §§ 1.0 to 19.0

Applicability All licensed or authorized insurers.

All licensed insurers.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years.

Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 30

NAIC MODEL RULE

DELAWARE

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Same as NAIC Model Audit Rule.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Same as NAIC Model Audit Rule.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Same as NAIC Model Audit Rule.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 31

FILING DEADLINES - NAIC MODEL RULE

DELAWARE

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Same as NAIC Model Audit Rule.

Audit Committee Election Notification of the election shall be made prior to the issuance of the statutory audit report and the election shall remain in effect until rescinded.

Same as NAIC Model Audit Rule.

Management’s Report of Internal Controls over Financial Reporting

Report shall be as of the December 31 immediately preceding and filed with the commissioner along with the Communication of Internal Control Related Matters Noted in an Audit (within 60 days of filing the audited financial statement).

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 32

This page is intentionally left blank

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 33

NAIC MODEL RULE DISTRICT OF COLUMBIA

Citation Model 205

D.C. CODE §§ 31-301 to 31-314

Applicability All licensed or authorized insurers.

All licensed or authorized insurers.

Size Exemptions Allowed for insurers having direct premiums in domestic state of < $1,000,000 in any calendar year and < 1,000 policyholders nationwide, unless reinsurance premiums assumed exceed $1,000,000.

Same as NAIC Model Audit Rule.

Exemption from Filing in Other States

Allowed if audited reports required by the domestic state are deemed substantially similar and Audited financial reports, Communication of Internal Control Related Matters Noted in an Audit, Qualification Letter, Notification of Adverse Condition, and Management’s Report of Internal Control over Financial Reporting are filed within the time specified.

Same as NAIC Model Audit Rule.

Partner Rotation Partner limited to five consecutive years after which he/she cannot act in that capacity for five years. An insurer may make application to the commissioner for relief from the rotation requirement on the basis on unusual circumstances.

Same as NAIC Model Audit Rule. Legislation introduced in the D.C. council includes this provision.

Workpaper Requirements Retained until Report of Examination covering period is issued, but no longer than seven years.

Same as NAIC Model Audit Rule.

Audit Committee Requirements

Every insurer required to file an annual Audited financial report shall designate a group of individuals as constituting its Audit committee. Ultimate controlling person shall provide written notice describing the basis for electing to designate a parent audit committee to serve in that function for the insurer. Audit committees are charged with specific oversight responsibilities. Audit committees for insurers with prior calendar year direct written and assumed premiums between $300 million and $500 million shall have a minimum of 50% of its members qualify as independent. Audit committees for insurers with prior calendar year direct written and assumed premiums greater than $500 million shall have a minimum of 75% of its members qualify as independent.

Legislation introduced in the D.C. council includes these provisions.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 34

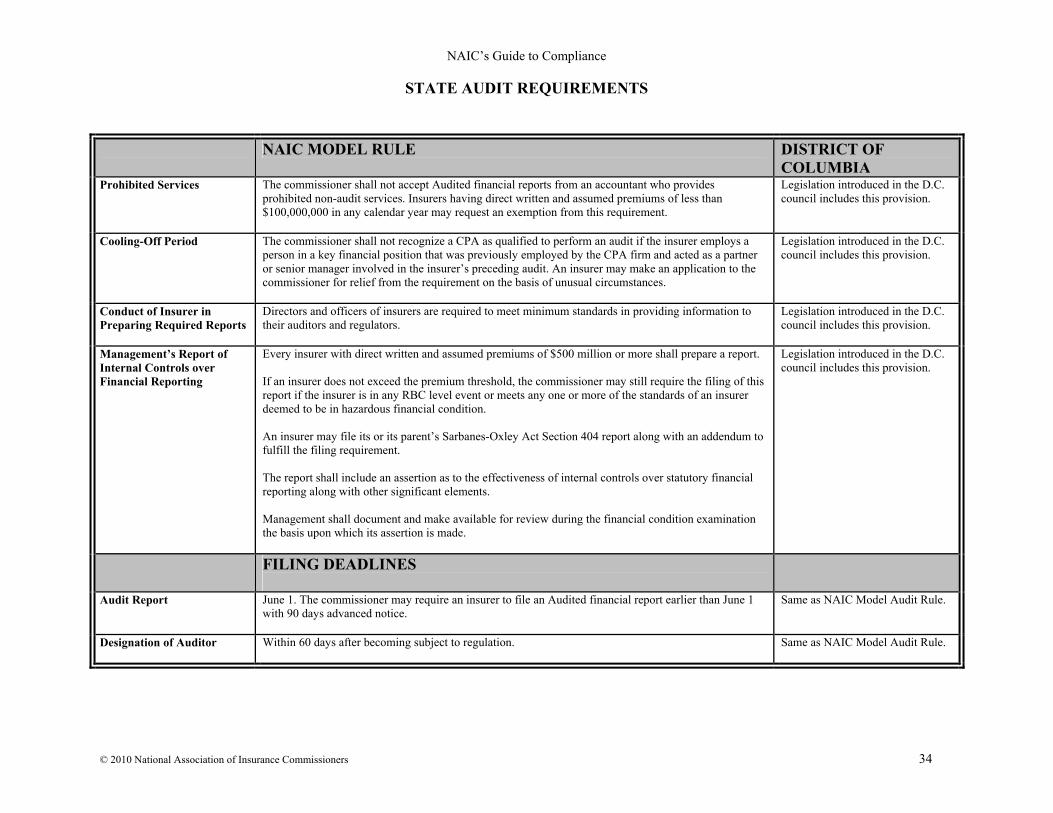

NAIC MODEL RULE DISTRICT OF COLUMBIA

Prohibited Services The commissioner shall not accept Audited financial reports from an accountant who provides prohibited non-audit services. Insurers having direct written and assumed premiums of less than $100,000,000 in any calendar year may request an exemption from this requirement.

Legislation introduced in the D.C. council includes this provision.

Cooling-Off Period The commissioner shall not recognize a CPA as qualified to perform an audit if the insurer employs a person in a key financial position that was previously employed by the CPA firm and acted as a partner or senior manager involved in the insurer’s preceding audit. An insurer may make an application to the commissioner for relief from the requirement on the basis of unusual circumstances.

Legislation introduced in the D.C. council includes this provision.

Conduct of Insurer in Preparing Required Reports

Directors and officers of insurers are required to meet minimum standards in providing information to their auditors and regulators.

Legislation introduced in the D.C. council includes this provision.

Management’s Report of Internal Controls over Financial Reporting

Every insurer with direct written and assumed premiums of $500 million or more shall prepare a report. If an insurer does not exceed the premium threshold, the commissioner may still require the filing of this report if the insurer is in any RBC level event or meets any one or more of the standards of an insurer deemed to be in hazardous financial condition. An insurer may file its or its parent’s Sarbanes-Oxley Act Section 404 report along with an addendum to fulfill the filing requirement. The report shall include an assertion as to the effectiveness of internal controls over statutory financial reporting along with other significant elements. Management shall document and make available for review during the financial condition examination the basis upon which its assertion is made.

Legislation introduced in the D.C. council includes this provision.

FILING DEADLINES

Audit Report June 1. The commissioner may require an insurer to file an Audited financial report earlier than June 1 with 90 days advanced notice.

Same as NAIC Model Audit Rule.

Designation of Auditor Within 60 days after becoming subject to regulation.

Same as NAIC Model Audit Rule.

NAIC’s Guide to Compliance

STATE AUDIT REQUIREMENTS

© 2010 National Association of Insurance Commissioners 35

FILING DEADLINES - NAIC MODEL RULE DISTRICT OF COLUMBIA

Qualification Letter June 1.

Same as NAIC Model Audit Rule.

Awareness Letter Due date not specified.

Same as NAIC Model Audit Rule.

Communication of Internal Control Related Matters Noted in an Audit

Prepared by the accountant and filed within 60 days after filing of audited financial statements; if no unremediated material weaknesses are noted, the communication should still be filed and so state. If unremediated material weaknesses are noted, the insurer is also required to provide a description of remedial actions to be taken with the filing.

Same as NAIC Model Audit Rule.

Adverse Condition CPA must notify insurer within five business days; insurer shall notify Commissioner within five business days of notification.

Same as NAIC Model Audit Rule.

Change in Auditor Insurer must notify Commissioner within five business days of dismissal or resignation of auditor.

Same as NAIC Model Audit Rule.

Application for Relief from Partner Rotation Requirements

The application for relief from partner rotation requirements must be made at least 30 days before the end of the calendar year. If approval is granted, the insurer shall file with its annual statement filing the approval for relief with the states that it is licensed or doing business in and the NAIC.

Legislation introduced in the D.C. council includes this provision.

Approval of Relief from Cooling-Off Requirements

The insurer shall file with its annual statement filing the approval for relief with all states it is licensed or doing business in and the NAIC.

Legislation introduced in the D.C. council includes this provision.