Embed Size (px)

Citation preview

Headline Verdana BoldEuropean Motor Insurance StudyThe rise of digitally-enabled motor insurance22 November 2016

Welcome & introduction

Glenn Gillard, Partner and Head of Insurance

Presentation title[To edit, click View > Slide Master > Slide Master]

3© 2016 Deloitte. All rights reserved

Contents

Welcome

Recent developments in the law relating

to general damages

Statistical review of the Irish Motor Market

Deloitte European Motor Study 2016

Motor Insurance reimagined

Cyber Risk and Data Privacy

The Future of Mobility

James Johnston│Senior Consultant, Financial Services, Strategy & Operations

Glenn Gillard│Partner and Head of Insurance

David Nolan SC│

Carmel Nivan│Actuarial Senior Manager

Darren Shaughnessy│Actuarial Manager

Ger Power│Actuarial Manager

Jacky Fox│Director, Enterprise Risk Services

John Kilbride│Director, Consulting

© 2016 Deloitte

Milestones

Nov 2015

RussellCase

Feb 2016

Oct 2016

Book of Quantum

Sep 2016

Mar 2016

Nov 2016

PPO published bill expected

Premiums

July 2016

Recent

developments

in the law

relating to

general

damages

David Nolan SC

© 2016 Deloitte. All rights reserved

Irish Motor Market

Environmental and Market Analysis

Carmel Niven

Darren Shaughnessy

Presentation title[To edit, click View > Slide Master > Slide Master]

7© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

8© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

9© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

10© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

11© 2016 Deloitte. All rights reserved

•Form 2 & Form 8 data

•CBI Insurance Statistics 2015

•An Garda Síochána Traffic Statistics

•Central Statistics Office (CSO)

•Department of Transport, Tourism and Sport

•Road Safety Authority

•Injuries Board

Data Sources

Presentation title[To edit, click View > Slide Master > Slide Master]

12© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

13© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

14© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

15© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

16© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

17© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

18© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

19© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

20© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

21© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

22© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

23© 2016 Deloitte. All rights reserved

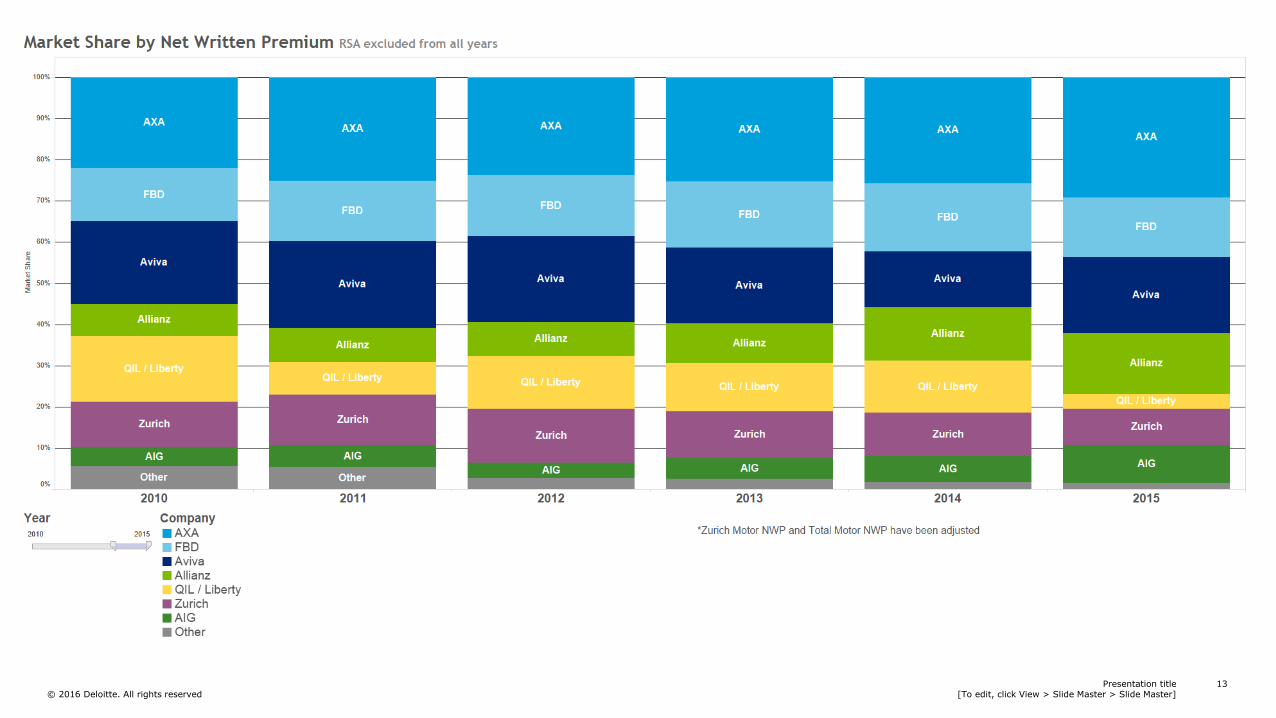

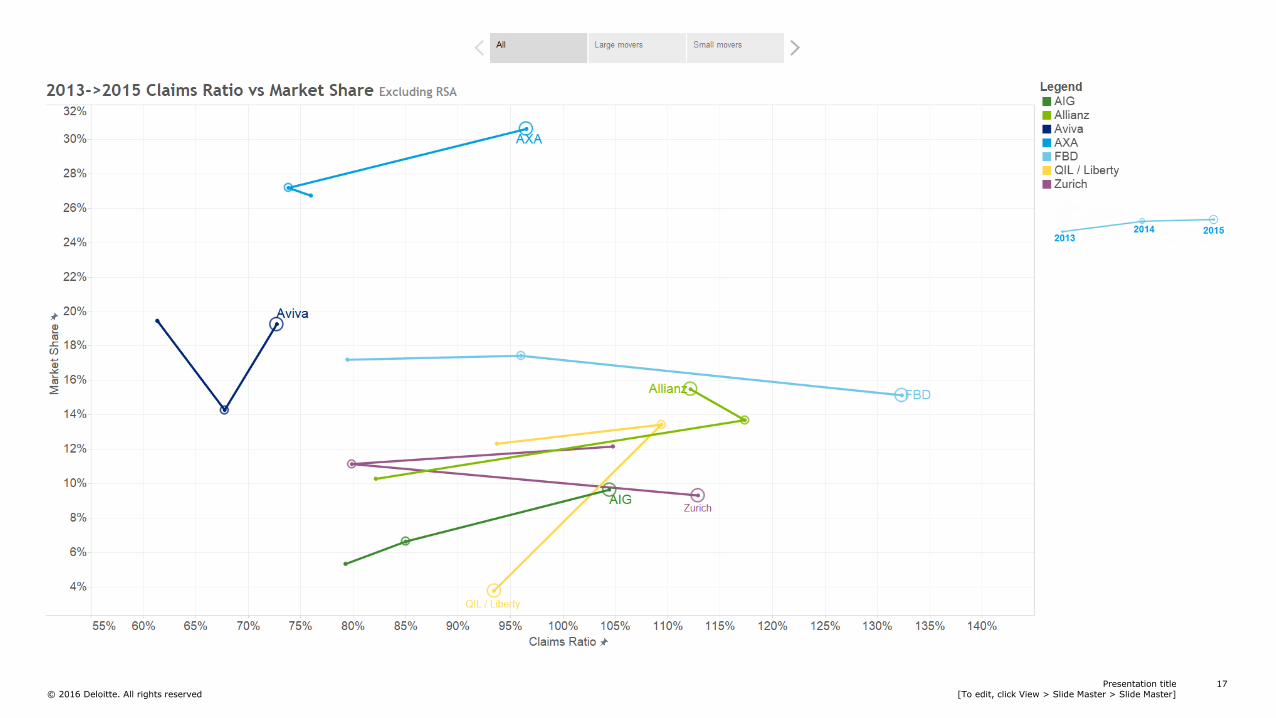

Aviva have been excluded due to inconsistencies in the data.

Presentation title[To edit, click View > Slide Master > Slide Master]

24© 2016 Deloitte. All rights reserved

Aviva have been excluded due to inconsistencies in the data.

Presentation title[To edit, click View > Slide Master > Slide Master]

25© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

26© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

27© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

28© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

29© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

30© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

31© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

32© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

33© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

34© 2016 Deloitte. All rights reserved

Presentation title[To edit, click View > Slide Master > Slide Master]

35© 2016 Deloitte. All rights reserved

European Motor

insurance study 2016

Gerard PowerActuarial Manager

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 37© 2016 Deloitte. All rights reserved

Overview of the study

The European motor market in numbers

Data sharing

Who is the digitally-enabled motor insurance customer?

What does the digitally-enabled motor insurance customer want?

App or dedicated device?

Customer concerns

Agenda

European Motor Insurance Study 2016

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 38© 2016 Deloitte. All rights reserved

• Objective of the study

• Conducted by over 20 Deloitte actuaries in 11 European countries:

• Austria, Belgium, France, Germany, Ireland, Italy, Netherlands, Poland, Spain, Switzerland, UK

• 2 main data sources –

• Large pan-European consumer survey

• Publicly available information on the size of each country’s personal motor market

Overview of the study

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 39© 2016 Deloitte. All rights reserved

Consumer survey

• The online survey contained a scenario-based conjoint analysis alongside a range of traditional questions

Overview of the study

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 40© 2016 Deloitte. All rights reserved

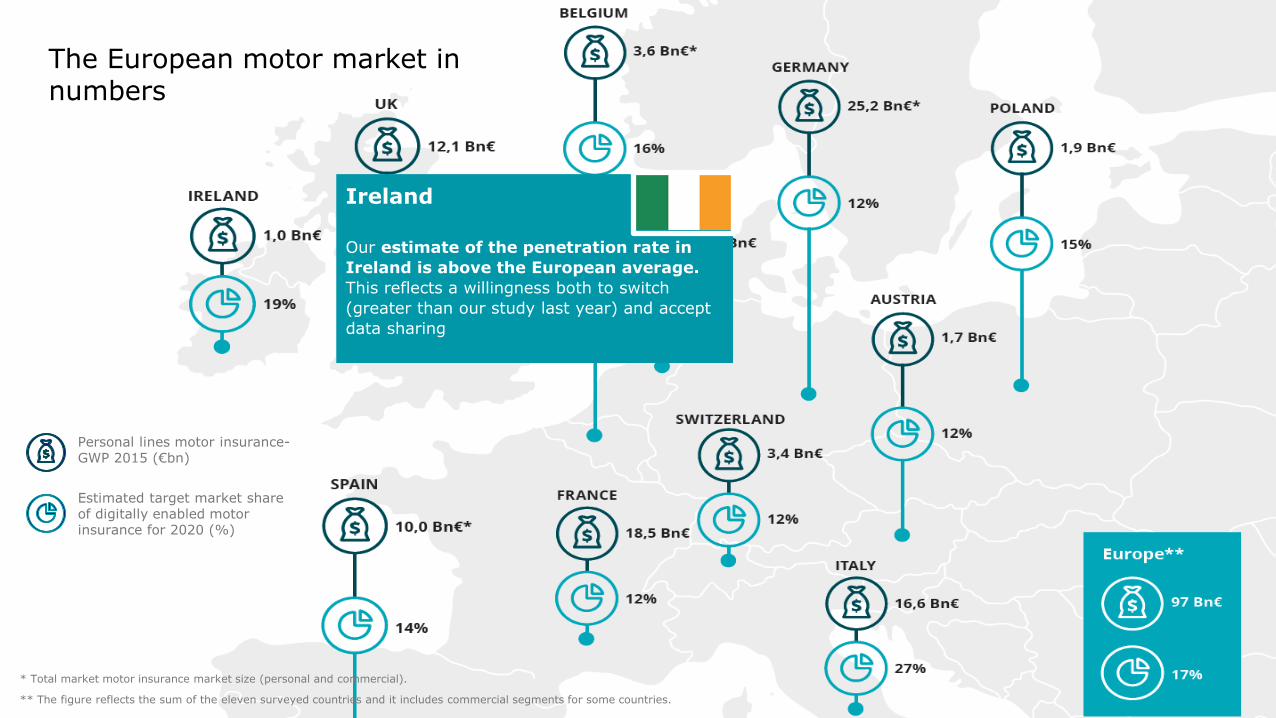

The European motor market in numbers

Personal lines motor insurance-GWP 2015 (€bn)

Estimated target market share of digitally enabled motor insurance for 2020 (%)

* Total market motor insurance market size (personal and commercial).

** The figure reflects the sum of the eleven surveyed countries and it includes commercial segments for some countries.

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 41© 2016 Deloitte. All rights reserved

The European motor market in numbers

Personal lines motor insurance-GWP 2015 (€bn)

Estimated target market share of digitally enabled motor insurance for 2020 (%)

* Total market motor insurance market size (personal and commercial).

** The figure reflects the sum of the eleven surveyed countries and it includes commercial segments for some countries.

Ireland

Our estimate of the penetration rate in

Ireland is above the European average.

This reflects a willingness both to switch

(greater than our study last year) and accept

data sharing

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 42© 2016 Deloitte. All rights reserved

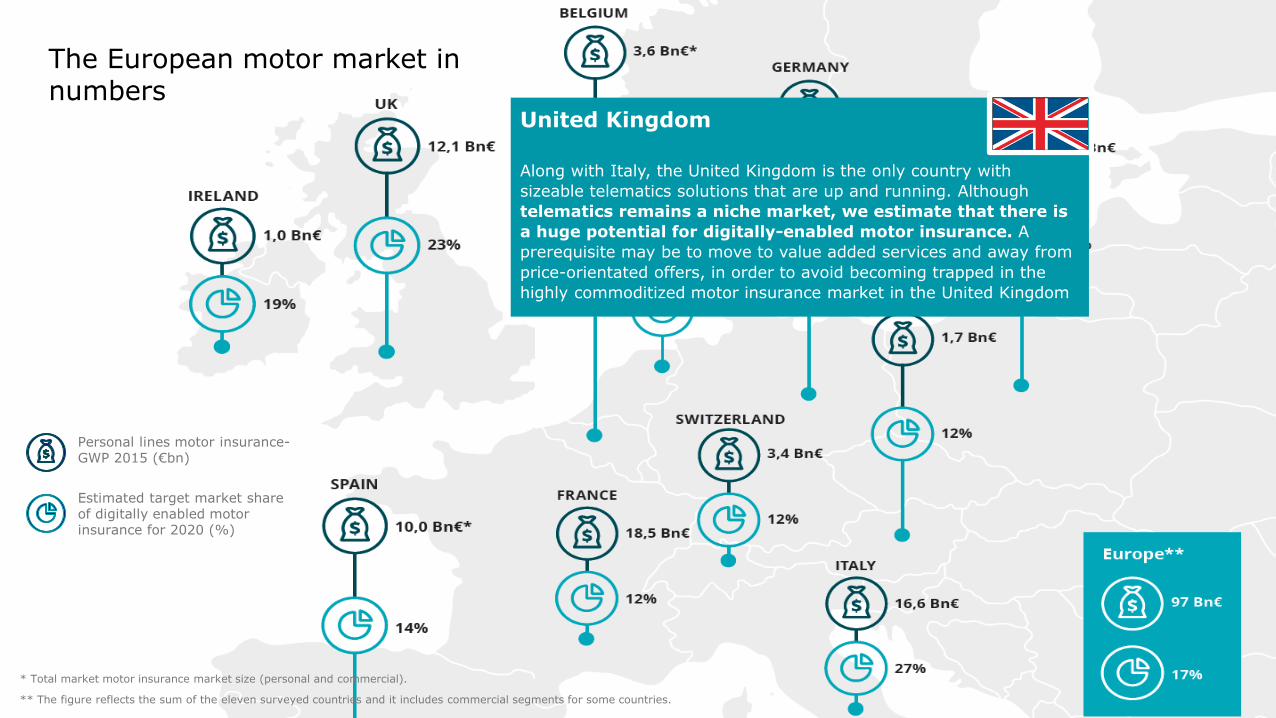

The European motor market in numbers

Personal lines motor insurance-GWP 2015 (€bn)

Estimated target market share of digitally enabled motor insurance for 2020 (%)

* Total market motor insurance market size (personal and commercial).

** The figure reflects the sum of the eleven surveyed countries and it includes commercial segments for some countries.

United Kingdom

Along with Italy, the United Kingdom is the only country with

sizeable telematics solutions that are up and running. Although

telematics remains a niche market, we estimate that there is

a huge potential for digitally-enabled motor insurance. A

prerequisite may be to move to value added services and away from

price-orientated offers, in order to avoid becoming trapped in the

highly commoditized motor insurance market in the United Kingdom

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 43© 2016 Deloitte. All rights reserved

The European motor market in numbers

Personal lines motor insurance-GWP 2015 (€bn)

Estimated target market share of digitally enabled motor insurance for 2020 (%)

* Total market motor insurance market size (personal and commercial).

** The figure reflects the sum of the eleven surveyed countries and it includes commercial segments for some countries.

Italy

In Italy, the telematics market share is

already 15%, and our projection indicates that

by 2020 digitally enabled motor insurance

could represent as much as 27% of the

motor insurance market

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 44© 2016 Deloitte. All rights reserved

The European motor market in numbers

Personal lines motor insurance-GWP 2015 (€bn)

Estimated target market share of digitally enabled motor insurance for 2020 (%)

* Total market motor insurance market size (personal and commercial).

** The figure reflects the sum of the eleven surveyed countries and it includes commercial segments for some countries.

Germany

Data sharing is a sensitive topic in Germany.

Nevertheless, assuming this issue is tackled, given

the size of the domestic market and the level of

willingness to switch, our projections point to it being

one of the biggest European markets for digitally-

enabled motor insurance.

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 45© 2016 Deloitte. All rights reserved

Data sharing

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 46© 2016 Deloitte. All rights reserved

Who is the digitally-enabled motor insurance customer?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 47© 2016 Deloitte. All rights reserved

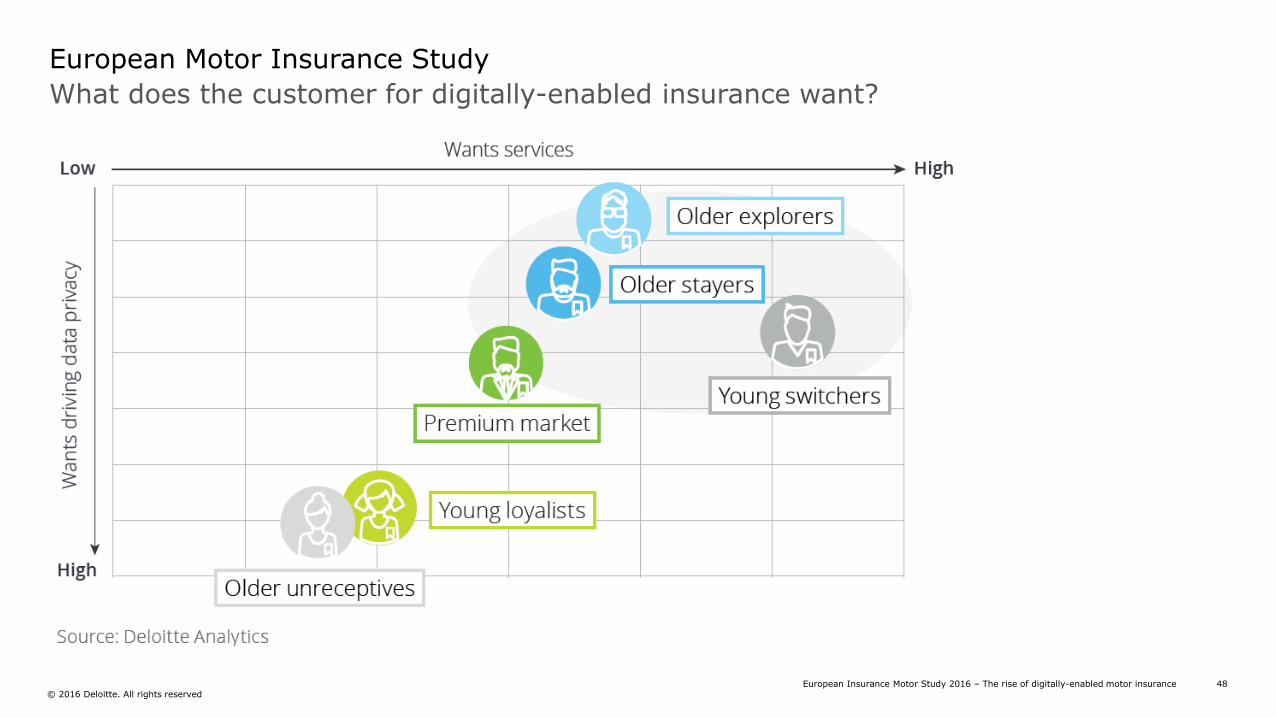

What does the customer for digitally-enabled insurance want?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 48© 2016 Deloitte. All rights reserved

What does the customer for digitally-enabled insurance want?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 49© 2016 Deloitte. All rights reserved

How to best serve your customers?

European Motor Insurance Study

Digitally-enabled motor insurance could be the opportunity for insurers to start a new type ofrelationship and product offering with their policyholders.

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 50© 2016 Deloitte. All rights reserved

How to best serve your customers?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 51© 2016 Deloitte. All rights reserved

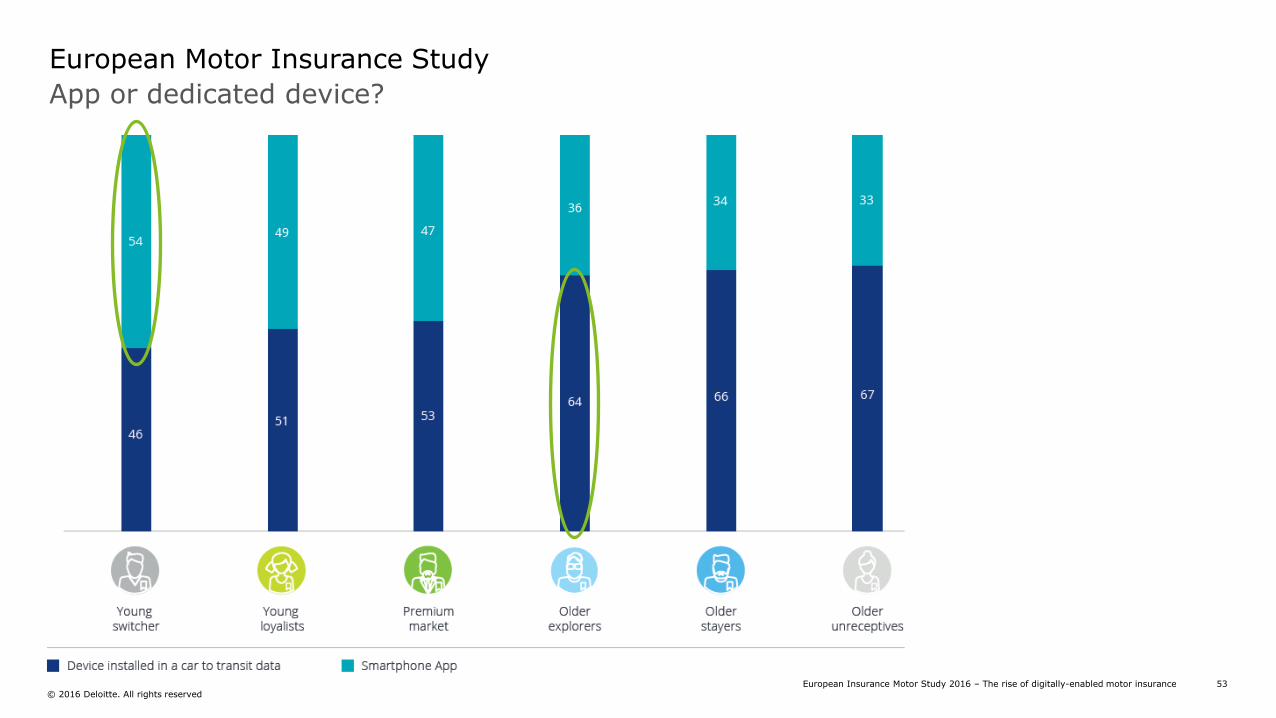

App or dedicated device?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 52© 2016 Deloitte. All rights reserved

App or dedicated device?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 53© 2016 Deloitte. All rights reserved

App or dedicated device?

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 54© 2016 Deloitte. All rights reserved

Customer concerns

European Motor Insurance Study

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 55

© 2016 Deloitte. All rights reserved

Conclusion

European Motor Insurance Study

Digitally-enabled motor insurance opens up a window of opportunity for motor insurers to extend the value proposition from claims-related services to a larger scope of services related to mobility.

Motor insurance

reimagined

James Johnston Senior Consultant, Financial Services, Strategy & Operations

Presentation title[To edit, click View > Slide Master > Slide Master]

57© 2016 Deloitte. All rights reserved

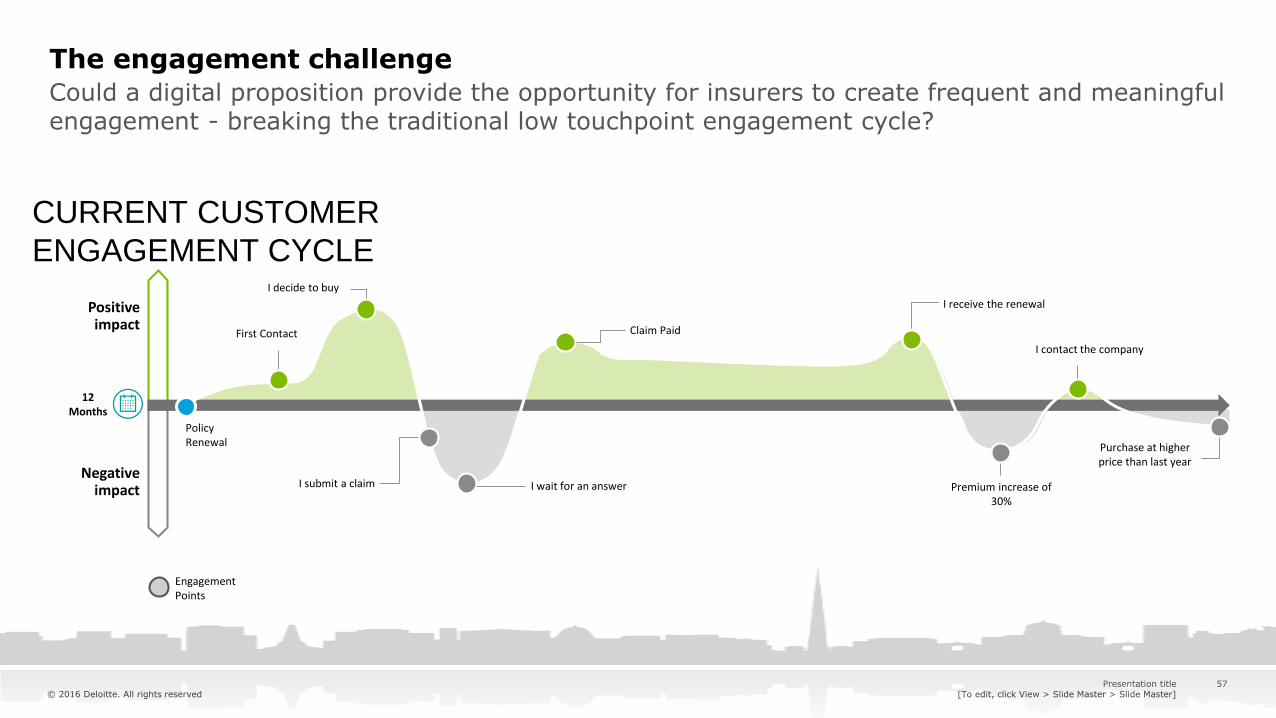

Could a digital proposition provide the opportunity for insurers to create frequent and meaningful engagement - breaking the traditional low touchpoint engagement cycle?

The engagement challenge

Policy Renewal

First Contact Claim Paid

I wait for an answer

I decide to buy

I receive the renewal

Premium increase of 30%

No I submit a claim

I contact the company

Positive impact

Negative impact

Engagement Points

Purchase at higher price than last year

12 Months

CURRENT CUSTOMER

ENGAGEMENT CYCLE

58© 2016 Deloitte. All rights reserved

Real-time Notifications Journey Assessments

Reactive Rewards

Car ConciergeAuto Claims Support

Green Driving

Usage Based

Motor re-imagined – through a digital proposition

Thinking outside of traditional product parameters, what features could be included to create meaningful engagement with customers?

Motor Insurance reimagined

Barry’s Story

Presentation title[To edit, click View > Slide Master > Slide Master]

60© 2016 Deloitte. All rights reserved

Getting on the road – usage based

Barry has provided his personal details to his insurer. He’s downloaded their app and permitted access to his digital wallet to pay his monthly usage based premium. He is now ready to get behind the wheel.

A discount in premium is the most important factor when deciding to

purchase a telematics product

Presentation title[To edit, click View > Slide Master > Slide Master]

61© 2016 Deloitte. All rights reserved

Real-time Notifications

Barry sets off to go Christmas shopping. There has been a crash on the M50, which is the route Barry takes to Dundrum. His insurer notifies Barry of this ahead of time and re-directs him to the fastest route.

53% of Irish customers are very comfortable with sharing vehicle data and 65% very/somewhat comfortable

with sharing geographical data

Presentation title[To edit, click View > Slide Master > Slide Master]

62© 2016 Deloitte. All rights reserved

Journey Assessment

On his way to Dundrum, Barry did not break any speed limits or use his phone while driving. He has earned 3 reward points as a result. He is now top of the leader board in his household and maintains his 5 star rating.

Irish customers are comfortable with sharing behaviour data (44% Very

and 33% Somewhat)

Presentation title[To edit, click View > Slide Master > Slide Master]

63© 2016 Deloitte. All rights reserved

Reactive Rewards

Barry receives an alert while in Dundrum to let him know he can use his rewards points to pick up a free coffee in Butlers, who are one of the affinity partners linked to his policy.

Almost two thirds of Irish customers are willing to share data in return for

geo-notification discounts

Presentation title[To edit, click View > Slide Master > Slide Master]

64© 2016 Deloitte. All rights reserved

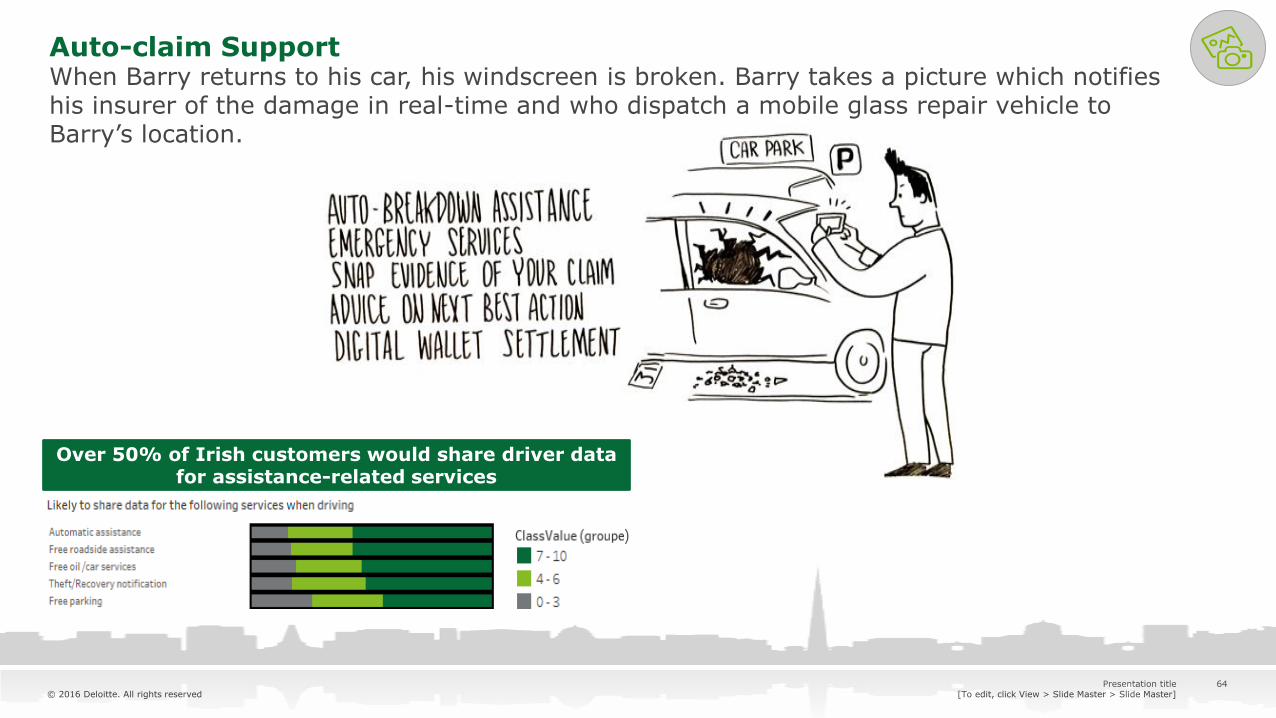

Auto-claim SupportWhen Barry returns to his car, his windscreen is broken. Barry takes a picture which notifies his insurer of the damage in real-time and who dispatch a mobile glass repair vehicle to Barry’s location.

Over 50% of Irish customers would share driver data for assistance-related services

Presentation title[To edit, click View > Slide Master > Slide Master]

65© 2016 Deloitte. All rights reserved

Car ConciergeBarry has allowed his insurer access to his personal calendar via Microsoft office. His NCT is due in the next month so his insurer schedules this in his calendar and books it at a time that suits him over the Christmas period.

66© 2016 Deloitte. All rights reserved

Real-time Notifications Journey Assessments

Reactive Rewards

Car ConciergeAuto Claims Support

Green Driving

Usage Based

Green driving rating

Snap evidence of your claimAdvice on next best action

Digital wallet settlement

Auto-breakdown assistanceEmergency services

Tips & tricks for environmentally friendly driving

Real-time routing

Vehicle Diagnostics & Servicing

Accident Area Avoidance

Personal Planner

NCT booking & tax renewal Service reminders

Car rental Airport parking booking

Location-based offers

Rewards Partnerships

Safety index rating

Geo-fencing

Societal & domestic leader board

Rewards tokens based on scorePremium discount

Behaviour based premium

Digital wallet

Individual driver record

67© 2016 Deloitte. All rights reserved

Jacky Fox

Cyber & Data

Securing your data - a regulatory perspective

Central Bank Focus

• Governance• Cyber Risk management• Security awareness training• Security Operations • Threat intelligence• Incident management• Data management• Identity and Access management• Management of outsourcing/third

parties

69© 2016 Deloitte. All rights reserved

Cyber video: Companies like yours

http://www2.deloitte.com/global/en/pages/risk/articles/cybervideo-companies-like-yours.html

Is your Battle Plan ready?

Deloitte 2016

General Data Protection Regulation May 2018

71© 2016 Deloitte. All rights reserved

• GDPR is a regulation as opposed to a local implementation of a directive

• Is your organisation ready for May 2018?

− governance, policies & procedures, DPO

• Has your organisation started preparing from a technology perspective?

− your legacy systems

− data analytics

− marketing

• Highlights of how GDPR affects some technology aspects of the data lifecycle

Overview

72© 2016 Deloitte. All rights reserved

• Data subjects are entitled to compensationfrom all data controllers in the chain of abreach

• Administrative fines for infringements ofcertain provisions the maximum fines are€10M or 2% global turnover

• Administrative fines for infringements ofArticles 5,6,7 & 9 or non-compliance with anorder from the supervisory can result in finesup to a maximum of €20M or 4% globalturnover

GDPR has Sanctions

73© 2016 Deloitte. All rights reserved

Authority to collect can be by contract, consentor other legal requirement e.g. tax authority

“Consent is presumed not to be freely given if itdoes not allow separate consent to be given todifferent data processing operations” (34)

• Systems need to explicitly demonstratepurpose of collection - this needs to be clearand transparent

• Record consent(s) - determine how to keepthis record

• Data elements needs to be proportionate insupport of data minimisation

Point of collection

74© 2016 Deloitte. All rights reserved

What about data that you already have collectedor extrapolated? How do you acquireretrospective consent.

• redesign of databases/repositories toaccommodate this

• How do you approach this from a systemperspective - campaign vs next contact

Full understanding of data third parties hold onyour behalf, data held in non-EEA countries andthe impact of events like Brexit

• Put systems in place to map data lifecycle andaudit and monitor compliance

Storage

75© 2016 Deloitte. All rights reserved

Processing needs to be compatible with theoriginal collection. “The controller should be ableto demonstrate that the data subject has givenconsent to the processing operation”

• Ability to restrict analytics on data in yourpossession e.g. marketing processes need tobe able to exclude non-consent subjects

• Need to modify apps & databases to put flagsin for various permissions e.g. share datawith other organisations

• Maintain and produce a record of processingactivities (Article 28)

• Subject is entitled to request details of thepurpose of processing activity (51)

Processing

76© 2016 Deloitte. All rights reserved

Setting a retention period is one thingimplementing this is practice is another.

Data spawns and replicates within organisationsand beyond e.g. insuring a car, crash, claim,points

• Systems will need to remove, anonymise orpseudonymise data when it is no longerrequired

• Designing or modifying a system to supportthe right to be forgotten (53)

• Designing systems that extend this right outfrom the original publisher to links andreplications (54) e.g. John Doe charged withassault

Removal & Right to be Forgotten

77© 2016 Deloitte. All rights reserved

“A subject should be able to receive the personaldata concerning him or her which he or she hasprovided to the controller in a structured,commonly used, machine-readable andinteroperable format” (55)

• To easily support this systems will need to bedesigned to easily extract and communicatesubject data. This process may need tosupport partial transfers and consider theprivacy of other subjects

• Controller to controller transfer may need tobe supported e.g. Utilities, banks, insurance

Portability

78© 2016 Deloitte. All rights reserved

Profiling includes the processing of data in orderto analyse or predict personal preferences,behaviours, and attitudes (21)

• Systems need to be in place to informsubjects of the existence and nature ofprofiling and record consent andpreferences. They also need to explain whatmight be lost for non-consent e.g. a betterphone or no claims bonus (48)

Profiling

79© 2016 Deloitte. All rights reserved

The required response period has decreasedfrom 40 days to one month. SARs will now beFOC.

• Controllers will need to provide systems toaccept SARs electronically

• Where possible a remote access securesystem for self service should be provided

− this would need to protect accidentalexposures (51) e.g. brother test

− Challenge around unstructured data

• Systems need to support rectification of data– this could be challenging for extrapolated orretrieved data

Subject Access Requests & Rectification

80© 2016 Deloitte. All rights reserved

• Data protection by design and by default(Article 23)

− Proportionality

− Consent

− Appropriate processing

− Access Control

• Data privacy impact assessments need to bepreformed on certain systems. This involvesmapping out data repositories, usage, access,consent (Article 33)

Privacy by Design & DPIA

81© 2016 Deloitte. All rights reserved

• Predict that pseudonymisation for historictrend and marketing analysis will be common,systems should be designed with this abilitybuilt in

• Smart use of encryption can greatly reducethe risk to your subjects

• Certification in some shape or form will beintroduced - (Article 39)

• Access control systems will be required

• Systems need to be designed to resistaccidental or unlawful events (39)

Security

82© 2016 Deloitte. All rights reserved

Some food for thought….Conclusion

The GDPR regulation does not differentiate between Legacy vs New systems - do not underestimate the budget and effort required to comply

If you do not have a register of your data assets and how they are used – how can you offer assurance that they are protected?

It is likely that CBI thematic inspections will focus on areas raised in the September 2016 report

Organisations need to review their Cyber Security Governance and embed a culture of Security and Privacy by design

€20M/4% of global turnover is significant

83© 2016 Deloitte. All rights reserved

Jacky Fox

Cyber & IT Forensic Lead

Deloitte

Thanks for listening

The future of mobility

John KilbrideDirector, Consulting

85© 2016 Deloitte. All rights reserved

Insuring the future of mobility video: Insurance industry business models under consideration

https://dupress.deloitte.com/dup-us-en/multimedia/videos/mobility-ecosystem-future-of-auto-insurance.html

86© 2016 Deloitte. All rights reserved

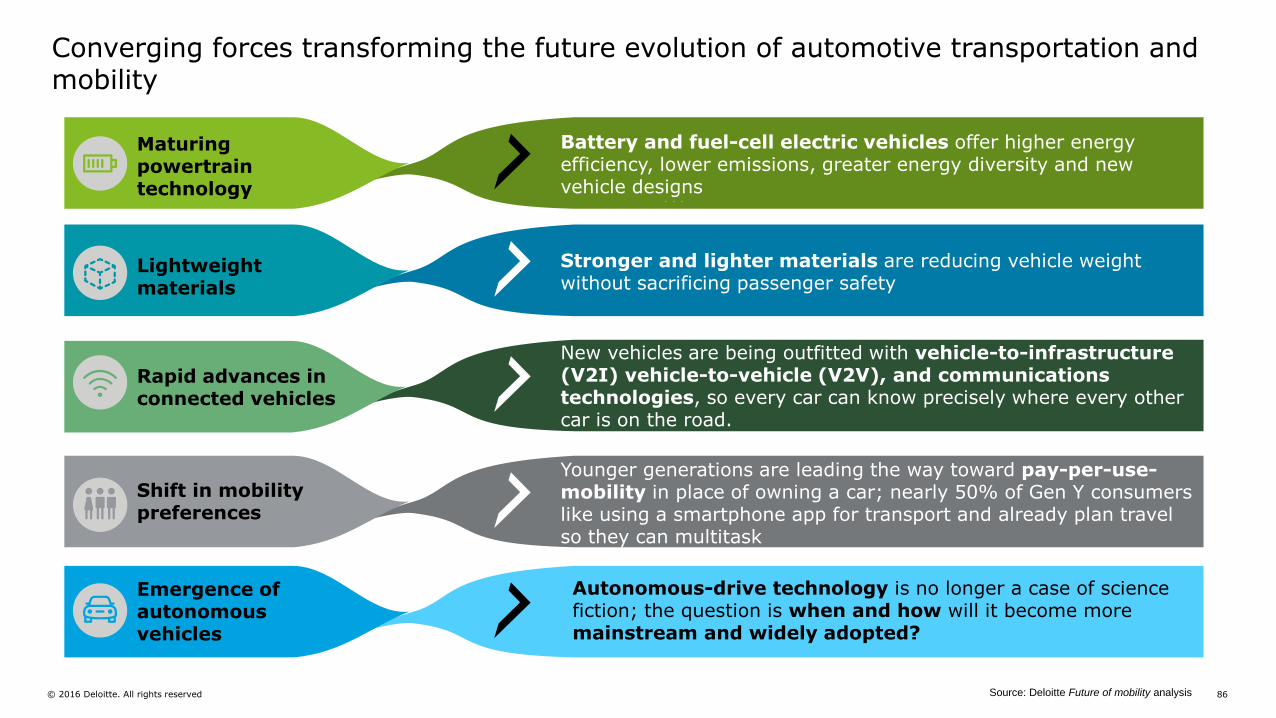

Converging forces transforming the future evolution of automotive transportation and mobility

Source: Deloitte Future of mobility analysis

Maturing powertrain technology

Lightweight materials

Rapid advances in connected vehicles

Shift in mobility preferences

Emergence of autonomous vehicles

Battery and fuel-cell electric vehicles offer higher energy efficiency, lower emissions, greater energy diversity and new vehicle designs

Stronger and lighter materials are reducing vehicle weight without sacrificing passenger safety

New vehicles are being outfitted with vehicle-to-infrastructure (V2I) vehicle-to-vehicle (V2V), and communications technologies, so every car can know precisely where every other car is on the road.

Younger generations are leading the way toward pay-per-use-mobility in place of owning a car; nearly 50% of Gen Y consumers like using a smartphone app for transport and already plan travel so they can multitask

Autonomous-drive technology is no longer a case of science fiction; the question is when and how will it become more mainstream and widely adopted?

87© 2016 Deloitte. All rights reserved

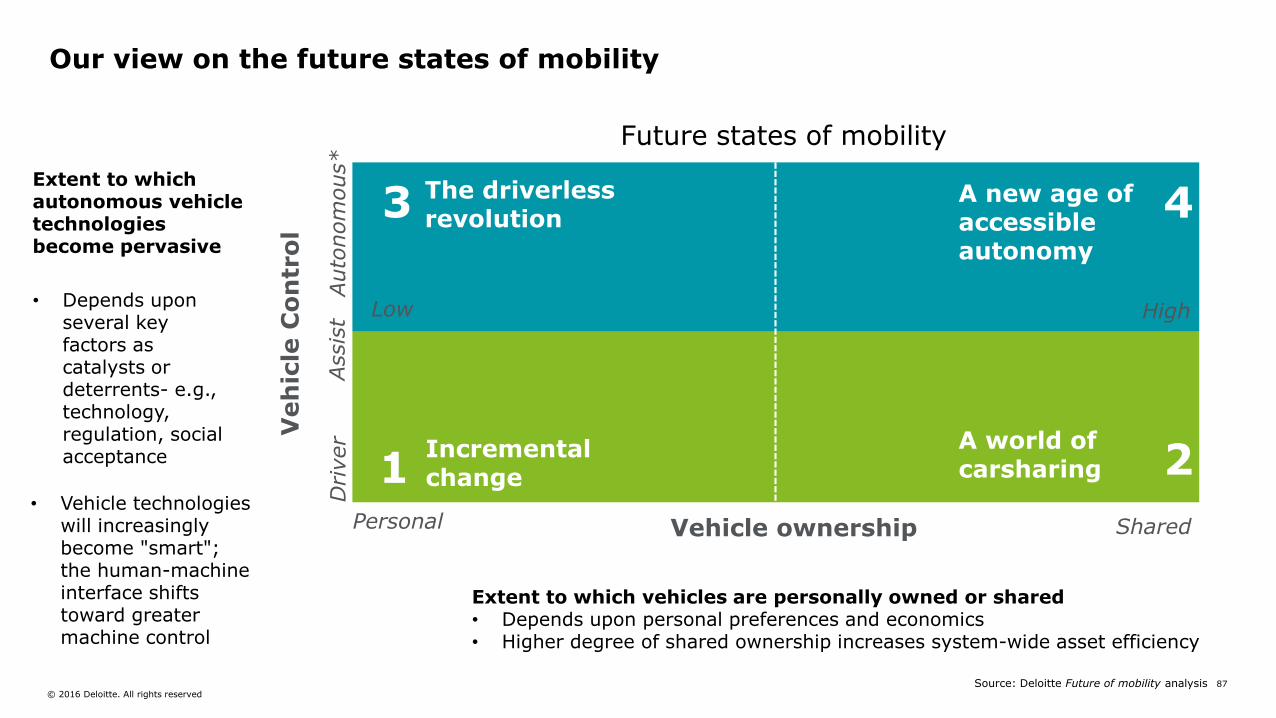

Our view on the future states of mobility

3

1

4

2

Extent to which autonomous vehicle technologies become pervasive

• Depends upon several key factors as catalysts or deterrents- e.g., technology, regulation, social acceptance

• Vehicle technologies will increasingly become "smart"; the human-machine interface shifts toward greater machine control

The driverless revolution

A new age of accessible autonomy

Incremental change

A world of carsharing

Extent to which vehicles are personally owned or shared• Depends upon personal preferences and economics• Higher degree of shared ownership increases system-wide asset efficiency

Low High

Personal Shared Vehicle ownership

Veh

icle

Co

ntr

ol

Assis

tD

river

Auto

nom

ous*

Future states of mobility

Source: Deloitte Future of mobility analysis

88© 2016 Deloitte. All rights reserved

Profound disruption will extend far beyond just the automotive industry

Motor Vehicles: decrease in personally-owned vehicle sales and increase in fleet vehicle sales.

Energy: Lower energy consumption from improved vehicle efficiency and the cost of commuting drops

Finance: Growth in fleet financing in place of auto loans and leasing

Insurance: Shifts from personal liability to catastrophic system-failure insurance

Media: Increase in consumption of multimedia and information due to not driving

Medical & Legal: Reduction of costs for emergency medical services and related legal fees because of fewer accidents

Retail: Increase in sales due to increased mobility of underserved segments (e.g. seniors)

Telecom: Additional bandwidth requirements to meet increased demand for connectivity and reliability

Technology: Emergence of automotive drive operating system players

Transportation: Substitution of demand for traditional taxis, limos, and rental vehicles with shared fleet vehicles

Closing comments

Glenn Gillard Partner and Head of Insurance

European Insurance Motor Study 2016 – The rise of digitally-enabled motor insurance 90© 2016 Deloitte. All rights reserved

Output from the study

European Motor Insurance Study

European Motor Study report Interactive Tableau dashboard

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/ie/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. With over 210,000 professionals globally, Deloitte is committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global Services Limited, Deloitte Global Services Holdings Limited, the Deloitte Touche Tohmatsu Verein, any of their member firms, or any of the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your finances or your business. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2016 Deloitte. All rights reserved