Embed Size (px)

Citation preview

Health Plan Coverage Effectuation: Payments, Grace Periods, and Terminations

November 3, 2017

Effectuated Enrollment Snapshot 2016-2017

Approximately 12.2 million consumers selected orwere automatically re-enrolled in Federally FacilitatedExchange (FFE) individual market plans during the2016-2017 Open Enrollment period.

However, of the approximately 12.2 million consumerswho selected a plan, an estimated 10.3 millionconsumers paid their first month’s premium (alsoknown as a “binder payment”) and had coverage takeeffect.

2

Steps to Effectuate Coverage Using the Federal Eligibility and Enrollment Platform

1. Consumer completes application.

2. Consumer selects a plan.

3. Issuer timely collects first premium from the consumer.

4. Issuer informs the FFE of effectuated coverage.

3

Binder Payment and Effectuation

Consumers must pay their first month’s premium (“binder payment”) for enrollment to be effectuated.

The deadline for making the binder payment for enrollment to be effectuated must be:

No earlier than the coverage effective date.

No later than 30 calendar days from the coverage effective date. 4

Scenario 1

5

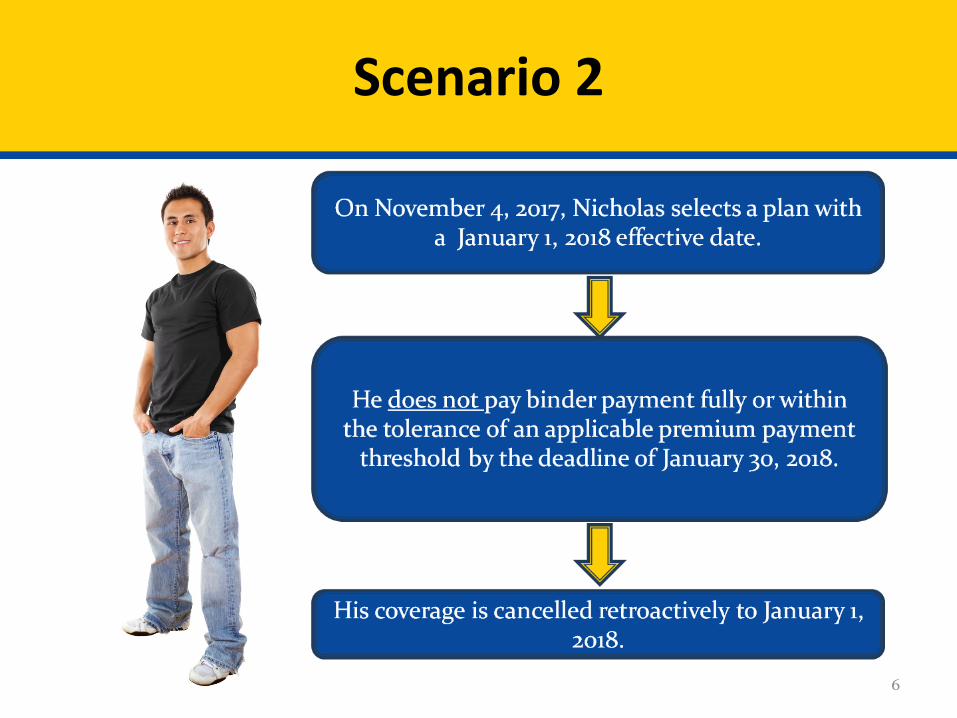

Scenario 2

6

What is a Grace Period?

A grace period is an extension, set by state or federal rules, that gives consumers additional time to pay the monthly health insurance premiums before the coverage is terminated for non-payment of premium.

The length of a grace period depends on the consumer’s eligibility according to the following guidelines: Consumers receiving Advanced Premium Tax Credits (APTCs) when they became

delinquent have a grace period of three (3) consecutive months. All other consumers not receiving the benefit of APTC have a grace period determined

by state rules. Contact your state Department of Insurance for information on grace periods in

your state. Grace periods generally do not apply to the deadline an issuer sets for the payment

of a binder to effectuate coverage.

TIP: It is important to pay all outstanding insurance premiums during a grace period so your health insurance company doesn’t end your coverage.

7

Payment Deadline Extensions 2017 Hurricane Disasters

In response to requests or direction from state authorities, issuers mayconsider setting more generous deadlines for payments to effectuateprospective coverage.

Issuers may consider allowing affected enrollees: To make a binder payment more than 30 days

after their coverage effective date if theenrollee’s coverage would be effectuated underthe regular coverage effective date.

To make a binder payment on a date occurringafter the later of either (1) the date the issuerreceives the enrollment transaction or (2) theeffective date for such coverage if the enrollee’sprospective coverage would be effectuatedunder special effective date rules.

In the absence of specific state guidancerelating to the length of such extensions,issuers may allow affected enrollees anextension of no more than 60 days fromthe original binder payment deadline.

8

Payment Deadline Extensions 2017 Hurricane Disasters (continued) In response to a request or direction from state health insurance

authorities, issuers may provide a more generous grace period forconsumers receiving APTC.

CMS will not take enforcement action against an issuer that does notimmediately terminate an affected individual’s coverage at the end of thethree-month grace period if the individual’s grace period expires (or willexpire) on or after the date one week prior to the start of a FEMA-designated incident period.

The QHP issuer may grant such an affected individual an additional 60days, or an extension period whose length is determined by the request ororder of the applicable state authorities, to satisfy past due premiumpayments.

Issuers may implement these grace period extensions from the date oneweek before the start of a FEMA-designated incident period through theend of such incident period.

9

Claims for Consumers that are Behindin Premium Payment

During the first month of a three-month grace period for consumersreceiving APTC, the issuer must pay all appropriate claims for servicesrendered to the consumer.

The issuer may pend claims for services rendered during the second andthird months of the grace period for consumers receiving APTC.

If a consumer fails to pay all outstandingpremium, or an amount that satisfies anyapplicable premium threshold, before theend of the grace period: The consumer’s coverage will be

terminated, effective on the last day ofthe first month of the grace period, fornon-payment of their premium.

The issuer will deny any claims that werepended during the second and thirdmonths of the three-month grace period. 10

Claims for Consumers that are Behind in Premium Payment due to 2017 Hurricane Disasters

Issuers must:

Provide consumers with adequate notice that the consumers’ coverage will not be terminated

Provide consumers with adequate notice on how grace period extensions might affect guaranteed availability for consumers during the 2018 Open Enrollment.

Pay all appropriate claims for services rendered to the consumer during the first month of the grace period and may pend claims for services rendered to the consumer in subsequent months of the grace period.

Notify the U.S. Department of Health and Human Services of such non-payment of premiums.

Notify providers of the possibility that claims submitted for services rendered after the first month of the grace period may be pended and, ultimately reversed.

11

Knowledge Check 1 Grace Period in General

John, who’s eligible for APTC, selectshis plan during Open Enrollment.

John makes his binder payment ontime to effectuate his coverage.

John does not make a premiumpayment for May.

By the end of the three-month graceperiod, John has not paid alloutstanding premium owed (withinthe tolerance of any applicablepremium payment threshold).

12

Knowledge Check 1: Question 1

When does John’s grace period expire? A. July 31 B. August 31 C. September 30 D. October 31

13

Knowledge Check 1: Question 1 Results

When does John’s grace period expire? A. July 31 B. August 31 C. September 30 D. October 31

14

Knowledge Check 1: Question 2

If John still has outstanding premium after July 31, may the issuer of John’s QHP deny any pended claims during June and July?

Answer: Yes or No

15

Knowledge Check 1: Question 2 Results

If John has outstanding premium after July 31, may the issuer of John’s QHP deny any pended claims during June and July?

16

Termination for Non-payment of Premiums

Consumers must pay all outstanding premium amounts or an amountsufficient to satisfy any premium payment threshold before the end ofthe grace period to avoid termination for non-payment of premiums.

A grace period does not “reset” when an enrollee makes a partialpayment.

When a consumer’s coverage is terminated for non-payment ofpremiums, the consumer does not qualify for an SEP for the resultingloss of minimum essential coverage. (MEC)

A consumer who is eligible for APTC but elects not to receive APTC isnot eligible for a three-month grace period but is eligible for the graceperiod required by the consumer’s state for consumers who aredelinquent in paying their premiums.

IMPORTANT: Enrollees who terminate their coverage due to hardship from a hurricane may be exempt from tax penalties. For more information, see: https://marketplace.cms.gov/technical-assistance-resources/exemption-general-hardship.pdf.

17

Knowledge Check 2 Termination for Non-payment

Patrick, who’s eligible for andelects to receive the benefit ofAPTC, selects his plan duringOpen Enrollment.

Patrick fails to make his Augustpayment.

Patrick fails to make hisSeptember payment.

Patrick pays his August andSeptember premium in full atthe end of September.

Patrick fails to make Octoberpayment.

18

Knowledge Check 2: Question 1

Is Patrick still in a grace period if he pays his August and September premiums in full before October’s premium is due?

Answer: Yes or No

19

Knowledge Check 2: Question 1 Results

Is Patrick still in a grace period if he pays his August and September premiums in full before October’s premium is billed and due?

20

Final Marketplace Stabilization Rule

A QHP issuer does not violate guaranteed availability requirements if the issuer: 1. Attributes a premium payment under the same or different product to

premiums due to that issuer within the prior 12 months, and 2. Refuses to effectuate new coverage for failure to pay premiums.

This means, to the extent permitted by state law, an issuer who has provided proper notice of the consequences of non-payment of premium to its enrollees can require an individual or employer to pay all past-due premiums for coverage in the preceding 12-month period before they will effectuate new coverage. This interpretation does not allow an issuer to condition effectuation of new

coverage on payment of premiums owed to a different issuer or to condition the effectuation of coverage on payment of past-due premiums by an individual other than the person contractually responsible for the premium payment. o An issuer may be able to collect past-due premiums for a different issuer

if both issuers are in the same controlled group. 21

Final Marketplace Stabilization Rule (Continued)

Issuers that adopt this premium payment policy, as wellas issuers that do not adopt the policy but are within anadopting issuer's controlled group, must, in enrollmentapplication materials and notices about non-payment ofpremiums (in paper or electronic form), clearly describethe consequences of non-payment of premium on futureenrollment.

An issuer that adopts such a payment policy is requiredto apply its uniformly to all employers or individuals insimilar circumstances regardless of health status andconsistent with non-discrimination requirements.

22

QHP Non-renewal for Medicare Entitlement

An issuer is prohibited from re-enrolling inindividual market coverage a consumer who theissuer knows is entitled to Medicare Part A orenrolled in Medicare Part B if the coverage wouldduplicate Medicare benefits to which the enrolleeis entitled.

Exception: Unless the renewal is under the samepolicy or contract of insurance, which would bedetermined using state rules.

23