Embed Size (px)

Citation preview

www.beyondphilosophy.com

A Get Well Card for Healthcare SectorsCustomer Experience Trend Tracker

Q1 2010

www.beyondphilosophy.com

1. Viewer Window 2. Control Panel

Beyond Philosophy © All rights reserved. 2001-2010 2

GoToWebinar Example Interface

www.beyondphilosophy.com 3Beyond Philosophy © All rights reserved. 2001-2010

The Beyond Philosophy Perspective

Customer Experience is all we do!

Thought leadership is our differentiator

Offices in London, Atlanta with Partners in

Europe & Asia

Fourth book launched in September 2010

Focus on the emotional side of the Customer Experience

Links with Academia

www.beyondphilosophy.com 4

We are Proud to Have Helped Some Great Organizations…

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

A Get Well Card for Healthcare SectorsCustomer Experience Trend Tracker

Q1 2010

www.beyondphilosophy.com

Agenda

6Beyond Philosophy © All rights reserved. 2001-2010

Introduction

The Cost-Health Outcome Balance

The Shift In Healthcare

The Artificial Divide in the Healthcare Experience

The Customer Experience Way

Recommendations

Q&A

www.beyondphilosophy.com

Healthcare = Koyaanisqatsi

7

In the Hopi language, “Koyaanisqatsi” means "crazy life, life in turmoil, life out of balance, life disintegrating, a state of life that calls for another way of living“

In the USA, one-third of health care expenditures, about $700 billion or nearly 5% of GDP, did not improve health

outcomes. (Source: Congressional Budget Office, 2006 )

In the UK, projections show that the cost of the existing [NHS] system will almost double by 2026, yet without any improvement in the outcomes that could be achieved through radical reform. (Source: King’s Fund, 2010)

www.beyondphilosophy.com

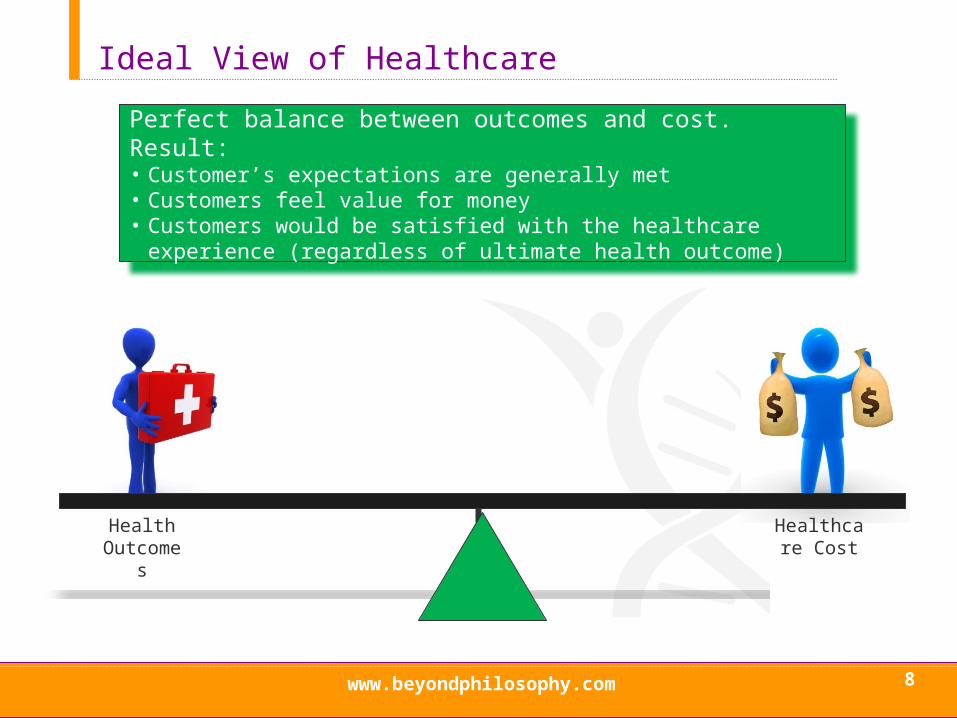

Ideal View of Healthcare

8

Perfect balance between outcomes and cost. Result:• Customer’s expectations are generally met• Customers feel value for money• Customers would be satisfied with the healthcare experience (regardless

of ultimate health outcome)

Health Outcomes

Healthcare Cost

www.beyondphilosophy.com

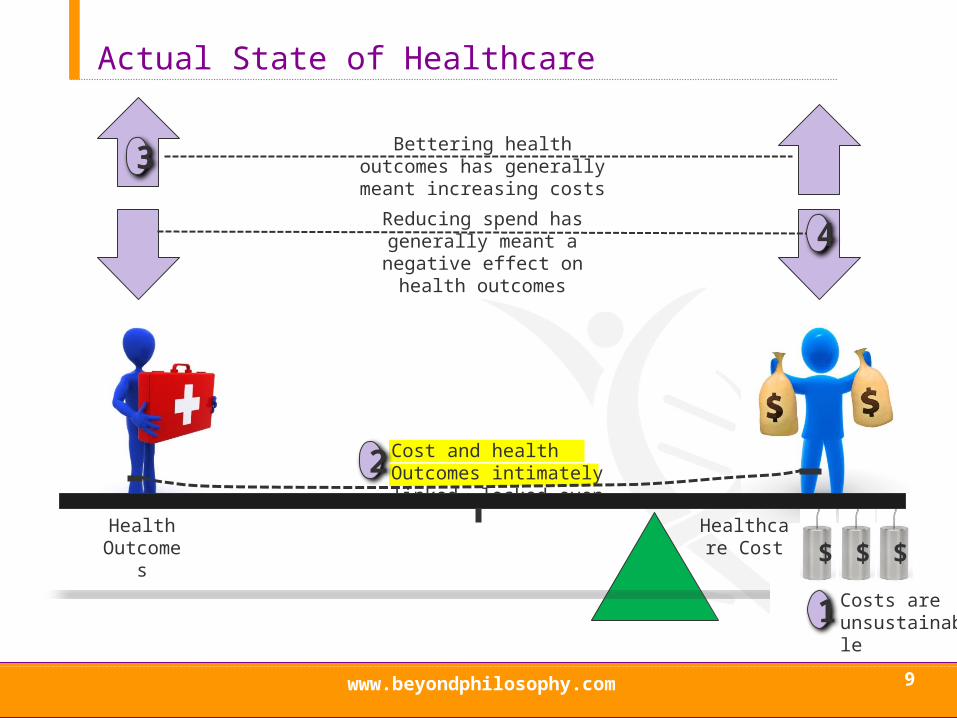

Actual State of Healthcare

9

3Bettering health outcomes has

generally meant increasing costs

Reducing spend has generally meant a negative effect on health outcomes 4

Health Outcomes

Healthcare Cost

2 Cost and health Outcomes intimately linked, locked even

1 Costs are unsustainable

$ $ $

www.beyondphilosophy.com

Customer Experience Trend Tracker Research

1,000 interviews

UK and USA

Online survey looking at the healthcare experience across four key touch points:

Physician/Primary healthcare provider

Hospital

Pharmaceutical Company

Health Insurer

10Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

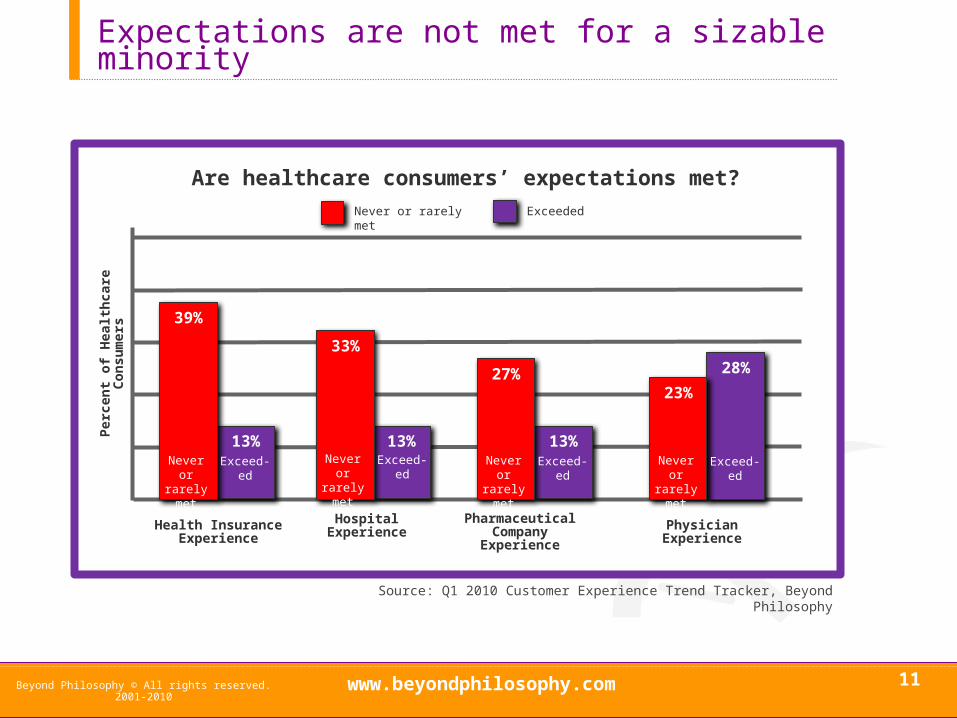

Expectations are not met for a sizable minority

11Beyond Philosophy © All rights reserved. 2001-2010

Health InsuranceExperience

Are healthcare consumers’ expectations met?

Perc

ent o

f Hea

lthca

re C

onsu

mer

s

Hospital Experience

13%

39%

Exceed-ed

13%

27%

Never or rarely met

Exceed-ed

13%

33%

Exceed-ed

Physician Experience

28%

23%

Never or rarely met

Exceed-ed

Never or rarely met

Pharmaceutical Company Experience

Never or rarely met

Source: Q1 2010 Customer Experience Trend Tracker, Beyond Philosophy

Never or rarely met Exceeded

www.beyondphilosophy.com

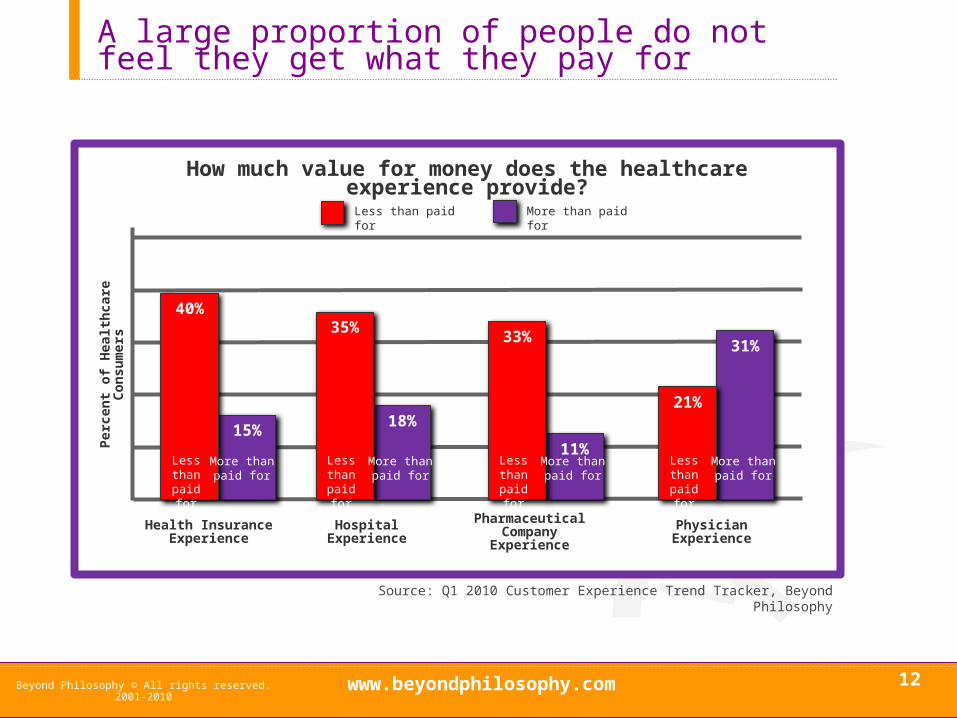

A large proportion of people do not feel they get what they pay for

12Beyond Philosophy © All rights reserved. 2001-2010

Value for money

How much value for money does the healthcare experience provide?

18%

35%

More than paid for

Less than paid

for

31%

21%

More than paid for

Less than paid

for

15%

40%

More than paid for

Less than paid

for

Health InsuranceExperience Hospital Experience Pharmaceutical

Company Experience

11%

33%

More than paid for

Less than paid

for

Physician Experience

Perc

ent o

f Hea

lthca

re C

onsu

mer

s

Source: Q1 2010 Customer Experience Trend Tracker, Beyond Philosophy

Less than paid for More than paid for

www.beyondphilosophy.com

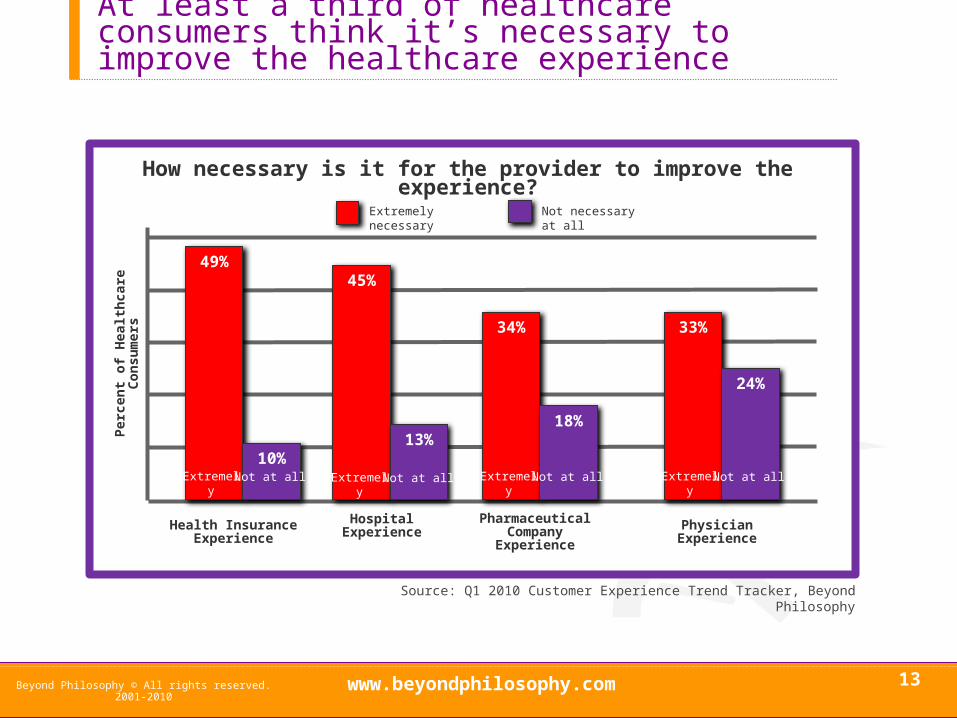

At least a third of healthcare consumers think it’s necessary to improve the healthcare experience

13Beyond Philosophy © All rights reserved. 2001-2010

Health InsuranceExperience

How necessary is it for the provider to improve the experience?

Hospital Experience Physician ExperiencePharmaceutical Company Experience

49%

10%Not at allExtremely

45%

13%

33%

24%

34%

18%

Perc

ent o

f Hea

lthca

re C

onsu

mer

s

Source: Q1 2010 Customer Experience Trend Tracker, Beyond Philosophy

Extremely necessary Not necessary at all

Not at allExtremely Not at allExtremely Not at allExtremely

www.beyondphilosophy.com

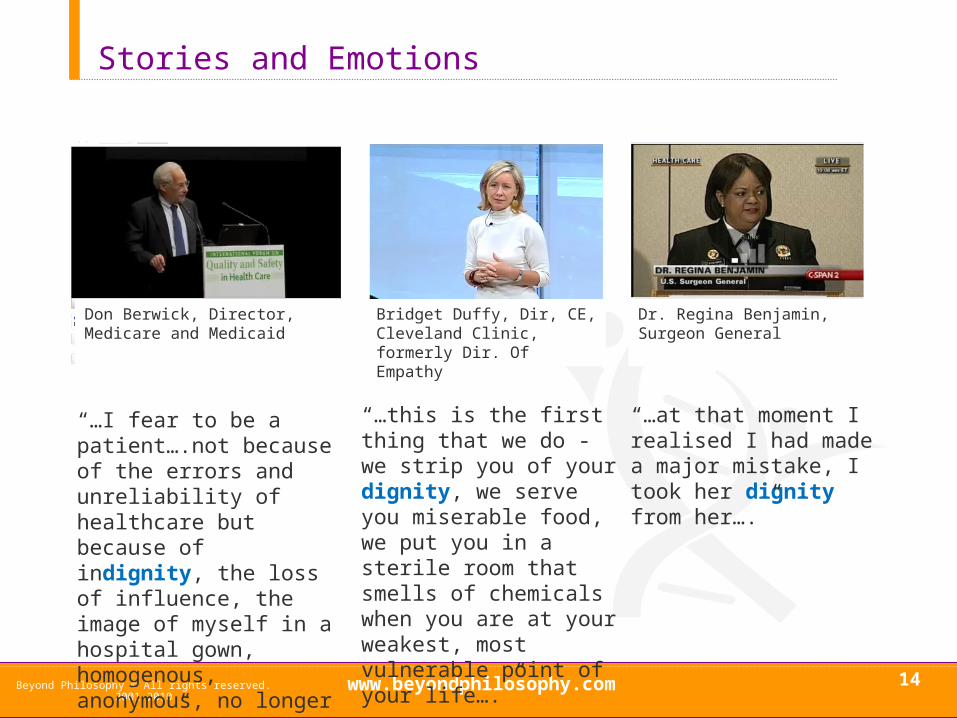

Stories and Emotions

14Beyond Philosophy © All rights reserved. 2001-2010

“…I fear to be a patient….not because of the errors and unreliability of healthcare but because of indignity, the loss of influence, the image of myself in a hospital gown, homogenous, anonymous, no longer myself…”

“…this is the first thing that we do - we strip you of your dignity, we serve you miserable food, we put you in a sterile room that smells of chemicals when you are at your weakest, most vulnerable point of your life….”

“…at that moment I realised I had made a major mistake, I took her dignity from her….”

Don Berwick, Director, Medicare and Medicaid

Bridget Duffy, Dir, CE, Cleveland Clinic, formerly Dir. Of Empathy

Dr. Regina Benjamin, Surgeon General

www.beyondphilosophy.com

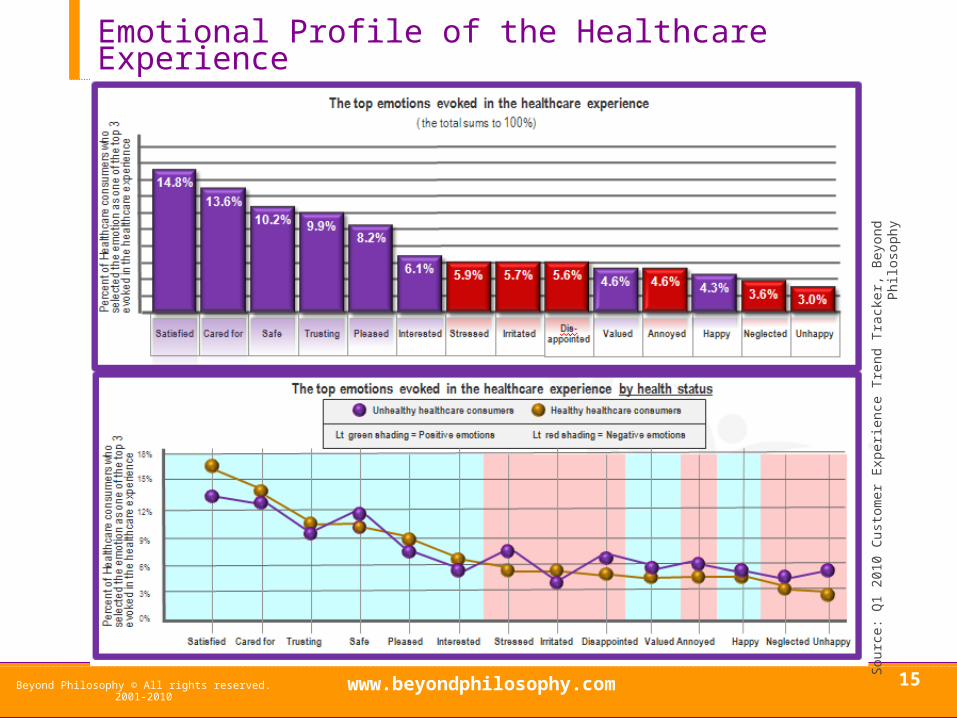

Emotional Profile of the Healthcare Experience

15

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

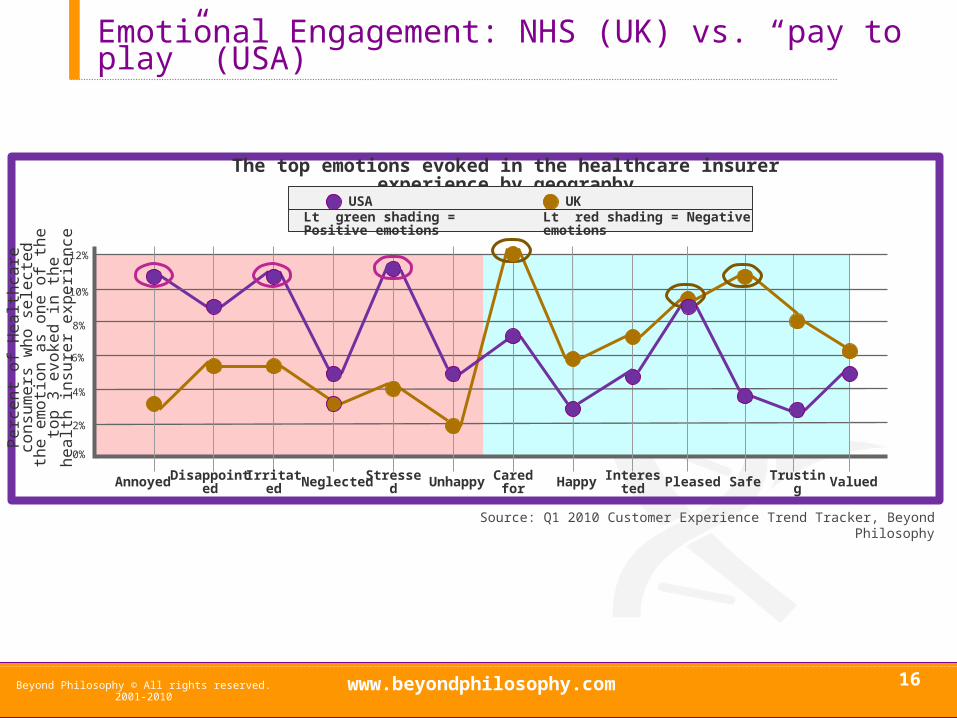

Emotional Engagement: NHS (UK) vs. “pay to play” (USA)

16

2%

6%

8%

The top emotions evoked in the healthcare insurer experience by geography

10%

0%

12%

USA UK

Cared for TrustingSafePleasedInterestedStressedIrritatedDisappointed ValuedAnnoyed HappyNeglected Unhappy

4%

Perc

ent o

f Hea

lthca

re c

onsu

mer

s wh

o se

lect

ed th

e em

otio

n as

one

of t

he to

p 3

evok

ed in

the

heal

th in

sure

r exp

erie

nce

Lt green shading = Positive emotions Lt red shading = Negative emotions

Source: Q1 2010 Customer Experience Trend Tracker, Beyond Philosophy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Solutions: Patient Centred Care has the Momentum

17

Point of Care“..aims to transform patients’ experience of care in hospital. The goal of the programme is to enable health care staff in hospitals to deliver the quality of care they would want for themselves and their own families.”

Medical Homes “…an approach to providing comprehensive primary care... that facilitates partnerships between individual patients, and their personal providers, and when appropriate, the patient’s family."

Planetree Model“…a patient-centered, holistic approach to healthcare, promoting mental, emotional, spiritual, social, and physical healing. It empowers patients and families through the exchange of information and encourages healing partnerships with caregivers. It seeks to maximize positive healthcare outcomes by integrating optimal medical therapies and incorporating art and nature into the healing environment.”

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

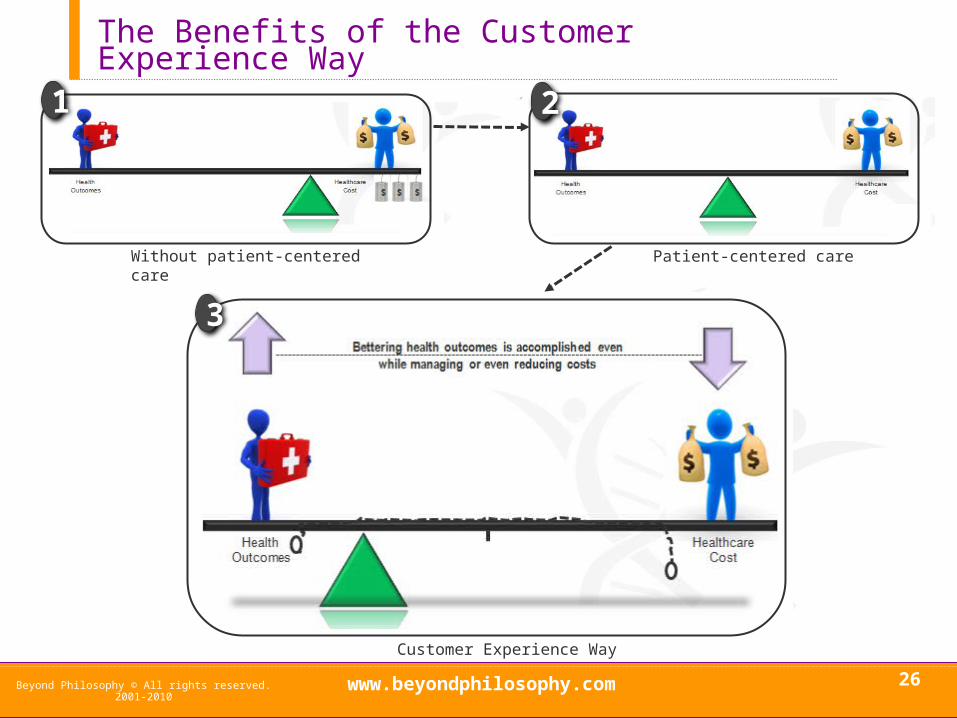

The Benefits from Patient-Centered Care

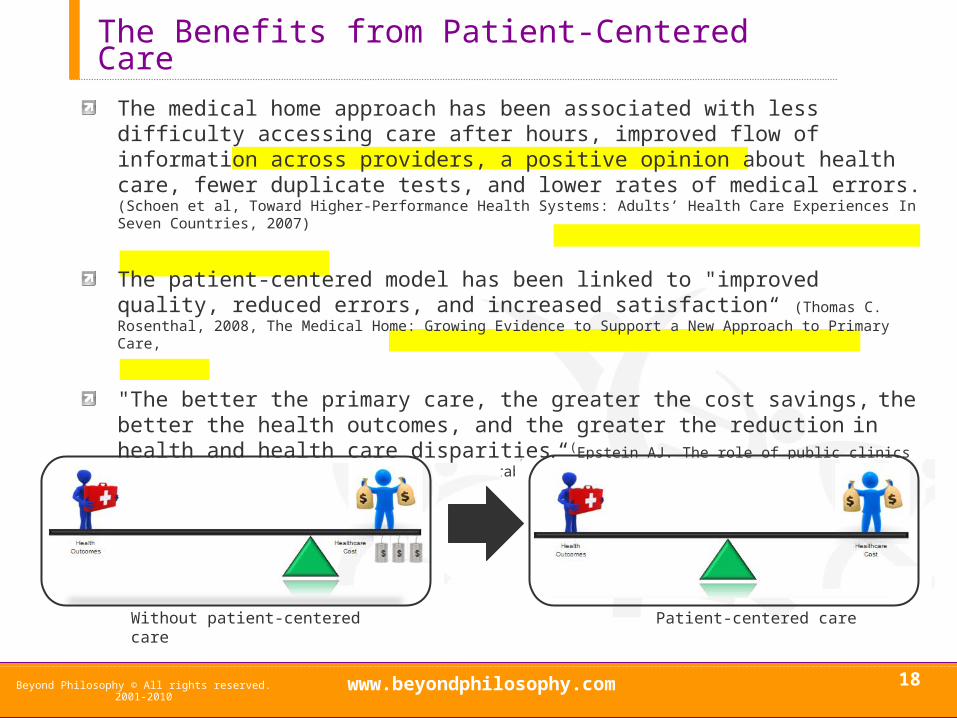

The medical home approach has been associated with less difficulty accessing care after hours, improved flow of information across providers, a positive opinion about health care, fewer duplicate tests, and lower rates of medical errors. (Schoen et al, Toward Higher-Performance Health Systems: Adults’ Health Care Experiences In Seven Countries, 2007)

The patient-centered model has been linked to "improved quality, reduced errors, and increased satisfaction“ (Thomas C. Rosenthal, 2008, The Medical Home: Growing Evidence to Support a New Approach to Primary Care,

"The better the primary care, the greater the cost savings, the better the health outcomes, and the greater the reduction in health and health care disparities.“(Epstein AJ. The role of public clinics in preventable hospitalizations among vulnerable populations. Health Serv Res 2001; 36: 405–20)

18Beyond Philosophy © All rights reserved. 2001-2010

Without patient-centered care Patient-centered care

www.beyondphilosophy.com

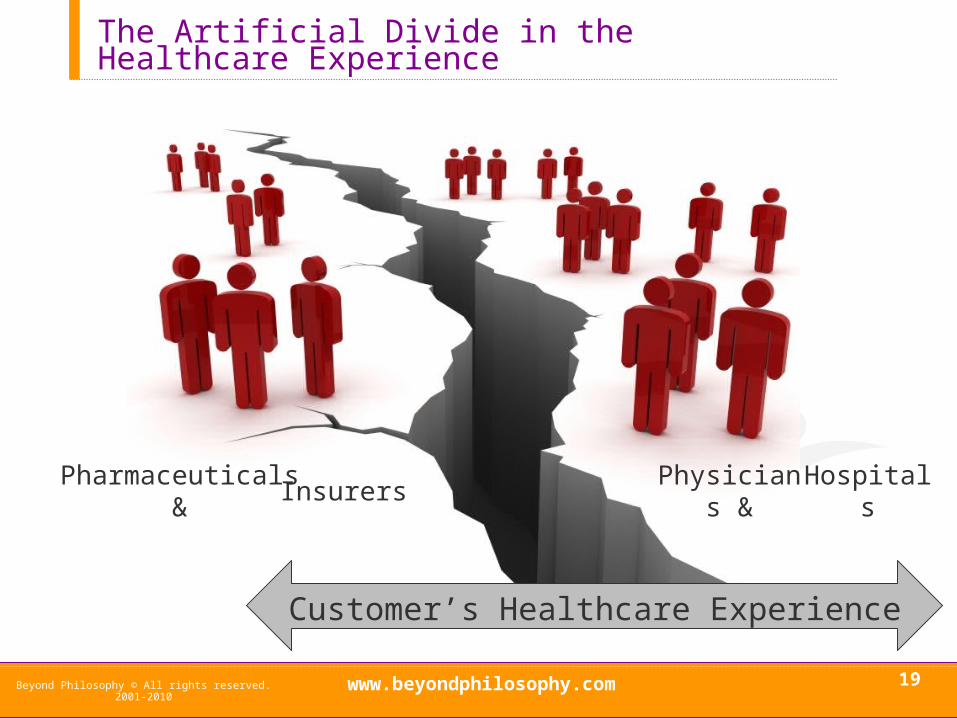

The Artificial Divide in the Healthcare Experience

19

Physicians & HospitalsPharmaceuticals & Insurers

Customer’s Healthcare Experience

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Poll Question

20

Shar

e of

role

in k

eepi

ng h

ealth

care

co

nsum

ers

heal

thy

Healthcare consumer’s perception of healthcare providers’ importance in keeping them healthy

( the total sums to 100%)

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Which provider do you think customers choose as the most important in keeping them healthy?

1. Hospital is most important

2. Physician is most important

3. Pharmaceutical Company is most important

4. Health Insurance Provider is most important

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

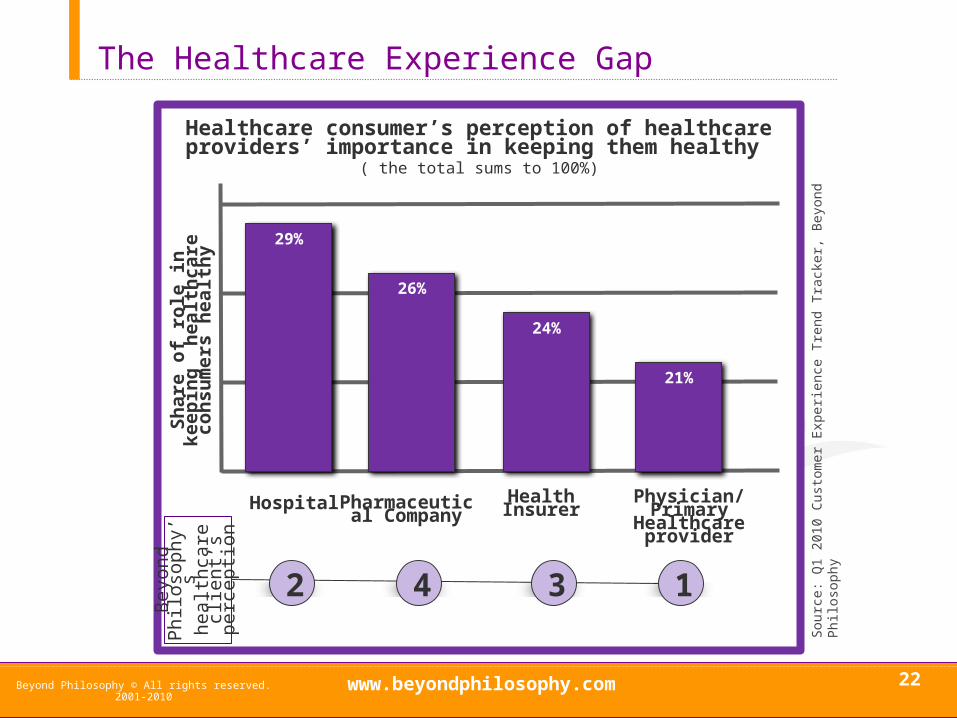

The Healthcare Experience Gap

21

Shar

e of

role

in k

eepi

ng h

ealth

care

co

nsum

ers

heal

thy

Healthcare consumer’s perception of healthcare providers’ importance in keeping them healthy

( the total sums to 100%)

Physician/ Primary Healthcare provider

Hospital Health InsurerPharmaceutical Company

1Beyo

nd

Philo

soph

y’s

heal

thca

re c

lient

’s pe

rcep

tion

342

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

The Healthcare Experience Gap

22

Shar

e of

role

in k

eepi

ng h

ealth

care

co

nsum

ers

heal

thy

Healthcare consumer’s perception of healthcare providers’ importance in keeping them healthy

( the total sums to 100%)

Physician/ Primary Healthcare provider

21%

Hospital

29%

Health Insurer

24%

Pharmaceutical Company

26%

1Beyo

nd

Philo

soph

y’s

heal

thca

re c

lient

’s pe

rcep

tion

342

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

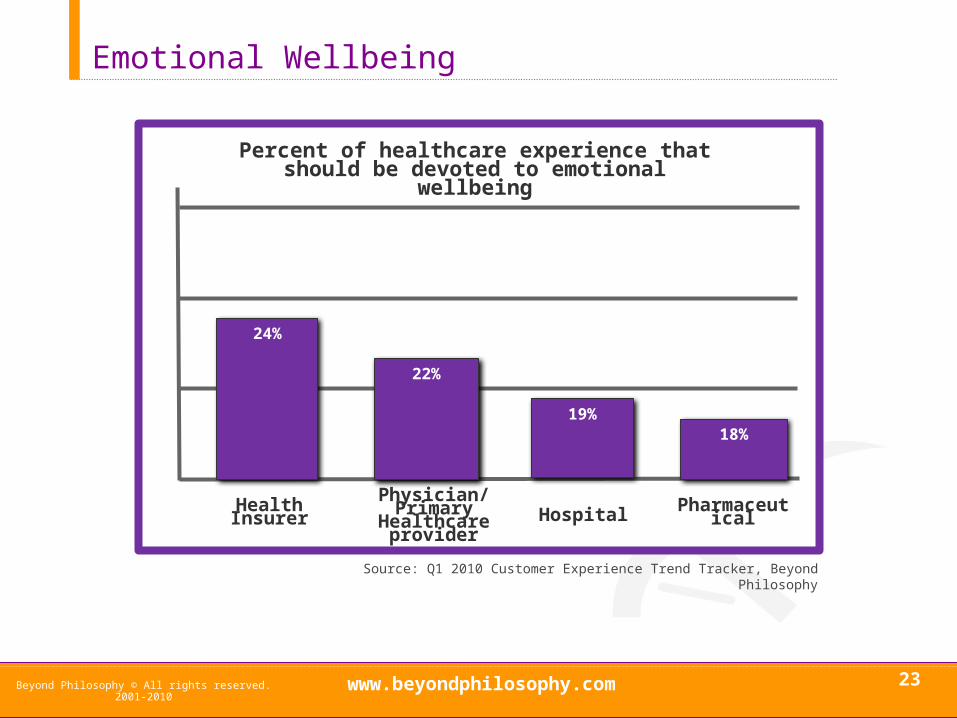

Emotional Wellbeing

23Beyond Philosophy © All rights reserved. 2001-2010

Percent of healthcare experience that should be devoted to emotional wellbeing

Hospital

19%

Pharmaceutical

18%

Physician/ Primary Healthcare provider

22%

Health Insurer

24%

Source: Q1 2010 Customer Experience Trend Tracker, Beyond Philosophy

www.beyondphilosophy.com

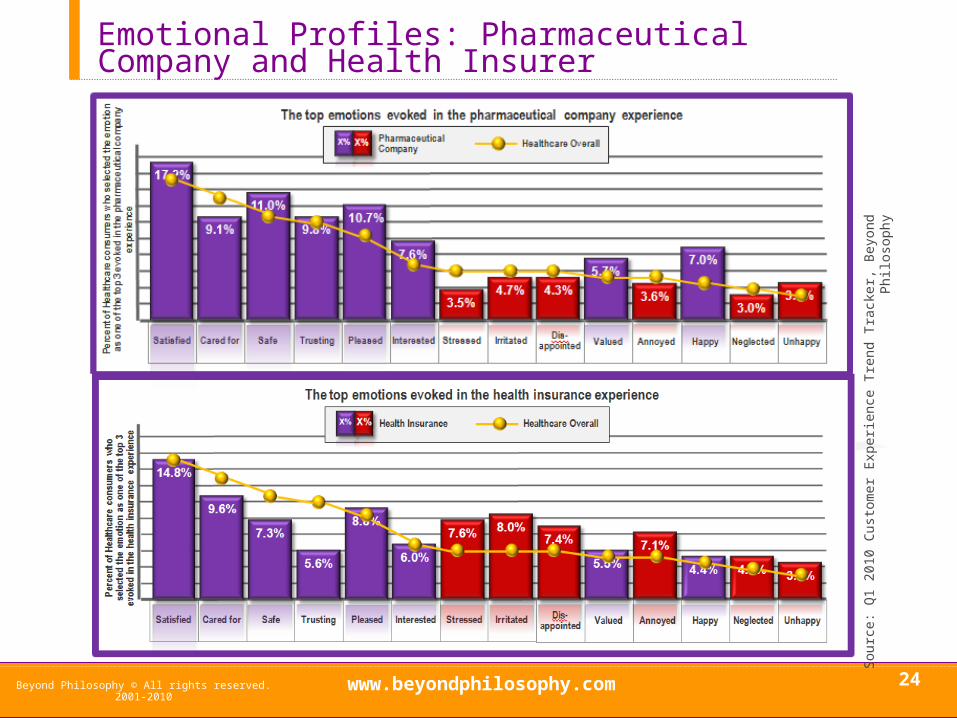

Emotional Profiles: Pharmaceutical Company and Health Insurer

24

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

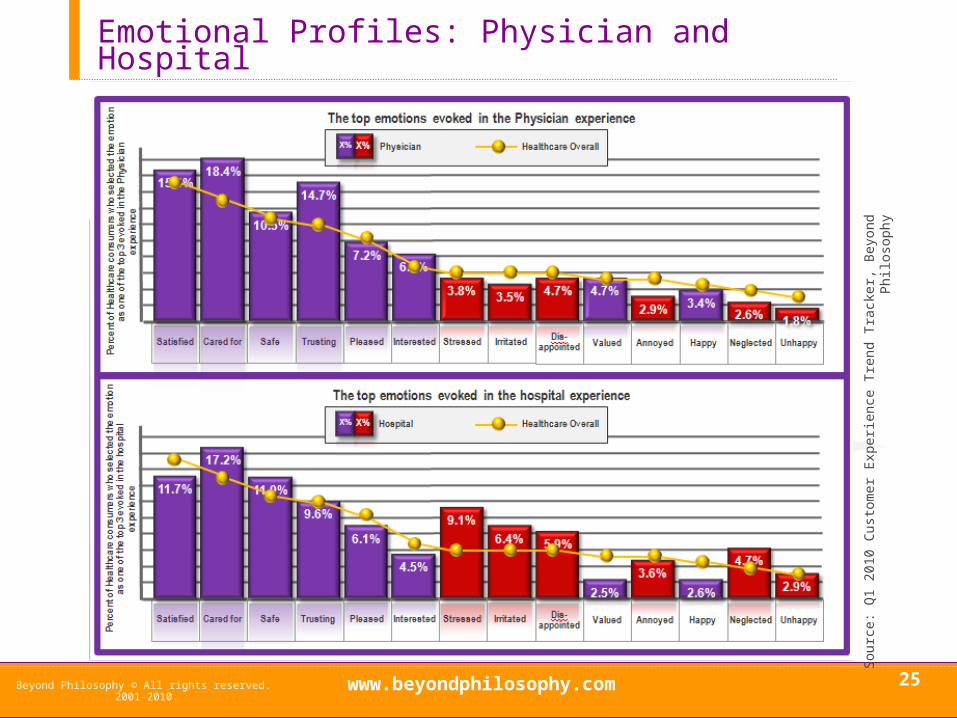

Emotional Profiles: Physician and Hospital

25

Sou

rce:

Q1

2010

Cus

tom

er E

xper

ienc

e T

rend

Tra

cker

, Bey

ond

Phi

loso

phy

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

The Benefits of the Customer Experience Way

26

Without patient-centered care Patient-centered care

Customer Experience Way

3

21

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Same as everybody else

More expensive

PRICING

Undifferentiated

Differentiated

EMOTIONAL ENGAGEMENT

Extract commodities

Stage experiences

Makegoods

Deliverservices

Source: Welcome to the Experience Economy, Pine & Gilmore, HBR, July-August 1998

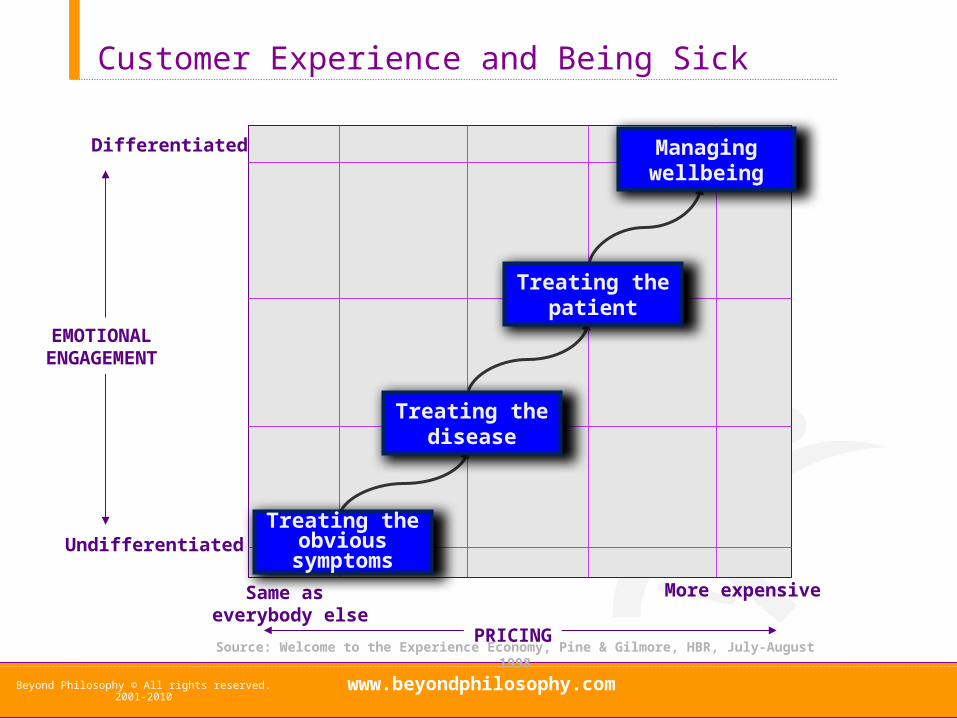

Treating the obvious

symptoms

Customer Experience and Being Sick

Treating the disease

Treating the patient

Managing wellbeing

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Ch

ron

ic I

lln

ess

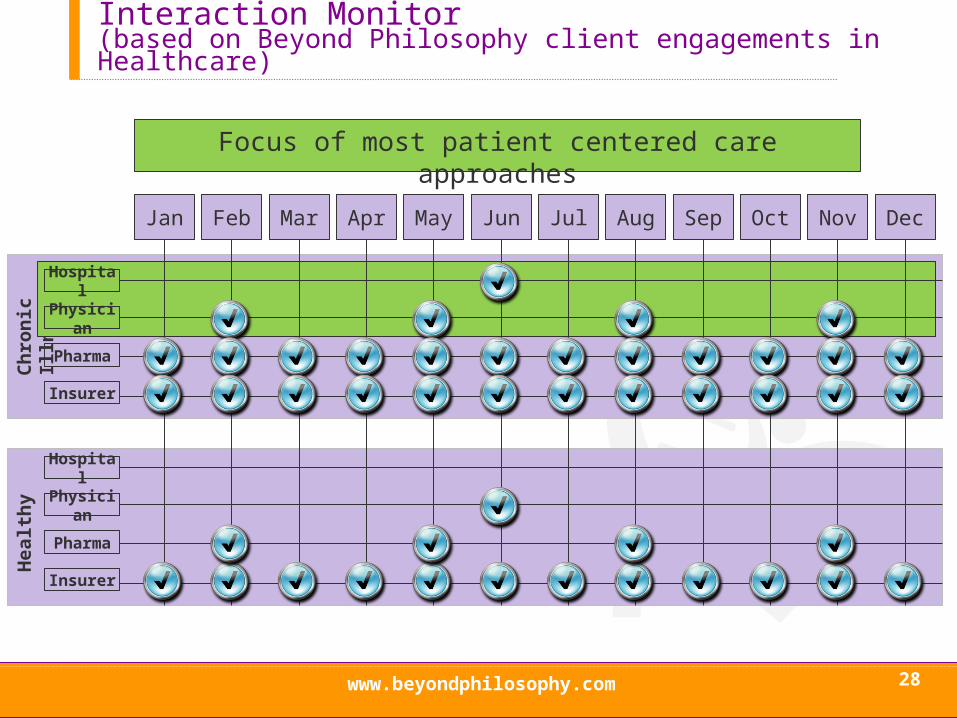

Interaction Monitor (based on Beyond Philosophy client engagements in Healthcare)

28

Jan Feb Mar Apr May Jun Jul Aug Oct Nov DecSep

Hospital

Physician

Pharma

Insurer

Hea

lth

y

Hospital

Physician

Pharma

Insurer

Focus of most patient centered care approaches

www.beyondphilosophy.com

Summary

29

Consumers experience healthcare as whole, not in discrete buckets.

Current Patient centered care solutions are based on customer experience principles but focus primarily on the patient – point of care experience (i.e. physician and hospital)

However, most of the health care experience occurs with pharmaceutical companies and health insurers providing these two sectors with untapped potential to maximize health outcomes while reducing costs.

The key to customer experience applications is an understanding of what drives emotional emotional involvement.

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Recommendations

30

Physicians• Don’t be hostile to

the outstretched hand of the pharmaceutical company and health insurers in their honest efforts to care for the patient.

Hospitals• Be conscious of

patients’ emotional needs in addition to their medical ones.

• Consider adopting the Planetree model.

Pharmaceuticals• Look to take on a

substantial role in the medical home.

• Utilize your numerous interaction points to engage customers more directly.

Health Insurers• Now that

universal coverage is coming to the US, focus on emotional engagement, track your emotional profile and use the UK as an initial benchmark.

• Approximately 15% of your budget should be devoted to improving customers’ emotional wellbeing.

• Keep track of the difference in the perception of the experience between healthy and unhealthy customers. Especially in their positive and negative emotional experiences.

• Assess the experience you actually provide with an outside-in point of view. We typically use “Customer Mirrors” for this purpose.

• Investigate and identify he root causes of the full customer experience you are delivering, making sure you uncover conscious and subconscious aspects of the experience.

Beyond Philosophy © All rights reserved. 2001-2010

www.beyondphilosophy.com

Questions?

31Beyond Philosophy © All rights reserved. 2001-2010

London Office: 0207-917-1717

Atlanta Office: 1-678-638-6162