Embed Size (px)

Citation preview

184-242-00 Rev June 2017

Home Specialty Orientation GuideCredit extended by Synchrony Bank • www.synchronybusiness.com

Home Specialty Orientation Guide

We’re delighted to help you help your

customers!

NOTE: This is for INTERNAL USE ONLY and is not to be shared with consumers for any reason.

Credit extended by Synchrony Bank • www.synchronybusiness.com

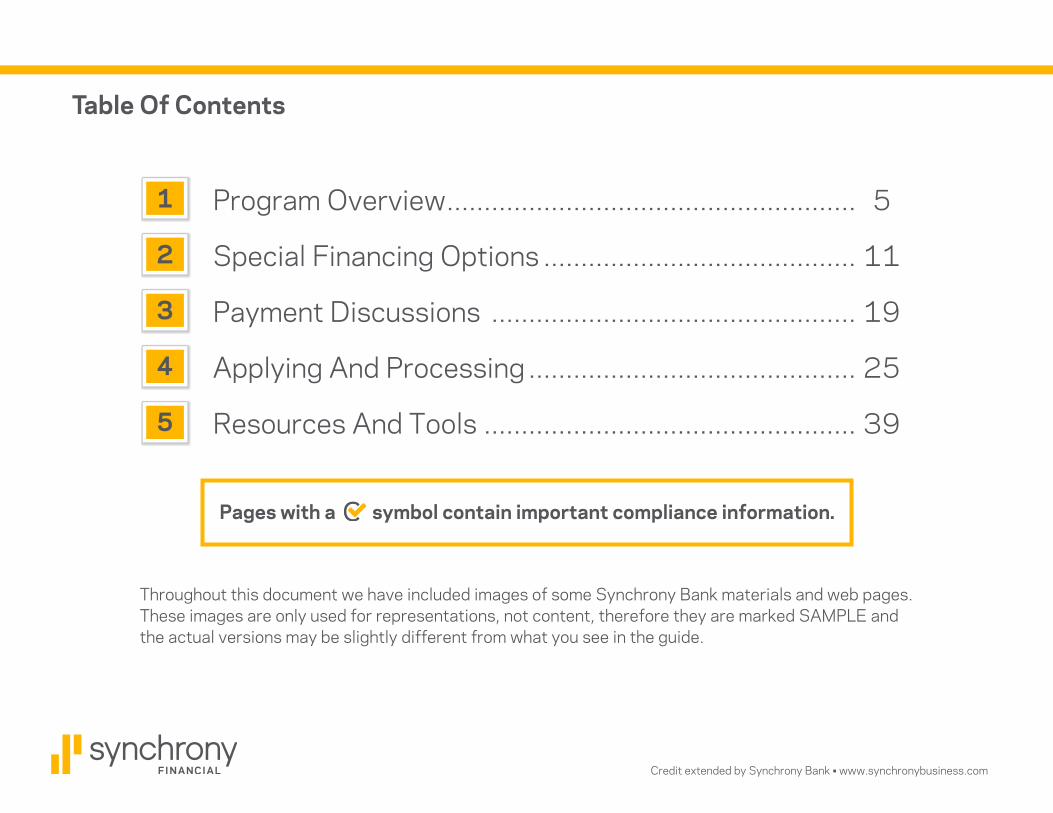

Table Of Contents

1 Program Overview ....................................................... 5

2 Special Financing Options .......................................... 11

3 Payment Discussions ................................................. 19

4 Applying And Processing ............................................ 25

5 Resources And Tools .................................................. 39

Pages with a symbol contain important compliance information.

Throughout this document we have included images of some Synchrony Bank materials and web pages. These images are only used for representations, not content, therefore they are marked SAMPLE and the actual versions may be slightly different from what you see in the guide.

This page intentionally left blank.

Home Specialty Orientation Guide – 51Credit extended by Synchrony Bank • www.synchronybusiness.com

Program Overview

Let’s introduce ourselves!

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 61Home Specialty Orientation Guide

This Is The First Step To Offering Financing Options For Your Customers.

Today I will…

■■ Review “What you need to know” about offering financing fairly and compliantly.■■ Show how to comply with applicable Federal and State regulations.■■ Get you set up and ready to introduce financing to your team and customers as part of

your sales process.■■ Demonstrate how to achieve your business goals by offering a Synchrony Bank credit

card (aka “financing”).■■ Show how financing can help your customers get what they really want or need.

Offer your customers the options they

WANT.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 71Home Specialty Orientation Guide

Program Basics

Your customer has access to special financing promotions for initial purchase and repeat purchasesPredictable budgeting plansPrivate label credit card with your business name on it Unsecured revolving credit line*

■■ Credit lines are based on consumer credit quality and estimated sale amount. There is no established credit line limit.■■ Open credit line for repeat purchases via a credit card■■ One of the lowest payment options in the industry

Simple application and funding process■■ Instant credit decisions■■ Funding generally within 24 to 48 hours of job completion

Important Notes:

■■ Applicant must own and reside at the property to be improved■■ A co-applicant should sign the Credit Application only if he/she wishes to be obligated to repay the debt. It is the customer’s

choice whether or not to have a co-applicant■■ One account per property (household) in a 60-day period■■ Synchrony Financial does not allow split ticket financing - i.e., processing a single purchase between two new separate credit

lines or two separate lenders■■ Always verify and document two forms of ID for all applicants■■ For purchases using an existing Synchrony Bank credit card account, always call Synchrony Bank for an authorization to ensure

the customer has enough available credit to complete the purchase■■ A one-time $29 Account Activation Fee will be charged at the time the first purchase posts to the cardholder’s account■■ At no cost to the Merchant or customer, cardholders may change their promotional option for up to 60 days post-funding through

Merchant request *Subject to credit approval. Proof of income may apply on loans over $25,000, depending on program. See page 35 for details.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 81Home Specialty Orientation Guide

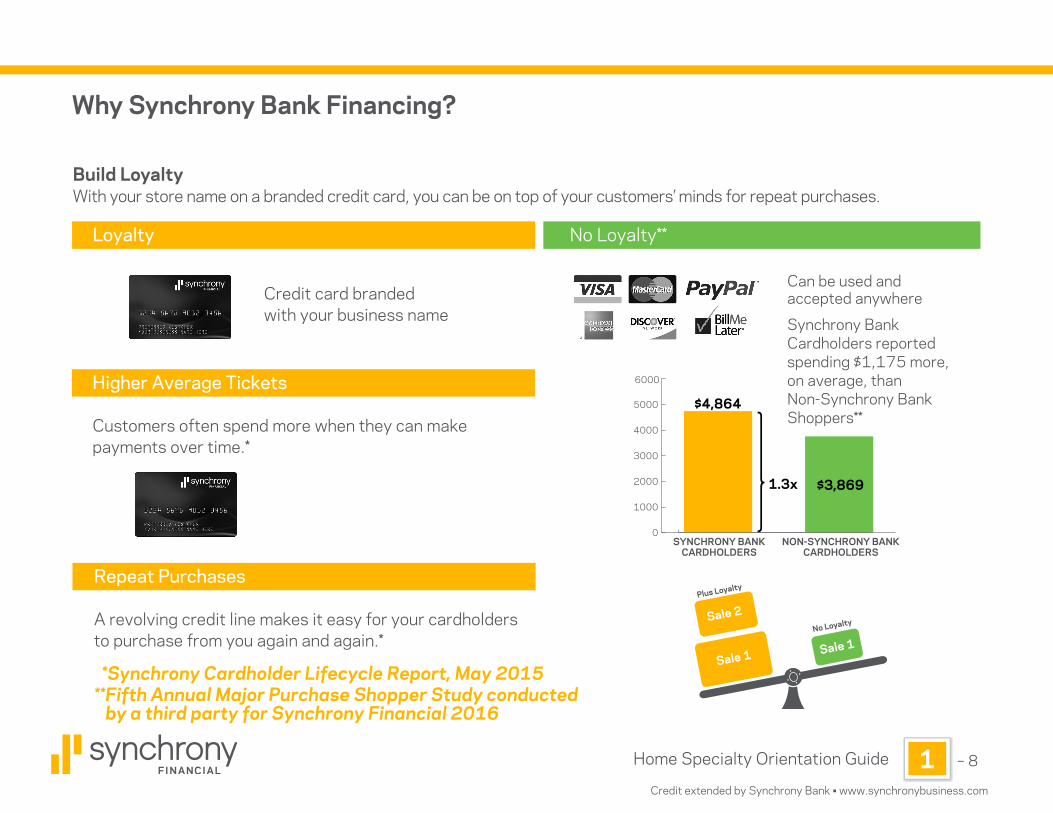

Why Synchrony Bank Financing?

Build LoyaltyWith your store name on a branded credit card, you can be on top of your customers’ minds for repeat purchases.

Loyalty No Loyalty**

Credit card branded with your business name

Can be used and accepted anywhere

Repeat Purchases A revolving credit line makes it easy for your cardholders to purchase from you again and again.*

*Synchrony Cardholder Lifecycle Report, May 2015**Fifth Annual Major Purchase Shopper Study conducted by a third party for Synchrony Financial 2016

Plus Loyalty

No Loyalty

Sale 1

Sale 2

Sale 1

Higher Average Tickets Customers often spend more when they can make payments over time.*

0

1000

2000

3000

4000

5000 $4,864

1.3x $3,869

6000

SYNCHRONY BANK CARDHOLDERS

NON-SYNCHRONY BANK CARDHOLDERS

Synchrony Bank Cardholders reported spending $1,175 more, on average, than Non-Synchrony Bank Shoppers**

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 91Home Specialty Orientation Guide

How Much Does It Cost To Get Those Results? Example:

*Synchrony Bank’s cost of credit is used for illustration purposes. Assumes no discount is offered for cash payment - Merchant offers a fixed price. Cost should be incorporated into Merchant’s General & Administrative expenses and any additional credit related surcharges or fees charged by Merchant are prohibited.

Incremental Blended Cost of Credit with Synchrony Bank Financing vs. Current Sales Mix:

1.20%

Current Sales Mix

By Payment Method*

Est. Sales Mix with Synchrony Bank Financing

By Payment Method*

Payment TypeCash/CheckCredit Card

Synchrony Bank

Total Blended Cost of Credit

% of Business25%75%0%

100%

% of Business20%50%30%

100%

Cost of Credit0.00%3.00%6.50%

3.45%

Cost of Credit0.00%3.00%0.00%

2.25%

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 101Home Specialty Orientation Guide

Who Benefits From Financing?

Your Customers Can:

Get more work done, with the products they really want, when they want it.*

Your Business Can:

Get more sales,from more customers,with more loyalty.

PLUS…With your Synchrony Bank financing program, you get payment in just 24-48 hours, and purchases are non-recourse**

Customers Benefit.You Benefit.

Everybody Wins.

Pause & Chat■■ Have you ever leveraged financing to upgrade your purchase or buy what you really wanted?■■ Would there be any reason you wouldn’t offer it, along with other payment options, to every customer?

*Subject to credit approval.**You must validate 2 forms of ID on the Credit Application for non-recourse. Subject to any chargeback rights in the Synchrony Bank Merchant Agreement and compliance with Synchrony Bank Operating Procedures.”

Home Specialty Orientation Guide – 112Credit extended by Synchrony Bank • www.synchronybusiness.com

Special Financing Options

Offering convenience and flexibility

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 122Home Specialty Orientation Guide

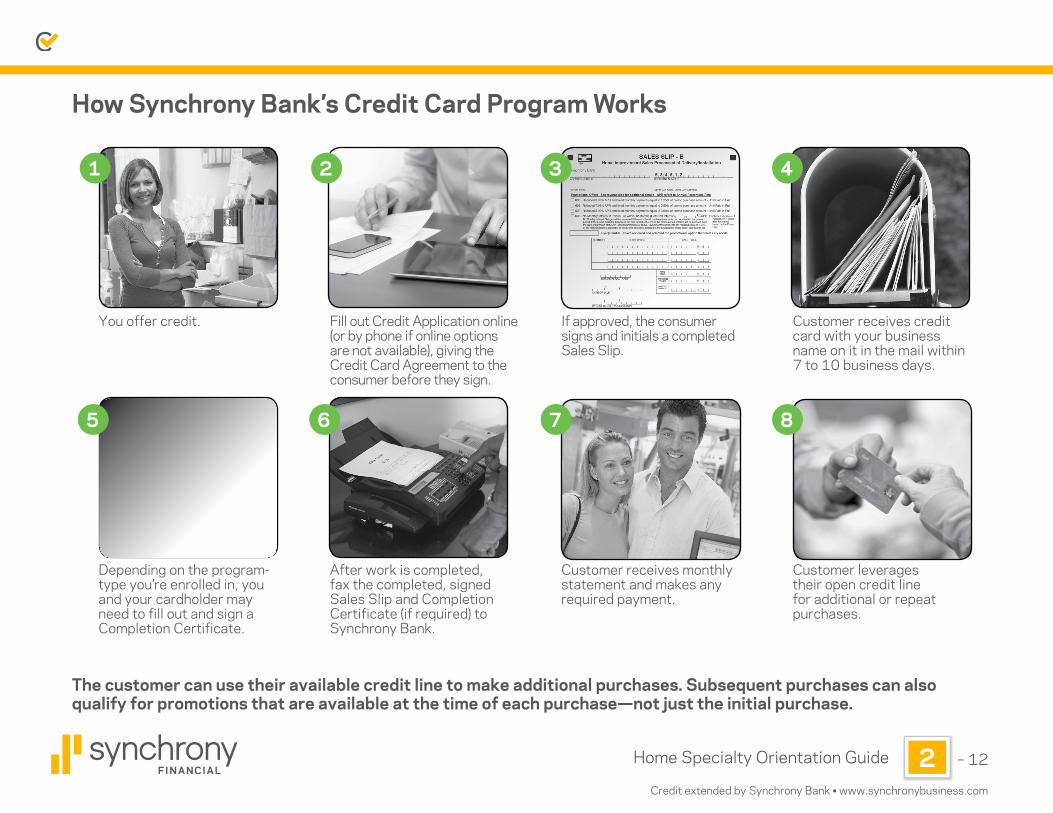

How Synchrony Bank’s Credit Card Program Works

You offer credit.

Depending on the program-type you’re enrolled in, you and your cardholder may need to fill out and sign a Completion Certificate.

Fill out Credit Application online (or by phone if online options are not available), giving the Credit Card Agreement to the consumer before they sign.

After work is completed, fax the completed, signed Sales Slip and Completion Certificate (if required) to Synchrony Bank.

If approved, the consumer signs and initials a completed Sales Slip.

Customer receives monthly statement and makes any required payment.

Customer leverages their open credit line for additional or repeat purchases.

Customer receives credit card with your business name on it in the mail within 7 to 10 business days.

1 2 3 4

6 7 8

The customer can use their available credit line to make additional purchases. Subsequent purchases can also qualify for promotions that are available at the time of each purchase—not just the initial purchase.

5

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 132Home Specialty Orientation Guide

Financing Benefits All Consumers

Cash Management Upgrades Budgeting

“I like to take advantage of special financing offers and save my on-hand cash for other things”

Business Benefit:Customer Loyalty

“I want to use financing to purchase a better product than I can get with on-hand cash”

Business Benefit:Bigger Tickets

“I need to use financing to make a purchase at this time”

Business Benefit:Close More Sales

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 142Home Specialty Orientation Guide

Simple & Easy Promotional Menus

Here’s how it works:

1. You choose one menu for your business.

See sample to the right for our most popular menus.

2. After being approved for credit, the customer selects the promotion that best meets his/ her needs from the Promotion Options menu flyer for your selected menu.

3. At the time of the sale, you fill out the Sales Slip form that is specific to the menu you are using. Note: There may be other menus depending on your program with Synchrony Financial.

Synchrony Financial offers Single-Priced and Variable-Priced Menus. See examples of both menus below.■■ Most merchants choose a Single-Priced Menu because the merchant fee for each promotion within the menu is the same,

predictable, and therefore easier to incorporate into pricing and budgets.■■ Variable-Priced Menus are available to select merchants. Variable-Priced Menus include multiple merchant fees that vary

by promotion, therefore making incorporating into pricing and budgets more complex.

Menu B - Single - Priced MenuTran Code Promotional Offer Monthly

PaymentSample

Merchant Fee

600 9.99% APR Until Paid in Full 1.250%

7.00%604 7.99% APR Until Paid in Full 2.000%

602 5.99% APR Until Paid in Full 3.000%

605 No Monthly Interest if Paid in Full within 18 Months* 2.500%

Menu M - Variable - Priced MenuTran Code Promotional Offer Monthly

PaymentSample

Merchant Fee

250 9.99% APR Until Paid in Full 1.250%

7.00%251 7.99% APR Until Paid in Full 2.000%

252 5.99% APR Until Paid in Full 3.000%

253 No Monthly Interest if Paid in Full within 18 Months* 2.500%

254 No Monthly Interest if Paid in Full within 25 Months* 4.000% 9.75%

*For new cardholders interest accrues at 26.99%. Existing cardholders should see their credit card agreement for their applicable APR. If the balance is paid in full prior to the promotional end date no interest will be charged.

One price for all offers

Differentprices onsome offers

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 152Home Specialty Orientation Guide

Financing Options Explained*

Deferred Interest:■■ Also known as “No Interest if Paid in Full”■■ Minimum monthly payments are required, which may or may not pay off the promotional purchase by the end of the

promotional period. This means in order to pay the promotion in full before the end of the promotional period, the cardholder may need to pay more than the minimum monthly payments.

■■ If monthly payments are made by their due dates and the purchase is paid in full within the promotional period, interest is not assessed on the promotional purchase.

■■ Interest accrues during the promotional period. To avoid paying the accrued interest, the entire promotional purchase balance must be paid in full by the end of the promotional period.

■■ If balance is not paid in full within the promotional period, the accrued interest is added to the balance, and the balance will continue to bill interest at the account level Annual Percentage Rate until the balance is paid in full.

No Interest:■■ Often referred to as “Equal Pay”■■ No interest is charged on the promotional purchase, regardless of the length of promotion■■ Monthly payments on promotional purchase are the same every month**

Reduced Interest:■■ Often referred to as “Fixed Pay”■■ A reduced interest rate is charged on the promotional purchase, regardless of the length of promotion■■ Monthly payments on promotional purchase are the same every month**

Payments are calculated by multiplying the loan amount by the Payment Factor, and are rounded to the next highest dollar. For example, $10,000 x 1.25% Payment Factor = $125

*Some promotions are not available on all menus. Cost should be incorporated into Merchant’s General & Administrative expenses and any additional credit related surcharges or fees charged by Merchant are prohibited. Cardholder may be charged fees for late payments.** A one-time $29 Account Activation Fee will be charged at the time the first purchase posts to the cardholder’s account.

Do you know your available promotions?

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 162Home Specialty Orientation Guide

$126 $65

$126 $65

MONTHS 1 - 11 MONTH 12

$126 $65

Flexible ways to manage payments

Repayment scenarios for the consumer $5,000 purchase

TOTAL PAID $5,029

$419

Minimum Payments + Payoff*

$126

Equal PaymentsOnly

TOTAL PAID $5,029

Deferred Interest/No Interest If Paid In Full* Options$5,000 Twelve-Month Deferred Interest/No Interest if Paid in Full* Financing Option:3 scenarios to show how the cardholders may choose to make their monthly payments.Note that the outcomes below assume that there are no other balances on the cardholder’s account.

$3,643

$4193

TOTAL PAID $11,783

($6,754 INTEREST)$126Minimum

Payments Only INTEREST ACCRUING

$651

2

OUTCOME

OUTCOMEMONTHS 1-93 MONTH 94

INTEREST ACCRUING

INTEREST ACCRUING

– 172Home Specialty Orientation Guide

Credit extended by Synchrony Bank • www.synchronybusiness.com

$200 $29

$63 $63.24 $63.65 $64.06 $64.47 $48.10

Reduced Interest Financing Options NOTES:

* All values are used for illustrative purposes only. Amounts may vary.• Payments are calculated by multiplying the loan amount by the Payment Factor (e.g., $10,000 x 1.25% pmt. factor = $125).• Fixed payments will vary during the final months when actual interest is less than the $2 minimum finance charge.• Final month payment includes $29 Account Activation Fee.

Fixed Payment Reduced Interest Until Paid in Full

TOTAL PAID $7,170.52$63 $63.24 $63.65 $64.06 $64.47 $48.10

OUTCOMEMOS. 1-109 MONTH 110 MONTH 111 MONTH 112 MONTH 113 MONTH 114

Includes principal and 7.99% interest with 1.25% payment factor.**7.99% is used here for illustrative purpose. Actual interest rate and payment factor may vary.

No Interest Financing OptionEquity Payment No Interest

TOTAL PAID $5,029$200 $29

OUTCOMEMOS. 1-25 MONTH 25

• No interest is often referred to as “Equal Pay”• Reduced interest is often referred to as “Fixed Pay”• Cardholder may be charged fees for late payments• Fixed/Equal monthly payments of principal and interest required until paid in full.• Fixed/Equal monthly payments based on a payment factor for the number of months in the promotional period.

184-277-00 (7/16)Credit extended by Synchrony Bank

This page intentionally left blank.

Home Specialty Orientation Guide – 193Credit extended by Synchrony Bank • www.synchronybusiness.com

Payment Discussions

They’re easy with Synchrony Bank

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 203Home Specialty Orientation Guide

Be Clear and Transparent

■■ Use Synchrony Bank training materials

■■ Utilize compliant program materials

■■ Let the customer choose the promotion that works best for them

Guiding Principles

Present financing…

■■ to every customer

■■ every time

■■ early in the sales process

Start by listening to your customer’s needs and wants

Typical Customer Conversation Steps

Mention your financing

promotions and offerings when

setting the appointment and early in the initial

sales consultation

1 2 3Break purchases

down into monthly payments when the customer

is considering the scope of the project

Present the menu of financing

options, allowing the customer to choose the promotion that

works best for them

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 213Home Specialty Orientation Guide

Customer Discussion Examples

■■ Tell me about how and when you discuss price today?

■■ How will you incorporate financing into your price discussions moving forward to make sure all customers are aware of their options?

At the beginning of the sales conversation“Thank you for taking the time to meet with me today. In case you weren’t already aware, we have some great special financing promotions that we can talk through when the time comes*. Let’s talk about what you’re looking to get done.”

When the customer is selecting a product or service“As I mentioned before, we have some great special financing promotions available to you*. Would you like to talk through your options and see how much your monthly payments would be, and other key details?”

When the customer has decided on the project scope“I’d like to walk through some special financing options with you. We offer Synchrony Bank credit card financing. I can help you with a quick application, and if it is approved, you can use your account immediately so you can take advantage of paying it off over time. Would you like to go ahead and submit an application?”

Customers can purchase today and

pay over time*

*Subject to credit approval for a Synchrony Bank credit card.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 223Home Specialty Orientation Guide

Responding To Customer Hesitations

My credit isn’t great.“I understand. I’ll be happy to process an application for you to see if it may be approved. We also offer the option of applying with a co-applicant.”

I’m worried about how my personal information might be used.“I can understand your concern about personal information; that is something that we take very seriously. We process applications all the time and we make every effort to keep your information secure to keep you protected.”

I don’t want another credit card.“I understand. Other competing general utility bank cards may offer special promotions periodically; however, our card features special promotional financing on an ongoing basis for qualifying purchases. Additionally, having a dedicated credit card for special purchases leaves your other bank cards available for emergencies and day to day needs.”

Focus on the benefits of paying

over time

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 233Home Specialty Orientation Guide

Synchrony Bank provides you with a variety of promotional financing offers designed to fit specific financial needs. The promotional options available to you are listed below. For additional disclosure information, please see the reverse side.

Promotion Options

Reduced APR with Fixed Payments promotional options are great choices if you are looking for a lower APR with predetermined payments to allow you to fit the purchase into your budget. Synchrony Bank offers your contractor three of these promotional financing options to best fit your needs

Save your cash by deferring interest during the promotional period. The Deferred Interest promotional option is a great choice if you will have funds to pay the balance in full by the end of the promotional period.

Plan 600

Plan 605

Plan 604

Plan 602

Reduced 9.99% APR and fixed monthly payments equal to 1.25% of promo purchase amount – Until Paid in Full 1

On purchases with your Synchrony Bank credit card. $29 account activation fee may apply. Estimated payoff period 132 months. See reverse side for additional information.

No Monthly Interest if Paid in Full Within 18 Months (Deferred Interest) 4

On purchases with your Synchrony Bank credit card. Monthly interest will be charged to your account from the purchase date if the promotional purchase is not paid in full within 18 months. $29 account activation fee may apply. Fixed monthly payments are required equal to 2.50% of the highest balance applicable to this promo purchase until paid in full. See reverse side for additional information.

Reduced 7.99% APR and fixed monthly payments equal to 2.00% of promo purchase amount – Until Paid in Full 2

On purchases with your Synchrony Bank credit card. $29 account activation fee may apply. Estimated payoff period 61 months. See reverse side for additional information.

Reduced 5.99% APR and fixed monthly payments equal to 3.00% of promo purchase amount – Until Paid in Full 3

On purchases with your Synchrony Bank credit card. $29 account activation fee may apply. Estimated payoff period 37 months. See reverse side for additional information.

Credit is extended by Synchrony Bank. Menu B

600-503-00 (02/17)

600-503-00_HI_Menu_B_v4ms_FINAL.indd 1 7/3/14 1:56 PM

Promotion Options Menu Flyer

This tool allows you to show your customers a more detailed description of what special financing promotions are available to them:

■■ Customizable, with your logo at the top■■ Space for your salespeople to fill in monthly payments■■ Gives your customers peace of mind by letting them

choose the special financing promotion that best meets their needs

■■ Available for all menu options

Contact your Synchrony Financial representative for assistance with adding your logo to this form.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 243Home Specialty Orientation Guide

Cardholder Statement

Understanding your cardholder statement

The first statement that your customers receive will also include an insert titled, “How to read your new statement.” A sample statement is on this page. If you have any questions about the statement, please contact your Synchrony Bank representative or visit Business Center online.

Payment Coupon Customer returns this with payment.

Look here for payment due date, minimum payment due, and new balance. Customers can also use this to update us with address changes.

Customer Service Information Information is provided on how to

reach us for mailing or submitting correspondence and payments online.

Account Information Information on the account number,

payment due date, amount past due, and over-limit amount are included here. The Minimum Payment Due is the amount that a customer must pay during the billing period. The Suggested Payment is the Minimum Payment Due plus any accrued finance charges and cardholder fees.

4. Balance Summary This section provides information on

previous balance, new purchases, payments, and more.

5. Account Activity Provided here is a chronological listing

of purchases and other transactions for the current billing period.

6. Promotional Purchase Summary Information is provided on all current

promotional purchases. Purchase amount, purchase type, finance charges, and current balance on promotions will be provided here.

7. Finance Charge Summary Interest rates and finance charges that

apply to portions of the customer’s account balance.

8. Cardholder news Information on customer account,

payment status, and special messages.

1

1 4

5

6

7

8

2

3

23

4

5

6

7

8

Home Specialty Orientation Guide – 254Credit extended by Synchrony Bank • www.synchronybusiness.com

Applying And Processing

Here are thenuts and bolts!

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 264Home Specialty Orientation Guide

A Simple Four-Step Process

CompleteApplication

1 2 3CompleteSales Slip

Obtain CompletionCertificate

(if required)

Before work begins Prior to funding After work is completed

4Submit

for Funding

Two Primary Methods to Apply and Process

PaperProcess

Online digital process paper and fax based

OR

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 274Home Specialty Orientation Guide

Synchrony Transact-Online Process

Synchrony Transact is a user-friendly online platform that supports the financingprocess end to end—from consumer application to contractor payment.

■■ Synchrony Transact is the preferred process and it follows much of the same steps as the paper process

■■ Visit bcpos.mysynchrony.com■■ Contact your Synchrony Financial sales representative or

call 877-891-9803

Synchrony Transact the following:

Apply for Credit Sales Slip Help customers apply for a credit card Complete transaction details

Payment Estimator My Transactions Review estimated monthly payments Manage your sales pipeline with customers, and view promotional and more financing options

Please refer to the “Synchrony Transact Overview and User Guide” for more in-depth detail.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 284Home Specialty Orientation Guide

How To Submit A Credit Application

Online (preferred) via our mobile app.To set up your business with the Mobile App, go to https://businesscenter.mysynchrony.com/HomeImprovement/home.do (URL is case-sensitive).

Online via Business Center at www.synchronybusiness.com

By phone: 888-222-2176

Phone hours: Monday through Saturday, 8:00am-11:00pm EST Sunday, 11:00am-9:00pm ESTPhone Express Processing (PEP) available 24X7

NOTE: Phone numbers can be found at the top of the printed Credit Application.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 294Home Specialty Orientation Guide

A Simple Four Step Paper Process: Step 1.

Complete Application1

Paper (Phone) 1. Fill out business and purchase information. Note: Leave Account # blank prior to submission. You will fill this in after an

application is submitted and approved. Credit Card Agreement disclosures are included on the form. • For hearing and speech impaired applicants with no home phone number submit the application to 888-222-2176.

2. Refer the customer to the Credit Card Agreement portion of the application for their review prior to completing and signing the application.

3. Verify and record primary and secondary ID for all applicants. 4. The applicant (and co-applicant, if desired) fills out the middle section with their contact information and income details.

Note: They must use the monthly net (after-tax) income. 5. Obtain applicant signature(s) and dates. 6. Submit:

• Phone in application to 888-222-2176. 7. Retain signed application in a secure location for at least 25 months.

When phoning in applications, you have two options: • For no hold times and fast processing, use Phone Express Process (PEP), available 24/7 OR • Speak to a client services representative.

Business Center 1. Give the applicant(s) the paper Credit Card Agreement disclosures. 2. Collect information verbally from applicant (and co-applicant, if desired) interview-style, or the customer can fill out a paper

application that you then enter into Business Center. 3. Verify and record primary and secondary ID for all applicants. 4. After all information is entered, click Print Application. 5. Keep the first page and give the rest of the pages to the customer. Those pages contain the account Credit Card Agreement. 6. Obtain the customer’s signature on the first page. 7. Click the box on-screen to confirm that the customer has signed and dated the printed application. 8. Click Submit. 9. Retain signed application in a secure location for no less than 25 months. See your Card Acceptance Agreement for additional

retention requirements.

Synchrony Bank provides gray areasMerchant completes gold areas

Customer completes green areas

52

4

3

1

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 304Home Specialty Orientation Guide

Validating Customer’s Identity

■■ At the time of application, you must verify and record two forms of identification. At least one of them must be “Primary.” See below for definitions of primary and secondary identification.

■■ On occasion, an application may be chosen by Synchrony Bank for a fraud review to protect both you and your customers. When needed, you may be asked to call Synchrony Bank and put the customer on the phone, or the customer may be asked to respond to a passcode message on their home or mobile phone after the application is submitted.

Valid Identification for Financing Applications

■■ Primary - State or government issued non-expired IDs (Driver’s License, State ID, Passport, Military ID, or Resident/Alien Green Card). Note: When using a passport, use state of residence. When using a military ID, the expiration is the date on the top right.

■■ Secondary - Major credit and debit cards (VISA, MasterCard, American Express, Discover), department store cards, or gas cards with the customer’s name and an expiration date on them (non-expired). Note: Synchrony Bank does not require or advocate the photocopying of customer identification.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 314Home Specialty Orientation Guide

Step 2: Complete Sales Slip

1. Account and Merchant Number • Fill in account number and Merchant number.

2. Buyer’s Information • Complete buyer’s name and Merchant’s name/ address.

3. Financing Options • Check the “Promotional Offer” that corresponds to the financing option that

the customer has selected. • For Deferred Interest/No Interest if Paid in Full promo, fill in the cardholder Annual Percentage Rate (APR). The APR is given when you obtain an authorization code. • Customer must initial that they have reviewed and selected a promotion.

4. Quantity/Description/Sale Price • Complete description - product category, brand, and model number.

• Enter sale price, total payments (if any), and amount financed.

5. Authorization Code • Write in authorization code (You should request this code at time of approval or call merchant services prior to funding to obtain it). • Write in the date of sale.

6. Buyer’s Signature* • Customer must sign. Only one signature is required on joint applications. • Give customer’s copy to the customer once signed.

• Retain signed Sales Slip in a secure location for no less than 25 months. See your Card Acceptance Agreement for additional retention requirements.

Complete Sales Slip2

Synchrony Bank provides gray areasMerchant completes gold areas

Customer completes green areas

6

4

5

1

2

3

*If no Completion Certificate is required for your program, follow the Funding Process on page 33 upon completion of the job.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 324Home Specialty Orientation Guide

Example: Unacceptable FeeTo ensure that you are operating within the terms of the Card Acceptance Agreement for Participating Merchants (“Merchant Agreement”) between you and Synchrony Bank, Synchrony Bank reminds you that fees may NOT be charged to consumers when applying for credit. The price offered to consumers must not separately designate the cost of credit from your regular price. This includes references to application fees, processing fees, surcharges, up charges, price increases or other special charges. For example, you cannot state that the regular price includes a “processing fee,” “bank fee,” or similar charge when presenting on estimate to a consumer.

We recommend that you treat the cost of promotional credit as overhead within your General and Administrative expenses that is included on all sales. This will enable you to create fair and transparent consumer experience. If you would like to learn more about this topic go to toolbox.mysynchrony.com and review the Cost of Credit Calculator.

Adding surcharges to your regular price for the purpose of covering financing charges is prohibited by the Merchant Agreement. If any provision of the Merchant Agreement is violated, Synchrony Bank may enforce and pursue all available remedies, including but not limited to, termination of the Merchant Agreement and indemnification for any and all liabilities incurred by Synchrony Bank (including the costs to refund any and all fees charged to consumers to apply for or use a Synchrony Bank card account).

Thank you in advance for your continued adherence to these policies and for ensuring a fair and transparent customer experience. If you have any questions, please reference the Merchant Agreement or call your Synchrony Bank representative.

IMPORTANT REMINDER: Charging Fees To Apply For Or Use Synchrony Bank Accounts

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 334Home Specialty Orientation Guide

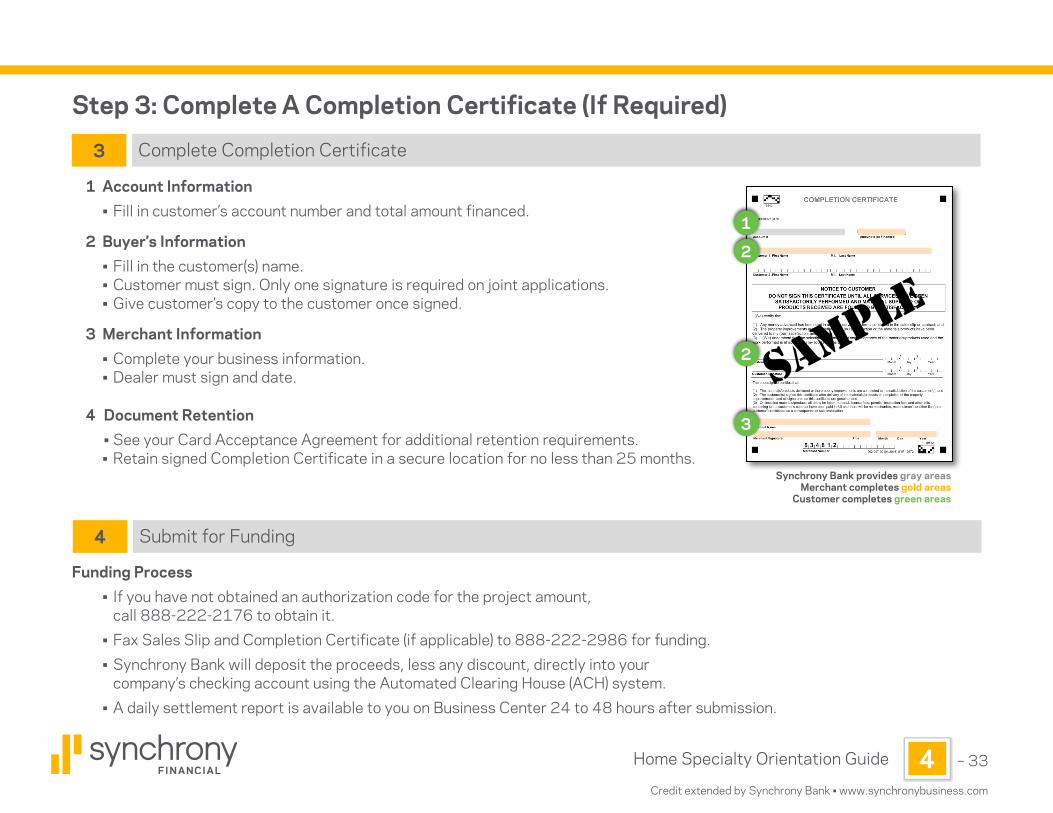

Step 3: Complete A Completion Certificate (If Required)

1 Account Information • Fill in customer’s account number and total amount financed.

2 Buyer’s Information • Fill in the customer(s) name. • Customer must sign. Only one signature is required on joint applications. • Give customer’s copy to the customer once signed.

3 Merchant Information • Complete your business information. • Dealer must sign and date.

4 Document Retention • See your Card Acceptance Agreement for additional retention requirements.

• Retain signed Completion Certificate in a secure location for no less than 25 months.

Funding Process • If you have not obtained an authorization code for the project amount,

call 888-222-2176 to obtain it. • Fax Sales Slip and Completion Certificate (if applicable) to 888-222-2986 for funding. • Synchrony Bank will deposit the proceeds, less any discount, directly into your

company’s checking account using the Automated Clearing House (ACH) system. • A daily settlement report is available to you on Business Center 24 to 48 hours after submission.

Complete Completion Certificate3

Synchrony Bank provides gray areasMerchant completes gold areas

Customer completes green areas

2

1

2

3

Submit for Funding4

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 344Home Specialty Orientation Guide

■■ When submitting customer Credit Applications, a signature is required and the customer must be given a copy of the Credit Card Agreement prior to submission.

■■ Two forms of ID, one primary and one secondary, must be presented by the customer at the time of application.Photocopies are not acceptable, and it is recommended that you not make photocopies of primary or secondary IDs.

■■ Regardless of which method you use for applying, all Synchrony documents must be retained in a secure location for 25 months (actual time period may be longer if specified in your Card Acceptance Agreement).

■■ Cardholder must sign a Sales Slip and Completion Certificate (if required) and receive a copy for all transactions.■■ Be sure to always use current versions of applications and other documents. Updated versions can be found on

Business Center (www.synchronybusiness.com) under Resources – Program Documents. You can also order pre-printed forms free of charge in Business Center under Resources – Order Supplies.

Things To Remember

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 354Home Specialty Orientation Guide

Application Outcomes

Approved

“I’m happy to tell you that your application has been approved.”

Pending

“The application came back ‘Pending,’ which simply means they need to clarify some information. Let’s give them a call to see what they need.”

Note: You must call 888-222-2176 on a pending application within 24 hours or it will be automatically denied.

Declined

“Unfortunately, Synchrony Bank wasn’t able to extend credit to you at this time. You will receive a letter within 30 days indicating the specific reasons for the decision.”

What to say aboutthe decision

■■ If approved, the applicant and joint applicant (if applicable) can immediately use account for initial purchase and can expect to receive a credit card in the mail in 7-10 business days for future purchases.

■■ Proof of income may apply on loans over $25,000, depending on program. If proof of income is required, the approved loan amount will be $25,100. Contact Synchrony Bank for additional instructions.

Declined ApplicationsHow you handle a declined Credit Application makes a difference.

Be positive. Say, “Let’s see what we can do.”

1. Double-check the Credit Application detail for accuracy.

2. Present the option of reapplying with a joint applicant. 3. Suggest other payment options, such as cash,

check, or credit card. 4. Remind them that they will receive a letter

within 30 days indicating the specific reasons for the decision.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 364Home Specialty Orientation Guide

1. You will ensure that training on how to offer, process and transact with the Synchrony Bank Program is integrated into your existing associate training program. Helpful training materials including videos, self-paced courses and pre-recorded webinars can be found online at Synchrony Financial’s Learning Center: https://learn.synchronybusiness.com.

2. Your customers must receive the Credit Card Agreement in writing and have the opportunity to review it and other disclosures in the application brochure before signing an application.

3. All Synchrony documents must be retained in a secure location for 25 months (actual time period may be longer if specified in your Card Acceptance Agreement). Failure to keep and, upon request, produce the signature page to Synchrony Bank may expose your business to an automatic chargeback upon consumer dispute.

4. Fees may not be charged to consumers for applying for credit or for using their Synchrony Bank account to finance purchases.

These fees have been called Administration Fees, Documentation Fees, Finance Fees, or other generic terms. All are prohibited by your Card Acceptance Agreement with Synchrony Bank and you will be responsible for refunding customers accordingly.

Transparency Principles : Compliance Requirements

Synchrony Bank promotes full transparency and disclosure to all applicants for its credit card program (the “Synchrony Bank Financing Program”). To assure that applicants are aware of several key attributes of the Synchrony Bank Financing Program, you hereby agree as follows:

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 374Home Specialty Orientation Guide

Transparency Principles : Compliance Requirements (Cont’d)

5. You or your staff must inform all Synchrony Bank Financing Program applicants of the following:■■ The Synchrony Bank Financing Program is a credit card and is NOT an in-house credit program. The Synchrony Financing

Program is NOT an interest-free credit card.■■ Cardholders should be provided with information about the different special financing options available to them and

how they work before requested to choose which one to use for their specific purchase. It is especially important that cardholders understand the basic features of No Interest , Reduced Interest and Deferred Interest/No Interest if Paid in Full options, if all these type of promotions are being offered. The key concepts include:• The length of the promotion• Whether the promotion expires and if so what happens upon expiration• Required payments during the promotional term

■■ For Deferred Interest promotions, deferred interest accrues on the outstanding balance during the promotional period from the date of the transaction. Finance charges can be avoided ONLY IF the promotional balance is paid off prior to the end of the promotional period.

6. You must provide the promotional terms to the customer on the completed, signed Sales Slip. 7. You will advise customers of any policy regarding returns/refunds. 8. These program guidelines are designed to provide transparency for cardholders. Synchrony Bank reserves the right to monitor

your adherence to these and other Synchrony Bank Financing Program policies subject to the consequences defined in your Card Acceptance Agreement.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 384Home Specialty Orientation Guide

Fair Lending Principles to Know Credit must be offered to all applicants fairly and consistently. Failure to do so may result in allegations of discrimination, potential violations of federal or state fair lending laws, litigation or reputational risk. All customers should be encouraged to apply for credit without regard to race, color, religion, national origin, sex, marital status, familial status, age, disability, receipt of income (in whole or in part) from public assistance programs, or an applicant’s good faith exercise of a right under the Consumer Credit Protection Act. In addition, credit-related activities must be conducted in a way that is not considered unfair, deceptive, or abusive from the customer’s perspective. Unfair activities are those that may cause unavoidable “substantial injury” (typically financial harm) to customers. Deceptive activities could include statements or omissions that mislead customers or influence their decision to buy or use a product or service. Abusive practices interfere with the customers’ ability to understand the terms and conditions of a product or service; or which take advantage of the customers’ lack of understanding or inability to protect their interests.

Clear and Accurate Communications Your advertising, signage, and conversations with customers should help them understand and make informed choices regarding your products and available financing options. Disclosures should clearly and accurately describe the terms, conditions, and any limitations associated with the purchase and the Synchrony Retail Bank relationship the customer is establishing.

Taking and Processing Applications All customers should be encouraged to complete and submit applications for credit . Do not discourage anyone from submitting an application, either through oral statements, body language, delays or discourtesy. Also, make certain that employees provide a consistent level of service in responding to questions from customers about the availability of credit and/or completing the application.

Completing the Credit Application The credit application and Credit Card Agreement must be provided to customers before they apply. It is the customer’s choice to have a joint applicant , but it is not required that a joint applicant be a spouse. Alimony, child support or separate maintenance payments do not need to be disclosed unless the customer wants this income to be considered.

Pricing and Fees No fees related to the application process or Synchrony Retail Bank financing are allowed, and the pricing of credit approved for customers cannot be changed from what Synchrony Retail Bank approved and communicated. The availability of promotions must be consistently shared with customers when they apply for credit.

Transparency Principles : Compliance Requirements (Cont’d)

Home Specialty Orientation Guide – 395Credit extended by Synchrony Bank • www.synchronybusiness.com

Resources And Tools

Important websites and apps

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 405Home Specialty Orientation Guide

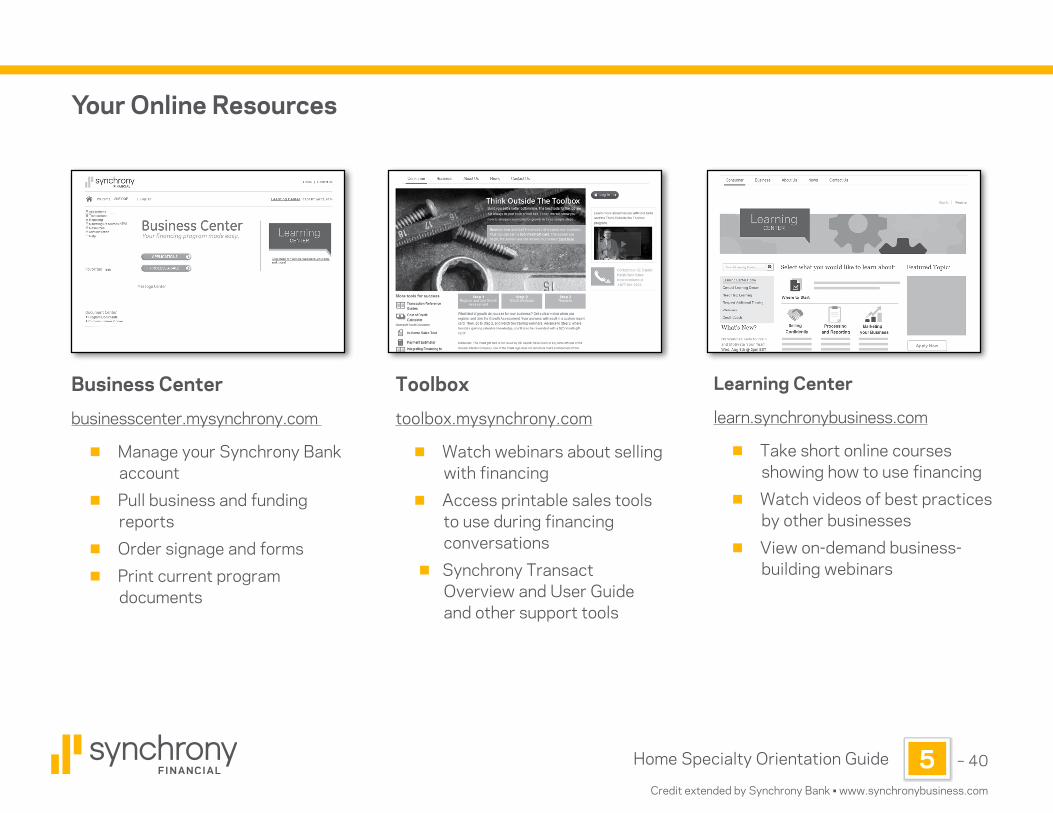

Your Online Resources

Business Center

businesscenter.mysynchrony.com

■■ Manage your Synchrony Bank account

■■ Pull business and funding reports

■■ Order signage and forms■■ Print current program

documents

Toolbox

toolbox.mysynchrony.com

■■ Watch webinars about selling with financing

■■ Access printable sales tools to use during financing conversations

■■ Synchrony Transact Overview and User Guide and other support tools

Learning Center

learn.synchronybusiness.com

■■ Take short online courses showing how to use financing

■■ Watch videos of best practices by other businesses

■■ View on-demand business-building webinars

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 415Home Specialty Orientation Guide

Business Center

Your online resource to manage your Synchrony Bank account

■■ Submit credit applications■■ Access reports■■ Order signage and forms■■ Access marketing tools■■ View training courses and videos■■ Access program updates and alerts

Let’s take a closer look at the tools found in Business Center

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 425Home Specialty Orientation Guide

Business Center Registration

1. How Do I Get Started? • Register at www.mysynchrony.com. (You will need your Merchant number and bank DDA number) • Person registering will be Location Administrator for Business Center and responsible for: - Providing an email address and other requested information - Adding all users for that location and setting permissions for each user - Adding Synchrony programs for that location

2. Get Familiar with Business Center • Access the Navigation map for a quick overview of all that Business Center has to offer • Access the Business Center training courses at: https://businesscenter.mysynchrony.com

3. Start Offering Credit • Offer to every customer • Offer early in the sales process

Use Business Center for all your processing, reporting and resources needs to begin enjoying the increased sales you can generate by offering credit today.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 435Home Specialty Orientation Guide

Reporting

Click the “Reporting” link from the left-hand menu to access the various reports offered.

The following reports are available for revolving financing programs:

■■ Business Dashboard - Summarizes application and credit line approvals

■■ Funding Report - Provides a daily update of funding

■■ Website User Activity Report - Displays Applications, Sales & Business Center login data

■■ Application Summary - Provides a history of your consumer applications

■■ Authorizations Report - View all authorization-only transactions

■■ Monthly Statement - Details your monthly transactions of sales, fees and deposits

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 445Home Specialty Orientation Guide

Marketing Resource Access

“Click” the “Marketing Resources” link in the left-hand menu to access Business Center tools that can help you promote your business:

■■ Marketing Toolkit – Create, customize and print personalized, offer specific direct mail for existing and prospective customers.

■■ My Customer List – Pull a list of your current customers with available credit.

■■ My Business Locator Info – Add your business to an online directory of dealers. Consumers can also search for dealers.

Advertising Guidelines

Review the Advertising Guidelines file, located in Advertising Center under Resources:

■■ View compliant headlines and disclosures to use in your advertisements in print, online and in other media.

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 455Home Specialty Orientation Guide

ResourcesResources

There is an assortment of resources in Business Center available to help you manage your financing program.

Click the “Resources” link in the left-hand menu to access the various resources offered in the Business Center.

The following resources are available for revolving financing programs.

■■ Order Supplies - Select supplies to be ordered and shipped to you

■■ Program Documents - Access to documents relating to your credit card program

■■ Learning Center - Videos, webinars, self-paced courses and useful downloads to learn to sell more with financing

■■ Website links - Access to common websites

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 465Home Specialty Orientation Guide

Today We discussed…

■■ How financing can help you achieve your business’s priorities, while helping your customers get what they really want or need.*

■■ How to complete Applications, Sales Slips and Completion Certificates.■■ How promotional financing works, including Deferred Interest, No Interest and

Reduced Interest promotions.■■ How and when to discuss financing with every customer clearly.■■ How to get additional training for new and existing team members.■■ Important rules for fair and compliant business practices when offering financing.

*Subject to credit approval.

You made it!

Any questions?

Credit extended by Synchrony Bank • www.synchronybusiness.com

– 475Home Specialty Orientation Guide

Merchant Support 888-222-2176

■■ Assistance with submitting applications

■■ Obtain names on an account ■■ Check available credit amount■■ Request a credit line increase■■ Technical assistance with

Business Center

Cardholder Support* 800-250-5411

■■ Account Questions■■ Credit Line Increases■■ Address updates

On-Demand Training

■■ Learning Center: https://learn.synchronybusiness.com

We are here to support you!Getting Help

*Please Note: Cardholder inquiry representatives are authorized to speak only with cardholders about their account.

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

184-242-00 Rev June 2017

Home Specialty Orientation GuideCredit extended by Synchrony Bank • www.synchronybusiness.com