Embed Size (px)

Citation preview

Hotel Intelligence Venice 2013

Hotels & Hospitality

Despite subdued hotel performance in the city in 2012, the first seven

months of 2013 have shown a return to growth for Venice. We expect

to see positive trading performance for the rest of 2013 on the back of

the Biennale event taking place over the six months from June to

November.

2 Hotel Intelligence: Venice

Contributors Table of Contents Market Snapshot Overall tourism demand contracted while international tourism peaked in 2012 Strong overall growth at Venice airports in 2012 International meetings grow in Venice in 2012 International tourism expected to fuel growth in 2013 Stable hotel supply in the city driven by boutique hotels Subdued growth in hotel trading performance in 2012, growth expected for 2013 Notable growth expected in the short term

Alexander French Research Assistant, EMEA [email protected]

Giuliano Esposito Vice President, Milan [email protected]

3

4

5

6

7

7

9

10

Jones Lang LaSalle’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centers; mixed-use developments and other hospitality properties. The firm’s more than 265 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totaling nearly US$25 billion, while also completing approximately 4,000 advisory and valuation assignments. The group’s hotels and hospitality specialists pro-vide independent and expert advice to clients, backed by industry-leading research. For more news, videos and research from Jones Lang LaSalle’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality

Hotel Intelligence: Venice 3

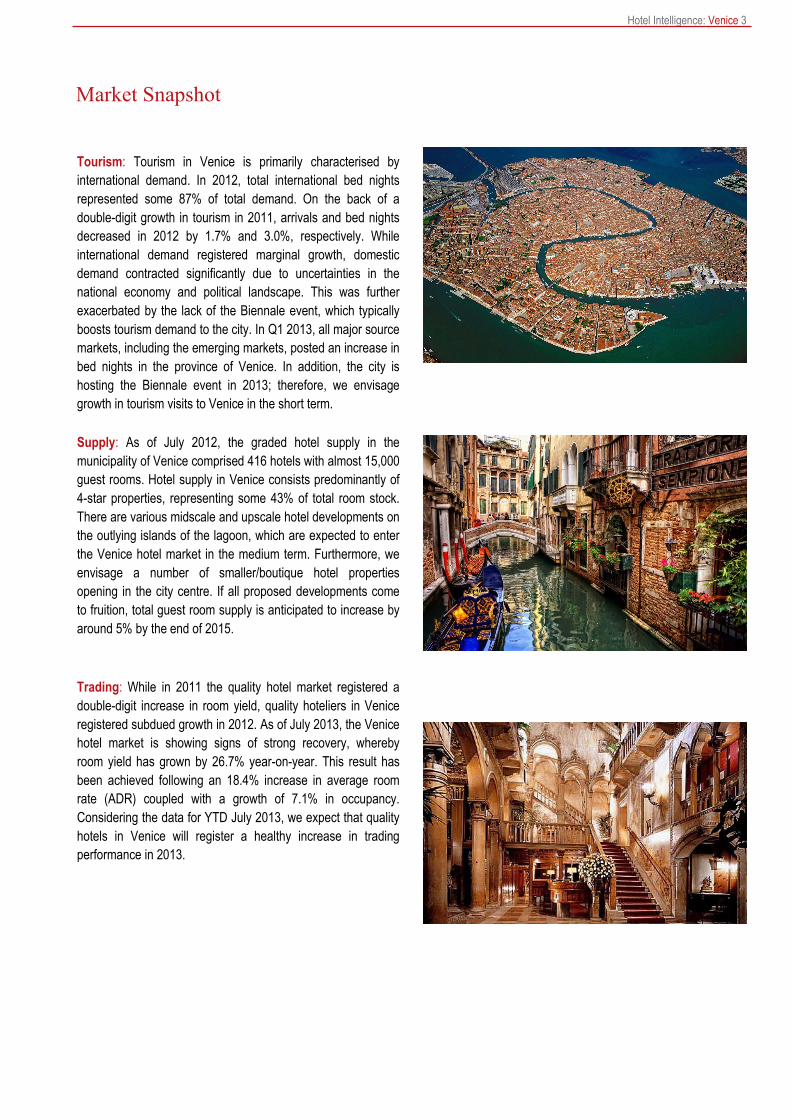

Market Snapshot

Tourism: Tourism in Venice is primarily characterised by

international demand. In 2012, total international bed nights

represented some 87% of total demand. On the back of a

double-digit growth in tourism in 2011, arrivals and bed nights

decreased in 2012 by 1.7% and 3.0%, respectively. While

international demand registered marginal growth, domestic

demand contracted significantly due to uncertainties in the

national economy and political landscape. This was further

exacerbated by the lack of the Biennale event, which typically

boosts tourism demand to the city. In Q1 2013, all major source

markets, including the emerging markets, posted an increase in

bed nights in the province of Venice. In addition, the city is

hosting the Biennale event in 2013; therefore, we envisage

growth in tourism visits to Venice in the short term.

Supply: As of July 2012, the graded hotel supply in the

municipality of Venice comprised 416 hotels with almost 15,000

guest rooms. Hotel supply in Venice consists predominantly of

4-star properties, representing some 43% of total room stock.

There are various midscale and upscale hotel developments on

the outlying islands of the lagoon, which are expected to enter

the Venice hotel market in the medium term. Furthermore, we

envisage a number of smaller/boutique hotel properties

opening in the city centre. If all proposed developments come

to fruition, total guest room supply is anticipated to increase by

around 5% by the end of 2015.

Trading: While in 2011 the quality hotel market registered a

double-digit increase in room yield, quality hoteliers in Venice

registered subdued growth in 2012. As of July 2013, the Venice

hotel market is showing signs of strong recovery, whereby

room yield has grown by 26.7% year-on-year. This result has

been achieved following an 18.4% increase in average room

rate (ADR) coupled with a growth of 7.1% in occupancy.

Considering the data for YTD July 2013, we expect that quality

hotels in Venice will register a healthy increase in trading

performance in 2013.

4 Hotel Intelligence: Venice

Overall tourism demand contracted while international tourism peaked in

2012

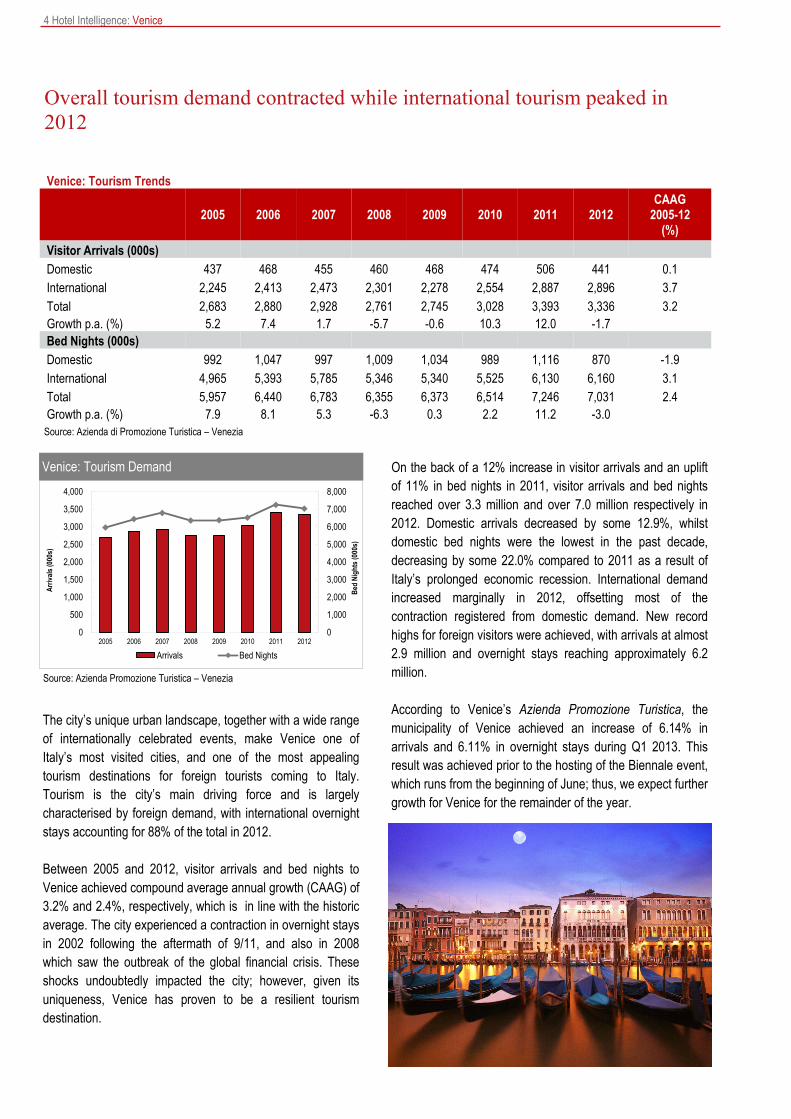

The city’s unique urban landscape, together with a wide range

of internationally celebrated events, make Venice one of

Italy’s most visited cities, and one of the most appealing

tourism destinations for foreign tourists coming to Italy.

Tourism is the city’s main driving force and is largely

characterised by foreign demand, with international overnight

stays accounting for 88% of the total in 2012.

Between 2005 and 2012, visitor arrivals and bed nights to

Venice achieved compound average annual growth (CAAG) of

3.2% and 2.4%, respectively, which is in line with the historic

average. The city experienced a contraction in overnight stays

in 2002 following the aftermath of 9/11, and also in 2008

which saw the outbreak of the global financial crisis. These

shocks undoubtedly impacted the city; however, given its

uniqueness, Venice has proven to be a resilient tourism

destination.

On the back of a 12% increase in visitor arrivals and an uplift

of 11% in bed nights in 2011, visitor arrivals and bed nights

reached over 3.3 million and over 7.0 million respectively in

2012. Domestic arrivals decreased by some 12.9%, whilst

domestic bed nights were the lowest in the past decade,

decreasing by some 22.0% compared to 2011 as a result of

Italy’s prolonged economic recession. International demand

increased marginally in 2012, offsetting most of the

contraction registered from domestic demand. New record

highs for foreign visitors were achieved, with arrivals at almost

2.9 million and overnight stays reaching approximately 6.2

million.

According to Venice’s Azienda Promozione Turistica, the

municipality of Venice achieved an increase of 6.14% in

arrivals and 6.11% in overnight stays during Q1 2013. This

result was achieved prior to the hosting of the Biennale event,

which runs from the beginning of June; thus, we expect further

growth for Venice for the remainder of the year.

Venice: Tourism Trends

2005 2006 2007 2008 2009 2010 2011 2012

CAAG 2005-12

(%)

Visitor Arrivals (000s)

Domestic 437 468 455 460 468 474 506 441 0.1

International 2,245 2,413 2,473 2,301 2,278 2,554 2,887 2,896 3.7

Total 2,683 2,880 2,928 2,761 2,745 3,028 3,393 3,336 3.2

Growth p.a. (%) 5.2 7.4 1.7 -5.7 -0.6 10.3 12.0 -1.7

Bed Nights (000s)

Domestic 992 1,047 997 1,009 1,034 989 1,116 870 -1.9

International 4,965 5,393 5,785 5,346 5,340 5,525 6,130 6,160 3.1

Total 5,957 6,440 6,783 6,355 6,373 6,514 7,246 7,031 2.4

Growth p.a. (%) 7.9 8.1 5.3 -6.3 0.3 2.2 11.2 -3.0

Source: Azienda di Promozione Turistica – Venezia

Source: Azienda Promozione Turistica – Venezia

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2006 2007 2008 2009 2010 2011 2012

Bed

Nig

hts

(00

0s)

Arr

ival

s (0

00s)

Arrivals Bed Nights

Venice: Tourism Demand

Hotel Intelligence: Venice 5

Venice’s major foreign source markets are the USA, and key

European countries such as France, the United Kingdom and

Germany. Bed nights from the USA declined marginally in

2012, whilst the European source markets posted mixed

results, with overnight stays increasing significantly from the

UK (+13.3%), although by only 1.1% from France, whereas

overnight stays from Spain and Germany fell by around 19%

and 4% respectively. A strong growth in demand was reported

from China (+16.8%), Russia (+7.5%) and Japan (+6.0%),

while Brazil posted a decrease of around 3.0%, following a

+40% increase in 2011.

The visitor mix to Venice is expected to change in the medium

to long term, with an increasing number of tourists coming

from the BRIC countries (Brazil, Russia, India and China) and

from other markets in South America and Asia. In 2013, we

expect a potential uplift in visitation from the Biennale event,

although domestic and European demand will likely remain

subdued.

As at Q1 2013, the province of Venice registered a contraction

in tourists arrivals from the USA and a marginal uplift in bed

nights. All principal European feeder markets, apart from

Spain, registered growth in both arrivals and bed nights during

the same period. Further growth in arrivals and bed nights

was recorded from the BRIC countries, with China growing by

11.9%, Brazil by 7.5% and Russia by 5.3% in terms of bed

nights. Bed nights from India posted a noteworthy 17.7%

increase in Q1 2013, albeit from a much lower base volume.

Source: Azienda Promozione Turistica – Venezia

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000

USA

France

UK

Germany

Spain

Japan

Brazil

China

Russia

Visitor Origin 2012 Visitor Origin 2011

Venice: Top Feeder Markets 2012 vs. 2011

Strong overall growth at Venice

airports in 2012

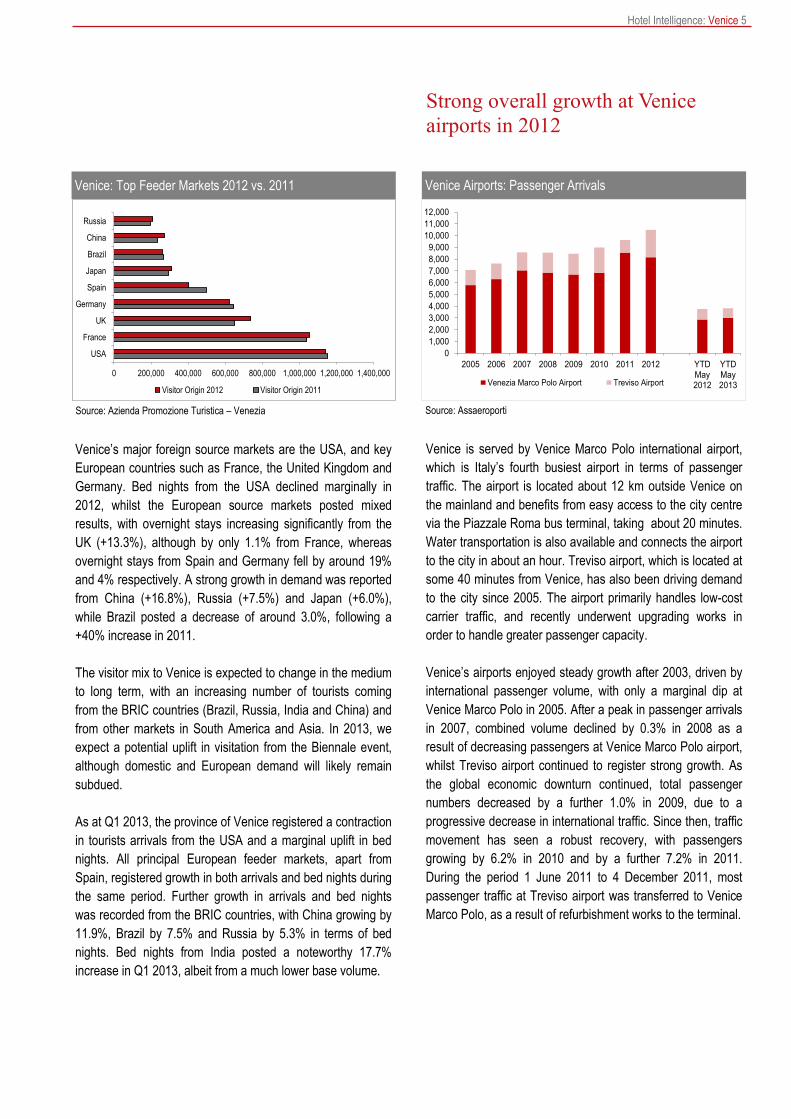

Venice is served by Venice Marco Polo international airport,

which is Italy’s fourth busiest airport in terms of passenger

traffic. The airport is located about 12 km outside Venice on

the mainland and benefits from easy access to the city centre

via the Piazzale Roma bus terminal, taking about 20 minutes.

Water transportation is also available and connects the airport

to the city in about an hour. Treviso airport, which is located at

some 40 minutes from Venice, has also been driving demand

to the city since 2005. The airport primarily handles low-cost

carrier traffic, and recently underwent upgrading works in

order to handle greater passenger capacity.

Venice’s airports enjoyed steady growth after 2003, driven by

international passenger volume, with only a marginal dip at

Venice Marco Polo in 2005. After a peak in passenger arrivals

in 2007, combined volume declined by 0.3% in 2008 as a

result of decreasing passengers at Venice Marco Polo airport,

whilst Treviso airport continued to register strong growth. As

the global economic downturn continued, total passenger

numbers decreased by a further 1.0% in 2009, due to a

progressive decrease in international traffic. Since then, traffic

movement has seen a robust recovery, with passengers

growing by 6.2% in 2010 and by a further 7.2% in 2011.

During the period 1 June 2011 to 4 December 2011, most

passenger traffic at Treviso airport was transferred to Venice

Marco Polo, as a result of refurbishment works to the terminal.

Source: Assaeroporti

Venice Airports: Passenger Arrivals

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

2005 2006 2007 2008 2009 2010 2011 2012 YTDMay2012

YTDMay2013Venezia Marco Polo Airport Treviso Airport

6 Hotel Intelligence: Venice

International meetings grow in Venice in 2012

In 2012, total passenger arrivals continued to grow, posting an

overall increase of 8.9% compared to 2011. This was driven

primarily by a strong boost in international passengers, which

registered CAAG rates of 13% at Venice Marco Polo airport

and 2% at Treviso airport.

As of May 2013, Venice’s airports registered an aggregate

increase of 1.6%, fuelled entirely by international demand.

International passengers continue to boost volume at Venice

Marco Polo airport, increasing by 8.8% compared to the same

period in 2012, while domestic passengers contracted by

8.4%. International passengers at Treviso airport registered a

9.7% decrease, while domestic passengers decreased by

3.4%.

Venice Convention, the city’s dedicated conference and

congress hub, is located about a 30 minute ferry ride from the

city centre on the Venice Lido. The facility comprises two

historic buildings (Palazzo del Cinema and Palazzo del

Casinò) and a large indoor arena (Palagalileo), which together

can host up to 4,000 delegates. The largest space is the

Palagalileo with a capacity of up to 1,500 attendees. The

proposed plans for a new Palazzo del Cinema are currently on

hold; however, should the project proceed it will be the largest

dedicated conference venue in Venice, with a capacity for

over 2,000 delegates.

In addition to Venice Convention, there are various hotels

outside the city centre and on the islands which have

historically provided significant meeting space for medium to

large-scale events. The Hotel Excelsior, located on the Venice

Lido, has been the venue for a wide range of recurring and

renowned events, such as the Venice International Film

Festival. In 2008, the Hilton Molino Stucky, located on

Giudecca Island, added a large conference facility to the city,

with a congress centre for up to 1,000 delegates. Other

conference and meeting facilities can be found at the San

Clemente Palace Hotel located on San Clemente Island,

however the hotel is closed at the time of writing after entering

financial difficulties. The Sacca Sessola hotel project on the

island of Sacca Sessola, which is slated to open in 2015, will

add additional meeting and conference space to the city.

According to the latest International Association Meetings

Market report, published by the International Congress and

Convention Association (ICCA), Venice hosted 34 meetings in

2012, an impressive increase on the 22 events hosted in

2011. As mentioned earlier, in 2013 the city is hosting the

Biennale event, which typically attracts a wide range of

associated meetings and events to the city; thus, we expect a

year of robust meeting and conference demand for Venice.

Venice: International Meetings

0

10

20

30

40

2007 2008 2009 2010 2011 2012

Nu

mb

er

of

Me

etin

gs

Meetings

Source: ICCA

Venice has a limited proportion of corporate demand and is

generally dominated by leisure tourism visits. Given the

intrinsic urban landscape of the city, there are few dedicated

conference and meeting facilities, consequently limiting the

number of large events that can be hosted.

Hotel Intelligence: Venice 7

International tourism expected to

fuel growth in 2013

According to the Venice Tourism Office, as of July 2013 the

municipality of Venice comprised 416 graded hotels consisting

of around 14,988 guest rooms. The average hotel size in

Venice comprises around 36 guest rooms, reflecting the

prevalence of small family-owned hotels, which is generally in

line with the national average. The 4-star category represents

about 43.3% of total guest rooms in the city, followed by the 3-

star guest rooms (31.6%) and 5-star guest rooms (13.4%).

Due to the inherent characteristics of the city, hotel supply in

Venice is generally concentrated in the following locations:

1.) The historic city centre. Here, hotel supply consists of

small independent or family operated hotels, guesthouses and

quality hotels as well as the traditional grand hotels.

2.) Mestre. The mainland, where it is possible to develop new

hotels. Here, a number of hotel properties are concentrated,

including the larger business hotels, varying in standard from

budget to luxury.

3.) Islands. There are many outlying islands in the Venetian lagoon, which over the years have been transformed into resorts. The Venice Lido, given its size and history, was the first resort destination in the Venice Lagoon.

Given the difficulties in identifying suitable sites and

restrictions in adapting historic buildings to hotel use, the 4-

star and 5-star hotel supply in the centre of Venice has

remained relatively stable in the last few years. Over the

years, international and domestic operators such as Starwood

Hotels & Resorts, Orient-Express, Hilton, NH Hoteles,

Starhotels and Baglioni Hotels have all made their mark in the

city, and we expect chain operators to continue to seek

desirable locations across the city.

On the back of a significant increase in tourism demand in

2011, Venice registered its first real decrease in arrivals and

bed nights in 2012 since 2009. This was the result of a

significant contraction in domestic demand due to the fragility

of the domestic economy, as well as the lack of the Biennale

event taking place.

The traditional feeder markets, as well as the emerging

markets, both posted increases in bed nights during Q1 2013.

We expect the emerging markets to sustain growth in tourism

demand to the city in the short and medium term. Domestic

demand is anticipated to remain muted until consumer

confidence returns and the Italian economy returns to growth.

The city’s architectural and cultural wealth, together with its

distinctive urban landscape, will continue to attract leisure

visitors from all over the globe. Furthermore, the wide range of

international events held throughout the year, including the

Biennale, the prestigious International Film Festival and the

celebrated Venice Carnival, will continue to support the city’s

appeal.

Stable hotel supply in the city driven

by boutique hotels

Venice: Hotel Supply (as at July 2013)

Grade Establishments Rooms % of Total

5 star 20 2,005 13.4%

4 star 105 6,490 43.3%

3 star 183 4,734 31.6%

Other* 108 1,759 11.7%

Total 416 14,988 –

*Includes 1– and 2– star hotels Source: Azienda Promozione Turistica – Venezia

8 Hotel Intelligence: Venice

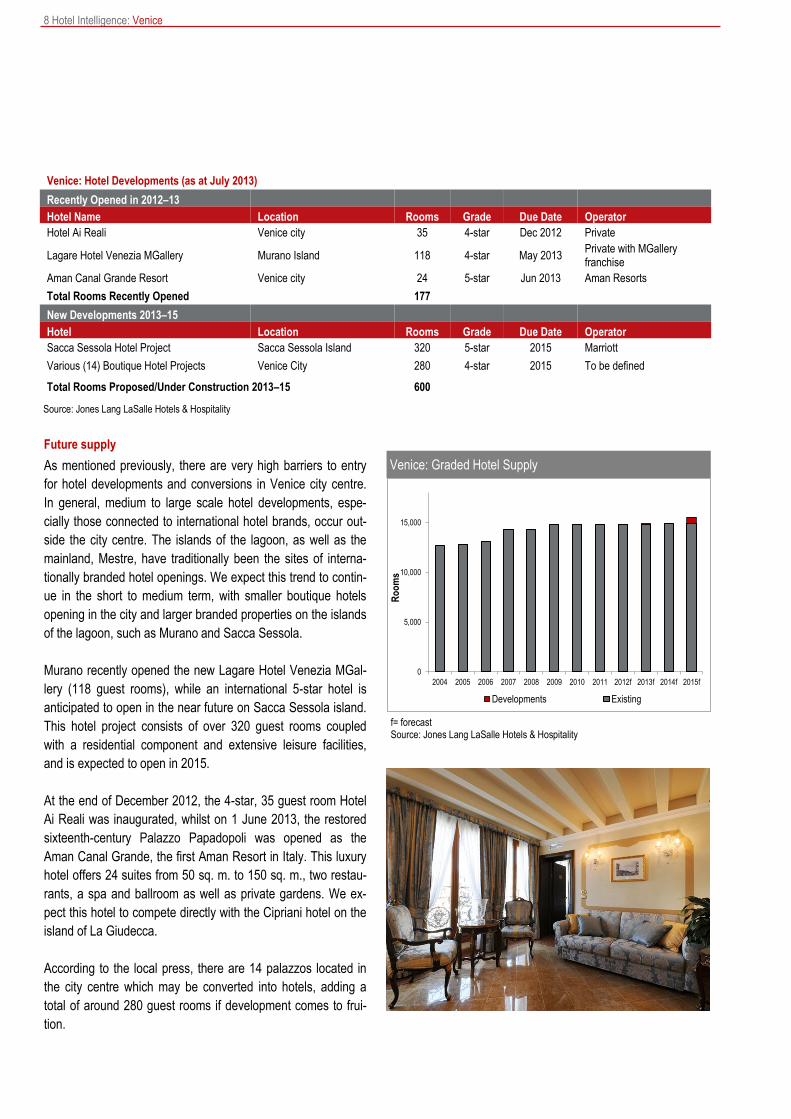

Future supply

As mentioned previously, there are very high barriers to entry

for hotel developments and conversions in Venice city centre.

In general, medium to large scale hotel developments, espe-

cially those connected to international hotel brands, occur out-

side the city centre. The islands of the lagoon, as well as the

mainland, Mestre, have traditionally been the sites of interna-

tionally branded hotel openings. We expect this trend to contin-

ue in the short to medium term, with smaller boutique hotels

opening in the city and larger branded properties on the islands

of the lagoon, such as Murano and Sacca Sessola.

Murano recently opened the new Lagare Hotel Venezia MGal-

lery (118 guest rooms), while an international 5-star hotel is

anticipated to open in the near future on Sacca Sessola island.

This hotel project consists of over 320 guest rooms coupled

with a residential component and extensive leisure facilities,

and is expected to open in 2015.

At the end of December 2012, the 4-star, 35 guest room Hotel

Ai Reali was inaugurated, whilst on 1 June 2013, the restored

sixteenth-century Palazzo Papadopoli was opened as the

Aman Canal Grande, the first Aman Resort in Italy. This luxury

hotel offers 24 suites from 50 sq. m. to 150 sq. m., two restau-

rants, a spa and ballroom as well as private gardens. We ex-

pect this hotel to compete directly with the Cipriani hotel on the

island of La Giudecca.

According to the local press, there are 14 palazzos located in

the city centre which may be converted into hotels, adding a

total of around 280 guest rooms if development comes to frui-

tion.

Venice: Graded Hotel Supply

f= forecast Source: Jones Lang LaSalle Hotels & Hospitality

0

5,000

10,000

15,000

2004 2005 2006 2007 2008 2009 2010 2011 2012f 2013f 2014f 2015f

Ro

om

s

Developments Existing

Venice: Hotel Developments (as at July 2013)

Recently Opened in 2012–13

Hotel Name Location Rooms Grade Due Date Operator

Hotel Ai Reali Venice city 35 4-star Dec 2012 Private

Lagare Hotel Venezia MGallery Murano Island 118 4-star May 2013 Private with MGallery franchise

Aman Canal Grande Resort Venice city 24 5-star Jun 2013 Aman Resorts

Total Rooms Recently Opened 177

New Developments 2013–15

Hotel Location Rooms Grade Due Date Operator

Sacca Sessola Hotel Project Sacca Sessola Island 320 5-star 2015 Marriott

Various (14) Boutique Hotel Projects Venice City 280 4-star 2015 To be defined

Total Rooms Proposed/Under Construction 2013–15 600

Source: Jones Lang LaSalle Hotels & Hospitality

Hotel Intelligence: Venice 9

Subdued growth in hotel trading performance in 2012, growth expected for

2013

Venice: Quality Hotel Trading Performance

2005 2006 2007 2008 2009 2010 2011 2012

Occupancy (%) 62.6 64.9 61.9 55.7 56.0 59.0 67.6 67.9

ADR (€) 299.9 316.3 350.8 302.5 264.4 255.5 289.4 288.5

RevPAR (€) 187.8 205.3 217.2 168.4 148.0 150.7 195.6 195.9

RevPAR growth (%) 2.8 9.3 5.8 -22.5 -12.2 1.9 29.8 0.1

Inflation (%) 2.1 2.5 2.0 3.3 0.8 1.6 2.8 2.3

ADR 2012 values (€) 348.7 358.9 403.1 325.8 282.5 268.7 296.1 288.5

RevPAR 2012 values (€) 218.4 233.0 241.7 181.4 158.1 158.5 200.1 195.9 Note: Selection of 4- and 5-star hotels Source: STR Global

As of July 2013, the Venice hotel market had posted an

impressive 26.7% increase in room yield year-on-year.

Although January registered a decrease in RevPAR of around

3%, the months of February and March, and from May to July,

achieved double-digit increases. This is partly attributable to

the activities surrounding the Biennale event.

The Venice hotel market consistently ranks as one of

Europe’s best-performing markets. In the past decade,

however, the city has experienced subdued performance as a

result of extraordinary events affecting the city’s primary

source market, the USA, as well as deteriorating conditions in

the domestic economic and political landscape.

During the period 2000 to 2007, the city of Venice registered

an annual increase in average room rates of about 2.6%. On

the back of this increase, occupancy decreased by some

2.4%, resulting in a marginal increase in revenue per available

room (RevPAR) during the period.

Following the peak in room yield in 2007, up to €242 in real

terms, the Venice hotel market experienced an average

annual decrease in RevPAR between 2007 and 2009 of

around 19%, driven predominantly by decreases in average

room rate. In 2010, a slight upturn was registered, with year-

end occupancy at 59%, representing a 3% increase compared

to 2009. Average daily rate continued to register decreases

(−3.4%) in 2010, resulting in an increase in RevPAR of around

1.9%. In 2011, Venice posted an impressive rebound in

trading with RevPAR growth of almost 30% year-on-year,

although RevPAR is still below historic levels. Hotel trading

performance in 2011 was fuelled by a general improvement in

the global financial and tourism markets coupled with the

Biennale event.

In 2012, quality hotel trading performance in Venice remained

generally stable compared to 2011, a positive result

considering that RevPAR jumped by around 30% in 2011 and

the city did not host the Biennale event. The first few months

of 2012 (January, February and April) as well as November

showed healthy increases in RevPAR, enabling hoteliers to

boost overall trading performance marginally by year-end.

Source: STR Global

Venice: Year-to-Date Trading

July 2012 2013 Change (%)

Occupancy (%) 65.4 70.0 7.0

ADR (€) 292.1 345.8 18.4

RevPAR (€) 190.9 242.0 26.8

Venice: Quality Hotel Trading

Source: STR Global

0%

20%

40%

60%

80%

100%

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012

Occ

up

ancy

€(2

012

Val

ues

)

ADR 2012 Values RevPAR € Occupancy %

10 Hotel Intelligence: Venice

Notable growth expected in the short

term

The table above shows the evolution of Venice’s quality

hotels’ trading performance over the past 5 and 10 years in

real terms. Occupancy in the last 5 years has been broadly in

line with the past decade, suggesting that although worsening

economic conditions have prevailed, demand to the city

remained robust, primarily from international markets. The

challenging economic conditions in the past 5 years, however,

put pressure on average room rate, which declined by 3.0%,

broadly in line with the 10-year period. However, given the

inherent appeal of the city, occupancy in the past 5 years has

returned to pre-crisis levels, boosting the RevPAR CAAG in

real terms to 1.9%.

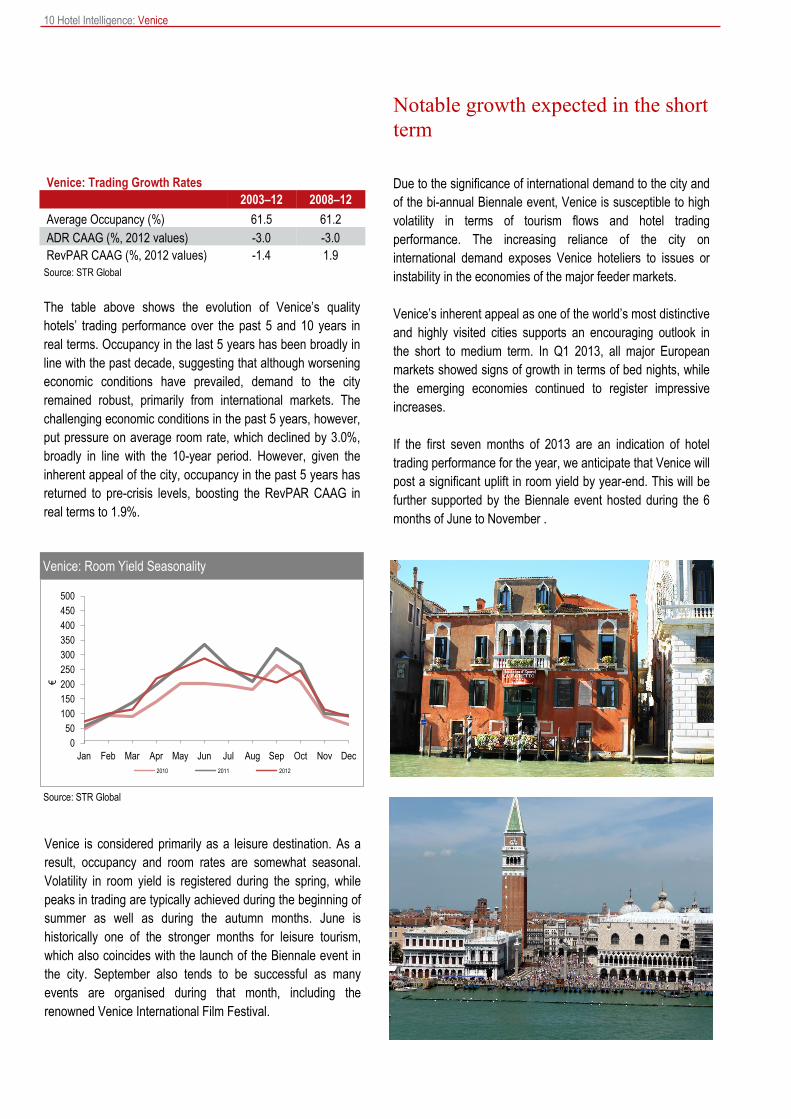

Venice is considered primarily as a leisure destination. As a

result, occupancy and room rates are somewhat seasonal.

Volatility in room yield is registered during the spring, while

peaks in trading are typically achieved during the beginning of

summer as well as during the autumn months. June is

historically one of the stronger months for leisure tourism,

which also coincides with the launch of the Biennale event in

the city. September also tends to be successful as many

events are organised during that month, including the

renowned Venice International Film Festival.

Venice: Room Yield Seasonality

Source: STR Global

0

50

100

150

200

250

300

350

400

450

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

€

2010 2011 2012

Due to the significance of international demand to the city and

of the bi-annual Biennale event, Venice is susceptible to high

volatility in terms of tourism flows and hotel trading

performance. The increasing reliance of the city on

international demand exposes Venice hoteliers to issues or

instability in the economies of the major feeder markets.

Venice’s inherent appeal as one of the world’s most distinctive

and highly visited cities supports an encouraging outlook in

the short to medium term. In Q1 2013, all major European

markets showed signs of growth in terms of bed nights, while

the emerging economies continued to register impressive

increases.

If the first seven months of 2013 are an indication of hotel

trading performance for the year, we anticipate that Venice will

post a significant uplift in room yield by year-end. This will be

further supported by the Biennale event hosted during the 6

months of June to November .

Venice: Trading Growth Rates

2003–12 2008–12

Average Occupancy (%) 61.5 61.2

ADR CAAG (%, 2012 values) -3.0 -3.0

RevPAR CAAG (%, 2012 values) -1.4 1.9

Source: STR Global

Hotel Intelligence: Venice

This report is confidential to the recipient of the report. No reference to the report or any part of it may be published in any document, state-ment or circular or in any communication with third parties without the prior written consent of Jones Lang LaSalle Hotels & Hospitality, including specifically in relation to the form and context in which it will appear. We stress that forecasting is a problematical exercise which at best should be regarded as an indicative assessment of possibilities rather than absolute certainties. The process of making forward projections involves assumptions in respect of a considerable number of varia-bles which are acutely sensitive to changing conditions, variations in any one of which may significantly affect the outcome and we draw your attention to this factor. Jones Lang LaSalle Hotels & Hospitality makes no representation, warranty, assurance or guarantee with re-spect to any material with which this report may be issued and this report should not be taken as an endorsement of or recommendation on any participation by any intending investor or any other party in any transaction whatsoever. This report has been produced solely as a general guide and does not constitute advice. Users should not rely on this report and must make their own enquiries to verify and satisfy themselves of all aspects of information set out in the report. We have used and relied upon information from sources generally regarded as authoritative and reputable, but the information obtained from these sources may not have been independently verified by Jones Lang LaSalle Hotels & Hospitality. Whilst the material contained in the report has been prepared in good faith and with due care, no representation or warranty is made in relation to the accuracy, currency, completeness, suitability or otherwise of the whole or any part of the report. Jones Lang LaSalle Hotels & Hospitality, its officers, employees, subcontractors and agents shall not be liable (to the extent permitted by law) to any person for any loss, liability, damage or expense (‘liability’) arising directly or indirectly from or connected in any way with any use of or reliance on this report. If any liability is established, notwithstanding this exclusion, it shall not exceed $1,000.

12 Hotel Intelligence: Venice

AMERICAS

Atlanta

Buenos Aires

Chicago

Dallas

Denver

Los Angeles

Mexico City

Miami

New York

San Francisco

Sao Paulo

Washington DC

EMEA

Barcelona

Dubai

Dusseldorf

Exeter

Frankfurt

Glasgow

Istanbul

Leeds

London

Lyon

Madrid

Manchester

ASIA

Bangkok

Chengdu

Jakarta

New Delhi

Peking

Shanghai

Singapore

Tokyo

ANZ

Auckland

Brisbane

Melbourne

Perth

Sydney

Marseille

Milan

Moscow

Munich

Paris

Rome

Our domestic & global reach

Hotels & Hospitality

Roberto Galano Executive Vice President Milan, Italy +39 02 8586 8671 [email protected]

For enquiries, please contact:

www.jll.com/hospitality | www.joneslanglasalle.it

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013

Milan Via Agnello 8 20121 Milan Italy

Rome Via Bissolati 20 00187 Rome Italy