Embed Size (px)

Citation preview

How Hong Kong can support your business in China and other Asian countries Daniel Booth Director Vistra (Hong Kong)

Rotterdam May, 2012

2

The role of Hong Kong

• A recognized and respected jurisdiction for active trading companies.

• The most favoured entry point for inbound investment into China.

• A simple and effective corporate holding jurisdiction.

• Increasing role as a centre for personal asset holding

• The jurisdiction of choice for outbound Chinese investment.

3

Hong Kong commonly used for:

• Holding company for inbound investments into China

• Contract Manufacturing structure with China

• Trading activities in Asia

• Outbound investment subsidiary of PRC investors

• Greater China offshore services

4

Why does Hong Kong support these roles – the client’s perspective

• A “soft-landing” in Asia

• Familiar legal system

• Free of corruption

• Strong domestic and international IP protection

• Highly transparent business environment

• Fully convertible currency with personal and Corporate RMB accounts allowed

• Simple domestic tax system

• Most advantageous tax agreement with China and now other nations

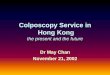

Hong Kong Tax Highlights - Companies

Hong Kong companies

Basis of taxation Territorial

Corporate income tax rate 16.5%

Capital gains tax rate -

Withholding tax (payments to non-residents) -Dividends -Interest -Royalties -Technical assistance/service/management fees

- -

4.95% -

Treaty network *at May 15 2012

- 23 comprehensive DTAs - 29 limited DTAs - 11 DTA’s currently under negotiation

*Capital duty in HK to be abolished effective June 1, 2012*

6

A simple system in comparison…

CHINA Business Tax: 3% to 20% Enterprise Income Tax: 25% Individual Income Tax: 5% to 45% VAT: 0% - 17% Consumption Tax: 1% - 50% Withholding Tax: 10% - 20% Capital Gains Tax: 10% - 20% Urban Real Estate Tax 1.2% Education Surcharge 3%-5% Urban Construction Tax 1%-7%

HONG KONG Business Tax: N/A Profits Tax: 16.5% Salaries Tax: 15.5% VAT: N/A Consumption Tax: N/A Withholding Tax: N/A Capital Gains Tax: N/A Estate Duty: abolished since Feb 2006

Hong Kong Tax Highlights – Comprehensive DTAs

ASIA / APAC EUROPE MIDDLE EAST

UNDER NEGOTIATION

Brunei China Indonesia Japan Malaysia New Zealand Thailand Vietnam

Austria Belgium Czech Republic France Hungary Ireland Jersey Liechtenstein Luxembourg Malta

Netherlands Portugal Spain Switzerland United Kingdom

Kuwait Bangladesh Canada Finland Guernsey India Italy Korea Macau (SAR) Mexico Saudi Arabia United Arab Emirates

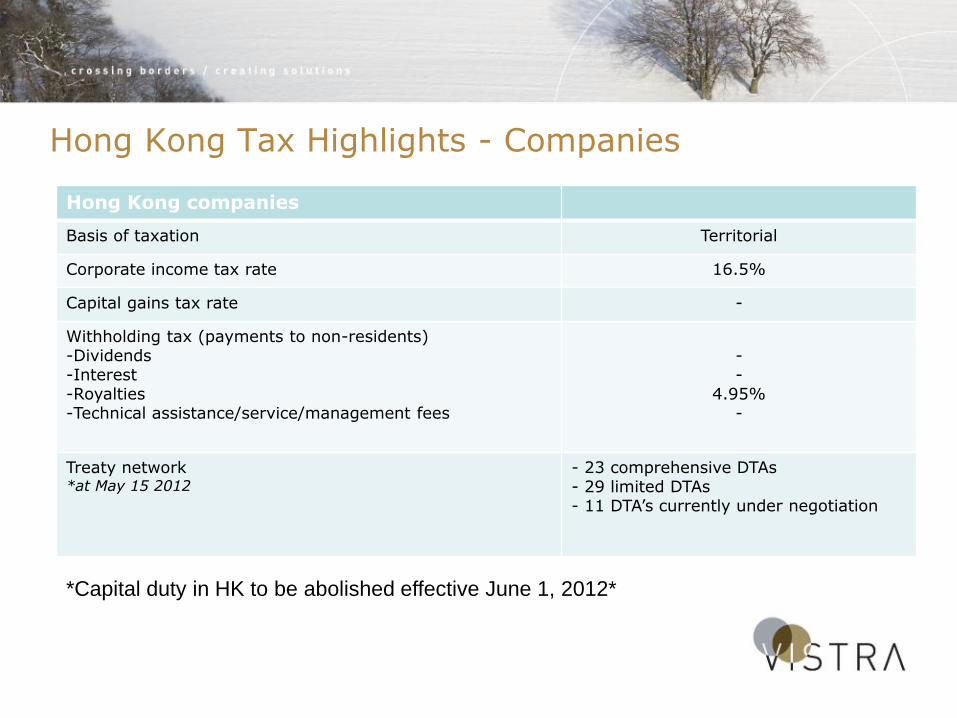

Comprehensive DTAs within Asia

Withholding tax rates (percentage)

Dividends Interest Royalties

Domestic Tax Treaty Domestic Tax Treaty Domestic Tax Treaty

ASIA

China 10 5a/10 10 0a/7 10 4.95a/16.5

Brunei 0 0 15 0a/5a/10 10 5

Indonesia 20 5a/10 20 0*/10 20 5

Japan 7c/15c/20 5a/7a/10 15 0/10 20 5

New

Zealand

30 0a/5a/15 15 10 15 5

Thailand 10 10 0c/15 0a/10a/15 15 5a/10a/15

Vietnam 0 10 10 0a/10 10 7a/10

Malaysia 0 5a/10 15 0a/10 10 8

9

Structuring a Hong Kong Limited company

• Company name For private company, must end with “Limited” • Statutory officer and shareholder requirements HK resident secretary HK registered office address Minimum 1 director Minimum 1 shareholder • All shareholder and officer information is publicly

available

Set-up and activation of a Hong Kong Limited company

• File application with Companies Registry

• Apply for BRC

– Time to arrange = 1 day

• Prepare post-incorporation documentation (e.g. officer appointments, share allotments and registers)

– Time to arrange = 1 to 4 days (depending on urgency)

• Legally capable of commencing business, entering contracts

Opening bank accounts

What are the options?

• “Hundreds” of banks in HK

• BUT, realistically only a handful really accessible and practical

• Typical commercial account types:

• Savings accounts

• Current accounts

• “Bills” accounts

• Currency options: All major currencies, and including RMB (“CNH”)

12

• Individuals or companies can now open RMB bank accounts in HK (“CNH” accounts)

• Limitation on individuals on how much they can buy and sell per day (RMB 20,000)

• No limitation on companies (subject to market liquidity)

• RMB can be bought for trade or non-trade purposes (exchange rates favour trade)

• To transfer RMB to trade supplier in China, recipient must have registered with China bank and Govt. authorities otherwise funds will be rejected

• Currently tendency is still to settle in USD

• Future will see more settlements in RMB

RMB (“CNH”) account options

13

Bank credit facilities and collateral requirements

• For new companies, loans must usually be secured by either;

- Standby Letter of Credit (SBLC) - Cash on deposit

(will lend 99% based on same currency)

• Same for issuing LC

• Credit card facilities secured by cash deposit (2 to 3

times credit limit)

• Debit cards are available without collateral (incl. UnionPay linked cards)

14

Taking profits out of Hong Kong companies

• No restrictions on payment of dividends, other than usual (from available profits)

• Interim and final dividends may be paid

• No currency or exchange controls in HK

• No Withholding Tax (WHT) on dividends paid to foreign shareholders

Using a Hong Kong Company to Trade with China/Asia

16

Specifically for businesses that:

• Are sourcing from Asia and reselling in their home country or third party destinations

• Are selling to large customers which accept direct shipment

• Want to centralize their sourcing function in Asia

• Need to have better control over quality

• Need to have better control over receipts and payments

• Want to sell on FOB Asia terms

Using a Hong Kong Trading Company to buy from China and sell to International Clients

17

Using a Hong Kong Trading Company to buy from China and sell to International Clients

Sale of goods

China Mfg

Company

HK Trading

Company

International

Buyers

Hong Kong Trading Company can be free of TAX

Order

Cash

Order

Cash

Flow of goods

Client/Partner

OS Holding

Company

18

Using a Hong Kong Trading Company to buy from

China and sell to International Clients

What are the benefits?:

• Potentially low or no taxes in Hong Kong

• Increased flexibility to sell FOB or ex-warehouse

• Free up capital financing on inventories

• Improved control by having HK-based service provider liaise with your vendors in Asia, in the same language and time zone

• Low risk as lease and staff overhead is borne by the service provider

• Growth through allowing clients to focus on growing their business rather than back-end infrastructure and staff

Using a Hong Kong Trading Company to buy from China and sell to International Clients

• Using the Hong Kong Trading Company

• Must negotiate, conclude and execute all sales and purchase agreements outside of Hong Kong

• Profits in Hong Kong company that are non-Hong Kong source may enjoy full tax exemption

• Bank accounts can be in Hong Kong

• Physical goods must not pass through Hong Kong customs

Using a Hong Kong Company to Invest in China

21

What are the common key issues for foreign

investors into China?

• Corruption

• IPR infringements

• Unfamiliar legal system

• Lack of transparency

• Non-convertible currency

• Internal management and financial control problems

• Cumbersome tax system

22

Typical HK Holding Company Model for China

PRC $ 100.00 Profit tax 25% $ (25.00) $ 75.00 PRC WHT 5% $ (3.75) $ 71.25 HK WHT 0% $ - _______ $ 71.25 =======

HK Holding Company

Foreign Investor

PRC WFOE/FICE

100%

100%

Advantages:

Changing shareholding in HK is a matter of

days

No capital gains tax in HK*

Extra layer of protection

Profits are ‘locked’ in Hong Kong instead of

PRC

23

What are the significant recent changes in China?

• Changes to regulations in relation to permanent establishment.

• Changes to regulations pertaining to holding companies and taxation of Representative Offices

• Amendments to capital gains rulings on sales of the parent company

• Substance requirements

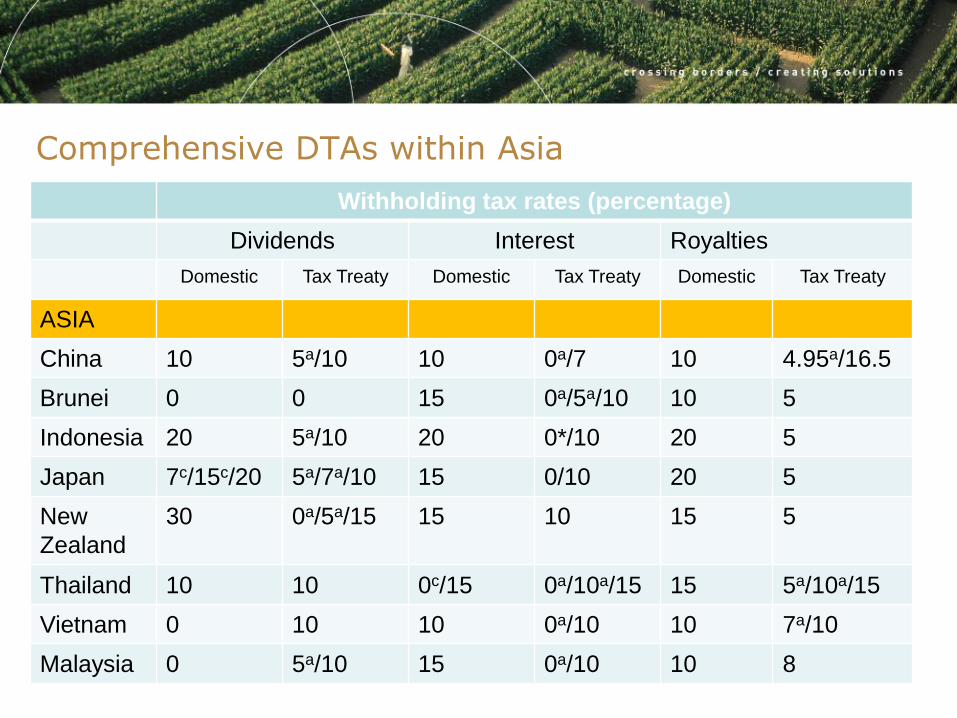

Substance for DTA Benefits

11

• Substance drivers

Substance Business Purpose

Physical and

economic substance

Operational alignment

Key personnel

Beneficial ownership

• Costs & benefits have to be analysed

25

Activities (substance) conducted in Hong Kong

• Receiving purchase invoices from suppliers

• Issuing sales invoices to (overseas) clients

• Operating bank accounts

• Receiving payments

• Opening and arranging of letters of credit

• Accounting & Reporting

• Arranging shipments, QC, logistics etc.

• Local staff on payroll / Local directors

• Physical presence in Hong Kong

Under the GAAR (2009), the benefits of any DTA with China will only be applicable if substance can be demonstrated!!!