Embed Size (px)

Citation preview

How Islamic Banking Becomes Safe in International Financial Crises

Presented By: Faraaz Shaul Hameed

Thrust of the Presentation

• First Global at a glance

• Sri Lanka as business center

• Introduction

• Issues & Challenges in the Islamic Finance World?

• Basics of islamic finance (IF)

• The financial crisis – what caused it?

• Why did the financial systems crumble?

• Islamic finance – An alternative

First Global at a glance

Recognized contributor to Islamic finance locally and globally

• First Global incorporated as public limited liability company in November 2007 in Colombo, Sri Lanka

• Received Aspiring Leader award in the global Islamic finance industry

• Instrumental in Abu Dhabi Commercial Bank’s venture into Islamic Banking, branded “Meethaq”

• Silver Award for Financial Related Services at Sri Lanka Malaysia Business Awards 2008,

• First Global with Investec Capital were joint lead arrangers for the first-ever Sri Lankan Sukuk

• In the Islamic Business & Finance Awards 2008 conducted by CPI Financial, First Global was a finalist in the categories Best Advisory Services and Best Investment House along with prominent players like Ernst & Young, McKenzie, and Unicorn Investment Bank

Our business lines

Sri Lanka as business center

Size 65,610 sq. km

Population 20.2 million

Per Capita GNP USD 1,969

Languages Sinhala, Tamil, English

Ethnic Groups Buddhists 77%Hindus 8% Muslims 9%

Christians 6%

Strategically located at crossroads of East and West

Business-friendly open economy with attractive and transparent investment laws offering the most business-friendly climate in South Asia

Highly literate labour force with high quality of life

“Peace dividend” as end of almost three decades of ethnic war enables public spending on infrastructure projects

Reawakening Programme aims to restore livelihoods through agriculture and irrigation projects

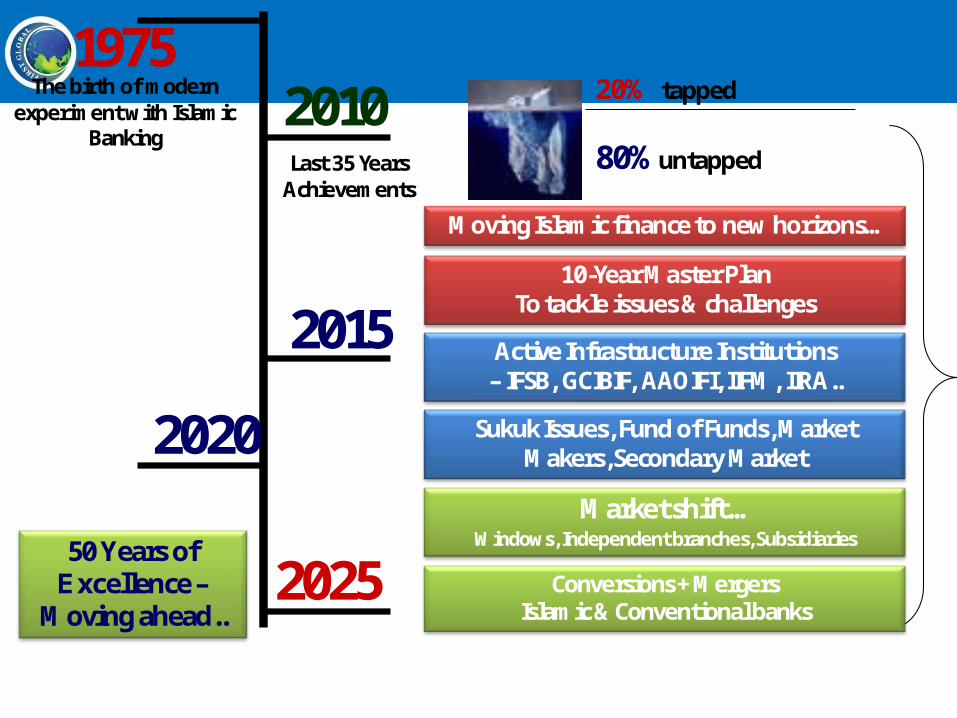

19752010

2025

Last 35 YearsAchievements

50 Years of Excellence –

Moving ahead..

The birth of modern experiment with Islamic

Banking

20% tapped

80% untapped

2015

2020

Moving Islamic finance to new horizons…

10-Year Master PlanTo tackle issues & challenges

Active Infrastructure Institutions – IFSB, GCIBIF, AAOIFI, IIFM, IIRA..

Sukuk Issues, Fund of Funds, Market Makers, Secondary Market

Market shift … Windows, Independent branches, Subsidiaries

Conversions + Mergers Islamic & Conventional banks

Issues & Challenges in the Islamic Finance World?

No International Islamic Money Market

Absence of/Underdeveloped Islamic Capital Market?

No Common Agreement on Shari'ah Issues?

No Lender of Last Resort?

No Harmonization of Islamic products or instruments?

Non-acceptance of standards, accounting practices by the industry players?

No secondary market for global Issues?

Integration of Islamic and International financial markets.

Emerging Stock Markets not fully compatible with Shari'ah

Innovation on Islamic Funds, still very slowNo uniform regulatory and legal framework

Educating the masses – lack of awareness

Islamic Banking & Finance is safe, given the global crisis- beyond economic and financial benefits…

Law & Justice

Ethics & Etiquettes Commerce & Economy

Politics & Governance

Social, moral & ethical life

Knowledge & learning

Hygiene

Human Rights & Relations

Moral Ethical Social Religious

and more….

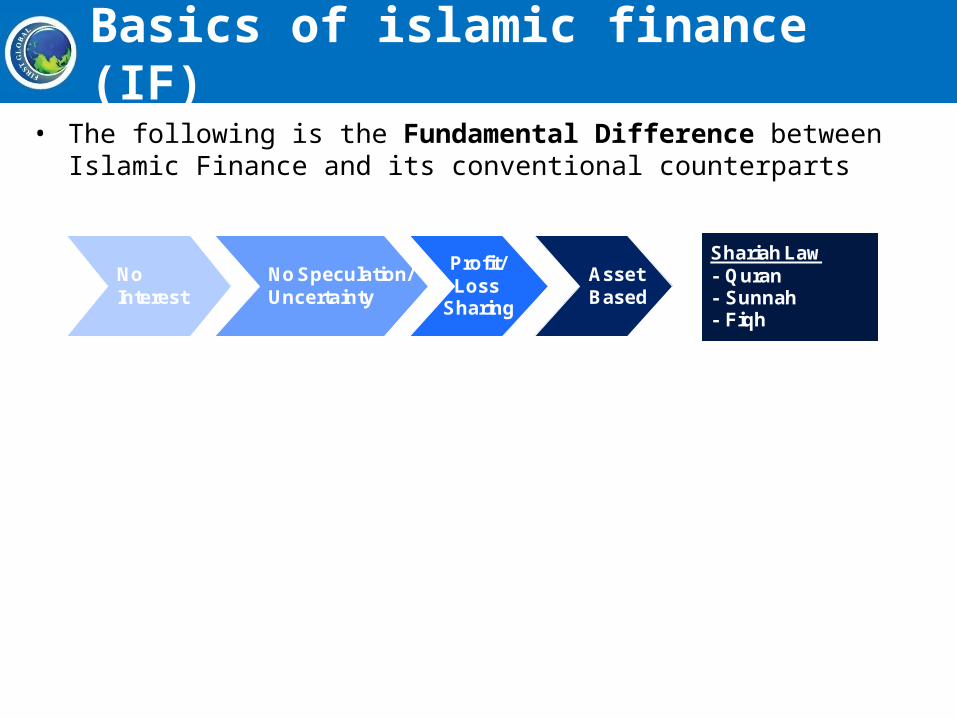

Basics of islamic finance (IF)• The following is the Fundamental Difference between Islamic Finance and its

conventional counterparts

No Interest

Asset Based

Profit/ Loss

Sharing

No Speculation/Uncertainty

Shariah Law- Quran- Sunnah- Fiqh

The financial crisis – what caused it?• Reckless lending fuelled by greed and irresponsible and excessive risk taking to

achieve higher profits

• Banks losing their vocation – traders rather than lenders

• Very fancy instruments developed with no substance other than a lot of hype and lack of transparency of its underlying value

The financial crisis – what caused it?• Rising defaults among mortgage borrowers

• Low interest rates causing a housing bubble that was bound to eventually burst

• Insufficient regulations of sub prime mortgage lending practices

• Insufficient monitoring of complex financial products and services, – Rating agencies and derivatives markets

• ‘Short selling’ – Selling assets that one does not own

• Rating Agencies giving very liberal ratings to instruments

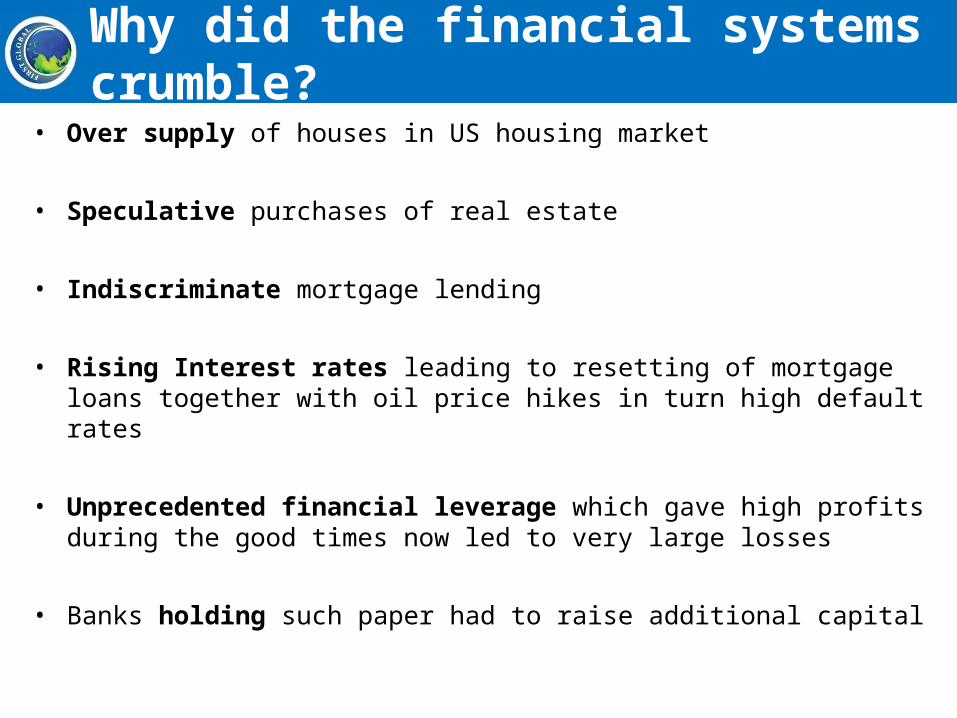

Why did the financial systems crumble?• Over supply of houses in US housing market

• Speculative purchases of real estate

• Indiscriminate mortgage lending

• Rising Interest rates leading to resetting of mortgage loans together with oil price hikes in turn high default rates

• Unprecedented financial leverage which gave high profits during the good times now led to very large losses

• Banks holding such paper had to raise additional capital

Islamic finance – An alternative• Basic principles

• Prohibitions

• How could Islamic finance have prevented the crisis

• Can Islamic finance come out of the mess?

• Islamic Finance Infrastructure Institutions (IFII’s)

• Successes of Islamic finance

Basic principles• Islamic economics and financial system is based on values, ideals and morals

• Ethical practices and fairness in all endeavors

• Prohibits economic and financial transactions that engage lying, gambling, cheating, monopoly, exploitation, greed, unfairness and unjustly taking people’s money

• Promotes participation in profit, loss and actual exchanges of money and assets

• No constant winner or loser; yet profit and loss is mutually shared

In a nutshell- Islamic Finance centers around Justice!!

Prohibitions – Riba/Usury (Interest)• Money is only a means of exchange – no intrinsic value

• Trading of debts/receivables prohibited

• Payment and receipt of interest is totally prohibited

• Interest bearing investments are prohibited

• Earnings must be by ‘profit sharing investments’ or ‘fee based’ returns

• Risk sharing - the risk taker is justly rewarded

Interest rate may be used as a means of calculating profit element or quantum of rent

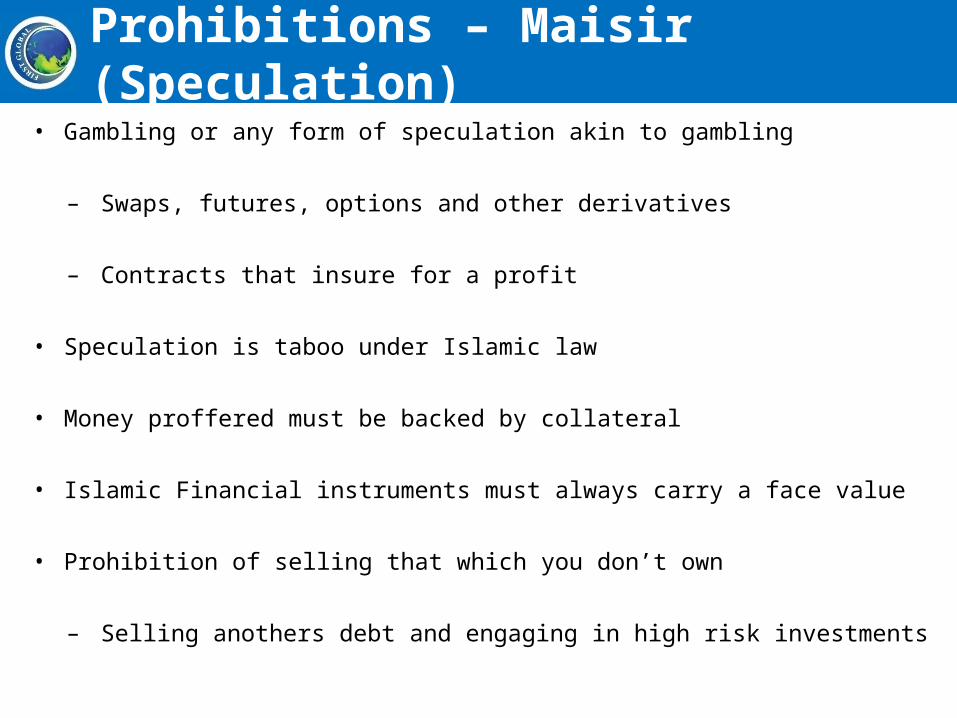

Prohibitions – Maisir (Speculation)• Gambling or any form of speculation akin to gambling

– Swaps, futures, options and other derivatives

– Contracts that insure for a profit

• Speculation is taboo under Islamic law

• Money proffered must be backed by collateral

• Islamic Financial instruments must always carry a face value

• Prohibition of selling that which you don’t own

– Selling anothers debt and engaging in high risk investments

Prohibitions – Gharar (Uncertainty)• Uncertainty as to fundamental terms in a contract

• Subject matter, price or time of delivery must be fixed in advance

• Conventional insurance prohibited

How could Islamic finance have prevented the crisis

• No lending on interest

• No selling on of mortgages or debts such as discounting promissory notes and cheques with postponed payments

• Financial derivatives are not permitted in Islamic finance

• Prohibits short selling - identified as a significant contributor to the global crisis

Can Islamic finance come out of the mess?It is believed that Islamic finance could emerge as a strong contender provided it overcomes the following challenges:

•Work towards eliminating the perception that Islamic finance is merely a interest bearing debt in disguise

•Aim for commonality in the application of Shari’ah to all Islamic finance products offered

– Currently many differences in the application of Shari’ah in different parts of the world

•Standardize Islamic finance products such that they look and feel the same wherever offered

Islamic Finance Infrastructure Institutions (IFII’s)

General Council for Islamic Banks and Financial Institutions

Islamic Finance Infrastructure Institutions (IFII’s)

• Must have ‘common thread’ to work together, whilst having ‘diversity’ in their mandates.

• Some of the areas looked into by these IFII’s are:

– Regulations…– Corporate Governance…– Capital Adequacy…– Risk & Liquidity Management…– Islamic Capital Market…– Accounting & Auditing Standards…– Rating…– Guidelines & Recommendations…– Awareness Programs…

• Otherwise:

– Loss of talents, skills, resources, etc.– Overlapping goals and objectives– Duplications and Repetitions– Deviation from the ‘common goal’

Successes of Islamic finance• Rapid growth of 15% - 20% annually

• US$ 4 Trillion worth market sector

• Crossed boundaries of Islamic world and spreading in non-Islamic countries

– UK, Germany, USA, France, Japan, Hong Kong, Thailand, etc.

• Dow Jones Islamic Market Indexes – Benchmarks for Islamic investment related categories have outperformed their non-Shari’ah compliant counterparts by 3 to 4 % in key indexes

• Osservatore Romano, Vatican’s official newspaper – ‘The ethical principles on which Islamic finance is based may bring banks closer to their clients and to the true spirit which should mark every financial service’

Thank You&

Jazaka Allah Khair

Mohamed Faraaz Shaul Hameed MBA(USA) BBA,PGDIBM-UK,AMABE-UK,DIBF-SL,DHRM-UK,DIBM-UK,DIM-UK

Mr. Faraaz is a Professional Banker for more than 20 years locally and internationally and embarked into Islamic Banking in 2007, and to date, he has gained a wealth of knowledge and experience, through his diverse positions held in various organizations* in Banking Operations, Management Consultancy, Business Management, Strategic Planning & Budgeting, Islamic Banking & Finance, Retail, Commercial and Investment Banking, Business Development, Compliance, Treasury training and career development etc.

Deputy CEO/Acting CEO

First Global Investments (Holdings)Sri Lanka

* Organizations• Commercial Bank Ltd, Sri Lanka (Best bank for last 11yeras-in Sri Lanka)

• Al - Rajhi Bank, Saudi Arabia• Seylan Bank, Sri lanka• Thomas Cook Ltd, India • Standard Chartered Bank , Sri Lanka•Habib Bank Ltd- Pakistan• Amana Bank , Sri Lanka• First Global Investments Holdings Limited, Sri Lanka

![[Aryeh Cohen, Shaul Magid] Beginning Again Toward(BookFi.org)](https://img.pdfslide.net/doc/110x75/553013364a7959a42c8b464b/aryeh-cohen-shaul-magid-beginning-again-towardbookfiorg.jpg)

![Shaul Hanany Eli Zeldov[3]](https://img.pdfslide.net/doc/110x75/62368975c63e1918235e705e/shaul-hanany-eli-zeldov3.jpg)