Embed Size (px)

Citation preview

lable at ScienceDirect

Energy xxx (2010) 1e15

Contents lists avai

Energy

journal homepage: www.elsevier .com/locate/energy

How much hope should we have for biofuels?q

Govinda R. Timilsina*, Ashish ShresthaEnvironment and Energy, Development Research Group, The World Bank, Washington, DC, United States

a r t i c l e i n f o

Article history:Received 13 January 2010Received in revised form12 August 2010Accepted 17 August 2010Available online xxx

Keywords:BiofuelsClimate changeFood crisis

q The views expressed in this paper are those ofnecessarily represent the World Bank and its affiliate* Corresponding author.

E-mail address: [email protected] (G.R. Ti1 Only liquid transport fuels are considered here, a

derived from biomass.2 For example, efforts to cultivate oil plants in China

in diesel fuel supply were abandoned after the drop i[2] the sugarcane based ethanol programs in Kenya aeighties but failed due to drought, poor infrastructure

0360-5442/$ e see front matter � 2010 Elsevier Ltd.doi:10.1016/j.energy.2010.08.023

Please cite this article in press as: Timilsinj.energy.2010.08.023

a b s t r a c t

This paper revisits the recent developments in biofuel markets and their economic, social and envi-ronmental impacts. Several countries have introduced mandates and targets for biofuel expansion.Production, international trade and investment have increased sharply in the last few years. However,some analysts linked biofuels to the 2007e2008 global food crisis. Existing studies diverge on themagnitude of the projected long-term impacts of biofuels on food prices and supply, with studies thatmodel only the agricultural sector showing higher impacts and studies that model the entire economyshowing relatively lower impacts. In terms of climate change mitigation, biofuels reduces GHG emissionsonly if GHG emissions related to land-use change are avoided. When biofuel production entailsconversion of forest to cropland, net reduction of GHG would not be realized for many years. Existingliterature does not favor the diversion of food for large-scale biofuels production, but the regulatedexpansion of biofuels in countries with surplus lands and a strong biofuel industry cannot be ruled out.Developments in non-food based or cellulosic (or second generation) biofuels may offer some hope, yetthey still compete with food supply through land use and are currently constrained by a number oftechnical and economic barriers.

� 2010 Elsevier Ltd. All rights reserved.

1. Introduction

The oil crises of the 1970s prompted interest in biofuels1 as analternative to fossil fuels for use in transportation in many coun-tries. Brazil accelerated its national ethanol programme (Proálcool)after oil prices peaked in 1979; the United States (US) launcheda corn-based ethanol program at almost the same time but ata smaller scale than Brazil [1]. Other countries, such as China, Kenyaand Zimbabwe, were also stirred into action by the oil crises, buttheir attempts to promote biofuels did not succeed [2,3].2 Subse-quent drops in oil prices evaporated much of the incentive andstalled the momentum to expand biofuels production in mostcountries, with the notable exception of Brazil. Issues related toenergy supply security, oil price volatility and climate changemitigation caused a resurgence of interest in biofuels, with rapid

the author only, and do notd organizations.

milsina).lthough there are other fuels

to insure against disruptionsn oil prices in the mid-1980snd Zimbabwe began in earlyand inconsistent policies [3].

All rights reserved.

a GR, Shrestha A, How mu

expansion in output, mandates and targets to guaranteeconsumption, and investment in the development of advancedbiofuel technologies. Declining production costs are making bio-fuels more competitive, especially when oil prices are high, but inalmost all cases, they still require subsidies to compete effectivelywith gasoline and diesel today.

Climate change consciousness has served as an important addi-tional driver to the embrace of biofuels because it assists climatechange mitigation efforts by displacing fossil fuel consumption.Given the enormous share of transportation in energy consumption,biofuels could contribute to the reduction of CO2 emissions from thetransport sector, but it could also lead to the conversion of forestlands and pastures to crop lands, thereby increasing CO2 emissionsfrom the agricultural sector. Whether or not biofuels cause netreduction of GHG emissions requires further investigation. More-over, the increasing scale of biofuel production and the escalation offoodprices in 2007 and 2008 created serious concerns regarding thepossible roleof biofuels in the2007e2008 food crisis that resulted inriots in many parts of the world.

A number of existing studies (e.g., [4e9]) have attempted topresent an overall picture of the current status of biofuels. Thesestudies, however, have focused on specific issues. For example,USAID [4] focuses on the sustainability of biofuels in Asia, whileBNDESandCGEE [5] discuss theBrazilian experiencewith ethanol indetail. FAO [6] concentrates on the relationship of biofuelswith foodprices; similarly, Ajanovic [7] investigates the impact of the recent

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e152

increase in biofuels production on feedstock prices. On the otherhand, OECD [8] assesses the impact of biofuel support policies,whereas Ajanovic and Haas [9] assess the economic prospects of 1stgeneration biofuels in Europe given current policy conditions. Asuccinct but broad assessment of biofuels is still lacking, particularlyaddressing some crucial issues, such as the promise of biofuels, theireconomics, investment trends and potential economic, social andenvironmental impacts. This paper aims to fill this gap.

This paper is organized as follows. Section 2 discusses the statusof biofuel technologies, followed by a look at production,consumption and trade patterns in recent years in Section 3. It thenreviews biofuel policies and mandates around the world in Section4. The cost of production and investment trends are presented inSection 5. Section 6 discusses the impact of biofuels on food prices,followed by a presentation of environmental impacts in Section 7.Section 8 examines the impact of biofuels on land use, and finally,we draw key conclusions in Section 9.

2. Technologies

Based on the feedstock used for production and the technolo-gies used to convert that feedstock into fuel, biofuel technologiescan be classified into two groups: first- and second-generationbiofuels. Technologies that normally utilize the sugar or starchportion of plants (e.g., sugarcane, sugar beet cereals and cassava) asfeedstock to produce ethanol and those utilizing oilseed crops (e.g.,rapeseed, sunflower, soybean and palm oil) to produce biodieselare known as first-generation biofuels [10,11]. On the other hand,biofuels produced using technologies that convert lignocellulosicbiomass (e.g., agricultural and forest residues) are called second-generation biofuels, as are biofuels produced from advancedfeedstock (e.g., jatropha and micro-algae) [1]. Whereas first-generation biofuels have already been in commercial productionfor several years in many countries, second-generation technolo-gies have yet to begin commercial production, with some excep-tions (e.g., Jatropha in India).3 While first-generation biofuelsdirectly compete with food supply, second generation can produceboth food and fuel together unless non-food crops4 are preferred.Because cellulosic biomass is the most abundant biological mate-rial on earth, the successful development of commercially viablesecond-generation biofuels could greatly enlarge the volume andvariety of feedstocks [6]. However, although the cost of cellulosicfeedstock is lower than that of first-generation feedstocks, cellu-losic biomass ismore difficult to break down than starch, sugar andoils, and the technology to convert it into liquid fuels is moreexpensive.

First-generation ethanol is produced from sugars and starches.Simple sugars in a variety of sugar crops are extracted and thenyeast-fermented, and the resulting wine distilled into ethanol.Starches require an additional step e first they are converted intosimple sugars through an enzymatic process under high heat,which uses additional energy and increases the cost of production[5]. Ethanol is typically blended with gasoline, and has a higheroctane value than gasoline but produces about 70% less energy.Biodiesel is derived from lipids and is produced by mixing the oilwith an alcohol like methanol or ethanol through the chemicalprocess of transesterification. The biodiesel, or fatty-acid methylester (FAME), made from this process has 88e95% of the energy

3 Some of the literature refers to more advanced technologies, such as thoseproducing biofuels from micro-algae, as third generation biofuels [13]. This study,however, treats these technologies as second-generation biofuels.

4 Non-food crops such as switchgrass, miscanthus, jatropha compete with foodsupply through land-use change.

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

content of conventional diesel, but better lubricity and a highercetane value, and so can deliver fuel economy close to that ofconventional diesel.

Biodiesel, however, is not without its problems. Exposure to air,heat, light, water and some metals can all cause it to degrade;a common symptom of which is plugged filters in vehicles [12].Since biodiesel has a significantly higher cloud point/pour pointthan petroleum diesel, it can cloud and gel in cold temperatures,leading to difficulty in starting vehicles in winter conditions. Coldweather fuel filter plugging has also been known to occur withbiodiesel blends as wax and water present in it can precipitate, andglycerin and sterol glycosides in it form particulates and drop out ofthe solution faster, in cold temperatures. Furthermore, the perfor-mance of advanced emission control equipment such as dieselparticle filters and NOx emission control catalysts with biodiesel isnot certain, and questions persist about their long-term durabilitywhen used with biodiesel [14]. Infrastructure such as storage tanks,associated piping and leak detectors, and fuel dispensers and hosesfor diesel fuel are considered to be compatible with blends of up to5% biodiesel, but the lack of third party certification for higherbiodiesel blends remains an impediment to the expansion of thebiodiesel market.

Second-generation ethanol is produced through the conversionof lignocellulosic biomass. In contrast to the first-generationethanol, which is produced from the sugar or starch fraction of theplant (i.e., a small percentage of the total mass), lignocellulosicconversion processes would enable full use of the lignocellulosicmaterial found in a range of biomass sources, such as waste seedhusks and stalks (making use of plant residues not needed for foodproduction) and fast-growing grasses and trees [15]. Lignocellulosicbiomass is comprised of polysaccharides (cellulose and hemi-cellulose), which are converted into sugars through hydrolysis orchemical (or combined) processes; the sugars are then fermentedinto ethanol using existing fermentation technology.

The other main approach to converting lignocellulosic biomassinto biofuels entails the gasification of the feedstock to producesynthetic gas (syngas) e a mixture of carbon monoxide, hydrogenand other compounds [16]. Then, the syngas can be converted toa variety of fuels, such as synthetic diesel, through FischereTropschsynthesis, the same technology used in gas-to-liquids and coal-to-liquids plants. Such biomass-to-liquid (BTL) production can alsoprocess lignin, which comprises about one-third of plant solidmatter, and can thus achievehigher liquid yields than lignocellulosicethanol production via hydrolysis [1]. Lignocellulosic ethanol andFischereTropsch biodiesel production is, for the most part, at thepilot and demonstration stages, but some commercial facilities areunder construction, and there is a commercial scale lignocellulosicethanol plant already operational in Sarpsborg, Norway [17].

An alternative process to esterification for producing renewablediesel fuel is the hydrotreatment of vegetable oils or animal fats.Chemically hydrotreated vegetable oils (HVOs) are mixtures ofparaffinic hydrocarbons that are free of sulfur and aromatics,feature a high cetane number and other properties similar to bio-diesel produced via FischereTropsch (FT) synthesis [18]. HVOs,however, address some of the known problems of fatty-acid methylester, namely the cold start issue as well as compatibility withexisting infrastructure, engines and exhaust aftertreatmentdevices. The first commercial scale HVO plant with a capacity of170,000 tons per year went on line in 2007 at Neste Oil’s Porvoo oilrefinery in Finland, followed by another plant of the same capacityat that location in 2009. HVO plants in Singapore and Rotterdam,with a capacity of 800,000 each, are planned to begin production in2011 [19]. Based on information available as of February 2010, totalplanned capacity for advanced biofuels worldwide in 2013 is esti-mated at 1.38 billion gallons [20].

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

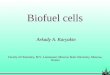

World Ethanol Production

Fig. 1. World ethanol production. REN21 [25, 26, 27, 28, 138]; Renewable Fuels Asso-ciation [29]

5 Exact ethanol trade statistics are difficult to gather since fuel and non-fuelethanol typically share the same tariff and are reported together [8]. The share ofnon-fuel ethanol in the international trade in ethanol is estimated to have droppedfrom 75% at the turn of the century to around 50e60% in recent years. Ethanol tradestatistics here refer to the total of fuel and non-fuel ethanol.

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e15 3

Biofuels can also be produced from second-generation feed-stocks. Jatropha, an oilseed bush that thrives onmarginal and semi-arid land, has attracted much attention as a feedstock for large-scale biodiesel production in India [21], where researchers projectthat up to 15 billion liters of biodiesel may be produced from thecultivation of jatropha on 11 million hectares of wasteland by 2012[22]. The use of micro-algae for biodiesel production appears to beanother very promising future technology [13] since 80% or more ofthe dry weight of algae biomass, compared to 5% for some foodcrops, may be retrieved as oil for some species [23]. They also createlittle pressure on arable land because they can be cultivated ina wide variety of conditions, even in salt water and water frompolluted aquifers [24].

3. Production, consumption and trade

3.1. Production and consumption

Global production of fuel ethanol grew from 30.8 billion liters in2004 to 76 billion liters in 2009 at an average annual growth rate of20%. The two leading producers, the US and Brazil, accounted forabout 88% of the total in 2009 (see Fig. 1).

Table 1 presents biofuels production by country for the 2004e2009 period. In 2006, the US surpassed Brazil, the longtime leader,to become the leading fuel ethanol producer in the world byproducing over 18 billion liters (20% more than the previous year)[27]. Aside from the US and Brazil, significant production increasesare found in France, China and Canada in recent years. Australia,Germany, Spain Colombia, India, Jamaica, Malawi, Poland, SouthAfrica, Sweden, Thailand, and Zambia also engage in the commer-cial production of ethanol.

Although total production of biodiesel around the worldremains small in comparison to ethanol, its growth is higher thanthat of ethanol, at an average annual growth rate of approximately50% between 2004 and 2009. This growth from 2.3 billion liters in2004 to 17 billion liters in 2009 is illustrated in Fig. 2. Germany,France and Italy are the biggest producers in the EU, but the USpassed France to become the second biggest producer of biodieselafter Germany in 2006.

Worldwide biodiesel production grew by 43% between 2005and 2007 despite slow growth within the EU, the traditional centerof biodiesel production [8]. This growth in other countries, espe-cially the US, led to a decline in the EU’s share of global biodieselproduction, which had been more than 90% until 2004 to less than60% in 2007 [30,36]. In recent years, some countries outside Europeand the US have begun to produce biodiesel. For example, Brazil

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

opened its first biodiesel plant, which uses a mixture of vegetableoil and sewage as feedstock, in March 2005 [11]. Indonesia andMalaysia have recently begun producing biodiesel for the Europeanmarket, and Argentina started biodiesel production in 2007 [8].

Despite this tremendous growth in biofuel production, the shareof biofuels in total transport fuel demand was above 2% in 2004 injust three countries e Brazil, Cuba and Sweden [16], and globaloutput accounted for approximately 1% of total road transport fuelconsumption in 2005 [15]. In 2007, ethanol production still onlyamounted to about 4% of the global gasoline consumption of 1300billion liters [27].

3.2. Trade

Global trade in biofuels relative to production remains modest;only about one-tenth of total biofuel production by volume is tradedinternationally [37]. Global trade in fuel ethanol is estimated at about3 billion liters per year in 2006 and 2007, compared to less than onebillion liters in 2000 [38]. Even asUS ethanol production increased by20 percent in 2006, with dozens of new production plants becomingoperational, blendingmandates led to ethanol imports increasing sixtimes to about 2.3 billion liters [27]. The US, the world’s largestethanol importer, receivedmore than half of its ethanol imports fromBrazil, the world’s leading exporter, at 3.5 billion liters annually.5

Brazil was responsible for about half of the ethanol exports to theEU, the second largest importer of ethanol in 2006. China, the secondlargest exporter of ethanol at 1 billion liters annually, exports mainlyto Japan, South Korea and other Asian countries [8].

About 12%, or 1.3 billion liters, of total biodiesel production in2007 was internationally traded. The EU, at more than 1.1 billionliters per year, is by far the largest importer, while Indonesia andMalaysia as the main exporters, combining to export about 800million liters [37]. While the US also appears to be a major biodieseltrader, this was in fact due to the importing of biodiesel to beblended with small quantities of conventional diesel for export toEurope in order to take advantage of a tax credit [31]. The loopholehas since been closed.

Since some major players, namely the US and the EU, havetargeted biofuel production for domestic consumption, not manycountries beside Brazil have the ability to be large exporters ofethanol or other biofuels. South and Central America, and Africato a lesser extent, possess the greatest differential betweentechnical production potential for biofuels and expecteddomestic transport energy demand, and so countries in theseregions have the most potential to export to North America,Europe and Asia [15]. Yet trade opportunities are furtherrestricted by the high tariffs many countries, such as India, haveestablished to protect their agriculture and biofuel industries.While import tariffs are relatively low in OECD countries, highsubsidies serve as a barrier to lower-cost foreign exporters andprotect domestic producers. In other cases, trade in biofuels islimited by regulatory measures, such as the EU’s sustainabilitycriteria for palm-oil imports from Malaysia and Indonesia, andThailand’s ban on palm-oil imports [4].

Global trade in biofuels is expected to increase due to compar-ative advantage of some countries to others to produce biofuels,such as favorable climate, lower labor costs and the greater avail-ability of land. Girard and Fallot [39] show that tropical countries

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

Table 1Biofuel production.

Country Fuel ethanol Biodiesel

Major feedstock Production (billion liters) Major feedstock Production (billion liters)

2004 2005 2006 2007 2008 2009 2004 2005 2006 2007 2008 2009

US Corn 13 15 18.3 24.6 34 41 Soybean 0.11 0.36 0.99 1.93 2.69 2.1Brazil Sugarcane 15 15 17.5 19 27 26 Soybean 0.07 0.4 1.2 1.6Germany Wheat 0.02 0.2 0.5 0.5 0.8 Rapeseed 1.18 1.9 3.02 3.28 3.2 2.6France Sugar beet, wheat 0.1 0.15 0.25 1.2 0.9 Rapeseed 0.4 0.56 0.84 0.99 2.06 2.6China Corn, sugarcane 2 1 1 1.8 1.9 2.1 Soybean, rapeseed 0.07 0.1 0.4Argentina Sugarcane e e e 0.02 e e Soybean 0.21 0.85 1.4Italy Cereals e e 0.13 0.13 0.1 Oilseeds 0.36 0.45 0.51 0.41 0.68 0.4Spain Barley, Wheat 0.2 0.3 0.4 0.4 0.4 Oilseeds 0.01 0.08 0.11 0.19 0.24 0.6India Sugarcane, wheat e 0.3 0.3 0.2 0.3 0.2 Soybean, rapeseed 0.03 0.02 0.1Canada Wheat 0.2 0.2 0.2 0.8 0.9 1.1 Oilseeds 0.1 0.05 0.1 0.1Poland Rye e 0.05 0.12 0.12 Rapeseed 0.11 0.13 0.09 0.31Czech Republic Sugar beet e 0.15 0.02 e Rapeseed 0.07 0.15 0.12 0.07 0.12Colombia Sugarcane e 0.2 0.2 0.3 0.3 0.3 Oil palm e e e e 0.1 0.2Sweden Wheat e 0.2 0.14 0.14 Rapeseed 0.002 0.001 0.01 0.07 0.11Malaysia e e e e e Oil palm 0.19 0.14 0.45 0.48UK e e e e e 0.2 Rapeseed 0.01 0.06 0.22 0.17 0.22 0.5Denmark Wheat e 0.1 e e Oilseeds 0.08 0.08 0.09 0.1 0.15Austria Wheat e 0.1 e e 0.1 Oilseeds 0.06 0.1 0.14 0.3 0.24 0.2Slovakia Corn e 0.1 e e Oilseeds 0.02 0.09 0.09 0.05 0.17Thailand Sugarcane, cassava 0.2 e e 0.3 0.3 0.4 Oil palm 0.4 0.6Australia Sugarcane 0.07 e e 0.1 e e e e e e e

Belgium Wheat 0.2 Rapeseed 0.3EU Various e e e 2.16 e e e e e e e

World total 31 33 39 49.6 67 76 2.3 4.3 6.9 9.5 14.7 17

Note: Ethanol figures do not include ETBE, a mixture of ethanol and isobutylene (petrochemical) used in low-concentration gasoline blends up to about 8e10% in fuels in partsof Europe, particularly France and Spain.Source: REN21 [25e28,135]; Renewable Fuels Association [29]; EBB [30]; EIA [31]; Pinzon [32]; Barros [33]; Hoh [34]; Joseph [35].

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e154

have two to three times higher productivity when water scarcity isnot a factor. Johnston and Holloway [40] find that Malaysia andIndonesia are the two countries with the highest absolute biodieselproduction potential in the world (other developing countries, i.e.,Argentina, Brazil and the Philippines, also feature in the top ten)and also the lowest average production costs per liter. Moreover,many countries may not be able to meet their biofuel targets andmandates with domestic production alone [15].

4. Biofuel policies and mandates

Biofuel programs have proliferated around the world in recentyears, whether motivated by a desire to bolster agriculturalindustries or achieve energy security or reduce GHG emissions orimprove urban air quality. Table 2 lists biofuels blending mandatesand timetables for their implementation (where available) aroundthe world.

World Biodiesel Production

Fig. 2. World biodiesel production. REN21 [27, 138]; EBB [30]; EIA [31]; Pinzon [32];Barros [33]; Hoh [34]; Joseph [35]

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

The growth of ethanol output in the US, derived mainly fromcorn (maize), has been driven by fiscal incentives (e.g., tax,subsidies) and regulatory instruments (e.g., biofuel blendingmandates) [41]. The Energy Policy Act of 2005 establisheda Renewable Fuel Standard (RFS) program, which increases thebiofuel mandate to 36 billion gallons by 2022 from 9 billion gallonsin 2008 [31]. The Farm Bill of 2008 introduced a tax credit of $1.01per gallon for cellulosic ethanol starting from 2009 [42]. The pre-existing tax credit for biodiesel of $1.00 was also extended (to theend of 2009).

In Brazil, the government mandates 20e25% ethanol blends inall regular gasoline sales and the use of ethanol in governmentvehicles. It also promotes the sale of flexible-fuel vehicles, whichrepresent 85% of all auto sales in Brazil [27]. While ethanolproduction in Brazil was supported through price guarantees andsubsidies, as well as public loans and state-guaranteed private bankloans, during the industry’s development, it no longer receives anydirect government subsidies [1]. However, it is still supportedthrough policies such as the ban on diesel-powered personalvehicles and one of the highest import tariffs on gasoline in theworld.

The EU Biofuels Directive of 2003 targets a 5.75% share of bio-fuels in transport energy by 2010, and 10% by 2020, promptingrapid growth in the production of biofuels [4]. Despite its higherproduction costs, biodiesel is sold for $0.18e$0.24 less per liter thanconventional diesel in Germany due to the $0.59 tax exemption itenjoys there [43].

China has set a biofuel production target of 12 million tons6 forthe year 2020, and it is projected that, depending on the types offeedstock, 5e10% of the total cultivated land in China would beneeded to meet that target [44]. Thailand has established an

6 All mentions of tons refer to metric tons.

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

Table 2Biofuels targets and blending mandates.

Country Biofuel targets Blending mandates

Australia 350 million liters of biofuels by 2010 E2 in New South Wales, increasing to E10 by 2011; E5 in Queensland by 2010Argentina E5 and B5 by 2010Bolivia B2.5 by 2007 and B20 by 2015Brazil E22eE25 existing (slight variation over time); B3 by 2008 and B5 by 2013Canada E5 by 2010 and B2 by 2012; E7.5 in Saskatchewan and Manitoba;

E5 by 2007 in OntarioChile E5 and B5 by 2008 (voluntary)China 12 million metric tons

of biodiesel by the year 2020E10 in 9 provinces

Colombia E10 and B10 existingDominican Republic E15 and B2 by 2015Germany 5.75% share of biofuels in transport

by 2010; 10% by 2020E5.25 and B5.25 in 2009; E6.25 and B6.25 from 2010 through 2014

India E5 by 2008 and E20 by 2018; E10 in 13 states/territoriesa

Italy 5.75% share of biofuels in transportby 2010; 10% by 2020

E1 and B1

Jamaica E10 by 2009Japan 20% of total oil demand met with biofuels

by 2030; 500 million liters by 2010Korea B3 by 2012Malaysia B5 by 2008New Zealand 3.4% total biofuels by 2012Paraguay B1 by 2007, B3 by 2008, and B5 by 2009; E18 or higher (existing)Peru B2 in 2009; B5 by 2011; E7.8 by 2010Philippines B1 and E5 by 2008; B2 and E10 by 2011South Africa E8eE10 and B2eB5 (proposed)Thailand 3 percent biodiesel share by 2011; 8.5 million liters

of biodiesel production by 2012E10 by 2007 and B10 by 2012

United Kingdom E2.5/B2.5 by 2008; E5/B5 by 2010United States 130 billion liters/year of biofuels nationally

by 2022; 3.4 billion liters/year by 2017 PennsylvaniaE10 in Iowa, Hawaii, Missouri, and Montana; E20 in Minnesota; B5 in New Mexico;E2 and B2 in Louisiana and Washington State;

Uruguay E5 by 2014; B2 from 2008e2011 and B5 by 2012

Source: REN21 [28]; USAID [4]; BNDES and CGEE [5]; Worldwatch [1].a Poor sugarcane yields in 2003e2004 forced India to import ethanol to meet state blending targets. It has postponed broader targets until adequate domestic supplies

become available.

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e15 5

ethanol programwith a target of replacing all conventional gasolinewith E10 gasohol (gasoline containing 10% by volume of ethanol) by2012 [45]. Other Asian countries such as India, Indonesia, Malaysia,the Philippines, Vietnam and Japan have all introduced blendingtargets, fiscal incentives, import tariffs or some combinationthereof to promote biofuels, some of destined to be exported toEurope to meet the EU’s ambitious targets [4].

5. Cost and investment

5.1. Biofuel production cost

Aside from sugarcane based ethanol in Brazil, biofuels are notpresently competitive without substantial government support ifoil prices are below US$70 per barrel [15]. As more than half of theproduction costs of biofuels are dependent on the price of thefeedstock, reductions in cost are closely tied to the prices of feed-stock commodities.

5.1.1. Cost of ethanolAccording to the IEA [16], the costs of ethanol production in new

plants in Brazil are the lowest in the world at $0.20 per liter ($0.30per liter of gasoline equivalent). This subsequently declined evenfurther to $0.18 per liter [1]. As compared to the cost of sugarcanebased ethanol in Brazil, ethanol from grains costs 50% more in theUS and a 100% more in the EU. Transportation, and blending anddistribution costs can add some $0.20 per liter to the retail price.Meanwhile, production costs for ethanol (previously from wheat,but from sweet sorghum and cassava going forward) in China arebetween $0.28 and $0.46 per liter, depending on the price of the

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

feedstock, and sugar-based ethanol production costs in India arearound $0.44 per liter [1]. The IEA [16] foresees a reduction of one-third in the cost of ethanol by 2030 due to technologicalimprovements and lower costs of feedstock. However, theincreasing demand for ethanol due to mandates and targets, theimpacts of the fuel vs. food debate on its supply, and recent trendsof feedstock prices imply that the cost of ethanol may not dropdown. Moreover, unless the price of oil is high, production ofethanol may not be competitive without substantial level ofsubsidies.

The cost of cellulosic ethanol, which is still in demonstrationstage, is high, typically about typically about $1.00 per liter ona gasoline-equivalent basis. Given the speed of technologicaldevelopments in an emerging field and uncertainty over the long-run costs of feedstock, projections of the future costs of lignocel-lulosic ethanol differ substantially, but the IEA [46] notes that thecosts are anticipated to drop to $0.50 per liter in the long term.Significant technological progress will be necessary to make thishappen: achievement of better ethanol concentrations before thedistillation, lower costs for enhanced enzymes (resulting frombiotechnological research) and improved separation techniques.There are some indications that this may be feasible. For example,Brazil’s leading manufacturer of sugar and biofuel equipment,Dedini SA, announced in May 2007 that it had devised a means toproduce cellulosic ethanol from bagasse on an industrial scale atbelow $0.41 per liter on a gasoline-equivalent basis [15]. Anotherpath to competitive lignocellulosic ethanol may be come from thegeneration of valuable co-products in biorefinery, which could cutthe costs of feedstock. Hamelinck and Faaij [47] estimate produc-tion costs of ethanol from the hydrolysis of cellulosic biomass to be

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e156

$0.63 per liter in the following 5e8 years, $0.37 per liter in 8e12years, and $0.25 per liter in 13e20 years.7

5.1.2. Cost of biodieselGenerally, production of biodiesel from palm-oil costs around

$0.70 per liter, whereas biodiesel produced from rapeseed oil maycost up to $1.00 per liter, with soybean diesel in between [16]. Thecost of biodiesel production in China, mainly from used cooking oil,ranges from $0.21 to $0.42 [1]. The IEA [16] anticipates a decline inbiodiesel production costs of more than 30% in the US and EUbetween 2005 and 2030 along with a decline of feedstock costs.However, the prices of biodiesel feedstocks have been moving inthe other direction for the most part since the IEA’s estimates wereproduced.

Substantial research is also being dedicated to lowering thecosts of producing diesel from biomass using the FischereTropschprocess, most of which concentrate on the use of heat or chemicals,rather than microbes, to break down the biomass. Although theFischereTropsch process permits higher yields per hectare thancurrent biodiesel production, production cost for large-scale plantsis estimated to be about $0.90 per liter of diesel equivalent in thenear term and expected to fall to $0.70e0.80 in the medium term[46]. While micro-algae is projected as a future source for biodiesel,production cost is still extremely high, in the range of US$2eUS$22per liter [48]. Making algae a viable commercial option will requirefurther improvements in genetic and metabolic engineering toproduce higher yielding and hardier strains. Although economies ofscale in production could lower the cost, it is challenging toincrease the yield to a level that ensures micro-algae based bio-diesel is competitive with other biodiesel technologies. Neverthe-less, the feasibility of biodiesel production frommicro-algae can beexpedited if large-scale production facilities can be integrated withother processes, such as wastewater treatment and utilization ofcarbon dioxide from power plants [4].

5.2. Investments in capacity

New financial investment in biofuels, i.e., total investment lesscorporate and government research and development and small-scale projects, amounted to a $18 billion in 2008, and an emergingcomponent of venture capital investment went to cellulosicethanol, estimated at more than $350 million in 2008 [28,136].However, financial investment biofuels declined dramatically to $7billion in 2009, with prospective project developers struggling tosecure credit and investors reluctant to invest in a sector recentlyplagued by high feedstock prices and over-capacity in 2007e2008.The single largest investment was Nestle’s V670 million biodieselplant near Rotterdam, Netherlands.

Biofuels production plants under construction and announcedconstruction through 2008 were valued in excess of $2.5 billion inthe United States, $3 billion in Brazil, and $1.5 billion in France [27].In the case of traditional or first-generation ethanol, North Americaand Brazil exhibit rapid expansion in capacity. In the US,construction of 12 new ethanol plants was completed in 2004,raising the total to more than 80. Construction was begun on anadditional 16 in the same year, representing production capacity of2.6 billion liters per year and an estimated $1 billion of investment[25]. At the end of 2005, 95 operation ethanol plants were inexistence in the USwith a capacity of 16.4 billion liters per year, andconstruction of 35 new plants ($2.5 billion of investment) andexpansion of 9 existing ones, i.e., additional capacity of 8 billionliters per year, were underway in 2006 [26]. Most of these are dry

7 Production costs per liter of ethanol, not per liter of gasoline equivalent.

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

mills that produce ethanol as the primary output as opposed to wetmills, which are designed to manufacture products like maize oil,syrup and animal feed along with ethanol [16]. The ethanolindustry association in the US estimates construction costs in 2005as follows: $0.40 per liter for a new dry mill plant, and $0.27 perliter for expansion of an existing plant [49].

Canada has six new ethanol plants with capacity of 0.7 billionliters/year were under construction, while in Brazil, 80 new sugar-mills/distilleries were licensed in 2005 to augment the 300 alreadyin operation, as part of a national plan to raise sugarcane produc-tion by 40 percent by 2009 [26]. Most of the refineries in Brazil arein the center and south of the country, where sugar yields arehighest, and about 250 separate producers, mostly grouped intotwo associations comprising 70% of the market [16]. The averagecapacity of ethanol plants in the US is three times greater than theaverage capacity of those in Brazil; the largest corn dry-millingplant in the US produces 416 million liters per year whereas thelargest plant in Brazil produces 328 million liters per year bycrushing sugarcane [1]. While theremay be a number of reasons forthe difference in capacities, chief among them is the fact that har-vested corn can be stored for an extended period of time, unlikesugarcane, which needs to be processed soon after harvest so thatthe sugar will not deteriorate. Elsewhere, China reversed its deci-sion to invest in facilities to produce more ethanol from grain onaccount of its food policies in 2006, and has instead targeted cas-sava and sweet potatoes as feedstocks for future increases inethanol production [50]. South Africa, which exports ethanol to theEU, is building a pilot 500-kilolitre per year ethanol plant [16].

Like the fuel ethanol industry, the biodiesel industry also grewrapidly (more than three fold in the EU between 2004 and 2006),adding four billion liters/year and an estimated $1.2 billion ofinvestment, to bring operating capacity to over 6 billion liters peryear. Biodiesel Production, a part of the German group Sauter,invested 50million euros in 2004 to establish a biodiesel productionplant with a capacity of 250,000 tons in Cartegena, Spain, whileIbserol, a subsidiary of the German food group Nutas, invested 25million euros in a biodiesel facility (100 ton capacity) that was tobegin production in Portugal in 2005 [25]. Biodiesel productioncapacity is also rising swiftly in the United States. The 44 new plantsunder construction in 2005 were expected to double the existingcapacity of 1.3 billion liters of the 53 operating plants [26]. Brazil isusing soybean oil as a feedstock to expand production of biodiesel inthe Center West to replace petrolediesel traditionally trucked infromthecoast, andArgentina is expandingbiodieselproduction fromsoybean oil for the exportmarket, while Canada is using rapeseed oilto increase biodiesel production in the Prairie Provinces [50].

In Asia, Malaysia aims to capture 10% of the global biodieselmarket by 2010 [27]. However, of the 92 licenses were approved forbiodiesel facilities in 2006 and 2007, only 14 facilities were built, ofwhich eight are now operating, producing at less than 10 percent oftotal capacitydue to thehigh costofpalmoil [51]. Similarly, Indonesiaplanned to expand palm-oil plantations by 1.5 million hectares by2008 for a total of 7million hectares under palm cultivation. Existingbiodiesel facilities and those under construction in Chinawill deliver3% of China’s expected diesel consumption by 2010, i.e., annualcapacity of about 2 million tons [1]. However, RaboBank has warnedof a surplus capacity of 1 million MT in Asia by 2010 [4].

Investments in jatropha plantations are surging in Africa, India,Indonesia and China [52]. India’s stated target of 20 percent biofuelby 2011 will demand 13 million hectares of jatropha plantations,and BP is funding a $9.4 million project there to investigate itspotential. Indonesia plans to plant 1.5 million hectares of jatrophaby 2010, while the Chinese forestry administration, in March 2007,announced its intention to develop 13million hectares of treeswithhigh oil content, including jatropha.

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

Table 3Impacts of increased biofuel production on food prices.

Study Coverage & key assumptions Key impacts of biofuels on food prices

Baier et al. [63] 24 months ending June 2008; historical cropprice elasticities from academic literature;bivariate regression estimates of indirect effects

Global biofuel production growth responsible for 17%, 14%and 100% of the rises in corn, soybean and sugar prices,respectively, and 12% of the rise in the IMF’s food price index.

Banse et al. [64] 2001e2010; Scenarios: reference(without mandatory biofuel blending),EU 5.75% mandatory blending, EU 11.5% mandatory blending

Price change under reference scenario, 5.75% blending,and 11.5% blending, respectively:Cereals: �4.5%, �1.75%, þ2.5%; Oilseeds: �1.5%, þ2%, þ8.5%;Sugar: �4%, �1.5%, þ5.75%

Lazear [65] 12 months ending March 2008 US ethanol production increase accounted for 20%of the rise in corn prices.

IMF [66] Estimated range covers the plausible valuesfor the price elasticity of demand

Range of 25e45% for the share of the rise in corn prices attributable to ethanolproduction increase in the US.

Collins [62] 2006/07e2008/09; Two scenarios considered:(1) normal and (2) restricted,with price inelastic market demand and supply

Under the normal scenario, the increasein ethanol production accounted for 30%of the rise in corn price; Under the restricted scenario,ethanol could account for 60%of the expected increase in corn prices.

Glauber [67] 12 months ending April 2008 Increase in US biofuels accounted for about 25 percentof the rise in corn prices; US biofuels production accountsfor about 10 percent of the rise in global food pricesIMF global food commodity price index.

Lipsky [68] and Johnson [69] 2005e2007 Increased demand for world biofuels accountsfor 70 percent of the increase in corn prices.

Mitchell [58] 2002emid-2008; ad hoc methodology: impact of movementin dollar and energy prices on food prices estimated,residual allocated to the effect of biofuels.

70e75 percent of the increase in food commodities priceswas due to world biofuels and the related consequencesof low grain stocks, large land use shifts, speculative activityand export bans.

Abbott et al. [70] Rise in corn price from about $2 to $6per bushel accompanying the risein oil price from $40 in 2004 to $120 in 2008

$1 of the $4 increase in corn price (25%) dueto the fixed subsidy of 51-cents per gallon of ethanol.

Rosegrant [71] 2000e2007; Scenario with actual increasedbiofuel demand compared to baseline scenariowhere biofuel demand grows accordingto historical rate from 1990 to 2000

Increased biofuel demand is found to have accountedfor 30 percent of the increase in weighted average grain prices,39 percent of the increase in real maize prices, 21 percentof the increase in rice prices and 22 percentof the rise in wheat prices.

Fischer et al. [72] (1) Scenario based on the IEA’s WEO 2008 projections;(2) variation of WEO 2008 scenariowith delayed 2nd gen biofuel deployment;(3) aggressive biofuel production target scenario;(4) and variation of target scenariowith accelerated 2nd gen deployment

Increase in prices of wheat, rice, coarse grains, protein feed,other food, and non-food, respectively,compared to reference scenario:(1) þ11%, þ4%, þ11%, �19%, þ11%, þ2%;(2) þ13%, þ5%, þ18%, �21%, þ12%, þ2%;(3) þ33%, þ14%, þ51%, �38%, þ32%, þ6%;(4) þ17%, þ8%, þ18%, �29%, þ22%, þ4%

8 Other factors include strong income growth and subsequent demand for meatproducts and feed grains for meat production in emerging economies, such asChina and India [59]; adverse weather conditions, such as the severe drought inAustralia [6]; the devaluation of the US dollar, growth in foreign exchange holdingsby major food-importing countries, and protective policies adopted by someexporting and importing countries to suppress domestic food price inflation [50];lower level of global stocks of grains and oilseeds [60] and increased oil prices [61].

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e15 7

Research and development (R&D) investments on advancedbiofuel technologies are also substantial in several countries. TheUS Department of Energy (DOE) is investing more than $400million to lower the cost of second-generation biofuels thougha directed research program, and has also approved 6 projects forup to $385 million in funding as part of the demonstration program[53]. While no commercial scale lignocellulosic ethanol plants areoperational as of early 2008, around 15e20 companies, mostly inthe US, are involved in pilot plant studies with different biotech-nological and thermo-chemical biomass conversion routes [8].With the efforts of the industry and strong support from the DOE,the first commercial lignocellulosic plant, may be operational in theUS in 2012.

In Europe, a company funded by DaimlerChrysler, Volkswagenand Royal Dutch Shell has been operating a demonstration plantfor the production of biodiesel from wood wastes via the gasifi-cation/FischereTropsch pathway in Freiberg since 2003. Thetechnology is being developed to reach the pre-commercial stagewith a capacity of 13,000 tons of biomass-to-liquid per year, andeventually for a commercial facility capable of delivering 200,000tons per year [54]. Other gasification/FischereTropsch schemes arealso being tested in Europe, and biodiesel from this technology isexpected to reach markets in the next decade [55]. The RFA [56]concludes that commercial scale plants are unlikely in the EUbefore 2018.

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

6. Impacts of biofuels on food prices

Expenditures on food amount to a large part of the budget of thepoorest households, and so rising food prices threaten them withfood insecurity, which is the lack of secure access to enough safe andnutritious for normal growth and development and for an active,healthy life [6]. The FAO [57] estimates that there were already 923million undernourished people worldwide, and rapid growth inbiofuel production,which is a significant source of demand for someagricultural commodities, suchas sugar,maize, cassava, oilseeds andpalm oil, has the potential to affect food security at both the nationaland household levels mainly through its impact on food prices.

Some studies criticize biofuels as one of the factors responsiblefor the 2008 food crisis.8 These studies concur that the diversion ofthe US corn crop to biofuels is the strongest demand-induced force

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e158

on food prices, given that the US accounts for about one-third ofglobal maize production and two-thirds of global exports [58].9 Anestimated 93 million tons of wheat and coarse grains, more thanhalf of the growth in wheat and coarse grain use during the period,were used for ethanol production in 2007, double the level of 2005[11]. Most of this growth comes from the United States of Americaalone, where the use of maize for ethanol grew to 81million tons in2007 and is expected to rise by another 30 percent in 2008 [57].Moreover, Collins [62] attributed 52% of the increase in soybean oiluse between 2005/06 and 2007/08 to biodiesel production. Table 3summarizes the recent literature on the impacts of increased bio-fuel production on food prices.

Baier et al. [63] estimate that the increase in worldwide biofuelsproduction over the two years ending June 2008 accounted foralmost 17 percent of the rise in corn prices and 14 percent of therise in soybean prices. More specifically, they attribute nearly 14percent of the rise in corn prices and nearly 10 percent of the rise insoybean prices to the increase in US biofuels production, whereasEU biofuels production growth accounted for roughly 2 percent ofthe increase in the price of these crops. In addition, the increase inEU biofuel production was responsible for around 3 percent of theincrease in the price of barley. In the case of sugar, they find that thegrowth of sugar-based ethanol production in Brazil accounted forthe entire escalation of the price of sugar over the same timeframe.

Although individual crop prices appear to be affected by bio-fuels, the impact of biofuels on global or aggregated food prices israther small. Worldwide biofuels production growth over the twoyears ending June 2008 is estimated to account for a little over 12percent of the rise in the IMF’s (International Monetary Fund’s)food price index, of which, roughly 60%, 14% and 15% can be attri-bute to increased biofuels production in the US, Brazil and the EUrespectively [63]. This means that about 88% of the rise in globalfood prices is caused by factors other than biofuels.

Banse et al. [64] show that if the mandatory 5.75% biofuelblending in EU member states is implemented, it would cause realprices of cereals, oilseeds and sugar in 2010 to be 2.75%, 3.5% and2.5% higher than that in the reference scenario. In the case of theimplementation of mandatory 11.5% biofuel blending, the corre-sponding price changes would be 7%, 10% and 9.75% (see Table 3).Rosegrant [71] shows that increased biofuel demand accounted for30 percent of the increase in weighted average grain prices in2000e2007 compared to the historical baseline. More specifically,increased biofuel demand is estimated to account for 39 percent ofthe increase in real maize prices, whereas it is estimated to accountfor 21 percent of the increase in rice prices and 22 percent of therise in wheat prices.

Some of the rises in food commodity prices are not caused bymarket forces, such as the price of gasoline, pertaining to biofuels,but rather by policy induced demand growth. McPhail et al. [73]argue that the elimination of federal tax credits and tariffs, and toa far lesser extent, mandates, in the US would reduce ethanolproduction by 18.6 percent, resulting in the decline of the price ofcorn by 14.5 percent. However, if gas prices are high enough, i.e., $3per gallon or higher, biofuel production may be profitable withoutsupport policies; ethanol production can be expected to rise fromthe current levels of 6.5 billion gallons to 14 billion gallons, andcorn price would remain at about $4 a bushel.

The existing literature not only assesses the impacts of biofuelson the 2007e2008 food crisis but also projects the impacts on foodprices in the future. The International Food Policy Research

9 The expansion of maize area in the US by 23% in 2007 entailed the contractionof soybean area by 16%, leading to lower soybean output and playing a part in the75% rise in soybean prices from April 2007 to April 2008.

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

Institute (IFPRI) finds price increases for maize of 23e72%, wheat of8e30%, oilseeds of 18e76%, and sugar of 11.5e66%, in response tocountries implementing the plans they have announced for bio-fuels by 2020 [74]. Trostle [50] projects price rises of 65%, 64%, 33%and 19%, for maize, sorghum, wheat and soy oil, respectively, due tothe expansion of biofuels, rising energy costs and demand fromemerging economies. Moreover, should biofuel production befrozen at 2007 levels for all countries and for all crops used asfeedstock, maize prices can be expected to decline by 6 percent by2010 and 14 percent by 2015, along with lesser price reductions foroil crops, cassava, wheat, and sugar [71]. If a global moratorium oncrop-based biofuel production is imposed from 2007 onwards, by2010, prices of key food crops would drop even further: by 20percent for maize, 14 percent for cassava, 11 percent for sugar, and 8percent for wheat.

Taheripour et al. [75] emphasize the importance of including by-products when modeling the impact on non-energy commodityprices of expanded biofuel production in response to US and EUbiofuel mandates. They show that the price of coarse grainsincreases sharply in the US, EU, and Brazil by 22.7%, 23.0%, and11.9%, respectively, over the period 2006e2015; once by-productsare incorporated into the model, the price of coarse grains exhibitssignificantly lower growth rates of 14%, 15.9%, and 9.6%, respec-tively. The inclusion of by-products reduces the price rise ofoilseeds in the EU from 62.5% to 56.4% in the same period. Theprices of most other agricultural commodities grow at a slightlylower rate when by-products are accounted for.

Fischer et al. [72] model the prices of food staples in 2020 and2030 under several different scenarios for biofuel production.Under a scenario based on the International Energy Agency’sWorldEnergy Outlook 2008 projections, price increases for both cerealsand other crops in 2020 are about 10 percent higher compared toa reference scenario where biofuel development after 2008 is keptconstant at the 2008 level. Since the contribution of second-generation biofuels is still small in 2020, a variation of this scenario,featuring delayed introduction of second-generation technologies,only results in moderate further crop price increases. In the moreaggressive target scenario, based on the mandates and targetsannounced by several developed and developing countries, theimpact of increased biofuel production on crop prices is muchmoresignificant: prices rises of about 30 percent. When the targetscenario is modified to incorporate the accelerated introduction ofcellulosic ethanol, the price impact on cereals is cut in half to about15 percent. Because of the high targets in developing countries,which feature a higher share of biodiesel and somewhat slowerdeployment of second-generation technologies, the price impacton non-cereal crops (especially vegetable oils) is greater than thaton cereals.

In addition to the impacts on food price, Fischer et al. [72] alsoexamine the impact of expanded biofuel production on food supply.The additional global demand for cereal commodities for ethanolproduction in 2020 in the various scenarios they examine rangesfrom around 100 million tons to 330 million tons. However, higheragricultural prices also lead to increased production, particularly indeveloped countries, along with reductions in the use of cereals foranimal feed. The remainder of the additional demand for cereals forbiofuel production is met by reduced food use, most of it indeveloping countries. Nevertheless, even in the worst case, thereduction in global cereal food consumption is about 29 milliontons, which only constitutes a 1% decline in from the global cerealconsumption of 2775 million tons in the reference case wherebiofuel production is frozen at 2008 levels.

One interesting observation from the existing literature is thatthe magnitude of the impacts of biofuels on food prices is verymuch sensitive to the models used to assess those impacts. Partial

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

10 The energy inputs comprise almost 80% of the energy output.11 It could be increased to 67% in the case of an advanced closed-loop biorefinerywith anaerobic digestion.12 Note however that converting degraded savannas for sugarcane production, orjatropha cultivation, may increase below-ground carbon stocks (Fischer et al., [72]).

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e15 9

equilibrium models (e.g., [50,71,74]), which model the food andagricultural sector in isolation, ignoring this sector’s interactionwith other sectors of the economy, find higher impacts on foodprices. On the other hand, general equilibrium models, whichaccount for interactions of various sectors and agents (e.g., [64,72])find the impacts to be relatively small.

7. Environmental impacts of biofuels

7.1. Impacts on climate change mitigation

Biofuels replace fossil fuels, thereby avoiding associated GHGemissions. However, a large-scale expansion of biofuels could causethe release of GHG emissions to the atmosphere through land-usechange as farmers might clear existing forests to meet increasedcrop demand to supply food and feedstock for biofuels. The climatechange mitigation potential through fossil fuel replacement variesacross types of feedstock, depending on feedstock productionprocess/technology (e.g., usage of nitrogen fertilizer) and fossil fuelconsumption in both production of feedstocks and subsequentconversion to biofuels. For example, useful heat and electricity maybe cogenerated along with liquid fuel in some biofuel productionsystems, and plants differ in their use of fossil inputs or residualplant materials like straw for process energy [72]. Even for a partic-ular feedstock, standard life-cycle analyses (LCA) of biofuels in theliterature exhibit a wide range in terms of the overall reduction inGHG emissions due to varying underlying assumptions on systemboundaries, co-product allocation, and energy sources used in theproduction of agricultural inputs and feedstock conversion to bio-fuels. Nevertheless, most studies show that biofuels do yield someemission reductions relative to their fossil fuel counterparts whenemissions from the direct or indirect land-use changes broughtabout by biofuel feedstock production are excluded.

Based on life-cycle assessments, ethanol from sugarcane inBrazil is found to deliver the greatest reductions in GHG emissions.This is due to high yields and the use of sugarcane waste (i.e.,bagasse) for process energy as well as for the cogeneration ofelectricity [76]. The 25% ethanol blending mandate (E25) wascalculated to reduce 1.87 ton of CO2eq for each cubic meter ethanolused in 2005/2006 in Brazil. OECD [8] estimates that sugarcaneethanol reduces GHG emissions by 90% as compared to an equiv-alent amount of gasoline. The next best are second-generationbiofuels from cellulosic feedstocks, which have yet to becomewidespread commercially, with typical life-cycle GHG reductions inthe range of 70e90% relative to gasoline or diesel [16]. Numerousstudies anticipate that advanced biofuels could dramatically reducelife-cycle GHG emissions compared to first-generation biofuelsbecause of higher energy yields per hectare and energy for pro-cessing available from the left-over parts of the plants (mainlylignin), similar to the use of bagasse in ethanol production in Braziltoday [6]. Some studies indicate that the savings could approachand even exceed 100% in cases, such as where the cogeneration ofelectricity displaces coal-fired electricity from the grid [15]. Simi-larly, syndiesel production via gasification with FischereTropschprocessing can supply GHG savings of close to 100% or even higherthan regular diesel when including credits from the surplusrenewable electricity that is produced [56].

Ethanol from sugar beets offers life-cycle GHG reductions ofroughly 40e60% [16], putting it in the middle of the pack amongstbiofuels, while ethanol produced from wheat generates slightlylower GHG reductions of 30e55% [72], although there is consid-erably more variation in the values for wheat in the literature, fromas low as 18% to as high as 90%. Ethanol from maize generates thesmallest reductions of GHG, and its performance is most variable,with results ranging from zero savings (even negative in some

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

cases) up to more than 50% savings compared to fossil gasoline.Farrell et al. [77] report that corn-based ethanol, in the US, couldreduce only 13% GHG emissions because the production process isso energy intensive.10 EBAMM [78] finds that corn-basedethanol delivers net emission savings of only 130 kg CO2eq/m3 ofethanol, almost 15 times less than that delivered by sugarcaneethanol. Despite this poor GHG balance, corn-based ethanoloccupies the largest share of the global biofuels market (as of 2007)due to vast US production [8]. However, more recent studies (e.g.,[79]) shows that the reduction potential could be significantlyimproved to 48e59% through enhanced yields and crop manage-ment, biorefinery operation, and co-product utilization.11

Of biodiesel from first-generation feedstocks, biodiesel frompalm oil is generally considered to yield the most substantial GHGsavings, typically in the range of 50e80 percent [6]. However,estimates of GHG savings from biodiesel from palm oil are espe-cially prone to understating the full GHG impacts since palmplantations in South East Asia often replace tropical forest orpeatland, resulting in the release of tremendous amounts of CO2from those natural reservoirs. Biodiesel both derived fromsunflower and from soybean delivers significant GHG savings, buta wide range of values is found in the literature, depending on thedifferent assumptions used in each study, particularly in the case ofsoybean biodiesel. Whereas emission savings from biodiesel basedon sunflower appear to converge around 60e80%, the emissionsavings from soybean biodiesel tend to be around 50e70%. Thewide variation in values is explained by the disparity in agriculturalyield across regions, the assumptions made regarding the alloca-tion of glycerin (an important co-product from the manufacture ofsoybean biodiesel), as well as the type of chemicals and processenergy utilized [80]. Another important feedstock for biodiesel israpeseed, and a large number of studies have analyzed the GHGimpacts of biodiesel from rapeseed. GHG savings from rapeseed-based biodiesel typically range 40e60 percent [16].

The rosy picture of the GHG savings potential of biofuelsdisappears once the release of carbon stored in forests or grasslandsduring land conversion to crop production is taken into account.12

Several studies find that if emissions related to land-use changecaused by biofuel expansion are included, the emissions would beso high that it would take tens to hundreds of years to offset thoseemissions through the replacement of fossil fuels. The number ofyears required to offset GHG released from land conversion by theemission reduction through the replacement of fossil fuels withbiofuels is also known as the ‘carbon payback period’ (see e.g.,[81e83]). Fargione et al. [81] estimate that it would take 48 years torepay if Conservation Reserve Program land is converted to cornethanol production in the US; over 300 years to repay if Amazonianrainforest is converted for soybean biodiesel production; and over400 years to repay if tropical peatland rainforest is converted forpalm-oil biodiesel production in Indonesia or Malaysia. Similarly,Danielsen et al. [82] estimate that 75e93 years of biofuel use wouldbe necessary for the carbon savings to make up for the carbon lostvia forest conversion, varying upon how the forest is cleared. Theyalso estimate that the conversion of peatland would require morethan 600 years to yield GHG savings, whereas cultivation of oil palmon degraded grassland could produce GHG savings within 10 years.

Searchinger et al. [83] argue that a decline in US corn exportsdue to the diversion of corn to increase ethanol output by 56

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e1510

billion liters above projected levels in 2016 will encourage othercountries to increase corn production. If the new productionoccurs on land that was previously forest or grassland, 167 years ofuse of ethanol from maize in the US will be necessary to offset theemissions from this indirect land-use change. Even second-generation biofuels are not attractive from this perspective. Forexample, if switchgrass is grown for biofuels on U.S. corn lands,the ensuing indirect land-use change would have a carbonpayback period of 52 years and would increase emissions over 30years by 50%. Hertel et al. [84], in a general equilibrium study, findthe indirect land-use change caused by the escalation of US maizeethanol production to satisfy the 2015 mandated level of 56.7billion liters to be two-fifths of that estimated by Searchinger et al.[83]. Their estimate of the emissions resulting from this indirectland-use change amounts to one-fourth of that calculated bySearchinger et al. [83].13 When combined with the direct emis-sions from US maize ethanol production, this corresponds toa carbon payback period of 28 years.

Using an engineering technique, Fritsche andWiegmann (2008)compare GHG balances for biofuels that includes the effect of directas well as well as indirect land-use change on emissions. Theyfound that, if emissions related to land-use change are ignored,biofuels could reduce 49e90% GHG emissions depending upon thetype of feedstock. On the other hand, if emissions from land-usechange are considered, total GHG emissions would increase by1e102%. Fischer et al. [72] estimate net GHG savings under variousscenarios for the deployment of biofuels using a general equilib-rium approach to capture emissions from land-use change. Sincethe carbon losses from land-use change are incurred at the time ofland conversion, while greenhouse gas savings from the substitu-tion of biofuels for fossil fuels accrue gradually over time, the netGHG savings resulting from the first-generation biofuels would notbe positive in the first 20 years in any of the scenarios theyconsidered. It would take 50 years to achieve a sizable savings ofGHG emissions from large-scale deployment of biofuels.

Some studies evaluate the attractiveness of biofuels as a GHGmitigation option. A rough, indicative calculation by the OECDprojects that lowering GHG through policy support to biofuels inthe US, Canada, and Europe in 2013e2017would cost taxpayers andconsumers on average between USD 960 and 1700 per ton of CO2-equivalent avoided [8]. Righelato and Spracklen [85] find thatemission reductions through biofuels would be less attractiveeconomically as compared to afforestation in pasture land. Simi-larly, Danielsen et al. [82] suggest that reducing deforestation maybe a more effective climate change mitigation strategy than the useof biofuels. Tax credits for ethanol production tend to encourage anoverall increase in vehicle miles traveled and a delay in the adop-tion of more fuel-efficient cars, which can lead to greater GHGemissions, while binding mandates, by pushing fuel prices up, mayproduce some GHG reductions from reduced vehicle miles traveledand increases in fuel economy [86]. Tollefson [87] asserts that animprovement of one mile per gallon in average US vehicle fuelefficiency may decrease GHG emissions the same as all currentUnited States ethanol production from maize. Doornbosch andSteenblik [15] estimate that GHG mitigation costs of US ethanolbased on corn and EU ethanol based on sugar beet and corn wouldbe as high as US$500/tCO2 and US$4,520/tCO2 respectively. Simi-larly, Enkvist et al. [88] find that energy efficiency improvement inheating and air-conditioning systems would be cheaper by V40

13 Hertel et al. [84] estimate the associated CO2 emissions at 800 g of CO2 per MJ,or 27 g per MJ per year over 30 years of ethanol production, while Searchinger et al.[83] estimated about 3000 g of CO2 per MJ, or around 100 g per MJ if allocated over30 years.

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

than biofuels. Amatayakul and Berndes [45] estimate the annualaverage cost of the substitution of gasoline with ethanol in Thailandto be 25e195 US$/tCO2eq which is much higher than the price ofproject-based certified emission reductions traded during 2006;this would be, however cheaper than the cost of substitution offossil fuels with biofuels in Europe.

7.2. Biofuels and local air quality

In most urban areas, road transport is the primary source ofparticulate matter (PM10) and emissions from fuel combustion,which poses an important public health concern [89]. Thereplacement of fossil fuels with biofuels for transportation has thepotential to reduce local air pollution in several ways. First, apartfrom rapeseed-based biodiesel, biofuels generally cause lessprimary PM10 and volatile organic chemicals (VOCs) than fossilfuels.14 Many studies can be found in the scientific literature onexhaust emissions of biodiesel or biodiesel blends. Second,compared to their fossil fuel counterparts, biodiesel does notproduce sulfur emissions, while ethanol substantially lowers sulfuremissions, and both emit far less lower carbon monoxide (CO),which are two major threats to local air quality [4,91].

However, biofuels, particularly biodiesel, generate up to 70%higher NOx emissions (and could also raise concentrations of NO2-based secondary PM10), depending on feedstock, which enablesozone formation in conjunction with VOCs and other pollutants[92]. Most studies show a slight increase in NOx and a reduction ofPMwhen diesel is replaced with biodiesel [93e95]. However, if theobjective is the improvement of local air quality, the performance ofbiodiesel should also be compared to fuels other than fossil dieselthat are currently available. Russi [96] compares the average tail-pipe NOx, PM and VOC emissions of a medium-sized passenger carrunning on different biodiesel blends with premium unleadedpetrol, liquefied petroleum gas (LPG) and compressed natural gas(CNG). It shows that far greater reductions in NOx and PM can beachieved by shifting from diesel to other readily available fossilfuels than by switching to biodiesel blends [96]. Even though bio-diesel can deliver better performance in terms of VOC than LPG,a 20% blend is necessary to surpass the performance of premiumunleaded petrol and pure biodiesel is required to exceed theperformance of CNG. These levels of blending are unlikely to beviable on a large scale.

Jacobson [97] shows that a broad displacement of gasoline withhigh ethanol blends in the US would lead to greater emission oflocal air pollutants and negative health impacts from deterioratingair quality. Moreover, the cultivation of biofuel feedstocks can alsoaffect local air quality through fugitive emissions of air pollutants.The frequent burning of cleared vegetation for biofuel production,as practiced in Brazil, Indonesia and Malaysia for example, causessevere smog and has adverse effects on human morbidity andmortality [98]. In addition, palm-oil production may result in thefugitive emission of methane from water surfaces and liquid pro-cessing wastes [99].

7.3. Impacts on biodiversity and ecosystems

The effect of biofuel production on biodiversity depends on thetype of land utilized. If degraded lands are restored for biofuelfeedstock production, the impact could be positive. On the otherhand, if peatlands are drained or natural landscapes are convertedto biofuel plantations, the effect is generally negative. Since many

14 A recent study in Thailand, however, found that biofuel in motorcycles couldproduce slightly higher VOC emissions than gasoline [90].

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e15 11

current biofuel crops are especially suited for cultivation in tropicalareas, biofuel expansion could convert natural ecosystems intropical countries that are biodiversity hotspots into feedstockplantations [100]. Ogg [101] points out that European biofuelsubsidies are major drivers of rainforest loss in Indonesia, thesource of the lowest cost vegetable oil (palm) in the world [121].The expansion of oil palm plantations, for example, which do notrequire much fertilizer or pesticide, can trigger the loss of rain-forests and the biodiversity in them. Koh and Wilcove [102] esti-mate that half of oil palm plantations expanded in Malaysia andIndonesia replaced natural forests. Similarly, more than 60% ofBrazil’s sugarcane cultivation is done in the Mata Atlantica region,one of the foremost biodiversity hotspots in the world, and sugar-cane and soybean production are contributing to the clearing of theCerrado, the world’s most biodiverse savannah [4]. Nelson andRobertson [103] find that areas rich in bird species diversity couldbe at risk from the expansion of agricultural lands in Brazil. Large-scale expansion of biofuels could result in loss of agro-biodiversitydue to the intensification of agriculture through mono-croppingsince most biofuel feedstock plantations rely on a single species [6].The Royal Society [104] highlights the vulnerability of grasses usedas biofuel feedstocks, such as sugarcane, to new pests and diseases.These pests and diseases have the potential to destroy the crop andspread into natural habitats [105].

Second-generation biofuels present another set of problems:some of the promising feedstocks are classified as invasive species,which will require proper management in order to avoid unin-tended consequences [6]. In addition, many of the enzymesnecessary to process the feedstock would also have to be carefullycontained in industrial production processes as they have beengenetically modified to improve their efficiency [106]. However,there is also some evidence to suggest that biodiversity can beenhanced and ecosystem functioning restored by biofuel feed-stock cultivation when it consists of the introduction of newperennial mixed species to degraded or marginal areas [100].Tilman et al. [107] use experimental data from test plots ondegraded and abandoned soils to demonstrate that, compared tomaize ethanol or soybean biodiesel, low-input high diversitymixtures of native grassland perennials yield higher net energygains, greater GHG emission reductions and less agrichemicalpollution, and that this performance is positively correlated to thenumber of species.

The potential impact of biofuels on water supply is anotherserious concern. Approximately 70% of the freshwater around theworld is already dedicated to agriculture [108]. The main biofuelfeedstocks, in particular, sugarcane, oil palm and maize, requirerelatively plentiful water at commercial yield levels. This impliesincreased demand for irrigation and strain water supply. Forexample, despite the fact that 76% of the sugarcane produced inBrazil is under rainfed conditions, some irrigated sugar-producingregions in northeastern Brazil are already approaching the hydro-logical limits of their river basins, e.g., the São Francisco river basin[6]. De Fraiture et al. [109] find that the strain on water resourceswould be so significant that large biofuel programs based ontraditional feedstocks would be challenging in India and China.

Increased water pollution due to biofuels is also a concern insome countries. Moreira [110] points out that water pollution dueto increased use of fertilizers and agrochemicals, sugarcanewashing and other stages in the ethanol production process remainmajor concerns in Brazil. Higher crop prices tend to encouragefarmers to intensify fertilizer application on existing cropland inorder to enhance yields during years with good weather conditionsand take advantage of higher crop prices [111,112]. Simpson et al.[113] note that expanded or intensified corn acreage for ethanol,even when accounting for fertilizer and land conservation

Please cite this article in press as: Timilsina GR, Shrestha A, How muj.energy.2010.08.023

measures, will result in a significant loss of nitrogen and phos-phorous to water. Runge and Senauer [114] warn that thedisplacement of maizeesoybean rotations with continuous maizecultivation for ethanol production in the United States will havenegative consequences: the ensuing runoff from additionalnitrogen fertilizer application will compound problems, such aseutrophication in the “dead zone” in the Gulf of Mexico.

Biofuels also affect soils both positively and negatively. Conver-sion of forest to plantations may lead to the loss of soil carbon[115,116], but growing perennials, such as oil palm, sugarcane,switchgrass, instead of annuals crops could increase soil cover andorganic carbon levels. The impacts differ with crop type, soil type,nutrient demand and land preparation necessary. Sugarcanegenerally has less of an impact on soils than rapeseed, maize andother cereals because soil fertility is maintained in sugarcane culti-vation by recycling nutrients from sugar-mill and distillery wastes[16]. However, the diversion of agricultural residues, such asbagasse, as an energy input to biofuel production reduces theamountof crop residues available for recycling,which coulddegradesoil quality, and soil organicmatter inparticular [117]. Hill et al. [118]explain that soybean production for biodiesel in the US requires farless fertilizer and pesticide per unit of energy produced than maizeproduction for ethanol, and that both feedstocks fare poorly incomparison to second-generation feedstocks such as switchgrass,woody plants or diverse mixtures of prairie grasses and forbs.Finally, the IEA [16] states that perennial lignocellulosic crops suchas eucalyptus, poplar, willow or grasses can be grown on poor-quality land, increasing soil carbon and quality, with less-intensivemanagement and fewer fossil-energy inputs.

8. Impact of biofuels on land use

The demand for land to produce biofuels augments the tradi-tional demands of agriculture and forestry. Moreover, global pop-ulation growth as well as rising per capita consumption ofdeveloping countries can be expected to increase demand for landfor food supply in the future. While some of this demand may bemet with improved crop yields per unit area, which has beenincreasing at about 1.5% in recent decades for staple crops, thiswould only increase production by 40% by 2030, requiringa conservatively estimated 500 Mha more land to be brought intocultivation in order to meet the additional demand for food alone[119]. There exist a large number of studies estimating landrequirement to meet specified biofuel targets (see [96,120e127]).However, the results vary considerably due to difference in meth-odological approach, different assumptions about crops used andconversion efficiencies from biomass to fuel.

Gurgel et al. [120] find that the expansion of biofuel cultivationwill occur largely at the expense of natural forest and pasture land(especially when no land supply response is assumed), whereascropland, managed forest, and natural grassland show little netchange. Much of this land dedicated to biofuel feedstock cultivationis found in Africa and Central and South America, and also, toa lesser extent, in the US, Mexico and Australia and New Zealand,reflecting the existence of vast natural forests and pastures in thoseareas and the superior biomass productivity of tropical regions,whereas China and India, due to their immense food demand andrelatively lower biomass land productivity, are not found to beregions supporting significant expansion of land for biofuel feed-stocks. Hertel et al. [128] also show that largest net reductions inland cover tend to be in pasture land, although large percentagedecreases in forest land are found in Brazil and the EU. Anotherimportant factor is that when biofuel producing countries convertcropland to biofuel production, the reduced food exports andhigher commodity prices induce land to be cleared for crops in

ch hope should we have for biofuels?, Energy (2010), doi:10.1016/

G.R. Timilsina, A. Shrestha / Energy xxx (2010) 1e1512

tropical countries such as Brazil, Argentina and Indonesia to satisfythe unmet food demand [129].