Embed Size (px)

Citation preview

2018 SC BAR CONVENTION

Real Estate Practices Section

“How to Build a Better Mousetrap”

Saturday, January 20

SC Supreme Court Commission on CLE Course No. 180887

How to Navigate the Commercial Real Estate Maze

Kara M. Bailey

William “Bill” O. Higgins Matthew “Matt” B. Hill

2018 SC BAR CONVENTION

Real Estate Practices Section

Saturday, January 20

- 1 -

Construction Loan for Single Tenant, Build to Suit Warehouse

LOAN CLOSING CHECKLIST

CLOSING:

LENDER:

LENDER’S COUNSEL: Kara M. Bailey, Esquire

ROGERS TOWNSEND & THOMAS, PC

BORROWER:

BORROWER’S COUNSEL:

THIS LOAN CLOSING CHECKLIST IS FOR CONVENIENCE ONLY TO ASSIST IN THE CLOSING OF THE LOAN

CONTEMPLATED HEREBY. NOTHING CONTAINED HEREIN SHALL BIND LENDER OR CONSTITUTE ANY

COMMITMENT, APPROVAL OR WAIVER BY LENDER. LENDER RESERVES THE RIGHT TO REQUIRE THAT

ALL OF ITS REQUIREMENTS BY FULLY SATISFIED PRIOR TO CLOSING, WHETHER OR NOT LISTED OR

SHOWN AS SATISFIED IN THIS LOAN CLOSING CHECKLIST. THIS LOAN CLOSING CHECKLIST IS ONLY A

PARTIAL LISTING OF LENDER’S REQUIREMENTS, AND DOES NOT INCLUDE OTHER MATTERS SET FORTH IN

THE LOAN COMMITMENT, LOAN APPLICATION OR OTHERWISE.

“D” = Drafted P/C= Post Closing

“N/A” = Not Applicable

“W” = Waived “C” or “R” = Complete or Received

- 2 -

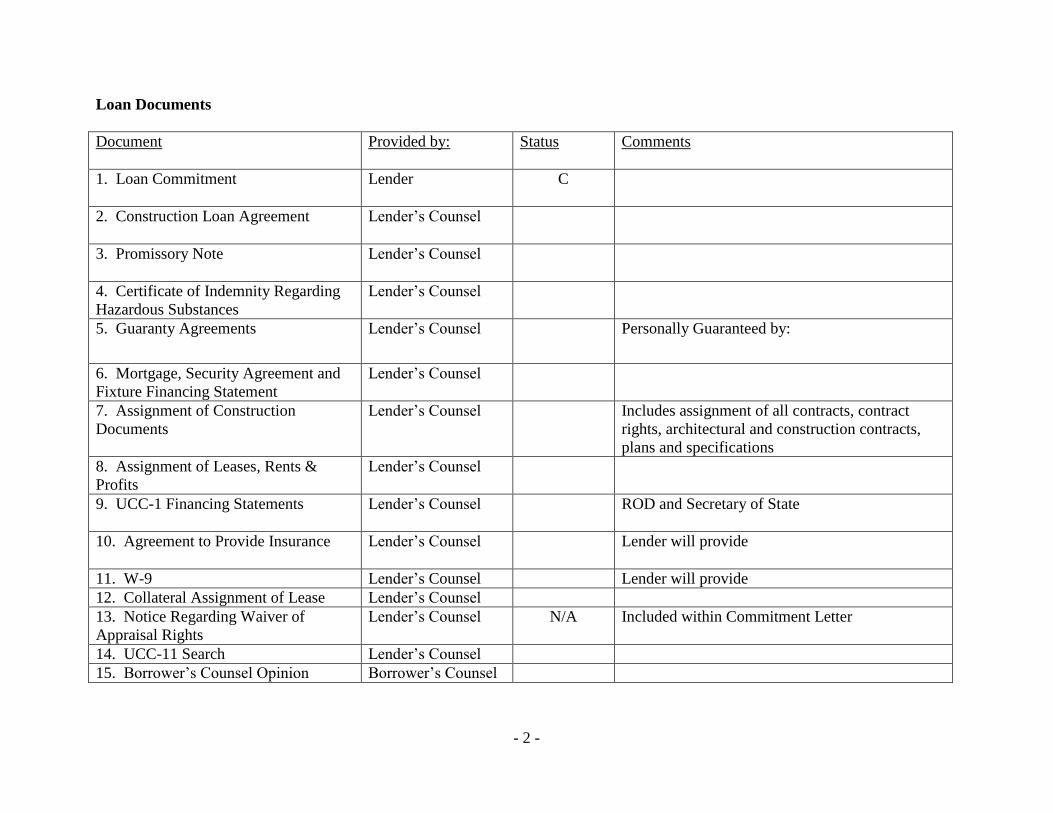

Loan Documents

Document

Provided by: Status Comments

1. Loan Commitment

Lender C

2. Construction Loan Agreement

Lender’s Counsel

3. Promissory Note

Lender’s Counsel

4. Certificate of Indemnity Regarding

Hazardous Substances

Lender’s Counsel

5. Guaranty Agreements

Lender’s Counsel Personally Guaranteed by:

6. Mortgage, Security Agreement and

Fixture Financing Statement

Lender’s Counsel

7. Assignment of Construction

Documents

Lender’s Counsel Includes assignment of all contracts, contract

rights, architectural and construction contracts,

plans and specifications

8. Assignment of Leases, Rents &

Profits

Lender’s Counsel

9. UCC-1 Financing Statements

Lender’s Counsel ROD and Secretary of State

10. Agreement to Provide Insurance

Lender’s Counsel Lender will provide

11. W-9 Lender’s Counsel Lender will provide

12. Collateral Assignment of Lease Lender’s Counsel

13. Notice Regarding Waiver of

Appraisal Rights

Lender’s Counsel N/A Included within Commitment Letter

14. UCC-11 Search Lender’s Counsel

15. Borrower’s Counsel Opinion Borrower’s Counsel

- 3 -

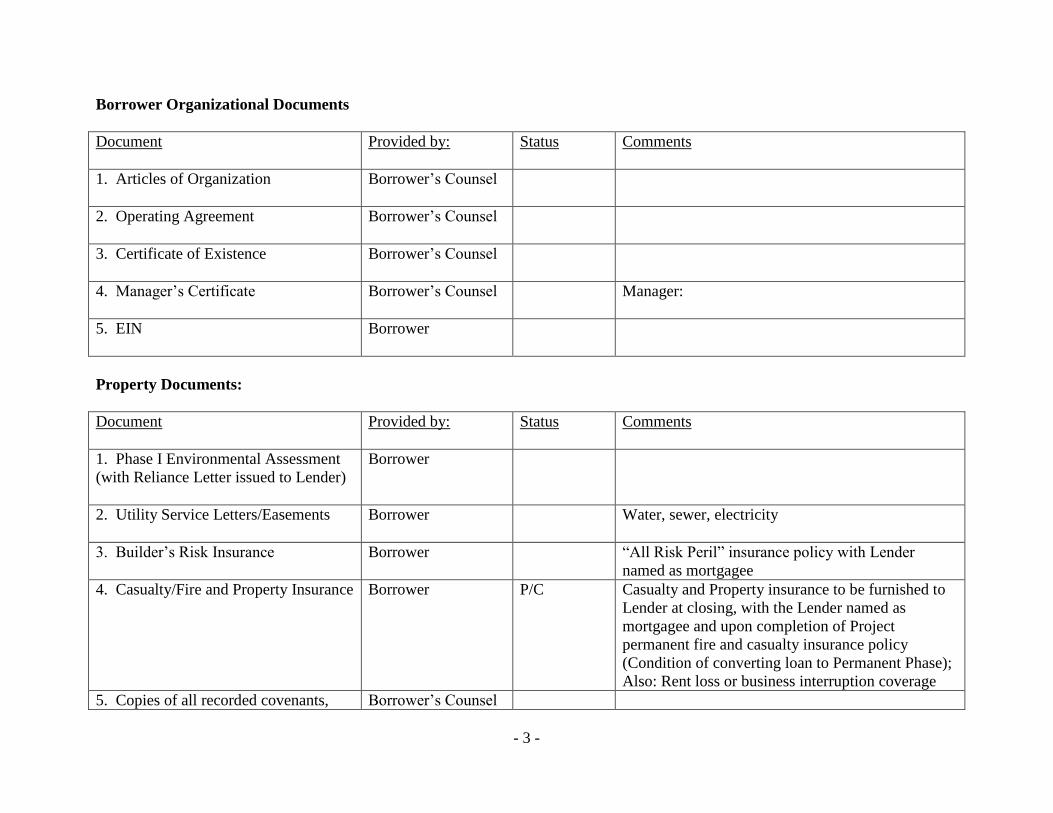

Borrower Organizational Documents

Document

Provided by: Status Comments

1. Articles of Organization

Borrower’s Counsel

2. Operating Agreement

Borrower’s Counsel

3. Certificate of Existence

Borrower’s Counsel

4. Manager’s Certificate

Borrower’s Counsel Manager:

5. EIN

Borrower

Property Documents:

Document

Provided by: Status Comments

1. Phase I Environmental Assessment

(with Reliance Letter issued to Lender)

Borrower

2. Utility Service Letters/Easements

Borrower Water, sewer, electricity

3. Builder’s Risk Insurance

Borrower “All Risk Peril” insurance policy with Lender

named as mortgagee

4. Casualty/Fire and Property Insurance

Borrower

P/C Casualty and Property insurance to be furnished to

Lender at closing, with the Lender named as

mortgagee and upon completion of Project

permanent fire and casualty insurance policy

(Condition of converting loan to Permanent Phase);

Also: Rent loss or business interruption coverage

5. Copies of all recorded covenants, Borrower’s Counsel

- 4 -

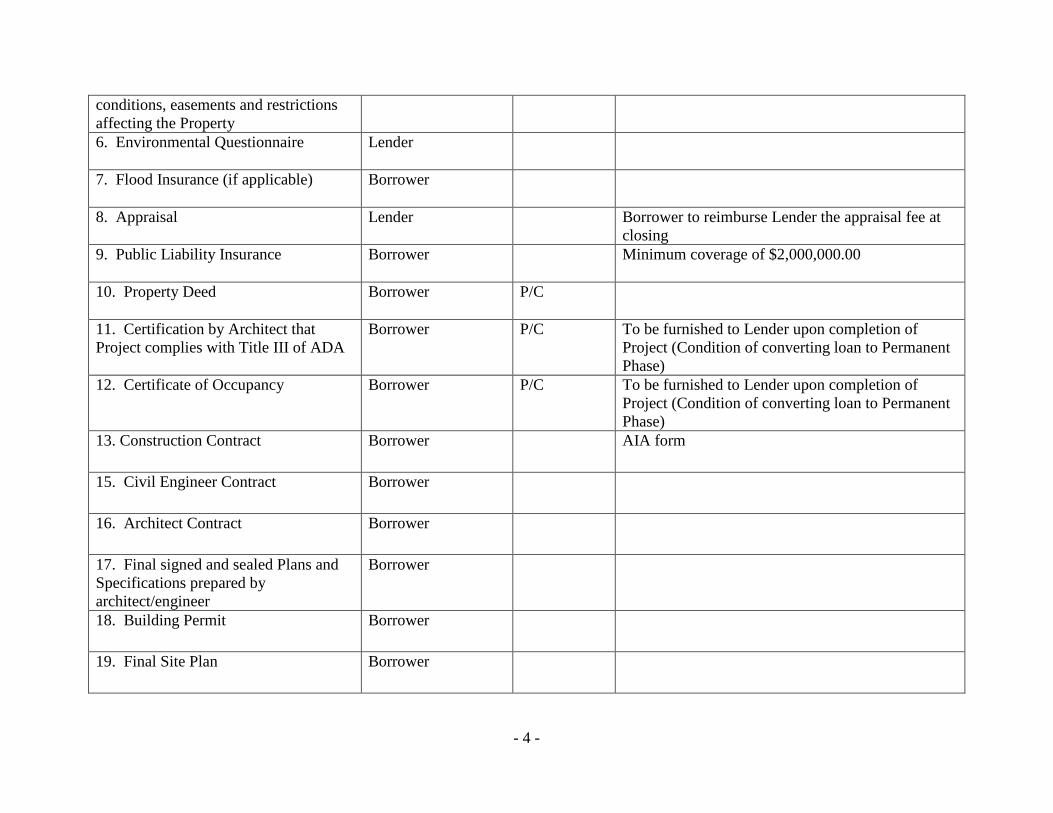

conditions, easements and restrictions

affecting the Property

6. Environmental Questionnaire

Lender

7. Flood Insurance (if applicable)

Borrower

8. Appraisal

Lender Borrower to reimburse Lender the appraisal fee at

closing

9. Public Liability Insurance

Borrower Minimum coverage of $2,000,000.00

10. Property Deed

Borrower P/C

11. Certification by Architect that

Project complies with Title III of ADA

Borrower P/C To be furnished to Lender upon completion of

Project (Condition of converting loan to Permanent

Phase)

12. Certificate of Occupancy Borrower P/C To be furnished to Lender upon completion of

Project (Condition of converting loan to Permanent

Phase)

13. Construction Contract Borrower AIA form

15. Civil Engineer Contract Borrower

16. Architect Contract Borrower

17. Final signed and sealed Plans and

Specifications prepared by

architect/engineer

Borrower

18. Building Permit Borrower

19. Final Site Plan Borrower

- 5 -

20. Boundary Survey Borrower ALTA/ACSM As-Built Survey to be furnished to

Lender upon completion of Project (Condition of

converting loan to Permanent Phase)

21. Zoning Compliance Letter Borrower

Title Documents:

Documents

Provided by: Status Comments

1. Title Insurance Commitment Borrower’s Counsel Endorsements: (a) zoning; (b) environmental (c)

survey (d) access and entry; (e) comprehensive; (f)

single tax parcel (g) waiver of arbitration, (h)

location, (i) subdivision (subject to change upon

review of title)

All beneficial easements must be insured.

2. Exceptions to Title Borrower’s Counsel Copies of all recorded covenants, conditions,

easements and restrictions affecting the property.

3. Title Insurance Policy Borrower’s Counsel P/C Within 30 days of Closing

4. Copy of Lease affecting the property

with Trane Corporation

Borrower’s Counsel Lease must executed by Tenant, and otherwise

acceptable to Lender.

5. Insured Closing Letter Borrower’s Counsel

THE STATE OF SOUTH CAROLINA

In The Supreme Court

Vance L. Boone, Thelma Boone, Travis G. Messex,

Theresa S. Messex, Brian Johnson, and Kelli Johnson, on

behalf of themselves and all others similarly situated,

Petitioners,

v.

Quicken Loans, Inc. and Title Source, Inc., Respondents.

Appellate Case No. 2013-002288

______________

IN THE ORIGINAL JURISDICTION OF THE SUPREME COURT

______________

Opinion No. 27727

Heard October 19, 2016 – Filed July 19, 2017

420 S.C. 452, 803 SE2d 707

______________

OPINION EXCERPTS:

We find the record in this case shows licensed South Carolina attorneys were involved at every critical step

of these refinancing transactions, as required by our precedents. We also find that requiring more attorney

involvement would not effectively further our stated goal of protecting the public from the dangers of UPL.

Prior to expanding into the South Carolina market, Quicken Loans engaged South Carolina attorneys[…]

to review the Quicken Loans refinance Procedure. […]the attorneys opined that the procedure would not

constitute UPL,[….]

Notably, each of the attorneys involved[…]testified that they maintained their independence and were not

controlled by Quicken Loans or Title Source in the exercise of their professional judgments.

[…]the Special Referee focused on the proper issue, that is, whether the supervision by the South Carolina

attorneys was sufficient and “meaningful.”

The common thread running through our decisions is the desire to protect the public.

[…]the goal of consumer protection was at the heart of this Court’s reasoning in Buyers Service,[….]

[…]this Court has refused to require attorney involvement it did not find necessary to protect the public.

To be clear, the lawyer’s involvement and supervisory role remain vital and necessary; however, this Court

has never found that, as a matter of consumer protection, attorneys are required to personally conduct the

myriad clerical tasks required to prepare for a transaction closing.

2

[…]this Court carefully considers the specific constellation of facts presented and legal rights implicated

to determine whether the degree of attorney involvement appropriately protects the public from potential

legal pitfalls without unduly burdening consumer choice or needlessly increasing consumer costs.

The record further reveals Title Source expected the South Carolina attorneys it engaged to take the steps

needed to comply with South Carolina law.

[…]we are firmly persuaded that, in each of the transactions at issue, the residential mortgage refinance

practice utilized by Quicken Loans and Title Source, which includes direct and independent attorney

supervision at each critical step, complies with the law.

[...]because each attorney involved at every critical point in these challenged transactions remained free to

exercise his or her independent professional judgment, the presence of a third party intermediary (such as

Title Source) does not transform the practice into UPL.

[…]we believe a finding that Respondents’ conduct constituted UPL would mark an unwise and

unnecessary intrusion into the marketplace.

Once it is determined that sufficient attorney involvement is present and further that the interest of the

public is protected, this Court should stay its hand and let the marketplace control. […there is no allegation

here of fault[….]

Simply put, we believe requiring more attorney involvement in cases such as this would belie the Court’s

oft-stated assertion that UPL rules exist to protect the public, not lawyers.

[…]we do not believe requiring more attorney involvement would appreciably benefit the public or justify

the concomitant increase in costs and reduction in consumer choice or access to affordable legal services.

Catch Me If You Can

Frank W. Abagnale

2018 SC BAR CONVENTION

Real Estate Practices Section

Saturday, January 20

No Materials Available