Embed Size (px)

Citation preview

Prepared for: Conference on the Role of Sukuk in Development

Global Sukuk Market: Current Status & Growth Potential

Date: May 18, 2012

HSBC Amanah

2

Contents

Overview of Islamic Finance Market Section 1

Overview of Sukuk Market Section 2

Sukuk Structures Section 3

A. Ijara Sukuk (Sale & Leaseback)

B. Wakala Sukuk

C. Istithmar Sukuk

D. Manafae Sukuk

Project Sukuk Section 4

Overview of Islamic Finance Market

4

262 354

445 489

235

293

369 406

67

87

109 120

18

19

24 27

3

3

4 5

54

66

85 92

1,424

-

500

1,000

1,500

2007 2008 2009 2010 2011(E)

Other countries

Indonesia

UK

Malaysia

Iran

GCC

(USD in mn)

639

822

1,0361,139

1,424

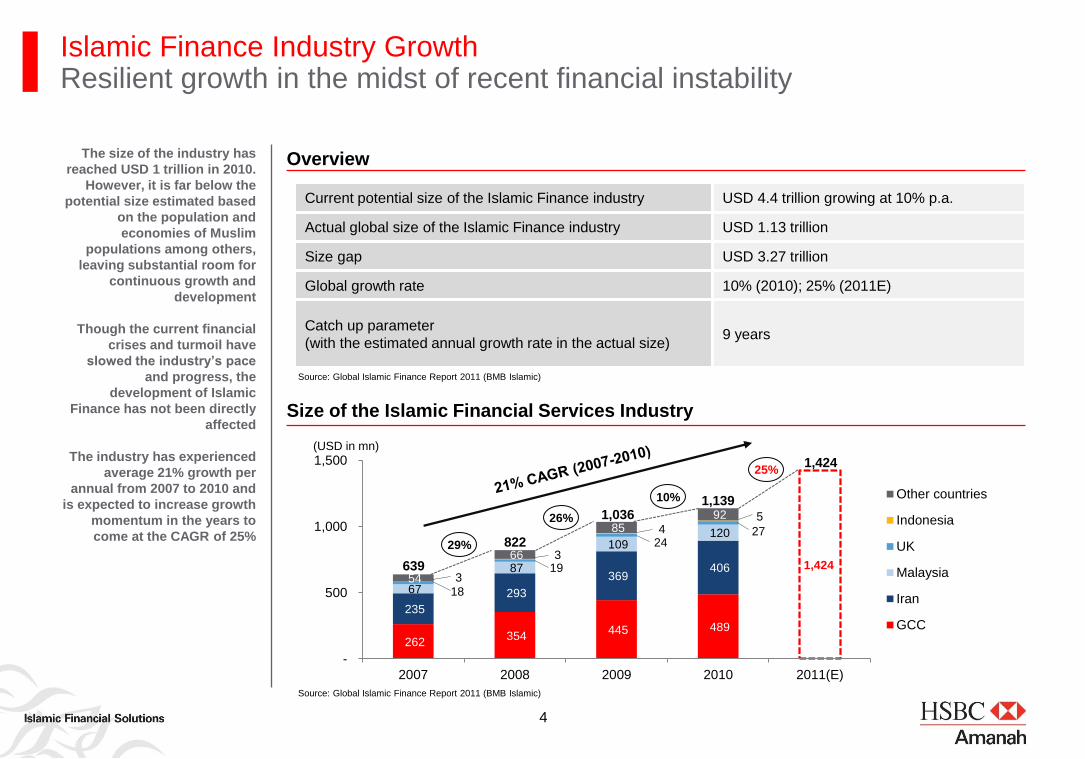

Current potential size of the Islamic Finance industry USD 4.4 trillion growing at 10% p.a.

Actual global size of the Islamic Finance industry USD 1.13 trillion

Size gap USD 3.27 trillion

Global growth rate 10% (2010); 25% (2011E)

Catch up parameter

(with the estimated annual growth rate in the actual size) 9 years

Source: Global Islamic Finance Report 2011 (BMB Islamic)

Source: Global Islamic Finance Report 2011 (BMB Islamic)

29%

26%

10%

25%

Islamic Finance Industry Growth Resilient growth in the midst of recent financial instability

The size of the industry has

reached USD 1 trillion in 2010.

However, it is far below the

potential size estimated based

on the population and

economies of Muslim

populations among others,

leaving substantial room for

continuous growth and

development

Though the current financial

crises and turmoil have

slowed the industry’s pace

and progress, the

development of Islamic

Finance has not been directly

affected

The industry has experienced

average 21% growth per

annual from 2007 to 2010 and

is expected to increase growth

momentum in the years to

come at the CAGR of 25%

Size of the Islamic Financial Services Industry

Overview

5

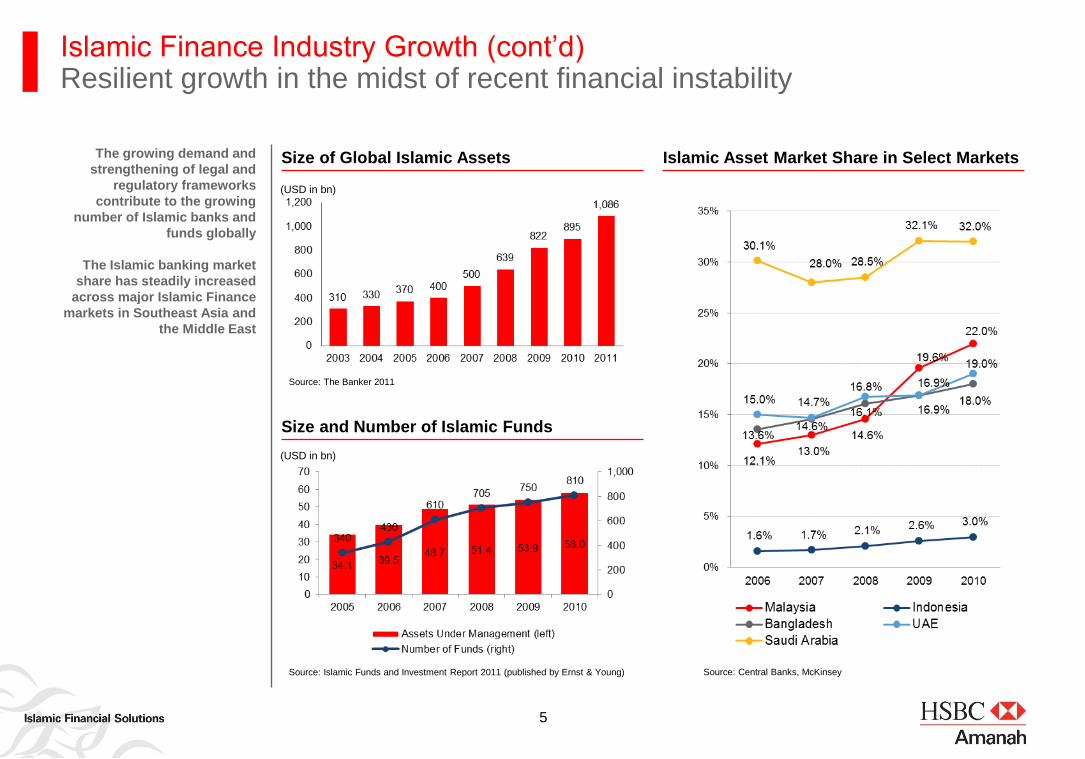

Islamic Finance Industry Growth (cont‟d) Resilient growth in the midst of recent financial instability

The growing demand and

strengthening of legal and

regulatory frameworks

contribute to the growing

number of Islamic banks and

funds globally

The Islamic banking market

share has steadily increased

across major Islamic Finance

markets in Southeast Asia and

the Middle East

Source: Islamic Funds and Investment Report 2011 (published by Ernst & Young)

Source: The Banker 2011

(USD in bn)

Source: Central Banks, McKinsey

Islamic Asset Market Share in Select Markets Size of Global Islamic Assets

Size and Number of Islamic Funds

(USD in bn)

6

1) Islamic Development Bank

2) Organization of the Islamic Conference

3) Accounting and Auditing Organisation for Islamic Financial Institutions

4) Islamic Financial Services Board

5) International Islamic Liquidity Management

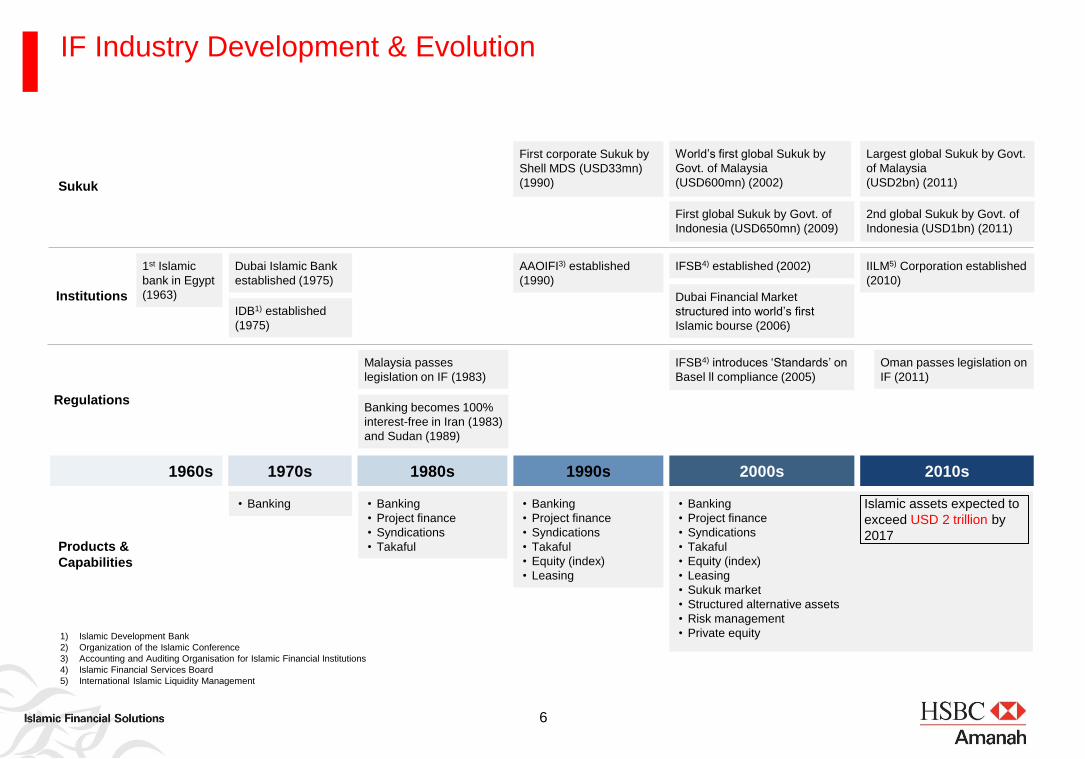

1960s 1970s 1980s 1990s 2000s 2010s

• Banking • Banking

• Project finance

• Syndications

• Takaful

• Banking

• Project finance

• Syndications

• Takaful

• Equity (index)

• Leasing

• Banking

• Project finance

• Syndications

• Takaful

• Equity (index)

• Leasing

• Sukuk market

• Structured alternative assets

• Risk management

• Private equity

Products &

Capabilities

Sukuk

Institutions

Regulations

1st Islamic

bank in Egypt

(1963)

IDB1) established

(1975)

Dubai Islamic Bank

established (1975)

Malaysia passes

legislation on IF (1983)

Banking becomes 100%

interest-free in Iran (1983)

and Sudan (1989)

AAOIFI3) established

(1990)

World‟s first global Sukuk by

Govt. of Malaysia

(USD600mn) (2002)

IFSB4) established (2002)

IFSB4) introduces „Standards‟ on

Basel ll compliance (2005)

First global Sukuk by Govt. of

Indonesia (USD650mn) (2009)

Islamic assets expected to

exceed USD 2 trillion by

2017

Largest global Sukuk by Govt.

of Malaysia

(USD2bn) (2011)

First corporate Sukuk by

Shell MDS (USD33mn)

(1990)

Oman passes legislation on

IF (2011)

IILM5) Corporation established

(2010)

Dubai Financial Market

structured into world‟s first

Islamic bourse (2006)

2nd global Sukuk by Govt. of

Indonesia (USD1bn) (2011)

IF Industry Development & Evolution

Overview of Sukuk Market

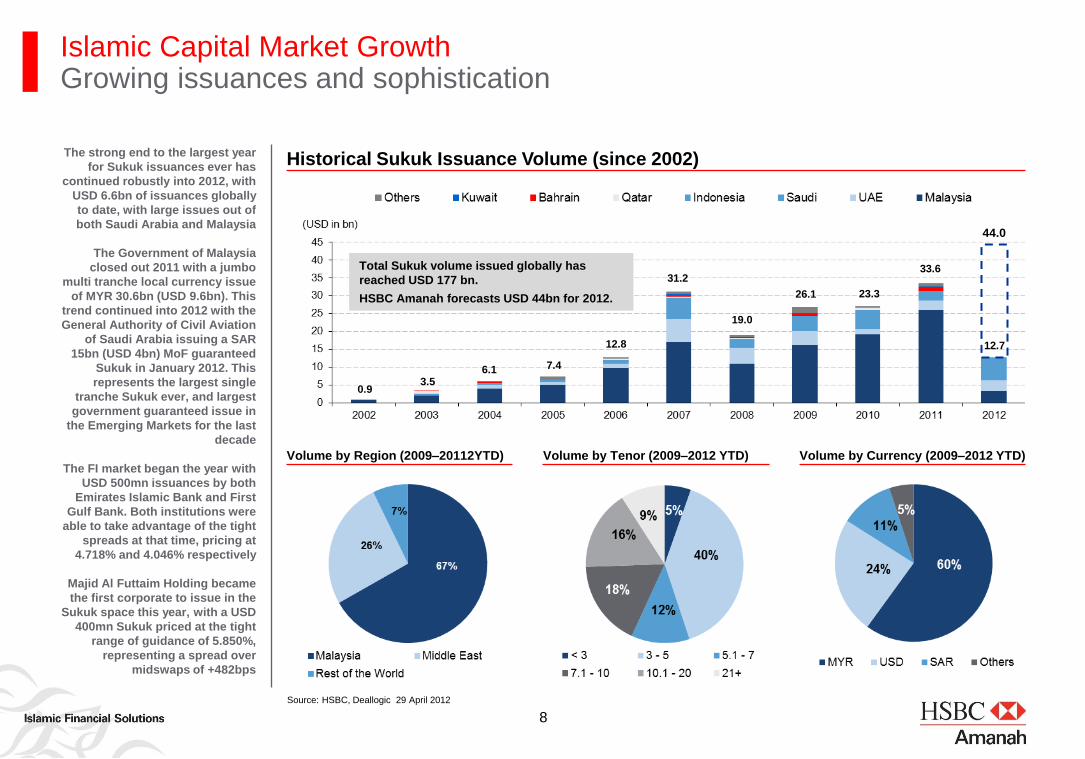

8

Total Sukuk volume issued globally has

reached USD 177 bn.

HSBC Amanah forecasts USD 44bn for 2012.

0.9 3.5

6.1 7.4

12.8

31.2

19.0

26.1 23.3

33.6

12.7

Islamic Capital Market Growth Growing issuances and sophistication

The strong end to the largest year

for Sukuk issuances ever has

continued robustly into 2012, with

USD 6.6bn of issuances globally

to date, with large issues out of

both Saudi Arabia and Malaysia

The Government of Malaysia

closed out 2011 with a jumbo

multi tranche local currency issue

of MYR 30.6bn (USD 9.6bn). This

trend continued into 2012 with the

General Authority of Civil Aviation

of Saudi Arabia issuing a SAR

15bn (USD 4bn) MoF guaranteed

Sukuk in January 2012. This

represents the largest single

tranche Sukuk ever, and largest

government guaranteed issue in

the Emerging Markets for the last

decade

The FI market began the year with

USD 500mn issuances by both

Emirates Islamic Bank and First

Gulf Bank. Both institutions were

able to take advantage of the tight

spreads at that time, pricing at

4.718% and 4.046% respectively

Majid Al Futtaim Holding became

the first corporate to issue in the

Sukuk space this year, with a USD

400mn Sukuk priced at the tight

range of guidance of 5.850%,

representing a spread over

midswaps of +482bps

Historical Sukuk Issuance Volume (since 2002)

Volume by Region (2009–20112YTD) Volume by Currency (2009–2012 YTD) Volume by Tenor (2009–2012 YTD)

Source: HSBC, Deallogic 29 April 2012

44.0

9

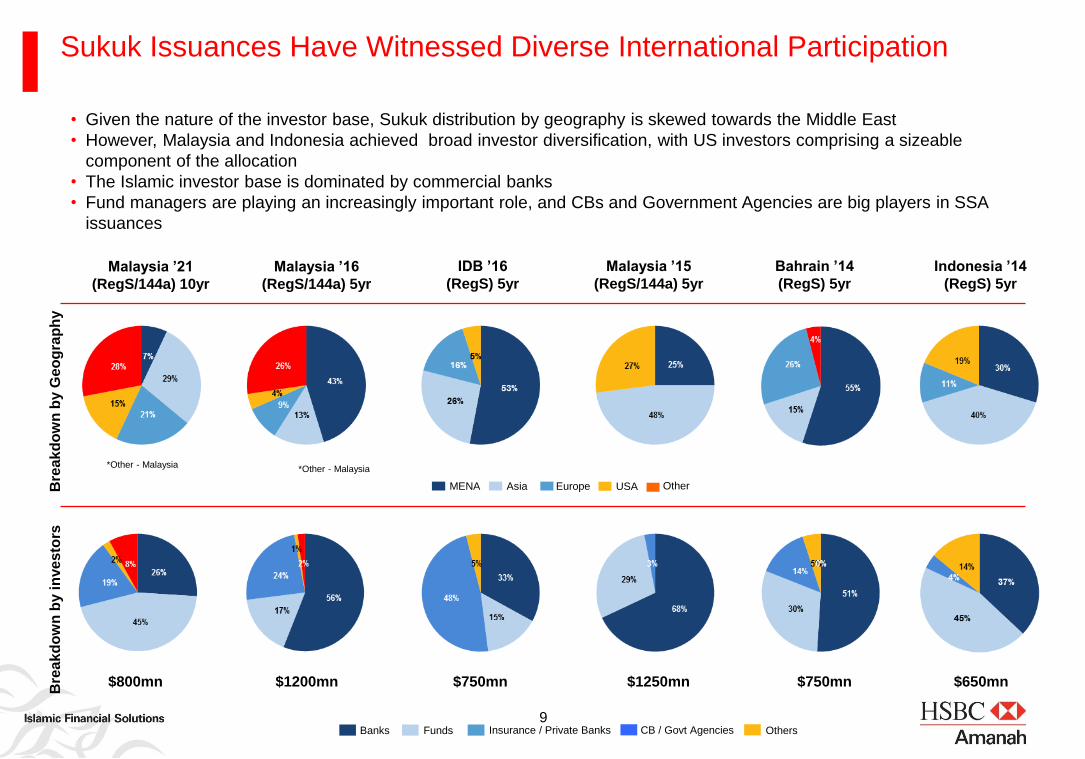

MENA

• Given the nature of the investor base, Sukuk distribution by geography is skewed towards the Middle East

• However, Malaysia and Indonesia achieved broad investor diversification, with US investors comprising a sizeable

component of the allocation

• The Islamic investor base is dominated by commercial banks

• Fund managers are playing an increasingly important role, and CBs and Government Agencies are big players in SSA

issuances

Sukuk Issuances Have Witnessed Diverse International Participation

USA

Bre

ak

do

wn

by i

nve

sto

rs

Bre

ak

do

wn

by G

eo

gra

ph

y

Asia Europe Other

Banks Funds Insurance / Private Banks Others CB / Govt Agencies

*Other - Malaysia *Other - Malaysia

$1250mn $750mn $1200mn $800mn $650mn $750mn

Malaysia ’21

(RegS/144a) 10yr

Malaysia ’16

(RegS/144a) 5yr

IDB ’16

(RegS) 5yr

Malaysia ’15

(RegS/144a) 5yr

Bahrain ’14

(RegS) 5yr

Indonesia ’14

(RegS) 5yr

10

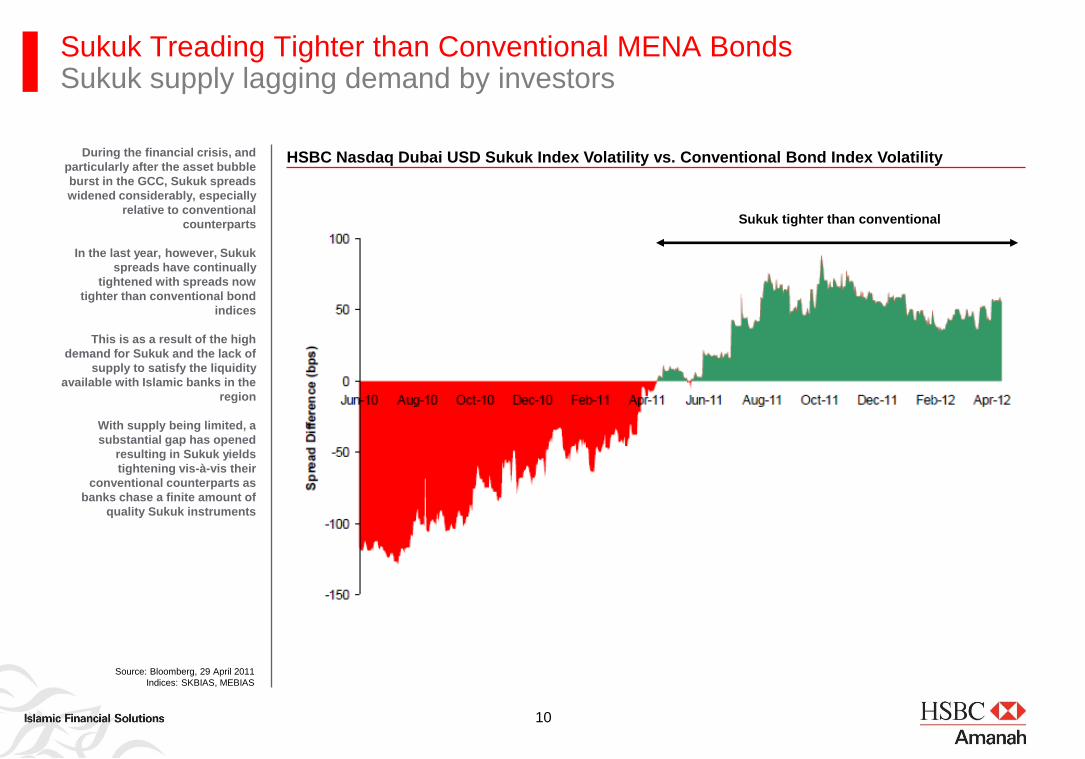

Sukuk Treading Tighter than Conventional MENA Bonds Sukuk supply lagging demand by investors

During the financial crisis, and

particularly after the asset bubble

burst in the GCC, Sukuk spreads

widened considerably, especially

relative to conventional

counterparts

In the last year, however, Sukuk

spreads have continually

tightened with spreads now

tighter than conventional bond

indices

This is as a result of the high

demand for Sukuk and the lack of

supply to satisfy the liquidity

available with Islamic banks in the

region

With supply being limited, a

substantial gap has opened

resulting in Sukuk yields

tightening vis-à-vis their

conventional counterparts as

banks chase a finite amount of

quality Sukuk instruments

Source: Bloomberg, 29 April 2011

Indices: SKBIAS, MEBIAS

HSBC Nasdaq Dubai USD Sukuk Index Volatility vs. Conventional Bond Index Volatility

Sukuk tighter than conventional

Sukuk Structures

Sukuk Structures

A. Ijara Sukuk (Sale & Leaseback)

13

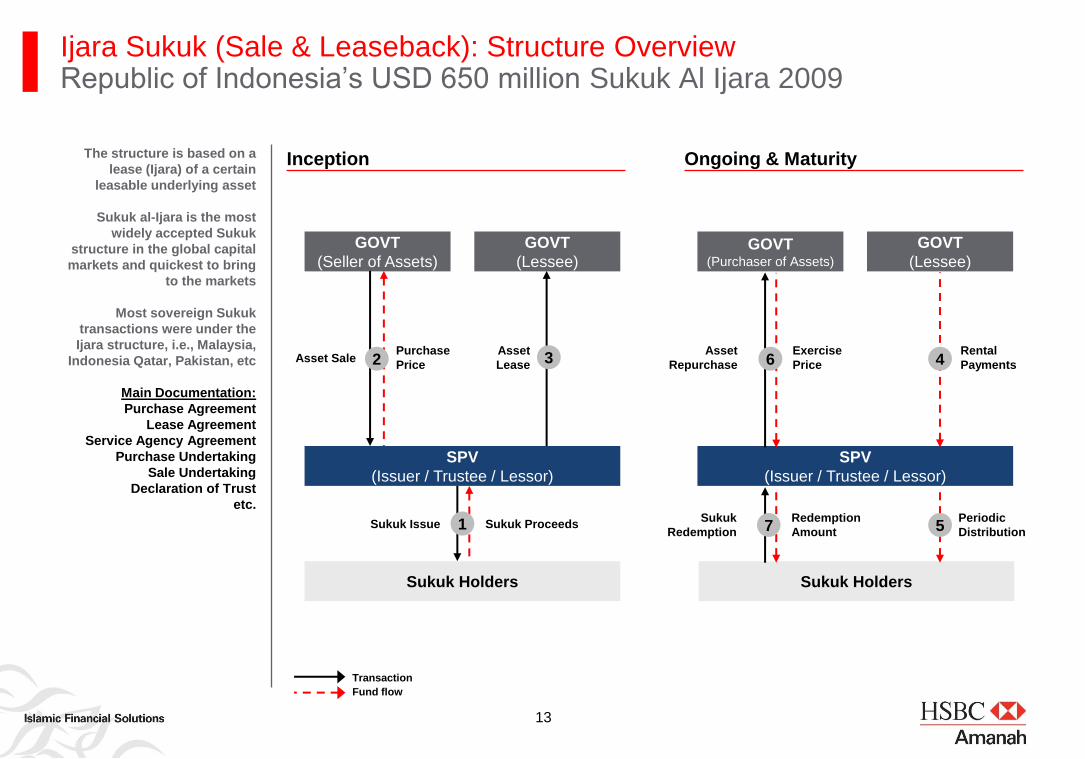

Ijara Sukuk (Sale & Leaseback): Structure Overview Republic of Indonesia‟s USD 650 million Sukuk Al Ijara 2009

SPV

(Issuer / Trustee / Lessor)

Sukuk Proceeds Sukuk Issue

GOVT

(Seller of Assets)

Sukuk Holders

Purchase

Price

GOVT

(Lessee)

Asset

Lease

SPV

(Issuer / Trustee / Lessor)

Sukuk Holders

Asset Sale

1

2 3 Rental

Payments

GOVT

(Lessee)

Periodic

Distribution

4

5

Asset

Repurchase

Exercise

Price

Redemption

Amount

Sukuk

Redemption

GOVT (Purchaser of Assets)

6

7

The structure is based on a

lease (Ijara) of a certain

leasable underlying asset

Sukuk al-Ijara is the most

widely accepted Sukuk

structure in the global capital

markets and quickest to bring

to the markets

Most sovereign Sukuk

transactions were under the

Ijara structure, i.e., Malaysia,

Indonesia Qatar, Pakistan, etc

Main Documentation:

Purchase Agreement

Lease Agreement

Service Agency Agreement

Purchase Undertaking

Sale Undertaking

Declaration of Trust

etc.

Inception Ongoing & Maturity

Transaction

Fund flow

14

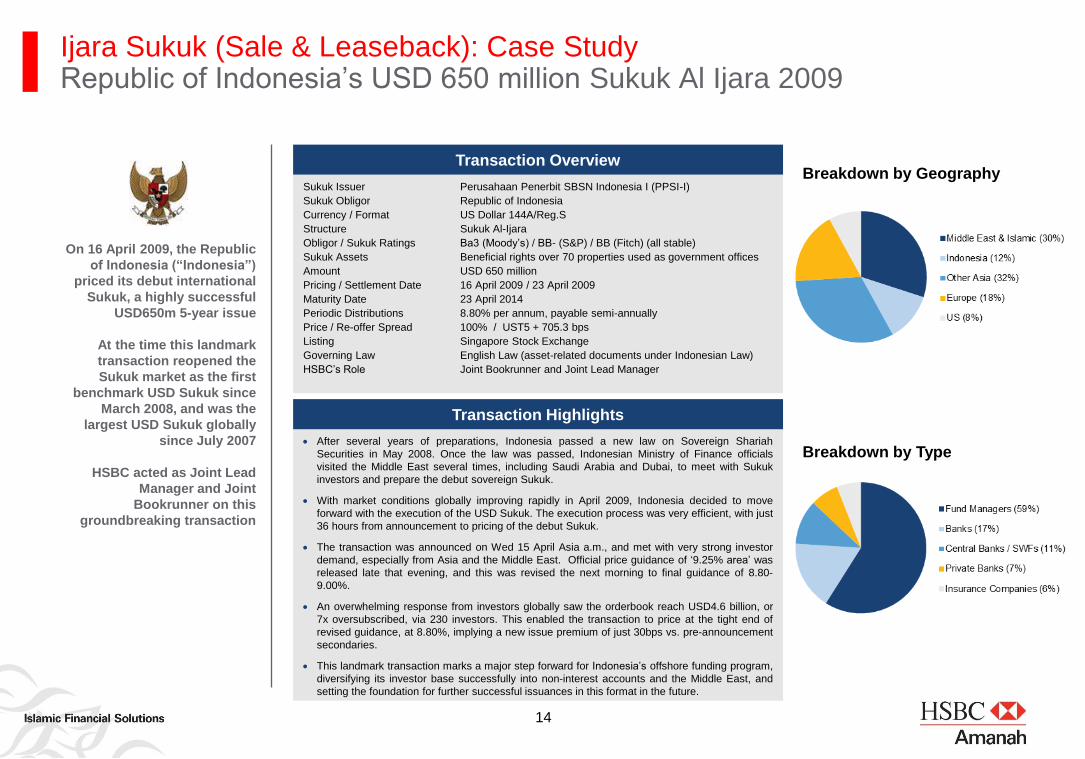

On 16 April 2009, the Republic

of Indonesia (“Indonesia”)

priced its debut international

Sukuk, a highly successful

USD650m 5-year issue

At the time this landmark

transaction reopened the

Sukuk market as the first

benchmark USD Sukuk since

March 2008, and was the

largest USD Sukuk globally

since July 2007

HSBC acted as Joint Lead

Manager and Joint

Bookrunner on this

groundbreaking transaction

After several years of preparations, Indonesia passed a new law on Sovereign Shariah

Securities in May 2008. Once the law was passed, Indonesian Ministry of Finance officials

visited the Middle East several times, including Saudi Arabia and Dubai, to meet with Sukuk

investors and prepare the debut sovereign Sukuk.

With market conditions globally improving rapidly in April 2009, Indonesia decided to move

forward with the execution of the USD Sukuk. The execution process was very efficient, with just

36 hours from announcement to pricing of the debut Sukuk.

The transaction was announced on Wed 15 April Asia a.m., and met with very strong investor

demand, especially from Asia and the Middle East. Official price guidance of „9.25% area‟ was

released late that evening, and this was revised the next morning to final guidance of 8.80-

9.00%.

An overwhelming response from investors globally saw the orderbook reach USD4.6 billion, or

7x oversubscribed, via 230 investors. This enabled the transaction to price at the tight end of

revised guidance, at 8.80%, implying a new issue premium of just 30bps vs. pre-announcement

secondaries.

This landmark transaction marks a major step forward for Indonesia‟s offshore funding program,

diversifying its investor base successfully into non-interest accounts and the Middle East, and

setting the foundation for further successful issuances in this format in the future.

Sukuk Issuer Perusahaan Penerbit SBSN Indonesia I (PPSI-I)

Sukuk Obligor Republic of Indonesia

Currency / Format US Dollar 144A/Reg.S

Structure Sukuk Al-Ijara

Obligor / Sukuk Ratings Ba3 (Moody‟s) / BB- (S&P) / BB (Fitch) (all stable)

Sukuk Assets Beneficial rights over 70 properties used as government offices

Amount USD 650 million

Pricing / Settlement Date 16 April 2009 / 23 April 2009

Maturity Date 23 April 2014

Periodic Distributions 8.80% per annum, payable semi-annually

Price / Re-offer Spread 100% / UST5 + 705.3 bps

Listing Singapore Stock Exchange

Governing Law English Law (asset-related documents under Indonesian Law)

HSBC‟s Role Joint Bookrunner and Joint Lead Manager

Transaction Overview

Transaction Highlights

Breakdown by Geography

Breakdown by Type

Ijara Sukuk (Sale & Leaseback): Case Study Republic of Indonesia‟s USD 650 million Sukuk Al Ijara 2009

Sukuk Structures

B. Wakala Sukuk

16

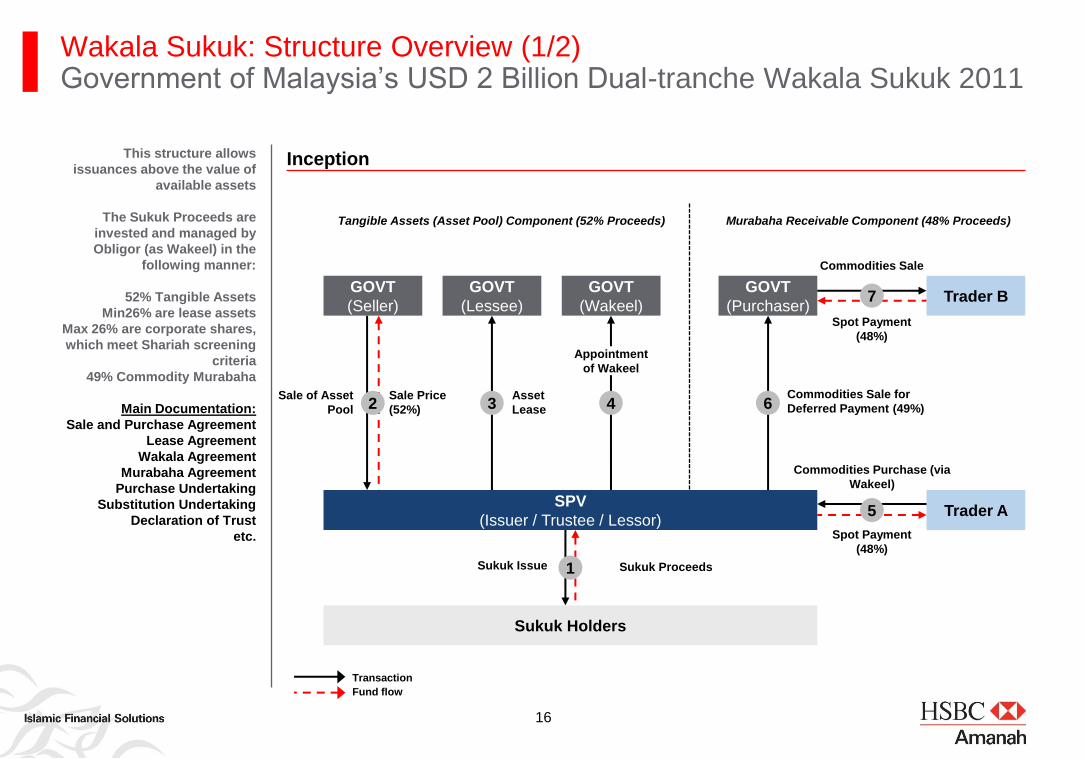

Sukuk Proceeds Sukuk Issue

Sale of Asset

Pool

Sale Price

(52%)

SPV

(Issuer / Trustee / Lessor)

Sukuk Holders

GOVT

(Seller)

GOVT

(Lessee)

GOVT

(Wakeel)

GOVT

(Purchaser)

Trader A

Trader B

Appointment

of Wakeel

Commodities Purchase (via

Wakeel)

Spot Payment

(48%)

Commodities Sale for

Deferred Payment (49%)

Commodities Sale

Spot Payment

(48%)

Murabaha Receivable Component (48% Proceeds) Tangible Assets (Asset Pool) Component (52% Proceeds)

Asset

Lease

1

2 3 4

5

6

7

Wakala Sukuk: Structure Overview (1/2) Government of Malaysia‟s USD 2 Billion Dual-tranche Wakala Sukuk 2011

This structure allows

issuances above the value of

available assets

The Sukuk Proceeds are

invested and managed by

Obligor (as Wakeel) in the

following manner:

52% Tangible Assets

Min26% are lease assets

Max 26% are corporate shares,

which meet Shariah screening

criteria

49% Commodity Murabaha

Main Documentation:

Sale and Purchase Agreement

Lease Agreement

Wakala Agreement

Murabaha Agreement

Purchase Undertaking

Substitution Undertaking

Declaration of Trust

etc.

Inception

Transaction

Fund flow

17

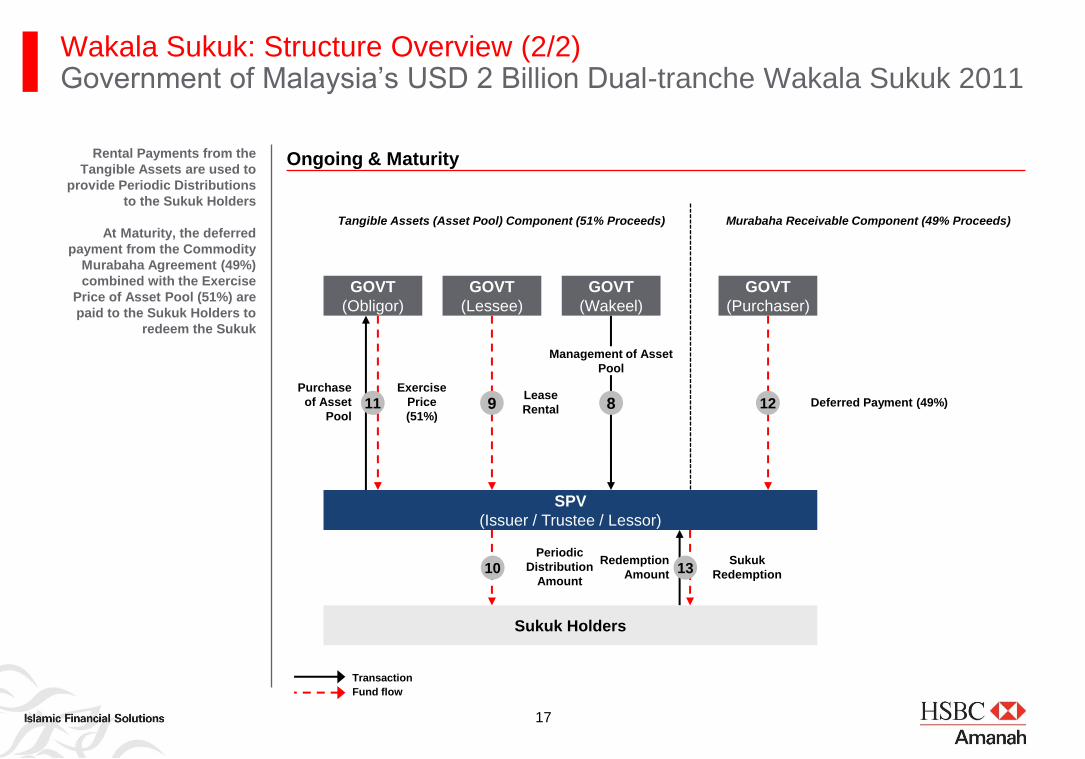

Redemption

Amount

Sukuk

Redemption

Purchase

of Asset

Pool

Exercise

Price

(51%)

Lease

Rental

GOVT

(Obligor)

Management of Asset

Pool

Deferred Payment (49%)

Murabaha Receivable Component (49% Proceeds) Tangible Assets (Asset Pool) Component (51% Proceeds)

Periodic

Distribution

Amount

8 9 11 12

10 13

Wakala Sukuk: Structure Overview (2/2) Government of Malaysia‟s USD 2 Billion Dual-tranche Wakala Sukuk 2011

Rental Payments from the

Tangible Assets are used to

provide Periodic Distributions

to the Sukuk Holders

At Maturity, the deferred

payment from the Commodity

Murabaha Agreement (49%)

combined with the Exercise

Price of Asset Pool (51%) are

paid to the Sukuk Holders to

redeem the Sukuk

Ongoing & Maturity

SPV

(Issuer / Trustee / Lessor)

Sukuk Holders

GOVT

(Lessee)

GOVT

(Wakeel)

GOVT

(Purchaser)

Transaction

Fund flow

18

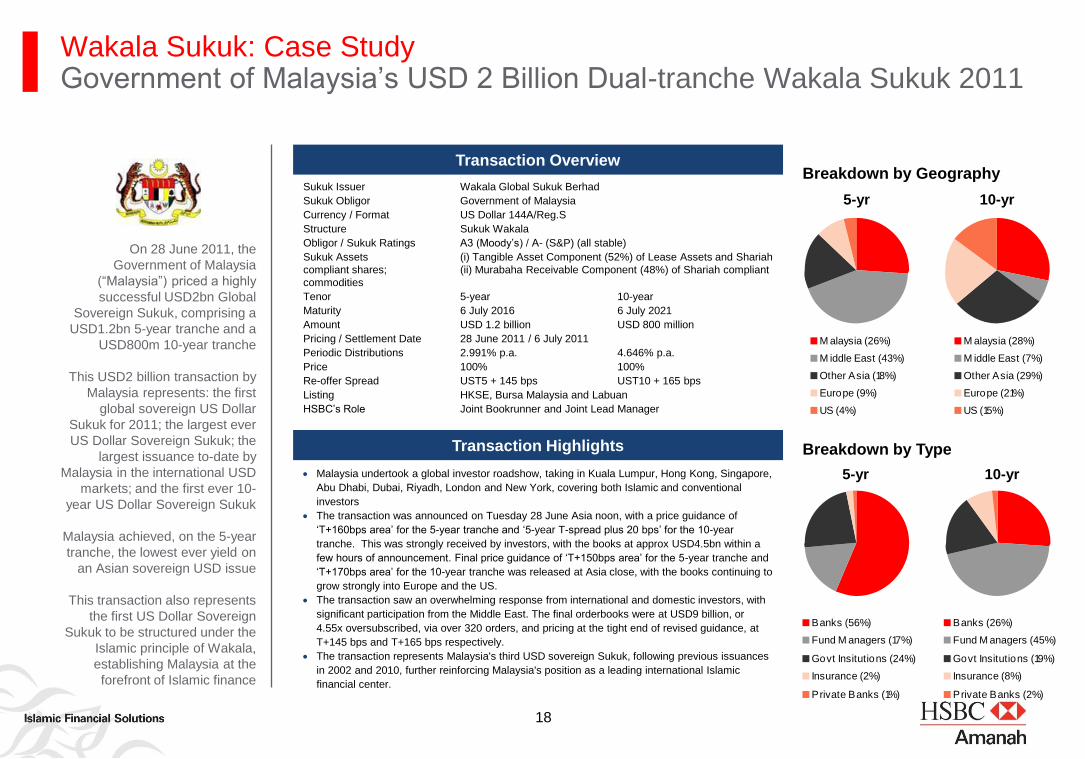

Banks (56%)

Fund M anagers (17%)

Govt Insitutions (24%)

Insurance (2%)

Private Banks (1%)

Banks (26%)

Fund M anagers (45%)

Govt Insitutions (19%)

Insurance (8%)

Private Banks (2%)

M alaysia (26%)

M iddle East (43%)

Other Asia (18%)

Europe (9%)

US (4%)

M alaysia (28%)

M iddle East (7%)

Other Asia (29%)

Europe (21%)

US (15%)

Sukuk Issuer Wakala Global Sukuk Berhad

Sukuk Obligor Government of Malaysia

Currency / Format US Dollar 144A/Reg.S

Structure Sukuk Wakala

Obligor / Sukuk Ratings A3 (Moody‟s) / A- (S&P) (all stable)

Sukuk Assets (i) Tangible Asset Component (52%) of Lease Assets and Shariah

compliant shares; (ii) Murabaha Receivable Component (48%) of Shariah compliant

commodities

Tenor 5-year 10-year

Maturity 6 July 2016 6 July 2021

Amount USD 1.2 billion USD 800 million

Pricing / Settlement Date 28 June 2011 / 6 July 2011

Periodic Distributions 2.991% p.a. 4.646% p.a.

Price 100% 100%

Re-offer Spread UST5 + 145 bps UST10 + 165 bps

Listing HKSE, Bursa Malaysia and Labuan

HSBC‟s Role Joint Bookrunner and Joint Lead Manager

Malaysia undertook a global investor roadshow, taking in Kuala Lumpur, Hong Kong, Singapore,

Abu Dhabi, Dubai, Riyadh, London and New York, covering both Islamic and conventional

investors

The transaction was announced on Tuesday 28 June Asia noon, with a price guidance of

„T+160bps area‟ for the 5-year tranche and „5-year T-spread plus 20 bps‟ for the 10-year

tranche. This was strongly received by investors, with the books at approx USD4.5bn within a

few hours of announcement. Final price guidance of „T+150bps area‟ for the 5-year tranche and

„T+170bps area‟ for the 10-year tranche was released at Asia close, with the books continuing to

grow strongly into Europe and the US.

The transaction saw an overwhelming response from international and domestic investors, with

significant participation from the Middle East. The final orderbooks were at USD9 billion, or

4.55x oversubscribed, via over 320 orders, and pricing at the tight end of revised guidance, at

T+145 bps and T+165 bps respectively.

The transaction represents Malaysia's third USD sovereign Sukuk, following previous issuances

in 2002 and 2010, further reinforcing Malaysia's position as a leading international Islamic

financial center.

10-yr 5-yr

10-yr 5-yr

Wakala Sukuk: Case Study Government of Malaysia‟s USD 2 Billion Dual-tranche Wakala Sukuk 2011

On 28 June 2011, the

Government of Malaysia

(“Malaysia”) priced a highly

successful USD2bn Global

Sovereign Sukuk, comprising a

USD1.2bn 5-year tranche and a

USD800m 10-year tranche

This USD2 billion transaction by

Malaysia represents: the first

global sovereign US Dollar

Sukuk for 2011; the largest ever

US Dollar Sovereign Sukuk; the

largest issuance to-date by

Malaysia in the international USD

markets; and the first ever 10-

year US Dollar Sovereign Sukuk

Malaysia achieved, on the 5-year

tranche, the lowest ever yield on

an Asian sovereign USD issue

This transaction also represents

the first US Dollar Sovereign

Sukuk to be structured under the

Islamic principle of Wakala,

establishing Malaysia at the

forefront of Islamic finance

Transaction Overview

Transaction Highlights

Breakdown by Geography

Breakdown by Type

Sukuk Structures

C. Istithmar Sukuk

20

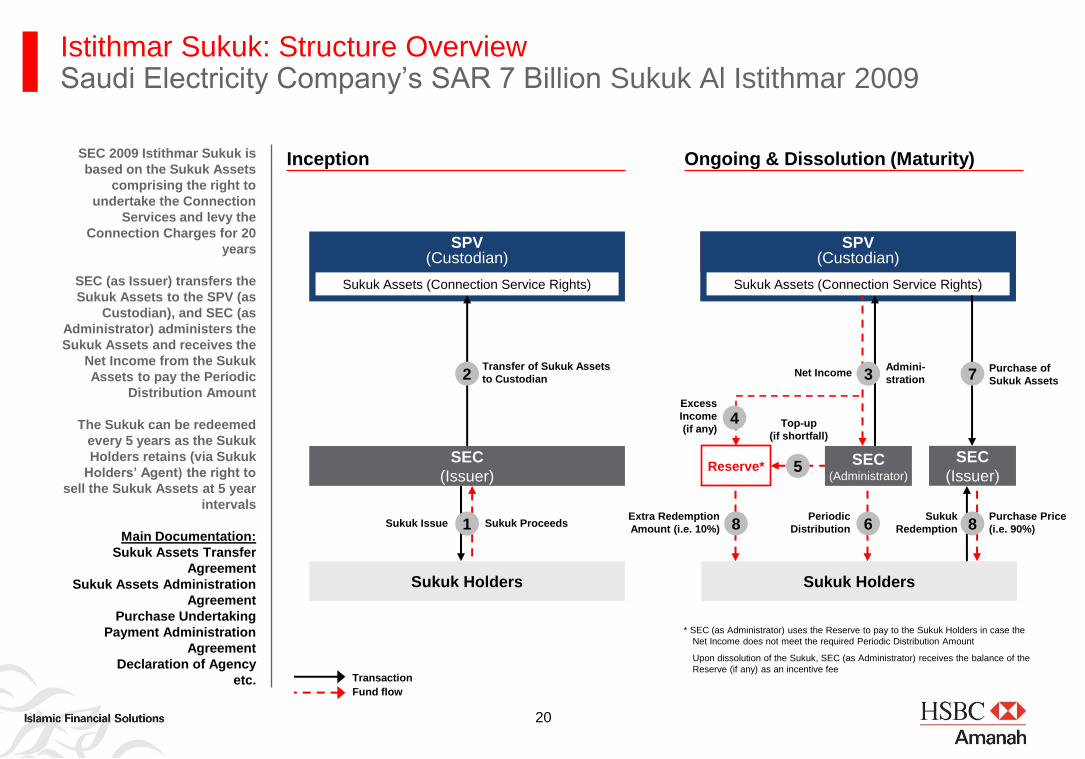

SPV (Custodian)

Excess

Income

(if any)

* SEC (as Administrator) uses the Reserve to pay to the Sukuk Holders in case the

Net Income does not meet the required Periodic Distribution Amount

Upon dissolution of the Sukuk, SEC (as Administrator) receives the balance of the

Reserve (if any) as an incentive fee

SEC

(Issuer)

Sukuk Holders

SEC

(Issuer / Trustee / Lessor)

Sukuk Holders

Sukuk Proceeds Sukuk Issue

Net Income

Periodic

Distribution

Purchase Price

(i.e. 90%)

Sukuk Assets (Connection Service Rights)

SPV (Custodian)

Sukuk Assets (Connection Service Rights)

SEC (Administrator)

Reserve*

Transfer of Sukuk Assets

to Custodian

Top-up

(if shortfall)

Purchase of

Sukuk Assets

Sukuk

Redemption

Admini-

stration

SEC

(Issuer)

1

2 7

8

3

4

5

6 8 Extra Redemption

Amount (i.e. 10%)

Istithmar Sukuk: Structure Overview Saudi Electricity Company‟s SAR 7 Billion Sukuk Al Istithmar 2009

Inception Ongoing & Dissolution (Maturity)

Transaction

Fund flow

SEC 2009 Istithmar Sukuk is

based on the Sukuk Assets

comprising the right to

undertake the Connection

Services and levy the

Connection Charges for 20

years

SEC (as Issuer) transfers the

Sukuk Assets to the SPV (as

Custodian), and SEC (as

Administrator) administers the

Sukuk Assets and receives the

Net Income from the Sukuk

Assets to pay the Periodic

Distribution Amount

The Sukuk can be redeemed

every 5 years as the Sukuk

Holders retains (via Sukuk

Holders’ Agent) the right to

sell the Sukuk Assets at 5 year

intervals

Main Documentation:

Sukuk Assets Transfer

Agreement

Sukuk Assets Administration

Agreement

Purchase Undertaking

Payment Administration

Agreement

Declaration of Agency

etc.

21

Put Option Exercise Timing Up to

Year 5

End of

Year 5

End of

Year 10

End of

Year 15

End of

Year 20

Purchase Price 100% 90% 60% 30% 0%

Extra Amount 0% 10% 20% 30% 40%

Total Face Value Received

(Redemption Amount) 100% 100% 80% 60% 40%

Istithmar Sukuk: Dissolution/Maturity Payment Options Saudi Electricity Company‟s SAR 7 Billion Sukuk Al Istithmar 2009

The maturity of the Sukuk is 20

years, but the Sukuk Holders

may request the purchase of

the Sukuk by the Issuer every

5 years, pursuant to the

Purchase Undertaking

The Sukuk Holders have an

incentive to exercise their right

to put the Sukuk at the end of

Year 5 to receive 100% of the

Suck's face value (i.e. 90%

Purchase Price and 10% Extra

Amount); after the end of Year

5, the Redemption Amount

gradually decreases after the

end of Year 5

In case the Net Income is not

sufficient to pay a Periodic

Distribution during the first 5

years, the Sukuk Holders have

the right to require the Issuer

to purchase their Sukuk for

100% of the total face value

22

For the second time in succession, HSBC lead managed for SEC (the largest utility company by

market value in the Middle East) a successful public Sukuk issuance in the Saudi Arabian

market, the first such public Sukuk in 2009

HSBC also acted as the sole rating advisor, assisting SEC in securing rating for both Sukuk.

The HSBC Amanah Shariah Supervisory Committee approved the structure, and SABB

Securities Ltd acted as Sukukholders‟ Agent

Notwithstanding the volatile credit environment, HSBC successfully positioned SEC‟s credit as

very closely aligned to the sovereign, and helped devise and execute a successful book-building

strategy to generate demand

As a result, the issuance was very well received by the market with total orders exceeding SAR

20.5 billion (USD 5.6 billion), incorporating existing and new investors

This helped SEC issue at a size of SAR 7 billion (the largest issuance by a GCC utility), at a

price tighter than similar-rated issuances by sovereigns or corporates in the region

This transaction firmly cements HSBC leadership in the Saudi market, having led all public

issuances in the Kingdom. HSBC has now raised SAR 28 billion in the public format since sole

leading the market‟s debut issuance in 2006

Issuer: Saudi Electricity Company (“SEC”)

Rating: A1/AA-/AA-

Structure: Sukuk Al Istithmar

Sukuk rating: AA- (Fitch)

Issue Date: 06 July 2009

Maturity Date: 06 July 2029 (first Put: 06 July 2014)

Issue Amount: SAR 7 billion (USD 1.9 billion)

Coupon/Profit: 3m SAR Sibor + 160 bps

HSBC‟s Role Joint Lead Manager and Bookrunner

Istithmar Sukuk: Case Study Saudi Electricity Company‟s SAR 7 Billion Sukuk Al Istithmar 2009

On 6th July 2009, Saudi

Electricity Company issued a

SAR 7 billion Sukuk-al-

Isthithmar, its second such

issuance in the local market

This was the largest local

currency Sukuk or bond for a

utility in the GCC region, and

generated by far the largest

order book in Saudi Arabia for

any debt issuance

Prior to this HSBC sole led

SEC’s debut Sukuk issuance,

and has now lead managed all

public SAR issues in Saudi

Arabia

Transaction Overview

Transaction Highlights

Breakdown by Geography

(Issue is restricted to Saudi nationals

and entities only)

Breakdown by Type

Sukuk Structures

D. Manafae Sukuk

24

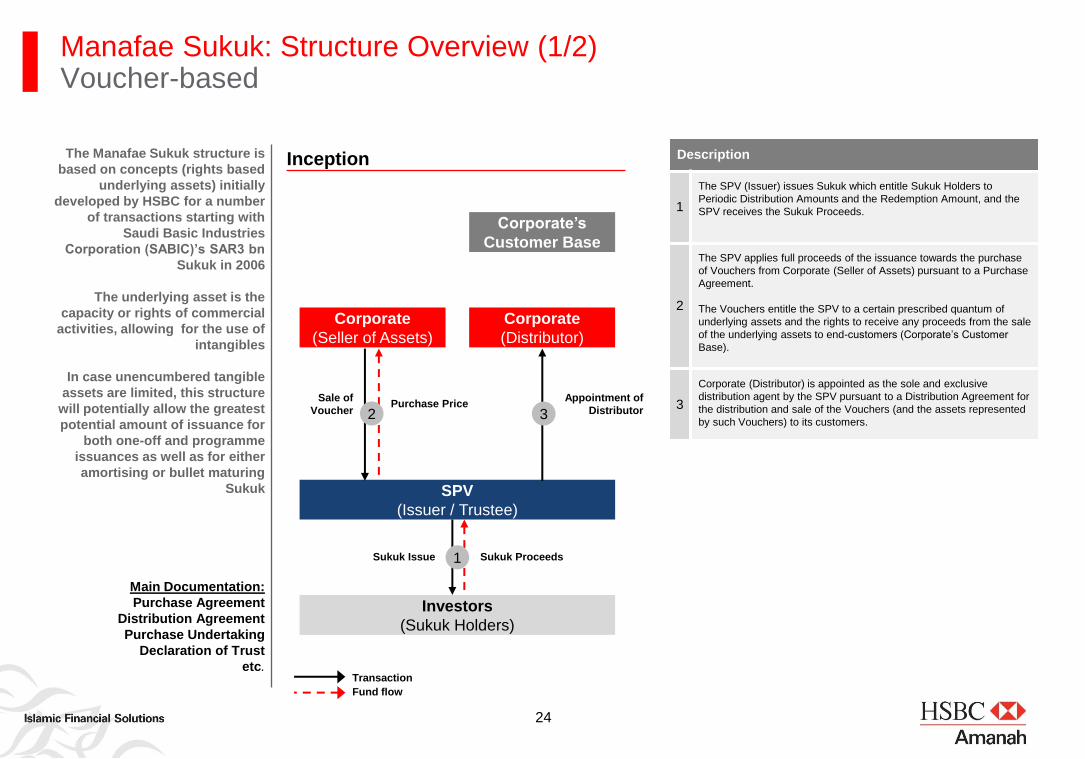

Manafae Sukuk: Structure Overview (1/2) Voucher-based

Main Documentation:

Purchase Agreement

Distribution Agreement

Purchase Undertaking

Declaration of Trust

etc.

The Manafae Sukuk structure is

based on concepts (rights based

underlying assets) initially

developed by HSBC for a number

of transactions starting with

Saudi Basic Industries

Corporation (SABIC)’s SAR3 bn

Sukuk in 2006

The underlying asset is the

capacity or rights of commercial

activities, allowing for the use of

intangibles

In case unencumbered tangible

assets are limited, this structure

will potentially allow the greatest

potential amount of issuance for

both one-off and programme

issuances as well as for either

amortising or bullet maturing

Sukuk

Purchase Price Sale of

Voucher

Appointment of

Distributor

Description

1

The SPV (Issuer) issues Sukuk which entitle Sukuk Holders to

Periodic Distribution Amounts and the Redemption Amount, and the

SPV receives the Sukuk Proceeds.

2

The SPV applies full proceeds of the issuance towards the purchase

of Vouchers from Corporate (Seller of Assets) pursuant to a Purchase

Agreement.

The Vouchers entitle the SPV to a certain prescribed quantum of

underlying assets and the rights to receive any proceeds from the sale

of the underlying assets to end-customers (Corporate‟s Customer

Base).

3

Corporate (Distributor) is appointed as the sole and exclusive

distribution agent by the SPV pursuant to a Distribution Agreement for

the distribution and sale of the Vouchers (and the assets represented

by such Vouchers) to its customers.

SPV

(Issuer / Trustee)

Sukuk Proceeds Sukuk Issue

Investors

(Sukuk Holders)

1

Corporate

(Seller of Assets)

Corporate

(Distributor)

2 3

Corporate’s

Customer Base

Transaction

Fund flow

Inception

25

Manafae Sukuk: Structure Overview (2/2) Voucher-based

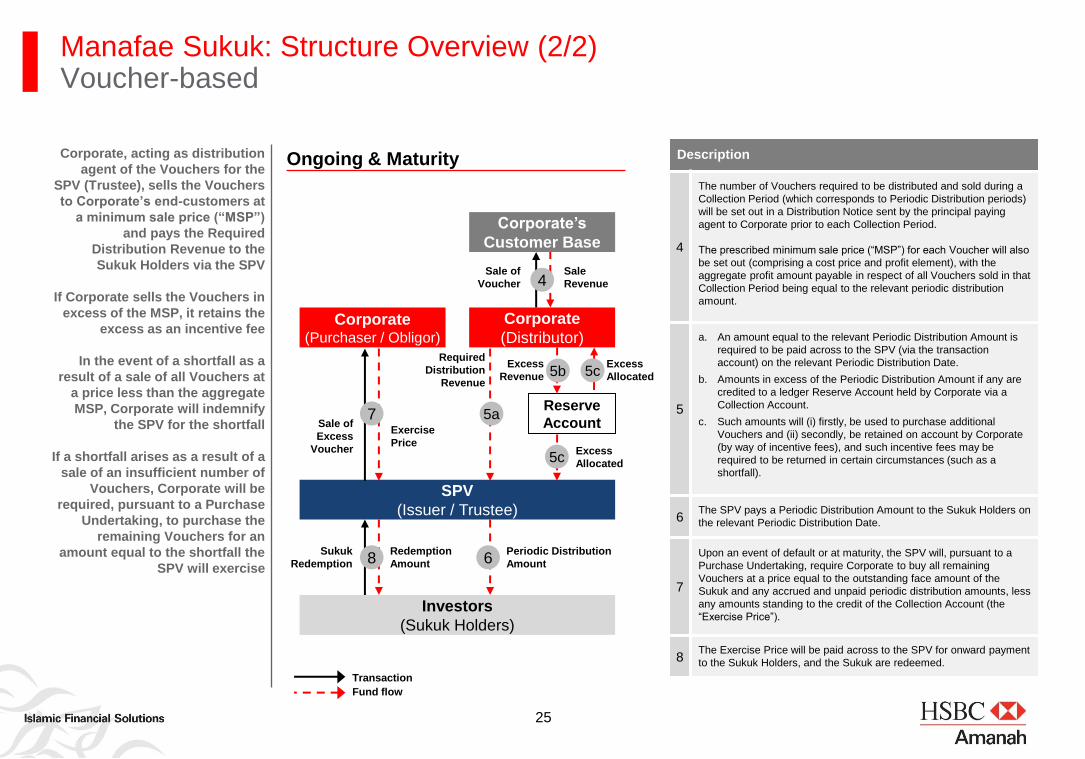

Corporate, acting as distribution

agent of the Vouchers for the

SPV (Trustee), sells the Vouchers

to Corporate’s end-customers at

a minimum sale price (“MSP”)

and pays the Required

Distribution Revenue to the

Sukuk Holders via the SPV

If Corporate sells the Vouchers in

excess of the MSP, it retains the

excess as an incentive fee

In the event of a shortfall as a

result of a sale of all Vouchers at

a price less than the aggregate

MSP, Corporate will indemnify

the SPV for the shortfall

If a shortfall arises as a result of a

sale of an insufficient number of

Vouchers, Corporate will be

required, pursuant to a Purchase

Undertaking, to purchase the

remaining Vouchers for an

amount equal to the shortfall the

SPV will exercise

Exercise

Price

Sale of

Excess

Voucher

Required

Distribution

Revenue

Description

4

The number of Vouchers required to be distributed and sold during a

Collection Period (which corresponds to Periodic Distribution periods)

will be set out in a Distribution Notice sent by the principal paying

agent to Corporate prior to each Collection Period.

The prescribed minimum sale price (“MSP”) for each Voucher will also

be set out (comprising a cost price and profit element), with the

aggregate profit amount payable in respect of all Vouchers sold in that

Collection Period being equal to the relevant periodic distribution

amount.

5

a. An amount equal to the relevant Periodic Distribution Amount is

required to be paid across to the SPV (via the transaction

account) on the relevant Periodic Distribution Date.

b. Amounts in excess of the Periodic Distribution Amount if any are

credited to a ledger Reserve Account held by Corporate via a

Collection Account.

c. Such amounts will (i) firstly, be used to purchase additional

Vouchers and (ii) secondly, be retained on account by Corporate

(by way of incentive fees), and such incentive fees may be

required to be returned in certain circumstances (such as a

shortfall).

6 The SPV pays a Periodic Distribution Amount to the Sukuk Holders on

the relevant Periodic Distribution Date.

7

Upon an event of default or at maturity, the SPV will, pursuant to a

Purchase Undertaking, require Corporate to buy all remaining

Vouchers at a price equal to the outstanding face amount of the

Sukuk and any accrued and unpaid periodic distribution amounts, less

any amounts standing to the credit of the Collection Account (the

“Exercise Price”).

8 The Exercise Price will be paid across to the SPV for onward payment

to the Sukuk Holders, and the Sukuk are redeemed.

SPV

(Issuer / Trustee)

Redemption

Amount

Sukuk

Redemption

Investors

(Sukuk Holders)

8

Corporate (Purchaser / Obligor)

Corporate

(Distributor)

7 5a

Corporate’s

Customer Base

4 Sale of

Voucher

Sale

Revenue

Reserve

Account

5b Excess

Revenue 5c

6 Periodic Distribution

Amount

5c Excess

Allocated

Excess

Allocated

Transaction

Fund flow

Ongoing & Maturity

Project Sukuk

27

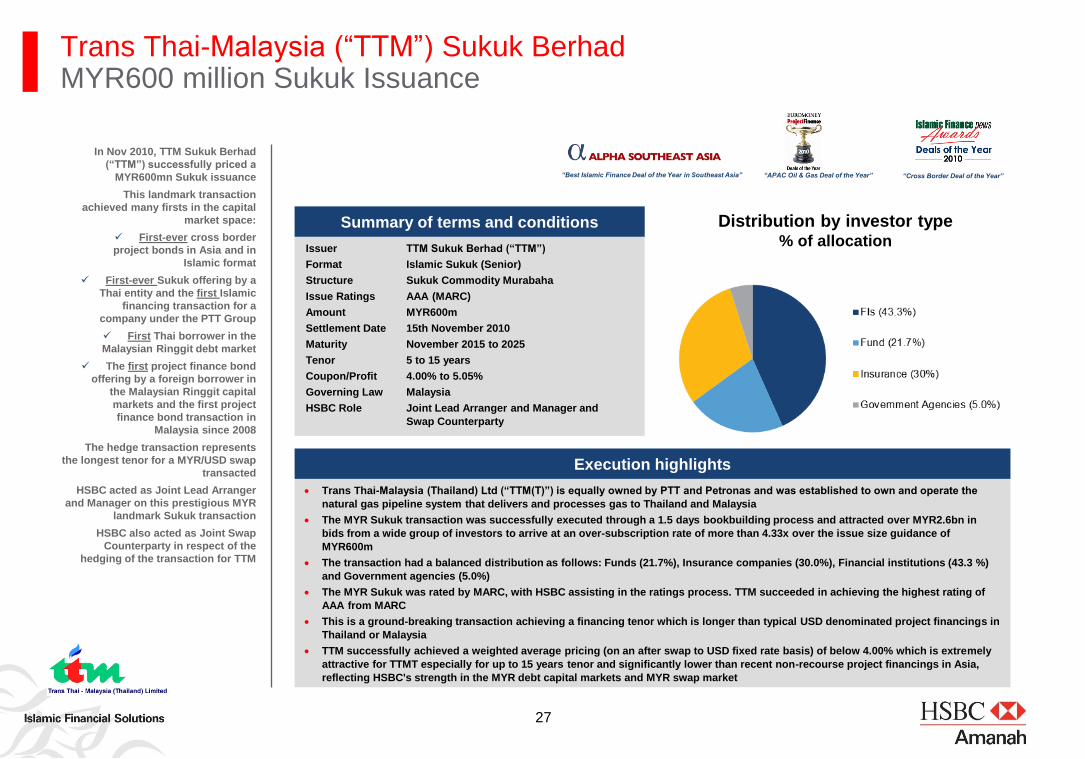

Trans Thai-Malaysia (Thailand) Ltd (“TTM(T)”) is equally owned by PTT and Petronas and was established to own and operate the

natural gas pipeline system that delivers and processes gas to Thailand and Malaysia

The MYR Sukuk transaction was successfully executed through a 1.5 days bookbuilding process and attracted over MYR2.6bn in

bids from a wide group of investors to arrive at an over-subscription rate of more than 4.33x over the issue size guidance of

MYR600m

The transaction had a balanced distribution as follows: Funds (21.7%), Insurance companies (30.0%), Financial institutions (43.3 %)

and Government agencies (5.0%)

The MYR Sukuk was rated by MARC, with HSBC assisting in the ratings process. TTM succeeded in achieving the highest rating of

AAA from MARC

This is a ground-breaking transaction achieving a financing tenor which is longer than typical USD denominated project financings in

Thailand or Malaysia

TTM successfully achieved a weighted average pricing (on an after swap to USD fixed rate basis) of below 4.00% which is extremely

attractive for TTMT especially for up to 15 years tenor and significantly lower than recent non-recourse project financings in Asia,

reflecting HSBC's strength in the MYR debt capital markets and MYR swap market

Distribution by investor type % of allocation

Summary of terms and conditions

Issuer TTM Sukuk Berhad (“TTM”)

Format Islamic Sukuk (Senior)

Structure Sukuk Commodity Murabaha

Issue Ratings AAA (MARC)

Amount MYR600m

Settlement Date 15th November 2010

Maturity November 2015 to 2025

Tenor 5 to 15 years

Coupon/Profit 4.00% to 5.05%

Governing Law Malaysia

HSBC Role Joint Lead Arranger and Manager and

Swap Counterparty

Execution highlights

“Best Islamic Finance Deal of the Year in Southeast Asia” “Cross Border Deal of the Year” “APAC Oil & Gas Deal of the Year”

Trans Thai-Malaysia (“TTM”) Sukuk Berhad MYR600 million Sukuk Issuance

In Nov 2010, TTM Sukuk Berhad

(“TTM”) successfully priced a

MYR600mn Sukuk issuance

This landmark transaction

achieved many firsts in the capital

market space:

First-ever cross border

project bonds in Asia and in

Islamic format

First-ever Sukuk offering by a

Thai entity and the first Islamic

financing transaction for a

company under the PTT Group

First Thai borrower in the

Malaysian Ringgit debt market

The first project finance bond

offering by a foreign borrower in

the Malaysian Ringgit capital

markets and the first project

finance bond transaction in

Malaysia since 2008

The hedge transaction represents

the longest tenor for a MYR/USD swap

transacted

HSBC acted as Joint Lead Arranger

and Manager on this prestigious MYR

landmark Sukuk transaction

HSBC also acted as Joint Swap

Counterparty in respect of the

hedging of the transaction for TTM

28

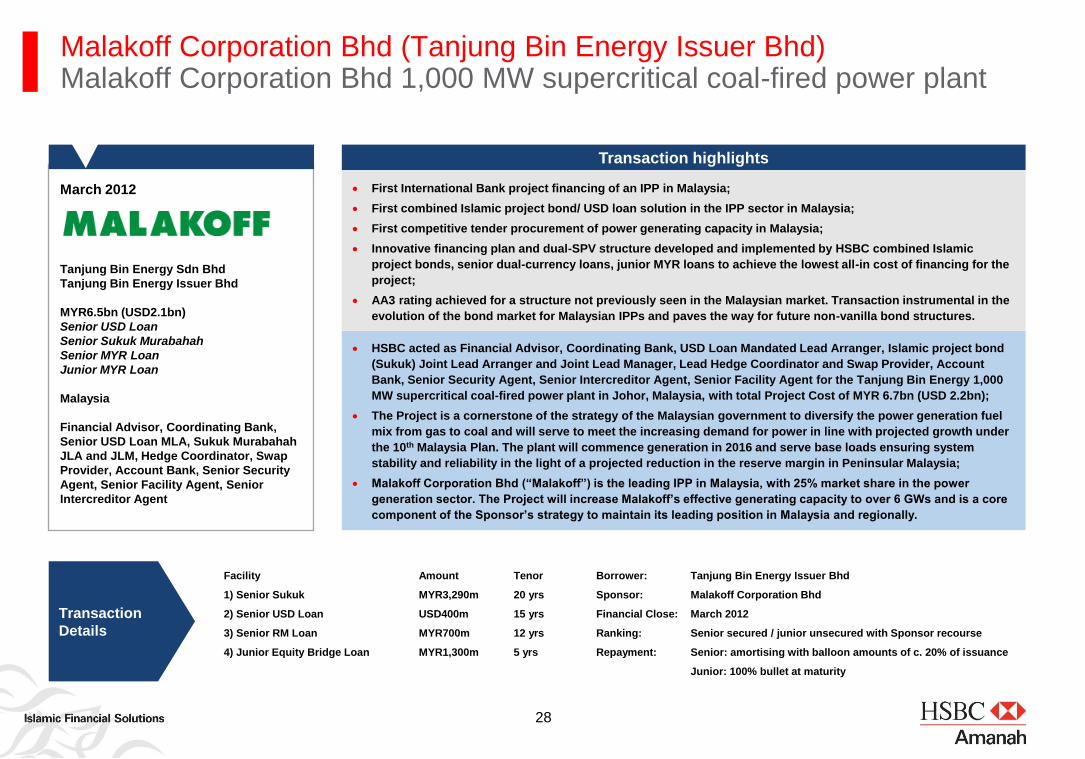

Tanjung Bin Energy Sdn Bhd

Tanjung Bin Energy Issuer Bhd

MYR6.5bn (USD2.1bn)

Senior USD Loan

Senior Sukuk Murabahah

Senior MYR Loan

Junior MYR Loan

Malaysia

Financial Advisor, Coordinating Bank,

Senior USD Loan MLA, Sukuk Murabahah

JLA and JLM, Hedge Coordinator, Swap

Provider, Account Bank, Senior Security

Agent, Senior Facility Agent, Senior

Intercreditor Agent

HSBC acted as Financial Advisor, Coordinating Bank, USD Loan Mandated Lead Arranger, Islamic project bond

(Sukuk) Joint Lead Arranger and Joint Lead Manager, Lead Hedge Coordinator and Swap Provider, Account

Bank, Senior Security Agent, Senior Intercreditor Agent, Senior Facility Agent for the Tanjung Bin Energy 1,000

MW supercritical coal-fired power plant in Johor, Malaysia, with total Project Cost of MYR 6.7bn (USD 2.2bn);

The Project is a cornerstone of the strategy of the Malaysian government to diversify the power generation fuel

mix from gas to coal and will serve to meet the increasing demand for power in line with projected growth under

the 10th Malaysia Plan. The plant will commence generation in 2016 and serve base loads ensuring system

stability and reliability in the light of a projected reduction in the reserve margin in Peninsular Malaysia;

Malakoff Corporation Bhd (“Malakoff”) is the leading IPP in Malaysia, with 25% market share in the power

generation sector. The Project will increase Malakoff’s effective generating capacity to over 6 GWs and is a core

component of the Sponsor’s strategy to maintain its leading position in Malaysia and regionally.

Transaction highlights

Transaction

Details

Early 2010

First International Bank project financing of an IPP in Malaysia;

First combined Islamic project bond/ USD loan solution in the IPP sector in Malaysia;

First competitive tender procurement of power generating capacity in Malaysia;

Innovative financing plan and dual-SPV structure developed and implemented by HSBC combined Islamic

project bonds, senior dual-currency loans, junior MYR loans to achieve the lowest all-in cost of financing for the

project;

AA3 rating achieved for a structure not previously seen in the Malaysian market. Transaction instrumental in the

evolution of the bond market for Malaysian IPPs and paves the way for future non-vanilla bond structures.

March 2012

Facility Amount Tenor

1) Senior Sukuk MYR3,290m 20 yrs

2) Senior USD Loan USD400m 15 yrs

3) Senior RM Loan MYR700m 12 yrs

4) Junior Equity Bridge Loan MYR1,300m 5 yrs

Borrower: Tanjung Bin Energy Issuer Bhd

Sponsor: Malakoff Corporation Bhd

Financial Close: March 2012

Ranking: Senior secured / junior unsecured with Sponsor recourse

Repayment: Senior: amortising with balloon amounts of c. 20% of issuance

Junior: 100% bullet at maturity

Malakoff Corporation Bhd (Tanjung Bin Energy Issuer Bhd) Malakoff Corporation Bhd 1,000 MW supercritical coal-fired power plant

29

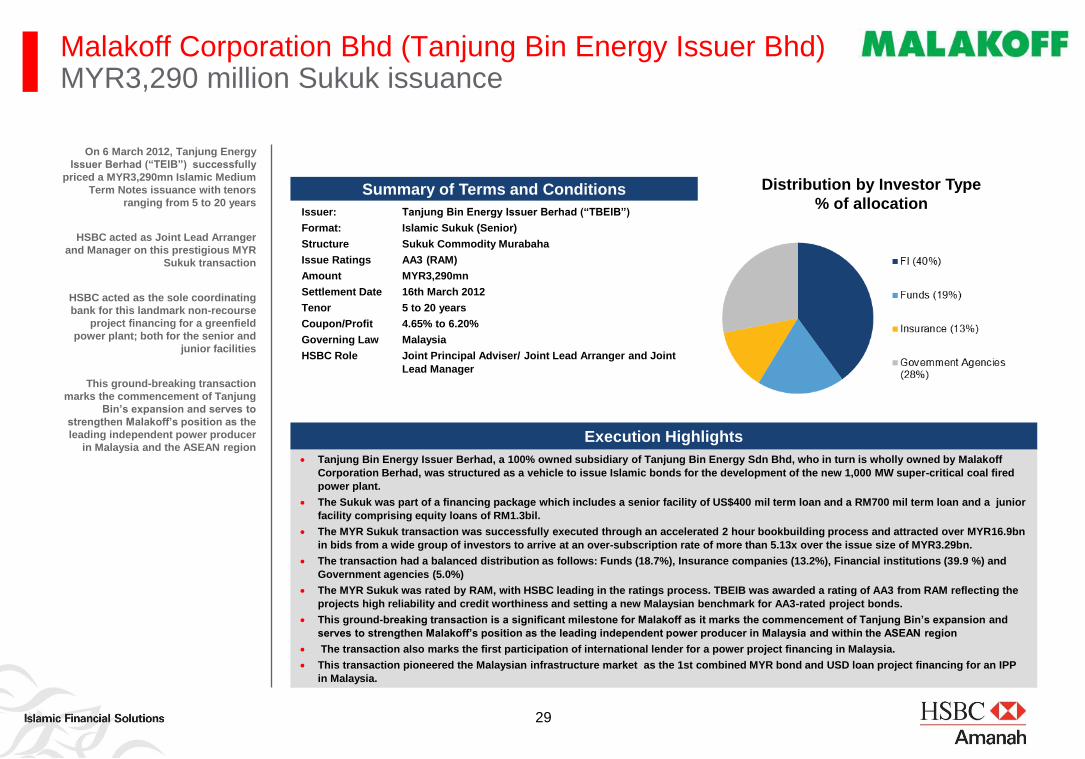

Tanjung Bin Energy Issuer Berhad, a 100% owned subsidiary of Tanjung Bin Energy Sdn Bhd, who in turn is wholly owned by Malakoff

Corporation Berhad, was structured as a vehicle to issue Islamic bonds for the development of the new 1,000 MW super-critical coal fired

power plant.

The Sukuk was part of a financing package which includes a senior facility of US$400 mil term loan and a RM700 mil term loan and a junior

facility comprising equity loans of RM1.3bil.

The MYR Sukuk transaction was successfully executed through an accelerated 2 hour bookbuilding process and attracted over MYR16.9bn

in bids from a wide group of investors to arrive at an over-subscription rate of more than 5.13x over the issue size of MYR3.29bn.

The transaction had a balanced distribution as follows: Funds (18.7%), Insurance companies (13.2%), Financial institutions (39.9 %) and

Government agencies (5.0%)

The MYR Sukuk was rated by RAM, with HSBC leading in the ratings process. TBEIB was awarded a rating of AA3 from RAM reflecting the

projects high reliability and credit worthiness and setting a new Malaysian benchmark for AA3-rated project bonds.

This ground-breaking transaction is a significant milestone for Malakoff as it marks the commencement of Tanjung Bin’s expansion and

serves to strengthen Malakoff’s position as the leading independent power producer in Malaysia and within the ASEAN region

The transaction also marks the first participation of international lender for a power project financing in Malaysia.

This transaction pioneered the Malaysian infrastructure market as the 1st combined MYR bond and USD loan project financing for an IPP

in Malaysia.

Distribution by Investor Type

% of allocation Summary of Terms and Conditions

Issuer: Tanjung Bin Energy Issuer Berhad (“TBEIB”)

Format: Islamic Sukuk (Senior)

Structure Sukuk Commodity Murabaha

Issue Ratings AA3 (RAM)

Amount MYR3,290mn

Settlement Date 16th March 2012

Tenor 5 to 20 years

Coupon/Profit 4.65% to 6.20%

Governing Law Malaysia

HSBC Role Joint Principal Adviser/ Joint Lead Arranger and Joint

Lead Manager

Execution Highlights

On 6 March 2012, Tanjung Energy

Issuer Berhad (“TEIB”) successfully

priced a MYR3,290mn Islamic Medium

Term Notes issuance with tenors

ranging from 5 to 20 years

HSBC acted as Joint Lead Arranger

and Manager on this prestigious MYR

Sukuk transaction

HSBC acted as the sole coordinating

bank for this landmark non-recourse

project financing for a greenfield

power plant; both for the senior and

junior facilities

This ground-breaking transaction

marks the commencement of Tanjung

Bin’s expansion and serves to

strengthen Malakoff’s position as the

leading independent power producer

in Malaysia and the ASEAN region

Malakoff Corporation Bhd (Tanjung Bin Energy Issuer Bhd) MYR3,290 million Sukuk issuance

30

Disclaimer

The Wholesale Banking division of HSBC Amanah Malaysia Berhad (“HSBC Amanah”) has prepared this document (the “Document”) for information

purposes only. This Document does not constitute a commitment to underwrite or purchase or subscribe for all or any portion of the securities

mentioned herein. Any such commitment shall be evidenced only by a fully executed subscription agreement, purchase agreement or similar

contractual document. This Document should also not be construed as an offer for sale of or subscription for any investment, nor is it calculated to

invite/solicit any offer to purchase or subscribe for any investment.

HSBC Amanah has based this Document on information obtained from sources it believes to be reliable but which it has not independently verified.

HSBC Amanah makes no guarantee, representation or warranty and accepts no responsibility or liability for the contents of this Document and/or as

to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or

any part of the contents of this Document. HSBC Amanah and its affiliates and/or its or their respective officers, directors and employees may have

positions in any securities mentioned in this Document (or in any related investment) and may from time to time add to or dispose of any such

securities (or investment). HSBC Amanah and/or any of its affiliates may act as market maker or have assumed an underwriting commitment in the

securities of any companies discussed in this Document (or in related investments), may sell them to or buy them from clients on a principal or

discretionary basis and may also perform or seek to perform banking or underwriting services for or relating to those companies. As HSBC Amanah

is part of a large global financial services organisation, it or one or more of its affiliates may have certain other relationships with the parties relevant

to the proposed activities as set out in this Document, and these proposed activities may give rise to a conflict of interest, which the addressee

hereby acknowledges.

No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This Document,

which is not for public circulation, must not be copied, transferred or the content disclosed to any third party and is not intended for use by any

person other than the addressee or the addressee's professional advisers for the purposes of advising the addressee hereon.