Embed Size (px)

Citation preview

August 17, 2015

HSIL Ltd.

Solid Market Leader… leveraging customers with more solutions!

CMP INR 285 Target INR 351 (Re)Initiating Coverage - BUY

SKP Securities Ltd www.skpmoneywise.com Page 1 of 18

Key Share Data

Face Value (INR) 2.0

Equity Capital (INR Mn) 144.6

Market Cap 20611.7

52 Week High/Low (INR) 474.4/255.2

6 Month Avg. Daily Volume (NSE) 1,32,087

BSE Code 500187

NSE Code HSIL

Reuters Code HSNT.NS

Bloomberg Code HSI:IN

Shareholding Pattern (as on June 30, 2015)

47%

10%

25%

18%Promoters

FII

DII

Public & Others

Particulars FY14 FY15 FY16E FY17E

Net Sales 18,582.1 19,806.2 22,084.3 24,646.3

Growth (%) 5.5% 6.6% 11.5% 11.6%

EBITDA 2,533.1 3,325.2 3,710.2 4,288.5

PAT 339.8 854.4 1,135.4 1,472.3

Growth (%) -58.6% 151.4% 32.9% 29.7%

EPS (INR) 5.1 12.9 15.7 20.4

BVPS (INR) 155.7 183.0 195.5 212.7

Key Financials (INR Million)

Particulars FY14 FY15 FY16E FY17E

P/E (x) 55.4 22.1 18.2 14.0

P/BVPS (x) 1.8 1.6 1.5 1.3

Mcap/Sales (x) 1.0 1.0 0.9 0.8

EV/EBITDA (x) 10.9 7.9 7.1 6.2

ROCE (%) 7.2% 10.9% 12.0% 13.7%

ROE (%) 3.3% 6.5% 8.0% 9.6%

EBITDA Mar (%) 13.6% 16.8% 16.8% 17.4%

PAT Mar (%) 1.8% 4.3% 5.1% 6.0%

Debt - Equity (x) 0.9 0.4 0.4 0.4

Key Financials Ratios

Source: Company, SKP Research

1 Yr price performanceHSIL vis-à-vis BSE Mid Cap

-20%

0%

20%

40%

60%

80%

Aug-14 Oct-14 Jan-15 Mar-15 May-15 Aug-15

HSIL BSE Mid Cap

Company Background

Hindustan Sanitaryware and Industries Limited (HSIL), of R.K.Somany Group, is India’s largest player in sanitaryware (~40% organised market share) and second largest player in glass containers (~17%). It also manufacturers faucets to leverage its customers and channels; PET bottles as a substitute product extension for glass containers and has presence in home retail furnishing.

Investment Rationale

Capacity addition to sustain market share and growth; entering synergic products to leverage customers and sales network

Higher economic growth in India will result in increased buying power in

the hands of a growing affluent and mass affluent segment with aspirations to improve lifestyle. To meet the resultant demand in premium sanitaryware, HSIL is increasing its sanitaryware capacity by 0.4 mn pieces, up 10.5% from its current 3.8 mn pieces capacity at a Capex of ~Rs 570 mn. The expanded capacity is expected to commission by March 2016 with a potential to generate additional revenue of ~Rs 915 mn at full capacity utilization.

HSIL is also venturing into further product extensions; in CPVC & UPVC pipes in building products segment and security caps & closures for protection of products from counterfeiting in packaging product segment, at an investment of Rs 2.17 bn, funded through debt and equity in the ratio of 2:1. Both projects are expected to commission in next 18 months with a potential to generate additional revenue of ~Rs 5.5-6.0 bn over next 4-5 years.

Turnaround in container glass business

In the last few years, HSIL’s packaging business (primarily glass containers) did not fare well and has been a drag on profitability due to oversupply conditions and muted demand from user industry. It voluntarily shut its 280 TPD capacity at Hyderabad, reducing its total capacity by 18%. Margins have improved now with better capacity utilization and change of fuel mix from furnace oil to pet coke.

Margins expected to improve with better operating leverage

HSIL is set to increase its sanitaryware and faucets current capacity utilization to ~97% and ~57% by FY17E from ~88% and ~35% respectively in FY15, offering visibility of margin improvement due to better operating leverage and product mix.

During FY15, HSIL reported net sales of Rs 19.8 bn, registering a marginal growth of 7% y-o-y due to slowdown in real estate segment, discontinuation of the low margins tiles business and oversupply conditions in the container glass industry.

On the backdrop of strong brand equity and distribution network, increasing disposable income and changing consumer preferences towards premium lifestyle products, HSIL’s net sales is expected to grow at a CAGR of 11.6% during FY15-FY17 to Rs 24.6 bn and EBITDA margins to improve to ~17.4% from 16.8% reported in FY15.

Valuation

GoI’s new initiatives on housing and sanitation will give a fillip to demand of sanitaryware, although not necessarily in HSIL’s premium product segment. Given HSIL’s strong brand equity & distribution network, changing consumer preferences towards premium & lifestyle products along with diverse product basket and a turnaround in its glass containers business augurs well for HSIL. We have valued the stock on SOTP basis and recommend a Buy on HSIL with a target price of Rs 351.3/- in 12 months.

Analysts: Nikhil Saboo

Tel No: +91-33-40077019; Mobile: +91-9330186643

e-mail: [email protected]

Vineet Agrawal

Tel No: +91-22-49226006; Mobile: +91-9819510575

e-mail: [email protected]

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 18

Industry Overview – Sanitaryware & Bathroom Fittings

Size and Growth Trends: Indian sanitaryware contributes ~8% of total global production and is the second largest market in the Asia Pacific Region. India’s sanitaryware and bathroom fittings industry is estimated at ~Rs. 80 bn in FY14 of which sanitaryware itself accounts for more than Rs. 28 bn, growing at a CAGR of 12.5%. This growth trend is likely to continue through 2016. The remaining Rs. 52 bn is attributed to bathroom fittings, which is expected to record a CAGR of 15% until 2016. Organised players comprise ~60% of India’s sanitaryware industry and ~45% of bathroom fittings.

Major players and their market share: Market Leader HSIL, Parryware ROCA and Cera

collectively control ~ 80-85% of the organised sanitaryware industry, resulting in low competition in premium sanitaryware industry.

Usage and Utility: Demand for sanitaryware is highest in residential sector followed by

commercial sector which includes malls, offices, hotels, hospitals etc. Only ~40% of the

total population of India enjoys sanitation facilities. About 70% population in rural areas

and 19% in urban areas are deprived from sanitation facilities. 92% demand originates

from new customers and 8% comes from the replacement market. As such, there is

enough growth potential for sanitaryware industry in India.

Opportunities & Demand Drivers

Low Sanitation Penetration: Sanitation penetration is lowest in India vis-a-vis other

emerging economies. According to Census 2011, the national sanitation coverage is

~40%, whereas rural sanitation coverage has remained a mere 30.7%. Rising need for

sanitation and special initiatives taken by the government to enhance sanitation

penetration indicates ample scope and growth available in the industry, going forward.

Exhibit: Asian Sanitation Levels

Source: Company, SKP Research

36

59

65

82

92

93

100

India

Indonesia

China

Korea

Sri Lanka

Thailand

Singapore

Changing demographics to drive demand: With 50% of India population below the age

of 30, the country’s ‘youth bulge’ is unequivocal about change, and demands better quality

products. Shift in consumer preferences along with greater brand awareness, superior

standards of living and higher disposable income, has opened opportunities for new

products, leading to a shift from unorganised to organised sector.

Government’s Initiatives to improve sanitation: GoI is taking special initiatives to

improve sanitation penetration in India. It has launched a multi-million dollar sanitation

project, ‘Nirmal Bharat Abhiyaan’ to raise awareness and improve sanitation levels in

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 18

India. Although, this may not have a direct impact on premium quality producers like HSIL,

there will certianly be a rub off effect. GoI also plans to develop 100 smart cities in India,

which would further boost the demand for sanitaryware products, including premium ones.

Heavily dependent on real estate market: Sanitaryware industry is quite dependent on

real estate sector as majority demand comes from new construction. Various initiatives of

Central and State Governments will revitalise the real estate and housing sector in the

country. With increasing urbanisation and infrastructure growth, urban population is

expected to reach to about 600 mn by 2031 which would lead to enhanced demand for

modern housing and building products thereby increasing demand for sanitaryware.

The middle income segment has become one of the principal drivers for real estate boom.

This segment has grown from 11 mn households in 2001-02 to 31 mn households in 2010-

11and is further expected to grow to 114 mn households by 2025-26.

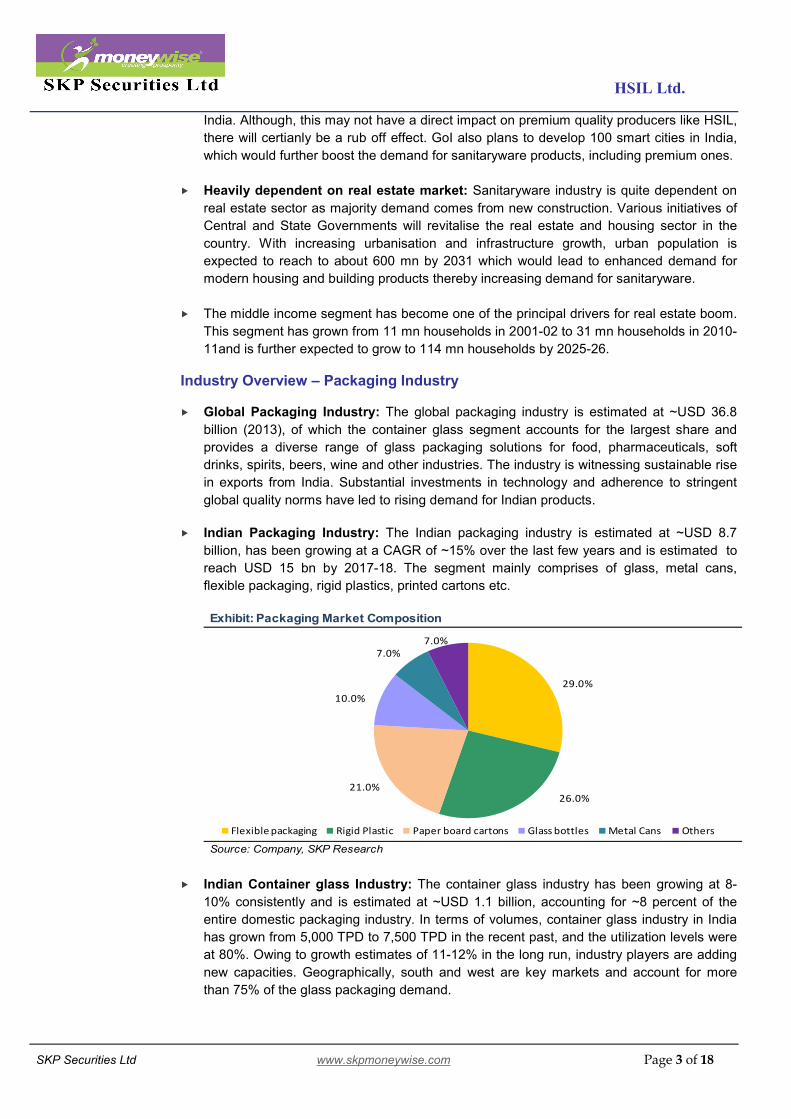

Industry Overview – Packaging Industry

Global Packaging Industry: The global packaging industry is estimated at ~USD 36.8

billion (2013), of which the container glass segment accounts for the largest share and

provides a diverse range of glass packaging solutions for food, pharmaceuticals, soft

drinks, spirits, beers, wine and other industries. The industry is witnessing sustainable rise

in exports from India. Substantial investments in technology and adherence to stringent

global quality norms have led to rising demand for Indian products.

Indian Packaging Industry: The Indian packaging industry is estimated at ~USD 8.7

billion, has been growing at a CAGR of ~15% over the last few years and is estimated to

reach USD 15 bn by 2017-18. The segment mainly comprises of glass, metal cans,

flexible packaging, rigid plastics, printed cartons etc.

Source: Company, SKP Research

Exhibit: Packaging Market Composition

29.0%

26.0%21.0%

10.0%

7.0%7.0%

Flexible packaging Rigid Plastic Paper board cartons Glass bottles Metal Cans Others

Indian Container glass Industry: The container glass industry has been growing at 8-

10% consistently and is estimated at ~USD 1.1 billion, accounting for ~8 percent of the

entire domestic packaging industry. In terms of volumes, container glass industry in India

has grown from 5,000 TPD to 7,500 TPD in the recent past, and the utilization levels were

at 80%. Owing to growth estimates of 11-12% in the long run, industry players are adding

new capacities. Geographically, south and west are key markets and account for more

than 75% of the glass packaging demand.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 18

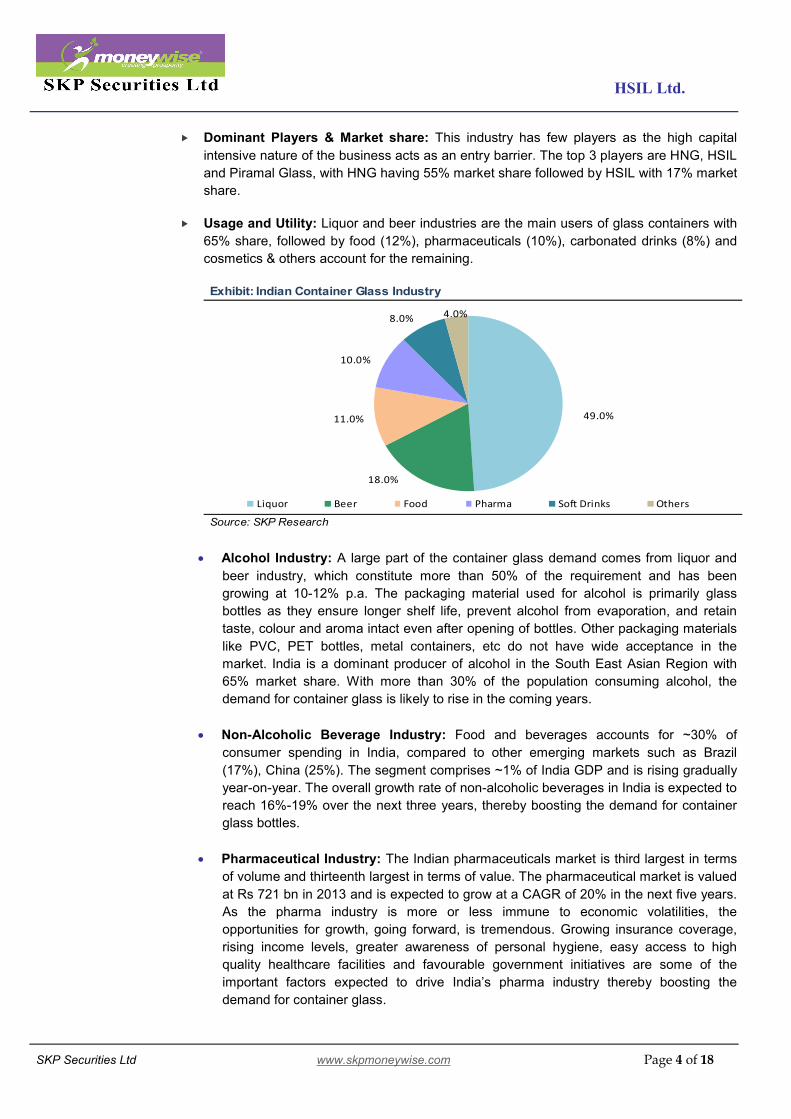

Dominant Players & Market share: This industry has few players as the high capital

intensive nature of the business acts as an entry barrier. The top 3 players are HNG, HSIL

and Piramal Glass, with HNG having 55% market share followed by HSIL with 17% market

share.

Usage and Utility: Liquor and beer industries are the main users of glass containers with

65% share, followed by food (12%), pharmaceuticals (10%), carbonated drinks (8%) and

cosmetics & others account for the remaining.

Source: SKP Research

Exhibit: Indian Container Glass Industry

49.0%

18.0%

11.0%

10.0%

8.0% 4.0%

Liquor Beer Food Pharma Soft Drinks Others

Alcohol Industry: A large part of the container glass demand comes from liquor and

beer industry, which constitute more than 50% of the requirement and has been

growing at 10-12% p.a. The packaging material used for alcohol is primarily glass

bottles as they ensure longer shelf life, prevent alcohol from evaporation, and retain

taste, colour and aroma intact even after opening of bottles. Other packaging materials

like PVC, PET bottles, metal containers, etc do not have wide acceptance in the

market. India is a dominant producer of alcohol in the South East Asian Region with

65% market share. With more than 30% of the population consuming alcohol, the

demand for container glass is likely to rise in the coming years.

Non-Alcoholic Beverage Industry: Food and beverages accounts for ~30% of

consumer spending in India, compared to other emerging markets such as Brazil

(17%), China (25%). The segment comprises ~1% of India GDP and is rising gradually

year-on-year. The overall growth rate of non-alcoholic beverages in India is expected to

reach 16%-19% over the next three years, thereby boosting the demand for container

glass bottles.

Pharmaceutical Industry: The Indian pharmaceuticals market is third largest in terms

of volume and thirteenth largest in terms of value. The pharmaceutical market is valued

at Rs 721 bn in 2013 and is expected to grow at a CAGR of 20% in the next five years.

As the pharma industry is more or less immune to economic volatilities, the

opportunities for growth, going forward, is tremendous. Growing insurance coverage,

rising income levels, greater awareness of personal hygiene, easy access to high

quality healthcare facilities and favourable government initiatives are some of the

important factors expected to drive India’s pharma industry thereby boosting the

demand for container glass.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 18

Food Packaging Industry: India’s packaged food industry is valued at more than USD

24 bn and is expected to grow at a CAGR of 12% during next 4-5 years. Within the

food packaging industry, container glass segment is growing at 15% annually. The per

capita consumption of packaged food in India is as low as 4.3 kg as against Germany’s

42 kg and Taiwan’s 20 kg, which in turn provides ample scope of growth.

Exhibit: Demand Forecast: Glass bottle packaging market

Source: Company, SKP Research

2990 3190 4330

30540 33260

50300

85009110

12900

0

10000

20000

30000

40000

50000

60000

70000

80000

2011-12 2012-13 2017-18

Fig

s. in

Rs

mill

ion

Food Beverages Non-Foods

Food CAGR: 8.3% Beverages CAGR: 8.6% Non-food CAGR: 7.2% Total CAGR: 7.2%

Opportunities & Demand Drivers

Favourable Demographics to boost demand: Favourable demographics like

proportionate rise in youth population, shift in consumer preferences from unbranded to

branded ones and rise in organised retail would boost the demand and drive growth for

consumer industry of container glass.

Per capita consumption of user industry is low: The demand for the glass packaging

industry is largely dependent on the user industries mainly alcoholic and other beverages,

pharmaceuticals and food. India is one of the lowest consumer of beer and liquor at less

than 2 litres. Liquor industry is expected to grow at 8% CAGR, while pharma industry is

slated to grow at 20% for the next 5 years and food industry is expected to double in the

next 5 years. The expected growth in the user industry coupled with low per capita

consumption indicates ample scope for container glass industry going forward.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 18

Exhibit: Per Capita Beer Consumption (Litres)

Source: Company, SKP Research

2

37

45

67

68

70

78

110

India

China

Japan

Russia

Brazil

UK

USA

Germany

Increasing emphasis on health based packaging: Food and drug regulators have put

special emphasis on hazards due to inappropriate packaging and have put greater

importance on the usage of safe recycled products like glass thereby driving the

consumption of glass as a packing substance.

PET Bottles Industry

Polyethylene Terephthalate (PET) is thermoplastic polyester which is widely used for the

production of beverage bottles. It is also used as a flexible packaging film due to its high

clarity, low permeability and excellent printability. Globally, PET demand is expected to

grow at a CAGR of 5-6% over the next five years and 15-18% domestically. The superior

characteristics of PET are expected to drive the growth of PET bottles for the industry.

India, Brazil, Russia and China are expected to dominate the overall PET market, with

India and China expected to emerge as market leaders. Asia-Pacific region is the

prominent consumer of PET accounting for ~40% of the global PET demand. Also global

demand for PET resin was 15.3 mn tonnes in 2012 which is expected to grow at 19.5%

CAGR during 2012-17.

Carbonated Soft Drinks (CSD) market is the largest consumer for PET bottles (blow

moulds) today. India is a major manufacturer and importer of soft drink beverages. The

Indian soft drink industry is vast and has been rapidly growing y-o-y. The volume of soft

drinks consumed in India stood at a whopping 11,755 mn litres in 2013. The industry has

grown at a CAGR of 11.2% during 2008-2013. It is further expected that soft drinks

industry may grow at a CAGR of 19%till 2018.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 18

Company Profile

HSIL was incorporated in 1960 as Hindustan Twyfords Ltd, in collaboration with Twyfords

Ltd, UK, to introduce vitreous china ceramic sanitaryware in India. The name was changed

to Hindustan Sanitaryware & Industries Ltd, in 1967 and to HSIL Ltd, in 2009.

It diversified into manufacturing of container glass in 1981, through acquisition of

Associated Glass Industries Ltd. It acquired faucet and accessories unit of Havells in May

2010 and launched products under the brand name Benelave. In 2012, it acquired Garden

Polymers Private Ltd., marking its entry into PET bottle segment.

Source: Company, SKP Research

Exhibit: Key Milestones

1960: Incorporated as Hindustan Twyfords Ltd. to introduce vitreous China for the first time in India

1962: Commercial production at Bahadurgarh started (sanitaryware)

1967: Changes name to Hindustan Sanitaryware & Industries Limited

1981: Forays into container glass manufacturing through acquisition of Associated Glass Industries Ltd.

1989: Expanded ceramics capacity through acquisition of Krishna Ceramics Ltd. (Bibinagar)

1991: Launches Hindware Brand

1999: Acquired Raasi Ceramics, further expands its sanitaryware business

2000: Building Products Division expanded to Bathroom Wellness category (Bathtubs, Showers etc.)

2003: Strategic partnership with Sanitec for introducing high-end Keramag Brand in the Indian market

2004: Building Products Division expanded to chrome plated bathroom fittings (faucets)

2008: Entered into home interior fashion design retail industry through its subsidiary HHRPL.

Changes name to HSIL Ltd.Commissioned new container glass capacity of 475 MTPA at Bhongir, A.P.Launches Hindware Lacasa display showrooms

2009:

Acquired bath fittings business of Havells India & UK based Barwood Products Ltd.Forays into tiles business

2010:

Launches premium bath fittings brand BENELAVELaunches luxury brand QUEO

2011:

Completes expansion of sanitaryware (0.7mn psc) at Bibinagar and faucets plant at Bhiwadi Completes expansion of container glass capacity at Bhongir (475 MTPA)

2012:

Garden Polymer Private Ltd. merged with HSIL Ltd.Container glass division renamed as "Packaging Product Division"

2014:

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 18

The company has eight manufacturing facilities in India - three in Andhra Pradesh (two

container glass units and one sanitaryware unit), two at Rajasthan (faucet units) and one

each in Haryana (sanitaryware unit), Uttarakhand (plastic containers) and Karnataka

(plastic containers).

Exhibit: Plant Overview

Plant Location Capacity Plant Location Capacity

Bahadurgar, Haryana 1.8 Bhiwadi, Rajasthan 0.5

Bibinagar, Telangana 2 Kaharani, Rajasthan 2.5

Total Capacity 3.8 Total Capacity 3.0

Container Glass

Plant Location Capacity Plant Location Capacity

Sanathnagar, Hyderabad 650 Selaqui, Uttarakhand 7050

Bhongir, Telangana 950 Dharwad, Karnataka 2450

Total Capacity 1600 Total Capacity 9500.0

Source: Company, SKP Research

Building Products (Figs in mn pieces)

Sanitaryware Faucets

Packaging Products (Figs in TPD)

PET Bottles

Raw Materials: HSIL has a strategic raw material substitution policy, to avoid dependence

on a few suppliers without affecting the overall quality levels.

Sanitaryware

Faucets

Container Glass

PET Bottles

Exhibit: Raw materials used in production process

Source: Company, SKP Research

Particulars

Build

ing

Segm

ent

Pack

agin

g

Segm

ent

Raw Materials Used

Kaolinite, clay, feldspar, quartz sand etc.

Brass etc.

Sil ica, l imestone, dolomite, soda ash, cullet etc.

Polyethylene terepeththalate (PET)

Power & fuel is one of the major costs for HSIL. Over the years the company has

successfully been able to curtail its power & fuel cost (from 22.9% of sales in FY13 to

14.1% in FY15) by replacing it with cheaper substitutes (replacing high cost furnace oil to

fluidised pet coke). Going forward, we expect the power & fuel cost to remain stable and

any further cost saving initiatives would have positive impact on margins.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 18

HSIL is engaged in manufacturing of building products and packaging products. The

product range in building products includes bathroom fittings, bath tubs, shower partitions,

shower enclosures, shower panels, kitchen appliances, sinks, ceramic tiles etc. while

product range in packaging products includes container glass and PET bottles.

* Manufactured

# Outsourced

Source: Company, SKP Research

Exhibit: Building Products Details

Building Products

Sanitaryware & Faucets *

Sanitaryware & Faucets #

Allied Products (Outsourced)

Hindware Italian Collection PVC Cisterns

Hindware Art Fitting & Seat Covers

Bathtubs, Showers, Enclosures, Whirlpools

Bath Accessories

Kitchen Sinks

Kitchen Chimneys & Hobs

Tiles

Vents

Queo:Luxury Sanitaryware Brand

AMore:Luxury Well ness & SPA Brands

Hindware

Raasi

Benelave

Market share: At present, HSIL is the largest manufacturer of sanitaryware products, with

~40% market share of the organised industry. It is also the market leader in the container

glass segment in the south (~66% market share) and the second largest player in India

with ~17% market share.

Robust distribution network: Over the years, HSIL established a strong and widespread

distribution network, encompassing ~3,000 dealers, ~18,000 retailers, 19 service locations

comprising 300 plumbers covering 600+ districts across India. Apart from this, company

also has ~458 hindware shop-in-shops, ~100 hindware Gallerias and direct dealer outlets.

This has helped the company to reach wide spectrum of retail customers and maintain its

dominating position in the sanitaryware industry. It plans to further expand dealer network,

gallerias, and shop-in-shops and increase its presence to Tier II & Tier III towns.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 18

Strong brand recall: The Company’s greatest asset is the recall value of its brands

among customers. HSIL has separate category brands for different price points: Rassi &

Benelave for mass affluent, Hindware, Hindware Art & Hindware Italian for premium

segments, Amora and Queo for luxury segments. Major brands include Hindware Italian

collection, Hindware Art and Hindware, account for more than 50% of building products

revenues.

Category Brands Offerings

Exhibit: HSIL brands at a glance

This segment offers complete range of world class faucets

and accessories. The business was acquired from Havells

India in May, 2010.

Hindware Art and Hindware Italian collection offers high

value added bathroom fittings ( cisterns, water closets,

urinals, and wash basins) whereas Hindware also offers

kitchen appliances (chimneys and built-in-ovens).

Mass

Rassi

&

Benelave

Premium

Hindware,

Hindware ART

&

Hindware Italian

collection

Note: Vents, Evok excluded as they are not sanitaryware products

Source: Company, SKP Research

LuxuryQueo, UK

& Amore

Queo brand offers high-end luxury sanitaryware from

Barwood, UK. As of December 2014, it has over 80 dealers.

Amore brand offers range of wellness products and

targets high end bathware segment. As of December 2014,

it has over 90 dealers.

EVOK Brand: HSIL operates its home retail furnishing business via its wholly-owned

subsidiary Hindware Home Pvt Ltd (HHRPL). HSIL launched its mega store under the

brand name “Evok” and currently has 19 retail outlets all over India. It is a chain of

specialty home showcasing a range of over 20,000 home interior products and provides

‘value for style’ home interior solutions for B2C business whereas ‘design to build’ interior

solutions to B2B businesses. In FY14, EVOK introduced a franchisee model opportunity in

North and South India to focus on Modular kitchens, a novel and upcoming concept in mini

metros with good business potential. This segment accounted for ~Rs 1.3 bn of FY15

consolidated revenues.

Outsourcing of products: HSIL also undertakes marketing and distribution of outsourced

products to capitalize on its existing brand and distribution network. HSIL latest offering of

its kitchen appliance house aids in effortless and efficient cooking experience. The product

basket is constantly upgraded and modified to match current trends and improved lifestyle

demand.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 18

Strong client base: Over five decades’ presence in the industry has enabled HSIL to

develop long standing customer relationships. It serves ~1,500 institutional clients in

building product segment and ~550 institutional clients in packaging product division. In

the building segment, company’s prominent client’s names include L&T, Shaporji Pallonji,

DLF, Prestige Group, Puravankara, Lokhandwala Developers etc. while in the packaging

segment it caters to growing brands like United Spirits, United Breweries, SAB Miller,

Pfizer, GSK, Ranbaxy, HUL, ITC Ltd, Coca Cola, Pepsi etc.

Liquor &

Beer

Food

Soft Drinks

Pharma

Source: Company, SKP Research

Exhibit: Clientele Base

Pac

kagi

ng

Div

isio

nB

uild

ing

Pro

du

cts

Investment Rationale

Capacity additions to sustain market share and growth India’s GDP is expected to grow ~8% in the coming years, resulting in increased buying

power in the hands of a growing and aspiring mass affluent segment. HSIL is increasing

its sanitaryware capacity by 0.4 million pieces (brownfield), of which, 0.1 million pieces is

added at Bahadurgarh and another 0.3 million pieces at Bibinagar respectively to take

advantage of the robust demand in premium category of sanitaryware. Premium category

sanitaryware products contributed ~56-57% to building product segment in FY15.

Capex for the expansion is ~Rs 570 mn which is expected to commission by March 2016

and has a potential to generate additional revenue of ~Rs 915 mn at full capacity.

Segmant Current Capacity Capacity Expansion Post Expansion

Sanitaryware 3.8 0.4 4.2

Faucets 3.0 - 3.0

Figs in million piecesExhibit: Capacity expansion at a glance

Source: Company, SKP research

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 18

HSIL has also planned to venture into new businesses of manufacturing CPVC & UPVC

pipes as an extension in building products segment (its these pipes which run into the

faucets installed on sanitaryware products) and producing security caps & closures for

protection of products from counterfeiting in packaging product segment, at an investment

of Rs 2.17 bn, funded through debt and equity in the ratio of 2:1. Both the projects are

expected to commission in next 18 months with a potential to generate additional revenue

of ~Rs 5.5-6.0 bn over next 4-5 years.

HSIL plans to setup 30,000 TPA capacity for manufacturing CPVC & UPVC (60% CPVC &

40% UPVC) pipes in Gujarat at a capex of Rs 1.05 bn and has entered into an agreement

with M/s Sekisui Chemical Co. Ltd, Japan for supply of CPVC resin. Security caps &

closures is required for protection of products from counterfeiting and mainly used in

pharma and liquor industry. This product will be a value addition to the existing portfolio

of the packaging products division and the company has filed for necessary product

patents for the same.

The overall capacity utilization of the company during FY15 for sanitaryware and faucets

were ~88% and 35%, which we expect to reach ~98% and 57% by FY17E.

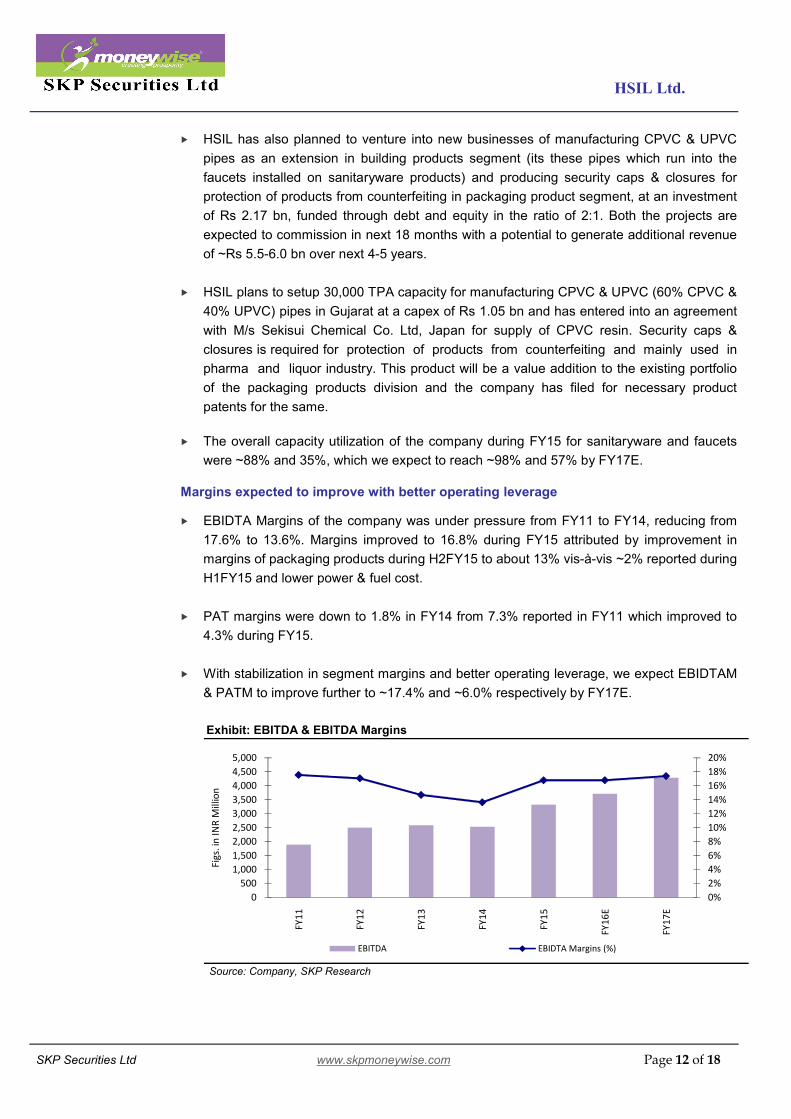

Margins expected to improve with better operating leverage EBIDTA Margins of the company was under pressure from FY11 to FY14, reducing from

17.6% to 13.6%. Margins improved to 16.8% during FY15 attributed by improvement in

margins of packaging products during H2FY15 to about 13% vis-à-vis ~2% reported during

H1FY15 and lower power & fuel cost.

PAT margins were down to 1.8% in FY14 from 7.3% reported in FY11 which improved to

4.3% during FY15.

With stabilization in segment margins and better operating leverage, we expect EBIDTAM

& PATM to improve further to ~17.4% and ~6.0% respectively by FY17E.

Exhibit: EBITDA & EBITDA Margins

Source: Company, SKP Research

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6E

FY1

7E

Figs

. in

INR

Mill

ion

EBITDA EBIDTA Margins (%)

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 18

Exhibit: ROE & ROCE

Source: Company, SKP Research

11.66%

9.69%7.99%

3.30%

6.46%

8.03%9.58%

12.4%

10.5%

8.4% 7.2%

10.9% 12.0%13.7%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6E

FY1

7E

ROE D/E (x)

Top-line expected to grow at a CAGR of 11.6% over FY15-17E

In FY15, HSIL reported net sales of Rs 19.8 bn, registering a marginal growth of 7% y-o-y

due to slowdown in building products segment which could be attributed to slowdown in

real estate segment and discontinuation of low margins tiles business. The packaging

business reported 6% muted growth, on the back of oversupply conditions in the industry.

Building products and packaging product segments contributed 47% each, whereas EVOK

brand, under the subsidiary - Hindware Home Retail Pvt Ltd, contributed ~6% to the

consolidated revenues of the Company.

HSIL is the only manufacturer of specialized coloured bottles in India, over and above

regular bottles, catering to the demands of niche players in the segment.

Since, unorganized sector in sanitaryware and faucets accounts for ~62% and 55%

respectively therefore, on the backdrop of strong brand equity and distribution network,

changing consumer preferences towards good quality and branded lifestyle products,

increasing disposable income creates a significant potential for HSIL to increase its market

share going forward.

In view of the facts mentioned above, we expect HSIL to grow at a CAGR of 11.6% during

FY15-FY17 with 13.4% and 9.1% CAGR growth in building products and packaging

products division, respectively.

Source: Company, SKP Research

Exhibit: Segmental Revenue

4,8

35

6,2

13

7,4

66

8,8

15

9,3

67

10,6

20

12,0

52

5,5

07

7,1

64

8,2

55

8,6

43

9,2

12

10,0

54

10,9

73

404

1,239

1,8761,109

1,2131,395

1,604

0

3000

6000

9000

12000

15000

18000

21000

24000

27000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Fig

s. in

Rs M

illio

n

Building Products Packaging Products Home Décor - EVOK Brand

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 18

Key Concerns

Competition from unorganised players:

Indian sanitaryware industry has significant presence of small unorganized players,

although mostly in non-premium products. Though, Indian consumers are gravitating

towards the organized segment, offering branded/premium products, any increase in

intensity of competition from unorganized segment may be detrimental for the

company. Indian container glass industry has a sizeable unorganized segment representing large

opportunities in terms of volume, which acts as a potential threat for the major

organised players. More so as packaging regulations are not very stringent in India.

There is always a real threat of consuming industries gravitating towards unorganised

segment to bring down their costs, which can reduce pricing power of organised

players, at least in some product segments.

Threat from substitutes packaging: Over the last few years, container glass industry

has been facing competition from segments like PET bottles, metal cans, Tetra Packs etc.

owing to factors like weight, fragility, cost etc. However, the threat is limited for HSIL due to

several advantages of glass over plastic. Glass is 100% recyclable with an excellent shelf

life. Besides, the growing awareness on account of hygienic packaging demand will drive

the demand for container glass over plastic alternatives. In any case, HSIL is already

present in PET bottles.

Extended slowdown in real estate sector may dampen business sentiments: HSIL’s

building product segment is highly dependent on real estate sector, any extension of

slowdown to Tier – I and Tier – II cities may dampen the business prospects of HSIL.

Valuations

Governments Initiative of “Housing for All” and “Swachh Bharat Abhiyan” is likely to give a

fillip to demand for low end sanitaryware products, thereby allowing organised players to

have a larger pie of the premium products segment. As HSIL accelerates up the chain

through premiumisation (premium and luxury segment accounting for ~57% of

sanitaryware business in FY14) coupled with strong brand equity & distribution network,

changing consumer preferences along with a gradual turnaround in demand of container

glass augurs well for HSIL.

We have valued the stock on SOTP basis and recommend a Buy on the stock with a

target price of Rs 351/- in 12 months (23.2% upside).

Segment EBITDA EV/EBITDA

Bui lding Products Segment 2567.8 9 x 23,110.2

Packaging Products Segment 1689.8 5 x 8,449.0

Target Enterprise Value 31,559.2

Less : FY17E Debt 6,454.1

Add: FY17E Cash 296.0

Target Market Cap 25,401.2

No of Shares 72.3

Target Price Per Share (Rs) 351

CMP (Rs) 285

Return (%) 23.2%

Source: SKP Research

Exhibit: SOTP Figs. in Rs Million

Multiple (x)

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 15 of 18

Q1FY16 Result Update

Particulars Q1 FY16 Q1 FY16 % Change Q4 FY15 % Change FY15 FY14 % Change

Net Sales 4,128.5 4,121.5 0.2% 5,589.1 -26.1% 19,806.2 18,582.0 6.6%

Total Expenditure 3,488.7 3,457.3 0.9% 4530.3 -23.0% 16,481.0 16,048.9 2.7%

Raw Material Consumed 969.0 754.6 28.4% 1409.0 -31.2% 3,341.2 2,941.2 13.6%

% to Sales 23.5% 18.3% -- 25.2% -- 16.9% 15.8% --

Purchase of traded goods 499.7 764.1 -34.6% 863.0 -42.1% 3,973.9 3,534.0 12.4%

% to Sales 12.1% 18.5% -- 15.4% -- 20.1% 19.0% --

Employee Expenses 515.1 429.4 20.0% 541.7 -4.9% 2,159.5 1,884.4 14.6%

% to Sales 12.5% 10.4% -- 9.7% -- 10.9% 10.1% --

Fuel Cost 577.6 684.6 -15.6% 631.5 -8.5% 2,801.2 3,770.2 -25.7%

% to Sales 14.0% 16.6% -- 11.3% -- 14.1% 20.3% --

Marketing & Advertisement 0.0 0.0 -- 0.0 -- 0.0 0.0 --

% to Sales 0.0% 0.0% -- 0.0% -- 0.0% 0.0% --

Other Expenses 927.3 824.6 12.5% 1085.1 -14.5% 4,205.2 3,919.1 7.3%

% to Sales 22.5% 20.0% -- 19.4% -- 21.2% 21.1% --

EBIDTA 639.8 664.2 -3.7% 1058.8 -39.6% 3,325.2 2,533.1 31.3%

EBIDTA Margin 15.5% 16.1% -- 18.9% -- 16.8% 13.6% --

Depreciation 282.2 275.5 2.4% 309.1 -8.7% 1,250.3 1,101.2 13.5%

EBIT 357.6 388.7 -8.0% 749.7 -52.3% 2,074.9 1,431.9 44.9%

EBIT Margin 8.7% 9.4% -- 13.4% -- 10.5% 7.7% --

Other Income 12.7 6.0 111.7% 5.2 144.2% 35.7 38.1 -6.3%

Interest 104.2 171.0 -39.1% 179.2 -41.9% 775.2 717.8 8.0%

Exceptional Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Forex Difference 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Tax 92.6 73.8 25.5% 177.2 -47.7% 481.0 412.4 16.6%

Extraordinary Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Prior period taxes written bk. 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Minority Interest 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Share of Associate Company 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Reported Profit After Tax 173.5 149.9 15.7% 398.5 -56.5% 854.4 339.8 151.4%

PAT Margin 4.2% 3.6% -- 7.1% -41.1% 4.3% 1.8% --

Diluted EPS (Rs) 2.4 2.3 5.7% 2.0 23.1% 12.9 5.1 150.6%

Figs in Rs. million

Source: Company, SKP Research

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 16 of 18

Exhibit: Balance Sheet

Particulars FY14 FY15 FY16E FY17E Particulars FY14 FY15 FY16E FY17E

Total Income 18,582.1 19,806.2 22,084.3 24,646.3 Share Capital 132.1 144.6 144.6 144.6

Growth (%) 5.5% 6.6% 11.5% 11.6% Reserve & Surplus 10,150.9 13,086.3 13,989.9 15,230.5

Expenditure 16,049.0 16,481.0 18,374.2 20,357.8 Shareholders Funds 10,283.0 13,230.9 14,134.5 15,375.1

Material Cost 2,941.2 3,341.2 5,079.4 5,520.8 Total Debt 9,490.5 5,761.6 5,839.2 6,454.1

Pur of Traded Goods 3,534.0 3,973.9 3,136.0 3,499.8 Deferred Tax (Net) 1,154.0 1,045.0 1,045.0 1,045.0

Employee Cost 1,884.4 2,159.5 2,374.1 2,649.5 Other Long Term Liab 154.4 179.9 200.6 223.9

Power & Fuel & Othr Exp. 7,689.3 7,006.4 7,784.7 8,687.8 Total Liabilities 21,081.9 20,217.4 21,219.3 23,098.0

EBITDA Margins (%) 13.6% 16.8% 16.8% 17.4%

EBITDA 2,533.1 3,325.2 3,710.2 4,288.5 Net Block inc. Capital WIP 16,388.2 16,181.9 16,309.9 16,654.1

Depreciation 1,101.2 1,250.3 1,315.4 1,302.4 Investments 108.6 108.6 108.6 108.6

EBIT 1,431.9 2,074.9 2,394.8 2,986.1 Non-Current Asset 19.6 14.7 16.4 18.3

Other Income 38.1 35.7 50.8 56.7 Inventories 4,443.3 4,743.6 5,410.7 5,742.6

Interest Expense 717.8 775.2 671.5 742.2 Sundry Debtors 4,191.7 4,137.8 4,969.0 5,299.0

Profit Before Tax (PBT) 752.3 1,335.4 1,774.1 2,300.5 Cash & Bank Balance 602.9 251.2 221.5 296.0

Income Tax 412.5 481.0 638.7 828.2 Other Current Assets 19.4 20.5 22.9 73.9

Effective Tax Rate (%) 54.8% 36.0% 36.0% 36.0% Loans & Advances 967.9 816.3 905.5 1,478.8

Profit After Tax (PAT) 339.8 854.4 1,135.4 1,472.3 Current Liabilities & Prov 5,659.7 6,092.0 6,779.8 6,608.1

Growth (%) -58.6% 151.4% 32.9% 29.7% Net Current Assets 4,565.5 3,877.4 4,749.7 6,282.2

Diluted EPS 5.1 12.9 15.7 20.4 Total Assets 21,081.9 20,217.4 21,219.3 23,098.0

Exhibit: Cash Flow

StatementExhibit: Ratio Analysis

Particulars FY14 FY15E FY16E FY17E Particulars FY14 FY15 FY16E FY17E

Profit Before Tax (PBT) 752.3 1,335.4 1,774.1 2,300.5 Earning Ratios (%)

Depreciation 1,101.2 1,250.3 1,315.4 1,302.4 EBITDA Margin (%) 13.6% 16.8% 16.8% 17.4%

Interest Provided 718.0 775.2 671.5 742.2 PAT Margins (%) 1.8% 4.3% 5.1% 6.0%

Chg. in Working Capital (787.0) 243.3 (883.0) (1,436.6) ROCE (%) 7.2% 10.9% 12.0% 13.7%

Direct Taxes Paid (157.0) (481.0) (638.7) (828.2) ROE (%) 3.3% 6.5% 8.0% 9.6%

Other Charges (3.0) - - - Per Share Data (INR)

Operating Cash Flows 1,624.5 3,123.2 2,239.3 2,080.3 Diluted EPS 5.1 12.9 15.7 20.4

Capital Expenditure (1,924.6) (1,044.0) (1,443.3) (1,646.7) Cash EPS (CEPS) 21.8 29.1 33.9 38.4

Investments (1,072.8) (0.0) - - BVPS 155.7 183.0 195.5 212.7

Others 1,111.6 - - - Valuation Ratios (x)

Investing Cash Flows (1,885.8) (1,044.0) (1,443.3) (1,646.7) P/E 55.4 22.1 18.2 14.0

Changes in Equity - 2,500.0 - - Price/BVPS 1.8 1.6 1.5 1.3

Inc / (Dec) in Debt 996.5 (3,728.9) 77.6 614.9 EV/Sales 1.5 1.3 1.2 1.1

Dividend Paid (inc tax) (231.0) (231.8) (231.8) (231.8) EV/EBITDA 10.9 7.9 7.1 6.2

Interest Paid (720.9) (775.2) (671.5) (742.2) EB/EBIT 19.4 12.6 11.0 9.0

Financing Cash Flows 44.6 (2,377.1) (825.7) (359.1) Balance Sheet Ratios

Chg. in Cash & Cash Eqv (216.8) (297.8) (29.7) 74.5 Debt - Equity 0.9 0.4 0.4 0.4

Opening Cash Balance 765.7 549.0 251.2 221.5 Current Ratio 1.8 1.6 1.7 2.0

Closing Cash Balance 549.0 251.2 221.5 296.0 Fixed Asset Turn. Ratios 1.2 1.2 1.4 1.7

Figures in INR Million

Source: Company Data, SKP Research

Exhibit: Income Statement Figures in INR Million Figures in INR Million

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 17 of 18

Notes:

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg,

Thomson First Call & Investext Myiris, Moneycontrol, Tickerplant and ISI Securities.

DISCLAIMER:

This document has been prepared by SKP Securities Ltd, hereinafter referred to as SKP to provide information about the company(ies)/sector(s), if any, covered in the report and may be distributed by it and/or its affiliates. SKP Securities Ltd., offers broking and depository participant services and is regulated by Securities and Exchange Board of India (SEBI). It also distributes investment products/services like mutual funds, alternative investment funds, bonds, IPOs, etc., renders corporate advisory services and invests its own funds in securities and investment products. We declare that no material disciplinary action has been taken against SKP by any regulatory authority impacting Equity Research Analysis. As a value addition to its clients, it offers its research services and reports in various formats to its clients and prospects. As such, SKP is making these disclosures under SEBI (Research Analysts) Regulations, 2014, under which it is in the process of seeking registration.

Terms & Conditions and Other Disclosures:

This research report (“Report”) is for the personal information of the selected recipient(s), does not construe to be any investment, legal or taxation advice, is not for public distribution and should not be copied, reproduced or redistributed to any other person or in any form without SKP’s prior permission. The information provided in the Report is from publicly available data, which we believe, are reliable. While reasonable endeavors have been made to present reliable data in the Report so far as it relates to current and historical information, but SKP does not guarantee the accuracy or completeness of the data in the Report. Accordingly, SKP or its promoters, directors, subsidiaries, associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained and views and opinions expressed in this publication. Past performance mentioned in the Report should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment of its original date of publication by SKP and are subject to change without notice. The price, value of and income from any of the securities mentioned in this report can rise or fall. The Report includes analysis and views of individual research analysts (which, hereinafter, includes persons reporting to them) covering this Report. The Report is purely for information purposes. Opinions expressed in the Report are SKP’s or its research analysts’ current opinions as of the date of the Report and may be subject to change from time to time without notice. SKP or any person connected with it does not accept any liability arising from the use of this document. Investors should not solely rely on the information contained in this Report and must make investment decisions based on their own investment objectives, judgment, risk profile and financial position. The recipients of this Report may take professional advice before acting on this information. SKP, along with its affiliates, are engaged in various financial services and so might have financial, businesses or other interest in other entities, including the subject company or its affiliates mentioned in this report, for which it might have received any compensation in the past twelve months. SKP does not provide any merchant banking or market making service and does not manage public offers. However, SKP encourages independence in preparation of research reports and strives to minimize conflict in preparation of research reports.SKP and its analysts did not receive any compensation or other benefits from the subject company mentioned in the Report or from a third party in connection with preparation of the Report. Accordingly, SKP and its Research Analyst do not have any material conflict of interest at the time of publication of this Report. SKP’s research analysts may provide input into its other business activities. Investors should assume that SKP and/or its affiliates are seeking or will seek business assignments from the company(ies) that are the subject of this material and that the research analysts who are involved in preparing this material may educate investors on investments in such businesses. The research analysts responsible for the preparation of this document may interact with trading desk/sales personnel and other parties for the purpose of gathering, applying and interpreting information. Our research analysts are paid on the profitability of SKP, which may include earnings from business activities for which this Report is being used, but not for the preparation of this report. SKP generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any company(ies) that the analyst covers. Additionally, SKP generally, prohibits its analysts and persons reporting to analysts from serving as an officer, director or advisory board member of any companies that the analyst cover. The following Disclosure of Interest Statement, clarifies it further: SKP or its Research Analyst(s) engaged in preparation of this Report or his/her relative (i) do not have any financial interests in the subject company mentioned in this report (ii) do not own 1% or

more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report (iii) do not have any other material conflict of interest at the time of publication of the research report. The distribution of this document in other jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

HSIL Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 18 of 18

Analyst Certification

The views expressed in this research report accurately reflect the personal views of the analyst about the subject securities or issues, which are subject to change without prior notice and does not represent to be an authority on the subject. No part of the compensation of the research analyst was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst in this report. The research analysts, strategists, or research associates principally responsible for preparation of SKP research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Disclosure of Interest Statement

Analyst ownership of the stock NIL

Served as an officer, director or employee NIL

SKP Securities Ltd

Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 4922 6006 033 4007 7000 022 4922 6000 033 4007 7400

Fax 022 4922 6066 033 4007 7007 022 4922 6066 033 4007 7007

E-mail [email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB

*Group Entities INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532

Institutional & Retail Broking Wealth Advisory & Distribution Investment Banking