Embed Size (px)

Citation preview

HUAHIN CONDOMINIUM MARKET REPORT 1H 2016

RESIDENTIAL RESEARCH

2

FIGURE 1

Accumulated Supply 2007-1H 2016

HIGHLIGHTS

RISINEE SARIKAPUTRADirector, Research and Consultancy

“ The average new unit

sold each year in Hua-hin

was approximately 2,600

units with the remaining of

5,200 units now, it will

probably take a few

more years to clear the

stock. ”

Market Overview

In mid-2016, the Hua-hin condominium

market is recovering from the stagnancy

earlier in the year. The market shows a

slightly increasing absorption rate and the

highlight of the first half of this year was to

release the remaining stock from the last

year. Demand for Hua-hin condominiums

is quite stable now, not massive as a

few years ago. New supply is likely to be

limited all through this year. There were

only two new projects launched in the

first half of 2016; both are located in the

Cha-am area. Also, two projects have

been halted due to financial problems

and political uncertainties, as their main

clients are foreigners. From a market

survey, we found that some projects with

units previously rented out as hotel rooms

on a daily rate have either decreased the

number of such units or have destined

the units for sale. This is in response to

negative media attention and the crack

down of authorities on such developers.

Regarding the potential growth of the

area, Hua-hin is ever changing, compared

to other areas. We have seen lots of

•Onlythreenewprojectswerelaunched in the first half of 2016; Two projects are located in Cha-am and one projects is located on the mountain side.

• Thenumberofprojectsde-creased, obviously implying that the developers decided to wait and see the absorption of remaining stock.

• Duetopromotionsfromthedevelopers and limited new supply, the overall take-up rate rose from 74 percent at the end of 2015 to 78 percent in 2Q 2016.

• Buyingtorenttrendisdecreasingcontinuously. Most buyers this year purchased based on real demand for second weekend homes.

•Weforecastthatthenewsupplyin the second half will be lower than the first half and mainly from listed developers. Until 2017 we might see various developers jumping into the market and we expect to see higher numbers of new projects, compared to this year. The anticipated new supply should be around 3,000 units for the upcoming year.

economic activities, with many hip

restaurants and ventures opening all the

time. Hua-hin will be more vibrant once

BluportResortMall,aprojectvaluedat

THB4billion,officiallyopensthisOctober.

Supply

The total accumulated supply located

between Cha-am and Khao Tao from 2007

to the first half of 2016 is 23,400 units and

sold rate is 78%, rising from 74% at the

end of 2015; approximately 5,200 unsold

units remain. The majority of remaining

stock is located in the Cha-am area, which

mostly includes mega projects by listed

developers. New supply added in the first

half of this year is from three projects:

Lumpini Seaview, which is high-rise

building containing 1,130 units; The

collections, a low-rise building containing

308 units; and Sansara retirement

condominiumprojectinBlackMountain.

The latter targets foreigners aged over 50

years old from Sweden and other Northern

European countries, the United Kingdom

and Australia.

20070

5,000

10,000

15,000

25,000

20,000

2008 2009 2010 2011 2012 2013 2014 2015 1H 2016

Existing SupplyNew Supply

942 1,06

7

303

1,02

9

6,07

9

5,44

3

3,08

7

3,08

7 1,46

8

895

Source : Knight Frank Thailand’s Research

3

2007

0 0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

39 %55 %

79 % 79 %

45 %

57 %61 %

72 %74 %

78 %

5,000

10,000

15,000

20,000

25,000

2008 2009 2010 2011 2012 2013 2014 2015 1H 2016

Supply Demand Sold rate

FIGURE 2

Supply by location

FIGURE 3

Supply by view

FIGURE 4

Huahin Condominium demand, supply, take-up rate between 2007-1H 2016

RESIDENTIAL RESEARCHHUAHIN MARKET REPORT 1H 2016

From the above graph, we see that after

2012 the average new supply added to

the market is roughly 3,000 units per

year, except in 2014 when Thailand

experienced political turmoil and a coup

d’état. In terms of known future supply,

about 300 units from two projects will

come on board: Lumpini place at Huahin

Soi7andLumpiniParkBeach2on

Cha-amBeach.Bothareexpectedtobe

added to the market by the end of 2016.

The majority of supply is located in

the Cha-am area, encompassing up

to 16,058 units, accounting for nearly

70 percent of the total supply. This is

followed by Khao Takiab at 12 percent.

Condominiums in Hua-hin and Khao Tao

included 1,753 units and 1,593 units,

respectively. Hence, both represent

the same proportion of the market, at 7

percent. The lowest-supply area is inland

located in the even-numbered sois,

representing only 5 percent of the total

supply.

The number of non-seaview units is

approximately 2 percent higher than

seaviewunits.But,attheendof2015,

the percentage of non-seaview units

was far greater than the percentage of

seaview units, roughly 10 percent higher.

This change mainly results from one

project in Cha-am, which launched 1,130

units in a high-rise building, allowing

most of the units to have partial seaviews

from their balconies.

Demand

As of 2Q2016, the take-up rate of Hua-hin

condominiums is 78 percent, rising

from 74 percent at the end 2015. This is

nearly equal to the highest sold rate in

the historical data that was 79 percent

in the years 2009 and 2010. The positive

Source : Knight Frank Thailand’s Research

Source : Knight Frank Thailand’s Research

Cha am 69 %

Inland 5 %

Khao Tao 7 %

Huahin 7 %

Khao Takiab 12 %

Non-seaview 51 %

Seaview 49 %

Source : Knight Frank Thailand’s Research

4

Cha am Huahin Khao Tao InlandKhaoTakiab

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

74 %

94 %

91 %

67 %

89 %

Sum of Total Demand Sold rate

performance of demand in the first half

of this year implies that the demand is

catching up to the supply in the market.

In addition, the average take-up over

the last three years is approximately

2,600 units per year. And, the remaining

stock now is about 5,200 units so it

will probably take a few more years to

clear the stock. As such, it is rational to

forecast more new supply launching in

2017 than in 2016. It seems 2016 is the

year of clearing inventory for developers;

the benefits belong to the purchaser via a

variety of promotions: special prices, free

common fees for one year, etc.

In terms of buyers, the majority are still

ThaipeoplelivinginBangkokwhoare

looking for a second home in Hua-hin.

From the survey, we found that, for some

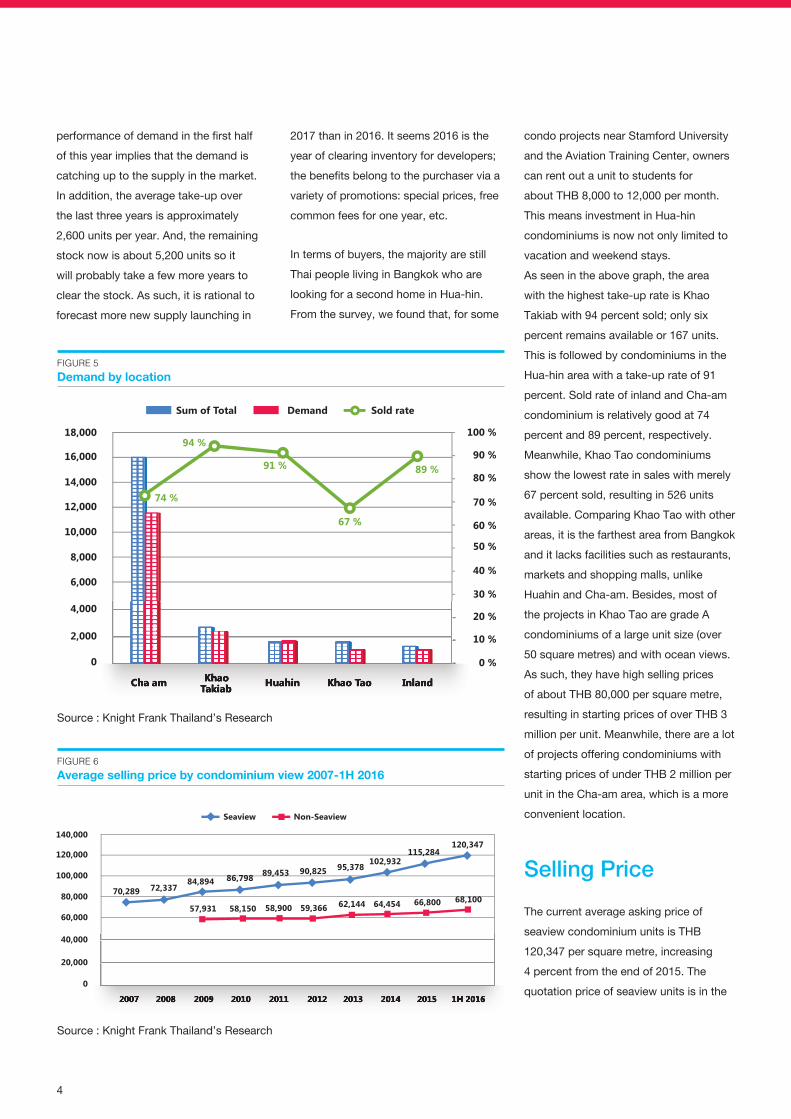

FIGURE 5

Demand by location

FIGURE 6

Average selling price by condominium view 2007-1H 2016

Source : Knight Frank Thailand’s Research

condo projects near Stamford University

and the Aviation Training Center, owners

can rent out a unit to students for

aboutTHB8,000to12,000permonth.

This means investment in Hua-hin

condominiums is now not only limited to

vacation and weekend stays.

As seen in the above graph, the area

with the highest take-up rate is Khao

Takiab with 94 percent sold; only six

percent remains available or 167 units.

This is followed by condominiums in the

Hua-hin area with a take-up rate of 91

percent. Sold rate of inland and Cha-am

condominium is relatively good at 74

percent and 89 percent, respectively.

Meanwhile, Khao Tao condominiums

show the lowest rate in sales with merely

67 percent sold, resulting in 526 units

available. Comparing Khao Tao with other

areas,itisthefarthestareafromBangkok

and it lacks facilities such as restaurants,

markets and shopping malls, unlike

HuahinandCha-am.Besides,mostof

the projects in Khao Tao are grade A

condominiums of a large unit size (over

50 square metres) and with ocean views.

As such, they have high selling prices

ofaboutTHB80,000persquaremetre,

resultinginstartingpricesofoverTHB3

million per unit. Meanwhile, there are a lot

of projects offering condominiums with

startingpricesofunderTHB2millionper

unit in the Cha-am area, which is a more

convenient location.

Selling Price

The current average asking price of

seaviewcondominiumunitsisTHB

120,347 per square metre, increasing

4 percent from the end of 2015. The

quotation price of seaview units is in the 2007 2008 2009 2010 2011 2012 2013 2014 2015 1H 2016

0

20,000

40,000

60,00057,931

70,289 72,33784,894 86,798 89,453 90,825 95,378

102,932115,284

120,347

58,150 58,900 59,366 62,144 64,454 66,800 68,10080,000

100,000

120,000

140,000

Seaview Non-Seaview

Source : Knight Frank Thailand’s Research

5

For the latest news, views and analysison the world of prime property, visit

KnightFrankblog.com/global-briefing

GLOBAL BRIEFING

Thailand Contacts

Phanom KanjanathiemthaoManaging Director+66 (0)2643 8223 Ext [email protected]

Chaturawit WattanaprukExecutive Director+66 (0)2643 8223 Ext [email protected]

Surasak Limpa-ArayakulExecutive Director, Head of Valuation and Advisory+66 (0)2643 8223 Ext [email protected]

Roong SitthisankunchornExecutive Director, Head of Property Management+66 (0)2643 8223 Ext [email protected]

Marcus BurtenshawExecutive Director, Head of Commercial Agency+66 (0)2643 8223 Ext [email protected]

Frank KhanExecutive Director, Head of Residential +66 (0)2643 8223 Ext [email protected]

Risinee SarikaputraDirector, Research and Consultancy+66 (0)2643 8223 Ext [email protected] Phuket ContactNattha KahapanaExecutive Director, Knight Frank Phuket+66 (0)7631 8151 Ext [email protected]

Important Notice© Knight Frank LLP 2016 – This report ispublished for general information only andnot to be relied upon in any way. Althoughhigh standards have been used in the preparation of the information, analysis, viewsand projections presented in this report, noresponsibility or liability whatsoever can beaccepted by Knight Frank LLP for any loss ordamage resultant from any use of, reliance onor reference to the contents of this document.As a general report, this material does notnecessarily represent the view of Knight FrankLLP in relation to particular properties or projects. Reproduction of this report in wholeor in part is not allowed without prior writtenapproval of Knight Frank LLP to the form and content within which it appears. KnightFrank LLP is a limited liability partnership registered in England with registered numberOC305934.Ourregisteredofficeis55BakerStreet, London, W1U 8AN, where you maylook at a list of members’ names.

RECENT MARKET-LEADING RESEARCH PUBLICATIONS

Knight Frank Research, Reports are available at KnightFrank.co.th/Research

Pattaya CondominiumMarket Overview 1H 2016

RESIDENTIAL RESEARCH

BangkokcondominiUm market Q2 2015

RESIDENTIAL RESEARCH

rangebetweenTHB80,000to130,000

per square metre; the lower price point

is likely to be partial seaview units not

directly facing the ocean. And, the

average selling prices in Hua-hin tend

to be higher than the other areas. Non-

seaview condominium units are now

quotedbetweenTHB55,000to80,000

per square metre. Even though some

units are non-seaview but if they face

the swimming pool inside the project,

they can command a higher selling price,

especially pool access units. The average

sellingpricefornon-seaviewunitisTHB

68,100 per square metre, a 2 percent

increase from the end of 2015.

APPENDIX

Location Definition :

Cha Am

the area incorporating Petchkasem Road

Km 210 to Km 225, as well as the sois in

between

Hua Hin

the area incorporating Soi Hua Hin 1

(next to Hua Hin Airport) to Soi Petchkasem

Road Km 235, as well as the sois in

between

Khao Takiab

the area from the road connected from

Petchkasem Road KM 235 to the south

for a distance of 14 km

Khao Tao

the area incorporating the Khao Tao area,

including Soi Hua Hin 126 to Soi Hua Hin

156, as well as the sois in between

Inland

the area incorporating the northern side of

Petchkasem Highway

*Knight Frank Thailand research data is

not inclusive of Areas in Pranburi

Condominium Type :

There are two condominium types

according to Knight Frank, which are :

Sea View Condominium

is defined as a condominium project that

is located on the beachfront with at least

50% of total units having sea views.

Non-Sea View Condominium

is defined as a condominium project

where less than 50% of total units have

non-sea views.

H1 2016 Logistics Property Market

RESIDENTIAL RESEARCH

BangkokcondominiUm market Q2 2015

RESIDENTIAL RESEARCH

BANGKOKSUPERPRIME AND PRIME CONDOMINIUM MARKET OVERVIEW H1 2016

Q2 2016 BangkokOficceMarket

RESIDENTIAL RESEARCH

BangkokcondominiUm market Q2 2015

RESIDENTIAL RESEARCH

BANGKOKSUPERPRIME AND PRIME CONDOMINIUM MARKET OVERVIEW H1 2016

COMMERCIAL RESEARCH

BANGKOKOFFICEMARKET OVERVIEW Q2 2016

COMMERCIAL RESEARCH

LOGISTICS PROPERTY MARKET H1 2016

Phuket CondominiumReport 2016

RESIDENTIAL RESEARCH

BangkokcondominiUm market Q2 2015

RESIDENTIAL RESEARCH

BANGKOKSUPERPRIME AND PRIME CONDOMINIUM MARKET OVERVIEW H1 2016

COMMERCIAL RESEARCH

LOGISTICS PROPERTY MARKET H1 2016PHUKET CONDOMINIUMREPORT 2016

RESIDENTIAL RESEARCH

PATTAYA CONDOMINIUMMARKET OVERVIEW 1H 2016

RESIDENTIAL RESEARCH