Embed Size (px)

Citation preview

Hyflux named Preferred Bidder

for Tuas II Desalination Plant,

Singapore

7 March 2011

2

Key Points

Singapore’s largest seawater desalination plant

Hyflux’s largest project by value

Second largest ultrafiltration membrane installation

after Magtaa Seawater Desalination Plant

3

Project Highlights

Capacity Seawater reverse osmosis (SWRO) desalination plant:

318,500 m3/day (70 million gallons/day)

Project Value S$890 million (EPC value S$750 million)

Contract Type Design, Build, Own, Operate (DBOO)

Off-taker PUB

Concession Period 25 years

Project Commercial

Operation2013

4

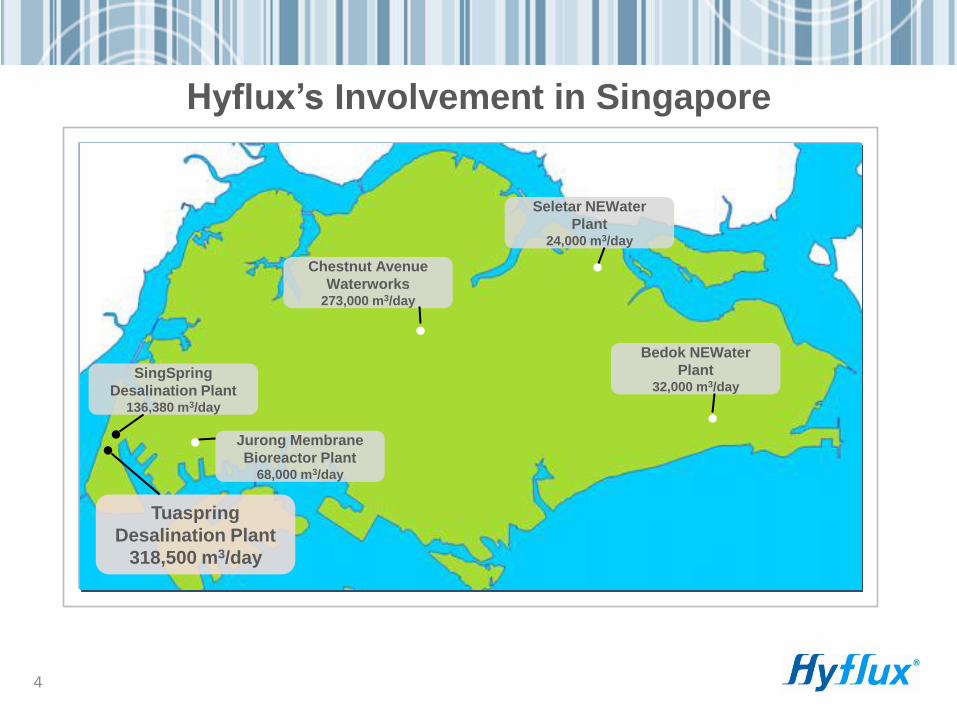

Hyflux’s Involvement in Singapore

SingSpring

Desalination Plant136,380 m3/day

Chestnut Avenue

Waterworks273,000 m3/day

Seletar NEWater

Plant24,000 m3/day

Bedok NEWater

Plant32,000 m3/day

Jurong Membrane

Bioreactor Plant68,000 m3/day

Tuaspring

Desalination Plant

318,500 m3/day

5

Overview of Desalination Plant

Reverse Osmosis

Building

CCGT Power

PlantUltrafiltration

Building

Tuaspring

SingSpring

6

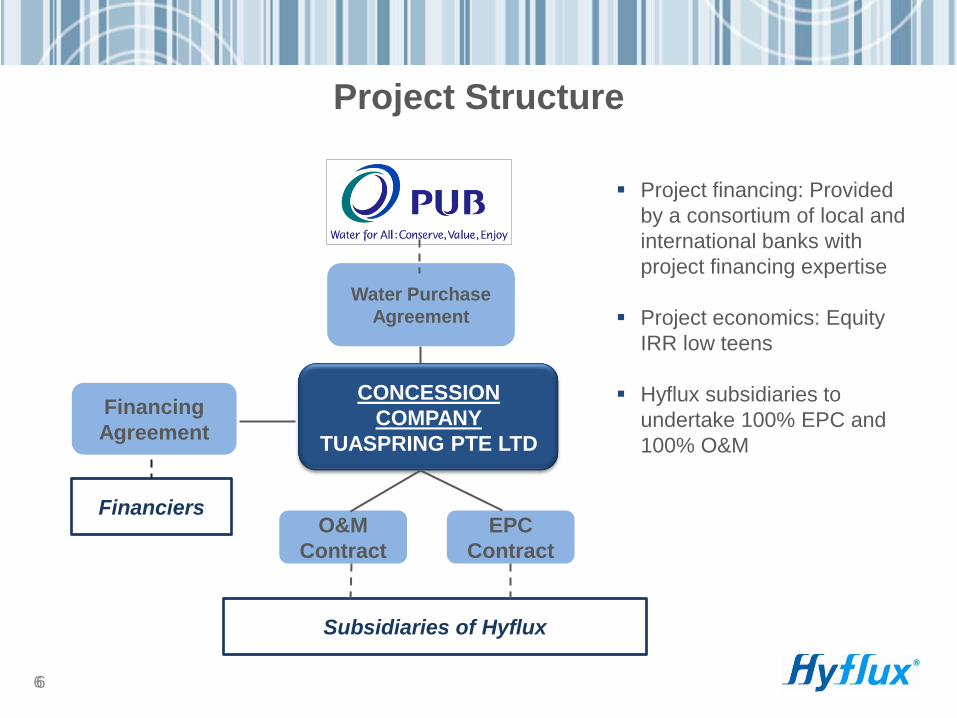

Project Structure

6

CONCESSION

COMPANY

TUASPRING PTE LTD

Water Purchase

Agreement

O&M

Contract

EPC

Contract

Financing

Agreement

Financiers

Subsidiaries of Hyflux

Project financing: Provided

by a consortium of local and

international banks with

project financing expertise

Project economics: Equity

IRR low teens

Hyflux subsidiaries to

undertake 100% EPC and

100% O&M

7

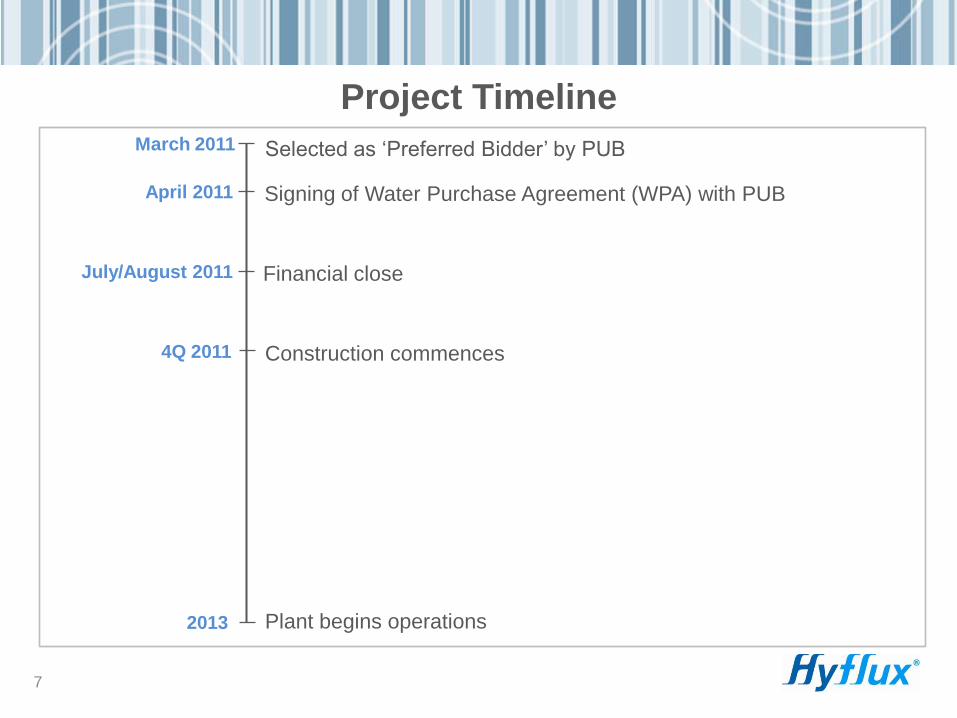

Project TimelineMarch 2011 Selected as ‘Preferred Bidder’ by PUB

Signing of Water Purchase Agreement (WPA) with PUBApril 2011

Financial closeJuly/August 2011

Construction commences4Q 2011

Plant begins operations2013

8

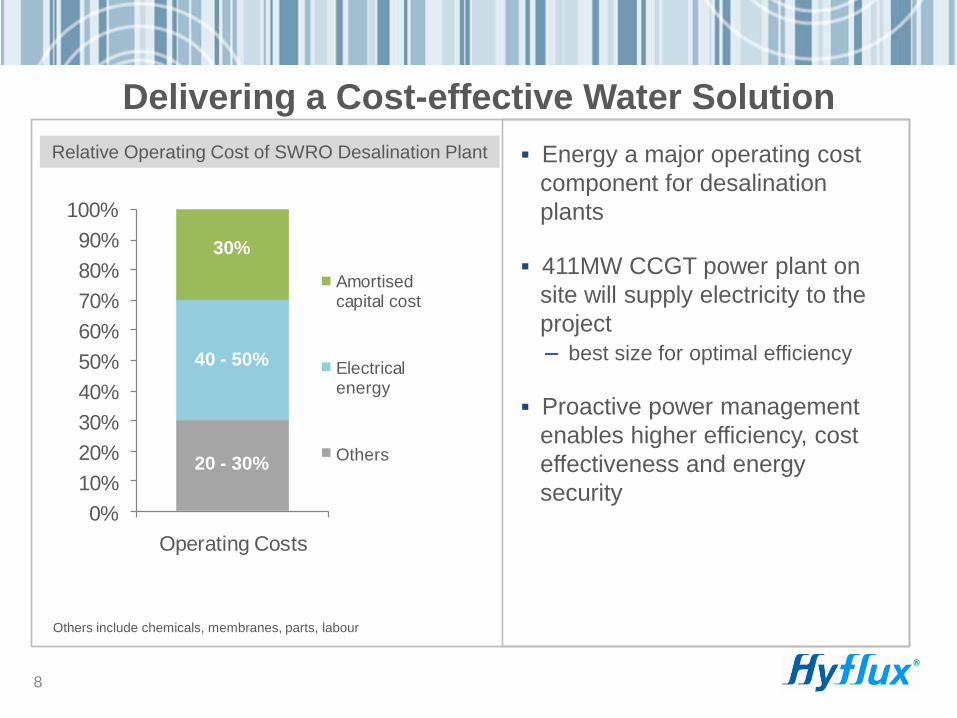

Delivering a Cost-effective Water Solution

Energy a major operating cost

component for desalination

plants

411MW CCGT power plant on

site will supply electricity to the

project

– best size for optimal efficiency

Proactive power management

enables higher efficiency, cost

effectiveness and energy

security

Relative Operating Cost of SWRO Desalination Plant

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Operating Costs

Amortised capital cost

Electrical energy

Others

Others include chemicals, membranes, parts, labour

30%

40 - 50%

20 - 30%

9

Driven by Our Innovative Membrane Technology

Second largest ultrafiltration

membrane installation after Magtaa

Desalination Plant in Algeria, the

world’s largest membrane-based

desalination plant

Proprietary Kristal ultrafiltration

membranes designed and developed

in-house

1) provide high quality water for reverse

osmosis pre-treatment

2) enhance performance and extend

lifespan of reverse osmosis membranes

3) consume less chemicals and energy

First ultrafiltration membrane to

achieve NSF certification for removal

of cryptosporidium

10

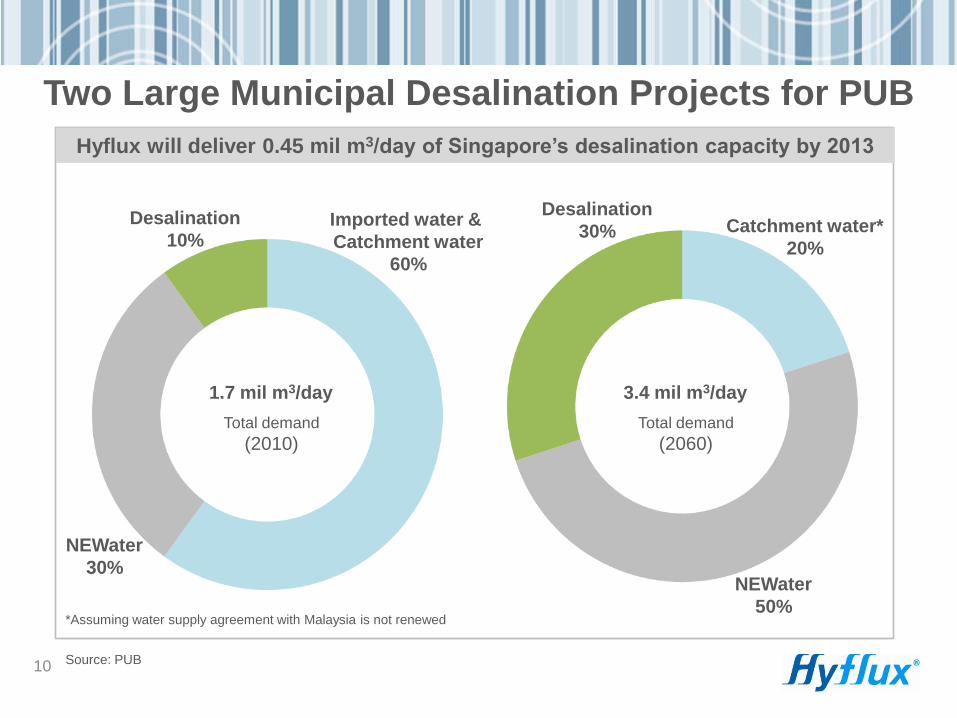

Two Large Municipal Desalination Projects for PUB

1.7 mil m3/day

Total demand

(2010)

3.4 mil m3/day

Total demand

(2060)

Desalination

10%

NEWater

30%

Imported water &

Catchment water

60%

NEWater

50%

Desalination

30% Catchment water*

20%

*Assuming water supply agreement with Malaysia is not renewed

Source: PUB

Hyflux will deliver 0.45 mil m3/day of Singapore’s desalination capacity by 2013

11

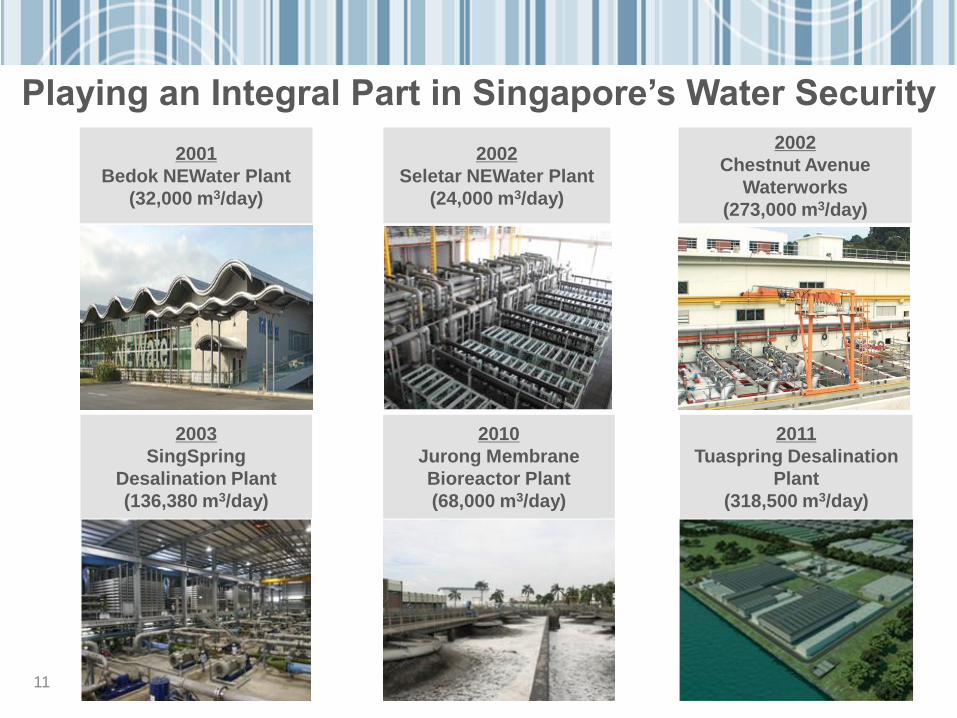

Playing an Integral Part in Singapore’s Water Security

2001

Bedok NEWater Plant

(32,000 m3/day)

2002

Seletar NEWater Plant

(24,000 m3/day)

2002

Chestnut Avenue

Waterworks

(273,000 m3/day)

2003

SingSpring

Desalination Plant

(136,380 m3/day)

2010

Jurong Membrane

Bioreactor Plant

(68,000 m3/day)

2011

Tuaspring Desalination

Plant

(318,500 m3/day)

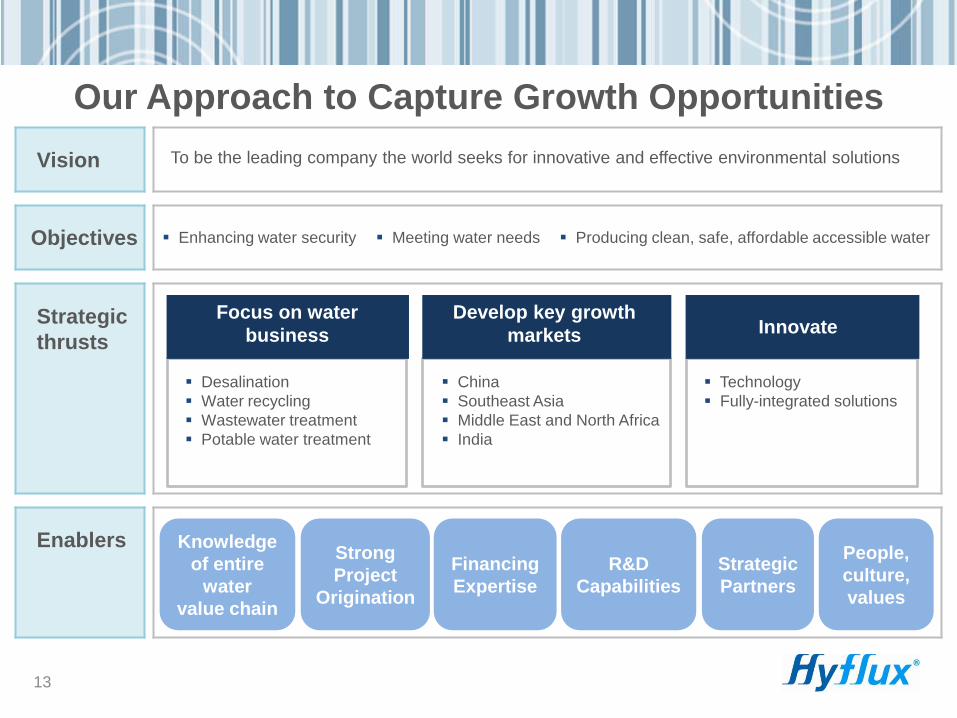

Hyflux’s Strategy

Vision To be the leading company the world seeks for innovative and effective environmental solutions

Objectives Enhancing water security Meeting water needs Producing clean, safe, affordable accessible water

Strategic

thrusts

Enablers

13

Our Approach to Capture Growth Opportunities

Knowledge

of entire

water

value chain

Strong

Project

Origination

Financing

Expertise

Strategic

Partners

R&D

Capabilities

People,

culture,

values

Focus on water

business

Develop key growth

markets Innovate

Desalination

Water recycling

Wastewater treatment

Potable water treatment

China

Southeast Asia

Middle East and North Africa

India

Technology

Fully-integrated solutions

14

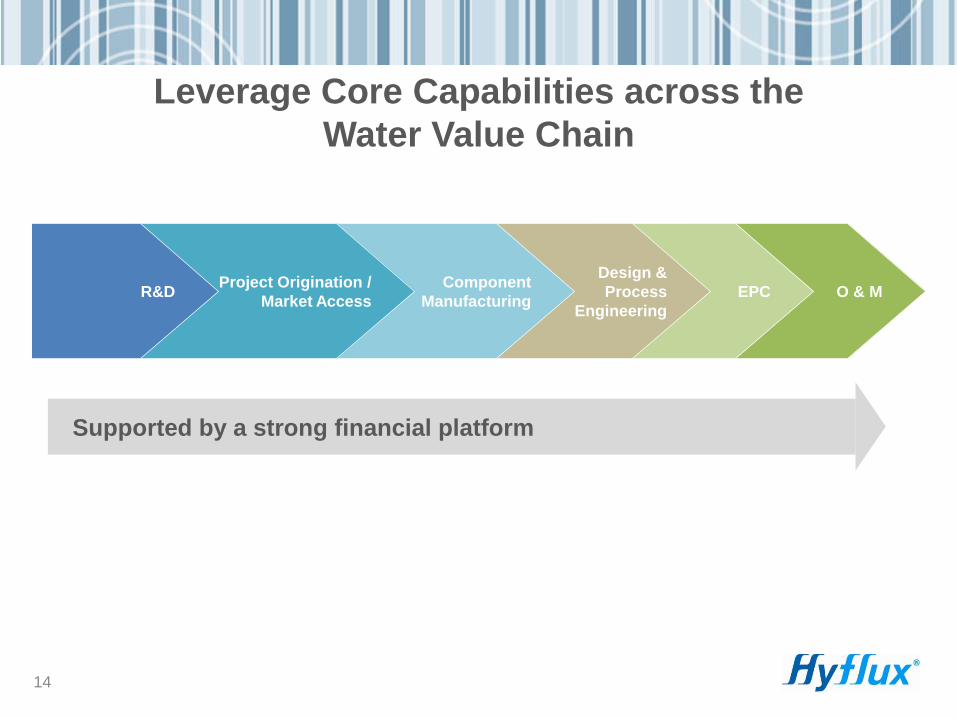

Leverage Core Capabilities across the

Water Value Chain

O & MEPC

Design &

Process

Engineering

Component

Manufacturing

Supported by a strong financial platform

Project Origination /

Market AccessR&D

15

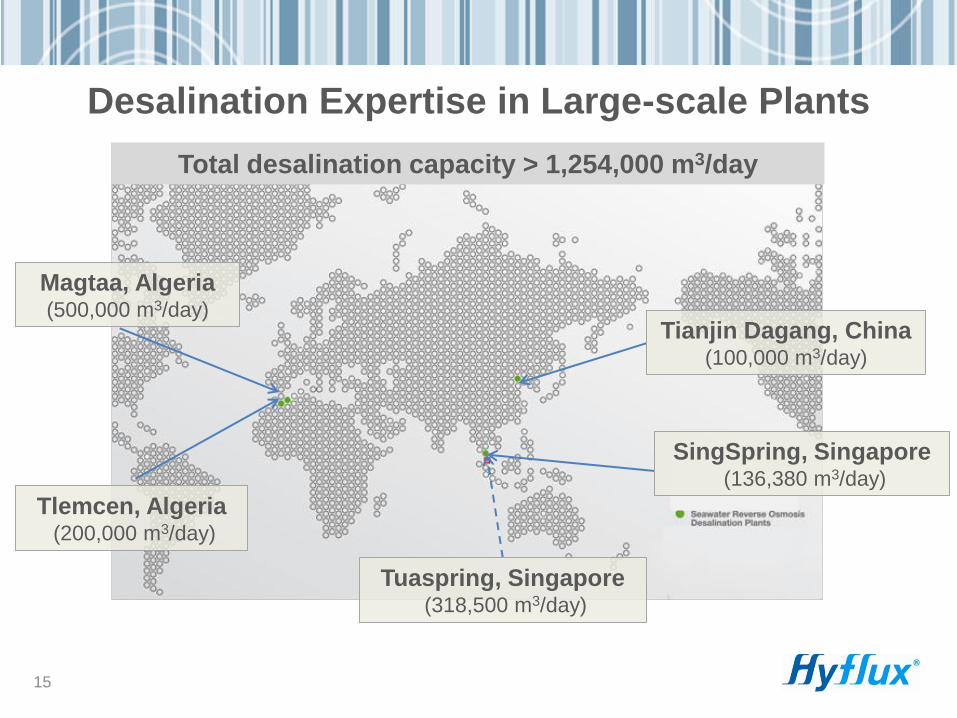

Magtaa, Algeria (500,000 m3/day)

Desalination Expertise in Large-scale Plants

Tlemcen, Algeria (200,000 m3/day)

Tianjin Dagang, China(100,000 m3/day)

SingSpring, Singapore (136,380 m3/day)

Tuaspring, Singapore (318,500 m3/day)

Total desalination capacity > 1,254,000 m3/day

16

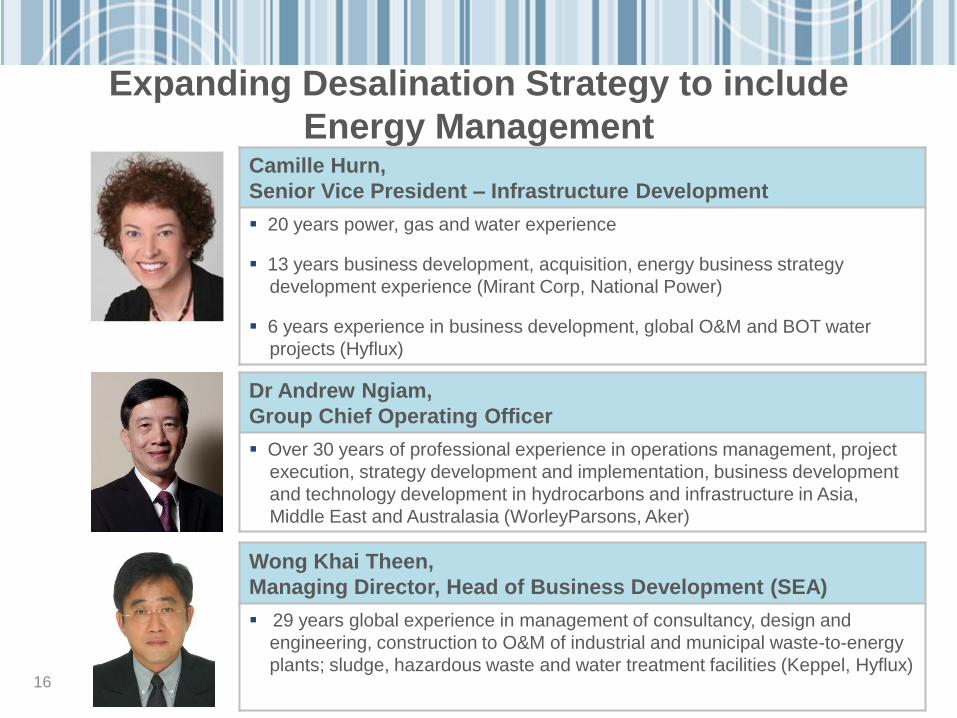

Expanding Desalination Strategy to include

Energy ManagementCamille Hurn,

Senior Vice President – Infrastructure Development

20 years power, gas and water experience

13 years business development, acquisition, energy business strategy

development experience (Mirant Corp, National Power)

6 years experience in business development, global O&M and BOT water

projects (Hyflux)

Wong Khai Theen,

Managing Director, Head of Business Development (SEA)

29 years global experience in management of consultancy, design and

engineering, construction to O&M of industrial and municipal waste-to-energy

plants; sludge, hazardous waste and water treatment facilities (Keppel, Hyflux)

Dr Andrew Ngiam,

Group Chief Operating Officer

Over 30 years of professional experience in operations management, project

execution, strategy development and implementation, business development

and technology development in hydrocarbons and infrastructure in Asia,

Middle East and Australasia (WorleyParsons, Aker)

17

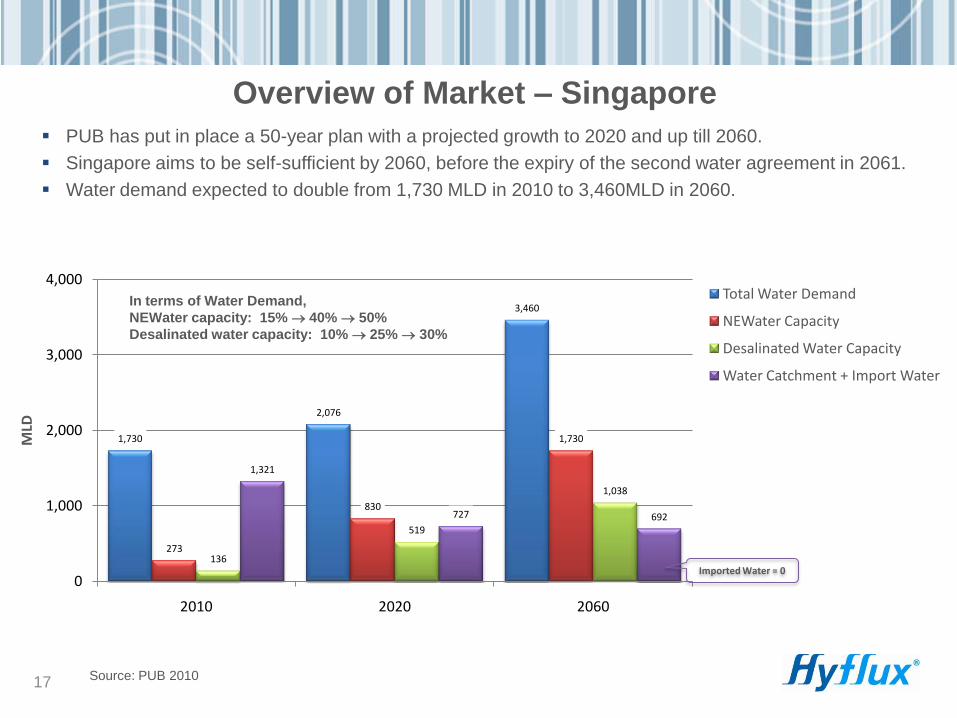

PUB has put in place a 50-year plan with a projected growth to 2020 and up till 2060.

Singapore aims to be self-sufficient by 2060, before the expiry of the second water agreement in 2061.

Water demand expected to double from 1,730 MLD in 2010 to 3,460MLD in 2060.

Overview of Market – Singapore

Source: PUB 2010

1,730

2,076

3,460

273

830

1,730

136

519

1,038

1,321

727 692

0

1,000

2,000

3,000

4,000

2010 2020 2060

MLD

Total Water Demand

NEWater Capacity

Desalinated Water Capacity

Water Catchment + Import Water

In terms of Water Demand,

NEWater capacity: 15% 40% 50%

Desalinated water capacity: 10% 25% 30%

Imported Water = 0

18

Overview of Market – Indonesia

Source: IE Singapore, GWI Indonesia, PPP in Indonesia, Ministry of National Development Planning

Currently, only 47% of total population have access to improved water source.

By end of 2014, as part of the roadmap to achieve the Millennium Development Goals (MDG) set by

United Nations, the Government wants to increase household access to an improved drinking water

source to ~70% of total population.

One of Water Resources Development Targets for 2010 – 2014: To increase the raw water infrastructure

service capacity by 43.4 m3/s (~3,740MLD).

214

242

278

317

354

379

170

193

223

253

280295

44 48 55 6474

84

0

100

200

300

400

500

2010 2011 2012 2013 2014 2015

S$ M

illio

n

Indonesia Market Forecast

Total CAPEX

WTP

WWTP

19

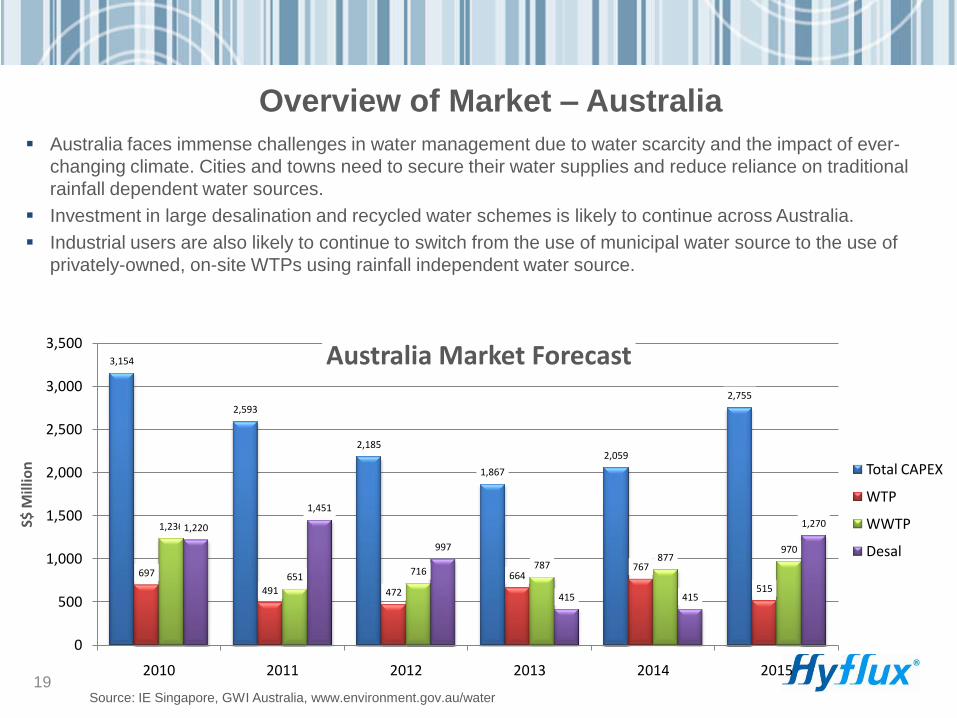

Australia faces immense challenges in water management due to water scarcity and the impact of ever-

changing climate. Cities and towns need to secure their water supplies and reduce reliance on traditional

rainfall dependent water sources.

Investment in large desalination and recycled water schemes is likely to continue across Australia.

Industrial users are also likely to continue to switch from the use of municipal water source to the use of

privately-owned, on-site WTPs using rainfall independent water source.

Overview of Market – Australia

Source: IE Singapore, GWI Australia, www.environment.gov.au/water

3,154

2,593

2,185

1,867

2,059

2,755

697

491 472

664767

515

1,236

651716

787877

970

1,220

1,451

997

415 415

1,270

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015

S$ M

illio

n

Australia Market Forecast

Total CAPEX

WTP

WWTP

Desal

China40%

SoutheastAsia

30%

Others30%

20

Focus on Diversifying Geographical Revenue Streams

Revenue contribution by region

2014(estimated)

S$ mil

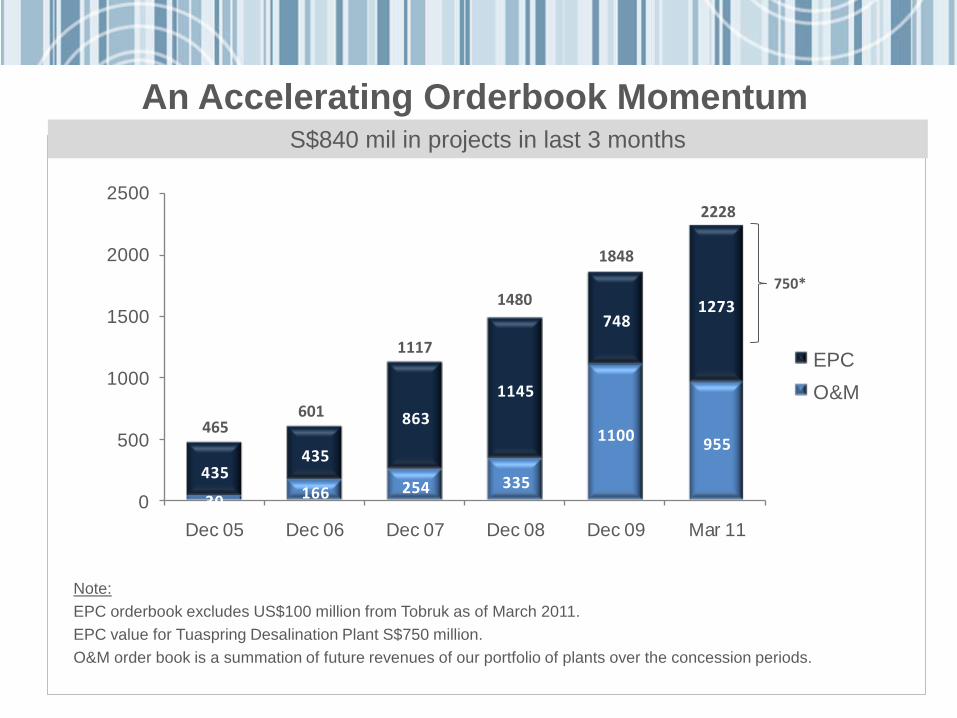

An Accelerating Orderbook Momentum

30 166 254 335

1100955

435435

863

1145

7481273

0

500

1000

1500

2000

2500

Dec 05 Dec 06 Dec 07 Dec 08 Dec 09 Mar 11

EPC

O&M

465601

1117

1480

1848

2228

S$840 mil in projects in last 3 months

750*

Note:

EPC orderbook excludes US$100 million from Tobruk as of March 2011.

EPC value for Tuaspring Desalination Plant S$750 million.

O&M order book is a summation of future revenues of our portfolio of plants over the concession periods.

WATER SOLUTIONS

THAT

IMPACT LIVES

23

Disclaimer

This presentation has been prepared by Hyflux Ltd for the information of the attendees of this presentation.

This presentation is not and does not constitute or form part of any offer, invitation or recommendation to subscribe for or purchase any security and neither this presentation nor anything contained in it shall form the basis of, or be relied upon in connection with, any contract, commitment or investment decision. This document may not be used or relied upon by any party, or for any other purpose, and may not be reproduced, disseminated or quoted without the prior written consent of Hyflux Ltd.

No representation or warranty express or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. None of Hyflux Ltd or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this presentation.