Embed Size (px)

Citation preview

IB Business and Management

5.2 – Costs and Revenues

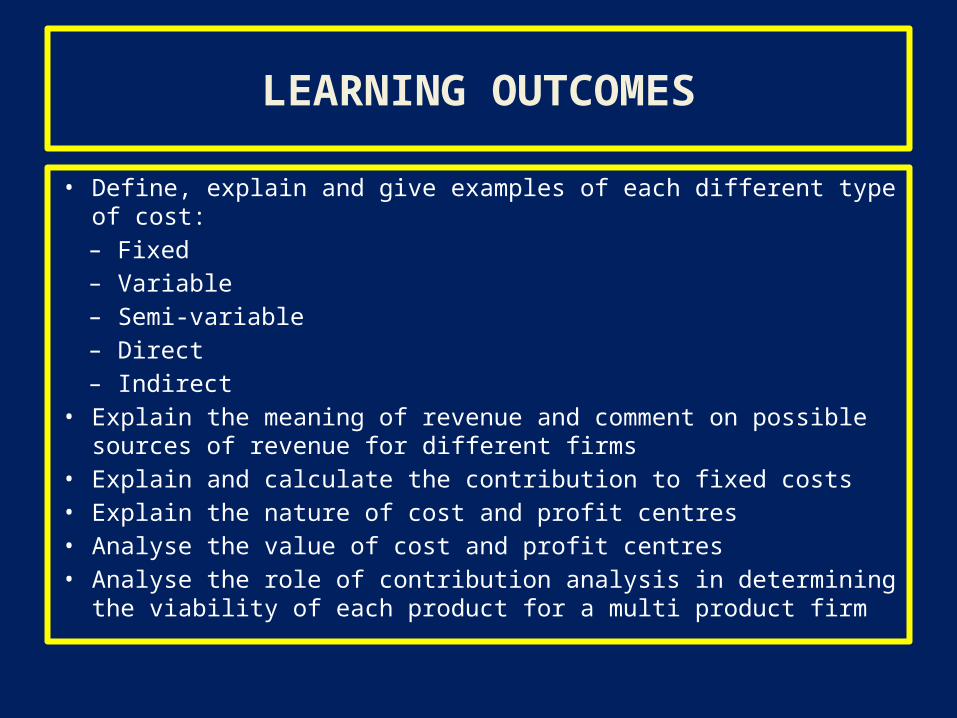

LEARNING OUTCOMES

• Define, explain and give examples of each different type of cost:– Fixed– Variable– Semi-variable– Direct– Indirect

• Explain the meaning of revenue and comment on possible sources of revenue for different firms

• Explain and calculate the contribution to fixed costs• Explain the nature of cost and profit centres• Analyse the value of cost and profit centres• Analyse the role of contribution analysis in determining the

viability of each product for a multi product firm

RECAP – COST CLASSIFICATIONS

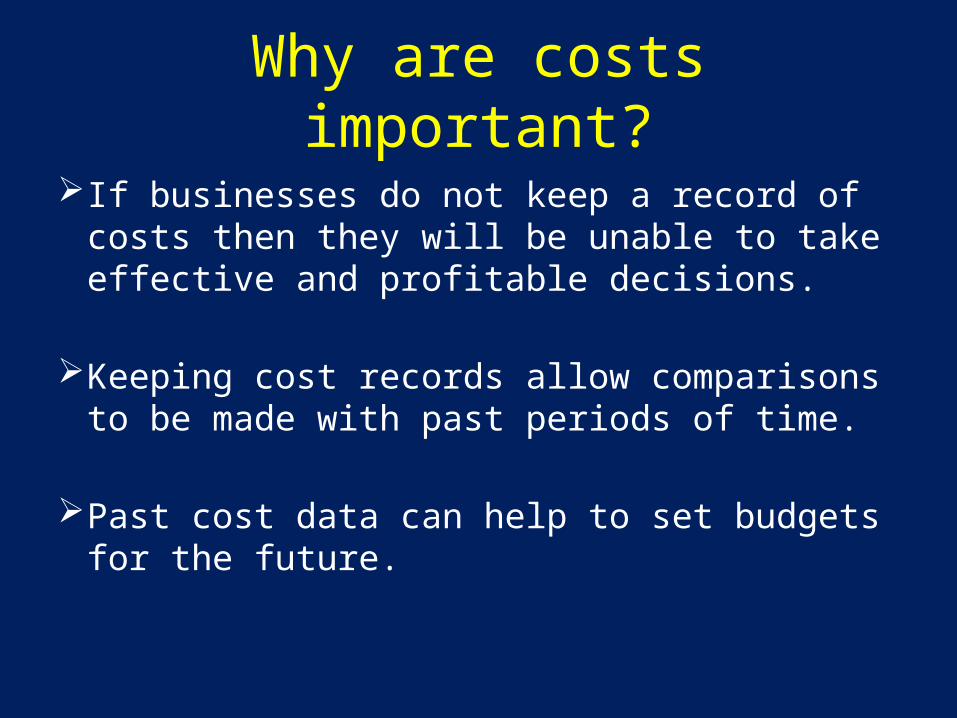

Why are costs important?

If businesses do not keep a record of costs then they will be unable to take effective and profitable decisions.

Keeping cost records allow comparisons to be made with past periods of time.

Past cost data can help to set budgets for the future.

Costs we need to know about…

– Fixed– Variable– Semi-variable– Direct– Indirect

In Pairs……Can you define each of these? (Imagine

you are writing a 2 mark definition answer)

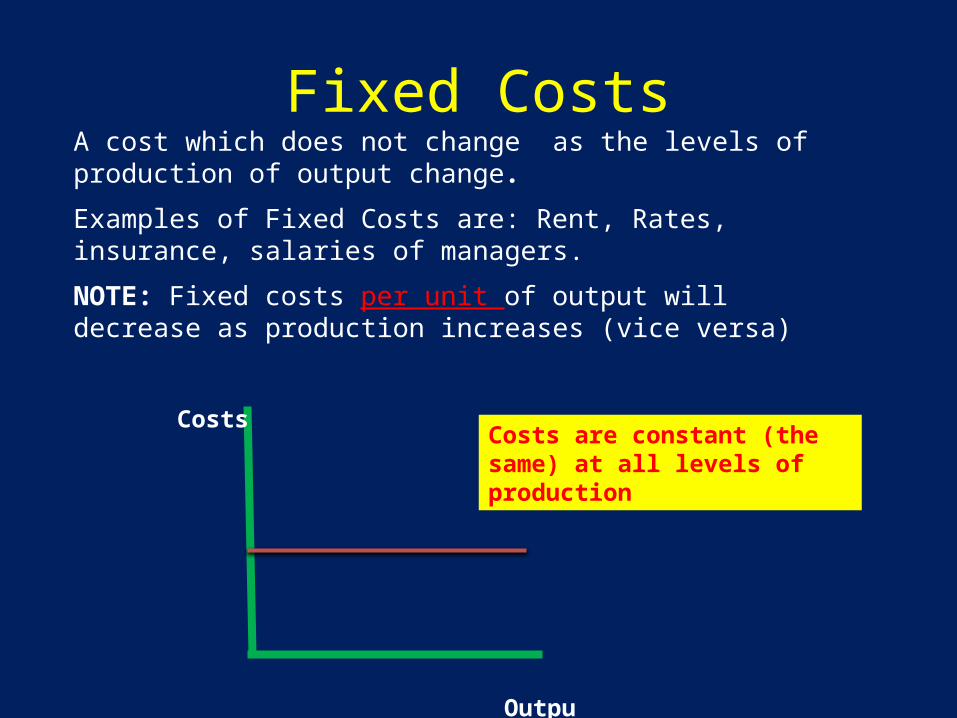

A cost which does not change as the levels of production of output change.

Examples of Fixed Costs are: Rent, Rates, insurance, salaries of managers.

NOTE: Fixed costs per unit of output will decrease as production increases (vice versa)

Costs are constant (the same) at all levels of production

Costs

Output

Fixed Costs

$1000

Output

Costs Variable Costs

400

$1500

600

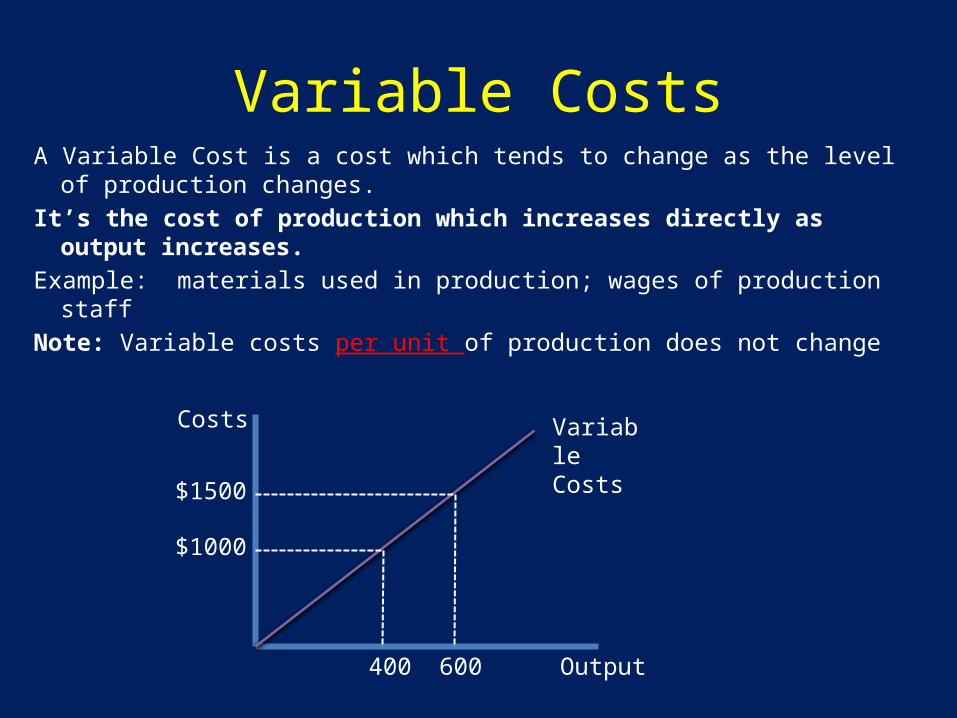

Variable CostsA Variable Cost is a cost which tends to change as the level of

production changes. It’s the cost of production which increases directly as

output increases. Example: materials used in production; wages of production

staffNote: Variable costs per unit of production does not change

Semi-variable Costs

Costs with both a fixed and a variable element.Often the cost is fixed up to a certain level of output and then becomes variable after that level is exceededExamples:-Telephone Bill -Electricity Bills-Some Labour costs

Can you explain why these costs are semi-variable?

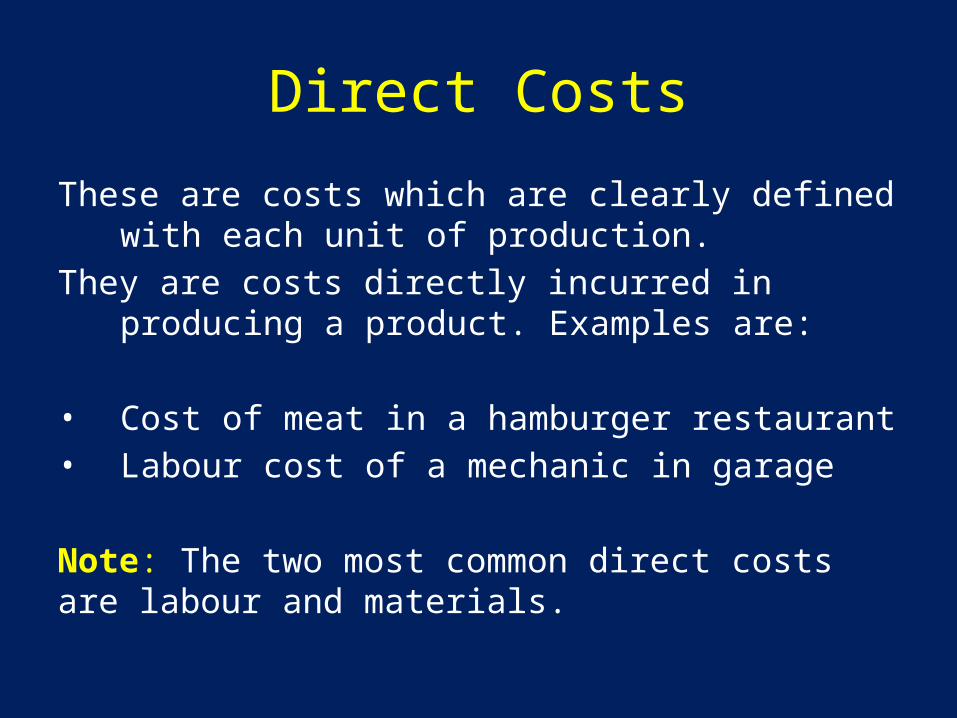

Direct Costs

These are costs which are clearly defined with each unit of production.

They are costs directly incurred in producing a product. Examples are:

• Cost of meat in a hamburger restaurant • Labour cost of a mechanic in garage

Note: The two most common direct costs are labour and materials.

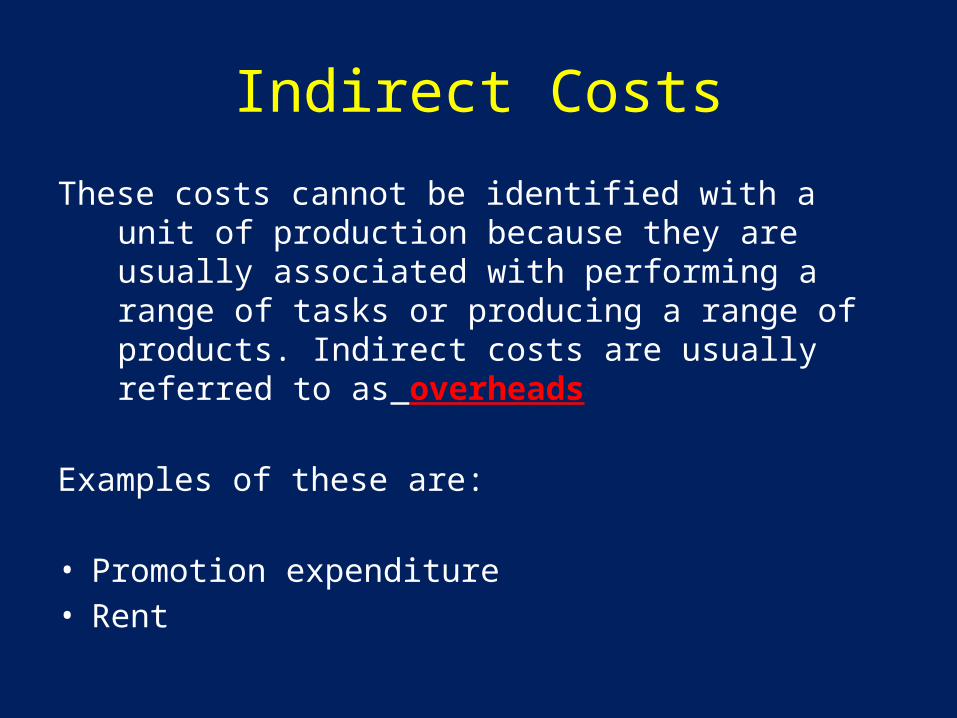

Indirect Costs

These costs cannot be identified with a unit of production because they are usually associated with performing a range of tasks or producing a range of products. Indirect costs are usually referred to as overheads

Examples of these are:

• Promotion expenditure• Rent

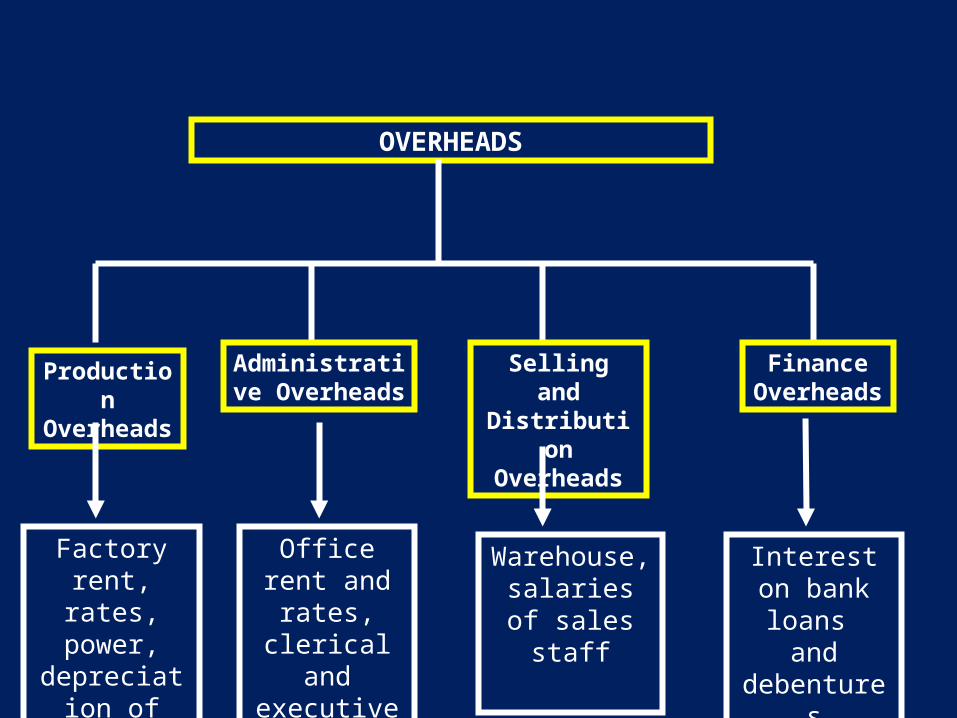

OVERHEADS

Production Overheads

Administrative Overheads

Selling and Distribution Overheads

Finance Overheads

Factory rent, rates, power, depreciation

of equipment.

Office rent and rates,

clerical and executive salaries

Warehouse, salaries of sales staff

Interest on bank loans

and debentures

Identify the costs…..Fixed CostsVariable CostsSemi Variable CostsDirect CostsIndirect Costs

REVENUEWhat is meant by revenue?

Revenue

Revenue or turnover is income that a company receives from its normal business activities, usually from the sale of goods and services to customers.

So what types of income does revenue NOT include?

Calculating Revenue

Revenue =

Selling PriceX

Quantity

What are the revenue streams?

CONTRIBUTION

Contribution:

• Contribution is the amount that each product sold makes towards paying off fixed costs.

• Once fixed costs have been covered all contribution will be profit

• What is the formula for contribution?Contribution Per Unit = Selling Price – Variable Cost per unit*

*or average variable cost

Contribution - Example

A carpenter makes tables that he sells for $500. He pays himself $50 an hour. The cost of the wood is $150 per table and takes him 4 hours to make. What is the contribution per unit?= $500 – [$150 + (4 x $50)] = $150

Total Contribution

• Total contribution is the overall amount of contribution that the business makes at a particular level of output:

Total Contribution = Contribution per unit x Quantity Sold

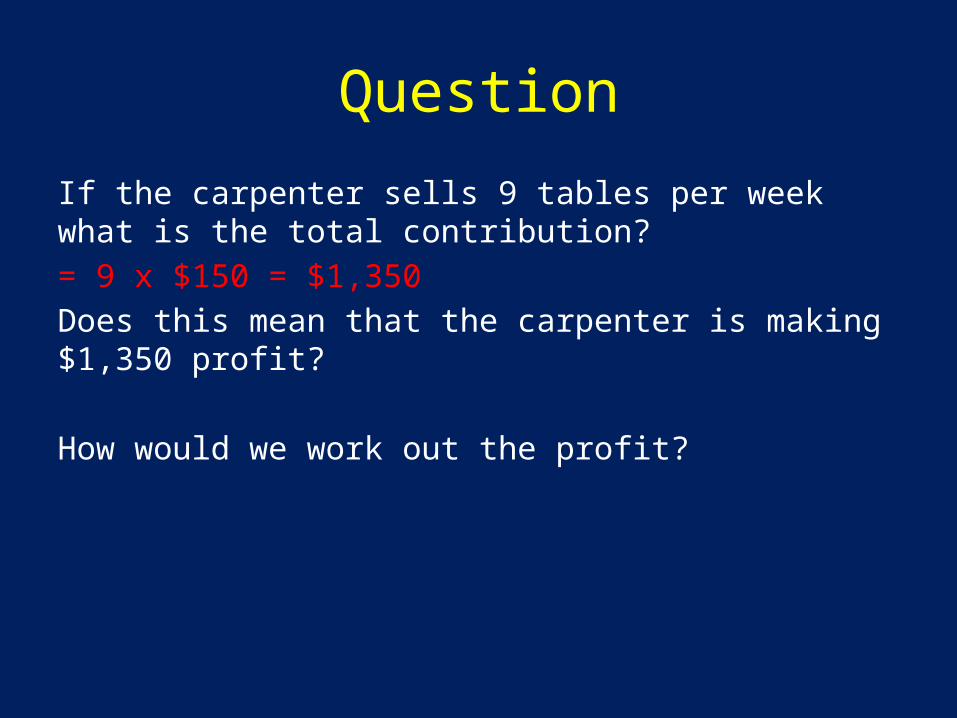

Question

If the carpenter sells 9 tables per week what is the total contribution?= 9 x $150 = $1,350Does this mean that the carpenter is making $1,350 profit?

How would we work out the profit?

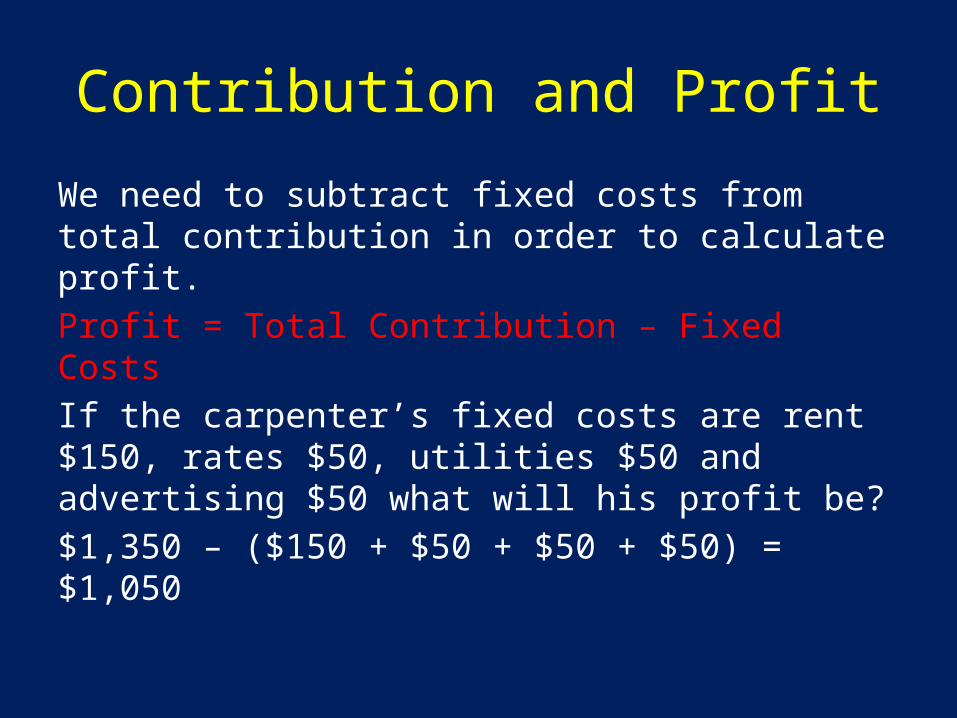

Contribution and Profit

We need to subtract fixed costs from total contribution in order to calculate profit.Profit = Total Contribution – Fixed Costs If the carpenter’s fixed costs are rent $150, rates $50, utilities $50 and advertising $50 what will his profit be?$1,350 – ($150 + $50 + $50 + $50) = $1,050

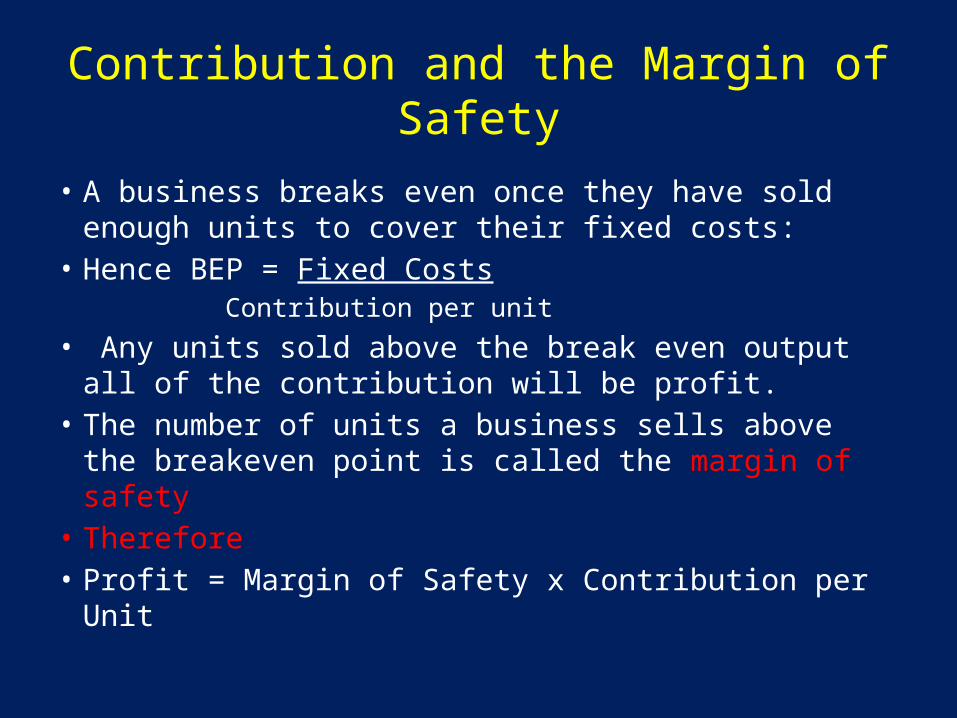

Contribution and the Margin of Safety

• A business breaks even once they have sold enough units to cover their fixed costs:

• Hence BEP = Fixed CostsContribution per unit

• Any units sold above the break even output all of the contribution will be profit.

• The number of units a business sells above the breakeven point is called the margin of safety

• Therefore • Profit = Margin of Safety x Contribution per

Unit

Uses of Contribution Analysis

• Special Order Decisions• Contribution Cost Pricing• Product Portfolio Management• Make or Buy Decisions

Scenario- Special order decision

Simpson Ltd produces cartons of freshly squeezed fruit juice. The average cost of producing one carton is £1.15.

It usually sells them for £1.50 to supermarkets and independent retailers.

A company have approached Simpson’s with a one-off order for 10,000 units but are only prepared to pay £1.10 per unit.

Should the company accept the order?

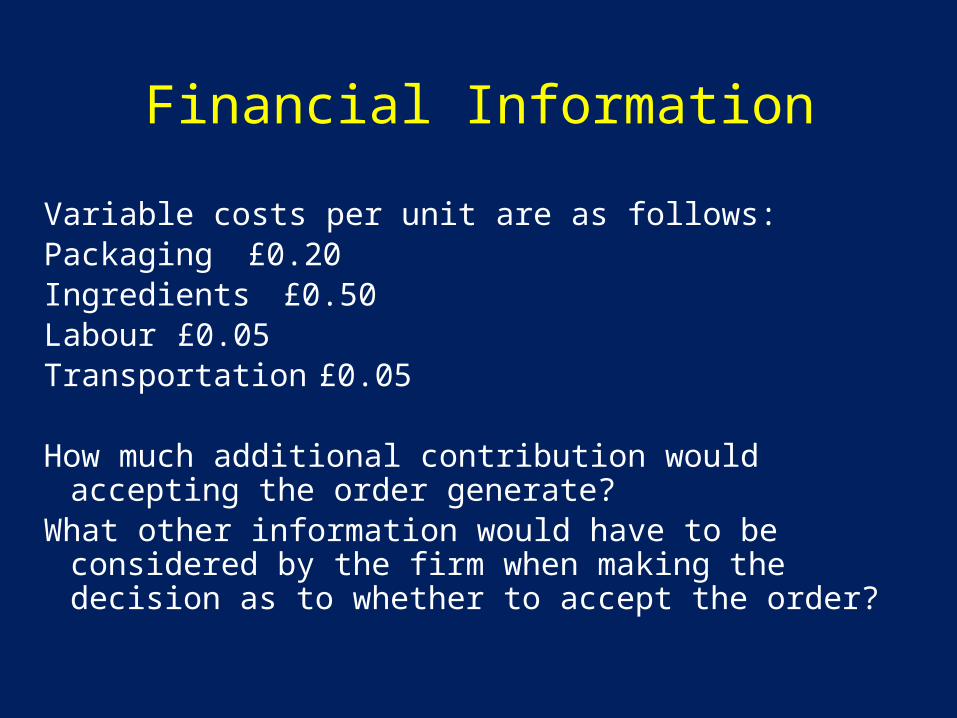

Financial Information

Variable costs per unit are as follows:Packaging £0.20Ingredients £0.50Labour £0.05Transportation £0.05

How much additional contribution would accepting the order generate?

What other information would have to be considered by the firm when making the decision as to whether to accept the order?

CONTRIBUTION ANALYSIS FOR MULTI-PRODUCT FIRMS

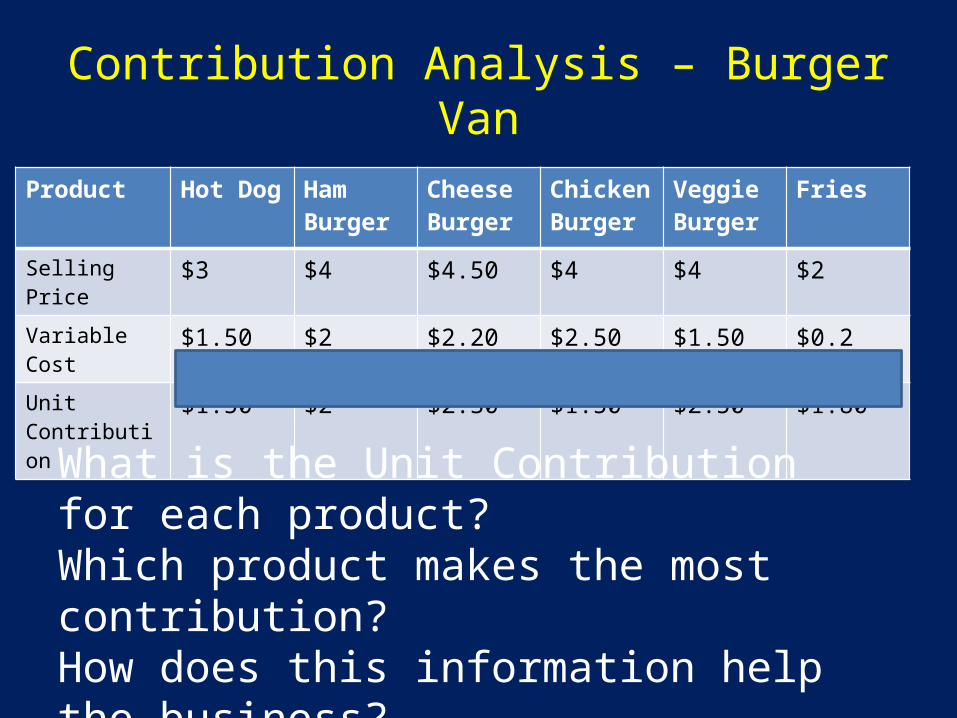

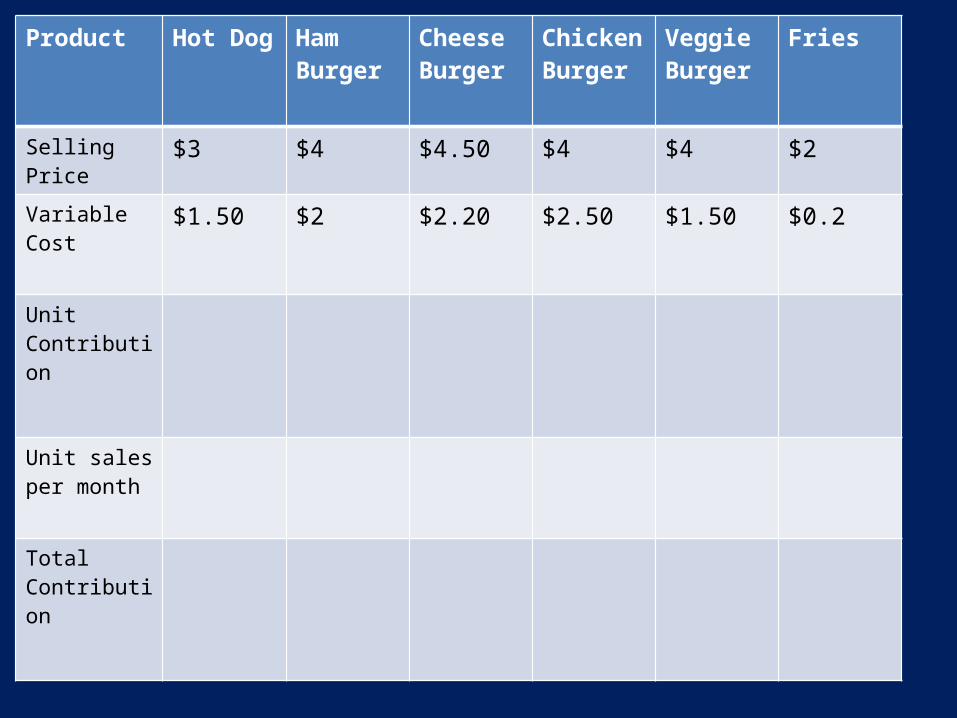

Contribution Analysis – Burger Van

Product Hot Dog Ham Burger

Cheese Burger

Chicken Burger

Veggie Burger

Fries

Selling Price $3 $4 $4.50 $4 $4 $2

Variable Cost $1.50 $2 $2.20 $2.50 $1.50 $0.2

Unit Contribution

$1.50 $2 $2.30 $1.50 $2.50 $1.80

What is the Unit Contribution for each product?Which product makes the most contribution?How does this information help the business?

Total contribution is also important:

Product Hot Dog Ham Burger

Cheese Burger

Chicken Burger

Veggie Burger

Fries

Selling Price $3 $4 $4.50 $4 $4 $2

Variable Cost $1.50 $2 $2.20 $2.50 $1.50 $0.2

Unit Contribution

$1.50 $2 $2.30 $1.50 $2.50 $1.80

Unit sales per month

400 600 700 600 100 3,000

Total Contribution

$600 $1,200 $1,610 $900 $250 $5,400

What is the total contribution?$9960Assuming that the burger van has fixed costs of $6,000 per month what will be the profit be?$3,960How can the burger van use this information to help them make decisions?Contribution Cost PricingProduct Portfolio ManagementMake or Buy Decisions

COST AND PROFIT CENTRES

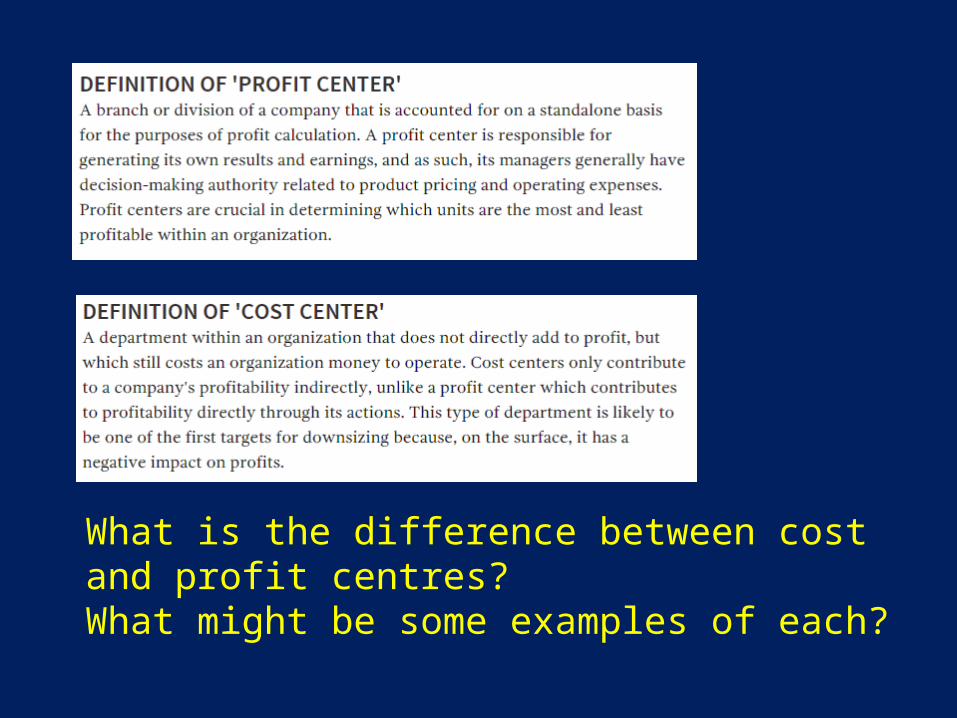

What are they and what is the difference?

What is the difference between cost and profit centres?What might be some examples of each?

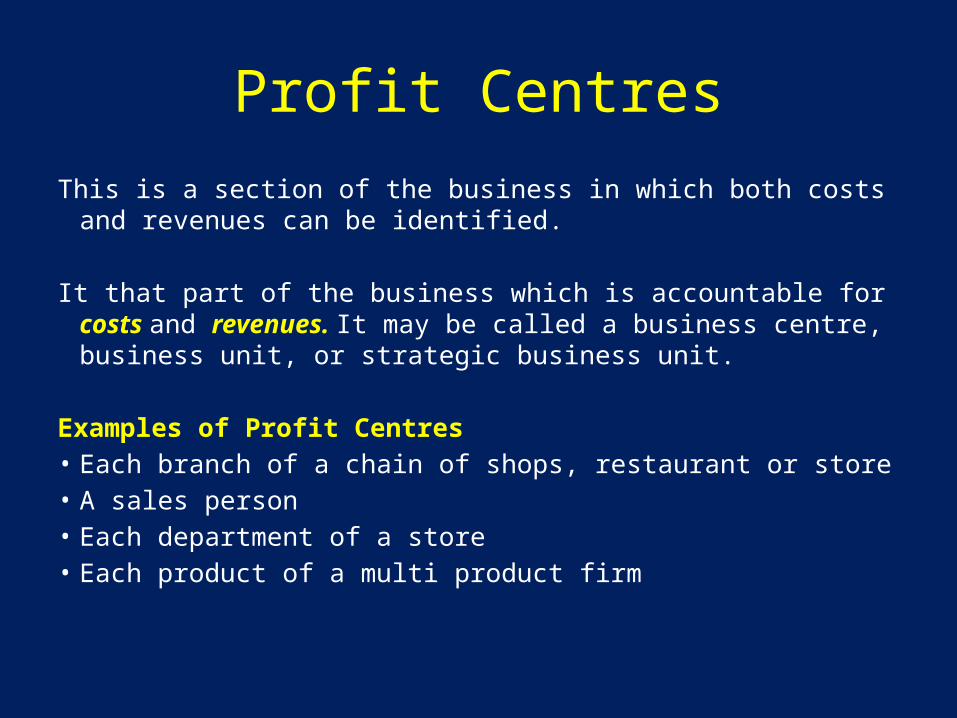

This is a section of the business in which both costs and revenues can be identified.

It that part of the business which is accountable for costs and revenues. It may be called a business centre, business unit, or strategic business unit.

Examples of Profit Centres• Each branch of a chain of shops, restaurant or store• A sales person• Each department of a store• Each product of a multi product firm

Profit Centres

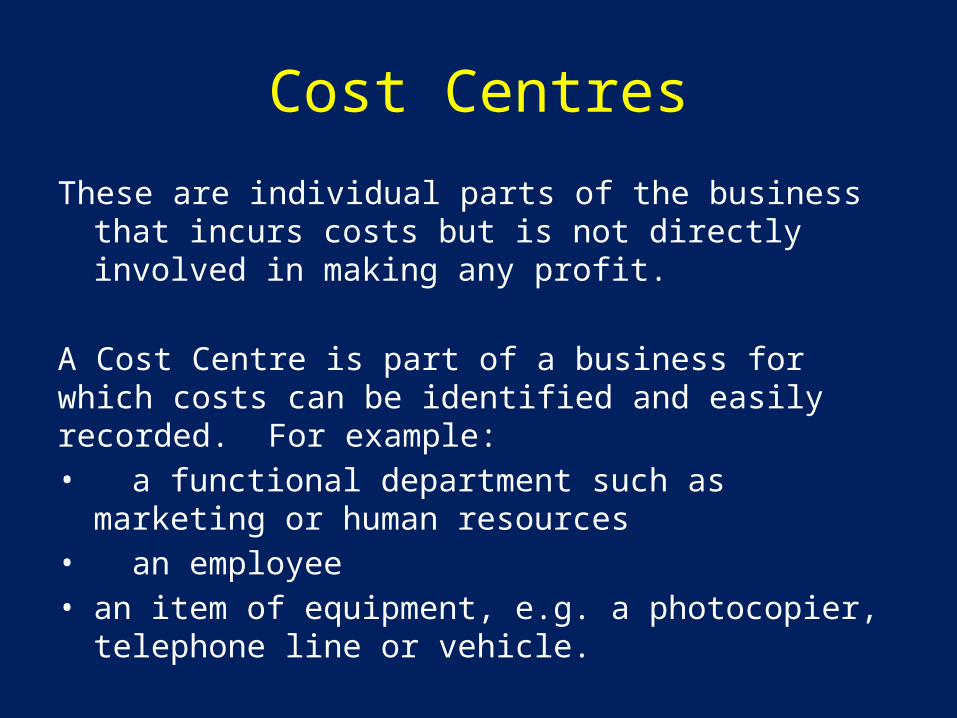

These are individual parts of the business that incurs costs but is not directly involved in making any profit.

A Cost Centre is part of a business for which costs can be identified and easily recorded. For example:• a functional department such as marketing or

human resources• an employee• an item of equipment, e.g. a photocopier,

telephone line or vehicle.

Cost Centres

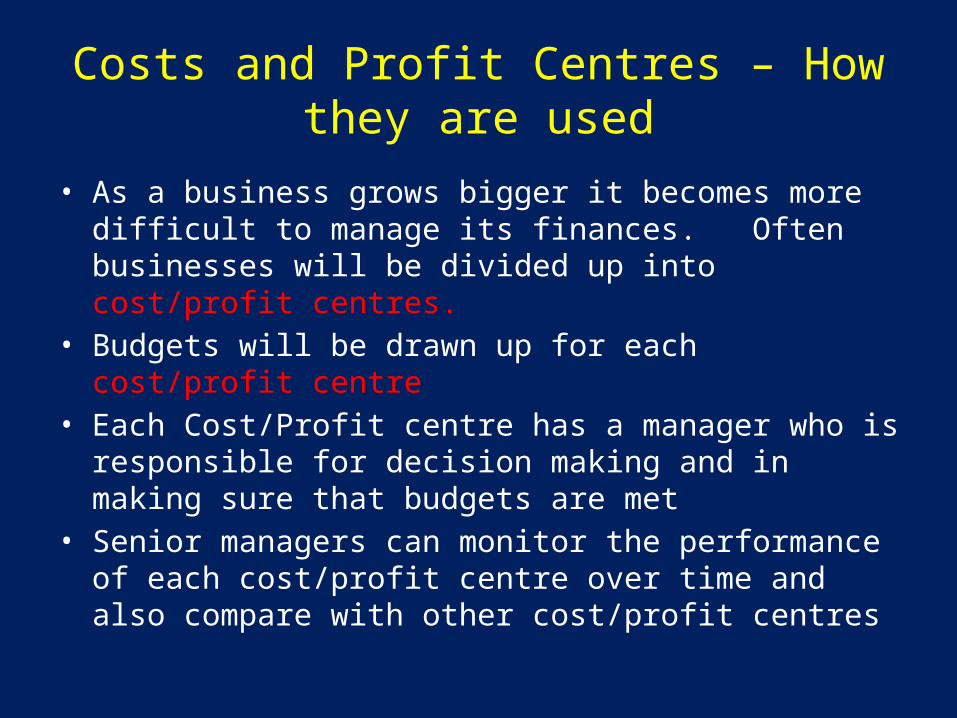

Costs and Profit Centres – How they are used

• As a business grows bigger it becomes more difficult to manage its finances. Often businesses will be divided up into cost/profit centres.

• Budgets will be drawn up for each cost/profit centre

• Each Cost/Profit centre has a manager who is responsible for decision making and in making sure that budgets are met

• Senior managers can monitor the performance of each cost/profit centre over time and also compare with other cost/profit centres

Benefits and drawbacks of Cost/Profit Centres?

• What do you think are the main benefits of cost/profit centres?

• Watch the video

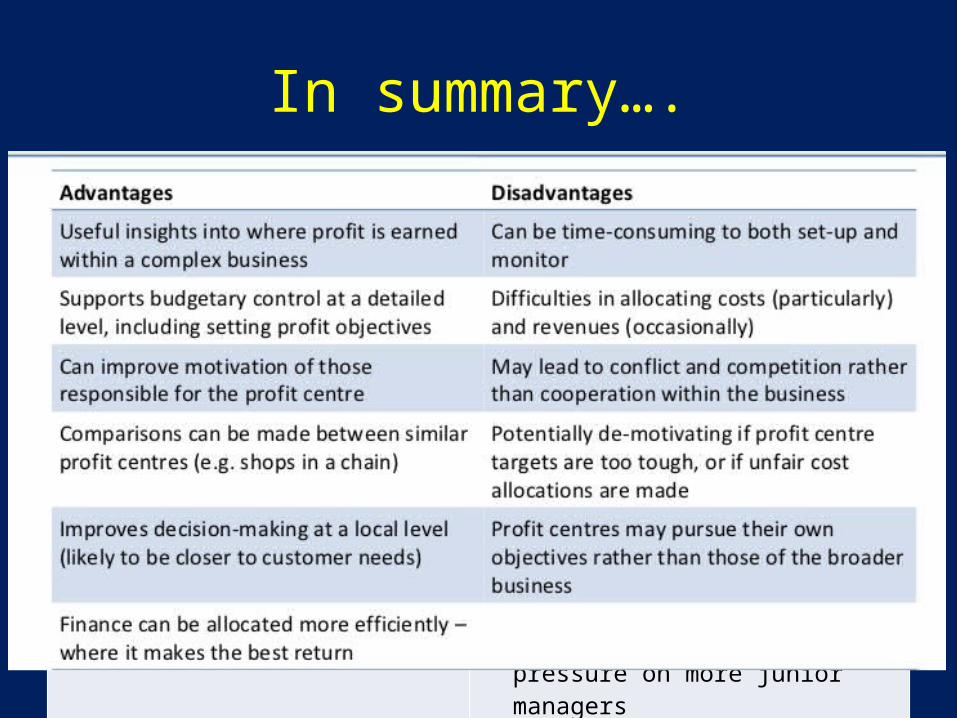

In summary….ADVANTAGES OF COST AND PROFIT

CENTRESDISADVANTAGES OF COST AND PROFIT

CENTRES* Some control of operations is

delegated to the local level, which can be motivating

* parts of the firm can put themselves before the business as a whole

* The success and failures of individual departments can be identified clearly

* The reason for good or bad performance may be external to the cost centre, and not under its control

* Problems can be traced more easily * Not all costs and revenues can be associated directly with a particular part of the firm

* Decision making is aided * They can create extra pressure on more junior managers

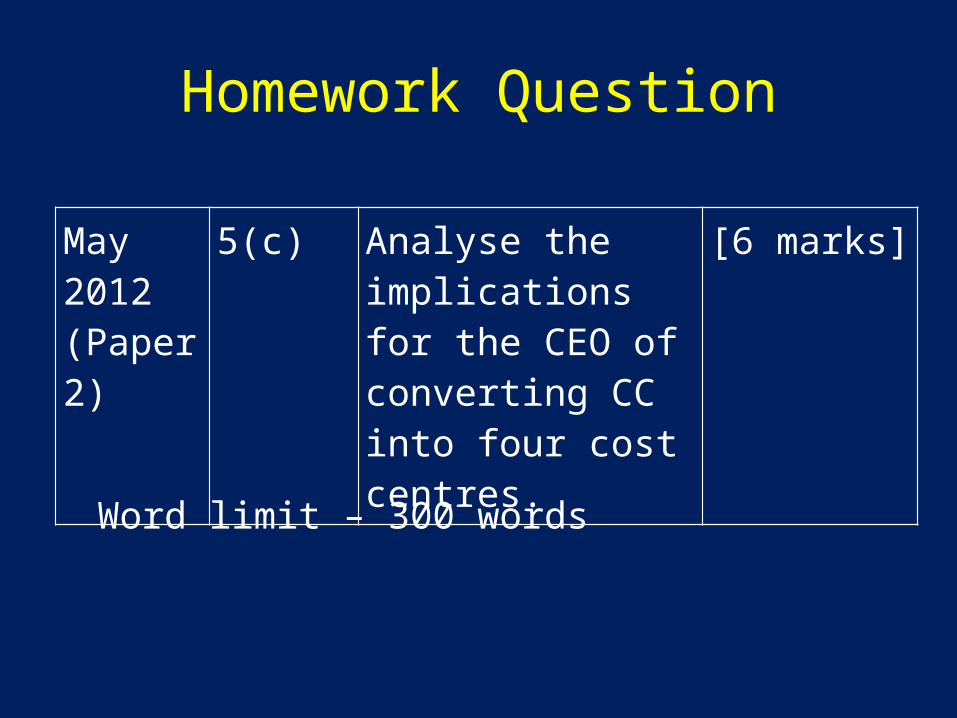

Homework Question

May 2012 (Paper 2)

5(c) Analyse the implications for the CEO of converting CC into four cost centres.

[6 marks]

Word limit – 300 words

Product Hot Dog Ham Burger

Cheese Burger

Chicken Burger

Veggie Burger

Fries

Selling Price $3 $4 $4.50 $4 $4 $2

Variable Cost $1.50 $2 $2.20 $2.50 $1.50 $0.2

Unit Contribution

Unit sales per month

Total Contribution