Embed Size (px)

Citation preview

ICICI Prudential PMS Flexicap Portfolio

A series under "Aggressive" Portfolio

All data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. ICICI Prudential Asset Management Company Limited (the

Portfolio Manager/ the AMC) takes no responsibility of updating any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this

material. The information contained herein are strictly confidential and are meant solely for the benefit of the addressee and shall not be altered in any way, transmitted to, copied or distributed, in part or in

whole, to any other person or to the media or reproduced in any form, without prior written consent of the AMC. Further, the information contained herein should not be construed as forecast or promise. Past

performance of the Portfolio Manager may not be indicative of the performance in the future. Please refer to page 15 & 16 for risk factors and disclaimers.

Global Indices Performance – India surges ahead

• Indian markets rose by 7.8%

on the back of increased FII

flows to the tune of Rs. 33,116

Crs

• With China markets

experiencing a slowdown last

year, the economy is gradually

reviving owing to monetary

expansion policies and heavy

infrastructure investments

thus aiding growth

Germany - DAX Index; China - SSE Composite Index; France - CAC 40 Index; Japan - Nikkei; Eurozone - Euronext 100; Hong Kong - HangSeng; US - Dow Jones; Singapore - Strait Times; Russia - RTS Index; Indonesia - Jakarta Composite Index; U.K. - FTSE; South

Korea - Kospi; Brazil - Ibovespa Sao Paulo Index; Indonesia – Jakarta Composite Index; Switzerland – Swiss Market Index; Taiwan – Taiwan Stock Exchange Corporation; India – S&P BSE Sensex; Returns in % terms. Data Source: MFI; Returns are absolute returns for

the PRI variant of the index calculated between Feb 28, 2019 – March 29, 2019. Past performance may or may not be sustained in future

7.8

5.1

2.9 2.8 2.3 2.1

1.5 0.9 0.8

0.4 0.1 0.0 0.0

-0.2 -0.8

-2.5 -4

-2

0

2

4

6

8

10

India

Chin

a

UK

Taiw

an

Europe

Fran

ce

Hong K

ong

Sw

itzerla

nd

Russia

Indo

nesia

Germ

any

US

Sin

gapore

Brazil

Japan

South K

orea

Returns (

%)

Returns Performance - March 2019

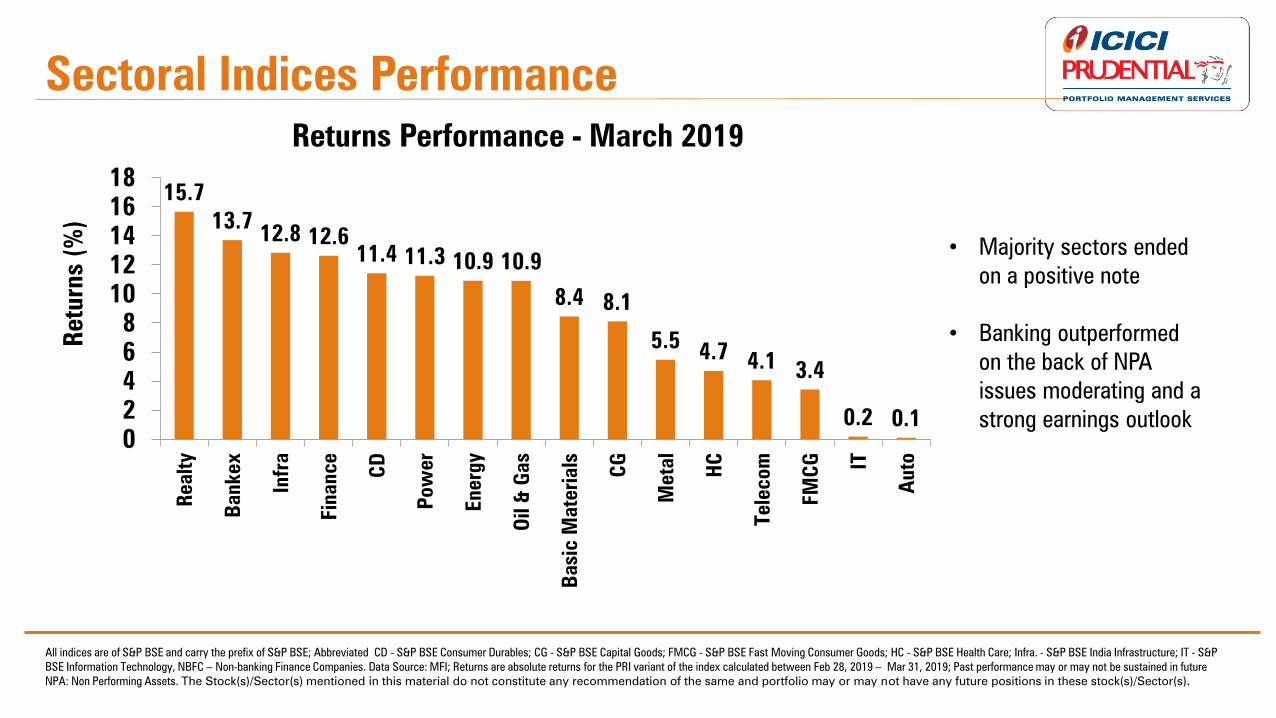

Sectoral Indices Performance

All indices are of S&P BSE and carry the prefix of S&P BSE; Abbreviated CD - S&P BSE Consumer Durables; CG - S&P BSE Capital Goods; FMCG - S&P BSE Fast Moving Consumer Goods; HC - S&P BSE Health Care; Infra. - S&P BSE India Infrastructure; IT - S&P

BSE Information Technology, NBFC – Non-banking Finance Companies. Data Source: MFI; Returns are absolute returns for the PRI variant of the index calculated between Feb 28, 2019 – Mar 31, 2019; Past performance may or may not be sustained in future

NPA: Non Performing Assets. The Stock(s)/Sector(s) mentioned in this material do not constitute any recommendation of the same and portfolio may or may not have any future positions in these stock(s)/Sector(s).

• Majority sectors ended

on a positive note

• Banking outperformed

on the back of NPA

issues moderating and a

strong earnings outlook

15.7

13.7 12.8 12.6

11.4 11.3 10.9 10.9

8.4 8.1

5.5 4.7

4.1 3.4

0.2 0.1

0

2

4

6

8

10

12

14

16

18R

ealt

y

Ban

kex

In

fra

Fin

an

ce

CD

Po

wer

Energy

Oil &

Gas

Basic

Materia

ls

CG

Metal

HC

Tele

com

FM

CG IT

Au

to

Returns (

%)

Returns Performance - March 2019

RESERVE BANK OF INDIA

• India’s GDP growth estimates for FY 2018-19 revised

downwards to 7.0% from 7.2% earlier

• RBI cut repo rates by 25 bps to 6.0% to support

growth and meet inflation target of 4%

Global Growth Concerns

Uncertainty about growth weighed on the minds of central banks everywhere resulting in them adopting a cautious stance.

US FEDERAL RESERVE BANK

• The Fed lowered its GDP

growth forecast (2.1% to

2.3% earlier for 2019) &

inflation expectations

• Adopted a dovish stance of

not hiking rates further in

2019

EUROPEAN CENTRAL BANK

• Weakening economic data

points to a sizeable

moderation in pace of

economic expansion &

underlying inflation continues

to be muted

• Interest Rates to remain

unchanged throughout 2019

Source: RBI, European Central Bank, US Federal Reserve Monetary Policy Meet Minutes

Growth Numbers

Change in US Fed Stance and Opinion Poll Comfort led to record FPI flows (best since March-16). Going forward, FPI

flows could get volatile depending on stability of the new government and Global Central Bank Policies

Source: SEBI, BSE, CDSL, Morgan Stanley Research; Data as of March 31, 2019. FPI: Foreign Portfolio Investor.

21,143

-18,244

30,906

11,654

-28,921

33,981

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Sep-18

Mar-19

FP

I F

low

s (

In I

NR

Crs.)

FPI Equity Flows (INR Crs)

Key Features

The investment strategy, approach and the structure of the portfolio herein involves risk and there can be no assurance that specific objectives will be met under differing market conditions or cycles.

The investment strategy and the composition of the portfolio as stated herein is only indicative in nature and is subject to change within the provisions of the disclosure document and client

agreement without any prior notice to investors. Please refer to the disclosure document & client agreement for details and risk factors.

The Satellite will be blend of strategies such as Special Situation,

GARP (Growth at Reasonable Price) Philosophy, thematic etc. This

bucket will be used opportunistically to book profit and increase

weight of Core Portfolio.

Core comprises of approximately 60%-70% of the Portfolio. The

core is predominantly targeted towards sectors which are value on a

relative or absolute basis.

Portfolio Strategy

Satellite

Core

• A focused portfolio of 20-25 stock ideas

• Investment Horizon : 3 Years & Above

• Benchmark Index: S & P BSE 200

• Minimum Investment Amount: Rs. 25,00,000

Data source: MFI Explorer; Calendar Year Absolute Performance.

Can you predict which market-cap segment will outperform?

Flexi cap approach

gives flexibility to

Portfolio manager to

move between the

different segments of

the market.

Why Flexicap Approach?

Calendar Year Nifty Mid Small

Cap 400 Nifty Midcap 50 Nifty 50

2018 -18% -11% 3%

2017 55% 51% 29%

2016 4% 7% 3%

2015 9% 1% -4%

2014 63% 46% 31%

2013 -5% -3% 7%

2012 42% 35% 27%

2011 -33% -40% -25%

2010 18% 10% 18%

2009 112% 100% 76%

2008 -67% -65% -52%

2007 82% 71% 54%

2006 28% 25% 40%

Stock Selection Process:

Portfolio uses blend of Top

Down and Bottom-up

approach.

Top-

Down

Bottom

Up

• Top-down approach: Identify key macroeconomic and sectorial

themes and subsequently help identify stocks.

• Bottom-up approach: Believes that individual companies providing

attractive investment opportunities exist in various industries and

market conditions.

• Prominence among the two would vary from time to time depending

on macroeconomic, sectorial and company specific fundamentals.

• The Core Portfolio predominantly invest to capture underlying

value of the business which gets “unlocked” over a period of time.

• The Satellite Portfolio is tactically managed aiming to take advantage of

market trend.

• Rebalancing: Portfolio aims to systematically increase weightage as

risk reward ratio improves in core portfolio by reducing satellite

portfolio weight.

The investment strategy as stated herein is only indicative in nature and is subject to change within the provisions of the disclosure document and client agreement without any prior notice to

investors. Please refer to the disclosure document & client agreement for details and risk factors.

Investment Strategy

Investment Universe

Broad-based market

cap range.

Investment

Concentration

Diversified across

marketcap and sectors.

Concentrated Portfolio of

20-30 stocks.

Investment Style

Core and Satellite

Approach. Blend of

Value & Growth.

Prominence varies

with microeconomic,

sectoral and

company specific

fundamentals

Benchmark

Agnostic Blend

Flexicap Top Down

+

Bottom

Up

Investment Style

Investment Approach

• ICICI Prudential PMS Flexicap Portfolio currently focuses on large cap quality & counter cyclical bets as compared to Midcaps.

• In periods of huge outperformance of midcaps/smallcaps over large caps, the portfolio looks to tilt its exposure towards high

quality large caps, similarly when midcaps/small caps underperform largecaps, the portfolio would look at increasing the exposure

in midcaps and small caps.

• In cricketing terms, there is a consistent player and there is an aggressive player. We believe, in long run a consistent player

generally may outperform an aggressive player (as measured by his batting average).

The table shown above is for illustration purpose only.

• A consistent player performs according to the different pitch and game conditions, similarly ICICI Prudential PMS Flexicap Portfolio

has outperformed its benchmark at various point of time, as showcased below:

T20 ODI Test

Consistent Performer 31 39 52

Aggressive Performer 22 35 49

Consistent’s performance vs.

Aggressive’s performance 41% 11% 6%

Past performance may or may not be sustained in future. Calendar year return in absolute terms.

2018 2017 2016 2015 2014 2013 2012

ICICI Prudential PMS Flexicap Portfolio -5.93 34.89 7.49 0.58 61.71 13.08 39.43

S&P BSE 200 -0.54 33.26 3.95 -1.48 35.47 4.38 30.98

The portfolio performance mentioned above is of benchmark client and the performance of an individual clients may vary significantly from the above.

How consistency helps in long run

Portfolio is tilted towards Large cap due

to relatively attractive valuations.

Top 10 Holdings

Stocks % to Net Assets

Axis Bank Ltd 7.28

HDFC Bank Ltd 6.55

Cipla Ltd 5.47

State Bank of India 5.28

ICICI Bank Ltd 4.82

Motherson Sumi Systems Ltd 4.64

Infosys Ltd 4.49

Orient Electric Limited 4.39

Bajaj Finserv Ltd 4.16

SBI Life Insurance Company Limited 3.92

Market Capitalization Break-up

The Stock(s)/Sector(s) mentioned in this material do not constitute any recommendation of the same and portfolio may or may not have any future positions in these stock(s)/Sector(s).

Data as on 29th

Mar, 2019.

The data mentioned above is of a benchmark client and data of an individual client may vary significantly from the above.

Current Positioning

Large

cap,

66.2

Mid

cap,

10.3

Small

cap,

23.5

• Bottoming of NPA Cycle.

• Passage of bankruptcy code

Chemicals / APIs Financials

•China’s actions on

environmental front

•Supply demand

mismatch. Positive

for local players

•On long term basis

exporters may

continue to gain in

key segments like

IT, Pharma, Auto

Ancillaries

•Bottoming of NPA

Cycle

•Passage of

bankruptcy code

• Increased

Consumption

•Navin Fluorine

International

•Dishman Carbogen

•Axis Bank

•HDFC Bank

•SBI

• ICICI Bank

•Bajaj Finserv

•Motherson Sumi

Systems Ltd

• Infosys Ltd

•Cipla

Core Strategy Core Strategy Core Strategy

Domestic Consumption

•Demographics

• Improved outlook on

rural

•GST Play

•Orient Electric

• Inox Leisure Ltd

•Blue Star

•Voltas

Satellite Strategy

The Stock(s)/Sector(s) mentioned in this material do not constitute any recommendation of the same and portfolio may or may not have any future positions in these stock(s)/Sector(s). API: Active

Pharmaceuticals Ingredients.

Data as on 29th

Mar, 2019

Bottom-up Ideas

•Special Situations

•Favourable Macro-

economic factors

•Potential market

share gain in

medium term

•Bharti Airtel

Exports Basket

Satellite Strategy

Current Theme

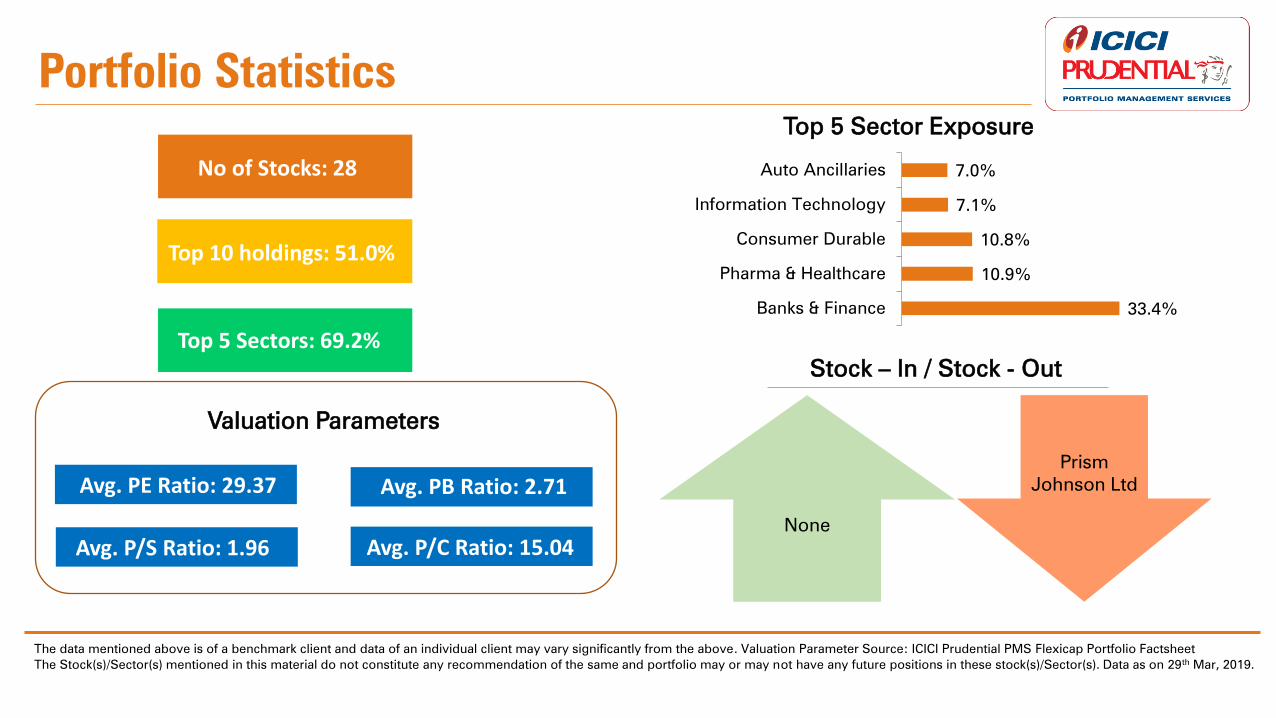

No of Stocks: 28

Top 5 Sectors: 69.2%

Top 10 holdings: 51.0%

Avg. PE Ratio: 29.37 Avg. PB Ratio: 2.71

Valuation Parameters

Avg. P/S Ratio: 1.96 Avg. P/C Ratio: 15.04

Top 5 Sector Exposure

Stock – In / Stock - Out

None

Prism

Johnson Ltd

The Stock(s)/Sector(s) mentioned in this material do not constitute any recommendation of the same and portfolio may or may not have any future positions in these stock(s)/Sector(s). Data as on 29th

Mar, 2019.

The data mentioned above is of a benchmark client and data of an individual client may vary significantly from the above. Valuation Parameter Source: ICICI Prudential PMS Flexicap Portfolio Factsheet

Portfolio Statistics

33.4%

10.9%

10.8%

7.1%

7.0%

Banks & Finance

Pharma & Healthcare

Consumer Durable

Information Technology

Auto Ancillaries

-

5,00,00,000

10,00,00,000

15,00,00,000

20,00,00,000

25,00,00,000

30,00,00,000

ICICI Prudential PMS Flexicap Portfolio S&P BSE 200

Dot-Com

Bubble

Fall of

NDA-I

Govt

LME Price

Crashed. Increase

in US Fed Rates Bull Phase

Global

Financial

Crisis

European

Debt Crises

Rupee

Depreciation

Rally Pre and Post

Union Election

Value rebased to INR 10,000,000.

Data as on 29th

Mar, 2019. Past performance may or may not be sustained in future. The return mentioned above is the return of the oldest client of the portfolio. Further, the portfolio value is re-based

as and when applicable. The portfolio performance mentioned above is of benchmark client and the performance of an individual clients may vary significantly from the above

Growth of Rs.1,00,00,000/-

25,54,21,304

11,49,63,690

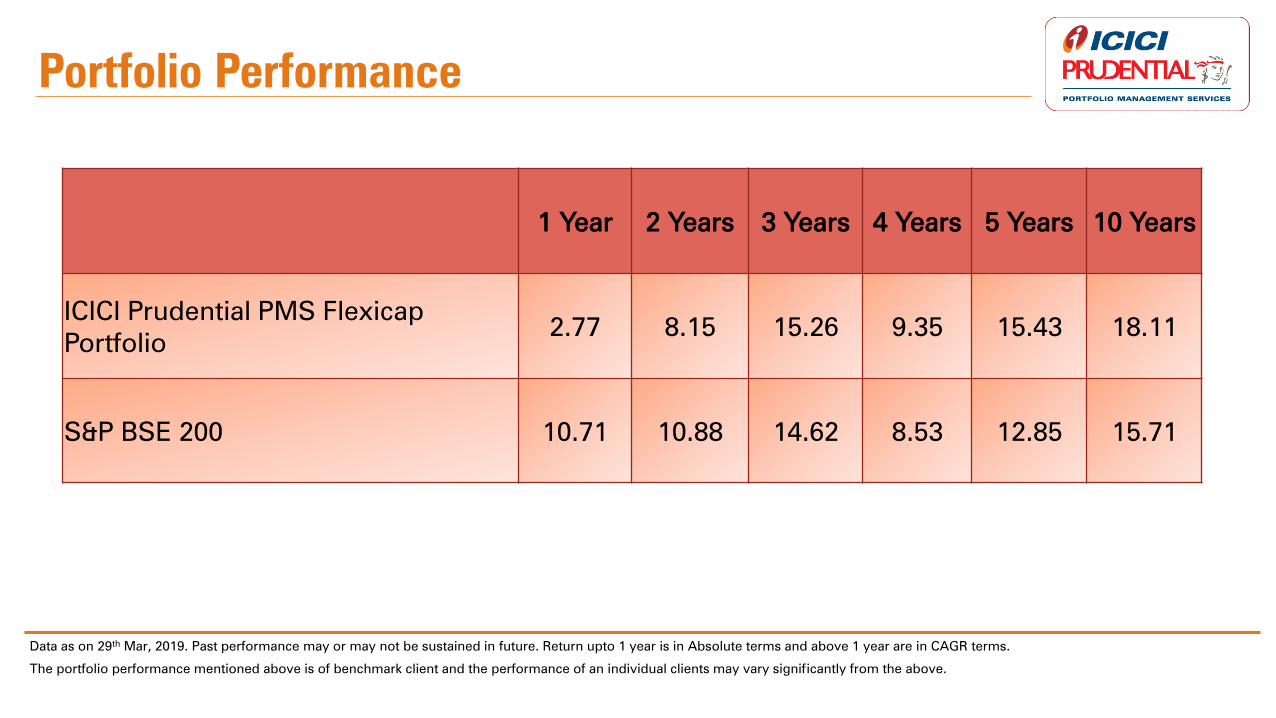

19 Years of Track Record

Data as on 29th

Mar, 2019. Past performance may or may not be sustained in future. Return upto 1 year is in Absolute terms and above 1 year are in CAGR terms.

1 Year 2 Years 3 Years 4 Years 5 Years 10 Years

ICICI Prudential PMS Flexicap

Portfolio 2.77 8.15 15.26 9.35 15.43 18.11

S&P BSE 200 10.71 10.88 14.62 8.53 12.85 15.71

The portfolio performance mentioned above is of benchmark client and the performance of an individual clients may vary significantly from the above.

Portfolio Performance

An Irrational

Market

Sentiment

Investing in securities involves certain risks and considerations associated generally with making investments in securities. The value of the portfolio investments may be affected

generally by factors affecting financial markets, such as price and volume, volatility in interest rates, currency exchange rates, changes in regulatory and administrative policies of the

Government or any other appropriate authority (including tax laws) or other political and economic developments. Consequently, there can be no assurance that the objective of the

Portfolio would be achieved. The value of the portfolios may fluctuate and can go up or down. The Stock(s)/Sector(s) mentioned in this material do not constitute any

recommendation of the same and the portfolios may or may not have any future positions in these Stock(s)/Sector(s).

The composition of the portfolio is subject to changes within the provisions of the disclosure document. The benchmark of the portfolios can be changed from time to time in the

future. The inability of the Portfolio Manager to make intended securities purchases due to settlement problems could cause the portfolio to miss certain investment opportunities. By

the same rationale, the inability to sell securities held in the portfolio due to the absence of a well-developed and liquid secondary market for securities would result, at times, in

potential losses to the portfolio. Please note that past performance of the financial products, instruments and the portfolio does not necessarily indicate the future prospects and

performance thereof. Such past performance may or may not be sustained in future. Portfolio Manager’s investment decisions may not be always profitable, as actual market

movements may be at variance with anticipated trends. The investors are not being offered any guaranteed or assured returns. The AMC may be engaged in buying/selling of such

securities. Please refer to the Disclosure Document and Client Agreement for portfolio specific risk factors.

Individual returns of Clients for a particular portfolio type may vary significantly from the data on performance of the portfolios as may be depicted by the Portfolio Manager from

time to time. This is due to factors such as timing of entry and exit, timing of additional flows and redemptions, individual client mandates, specific portfolio construction

characteristics or structural parameters, which may have a bearing on individual portfolio performance. No claims may be made or entertained for any variances between the

performance depictions and individual portfolio performance. Neither ICICI Prudential Asset Management Company Ltd. (the AMC) nor its Directors, Employees or Sponsors shall be

in any way liable for any variations noticed in the returns of individual portfolios.

The Client shall not make any claim against the Portfolio Manager against any losses (notional or real) or against any loss of opportunity for gain under various PMS Products, on

account of or arising out of such circumstance/ change in market condition or for any other reason which may specifically affect a particular sector or security.]

Risk Factors & Disclaimers

An Irrational

Market

Sentiment

The Portfolio Manager shall have the sole and absolute discretion to invest in respect of the Client’s investment in any type of security subject to the Agreement and as stated in the

Disclosure Document and make such changes in the investments and invest some or all of the Client’s investment amount in such manner and in such markets as it deems fit would

benefit the Client. The Portfolio Manager’s decision (taken in good faith) in deployment of the Clients’ account is absolute and final and can never be called in question or be open to

review at any time during the currency of the agreement or any time thereafter except on the ground of malafide, fraud, conflict of interest or gross negligence. This right of the

Portfolio Manager shall be exercised strictly in accordance with the relevant Acts, rules and regulations, guidelines and notifications in force from time to time.

By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses

could materially differ from those that have been estimated. The recipient(s) alone shall be fully responsible/are liable for any decision taken on the basis of this material. All recipients

of this material should before dealing and/or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice. The

investments discussed in this may not be suitable for all investors. Financial products and instruments are subject to market risks and yields may fluctuate depending on various

factors affecting capital/debt markets. There is no assurance or guarantee that the objectives of the portfolio will be achieved. Please note that past performance of the financial

products, instruments and the portfolio does not necessarily indicate the future prospects and performance thereof. Such past performance may or may not be sustained in future.

Portfolio Manager’s investment decisions may not be always profitable, as actual market movements may be at variance with anticipated trends. The investors are not being offered

any guaranteed or assured returns.

In the preparation of this material the AMC has used information that is publicly available, including information developed in-house. Some of the material used herein may have

been obtained from members/persons other than the AMC and/or its affiliates and which may have been made available to the AMC and/or to its affiliates. Information gathered and

material used herein is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and/or completeness of any information. For data

reference to any third party in this material no such party will assume any liability for the same. We have included statements/opinions/recommendations in this material, which

contain words, or phrases such as “will”, “expect”, “should”, “believe” and also PE ratios, EPS and Earnings Growth for forthcoming years and similar expressions or variations of

such expressions, that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties

associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, the

monitory and interest policies of India, inflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices, the performance of the financial markets in India and

globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry.

All data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. The Portfolio Manager/ the AMC

takes no responsibility of updating any data/information in this material from time to time. The Portfolio Manager/ the AMC (including its affiliates), and any of its officers directors,

personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, exemplary, consequential, as also any loss of profit

in any way arising from the use of this material in any manner

Risk Factors & Disclaimers

Thank You