Embed Size (px)

DESCRIPTION

Presentation to the Productivity Hub in December 2013 by Ron Crawford, of work contributing to the inquiry boosting productivity in the services sector. For more information see www.productivity.govt.nz

Citation preview

Boosting productivity in the services sectorICT and productivity in the retail & wholesale industries

December 2013

Outline

• ICT has enabled a revolution in retail and wholesale

• Walmart & the US retail and wholesale shake-out

• Europe & the UK trailed the US – why?

• NZ retail and wholesale compared to Australia

• NZ retail and wholesale developments

• NZ barriers?

ICT in retail and wholesale industries

• 100s of millions of retail transactions per day in US alone

• ICT allows:

– Real-time tracking of inventories & supply– International integration of supply chains– Data analysis to improve purchasing, pricing and promotion– Automating in-store processes

• Store and firm level economies of scale

• Complementary investments

The US retail story is a Walmart story

• Contribution to labour productivity growth in US general merchandise

• Prices 10% lower than competitors

• Early adopter of ICT

• Expansion strategy

• Scale, cost and technology interactions.

• 4,000 stores and 1.3 million employees in the US

• 15% of consumer good imports from China (2007)

• 6.5% of US retail sales (2004)

Retail chains & market dynamics

• Retail contributes 11% of aggregate US LP growth 1993 – 2000

• 95% of labour productivity (LP) growth in US retail due to entry of more productive and exit of less productive stores 1987-1997

• Firm size increased, numbers of single-store firms fell

• Learning and vintage effects

• Massive reallocation of labour and capital

• Similar dynamics in Canada

Europe & the UK lag the US

• Europe & UK retail labour productivity levels lower than the US

• Slower adoption of new technologies due to:

Later transport deregulation (Europe)

Smaller markets (geography, culture, language, border effects)

More restrictive labour market regulation (Europe)

Restrictive land-use regulation (e.g. UK, Denmark)

“Americans do IT better” - People management practices

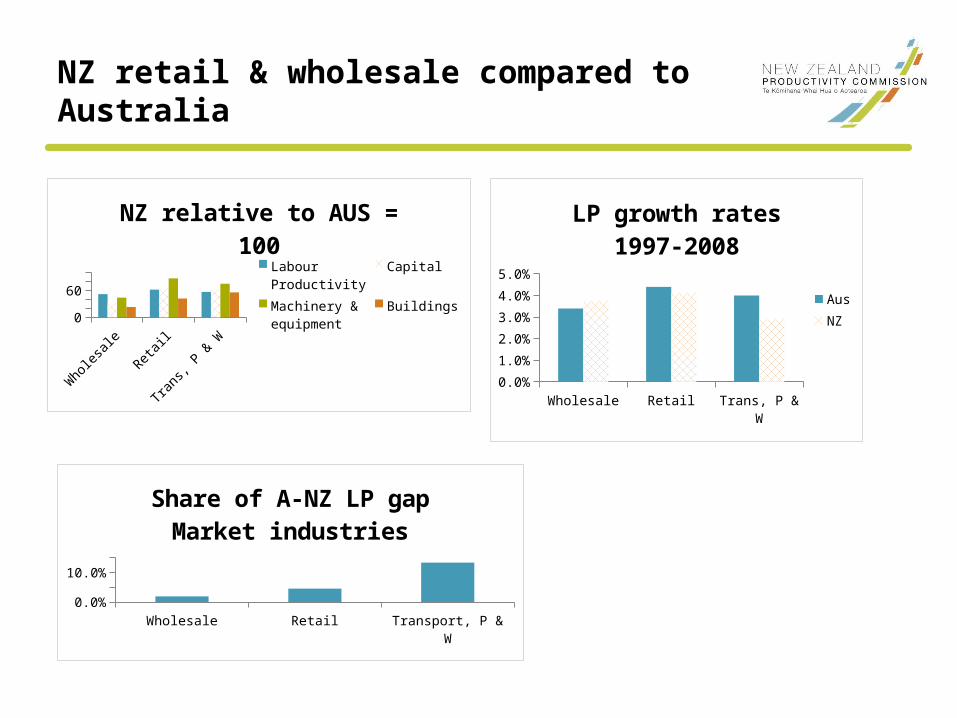

NZ retail & wholesale compared to Australia

Wholesale Retail Trans, P & W0

102030405060708090

100

NZ relative to AUS = 100

Labour ProductivityCapitalMachinery & equipmentBuildings

Wholesale Retail Trans, P & W0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%5.0%

LP growth rates 1997-2008

AusNZ

Wholesale Retail Transport, P & W0.0%

4.0%

8.0%

12.0%

Share of A-NZ LP gapMarket industries

New Zealand developments• Rise of The Warehouse

• Role of Australian chains (e.g. Woolworths, Bunnings)

• Rise of malls (e.g. Sylvia Park)

• Costco, IKEA absent

• Rise of online shopping

• Retail store and firm size growing(1997-2012)

• Wholesale store and firm size growing (2000s)

Industry share of aggregate NZ LP growth & GDP 1996-2011(average aggregate annual LP growth = 1.4%)

Wholesale Retail Trans, P & W0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

LP growthGDP

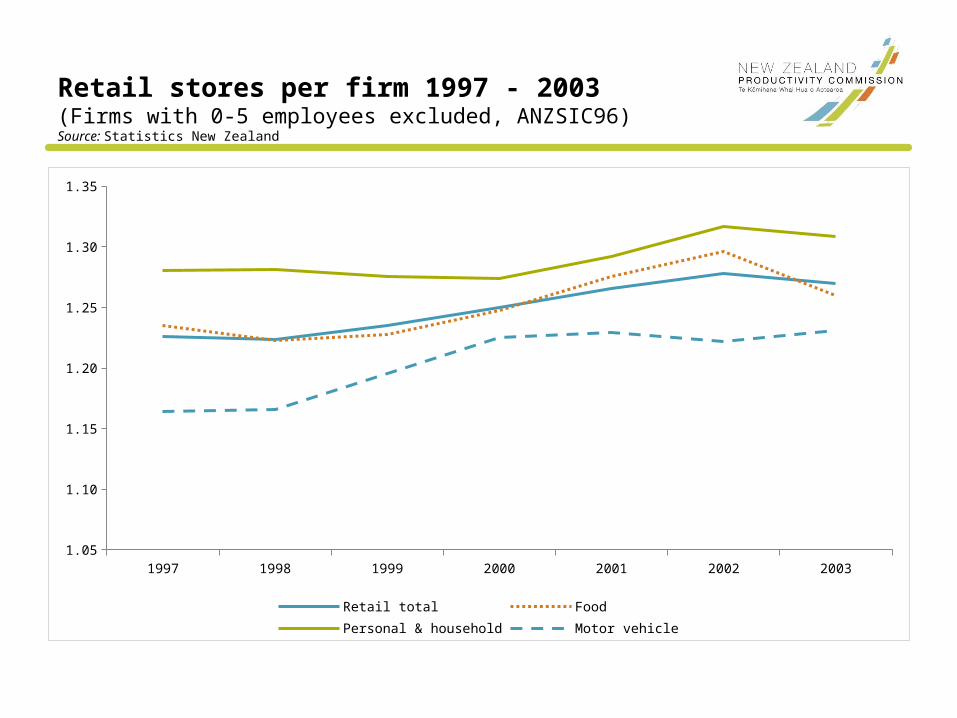

Retail stores per firm 1997 - 2003(Firms with 0-5 employees excluded, ANZSIC96)Source: Statistics New Zealand

1997 1998 1999 2000 2001 2002 20031.05

1.10

1.15

1.20

1.25

1.30

1.35

Retail total Food Personal & household Motor vehicle

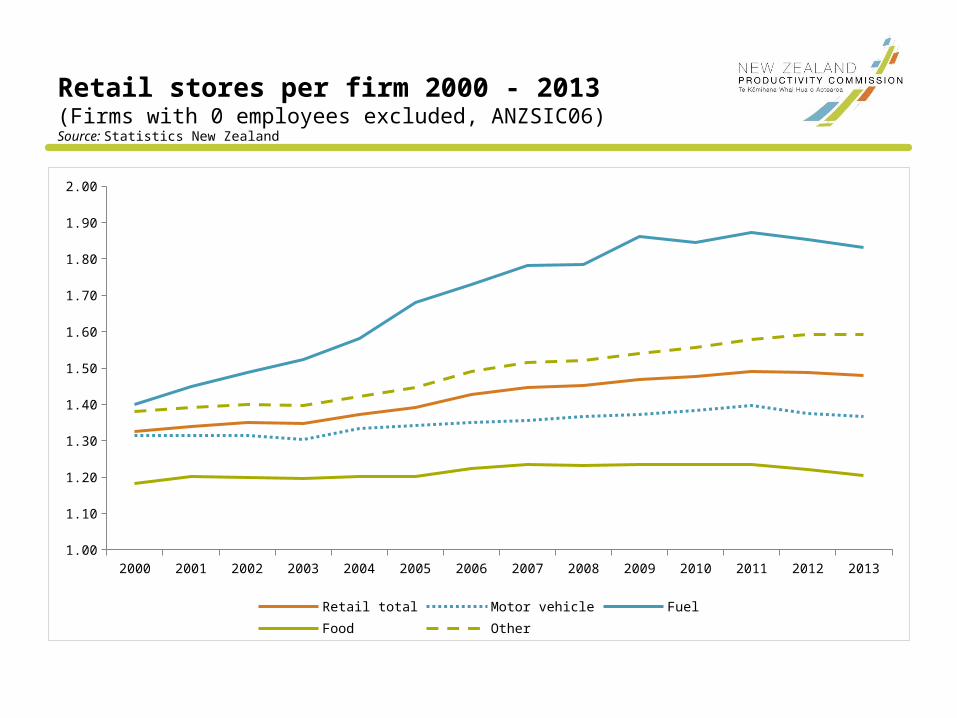

Retail stores per firm 2000 - 2013(Firms with 0 employees excluded, ANZSIC06)Source: Statistics New Zealand

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20131.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

Retail total Motor vehicle Fuel Food Other

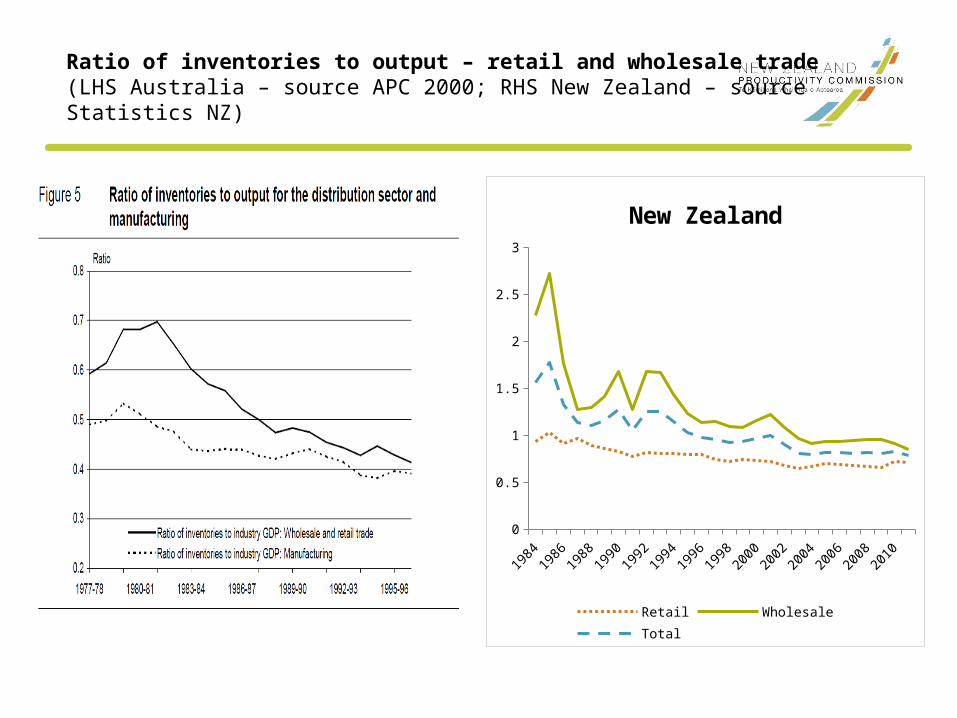

Ratio of inventories to output – retail and wholesale trade(LHS Australia – source APC 2000; RHS New Zealand – source Statistics NZ)

19841986

19881990

19921994

19961998

20002002

20042006

20082010

0

0.5

1

1.5

2

2.5

3

New Zealand

Retail Wholesale Total

Barriers to ICT in NZ retail & wholesale?

• Market scale

• Less intense competition

• Internal geography and infrastructure – effects on distribution networks

• Land-use regulation (e.g. IKEA experience)

• Entry barriers – eg to FDI?

• Labour market regulation – NZ relatively flexible