Embed Size (px)

DESCRIPTION

AEHYGWSHY

Citation preview

IFRS-Based Financial Reporting

Putu Agus ArdianaFaculty of Economics and Business

Udayana University, Indonesia

Agenda

• What is IFRS?• The Use of IFRS• Who Develops IFRS?• IFRS Adoption and Convergence in Selected Countries

(Indonesia, UK, USA)• Objective of Financial Reporting• Revenue• Expense• Assets• Liability• Equity

What is IFRS?

• International Financial Reporting Standards (IFRS) is a single set of accounting standards, developed and maintained by the IASB with the intention of those standards being capable of being applied on a globally consistent basis—by developed, emerging and developing economies—thus providing investors and other users of financial statements with the ability to compare the financial performance of publicly listed companies on a like-for-like basis with their international peers.

The Use of IFRS

• IFRS is now mandated for use by more than 100 countries, including the European Union and by more than two-thirds of the G20

• The G20 and other international organisations have consistently supported the work of the IASB and its mission of global accounting standards.

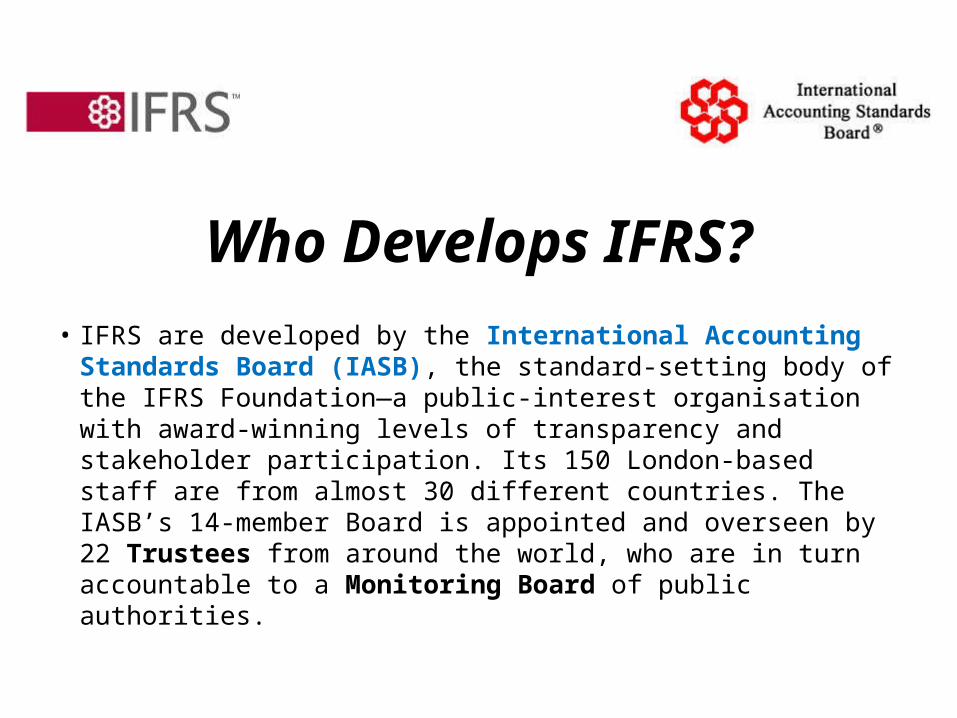

Who Develops IFRS?• IFRS are developed by the International Accounting

Standards Board (IASB), the standard-setting body of the IFRS Foundation—a public-interest organisation with award-winning levels of transparency and stakeholder participation. Its 150 London-based staff are from almost 30 different countries. The IASB’s 14-member Board is appointed and overseen by 22 Trustees from around the world, who are in turn accountable to a Monitoring Board of public authorities.

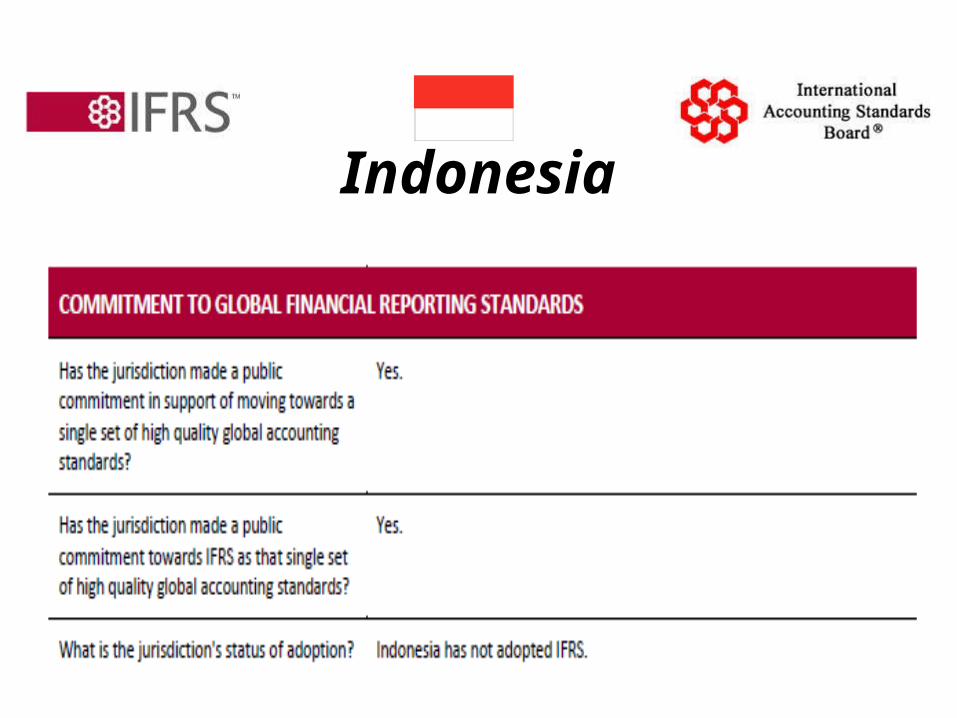

Indonesia

Indonesia

Indonesia

Indonesia

Indonesia

Indonesia

Indonesia

Indonesia

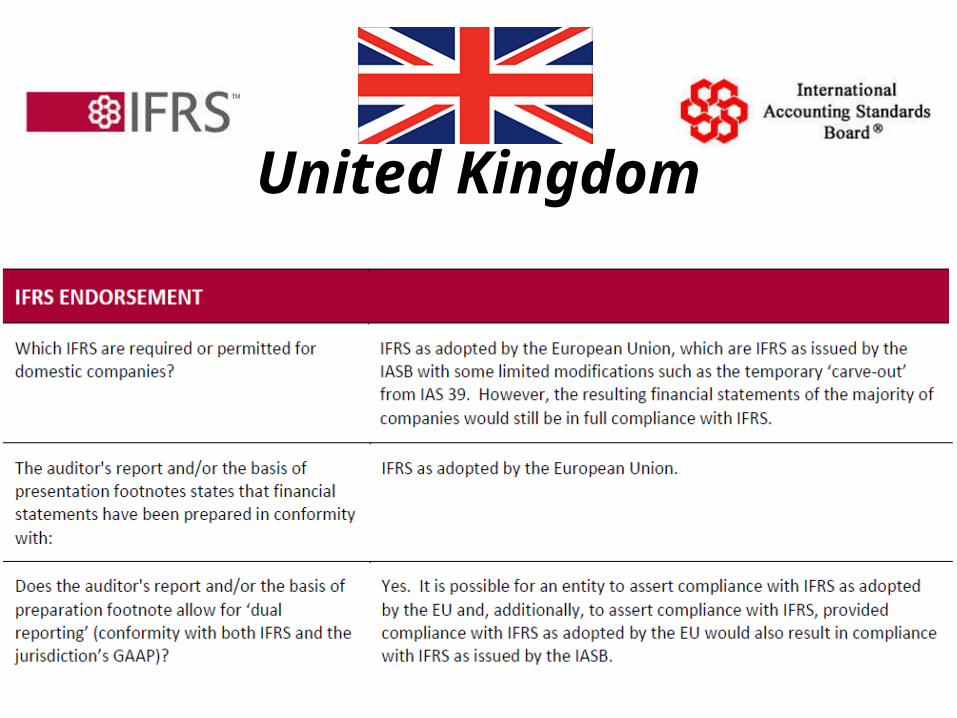

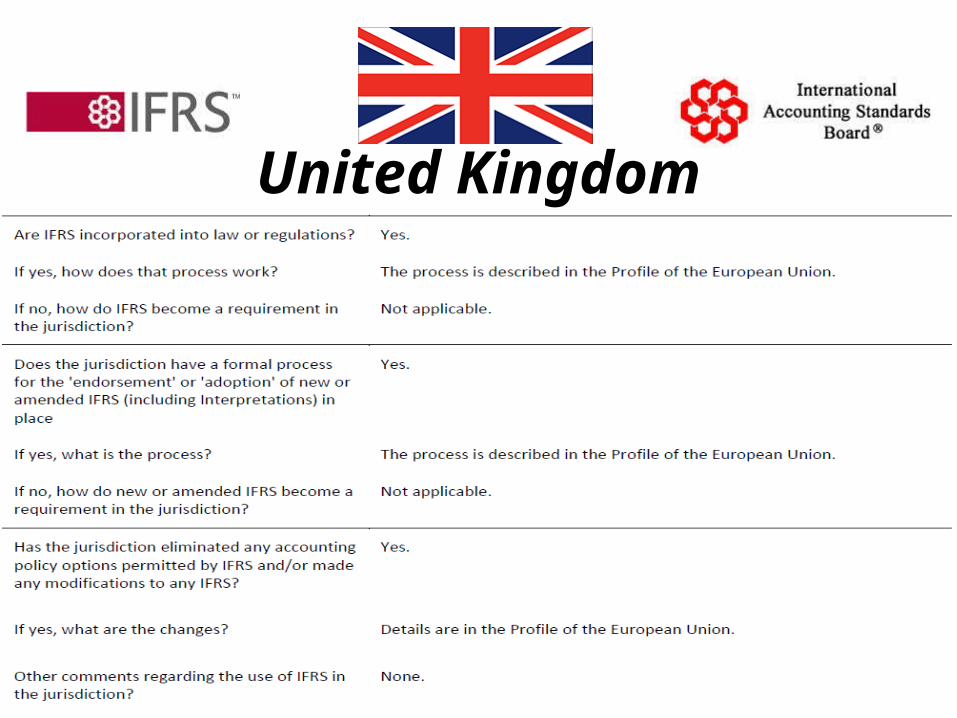

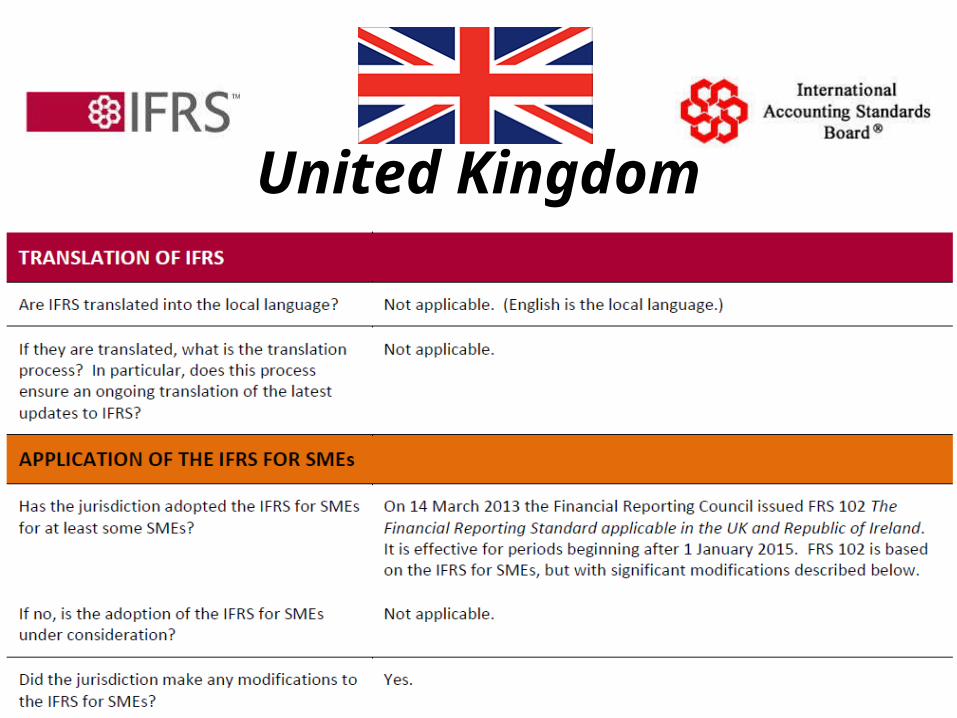

United Kingdom

United Kingdom

United Kingdom

United Kingdom

United Kingdom

United Kingdom

United Kingdom

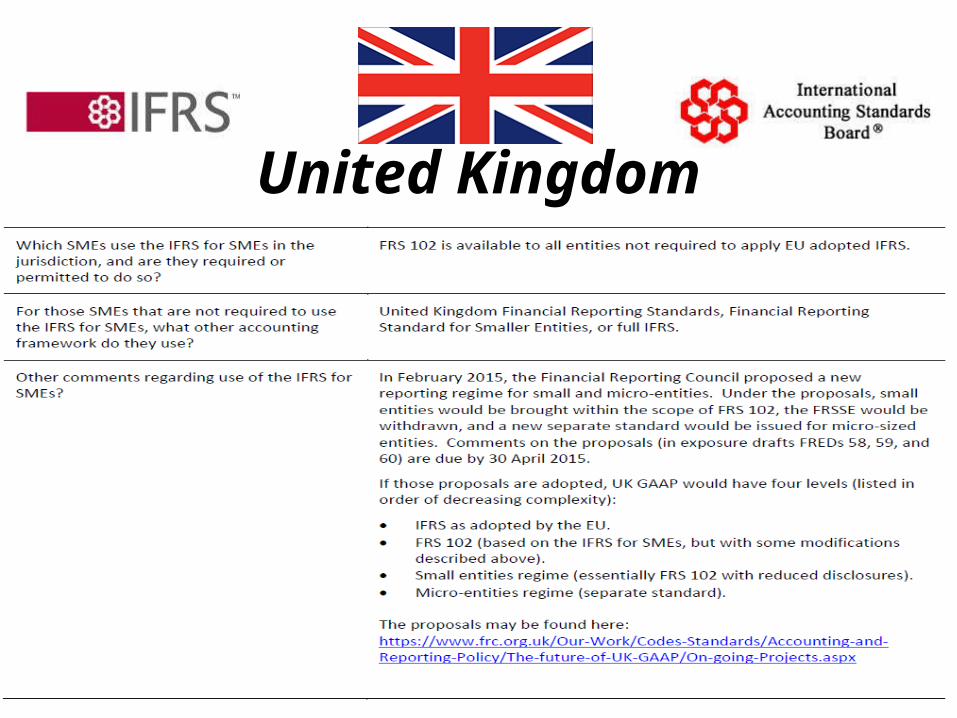

United Kingdom

United Kingdom

United Kingdom

United Kingdom

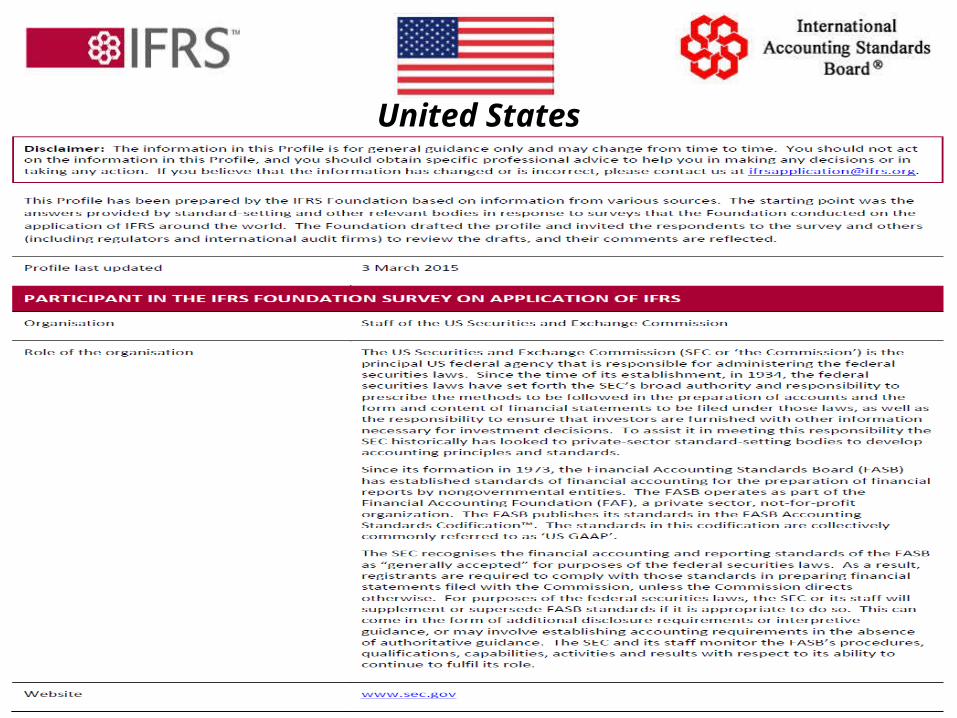

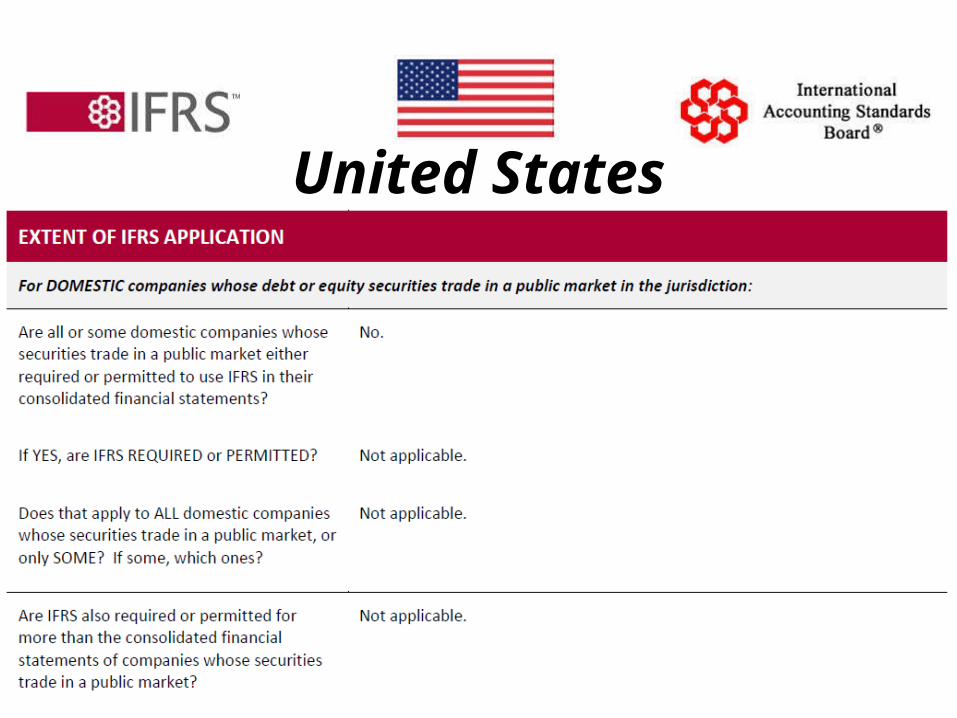

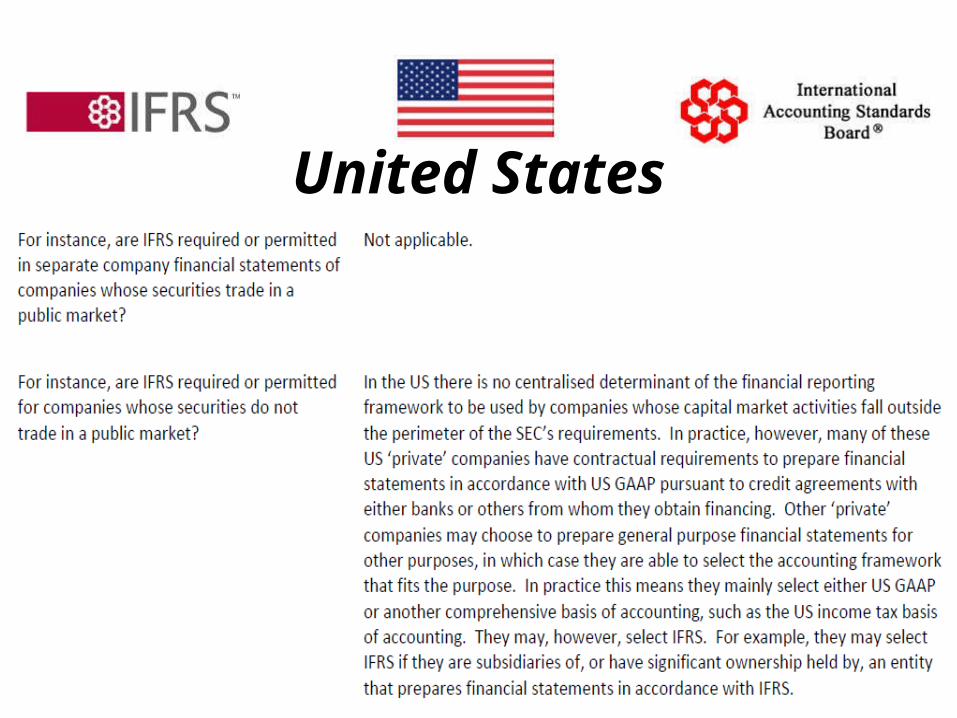

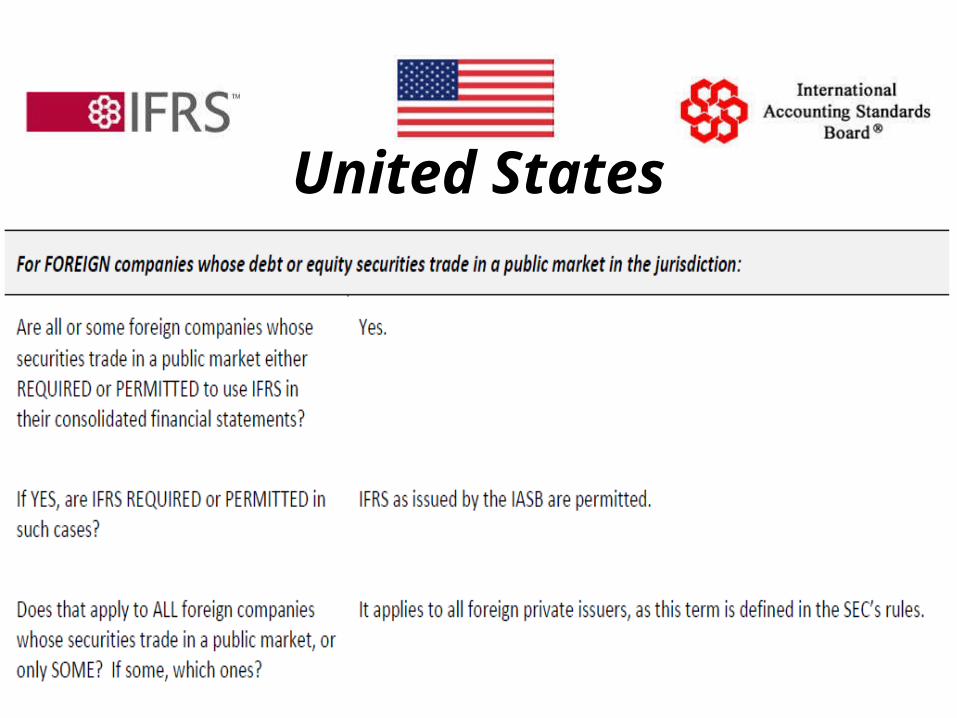

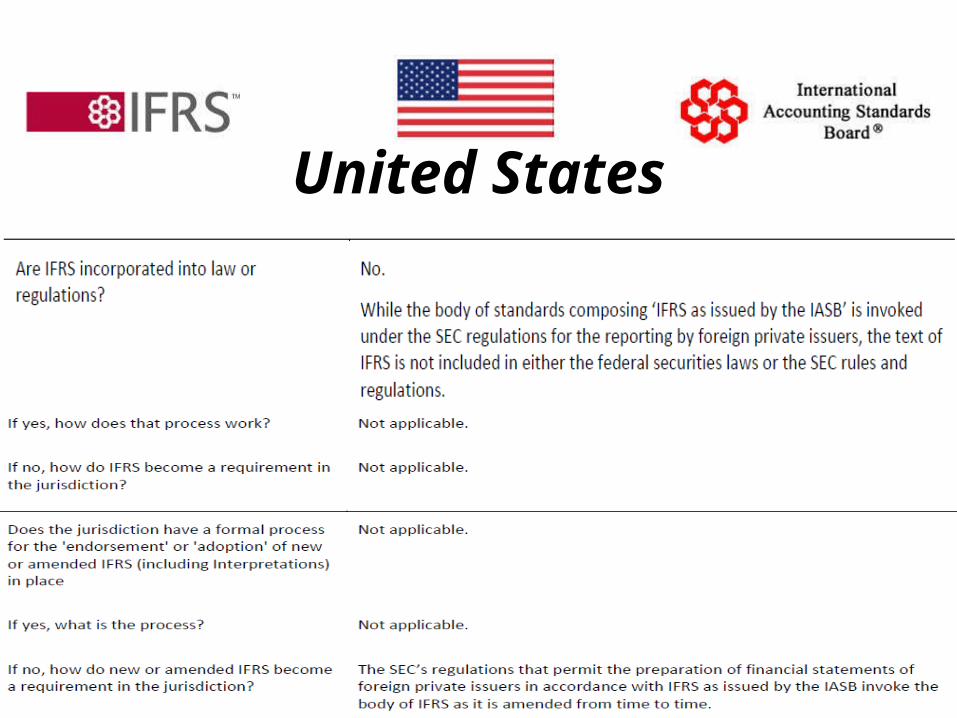

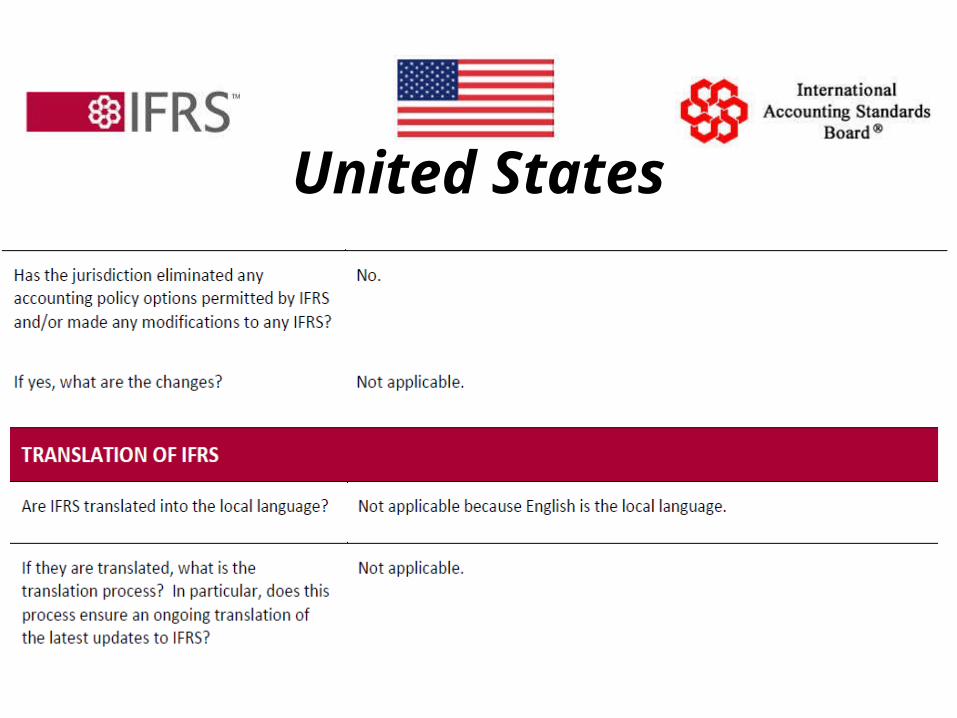

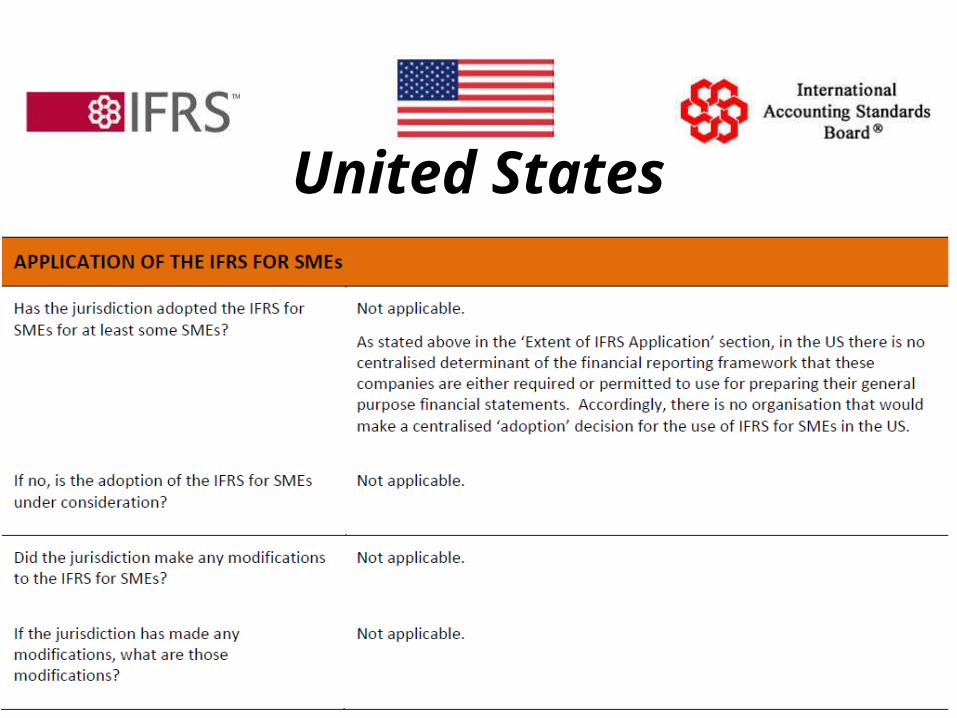

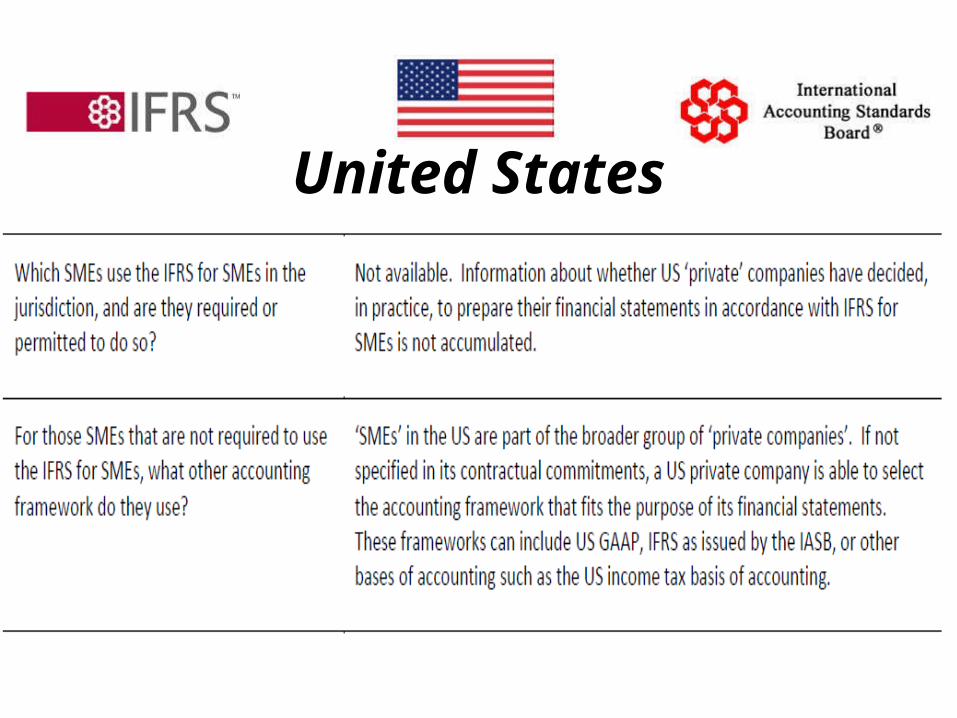

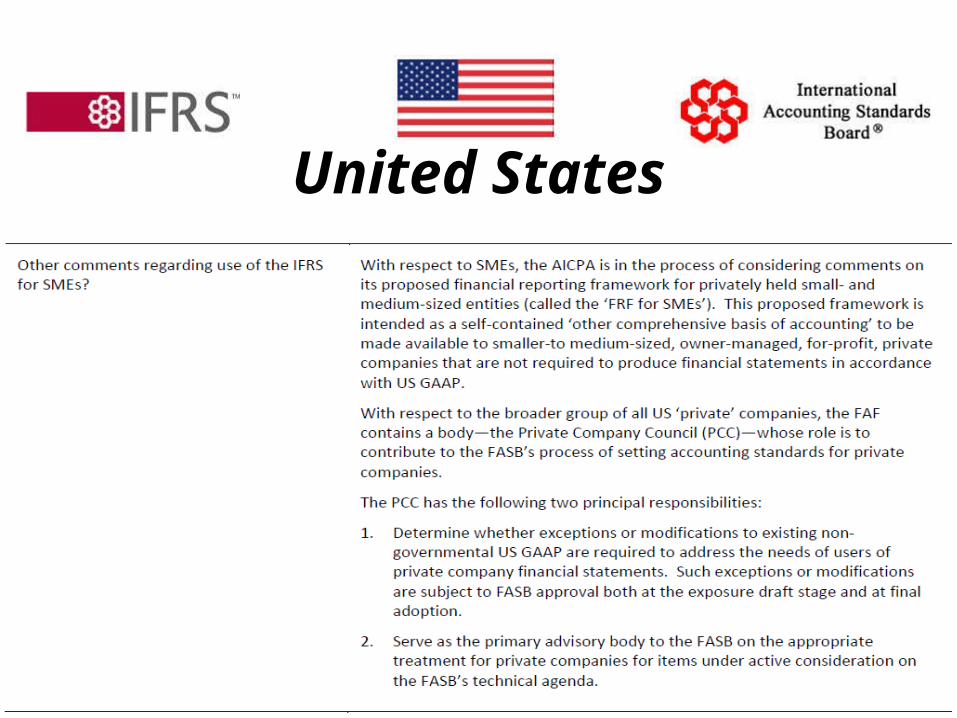

United States

United States

United States

United States

United States

United States

United States

United States

United States

United States

United States

United States

United States

• to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in making decisions in their capacity as capital providers

Objective of Financial Reporting

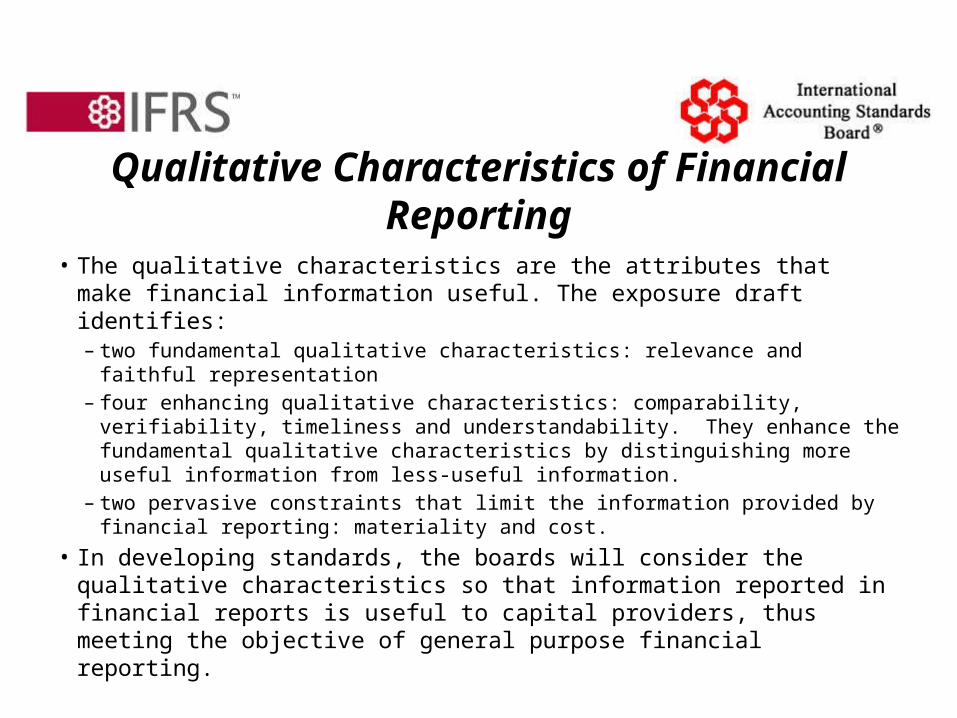

• The qualitative characteristics are the attributes that make financial information useful. The exposure draft identifies:– two fundamental qualitative characteristics: relevance and faithful

representation – four enhancing qualitative characteristics: comparability, verifiability,

timeliness and understandability. They enhance the fundamental qualitative characteristics by distinguishing more useful information from less-useful information.

– two pervasive constraints that limit the information provided by financial reporting: materiality and cost.

• In developing standards, the boards will consider the qualitative characteristics so that information reported in financial reports is useful to capital providers, thus meeting the objective of general purpose financial reporting.

Qualitative Characteristics of Financial Reporting

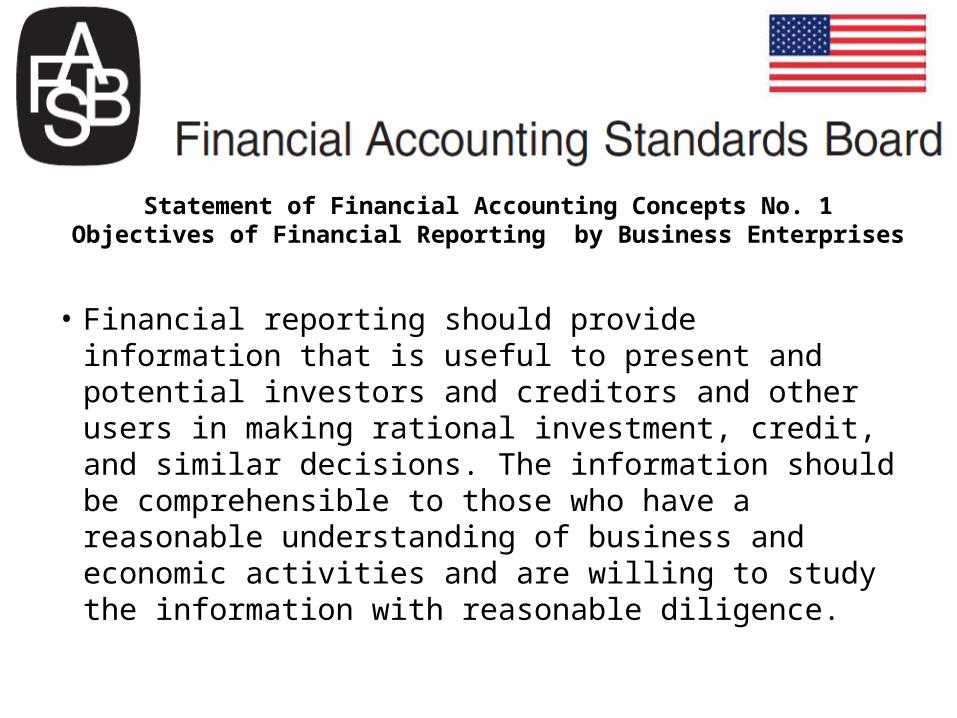

• Financial reporting should provide information that is useful to present and potential investors and creditors and other users in making rational investment, credit, and similar decisions. The information should be comprehensible to those who have a reasonable understanding of business and economic activities and are willing to study the information with reasonable diligence.

Statement of Financial Accounting Concepts No. 1Objectives of Financial Reporting by Business Enterprises

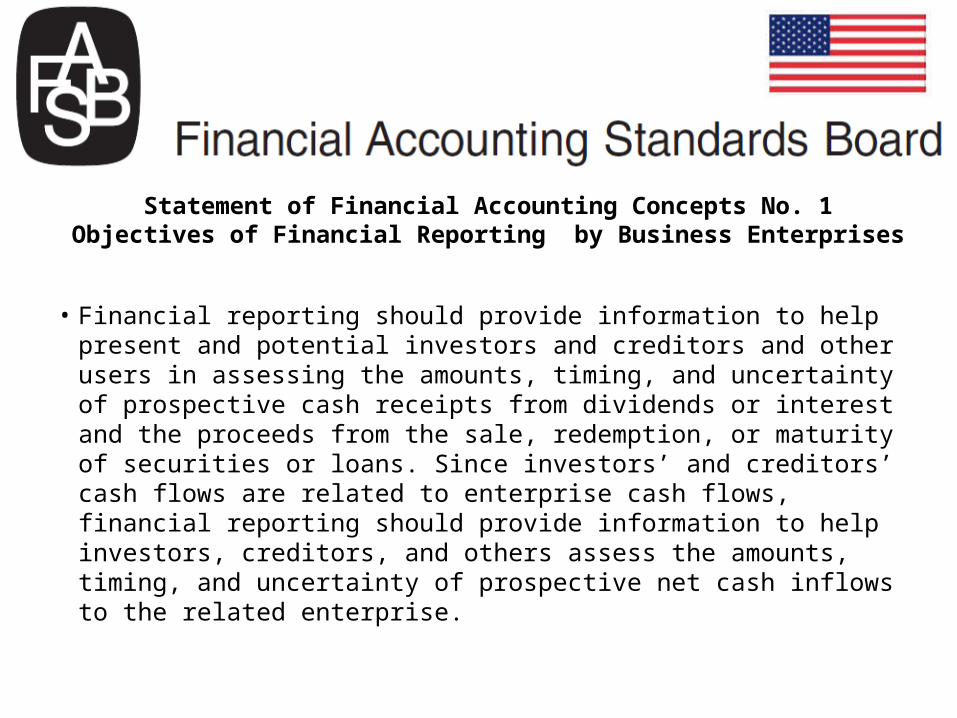

• Financial reporting should provide information to help present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts from dividends or interest and the proceeds from the sale, redemption, or maturity of securities or loans. Since investors’ and creditors’ cash flows are related to enterprise cash flows, financial reporting should provide information to help investors, creditors, and others assess the amounts, timing, and uncertainty of prospective net cash inflows to the related enterprise.

Statement of Financial Accounting Concepts No. 1Objectives of Financial Reporting by Business Enterprises

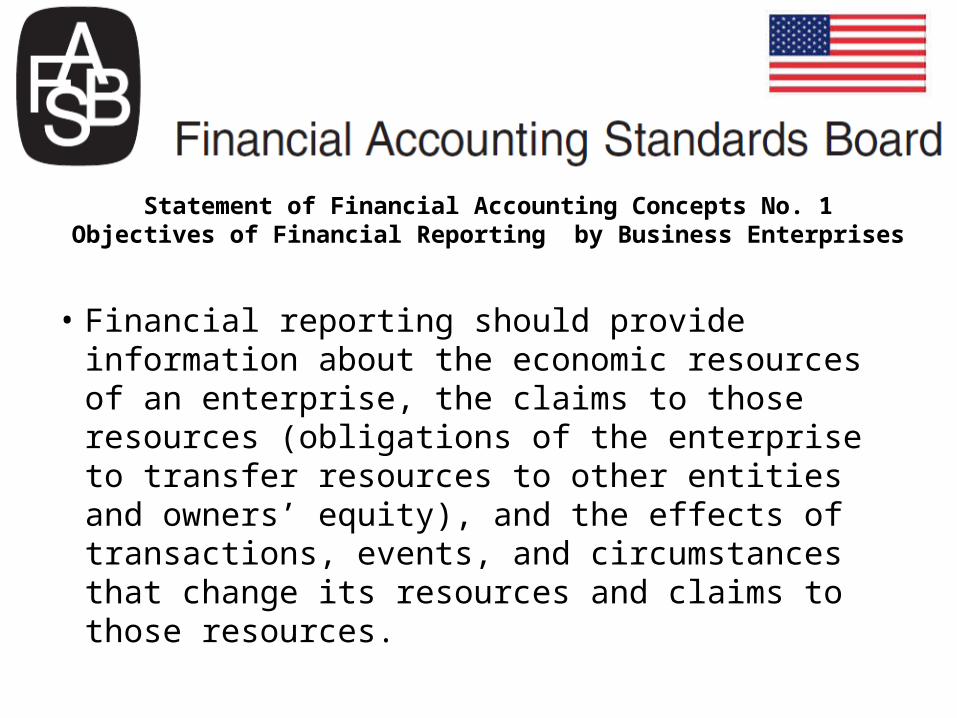

• Financial reporting should provide information about the economic resources of an enterprise, the claims to those resources (obligations of the enterprise to transfer resources to other entities and owners’ equity), and the effects of transactions, events, and circumstances that change its resources and claims to those resources.

Statement of Financial Accounting Concepts No. 1Objectives of Financial Reporting by Business Enterprises

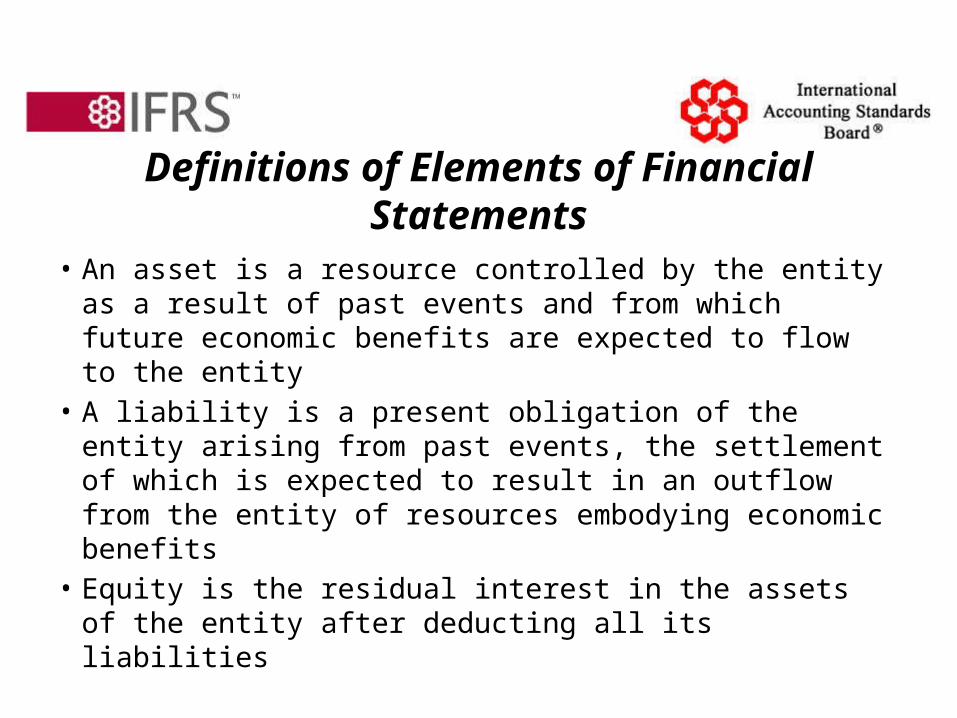

• An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity

• A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits

• Equity is the residual interest in the assets of the entity after deducting all its liabilities

Definitions of Elements of Financial Statements

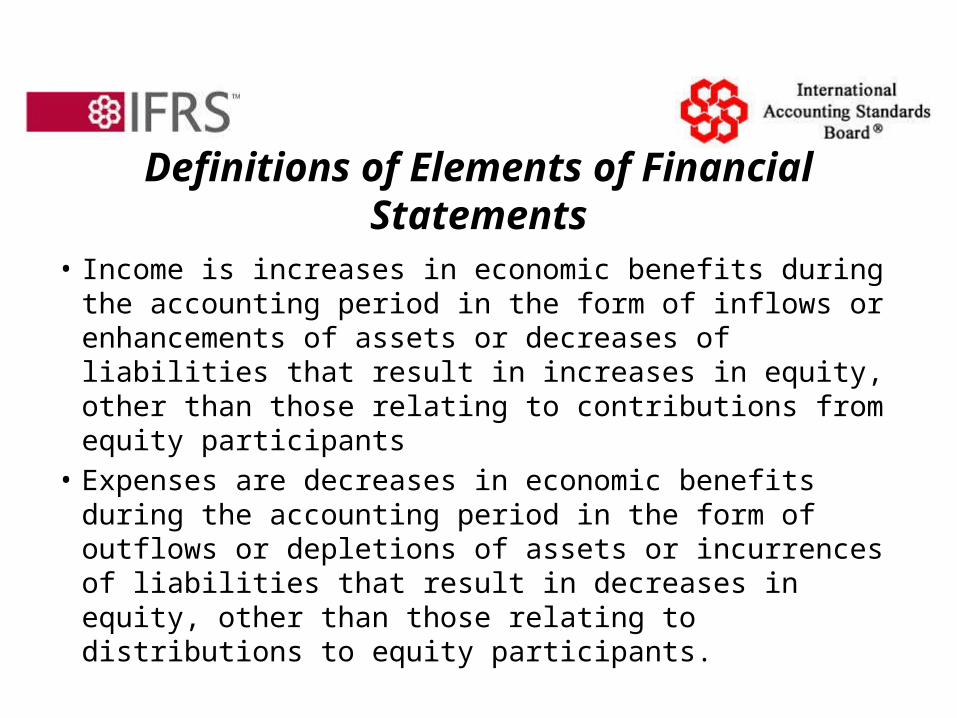

• Income is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants

• Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those relating to distributions to equity participants.

Definitions of Elements of Financial Statements

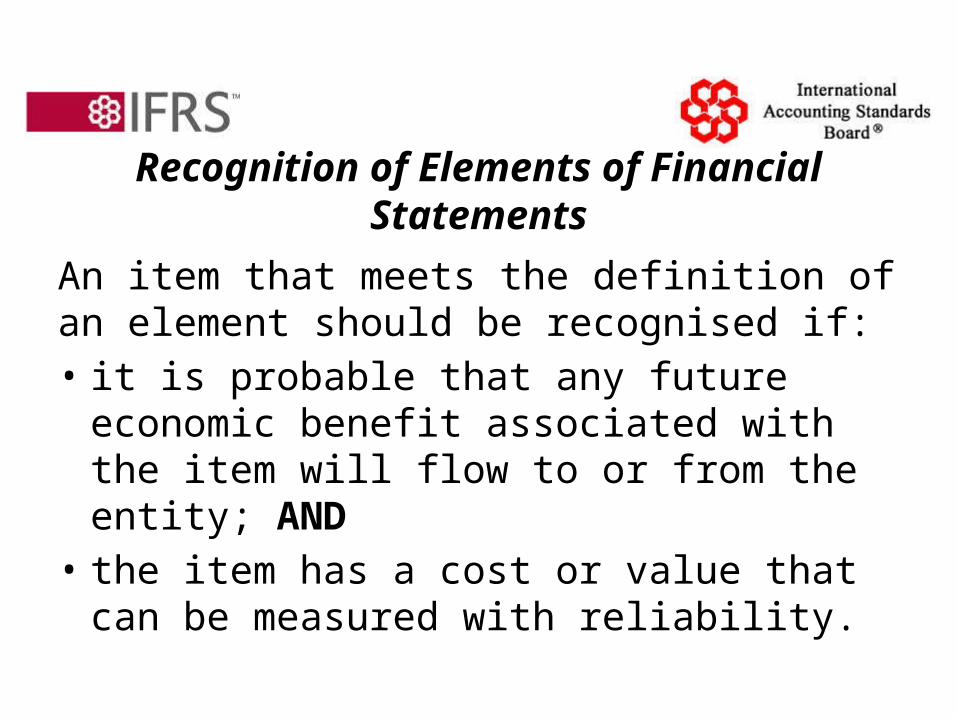

An item that meets the definition of an element should be recognised if:• it is probable that any future economic benefit

associated with the item will flow to or from the entity; AND

• the item has a cost or value that can be measured with reliability.

Recognition of Elements of Financial Statements

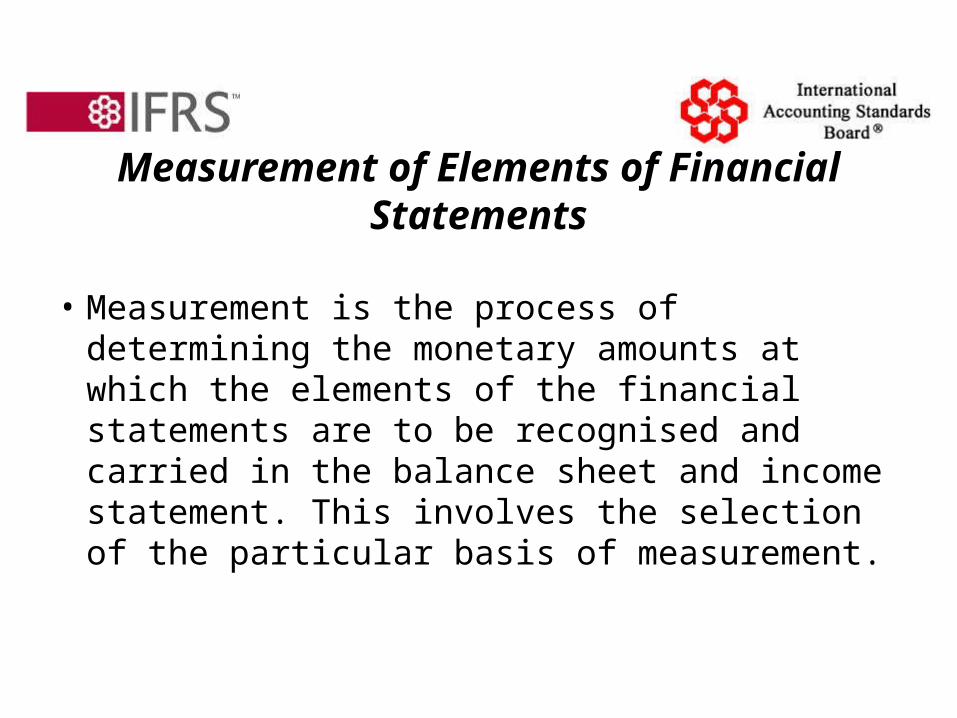

• Measurement is the process of determining the monetary amounts at which the elements of the financial statements are to be recognised and carried in the balance sheet and income statement. This involves the selection of the particular basis of measurement.

Measurement of Elements of Financial Statements

End of Presentation