Embed Size (px)

Citation preview

1. Introduction and outlineIt is a distinct pleasure to deliver the 2005 PDLeake Lecture, and I sincerely thank the Instituteof Chartered Accountants in England and Wales(ICAEW) for inviting me to do so. PD Leake wasan early contributor to a then fledgling but nowmature accounting literature. His work on good-will (Leake, 1921a,b) stands apart from its con-temporaries, so it is an honour to celebrate thecontributions of such a pioneer. My introduction toLeake’s work came from a review article(Carsberg, 1966) that I read almost 40 years ago.Ironically, the review was published in a journal Inow co-edit (Journal of Accounting Research),and was written by a man who later became a pio-neer in what now are known as InternationalFinancial Reporting Standards (the subject of thislecture), and with whom I once co-taught a courseon International Accounting (here in London, atLondon Business School). It truly is a small worldin many ways – which goes a long way to explain-ing the current interest in international standards.

International Financial Reporting Standards(IFRS) are forefront on the immediate agenda be-cause, starting in 2005, listed companies inEuropean Union countries are required to reportconsolidated financial statements prepared accord-ing to IFRS. At the time of speaking, companiesare preparing for the release of their first full-yearIFRS-compliant financial statements. Investorshave seen interim reports based on IFRS, but havenot yet experienced the full gamut of year-end ad-justments that IFRS might trigger. Consequently,the advantages and disadvantages of IFRS for in-vestors (the specific topic of this lecture) are amatter of current conjecture. I shall try to shedsome light on the topic but, as the saying goes,only time will tell.

1.1. OutlineI begin with a description of IFRS and their his-

tory, and warn that there is little settled theory orevidence on which to build an assessment of theadvantages and disadvantages of uniform account-ing rules within a country, let alone international-ly. The pros and cons of IFRS therefore aresomewhat conjectural, the unbridled enthusiasm ofallegedly altruistic proponents notwithstanding. Ithen outline my broad framework for addressingthe issues, which is economic and political.

On the ‘pro’ side of the ledger, I conclude thatextraordinary success has been achieved in devel-oping a comprehensive set of ‘high quality’ stan-dards and in persuading almost 100 countries toadopt them. On the ‘con’ side, a deep concern isthat the differences in financial reporting quality

Accounting and Business Research, International Accounting Policy Forum. pp. 5-27. 2006 5

International Financial Reporting Standards(IFRS): pros and cons for investorsRay Ball*

Abstract—Accounting in shaped by economic and political forces. It follows that increased worldwide integrationof both markets and politics (driven by reductions in communications and information processing costs) makes in-creased integration of financial reporting standards and practice almost inevitable. But most market and politicalforces will remain local for the foreseeable future, so it is unclear how much convergence in actual financial re-porting practice will (or should) occur. Furthermore, there is little settled theory or evidence on which to build anassessment of the advantages and disadvantages of uniform accounting rules within a country, let alone interna-tionally. The pros and cons of IFRS therefore are somewhat conjectural, the unbridled enthusiasm of allegedly al-truistic proponents notwithstanding. On the ‘pro’ side of the ledger, I conclude that extraordinary success has beenachieved in developing a comprehensive set of ‘high quality’ IFRS standards, in persuading almost 100 countriesto adopt them, and in obtaining convergence in standards with important non-adopters (notably, the US). On the‘con’ side, I envisage problems with the current fascination of the IASB (and the FASB) with ‘fair value account-ing’. A deeper concern is that there inevitably will be substantial differences among countries in implementation ofIFRS, which now risk being concealed by a veneer of uniformity. The notion that uniform standards alone will pro-duce uniform financial reporting seems naive. In addition, I express several longer run concerns. Time will tell.

*The author is Sidney Davidson Professor of Accounting atthe University of Chicago. His paper is based on the PD LeakeLecture delivered on 8 September 2005 at the Institute ofChartered Accountants in England and Wales, which can beaccessed at http://www.icaew.co.uk/index.cfm?route=112609.It draws extensively on the framework in Ball (1995) and ben-efited from comments by Steve Zeff. Financial support fromthe PD Leake Trust and the Graduate School of Business at the University of Chicago is gratefully acknowledged.Correspondence should be addressed to Professor Ball at theGraduate School of Business, University of Chicago, 5807 S.Woodlawn Avenue, Chicago, IL 60637. Tel. +00 1 (773) 8345941; E-mail: [email protected]

that are inevitable among countries have beenpushed down to the level of implementation, andnow will be concealed by a veneer of uniformity.The notion that uniform standards alone will pro-duce uniform financial reporting seems naïve, ifonly because it ignores deep-rooted political andeconomic factors that influence the incentives offinancial statement preparers and that inevitablyshape actual financial reporting practice. I envis-age problems with the current fascination of theIASB (and the FASB) for ‘fair value accounting’.In addition, I express several longer run concerns.

2. Background2.1. What are IFRS?

IFRS are accounting rules (‘standards’) issuedby the International Accounting Standards Board(IASB), an independent organisation based inLondon, UK. They purport to be a set of rules thatideally would apply equally to financial reportingby public companies worldwide. Between 1973and 2000, international standards were issued bythe IASB’s predecessor organisation, theInternational Accounting Standards Committee(IASC), a body established in 1973 by the profes-sional accountancy bodies in Australia, Canada,France, Germany, Japan, Mexico, Netherlands,United Kingdom and Ireland, and the UnitedStates. During that period, the IASC’s rules weredescribed as ‘International Accounting Standards’(IAS). Since April 2001, this rule-making functionhas been taken over by a newly-reconstitutedIASB.1 The IASB describes its rules under the newlabel ‘International Financial ReportingStandards’ (IFRS), though it continues to recog-nise (accept as legitimate) the prior rules (IAS) is-sued by the old standard-setter (IASC).2 The IASBis better-funded, better-staffed and more independ-ent than its predecessor, the IASC. Nevertheless,there has been substantial continuity across time inits viewpoint and in its accounting standards.3

2.2. Brave New WorldI need to start by confessing substantial igno-

rance on the desirability of mandating uniform ac-counting, and to caution that as a consequencemuch of what I have to say is speculative. Theresimply is not much hard evidence or resolved the-ory to help.

This was an unsettled issue when I was an ac-counting student, over 40 years ago. A successfulpush for mandating uniformity at a national leveloccurred around the turn of the twentieth century.National uniformity was a central theme of thefirst Congress of Accountants in 1904.4 A centurylater, there is an analogous push for mandatinguniformity at an international level, but in themeantime no substantial, settled body of evidenceor literature has emerged in favour – or against –

uniformity in accounting standards, at least to myknowledge.5

There thus is good reason (and, I will arguebelow, some evidence) to be sceptical of the strongclaims that its advocates make for a single globalset of accounting standards. So while this meansEurope’s adoption of IFRS is a leap of faith, it alsomeans it is a Brave New World for commentatorson IFRS, myself included. I therefore caution thatthe following views are informed more by basictenets of economics (and some limited evidence)than by a robust, directly-relevant body of re-search.

2.3. Some thoughts on the role of mandatory uni-form accounting standards

IFRS boosters typically take the case for manda-tory (i.e., required by state enactment) uniform(i.e., required of all public companies) accountingstandards as self evident. In this regard, they arenot alone: in my experience, most accounting text-books, most accounting teachers and much of theaccounting literature are in the same boat. But thecase for imposing accounting uniformity by fiat isfar from clear. Some background analysis of theeconomic role of mandatory uniform accountingstandards, one hopes, will assist the reader in sort-ing through claims as to the pros and cons of theEuropean Union mandating of IFRS.

Voluntary standards. The fundamental economicfunction of accounting standards is to provide‘agreement about how important commercialtransactions are to be implemented’ (Ball,1995:19). For example, if lenders agree to lend toa company under the condition that its debt fi-nancing will not exceed 60% of tangible assets, ithelps to have agreement on how to count the com-pany’s tangible assets as well as its debts. Are non-cancellable leases debt? Unfunded health carecommitments to employees? Expected future taxpayments due to transactions that generate bookincome now? Similarly, if a company agrees toprovide audited profit figures to its shareholders, itis helpful to be in agreement as to what constitutesa profit. Specifying the accounting methods to be

6 ACCOUNTING AND BUSINESS RESEARCH

1 The International Accounting Standards Committee(IASC) Foundation was incorporated in 2001 as a not-for-profit corporation in the State of Delaware, US. The IASCFoundation is the legal parent of the International AccountingStandards Board.

2 For convenience, I will refer to all standards recognised bythe IASB as IFRS.

3 The IASB account of its history can be found athttp://www.iasb.org/about/history.asp.

4 The proceedings of the Congress can be found on the web-site of the 10th World Congress of Accounting Historians:http://accounting.rutgers.edu/raw/aah/worldcongress/high-lights.htm. See also Staub (1938).

5 The available literature includes Dye (1985), Farrell andSaloner (1985), Dye and Verrecchia (1995) and Pownall andSchipper (1999).

followed constitutes an agreement as to how to im-plement important financial and legal conceptssuch as leverage (gearing) and earnings (profit).Accounting methods thus are an integral compo-nent of the contracting between firms and otherparties, including lenders, shareholders, managers,suppliers and customers.

Failure to specify accounting methods ex antehas the potential to create uncertainty in the pay-offs to both contracting parties. For example, fail-ure to agree in advance whether unfunded healthcare commitments to employees are to be countedas debt leaves both the borrower and the lender un-sure as to how much debt the borrower can havewithout violating a leverage covenant. Similarly,failure to specify in advance the rules for countingprofits creates uncertainty for investors when theyreceive a profit report, and raises the cost of capi-tal to the firm. But accounting standards are costlyto develop and specify in advance, so they cannotbe a complete solution. Economic efficiency im-plies a trade-off, without a complete set of stan-dards that fully determine financial reportingpractice in all future states of the world (i.e., ex-actly and for all contingencies). Some future statesof the world are extremely costly to anticipate andexplicitly contract for.6 Standards thus have theirlimits.

The alternative to fully specifying ex ante the ac-counting standards to meet every future state of theworld requires what I call ‘functional completion’(Ball, 1989). Independent institutions then are in-serted between the firm and its financial statementusers, their function being to decide ex post on theaccounting standards that would most likely havebeen specified ex ante if the actually realised statehad been anticipated and provided for. Prominentexamples of independent institutions that play thisrole in contracting include law courts, arbitrators,actuaries, valuers and auditors. When decidingwhat would most likely have been specified exante if the realised state had been anticipated andprovided for, some information is contained inwhat was anticipated and provided for. This infor-mation will include provisions that were specifiedfor similar states to that which occurred. It alsowill include abstract general provisions that wereintended for all states. In financial reporting, this isthe issue involved in so-called ‘principles-based’accounting: the balance between general and spe-cific provision for future states of the world.

Uniform voluntary standards. I am aware of atleast three major advantages of uniform (here in-terpreted as applying equally to all public compa-nies) standards that would cause them to emergevoluntarily (i.e., without state fiat). The first ad-vantage – scale economies – underlies all forms ofuniform contracting: uniform rules need only beinvented once. They are a type of ‘public good’, in

that the marginal cost of an additional user adopt-ing them is zero. The second advantage of uniformstandards is the protection they give auditorsagainst managers playing an ‘opinion shopping’game. If all auditors are required to enforce thesame rules, managers cannot threaten to shop foran auditor who will give an unqualified opinion ona more favourable rule. The third advantage iseliminating informational externalities arisingfrom lack of comparability. If firms and/or coun-tries use different accounting techniques – even ifunambiguously disclosed to all users – they canimpose costs on others (in the language of eco-nomics, create negative externalities) due to lackof comparability. To the extent that firms inter-nalise these effects, it will be advantageous forthem to use the same standards as others.

These advantages imply that some degree of uni-formity in accounting standards could be expectedto arise in a market (i.e., non-fiat) setting. This iswhat happened historically: as is the case for mostprofessions, uniform accounting standards initiallyarose in a market setting, before governments be-came involved. In the UK, the ICAEW functionedas a largely market-based standard-setter until re-cently. In the US, the American Association ofPublic Accountants – the precursor to today’sAmerican Institute of Certified Public Accountants– was formed in 1887 as a professional body with-out state fiat. In 1939, the profession accepted gov-ernment licensure and bowed to pressure from theSEC to establish a Committee on AccountingProcedure. The CAP issued 51 AccountingResearch Bulletins before being replaced in 1959by the AICPA’s Accounting Principles Board(APB), which in turn was replaced in 1973 by thecurrent FASB. While the trend has been to in-creased regulation (fiat) over time, the origin ofuniform accounting standards lies in a voluntary,market setting.7

There also are at least three important reasons toexpect somewhat less-than-uniform accountingmethods to occur in a voluntary setting. First, it isnot clear that uniform financial reporting qualityrequires uniform accounting rules (‘one size fitsall’). Uniformity in the eyes of the user could re-quire accounting rules that vary across firms,across locations and across time. Firms differ onmyriad dimensions such as strategy, investmentpolicy, financing policy, industry, technology, cap-ital intensity, growth, size, political scrutiny, andgeographical location. The types of transactionsthey enter into differ substantially. Countries differ

International Accounting Policy Forum. 2006 7

6 In the extreme case of presently unimaginable futurestates, it is infinitely costly (i.e., impossible, even with infiniteresources) to explicitly contract for optimal state-contingentpayoffs, including those affected by financial reporting.

7 Watts and Zimmerman (1986) note the market origins offinancial reporting and auditing more generally.

in how they run their capital, labour and productmarkets, and in the extent and nature of govern-mental and political involvement in them. It hasnever been convincingly demonstrated that thereexists a unique optimum set of rules for all.

Second, as observed above it is costly to developa fully detailed set of accounting standards to coverevery feasible contingency, so standards are not theonly way of solving accounting method choices.Some type of ‘functional completion’ is required.For example, under ‘principles based’ accounting,general principles rather than detailed standards aredeveloped in advance and then adapted to specificsituations with the approval of independent audi-tors. It therefore is not optimal for all accountingchoices to be made according to uniform standards.

The above-mentioned reasons to expect less thanuniform accounting methods in a voluntary settingshare the property that uniformity is not the opti-mal way to go. The third reason, that firms and/orcountries using different accounting methodsmight not fully internalise the total costs imposedon others due to lack of comparability, does nothave that property. It therefore provides a rationalefor mandating uniformity, to which I now turn.

Mandatory uniform standards are a possible so-lution to the problem of informational externali-ties. If their use of different accounting methodsimposes costs on others that firms and/or countriesdo not take into account in their decisions, then itis feasible that the state can improve aggregatewelfare by imposing uniformity. Whether thestate-imposed solution can be expected to be opti-mal is another matter. Political factors tend to dis-tort state action, a theme I shall return to.

At a more basic level, it is not clear that imper-fect comparability in financial reporting practice isa substantial problem requiring state action. Is ac-counting information a special economic good?Hotel accommodation, for example, differs enor-mously in quality. Different hotels and hotel chainsdiffer in the standards they set and the rules theyapply. Their rooms are not comparable in size ordecor, their elevators do not operate at comparablespeed, their staffs are not equally helpful, theyhave different cancellation policies, etc. There isno direct comparability of one hotel room with an-other, even with the assistance of the myriad ratingsystems in the industry, but consumers makechoices without the dire consequences frequentlyalleged to occur from differences in accountingrules. All things considered, the case for imposingaccounting uniformity by fiat is far from clear.

2.4. Why is international convergence in accounting standards occurring now?

Accounting is shaped by economics and politics(Watts, 1977; Watts and Zimmerman, 1986), so thesource of international convergence in accounting

standards is increased cross-border integration ofmarkets and politics (Ball, 1995). Driving this in-tegration is an extraordinary reduction in the costof international communication and transacting.The cumulative effect of innovations affecting al-most all dimensions of information costs – for ex-ample in computing, software, satellite andfibre-optic information transmission, the internet,television, transportation, education – is a revolu-tionary plunge in the cost of being informed aboutand becoming an actor in the markets and politicsof other countries. In my youth, only a small elitepossessed substantial amounts of current informa-tion about international markets and politics.Today, orders of magnitude more information isfreely available to all on the internet. Informedcross-border transacting in product markets andfactor markets (including capital and labour mar-kets) has grown rapidly as a consequence.Similarly, voters and politicians are much betterinformed about the actions of foreign politicians,and their consequences, than just a generation ago.We have witnessed a revolutionary internationali-sation of both markets and politics, and inevitablythis creates a demand for international conver-gence in financial reporting.

How far this will go is another matter. Despitethe undoubted integration that has occurred, no-tably in the capital and product markets, most mar-ket and political forces are local, and will remainso for the foreseeable future. Consequently, it isunclear how much convergence in actual financialreporting practice will (or should) occur. I returnto this theme below.

3. Scoring IASB against its stated objectivesThis section evaluates the progress the IASB hasmade toward achieving its stated objectives, whichinclude:8

1. ‘develop ... high quality, understandable and en-forceable global accounting standards ... thatrequire high quality, transparent and compara-ble information ... to help participants in theworld’s capital markets and other users ... .’

2. ‘promote the use and rigorous application ofthose standards.’

3. ‘bring about convergence ... .’I discuss progress toward each of these objec-

tives in turn.

3.1. DevelopmentHere the IASB has done extraordinarily well.9 It

8 ACCOUNTING AND BUSINESS RESEARCH

8 Source: http://www.iasb.org/about/constitution.asp9 Deloitte & Touche LLP provide a comprehensive review

of IFRS at www.iasplus.com/dttpubs/pubs.htm.

has developed a nearly complete set of standardsthat, if followed, would require companies to report ‘high quality, transparent and comparableinformation’.

I interpret financial reporting ‘quality’ in verygeneral terms, as satisfying the demand for finan-cial reporting. That is, high quality financial state-ments provide useful information to a variety ofusers, including investors. This requires:• accurate depiction of economic reality (for ex-

ample: accurate allowance for bad debts; notignoring an imperfect hedge);

• low capacity for managerial manipulation;• timeliness (all economic value added gets

recorded eventually; the question is howpromptly); and

• asymmetric timeliness (a form of conservatism):timelier incorporation of bad news, relative togood news, in the financial statements.

Accounting standard-setters historically haveviewed the determinants of ‘quality’ as ‘relevance’and ‘reliability,’ but I do not find these conceptsparticularly useful. For example, IASB and FASBrecently have been placing less emphasis on relia-bility. In my view, this arises from a failure to dis-tinguish reliability that is inherent in theaccounting for a particular type of transaction (theextent to which a reported number is subject to un-avoidable estimation error) from reliability arisingfrom capacity for managerial manipulation (theextent to which a reported number is subject toself-interested manipulation by management).

Compared to the legalistic, politically and tax-influenced standards that historically have typifiedContinental Europe, IFRS are designed to:• reflect economic substance more than legal form;• reflect economic gains and losses in a more

timely fashion (in some respects, even more sothan US GAAP);

• make earnings more informative;• provide more useful balance sheets; and• curtail the historical Continental European dis-

cretion afforded managers to manipulate provi-sions, create hidden reserves, ‘smooth’ earningsand hide economic losses from public view.

The only qualification I would make to myfavourable assessment of IFRS qua standards

therefore is the extent to which they are imbued bya ‘mark to market’ philosophy, an issue to which Ireturn below.

3.2. PromotionHere the IASB also has experienced remarkable

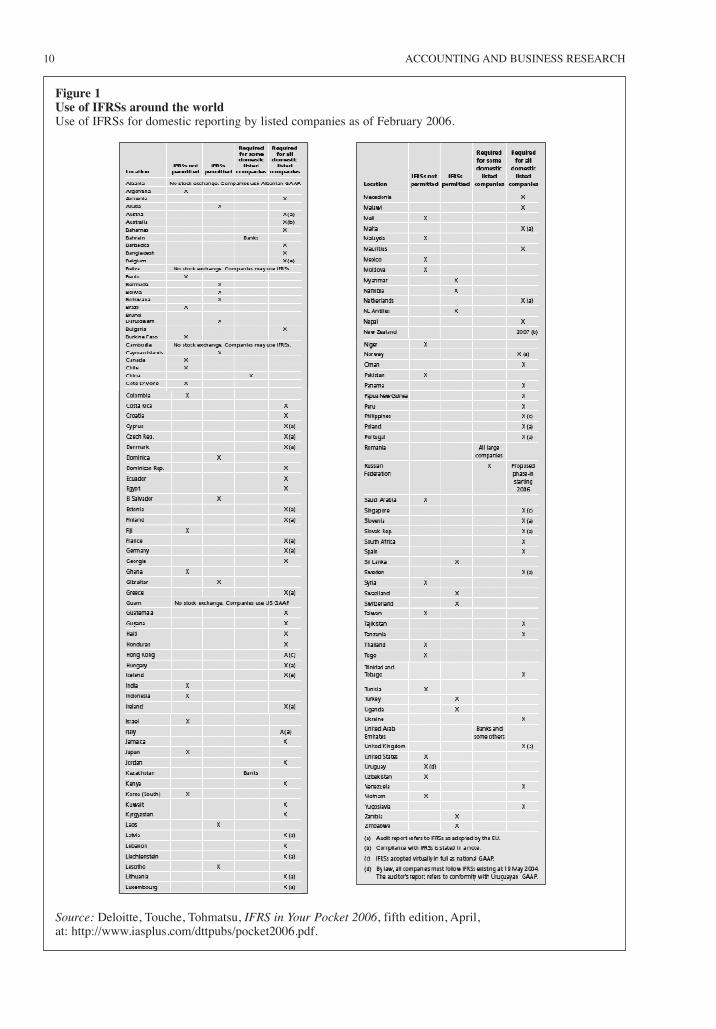

success. Indicators of this success include:• Almost 100 countries now require or allow

IFRS. A complete list, provided by Deloitte andTouche LLP (2006), is provided in Figure 1.

• All listed companies in EU member countriesare required to report consolidated financialstatements complying with IFRS, effective in2005.10

• Many other countries are replacing their na-tional standards with IFRS for some or all do-mestic companies.

• Other countries have adopted a policy of re-viewing IFRS and then adopting them eitherverbatim or with minor modification as theirnational standards.

• The International Organization of SecuritiesCommissions (IOSCO), the international or-ganisation of national securities regulators, hasrecommended that its members permit foreignissuers to use IFRS for cross-border securitiesofferings and listings.

The IASB has been tireless in promoting IFRS ata political level, and its efforts have paid off hand-somely in terms ranging from endorsement tomandatory adoption. Whether political actiontranslates into actual implementation is anothermatter, discussed below.

3.3. ConvergenceConvergence refers to the process of narrowing

differences between IFRS and the accounting stan-dards of countries that retain their own standards.Depending on local political and economic factors,these countries could require financial reporting tocomply with their own standards without formallyrecognising IFRS, they could explicitly prohibitreporting under IFRS, they could permit all com-panies to report under either IFRS or domesticstandards, or they could require domestic compa-nies to comply with domestic standards and permitonly cross-listed foreign companies to complywith either. Convergence can offer advantages,whatever the reason for retaining domestic stan-dards. It is a modified version of adoption.

Several countries that have not adopted IFRS atthis point have established convergence projectsthat most likely will lead to their acceptance ofIFRS, in one form or another, in the not too distantfuture. Most notably:

International Accounting Policy Forum. 2006 9

10 The regulation was adopted on 19 July 2002 by theEuropean Parliament and Council (EC)1606/2002. After ex-tensive political lobbying and debate, the EC ‘carved out’ twosections of IAS 39, while at the same time announcing this ac-tion as exceptional and temporary, and reiterating its supportfor IFRS.

10 ACCOUNTING AND BUSINESS RESEARCH

Figure 1Use of IFRSs around the worldUse of IFRSs for domestic reporting by listed companies as of February 2006.

Source: Deloitte, Touche, Tohmatsu, IFRS in Your Pocket 2006, fifth edition, April, at: http://www.iasplus.com/dttpubs/pocket2006.pdf.

• Since October 2002, the IASB and the FASBhave been working systematically toward con-vergence of IFRS and US GAAP. TheSecurities and Exchange Commission (SEC),the US national market regulator, has set a tar-get date no later than 2009 for it accepting fi-nancial statements of foreign registrants thatcomply with IFRS.

• The IASB recently commenced a similar,though seemingly less urgent and ambitious,convergence project with Japan.

I repeat the caveat that converge de facto is lesscertain than convergence de jure: convergence inactual financial reporting practice is a differentthing than convergence in financial reporting stan-dards. I return to this point in Section 6 below.

4. Advantages of IFRS for investors4.1. Direct IFRS advantages for investors

Widespread international adoption of IFRS of-fers equity investors a variety of potential advan-tages. These include:1. IFRS promise more accurate, comprehensive

and timely financial statement information, rel-ative to the national standards they replace forpublic financial reporting in most of the coun-tries adopting them, Continental Europe in-cluded. To the extent that financial statementinformation is not known from other sources,this should lead to more-informed valuation inthe equity markets, and hence lower risk to in-vestors.

2. Small investors are less likely than investmentprofessionals to be able to anticipate financialstatement information from other sources.Improving financial reporting quality allowsthem to compete better with professionals, andhence reduces the risk they are trading with abetter-informed professional (known as ‘ad-verse selection’).11

3. By eliminating many international differencesin accounting standards, and standardising re-porting formats, IFRS eliminate many of the

adjustments analysts historically have made inorder to make companies’ financials morecomparable internationally. IFRS adoptiontherefore could reduce the cost to investors ofprocessing financial information. The gainwould be greatest for institutions that createlarge, standardised-format financial databases.

4. A bonus is that reducing the cost of processingfinancial information most likely increases theefficiency with which the stock market incor-porates it in prices. Most investors can be ex-pected to gain from increased marketefficiency.

5. Reducing international differences in account-ing standards assists to some degree in remov-ing barriers to cross-border acquisitions anddivestitures, which in theory will reward in-vestors with increased takeover premiums.12

In general, IFRS offer increased comparabilityand hence reduced information costs and informa-tion risk to investors (provided the standards areimplemented consistently, a point I return tobelow).

4.2. Indirect IFRS advantages for investorsIFRS offer several additional, indirect advan-

tages to investors. Because higher informationquality should reduce both the risk to all investorsfrom owning shares (see 1. above) and the risk toless-informed investors due to adverse selection(see 2. above), in theory it should lead to a reduc-tion in firms’ costs of equity capital.13 This wouldincrease share prices, and would make new invest-ments by firms more attractive, other things equal.

Indirect advantages to investors arise from im-proving the usefulness of financial statement in-formation in contracting between firms and avariety of parties, notably lenders and managers(Watts, 1977; Watts and Zimmerman, 1986).Increased transparency causes managers to actmore in the interests of shareholders. In particular,timelier loss recognition in the financial state-ments increases the incentives of managers to at-tend to existing loss-making investments andstrategies more quickly, and to undertake fewernew investments with negative NPVs, such as‘pet’ projects and ‘trophy’ acquisitions (Ball 2001;Ball and Shivakumar, 2005). Ball (2004) concludesthis was the primary motive behind the 1993 deci-sion of Daimler-Benz (now DaimlerChrysler) AGto list on the New York Stock Exchange and reportfinancial statements complying with US GAAP:due to intensifying product market competitionand hence lower profit margins in its core automo-bile businesses, Daimler no longer could afford tosubsidise loss-making activities. Bushman et al.(2006) report evidence that firms in countries withtimelier financial-statement recognition of losses

International Accounting Policy Forum. 2006 11

11 See Glosten and Milgrom (1985), Diamond andVerrecchia (1991) and Leuz and Verrecchia (2000).

12 See Bradley, Desai and Kim (1988).13 The magnitude of cost of capital benefits from disclosure

is an unsettled research question, both theoretically and em-pirically. Empirical studies encounter the problem of control-ling for correlated omitted variables, notably companies’growth opportunities. Theory research is sensitive to modelassumptions, and frequently can offer insights into the direc-tion but not the magnitude of any effects. See Diamond andVerrecchia (1991), Botosan (1997), Leuz and Verrecchia(2000), Botosan and Plumlee (2002), Hail (2002), Daske(2006) and Easton (2006).

are less likely to undertake negative-NPV invest-ments. The increased transparency and loss recog-nition timeliness promised by IFRS thereforecould increase the efficiency of contracting be-tween firms and their managers, reduce agencycosts between managers and shareholders, and en-hance corporate governance.14 The potential gainto investors arises from managers acting more intheir (i.e., investors’) interests.

The increased transparency promised by IFRSalso could cause a similar increase in the efficien-cy of contracting between firms and lenders. Inparticular, timelier loss recognition in the financialstatements triggers debt covenants violations morequickly after firms experience economic lossesthat decrease the value of outstanding debt (Ball2001, 2004; Ball and Shivakumar 2005; Ball et al.,2006). Timelier loss recognition involves timelierrevision of the book values of assets and liabilities,as well as earnings and stockholders’ equity, caus-ing timelier triggering of covenants based on fi-nancial statement variables. In other words, theincreased transparency and loss recognition timeli-ness promised by IFRS could increase the effi-ciency of contracting in debt markets, withpotential gains to equity investors in terms of re-duced cost of debt capital.

An ambiguous area for investors will be the ef-fect of IFRS on their ability to forecast earnings.One school of thought is that better accountingstandards make reported earnings less noisy andmore accurate, hence more ‘value relevant’. Otherthings equal (for example, ignoring enforcementand implementation issues for the moment) thiswould make earnings easier to forecast and wouldimprove average analyst forecast accuracy.15 Theother school of thought reaches precisely the op-posite conclusion. This reasoning is along the linesthat managers in low-quality reporting regimes areable to ‘smooth’ reported earnings to meet a vari-ety of objectives, such as reducing the volatility oftheir own compensation, reducing the volatility ofpayouts to other stakeholders (notably, employeebonuses and dividends), reducing corporate taxes,and avoiding recognition of losses.16 In contrast,earnings in high-quality regimes are more inform-ative, more volatile, and more difficult to predict.This argument is bolstered in the case of IFRS by their emphasis on ‘fair value accounting’, asoutlined in the following section. Fair value ac-counting rules aim to incorporate more-timely in-formation about economic gains and losses onsecurities, derivatives and other transactions intothe financial statements, and to incorporate more-timely information about contemporary economiclosses (‘impairments’) on long term tangible andintangible assets. IFRS promise to make earningsmore informative and therefore, paradoxically,more volatile and more difficult to forecast.

In sum, there are a variety of indirect ways inwhich IFRS offer benefits to investors. Over thelong term, the indirect advantages of IFRS to in-vestors could well exceed the direct advantages.

5. Fair value accountingA major feature of IFRS qua standards is the extentto which they are imbued with fair value account-ing [a.k.a. ‘mark to market’ accounting]. Notably:• IAS 16 provides a fair value option for proper-

ty, plant and equipment;• IAS 36 requires asset impairments (and impair-

ment reversals) to fair value;• IAS 38 requires intangible asset impairments to

fair value;• IAS 38 provides for intangibles to be revalued

to market price, if available;• IAS 39 requires fair value for financial instru-

ments other than loans and receivables that arenot held for trading, securities held to maturity;and qualifying hedges (which must be near-perfect to qualify);17

• IAS 40 provides a fair value option for invest-ment property;

• IFRS 2 requires share-based payments (stock,options, etc.) to be accounted at fair value; and

• IFRS 3 provides for minority interest to berecorded at fair value.

This list most likely will be expanded over time.Both IASB and FASB have signalled their intent todo so.

I have distinctly mixed views on fair value ac-counting. The fundamental case in favour of fairvalue accounting seems obvious to most econo-mists: fair value incorporates more informationinto the financial statements. Fair values containmore information than historical costs wheneverthere exist either:1. Observable market prices that managers cannot

materially influence due to less than perfectmarket liquidity; or

12 ACCOUNTING AND BUSINESS RESEARCH

14 These ‘numerator’ effects of higher quality financial re-porting (i.e., increasing the cash flows arising from managers’actions) in my view are likely to have a considerably larger influence on firms’ values than any ‘denominator’ effects (i.e., reducing the cost of capital). See Ball (2001: 140–141).However, it is difficult to disentangle the two effects in prac-tice.

15 See Ashbaugh and Pincus (2001), Hope (2003) and Lang,Lins and Miller (2003).

16 See Ball, Kothari and Robin (2000) and Ball, Robin andWu (2003).

17 Available-for-sale securities are to be shown at Fair Valuein the Balance Sheet only.

2. Independently observable, accurate estimatesof liquid market prices.

Incorporating more information in the financialstatements by definition makes them more inform-ative, with potential advantages to investors, andother things equal it makes them more useful forpurposes of contracting with lenders, managersand other parties.18

Over recent decades, the markets for many com-modities and financial instruments, including de-rivatives, have become substantially deeper andmore liquid. Some of these markets did not evenexist 30 years ago. There has been enormous con-current growth in electronic databases containingtransactions prices for commodities and securities,and for a variety of assets such as real estate forwhich comparable sales can be used in estimatingfair values. In addition, a variety of methods for re-liably estimating fair values for untraded assetshave become generally acceptable. These includethe present value (discounted cash flow) method,the first application of which in formal accountingstandards was in lease accounting (SFAS No. 13 in1976), and a variety of valuation methods adaptedfrom the original Black-Scholes (1973) model. Inview of these developments, it stands to reasonthat accountants have been replacing more andmore historical costs with fair values, obtainedboth from liquid market prices and from model-based estimates thereof.

The question is whether IASB has pushed (andintends to push) fair value accounting too far.There are many potential problems with fair valuein practice, including:19

• Market liquidity is a potentially important issuein practice. Spreads can be large enough tocause substantial uncertainty about fair valueand hence introduce noise in the financial state-ments.

• In illiquid markets, trading by managers can in-fluence traded as well as quoted prices, andhence allows them to manipulate fair value es-timates.

• Worse, companies tend to have positively cor-related positions in commodities and financialinstruments, and cannot all cash out simultane-ously at the bid price, let alone at the ask. Fairvalue accounting has not yet been tested by amajor financial crisis, when lenders in particu-lar could discover that ‘fair value’ means ‘fairweather value’.

• When liquid market prices are not available,fair value accounting becomes ‘mark to model’accounting. That is, firms report estimates ofmarket prices, not actual arm’s length marketprices. This introduces ‘model noise,’ due toimperfect pricing models and imperfect esti-

mates of model parameters.• If liquid market prices are available, fair value

accounting reduces opportunities for self-inter-ested managers to influence the financial state-ments by exercising their discretion overrealising gains and losses through the timing ofasset sales. However, fair value accounting in-creases opportunities for manipulation when‘mark to model’ accounting is employed tosimulate market prices, because managers caninfluence both the choice of models and the pa-rameter estimates.

It is important to stress that volatility per se isnot the concern here. Volatility is an advantage infinancial reporting, whenever it reflects timely in-corporation of new information in earnings, andhence onto balance sheets (in contrast with‘smoothing,’ which reduces volatility). However,volatility becomes a disadvantage to investors andother users whenever it reflects estimation noiseor, worse, managerial manipulation.

The fair value accounting rules in IFRS placeconsiderable faith in the ‘conceptual framework’that IASB and FASB are jointly developing(IASB, 2001). This framework:• is imbued with a highly controversial ‘value

relevance’ philosophy;• emphasises ‘relevance’ relative to ‘reliability;’• assumes the sole purpose of financial reporting

is direct ‘decision usefulness;’• downplays the indirect ‘stewardship’ role of

accounting; and• could yet cause IASB and FASB some grief.

IASB and FASB seem determined to push aheadwith it nevertheless. FASB staff member L. ToddJohnson (2005) concludes:

‘The Board has required greater use of fair valuemeasurements in financial statements because itperceives that information as more relevant to in-vestors and creditors than historical cost informa-tion. Such measures better reflect the presentfinancial state of reporting entities and better facil-itate assessing their past performance and future

International Accounting Policy Forum. 2006 13

18 Ball, Robin and Sadka (2006) conclude from a cross-country analysis that providing new information to equity in-vestors is not the dominant economic function of financialreporting (investors can be informed about gains and losses ina timely fashion via disclosure, without financial statementrecognition). Conversely, the dominant function of timely lossrecognition is to facilitate contracting (the study focused ondebt markets).

19 In addition, gains and losses in fair value are transitory innature and hence are unlike recurring business income. For ex-ample, they normally will sell at lower valuation multiples. Toavoid misleading investors, fair value gains and losses need tobe clearly labelled as such.

prospects. In that regard, the Board does not acceptthe view that reliability should outweigh relevancefor financial statement measures.’

Noisy information on gains and losses is more in-formative than none, so even the least reliable ‘markto model’ estimates certainly incorporate more in-formation. But this is not a sufficient basis for justi-fying fair value accounting, for at least four reasons:1. ‘Value relevance’ (i.e., informing users) is by

no means the sole criterion for financial report-ing. One also has to consider the role of finan-cial reporting in contexts where noise matters,including debt and compensation contracts(Watts and Zimmerman, 1986; Holthausen andWatts, 2001). Noise in any financial informa-tion that affects contractual outcomes (e.g.,lenders’ rights when leverage ratio or interestcoverage covenants are violated; managers’bonuses based on reported earnings) increasesthe risk faced by both the firm and contractingparties. Other things equal, it thus is a source ofcontracting inefficiency. Providing more infor-mation thus can be worse than providing less,if it is accompanied by more noise. ‘Mark tomodel’ fair value accounting can add volatilityto the financial statements in the form of bothinformation (a ‘good’) and noise arising frominherent estimation error and managerial ma-nipulation (a ‘bad’).

2. It is important to distinguish ‘recognition’ (in-corporating information in the audited financialstatements, notably by including estimatedgains and losses in earnings and book value)from ‘disclosure’ (informing investors, for ex-ample by audited footnote disclosure or provi-sion of unaudited information, withoutincorporation in earnings or on balance sheets).Noisy fair value information does not necessar-ily have to be recognised to be useful to equityinvestors.20 The case for increased deploymentof fair value accounting in the audited financialstatements is not based on any substantial bodyof evidence – at least of which I am aware – thatgain and loss information is not available fromsources outside the financial statements, andthat value is added in the economy by auditingit, let alone by incorporating it in earnings.

3. Financial reporting conveys an important eco-nomic role by accurately and independentlycounting actual outcomes, and hence confirm-ing prior information about expected out-comes. In particular, if managers believe actualoutcomes are more likely to be reported accu-rately and independently, they are less likely todisclose misleading information about their ex-pectations. It is possible that, as a financial re-porting regime strays far from reportingoutcomes by incorporating more information

about expectations, the reliability of the avail-able information about expectations begins tofall. A feasible outcome is that the amount ofinformation contained in the financial state-ments rises, and at the same time the totalamount of information falls.21

4. Accounting standards and – what is more im-portant – accounting practice have long sincebeen imbued with one of the two sides of ‘fairvalue’ accounting. That is, timely loss recogni-tion, in which expected future cash losses arecharged against current earnings and bookvalue of equity, is a long-standing property offinancial reporting. The other side of ‘fairvalue,’ timely gain recognition, is not as preva-lent in practice (Basu, 1997). Loss recognitiontimeliness is particularly evident in common-law countries such as Australia, Canada, UKand US (Ball et al., 2000). It affects financialreporting practice in many ways, including thepervasive ‘lower of cost or market’ rule (for ex-ample, accruing expected decreases in the fu-ture realisable value of inventory againstcurrent earnings, but not expected increases),accruing loss contingency provisions (but set-ting a higher standard for verification of gaincontingencies), and long term asset impairmentcharges (but not upward revaluations). It sim-ply is incorrect to view the prevailing financialreporting model as ‘historical cost accounting’.Financial reporting, particularly in common-law countries, is a mixed process involvingboth historical costs and (especially contingenton losses) fair values.

In sum, I have mixed views about the extent towhich IFRS are becoming imbued with the currentIASB/FASB fascination with ‘fair value account-ing’. On the one hand, this philosophy promises toincorporate more information in the financialstatements than hitherto. On the other, it does notnecessarily make investors better off and its use-fulness in other contexts has not been clearlydemonstrated. Worse, it could make investors andother users worse off, for a variety of reasons. Thejury is still out on this issue.

14 ACCOUNTING AND BUSINESS RESEARCH

20 Barth, Clinch and Shibano (2003) provide some theoreti-cal support for the proposition that recognition matters per se,though the result flows directly from the model’s assumptions.Ball, Robin and Sadka (2006) argue that equity investors arerelatively indifferent between receiving a given amount of in-formation (i.e., controlling for the amount of noise) via dis-closure and via recognition in the financial statements.Conversely, they argue that the demand for recognition versusdisclosure arises primarily from the use of financial statementsin debt markets.

21 See Ball (2001: 133–138) for elaboration.

6. Effect on investors of uneven implementationI believe there are overwhelming political and eco-nomic reasons to expect IFRS enforcement to beuneven around the world, including withinEurope. Substantial international differences in fi-nancial reporting practice and financial reportingquality are inevitable, international standards or nointernational standards. This conclusion is basedon the premise that – despite increased globalisa-tion – most political and economic influences onfinancial reporting practice remain local. It is rein-forced by a brief review of the comparativelytoothless body of international enforcement agen-cies currently in place. The conclusion also is sup-ported by a fledgling academic literature on therelative roles of accounting standards and the in-centives of financial-statement preparers in deter-mining actual financial reporting practice.

One concern that arises from widespread IFRSadoption is that investors will be mislead into be-lieving that there is more uniformity in practicethan actually is the case and that, even to sophisti-cated investors, international differences in report-ing quality now will be hidden under the rug ofseemingly uniform standards. In addition, unevenimplementation curtails the ability of uniformstandards to reduce information costs and informa-tion risk, described above as an advantage to in-vestors of IFRS. Uneven implementation couldincrease information processing costs to transna-tional investors – by burying accounting inconsis-tencies at a deeper and less transparent level thandifferences in standards. In my view, IFRS imple-mentation has not received sufficient attention,perhaps because it lies away from public sight,‘under the rug’.

6.1. Markets and politics remain primarily local,not global

The fundamental reason for being scepticalabout uniformity of implementation in practice isthat the incentives of preparers (managers) and en-forcers (auditors, courts, regulators, boards, block

shareholders, politicians, analysts, rating agencies,the press) remain primarily local.

All accounting accruals (versus simply countingcash) involve judgments about future cash flows.Consequently, there is much leeway in implement-ing accounting rules. Powerful local economic andpolitical forces therefore determine how managers,auditors, courts regulators and other parties influ-ence the implementation of rules. These forceshave exerted a substantial influence on financialreporting practice historically, and are unlikely to suddenly cease doing so, IFRS or no IFRS.Achieving uniformity in accounting standardsseems easy in comparison with achieving unifor-mity in actual reporting behaviour. The latterwould require radical change in the underlyingeconomic and political forces that determine actu-al behaviour.

Sir David Tweedie, IASB chairman, premisesthe case for international uniformity in accountingstandards on global integration of markets:22

‘As the world’s capital markets integrate, thelogic of a single set of accounting standards is ev-ident. A single set of international standards willenhance comparability of financial informationand should make the allocation of capital acrossborders more efficient. The development and ac-ceptance of international standards should also re-duce compliance costs for corporations andimprove consistency in audit quality.’

But this logic works both ways. One can changethe underlying premise to make a case against uni-formity. Because capital markets are not perfectlyintegrated (debt markets in particular), and be-cause more generally economic and political inte-gration are both far from being complete, the logicof national differences should be equally evident.While increased internationalisation of marketsand politics can be expected to reduce some of thediversity in accounting practice across nations, na-tions continue to display clear and substantial do-mestic facets in both their politics and how theirmarkets are structured, so increased internationali-sation cannot be expected to eliminate diversity inpractice.

I have heard an analogy made between IFRS andthe metric system of uniform weights and meas-ures.23 The analogy is far from exact, but instruc-tive nevertheless. There is an old saying: ‘Theweight of the butcher’s thumb on the scale is heav-ier in ... [other country X].’ Despite uniform meas-urement rules, the butcher’s discretion inimplementing them is limited only by the practisedeye of the customer, by concern for reputation, andby the monitoring of state and private inspectionsystems. The lesson from this saying is that moni-toring mechanisms operate differently across na-tions. There is considerably more discretion inimplementing financial reporting rules than in

International Accounting Policy Forum. 2006 15

22 Considering the amount of time the IASB has exerted inlobbying governments (the EU included) on IFRS adoption,there is some irony in Sir David focusing on international in-tegration of markets, without mentioning integration of politi-cal forces. The strongly adverse initial reaction to thepublication of Watts (1977) and Watts and Zimmerman(1978), introducing the topic of political influences on finan-cial reporting practice, suggests this is a sensitive issue.

23 The metric system was first proposed in 1791, was adopt-ed by the French revolutionary assembly in 1795, and wassubstantially refined and widely adopted during the secondhalf of the nineteenth century (primarily in code law coun-tries). France then ceded control of the system to an interna-tional body, and in 1875 the leading industrialised countries(including the US, but not the UK) created the InternationalBureau of Weights and Measures to administer it.

weighing meat, and consequently this is offset byconsiderably more complex, frequent and effectivefinancial reporting monitoring mechanisms. Buthere too the monitoring mechanisms operate dif-ferently across nations.

Before getting too carried away with globalisa-tion, it is worth remembering that in fact mostmarkets and most politics are local, not global. Thelate Tip O’Neill, long-time speaker of the USHouse of Representatives, famously stated(O’Neill, 1993): ‘All politics is local.’ Much thesame could be said about markets. Important di-mensions in which the world still looks consider-ably more local than global include:• Extent and nature of government involvement

in the economy;• Politics of government involvement in finan-

cial reporting practices (e.g., political influenceof managers, corporations, labour unions,banks);

• Legal systems (e.g., common versus code law;shareholder litigation rules);

• Securities regulation and regulatory bodies;• Depth of financial markets;• Financial market structure (e.g., closeness of re-

lationship between banks and client companies);• The roles of the press, financial analysts and

rating agencies;• Size of the corporate sector;• Structure of corporate governance (e.g., rela-

tive roles of labour, management and capital);• Extent of private versus public ownership of

corporations;• Extent of family-controlled businesses;• Extent of corporate membership in related-

company groups (e.g., Japanese keiretsu orKorean chaebol);

• Extent of financial intermediation;• The role of small shareholders vs. institutions

and corporate insiders;• The use of financial statement information, in-

cluding earnings, in management compensa-tion; and

• The status, independence, training and com-pensation of auditors.

The above list is far from complete, but it givessome sense of the extent to which financial report-ing occurs in a local, not global, context. Despiteincreased globalisation, the clear majority of eco-nomic and political activity remains intranational,

the implication being that the primary drivingforces behind the majority of actual accountingpractices seem likely to remain domestic in naturefor the foreseeable future.

The most visible effect of local political and eco-nomic factors on IFRS lies at the level of the na-tional standard adoption decision.24 This alreadyhas occurred to a minor degree, in the EU ‘carveout’ from IAS 39 in the application of fair valueaccounting to interest rate hedges. The Europeanversion of IAS 39 emerged in response to consid-erable political pressure from the government ofFrance, which responded to pressure from domes-tic banks concerned about balance sheet volatili-ty.25 Episodes like this are bound to occur in thefuture, whenever reports prepared under IFRS pro-duce outcomes that adversely affect local interests.

Another level at which local political and eco-nomic factors are likely to visibly influence IFRSadoption stems from the latitude IFRS give tofirms to choose among alternative accountingmethods.26 Local factors make it unlikely that thisdiscretion will be exercised uniformly acrosscountries, and across firms within countries.

Nevertheless, in my view the most likely effectof local politics and local market realities on IFRSwill be much less visible than was the case withthe prolonged political debate on IAS 39. I believethe primary effect of local political and market fac-tors will lie under the surface, at the level of im-plementation, which is bound to be substantiallyinconsistent across nations.

Does anyone seriously believe that implementa-tion will be of equal standard in all the nearly 100countries, listed in Figure 1, that have announcedadoption of IFRS in one way or another? The listof adopters ranges from countries with developedaccounting and auditing professions and devel-oped capital markets (such as Australia) to coun-tries without a similarly developed institutionalbackground (such as Armenia, Costa Rica,Ecuador, Egypt, Kenya, Kuwait, Nepal, Tobagoand Ukraine).

Even within the EU, will implementation ofIFRS be at an equal standard in all countries? Thelist includes Austria, Belgium, Cyprus, CzechRepublic, Denmark, Germany, Estonia, Greece,Spain, France, Ireland, Italy, Latvia, Lithuania,Luxembourg, Hungary, Malta, Netherlands, Poland,Portugal, Slovenia, Slovakia, Finland, Sweden and

16 ACCOUNTING AND BUSINESS RESEARCH

24 Zeff (2006) surveys political influences on standard adop-tions in the US, Canada, the UK and Sweden, and also in re-lation to IFRS.

25 In my view, governments will not in practice cede the de-cision to impair banks’ balance sheets to accountants. In theevent of a financial crisis, there is strong political pressure tonot mark banks’ balance sheets to market, in order to avoidbank closures resulting from violating prudential ratios, aswitnessed in Japan over the last decade.

26 See Watts (1977) and Watts and Zimmerman (1986).

the UK. It is well known that uniform EU econom-ic rules in general are not implemented evenly, withsome countries being notorious standouts.27 Whatmakes financial reporting rules different?

Accounting accruals generally require at leastsome element of subjective judgment and hencecan be influenced by the incentives of managersand auditors. Consider the case of IAS 36 and IAS38, which require periodic review of long termtangible and intangible assets for possible impair-ment to fair value. Do we seriously believe thatmanagers and auditors will comb through firms’asset portfolios to discover economically impairedassets with the same degree of diligence and ruth-lessness in all the countries that adopt IFRS? Willauditors, regulators, courts, boards, analysts, ratingagencies, the press and other monitors of corporatefinancial reporting provide the same degree ofoversight in all IFRS-adopting countries? In theevent of a severe economic downturn creatingwidespread economic impairment of companies’assets, will the political and regulatory sectors ofall countries be equally likely to turn a blind eye?Will they be equally sympathetic to companiesfailing to record economic impairment on their ac-counting balance sheets, in order to avoid loan de-fault or bankruptcy (as did Japanese banks for anextended period)? Will local political and econom-ic factors cease to exert the influence on actual financial reporting practice that they have in thepast? Or will convergence among nations in adopt-ed accounting standards lead to an offsetting di-vergence in the extent to which they areimplemented?

The drift toward fair value accounting in IFRSwill only accentuate the extent to which IFRS im-plementation depends on manager and auditorjudgment, and hence is subject to local politicaland economic influence. Furthermore, the clearmajority of IFRS adopting countries cannot be saidto possess deep securities, derivatives and curren-cy markets. Implementation of the IFRS fair valueaccounting standards in many countries will en-counter problems with illiquidity, wide spreadsand subjectivity in ‘mark to model’ estimates offair value. Furthermore, in many countries theavailable information needed to implement theasset impairment standards is meagre and not read-ily observable to auditors and other monitors. Tomake matters worse, the countries in which therewill be greater room to exercise judgment underfair value accounting, due to lower-liquidity mar-

kets and poorer information about asset impair-ment, are precisely the countries with weaker localenforcement institutions (audit profession, legalprotection, regulation, and so on). Judgment is ageneric property of accounting standard imple-mentation, but worldwide reliance on judgmenthas been widely expanded under IFRS by the driftto fair value accounting and by the adoption of fairvalue standards in countries with illiquid markets.

It is worth bearing in mind that from the outsetthe IASC, the precursor to the IASB, has beenstrongly supported by the ‘G4+1’ common lawcountries (Australia, Canada, New Zealand, UKand US) which have comparatively deep marketsand comparatively developed shareholders’ rights,auditing professions, and other monitoring sys-tems. Its philosophy has been tilted toward a com-mon-law view of financial reporting (a topicdiscussed further below). This view forms thefoundation for accounting standards that requiretimely recognition of losses, in particular the assetimpairment standards IAS 36 and IAS 38.Historically, common-law financial reporting hasexhibited a substantially greater propensity torecognise economic losses in a timely fashion thanfinancial reporting in Continental Europe and Asia(Ball, Kothari and Robin, 2000; Ball et al., 2003).Implementation of IAS 36 and IAS 38 requiressubjective assessments of future cash flows, some-times decades into the future, and thus is subject toa large degree of discretion. It remains to be seenif managers, auditors, regulators and other moni-tors outside of the common-law countries will bepersuaded by IFRS adoption that it is in their in-terests to radically change their behaviour.

In sum, even a cursory review of the politicaland economic diversity among IFRS-adopting na-tions, and of their past and present financial re-porting practices, makes the notion that uniformstandards alone will produce uniform financial re-porting seems naive. This conclusion is strength-ened by the following review of the weakinternational IFRS enforcement mechanisms thatare in place, and by a review of the relevant litera-ture on the relative roles of accounting standardsand the reporting incentives of financial statementpreparers (i.e., managers and auditors).

6.2. IFRS enforcement mechanismsUnder its constitution, the IASB is a standard-

setter and does not have an enforcement mecha-nism for its standards: it can cajole countries andcompanies to adopt IFRS in name, but it cannot re-quire their enforcement in practice. It cannot pe-nalise individual companies or countries that adoptits standards, but in which financial reporting prac-tice is of low quality because managers, auditorsand local regulators fail to fully implement thestandards. Nor has it shown any interest in disal-

International Accounting Policy Forum. 2006 17

27 For example, the Financial Times (July 19, 2005) reportsthat ‘Italy has the worst record of all European Union memberstates when it comes to implementing the laws that underpinthe EU’s internal market, according to data released by theEuropean Commission yesterday. ... The worst performersapart from Italy are Luxembourg, Greece, the Czech Republicand Portugal.’

lowing or even dissuading low-quality companiesor countries from using its ‘brand name’.Individual countries remain primarily regulators oftheir own financial markets, EU member countriesincluded. That exposes IFRS to the risk of adop-tion in name only.

Worldwide regulatory bodies generally are re-garded as toothless watchdogs, despite recent at-tempts to strengthen them. The ‘alphabet soup’ ofinternational regulators now includes:• International Auditing and Assurance

Standards Board (IAASB), a committee of theInternational Federation of Accountants(IFAC). IAASB issues and promotes uniformauditing practices worldwide, but lacks effec-tive enforcement powers.

• International Organization of SecuritiesCommissions (IOSCO), an umbrella organisa-tion of national regulators. IOSCO developsand promotes securities regulation standardsand their enforcement. It encourages membercountries to adopt IFRS, but does not policetheir enforcement.

• Public Interest Oversight Board (PIOB), estab-lished in February 2005 by IOSCO, the BaselCommittee on Banking Supervision (BCBS),the International Association of InsuranceSupervisors (IAIS), the World Bank, and theFinancial Stability Forum. PIOB will overseeIFAC’s standard-setting activities in audit per-formance, independence, ethics, quality con-trol, assurance and education. In relation toenforcement, it will oversee IFAC’s MemberBody Compliance Program.

European regulatory bodies include:• Committee of European Securities Regulators

(CESR). CESR promulgates high-level IFRSenforcement principles.

• EU Directive on Statutory Audit of AnnualAccounts and Consolidated Accounts. The EUDirective mandates EU-wide auditing stan-dards.

Whether these bodies will substantially har-monise actual reporting behaviour in not yet clear.Even if all IFRS-adopting nations agreed to fullycede their sovereignty over regulation of financialreporting to these transnational bodies, whichseems highly doubtful, domestic political and eco-nomic forces most likely would cause them to ab-rogate that agreement whenever it suited them.28

6.3. Standards versus incentivesAn emerging literature investigates the extent to

which differences in actual reporting behaviour areendogenous (i.e., determined by real economic andpolitical factors that are local in nature and that

differ among countries). The relevance of this lit-erature to IFRS implemenation is the implicationthat, to the extent financial reporting practice is en-dogenous, an exogenously-developed set of ac-counting standards is unlikely to materially changefirms’ actual reporting behaviour. Complete endo-geneity would imply that change in financial re-porting would occur only if there was change inthe real economic and political factors that deter-mine it – for example, it would imply that uniformfinancial reporting would only occur under per-fectly integrated world markets and political sys-tems, uniform standards notwithstanding. Partialendogeneity would imply that adopting uniforminternational standards would have some, but lim-ited, success in overcoming national differences inthe real economic and political factors that deter-mine actual practice, and hence in reducing differ-ences in financial reporting practice.

Research on the economic and political factorsthat influence financial reporting practice interna-tionally includes Ball, Kothari and Robin (2000);Pope and Walker (1999); Ball, Robin and Wu(2000, 2003); Ali and Hwang (2000); Leuz (2003);Leuz, Nanda and Wysocki (2003); Bushman,Piotroski and Smith (2004, 2006); Bushman andPiotroski (2006); Ball, Robin and Sadka (2006);and Leuz and Oberholzer (2006). One contributionof this research is to document substantial differ-ences among countries in reporting behavior thatare endogenously determined by local economicand political factors. This evidence implies thatadopting uniform IFRS would not fully overcomenational differences in financial reporting practice.A related contribution is more direct evidence thatexogenously imposed standards do not substantial-ly influence financial reporting quality.

Ball, Kothari and Robin (2000) investigate dif-ferences in financial reporting quality betweencommon-law and code-law countries.29 Commonlaw takes its name from the process whereby lawsoriginate: it its pure form, common law arises fromwhat is commonly accepted to be appropriate prac-tice. Common law originated in England andspread to its former colonies (US, Canada,

18 ACCOUNTING AND BUSINESS RESEARCH

28 A recent parallel is France’s refusal to enforce EUtakeover rules, which has led to considerable watering downof the rules after a decade of negotiation. In the meantime,France announced it would block rumoured takeovers ofGroupe Danone SA by the US company PepsiCo Inc., and ofSuez SA by Italy’s Enel SpA. As a result of France’s politicalposition, EU rules have been loosened so that member statesnow have wide latitude to set their own standards in relationto takeover defences. The notion of an integrated Europeanmarket for corporate control thereby has been considerably di-luted. The lesson is that global rules will prevail so long asthey do not run foul of important local interests. Why wouldfinancial reporting rules be any different?

29 Ball, Kothari and Robin (2000) was replicated and ex-tended (the publication dates are misleading) by Pope andWalker (1999).

Australia, New Zealand). It tends to be more mar-ket-oriented, supports a proportionately larger list-ed corporate sector, is more litigious, tends topresume that investors are outsiders ‘at arm’s-length’ from the company, and hence is more like-ly to presume that investors rely on timely publicdisclosure and financial reporting. Financial re-porting practice (and rules) emphasises timelyrecognition of losses in the financial statements.Earnings are more volatile, more informative, andmore closely-followed by investors and analysts.Unlike code law, common law in its purest formmakes standard-setting a private-sector responsi-bility.

Code law also takes its name from the processwhereby laws, including financial reporting rules,are created: they are ‘coded’ in the public sector.Politically powerful stakeholder groups necessari-ly are represented in both codifying and imple-menting rules. Code law originated in ContinentalEurope and spread to the former colonies ofBelgium, France, Germany, Italy, Portugal andSpain. Code-law countries generally are less mar-ket-oriented, have proportionately larger govern-ment and unlisted private-company sectors, areless litigious, and are more likely to operate an ‘in-sider access’ model with less emphasis on publicfinancial reporting and disclosure. There is lessemphasis on timely recognition of losses in thepublic financial statements, and earnings havelower volatility and lower informativeness.

Ball, Robin and Wu (2003) study four East Asiancountries. They argue that the companies in thesecountries are more likely to be members of relatedcorporate groups, including those under familycontrol, in which a version of the ‘insider access’model operates and hence there is less emphasisthan under common law on public financial re-porting and disclosure. While the specific politi-cally powerful stakeholder groups are differentthan in typical code-law countries (notably, organ-ised labour typically has less political clout in Asiathan in code law countries), governments play asimilar role in the economy.

In practice, the distinction between the code-law,common-law and Asian groupings is blurred (forexample, where does one place Hong Kong overtime?). Ball, Kothari and Robin (2000) and Ball,Robin and Wu (2003) use the categories as an im-perfect proxy for the extent and type of politicalinvolvement in the economy, and hence of the ex-tent to which political (versus market) factors in-fluence finacial reporting practice. Countries withhighly politicised economies are more likely topoliticise financial reporting practice, but they alsotend to gravitate toward an ‘insider access’ (versuspublic disclosure) model and to grant politicallypowerful stakeholder groups an important role.Leuz, Nanda and Wysocki (2003) eschew country-

type classifications and employ the more-detailedlegal-system variables reported in La Porta et al.(1997, 1998), though in a different context Ball,Robin and Sadka (2006) report evidence that coun-try-type variables work better, consistent with theview that detailed institutional variables are en-dogenously determined by more primitive politicaland economic factors. Which approach better ex-plains international differences in financial report-ing practice is an interesting and not fully resolvedissue. Nevertheless, all studies indicate that differ-ences in actual reporting behavior are endogenous(i.e., determined by real economic and politicalfactors that differ among countries).

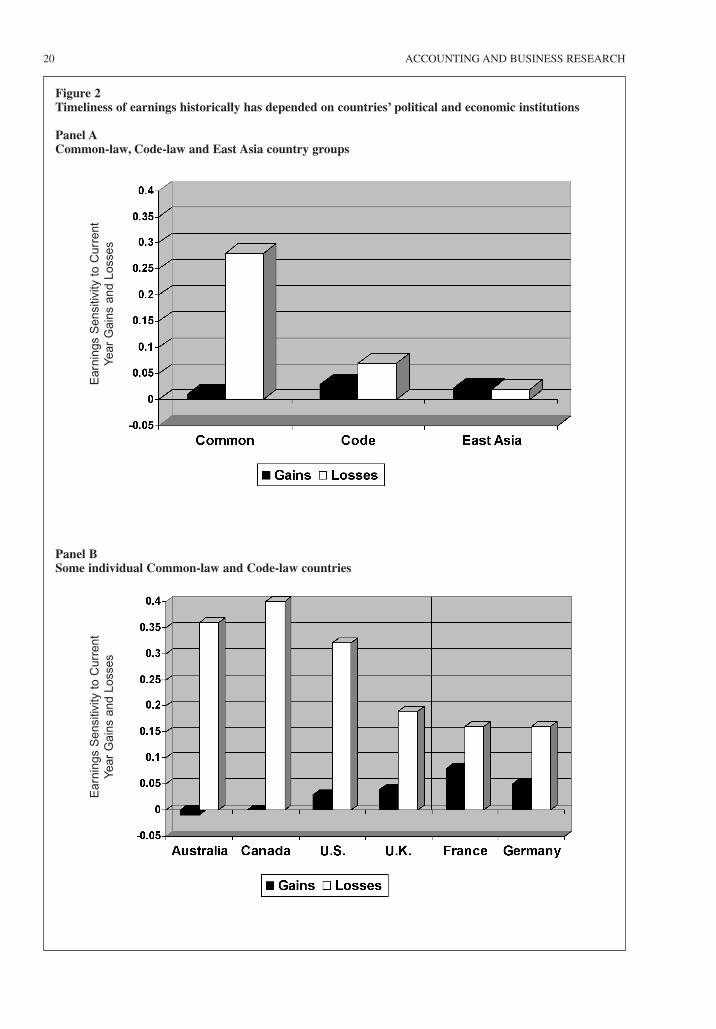

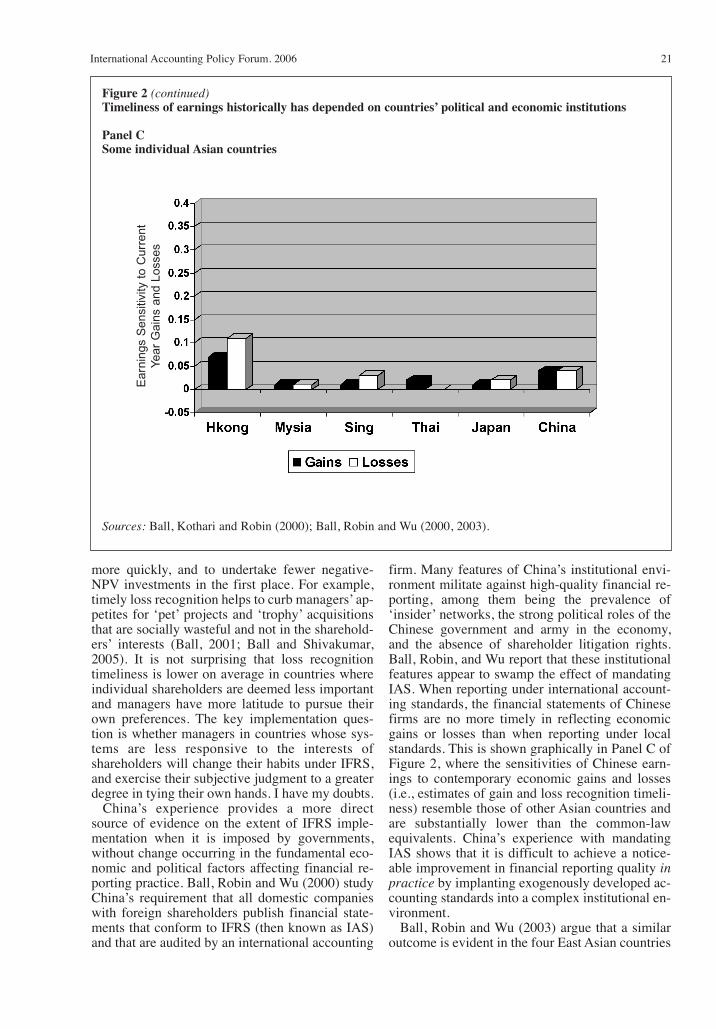

Some idea of international differences in finan-cial reporting quality can be obtained from Figure2, which summarises results in Ball, Kothari andRobin (2000) and Ball, Robin and Wu (2000,2003). The three panels graph the sensitivity of re-ported earnings to contemporary economic gainsand losses, as measured imperfectly by fiscal-yearstock returns (details are provided in the source ar-ticles). The heights of the bars represent estimatesof the sensitivity of earnings to contemporary eco-nomic gains (black bars) and to contemporary eco-nomic losses (white bars) in a particular country orgroup of countries. These sensitivity estimatescapture the timeliness of gain and loss recognitionin the countries and country groups – important at-tributes of financial reporting quality.30

Panel A summarises the results for three countrygroups: common-law, code-law and East Asia.Panels B and C provide estimates for a selection ofindividual countries. Differences in financial re-porting practice among the three groups are readi-ly apparent. The most notable difference is theconsiderably higher sensitivity of earnings to con-temporary economic losses in the common-lawcategory. This evidence of timelier recognition ofeconomic losses under common-law accounting isconsistent with the greater emphasis on sharehold-er value in common-law countries.

The converse is especially relevant to doubtsabout the quality of IFRS implementation that willoccur, over time, outside of common-law coun-tries. Timelier loss recognition is less likely incountries where managers are more protected, andshareholders have a lesser role in governance, be-cause it puts unwelcome pressure on managers tofix their loss-making investments and strategies

International Accounting Policy Forum. 2006 19

30 Starting with Ball, Kothari and Robin (2000), researchershave been concerned that the estimates reported in Figure 2could differ in reliability (or bias) across countries and groups,because they rely on share price data. While Ball, Kothari andRobin (2000: 48) note several reasons to discount this con-cern, researchers have developed other tests, which corrobo-rate the price-based results. These include tests based on thetime series of reported earnings (Ball and Robin, 1999; Ball,Robin and Wu, 2003) and accruals-based tests (Ball andShivakumar, 2005; Bushman, Piotroski and Smith, 2006).

20 ACCOUNTING AND BUSINESS RESEARCH

Figure 2Timeliness of earnings historically has depended on countries’ political and economic institutions

Panel ACommon-law, Code-law and East Asia country groups

Panel BSome individual Common-law and Code-law countries

Ear

ning

s S

ensi

tivity

to

Cur

rent

Year

Gai

ns a

nd L

osse

sE

arni

ngs

Sen

sitiv

ity t

o C

urre

ntYe

ar G

ains

and

Los

ses

more quickly, and to undertake fewer negative-NPV investments in the first place. For example,timely loss recognition helps to curb managers’ ap-petites for ‘pet’ projects and ‘trophy’ acquisitionsthat are socially wasteful and not in the sharehold-ers’ interests (Ball, 2001; Ball and Shivakumar,2005). It is not surprising that loss recognitiontimeliness is lower on average in countries whereindividual shareholders are deemed less importantand managers have more latitude to pursue theirown preferences. The key implementation ques-tion is whether managers in countries whose sys-tems are less responsive to the interests ofshareholders will change their habits under IFRS,and exercise their subjective judgment to a greaterdegree in tying their own hands. I have my doubts.

China’s experience provides a more directsource of evidence on the extent of IFRS imple-mentation when it is imposed by governments,without change occurring in the fundamental eco-nomic and political factors affecting financial re-porting practice. Ball, Robin and Wu (2000) studyChina’s requirement that all domestic companieswith foreign shareholders publish financial state-ments that conform to IFRS (then known as IAS)and that are audited by an international accounting

firm. Many features of China’s institutional envi-ronment militate against high-quality financial re-porting, among them being the prevalence of‘insider’ networks, the strong political roles of theChinese government and army in the economy,and the absence of shareholder litigation rights.Ball, Robin, and Wu report that these institutionalfeatures appear to swamp the effect of mandatingIAS. When reporting under international account-ing standards, the financial statements of Chinesefirms are no more timely in reflecting economicgains or losses than when reporting under localstandards. This is shown graphically in Panel C ofFigure 2, where the sensitivities of Chinese earn-ings to contemporary economic gains and losses(i.e., estimates of gain and loss recognition timeli-ness) resemble those of other Asian countries andare substantially lower than the common-lawequivalents. China’s experience with mandatingIAS shows that it is difficult to achieve a notice-able improvement in financial reporting quality inpractice by implanting exogenously developed ac-counting standards into a complex institutional en-vironment.

Ball, Robin and Wu (2003) argue that a similaroutcome is evident in the four East Asian countries

International Accounting Policy Forum. 2006 21

Figure 2 (continued)Timeliness of earnings historically has depended on countries’ political and economic institutions

Panel CSome individual Asian countries

Sources: Ball, Kothari and Robin (2000); Ball, Robin and Wu (2000, 2003).

Ear

ning

s S

ensi

tivity

to

Cur

rent

Year

Gai

ns a

nd L

osse

s