Embed Size (px)

Citation preview

Ivo Besselink UNDP Asia-Pacific Resource Centre

ILO training 8 December

Introduction to climate change mitigation

2

• Global emissions and emission trends

• Climate Change mitigation actions and technologies

• Barriers and interventions

• Climate change negotiations

3

• Global emissions and emission trends

• Climate Change mitigation actions and technologies

• Barriers and interventions

• Climate change negotiations

44

Greenhouse gas emissions

Climate change impacts

Global Climate Change

Mitigation : reduce emissions, reduce magnitude of CC(less CO2)

Adaptationreduce vulnerability to CC impacts; reduce losses

What are we talking about?

Mitigation:Carbon sinks : forests and land use changes (CO2 sequestration)

linkages

5

Terminology

Greenhouse gases under Kyoto Protocol:– Carbon dioxide (CO2)– Methane (CH4)– Nitrous oxide (N2O)– Hydrofluorocarbons (HFCs)– Perfluorocarbons (PFCs)– Sulphur hexafluoride (SF6)

(Certified) Emission Reduction = (C)ER– 1 CER = 1 ton of CO2-eq

6

Terminology

• Some greenhouse gases are more ‘potent’. Global warming potential = ‘GWP’E.g. methane is 21 x stronger than CO2.

• Therefore:1 ton of CH4 =21 tons of CO2 = 21 tons of CO2-eq

7

• Global GHG emissions have grown since pre-industrial times. • Between 1970 and 2004 emissions have increased 70%• Broken down on sectors the growth in GHG emissions was as

follows:•Energy supply: 145%•Transport: 120%• Industry: 65%•LULUCF: 40%•Agriculture: 27%•Buildings: 26%

• The emission of GHGs have increased at different rates:• CO2 emissions represent about 77% of total anthropogenic GHGs and have grown about 80% from 1970 - 2004

Global trends in GHG emissions

8

9

GHG Emissions Projections for 2025

� Largest emitters where not included in the 1st commitment period of KP

� Developed and developing country emissions currently about equal

10

The mitigation challenge according to IPCC

• Without action - global CO 2 emissions will grow between 40 and 110% between 2000 and 2030

• To stay below 2 degrees global average warming and avoid major damages: • global CO2 emissions should start declining by

2015 and• be reduced with 50-85% below 2000 level by

2050

11

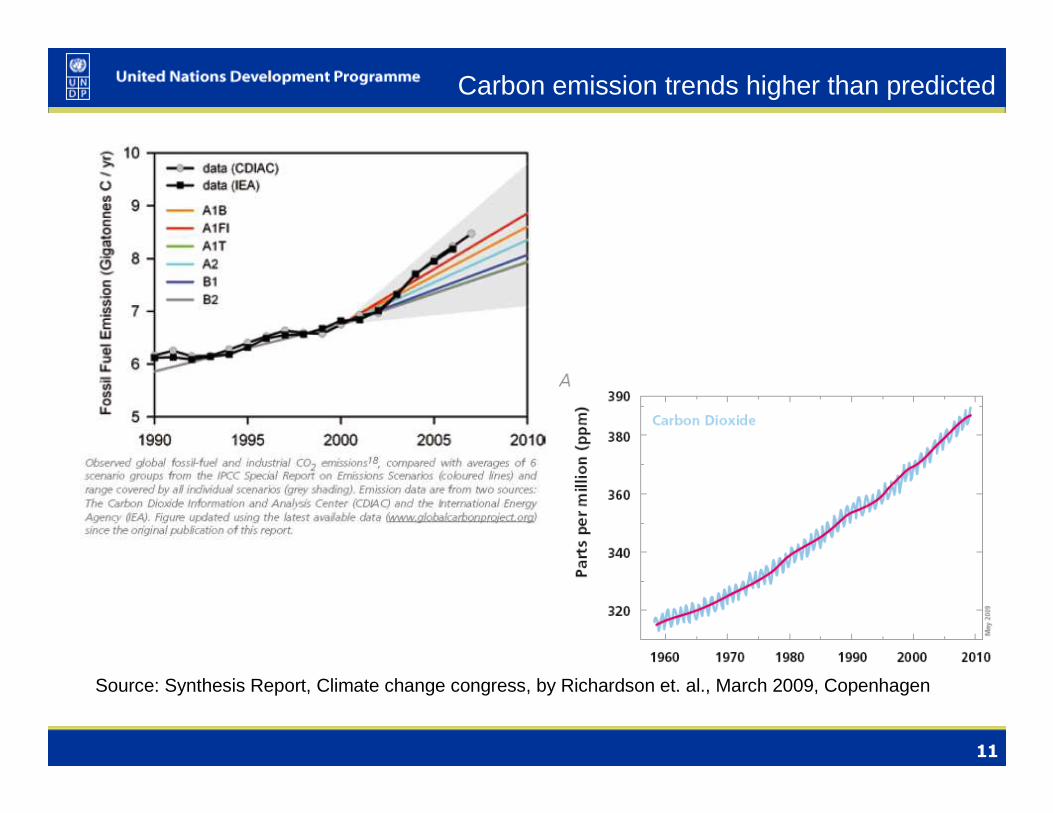

Carbon emission trends higher than predicted

Source: Synthesis Report, Climate change congress, by Richardson et. al., March 2009, Copenhagen

12

World GHG emissions – three scenarios

While energy-related CO2 will continue to dominate, there is strong potential to reduce other

emissions through improved efficiency, better farm management & reduced gas flaring

13

Impacts of 2°C warming – worse

14

• Global emissions and emission trends

• Climate Change mitigation actions and technologies

• Barriers and interventions

• Climate change negotiations

15

Methane capture lagoon

CH4CH4

Slurry as fertilizerBiogas for energy

16

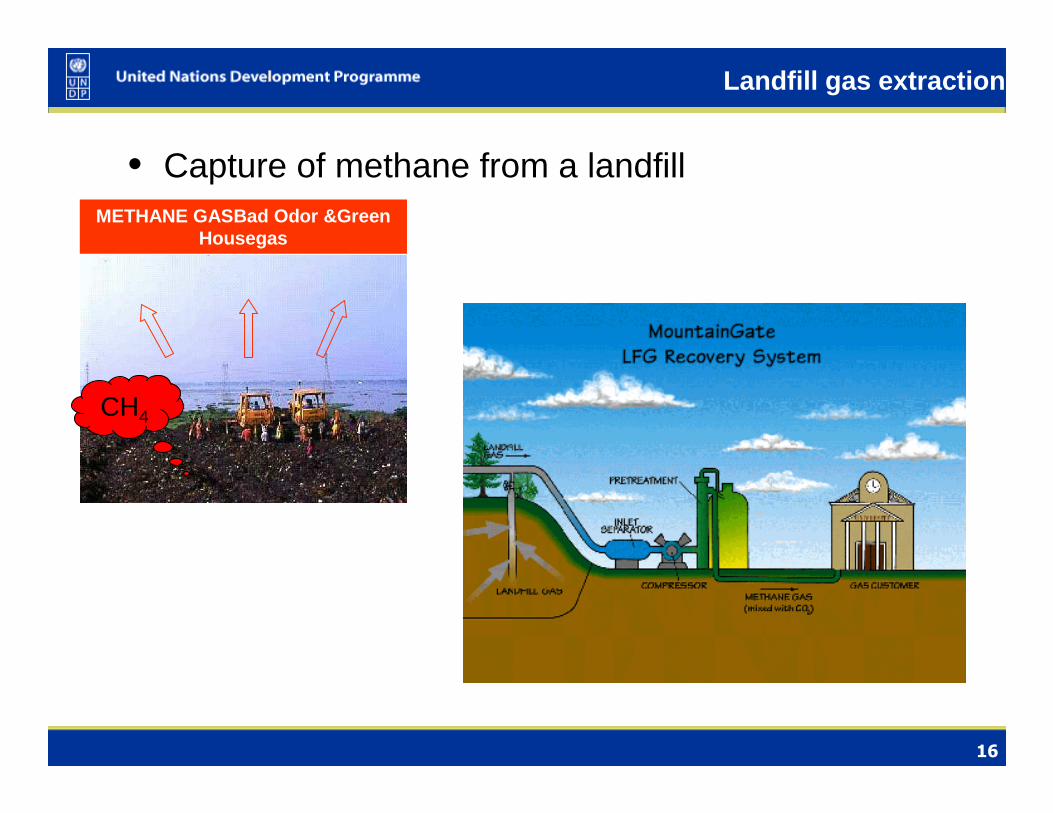

Landfill gas extraction

• Capture of methane from a landfillMETHANE GASBad Odor &Green

Housegas

CH4

17

Energy Efficiency in industries

• Savings on fossil fuel spending, e.g. factories. Biogas for heating in stead of heavy fuel oil. (e.g. brewery)

18

Renewable Energy projects (hydropower)

• Hydropower projects which replace greenhouse gas emissions (e.g. from coal fired power plants)

19

RE projects (biogas for households)

• Households using biogas in stead of kerosene, anthracite coal, firewood, etc. for cooking

Input: Animal dung (and

human faeces)

Output: bio-slurry

(fertilizer)

Output: Biogas (used for cooking and

lighting)

20

Reforestation and afforestation

• Reforestation of degraded areas (before 1990 deforested) or afforestation (already deforested more than 50 years)

21

Global mitigation cost curves

22

Examples of technologies

23

• Global emissions and emission trends

• Climate Change mitigation actions and technologies

• Barriers and interventions

• Climate change negotiations

24

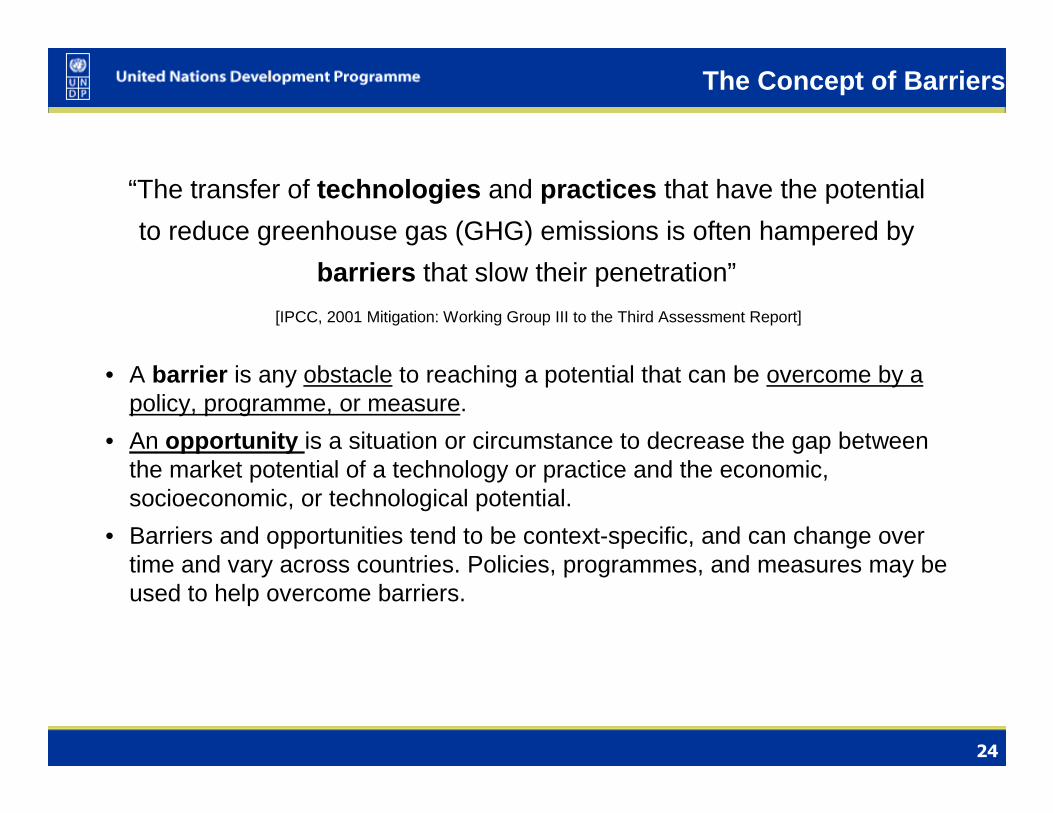

“The transfer of technologies and practices that have the potential

to reduce greenhouse gas (GHG) emissions is often hampered by

barriers that slow their penetration”

[IPCC, 2001 Mitigation: Working Group III to the Third Assessment Report]

• A barrier is any obstacle to reaching a potential that can be overcome by a policy, programme, or measure.

• An opportunity is a situation or circumstance to decrease the gap between the market potential of a technology or practice and the economic, socioeconomic, or technological potential.

• Barriers and opportunities tend to be context-specific, and can change over time and vary across countries. Policies, programmes, and measures may be used to help overcome barriers.

The Concept of Barriers

25

Source: UNFCCC (2006)

Barriers

• According to WBCST: economic and market barriers are the greatest obstacles to

climate change mitigation/technology transfer.

26

Mitigation potential and barriers

274.27

Barriers categoriesor areas…

1. prices2. financing3. trade4. market structure5. institutional frameworks6. Information provision7. social, cultural and behavioral norms and aspirations

Within each of these areas, barriers and opportunities represent:

– failures or imperfections in markets, policies, or other institutions that lie between the market potential and the possible achievement of the economic potential

– Other barriers are aspects of institutions or social and cultural systems that separate the economic and socioeconomic potentials .

Sources of Barriers and Opportunities

284.28

Opportunities for Mitigation differ by Region

• In industrialized countries, opportunities lie primarily in removing social and behavioral barriers;

• In countries with economies in transition , opportunities lie primarily in price rationalization;

• In developing countries , opportunities lie primarily in price rationalization, increased access to data and information, availability of advanced technologies, financial resources, and training and capacity building.

• NB: These three categories of countries are nothomogenous

• Opportunities for any given country might be found in the removal of any combination of barriers.

29

• Effectiveness of policies depends on national circumstances, their design, interaction, stringency and implementation

• Integrating climate policies in broader development policies • Regulations and standards • Taxes and charges • Tradable permits • Financial incentives• Voluntary agreements • Information instruments • Research and development

Institutional capacity to develop and implement policies needed

Policy options available

30

Examples

Sector Mitigation ’tools’

Energy supply • Reduction of fossil fuel subsidies• Taxes or carbon charges on fossil fuels• Feed-in-tariffs for RE technologies• RE obligations• Producer subsidies

Transport • Mandatory fuel economy• Biofuel blending • Taxes on vehicles purchase• Registration, use and motor fuels, road and parking pricing• Land use regulations and infrastructure planning to influence mobility needs• Investment in public transport and non-motorised forms of transport

31

Sector Mitigation ’tools’

Buildings • Appliance standards and labelling• Building codes and certification• Demand-side management programmes• Public sector leadership programmes including procurement• Incentives for energy service companies

Industry • Provision of benchmark information• Performance standards• Subsidies, tax credits• Tradable permits• Voluntary agreements

Examples

32

Sector Mitigation ’tools’

Agriculture • Financial incentives and regulations for improved land management• Maintaining soil carbon content• Efficient use of fertilizers and irrigation

Forestry • Financial incentives (national and international) to increase forest area and reduce deforestation and maintain and manage forests• Land use regulation and enforcement

Waste management

• Financial incentives for improved waste and wastewater management• Renewable energy incentives or obligations• Waste management regulations

Examples

333333

A Big Vision - Transforming Economies

Assessment and Policy

Setting

Build capacity for countries

to make informed and sustainable policy and investment decisions

Public and Private

Investments International

Financial Institutions

UNDP and many others

REQUIRES IMPACT ON

34

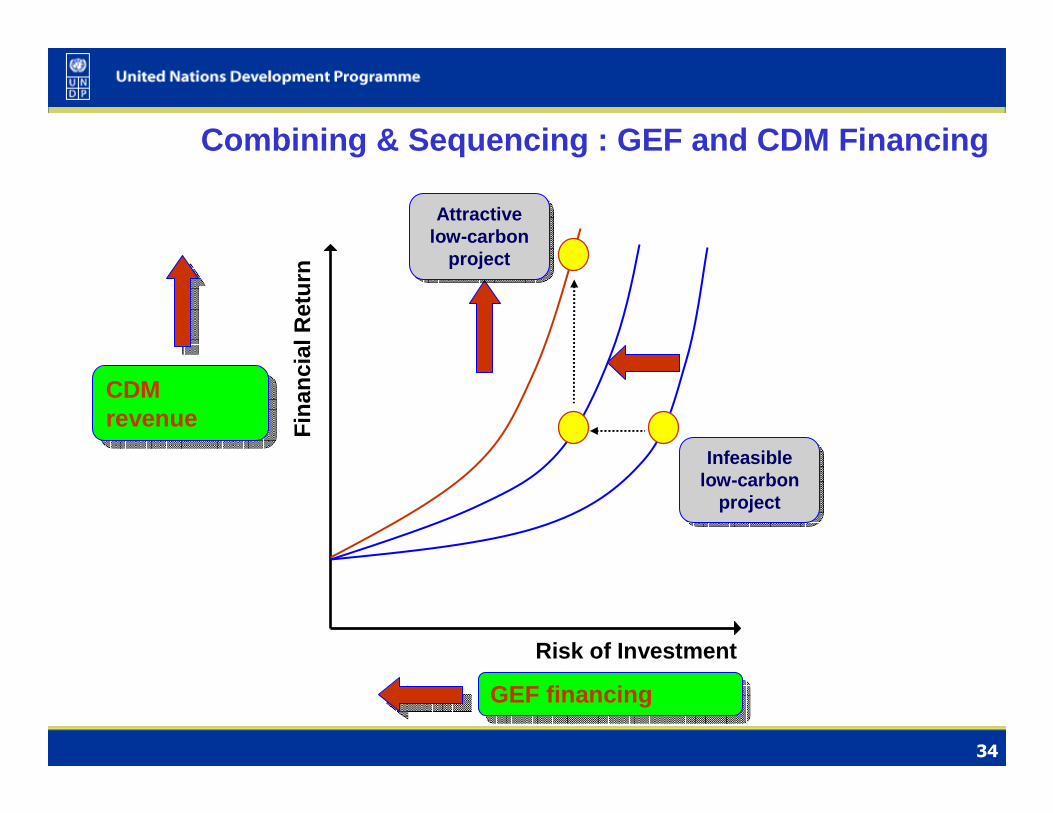

Combining & Sequencing : GEF and CDM Financing

Fin

anci

al R

etur

n

Risk of Investment

Infeasiblelow-carbon

project

Infeasiblelow-carbon

project

CDM revenue

CDM revenue

Attractivelow-carbon

project

Attractivelow-carbon

project

GEF financingGEF financing

35

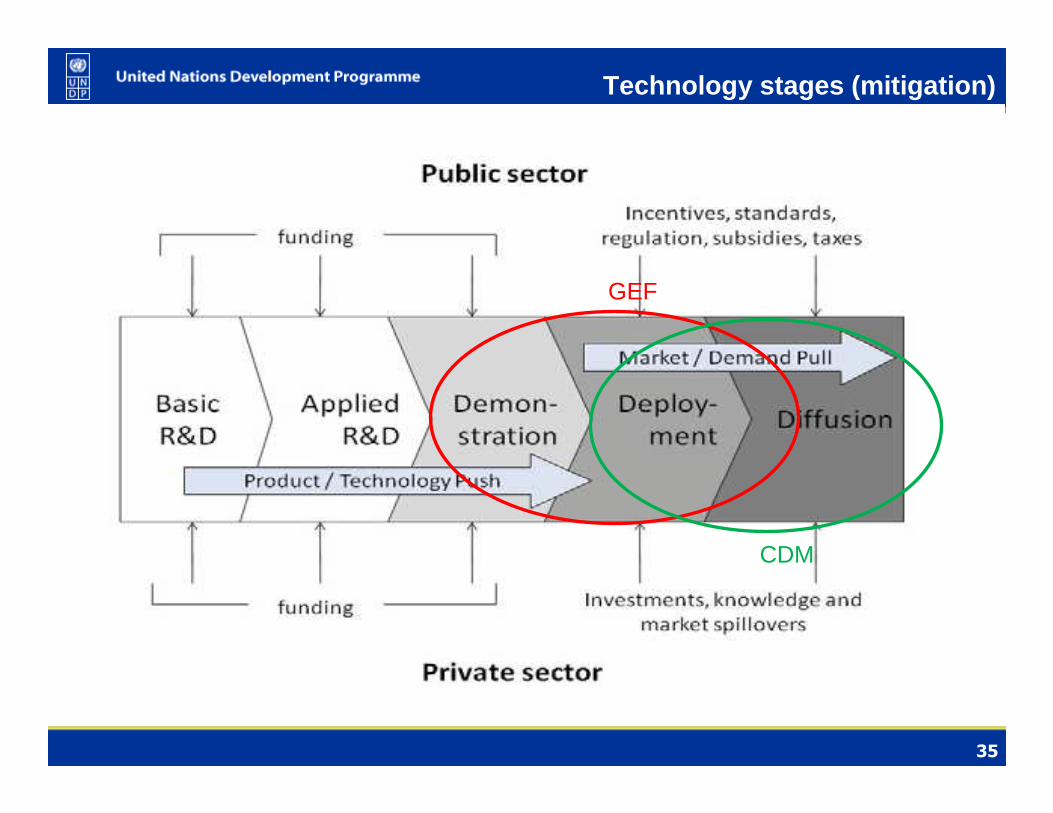

Technology stages (mitigation)

GEF

CDM

36

CDM projects in pipeline

37

GOAL: support developing countries and economies in trans ition toward a low-

carbon development path

Promote demonstration, deployment, and transferof advanced low-carbon technologies

Promote market transformation for energy efficiency in industry and buildings

Promote investment in renewable energy technologies

Promote energy efficient, low-carbon transport and urban systems

Conserve and enhance carbon stocks through sustainable management of land use, land-use change, and forestry (LULUCF)

OBJECTIVES

Enabling Activities and Capacity Building

GEF Climate Change focal Area

38

GEF ‘track’ record

• Established in 1991, over the past 18 years, the GEF has invested $8.6 billion directly and leveraged $36.1 billion in co-financing for more than 2,400 projects in more than 165 countries.

• Through its Small Grants Programme (SGP), the GEF has also made more than 12,000 small grants directly to nongovernmental and community organizations, totalling $495 million.

39

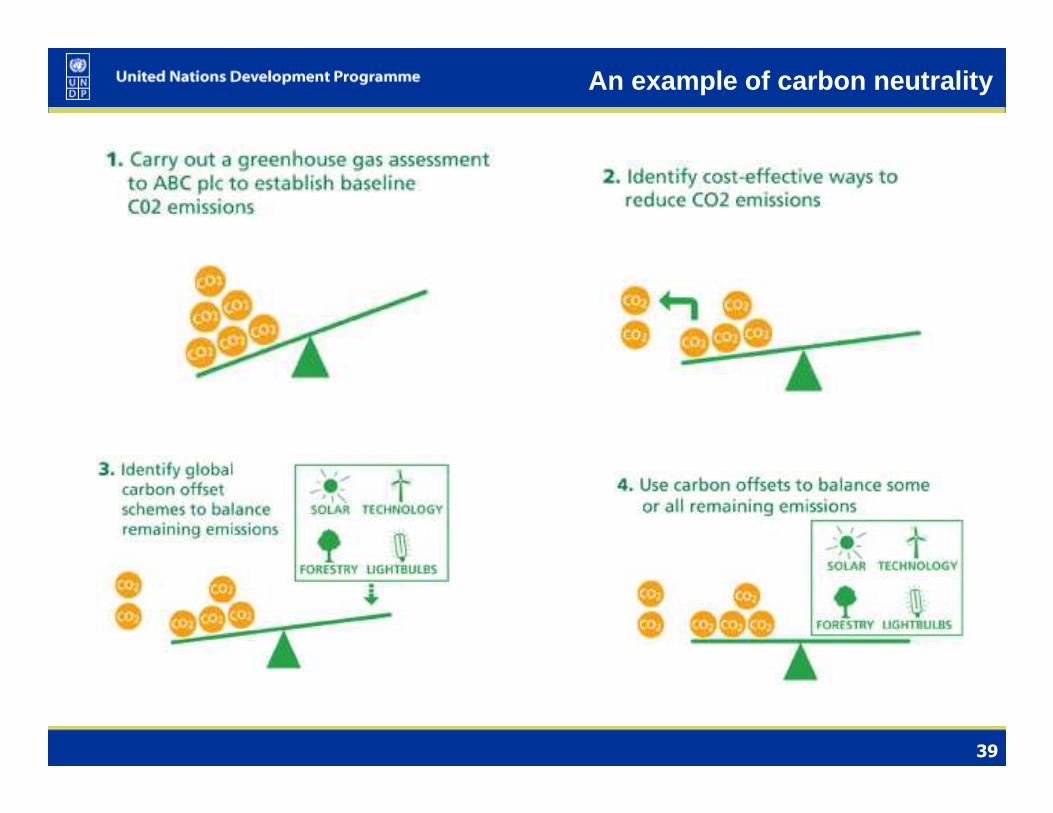

An example of carbon neutrality

40

• Global emissions and emission trends

• Climate Change mitigation actions and technologies

• Barriers and interventions

• Climate change negotiations

41

Mitigation in Developing Countries

Main sticking point of the negotiations

Agreement:• Developing countries will develop low emission development strategies

that include NAMAs (National Appropriate Mitigation Actions)• Developed countries will provide financing, capacity building and

technology for some NAMAs• LDCs and SIDS will be exempt from undertaking unsupported NAMAs

Disagreement• Supported NAMAs be internationally recorded in a registry, and their

implementation monitored, reviewed, and verified (MRV)• Unsupported NAMAs may be subject to International Consultation and

Analysis (ICA)• Annex I in favour of these options; G77 (mainly large developing countries)

opposed

42

Technology Development and

TransferCancun decision likely to establish a Technology Mechanism• This will handle technology finance from the mitigation and adaptation windows of

the new fund

3 key elements:

1. Technology Executive Committee (similar to Adaptation Committee)• Replace the Expert Group on Technology Transfer and provide oversight

and monitoring

2. Climate Technology Centre with regional units• Development of Technology Action Plans, as well as providing capacity

development (national planning, policy advice, etc) to government. • Facilitate knowledge sharing and South-South collaboration • Act as a matching entity between developing countries and the network

3. Climate Technology Network• In-country network of companies, multilaterals, NGOs, academic institutions,

and R&D institutions that provide transfer, development and deployment of technology at the national level (e.g. incubation services, seed finance)