Embed Size (px)

Citation preview

Impact of non-tariff measures on sea food industry and its potential implication for

sustainable development goals

Case of the EU export ban on Sri Lankan seafood industry

K.P.G. Lahiru Sandaruwan, Dr. Senal Weerasooriya and Prof. JeewikaWeerahewa

University of PeradeniyaSri Lanka

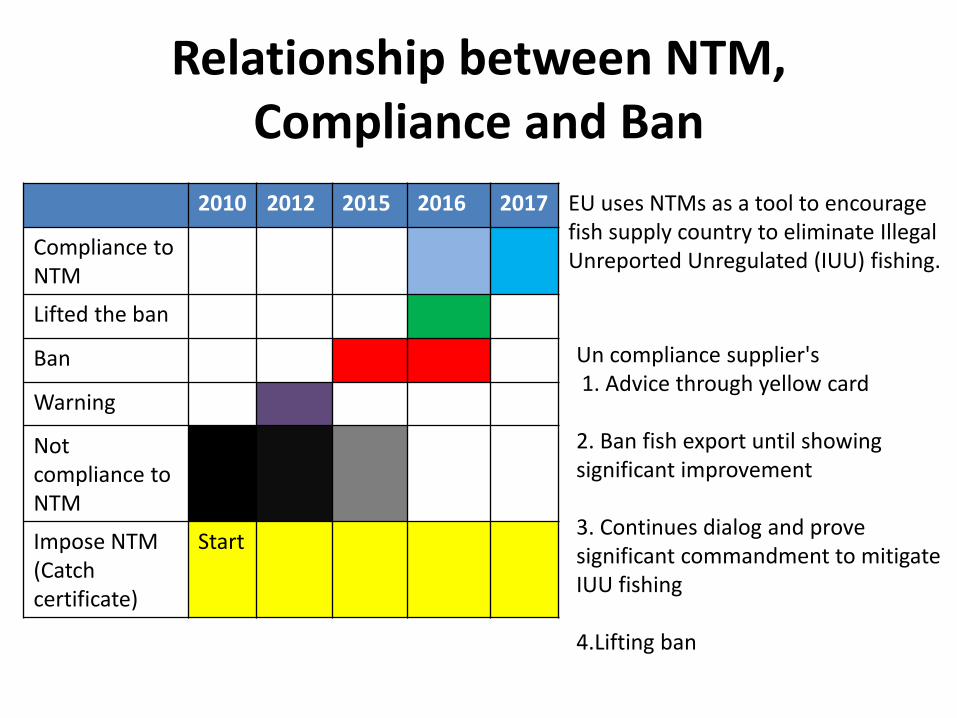

Relationship between NTM, Compliance and Ban

2010 2012 2015 2016 2017

Compliance to NTM

Lifted the ban

Ban

Warning

Not compliance to NTM

Impose NTM (Catchcertificate)

Start

EU uses NTMs as a tool to encourage fish supply country to eliminate Illegal Unreported Unregulated (IUU) fishing.

Un compliance supplier's1. Advice through yellow card

2. Ban fish export until showing significant improvement

3. Continues dialog and prove significant commandment to mitigate IUU fishing

4.Lifting ban

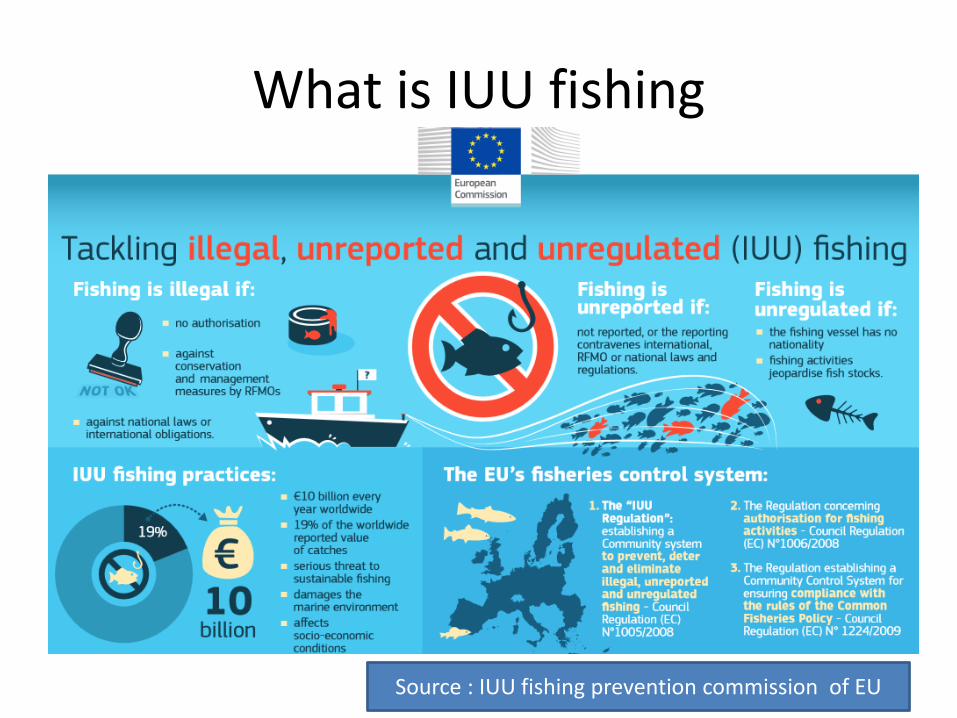

What is IUU fishing

Source : IUU fishing prevention commission of EU

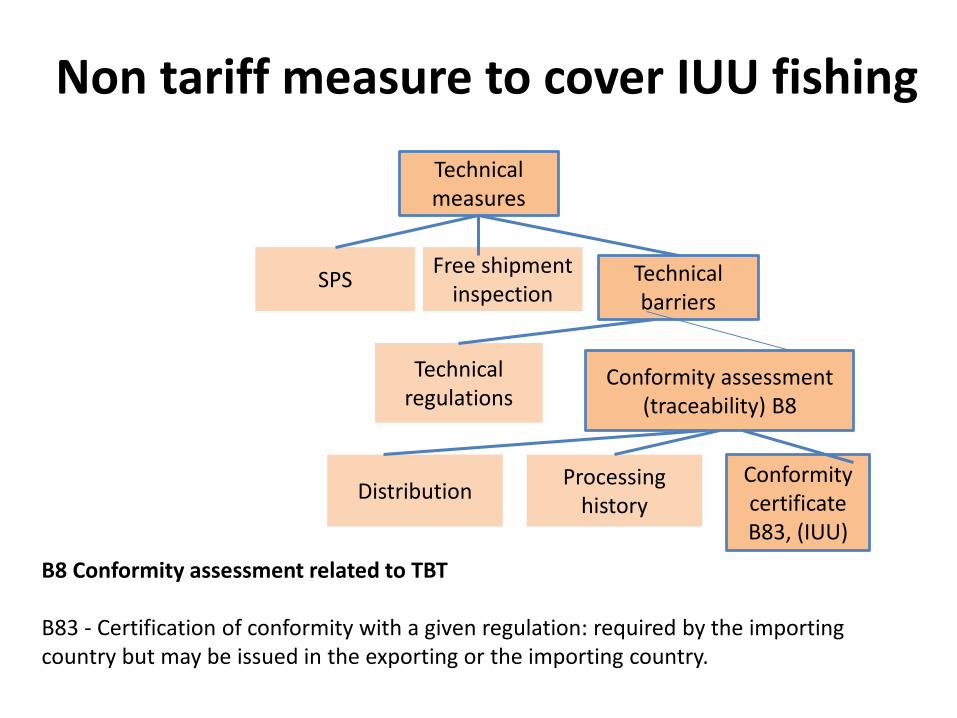

Technical measures

Technical barriers

Free shipment inspection

SPS

Technical regulations

Conformity assessment (traceability) B8

DistributionProcessing

history

Conformity certificate B83, (IUU)

Non tariff measure to cover IUU fishing

B8 Conformity assessment related to TBT

B83 - Certification of conformity with a given regulation: required by the importing country but may be issued in the exporting or the importing country.

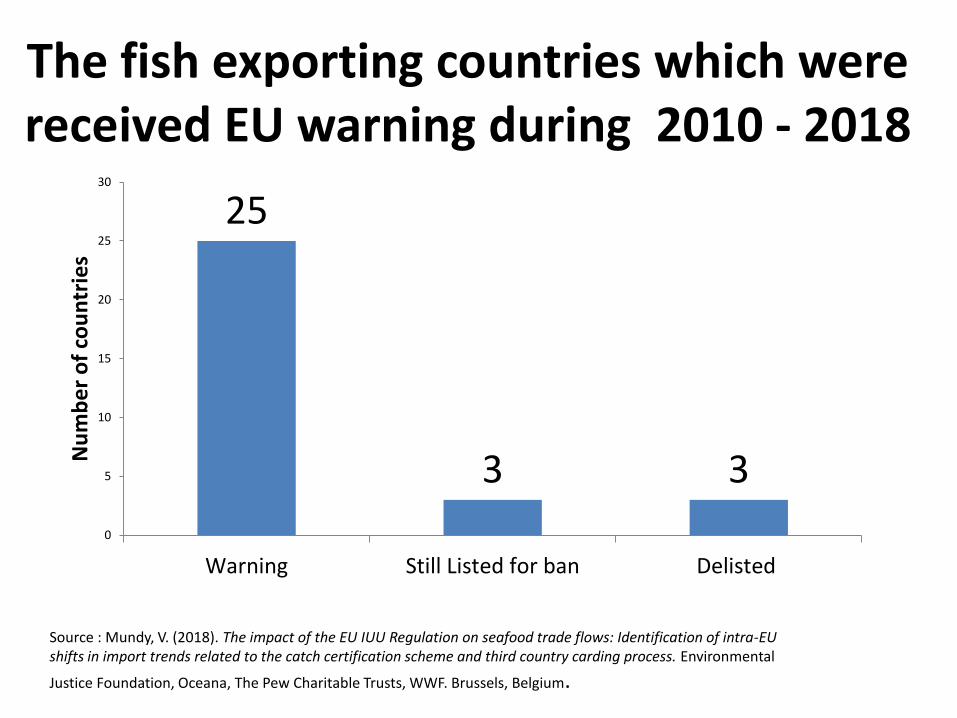

The fish exporting countries which were received EU warning during 2010 - 2018

25

3 3

0

5

10

15

20

25

30

Warning Still Listed for ban Delisted

Nu

mb

er

of

cou

ntr

ies

Source : Mundy, V. (2018). The impact of the EU IUU Regulation on seafood trade flows: Identification of intra-EU shifts in import trends related to the catch certification scheme and third country carding process. Environmental

Justice Foundation, Oceana, The Pew Charitable Trusts, WWF. Brussels, Belgium.

Relationship between NTM and SDG

• In the sustainable development process a country should maintain dynamic equilibrium among development aspects.

• When change policy (eg:- NTM) this equilibrium change and social, economic and environment structures shift towards new equilibrium.

• This policy changes may have synergetic or/and trade- off spill over effect of SDG

• To understand how non-tariff measures interact with sustainable development, it is helpful to distinguish between indirect and direct linkages.

• Challenge is how identify the possible linkages and who that effect measure ?

Objectives of the istudy

• To explore the performance of fish product export industry of Sri Lanka before, during and after the EU ban

• To study the producer level response for the EU ban

• To develop indicators and measure the impact of fish export ban and remedial measures taken to lift the ban on SDG of stake holders of the industry

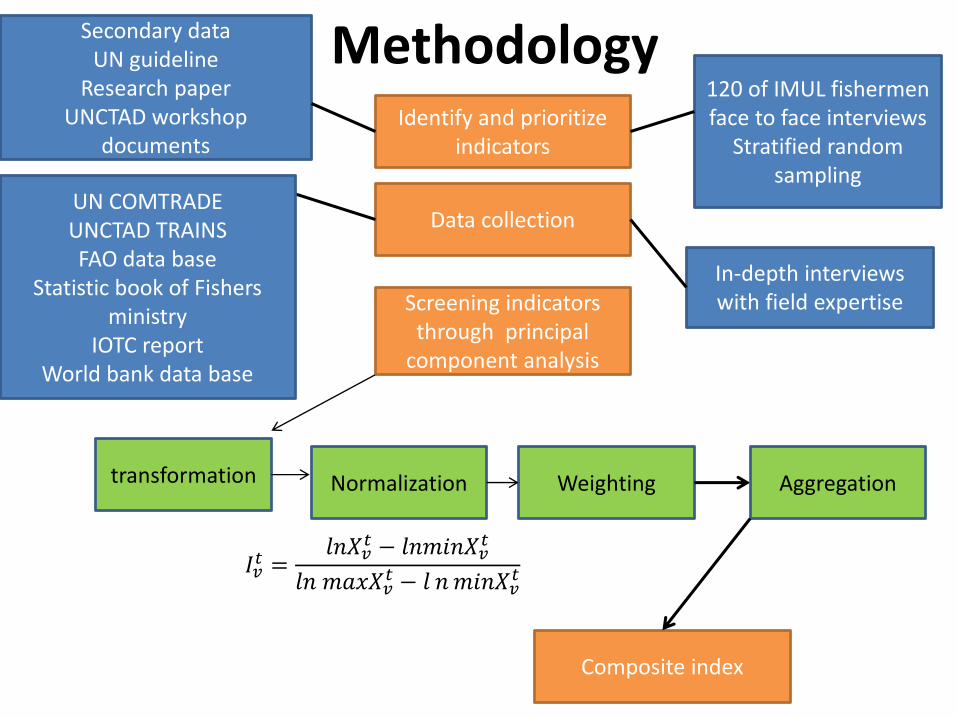

Methodology Identify and prioritize

indicators

Secondary dataUN guideline

Research paperUNCTAD workshop

documents

In-depth interviews with field expertise

Data collection

120 of IMUL fishermen face to face interviews

Stratified random sampling

Composite index

Screening indicators through principal

component analysis

transformation Weighting

𝐼𝑣𝑡 =

𝑙𝑛𝑋𝑣𝑡 − 𝑙𝑛𝑚𝑖𝑛𝑋𝑣

𝑡

𝑙𝑛 𝑚𝑎𝑥𝑋𝑣𝑡 − 𝑙 𝑛𝑚𝑖𝑛𝑋𝑣

𝑡

AggregationNormalization

UN COMTRADEUNCTAD TRAINSFAO data base

Statistic book of Fishers ministry

IOTC reportWorld bank data base

Impact on fish trade

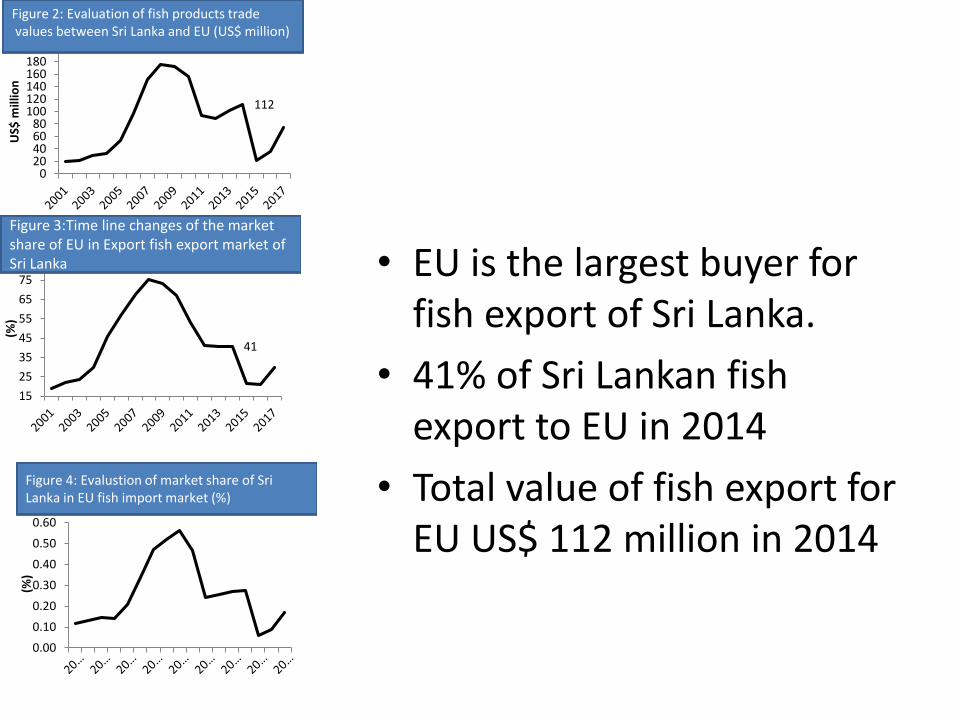

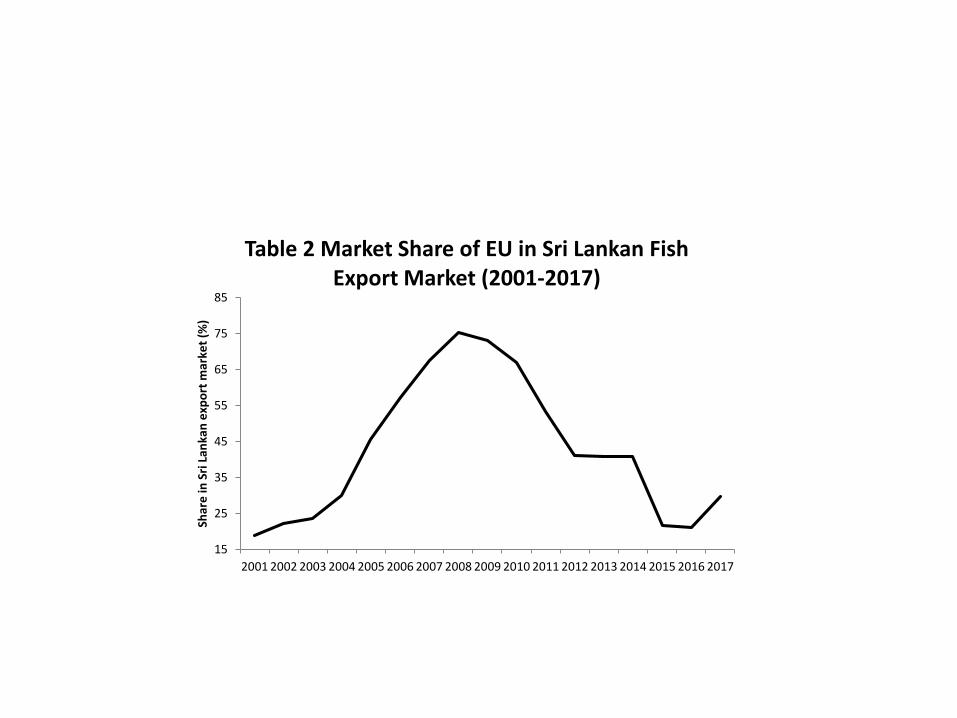

• EU is the largest buyer for fish export of Sri Lanka.

• 41% of Sri Lankan fish export to EU in 2014

• Total value of fish export for EU US$ 112 million in 2014

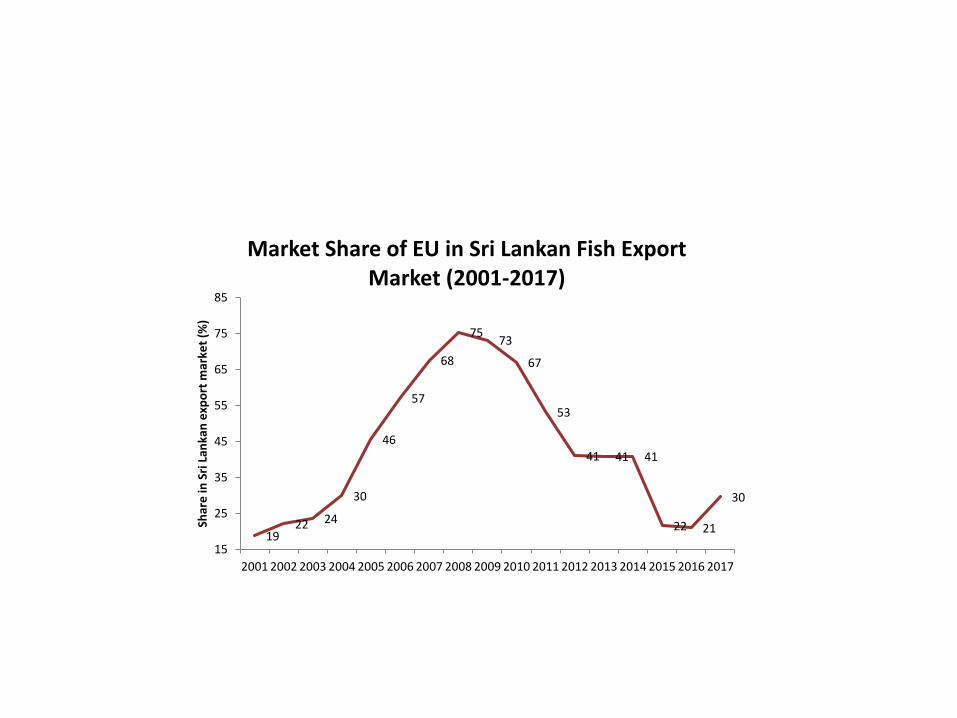

41

15

25

35

45

55

65

75

85

(%)

Figure 3:Time line changes of the market share of EU in Export fish export market of Sri Lanka

112

020406080

100120140160180200

US$

mill

ion

Figure 2: Evaluation of fish products tradevalues between Sri Lanka and EU (US$ million)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

(%)

Figure 4: Evalustion of market share of Sri Lanka in EU fish import market (%)

Market performance

HERFINDAHL-HIRSCHMAN PRODUCT CONCENTRATION INDEX

0.00

0.05

0.10

0.15

0.20

0.25

0.30

HH

ind

ex

𝐻𝑖 =

σ𝑖=1𝑛 𝑋𝑖,𝑑,𝑡

𝑋𝑑,𝑡

2

− 1/𝑛𝑡

1 − ൗ1 𝑛𝑡

2

2.5

3

3.5

4

4.5

5

RC

A

-40

-30

-20

-10

0

10

20

30

40

50

Gro

wth

𝐺𝑟𝑜 =𝑋𝑑𝑡

𝑋𝑑,𝑖𝑡0

1/ 𝑡−𝑡0

− 1 ∗ 100

𝑅𝐶𝐴𝑑,𝑖,𝑡 = ൚

𝑋𝑑,𝑖,𝑡𝑋𝑑,𝑡

𝑋𝑤,𝑖,𝑡𝑋𝑤,𝑡

Table 5: Top 10 Export destination of Sri Lanka

Country 2012 2013 2014 2015 2016 2017

EU 1 1 2 2 2 1

USA 3 2 1 1 1 2

Japan 2 3 3 3 3 3

Hong Kong, China 4 5 6 6 6 6

Taipei, Chinese 6 4 5 5 5 7

Canada 5 6 4 4 4 4

Viet Nam 9 7 8 7 7 5

Saudi Arabia 8 8

Israel 8 9 10 9 9

United Arab Emirates 9 8 10 10

Singapore 7 8 7 9

Thailand 10 10 10

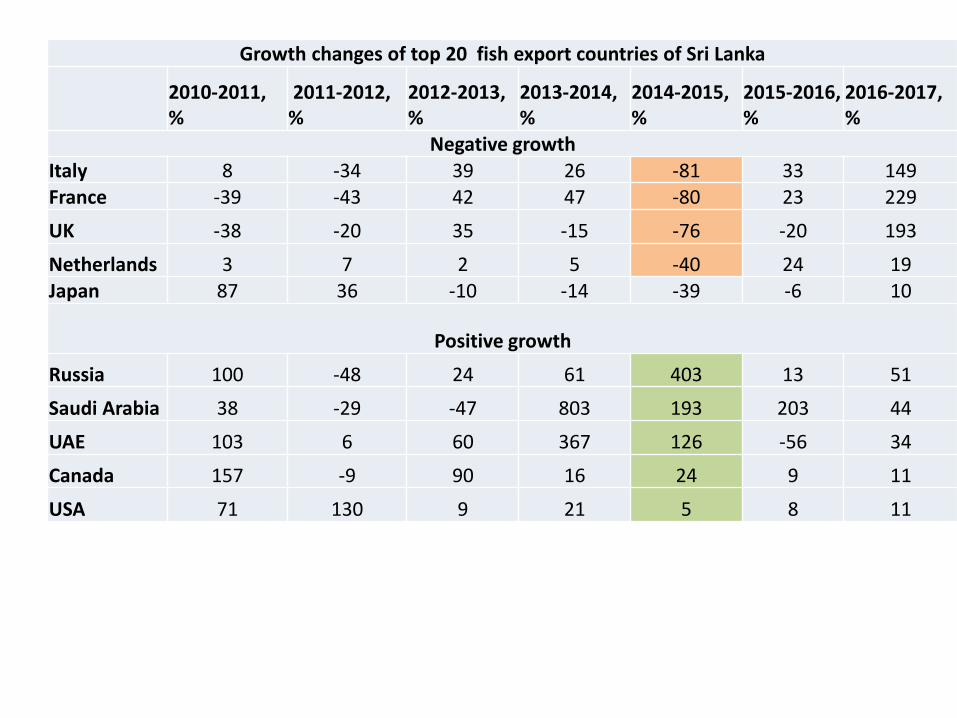

Growth changes of top 20 fish export countries of Sri Lanka

2010-2011, %

2011-2012, %

2012-2013, %

2013-2014, %

2014-2015, %

2015-2016, %

2016-2017, %

Negative growth Italy 8 -34 39 26 -81 33 149France -39 -43 42 47 -80 23 229

UK -38 -20 35 -15 -76 -20 193

Netherlands 3 7 2 5 -40 24 19Japan 87 36 -10 -14 -39 -6 10

Positive growth

Russia 100 -48 24 61 403 13 51

Saudi Arabia 38 -29 -47 803 193 203 44

UAE 103 6 60 367 126 -56 34

Canada 157 -9 90 16 24 9 11

USA 71 130 9 21 5 8 11

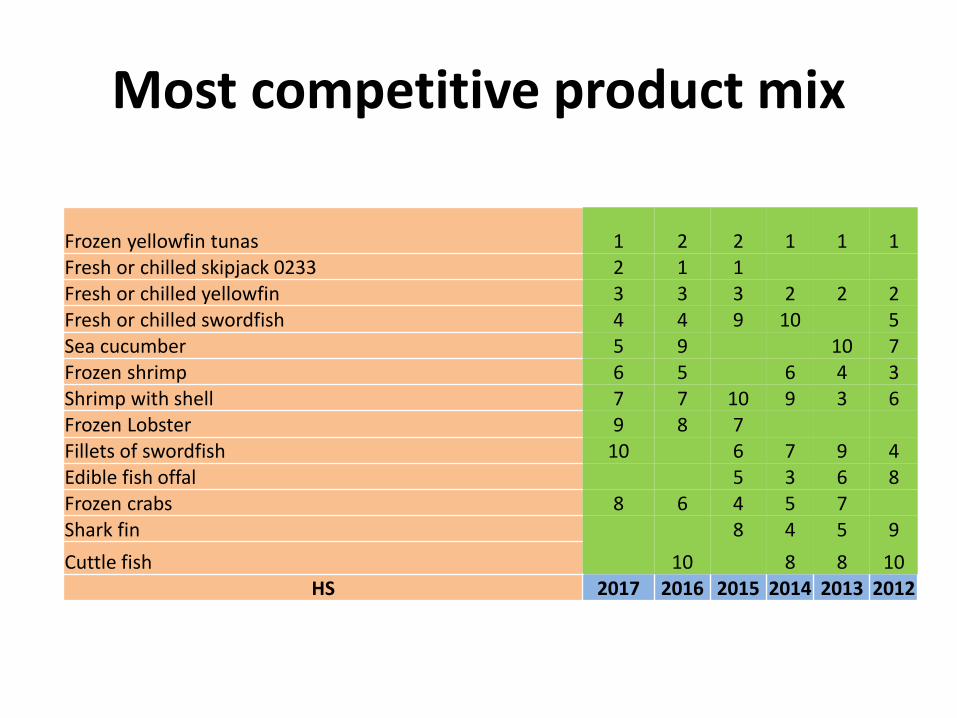

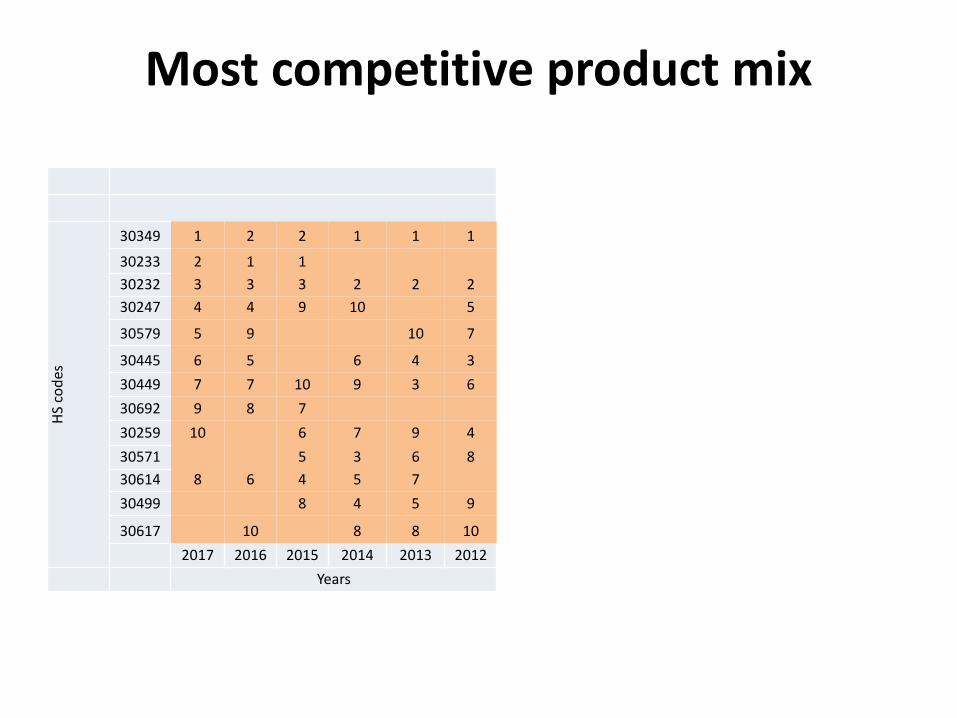

Most competitive product mix

Frozen yellowfin tunas 1 2 2 1 1 1Fresh or chilled skipjack 0233 2 1 1Fresh or chilled yellowfin 3 3 3 2 2 2Fresh or chilled swordfish 4 4 9 10 5Sea cucumber 5 9 10 7Frozen shrimp 6 5 6 4 3Shrimp with shell 7 7 10 9 3 6Frozen Lobster 9 8 7Fillets of swordfish 10 6 7 9 4Edible fish offal 5 3 6 8Frozen crabs 8 6 4 5 7Shark fin 8 4 5 9

Cuttle fish 10 8 8 10HS 2017 2016 2015 2014 2013 2012

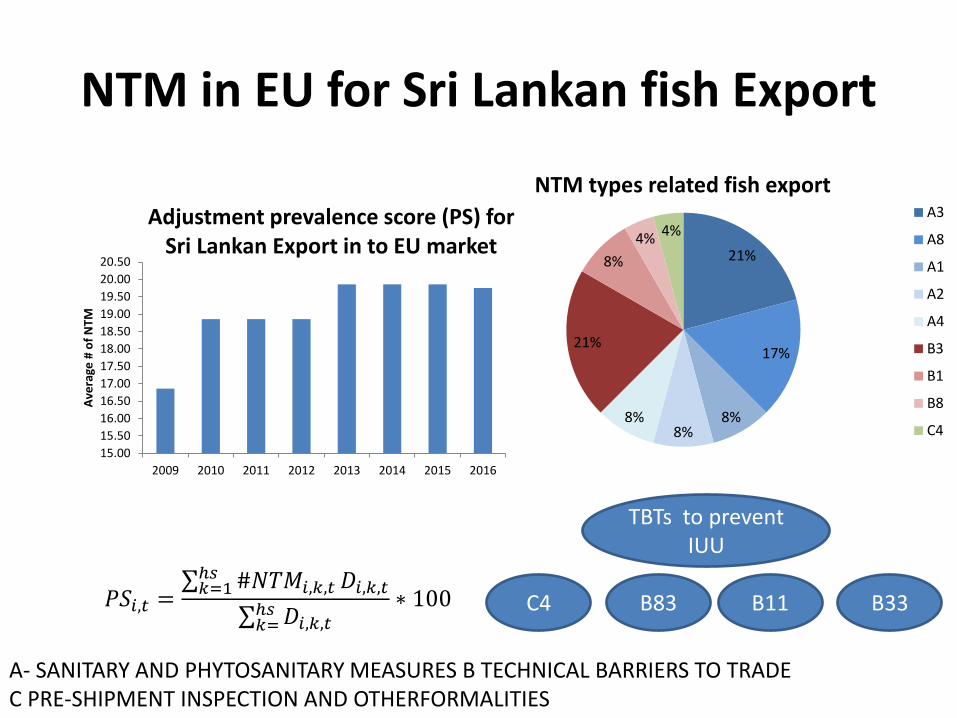

NTM in EU for Sri Lankan fish Export

21%

17%

8%8%

8%

21%

8%

4% 4%

NTM types related fish export A3

A8

A1

A2

A4

B3

B1

B8

C4

𝑃𝑆𝑖,𝑡 =σ𝑘=1ℎ𝑠 #𝑁𝑇𝑀𝑖,𝑘,𝑡 𝐷𝑖,𝑘,𝑡

σ𝑘=ℎ𝑠 𝐷𝑖,𝑘,𝑡

∗ 100

15.00

15.50

16.00

16.50

17.00

17.50

18.00

18.50

19.00

19.50

20.00

20.50

2009 2010 2011 2012 2013 2014 2015 2016

Ave

rage

# o

f N

TM

Adjustment prevalence score (PS) for Sri Lankan Export in to EU market

TBTs to prevent IUU

C4 B83 B11 B33

A- SANITARY AND PHYTOSANITARY MEASURES B TECHNICAL BARRIERS TO TRADEC PRE-SHIPMENT INSPECTION AND OTHERFORMALITIES

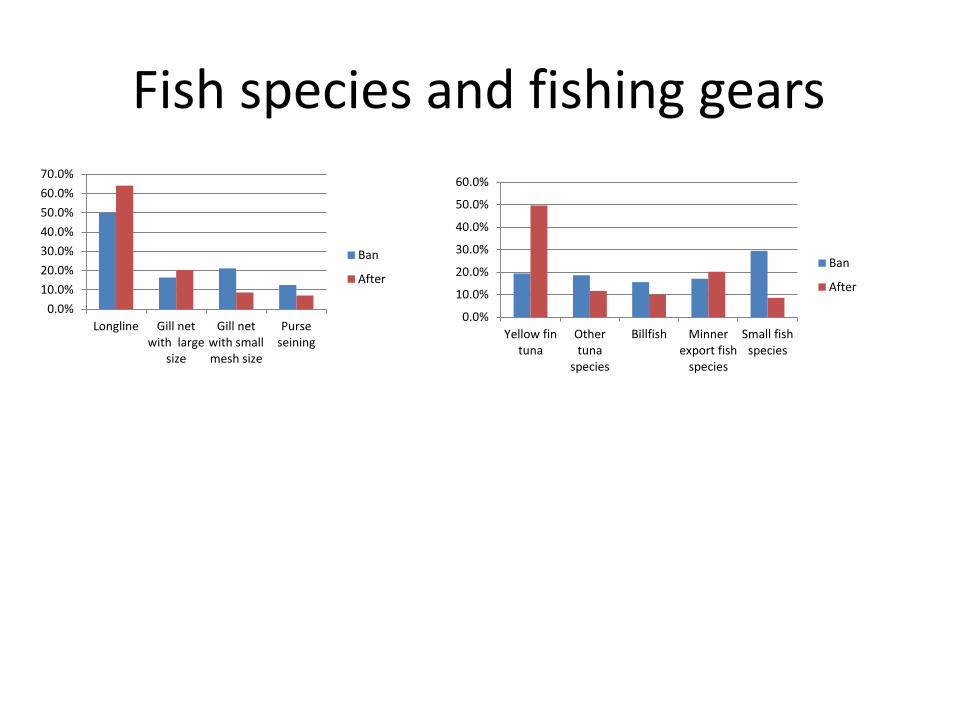

Producer level response for the ban

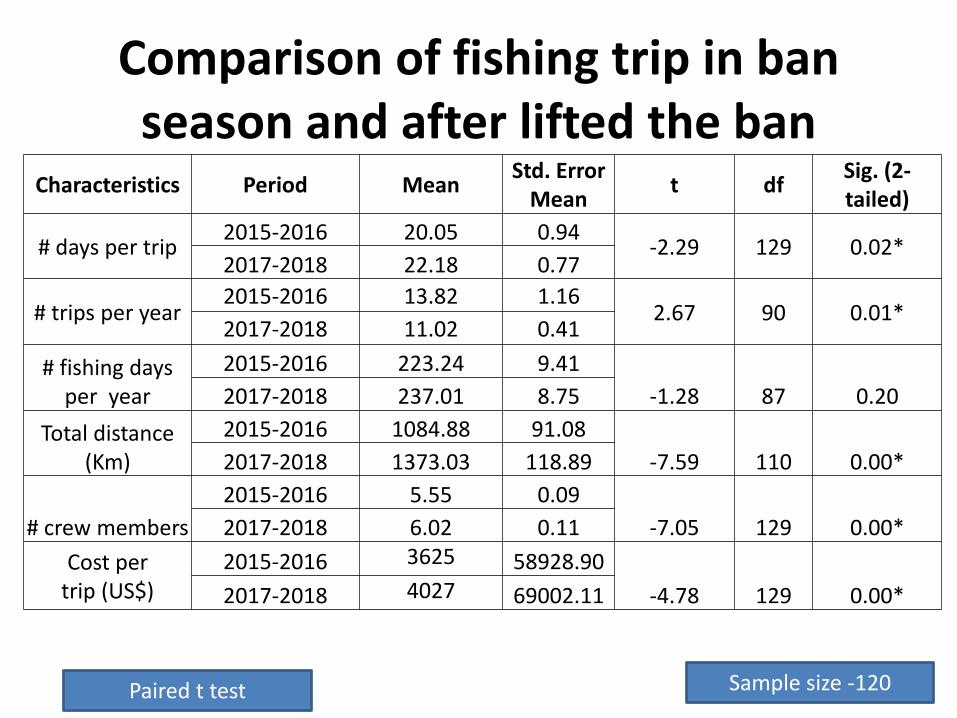

Comparison of fishing trip in ban season and after lifted the ban

Paired t test

Characteristics Period MeanStd. Error

Meant df

Sig. (2-tailed)

# days per trip2015-2016 20.05 0.94

-2.29 129 0.02*2017-2018 22.18 0.77

# trips per year2015-2016 13.82 1.16

2.67 90 0.01*2017-2018 11.02 0.41

# fishing days per year

2015-2016 223.24 9.41

-1.28 87 0.202017-2018 237.01 8.75

Total distance (Km)

2015-2016 1084.88 91.08

-7.59 110 0.00*2017-2018 1373.03 118.89

# crew members

2015-2016 5.55 0.09

-7.05 129 0.00*2017-2018 6.02 0.11

Cost per trip (US$)

2015-2016 3625 58928.90

-4.78 129 0.00*2017-2018 4027 69002.11

Sample size -120

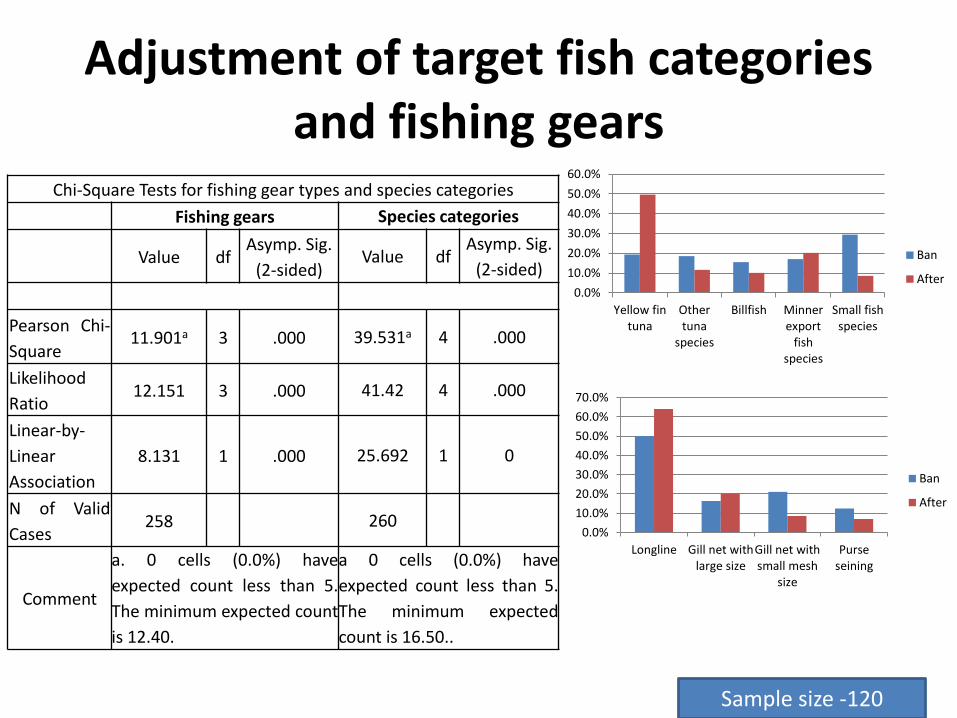

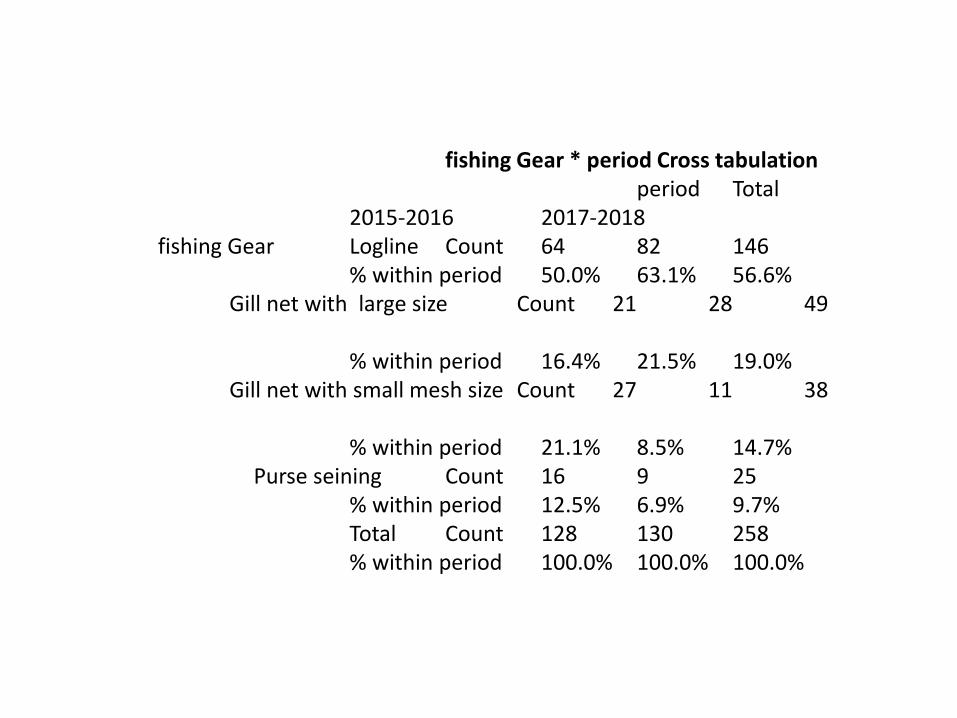

Adjustment of target fish categories and fishing gears

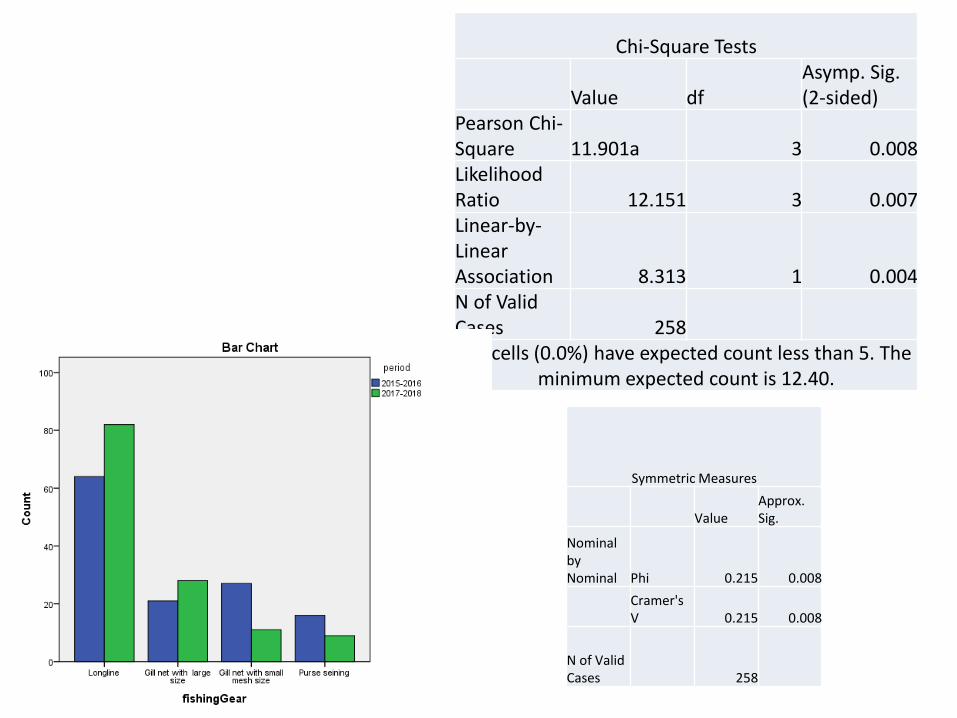

Chi-Square Tests for fishing gear types and species categories

Fishing gears Species categories

Value dfAsymp. Sig.

(2-sided)Value df

Asymp. Sig.

(2-sided)

Pearson Chi-

Square11.901a 3 .000 39.531a 4 .000

Likelihood

Ratio12.151 3 .000 41.42 4 .000

Linear-by-

Linear

Association

8.131 1 .000 25.692 1 0

N of Valid

Cases258 260

Comment

a. 0 cells (0.0%) have

expected count less than 5.

The minimum expected count

is 12.40.

a 0 cells (0.0%) have

expected count less than 5.

The minimum expected

count is 16.50..

Sample size -120

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Longline Gill net withlarge size

Gill net withsmall mesh

size

Purseseining

Ban

After

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Yellow fintuna

Othertuna

species

Billfish Minnerexport

fishspecies

Small fishspecies

Ban

After

Impact on SDG

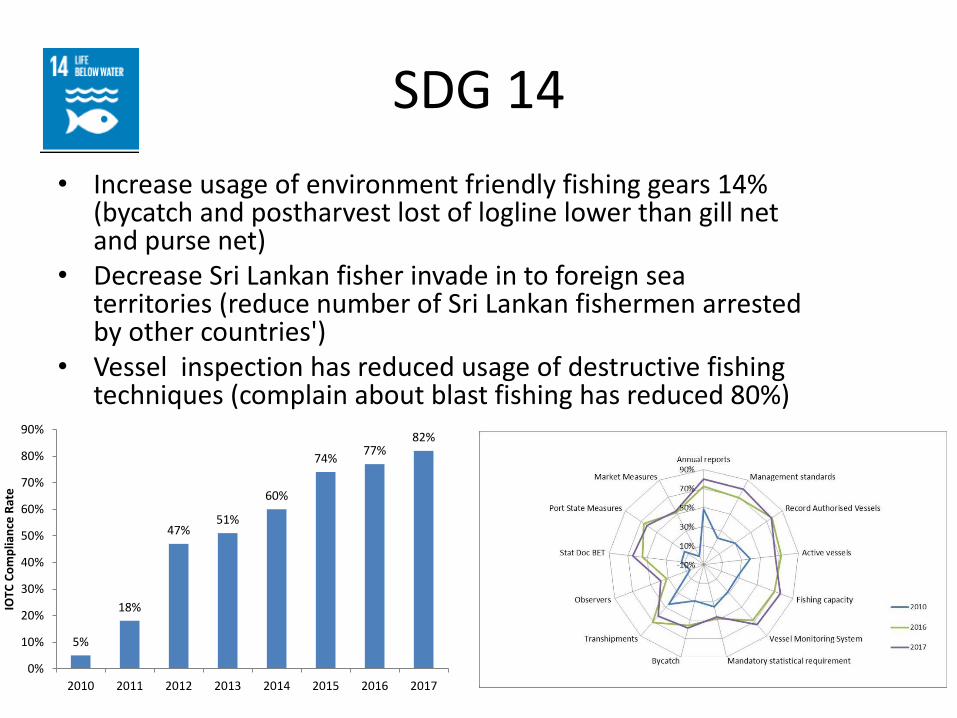

SDG 14

• Increase usage of environment friendly fishing gears 14% (bycatch and postharvest lost of logline lower than gill net and purse net)

• Decrease Sri Lankan fisher invade in to foreign sea territories (reduce number of Sri Lankan fishermen arrested by other countries')

• Vessel inspection has reduced usage of destructive fishing techniques (complain about blast fishing has reduced 80%)

5%

18%

47%51%

60%

74%77%

82%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2010 2011 2012 2013 2014 2015 2016 2017

IOTC

Co

mp

lian

ce R

ate

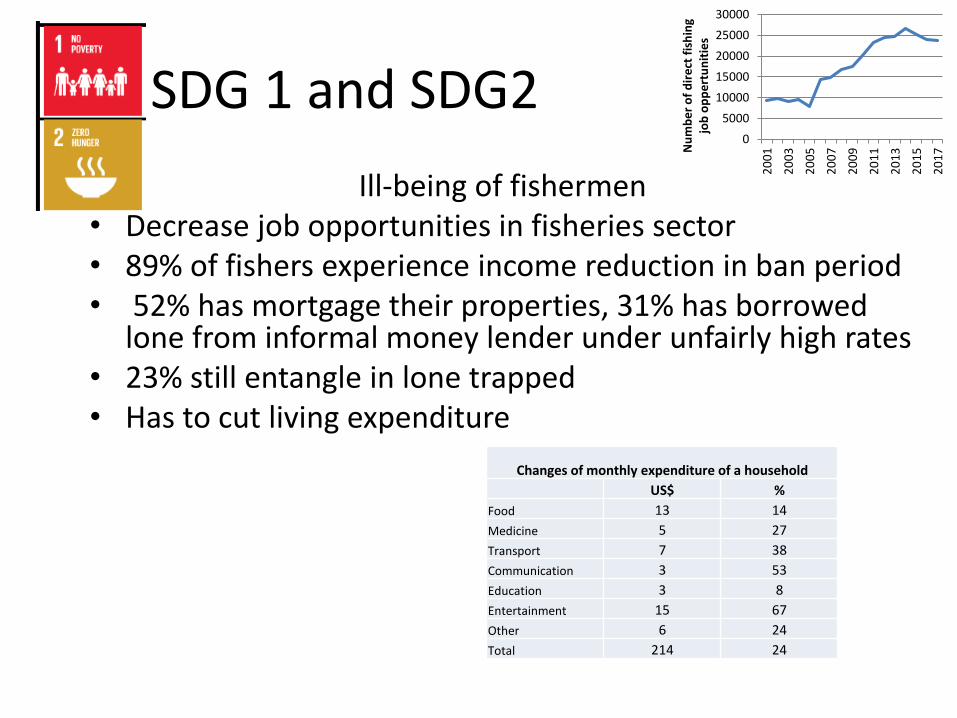

SDG 1 and SDG2

Ill-being of fishermen• Decrease job opportunities in fisheries sector• 89% of fishers experience income reduction in ban period • 52% has mortgage their properties, 31% has borrowed

lone from informal money lender under unfairly high rates • 23% still entangle in lone trapped • Has to cut living expenditure

0

5000

10000

15000

20000

25000

30000

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17N

um

be

r o

f d

ire

ct f

ish

ing

job

op

pe

rtu

nit

ies

Changes of monthly expenditure of a household

US$ %

Food 13 14

Medicine 5 27

Transport 7 38

Communication 3 53

Education 3 8

Entertainment 15 67

Other 6 24

Total 214 24

SDG 12 and 2

• Consumer has opportunity to know origin of their fish food

• Per capita fish consumption of local consumer increased – Fish is the main animal protein for Sri Lankan poor

communities. During ban period they had opportunity buy fish under affordable price

– Take away catch (free of charge fish for crew members) is increased and it may cause to increase fish consumption in fishing community

SDG 9

• VMS and Digital, log book and web portal harness conventional fisheries sector with modern IT

• VMS detect the position of the boat and it help to request help in accident

• As a part of IOTC compliance government has improved facilities in fisheries harbors and provided loan to upgrade the facilities of fishing boats.

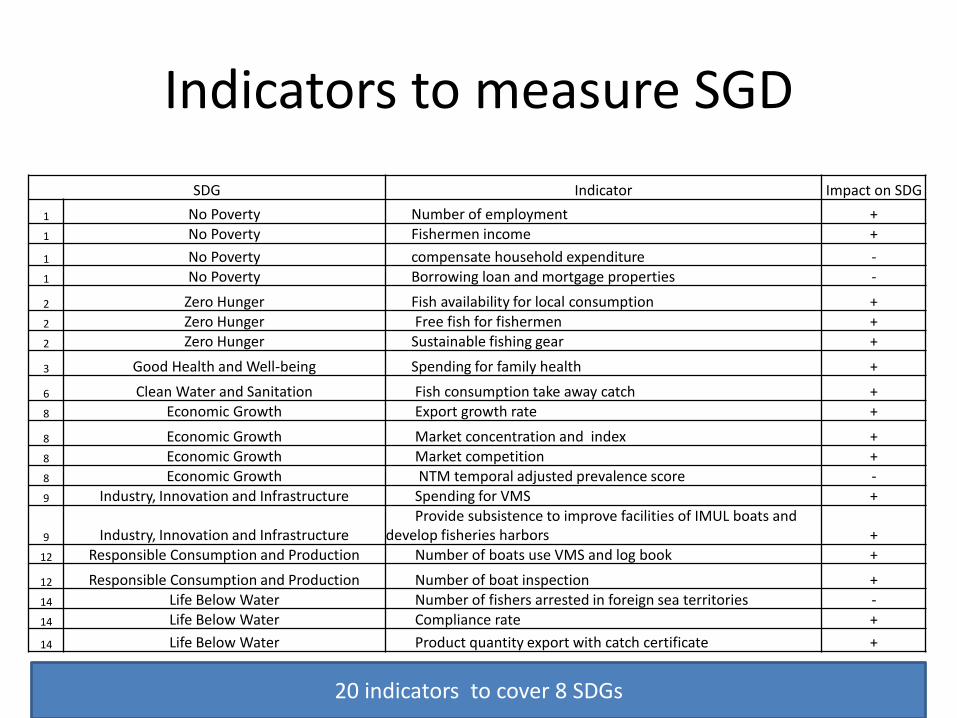

Indicators to measure SGD

SDG Indicator Impact on SDG

1 No Poverty Number of employment +

1 No Poverty Fishermen income +

1 No Poverty compensate household expenditure -

1 No Poverty Borrowing loan and mortgage properties -

2 Zero Hunger Fish availability for local consumption +

2 Zero Hunger Free fish for fishermen +

2 Zero Hunger Sustainable fishing gear +

3 Good Health and Well-being Spending for family health +

6 Clean Water and Sanitation Fish consumption take away catch +

8 Economic Growth Export growth rate +

8 Economic Growth Market concentration and index +

8 Economic Growth Market competition +

8 Economic Growth NTM temporal adjusted prevalence score -

9 Industry, Innovation and Infrastructure Spending for VMS +

9 Industry, Innovation and InfrastructureProvide subsistence to improve facilities of IMUL boats and

develop fisheries harbors +

12 Responsible Consumption and Production Number of boats use VMS and log book +

12 Responsible Consumption and Production Number of boat inspection +

14 Life Below Water Number of fishers arrested in foreign sea territories -

14 Life Below Water Compliance rate +

14 Life Below Water Product quantity export with catch certificate +

20 indicators to cover 8 SDGs

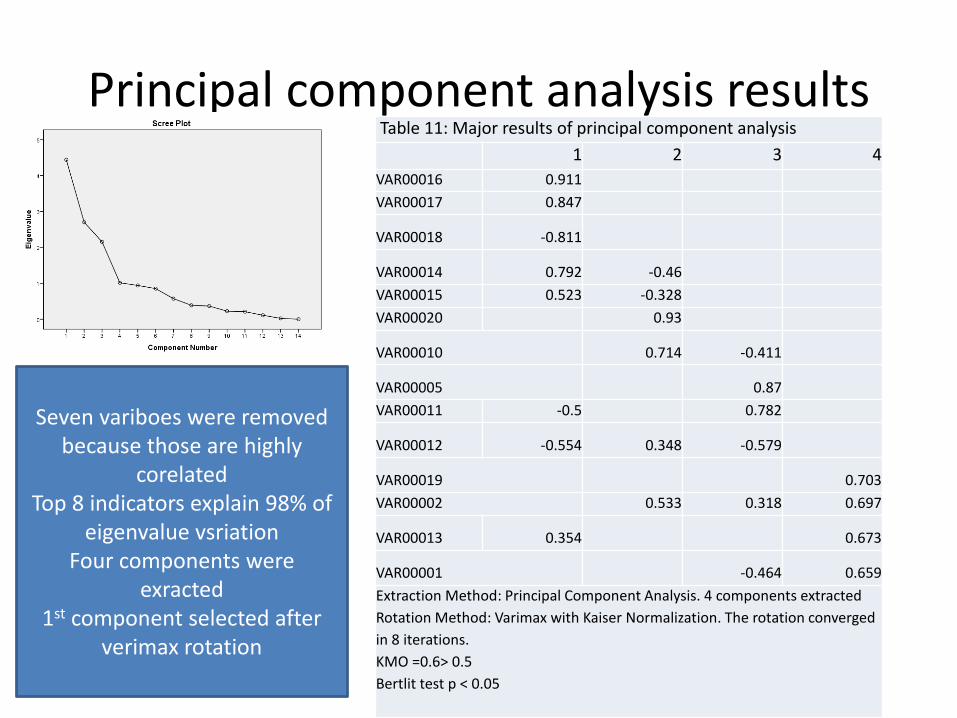

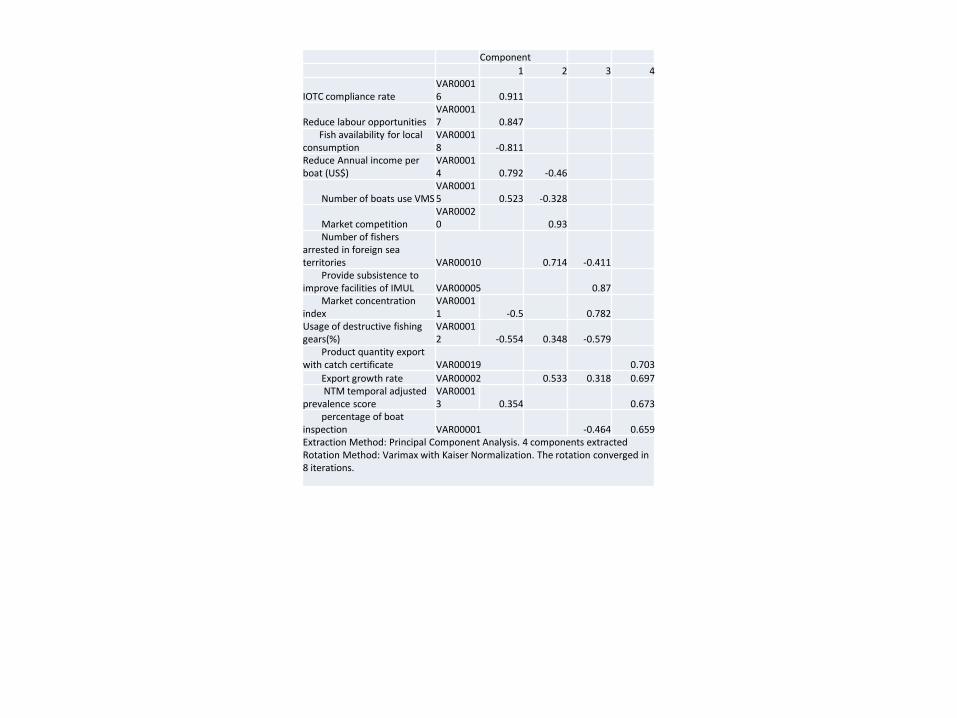

Principal component analysis resultsTable 11: Major results of principal component analysis

1 2 3 4

VAR00016 0.911

VAR00017 0.847

VAR00018 -0.811

VAR00014 0.792 -0.46

VAR00015 0.523 -0.328

VAR00020 0.93

VAR00010 0.714 -0.411

VAR00005 0.87

VAR00011 -0.5 0.782

VAR00012 -0.554 0.348 -0.579

VAR00019 0.703

VAR00002 0.533 0.318 0.697

VAR00013 0.354 0.673

VAR00001 -0.464 0.659

Extraction Method: Principal Component Analysis. 4 components extracted

Rotation Method: Varimax with Kaiser Normalization. The rotation converged

in 8 iterations.

KMO =0.6> 0.5

Bertlit test p < 0.05

Seven variboes were removed because those are highly

corelatedTop 8 indicators explain 98% of

eigenvalue vsriationFour components were

exracted1st component selected after

verimax rotation

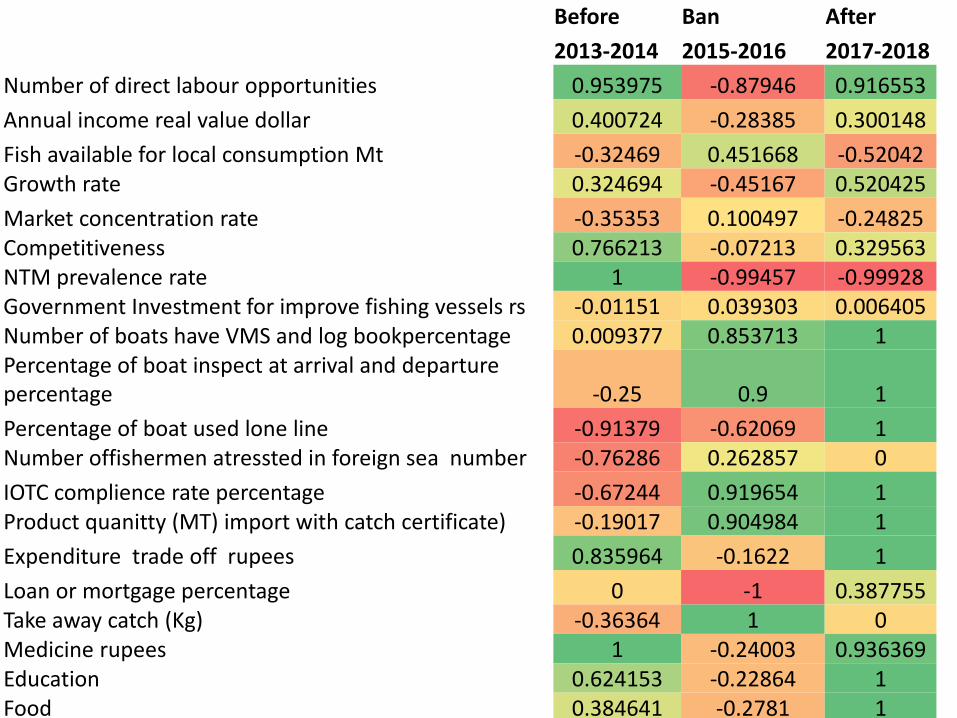

Before Ban After

2013-2014 2015-2016 2017-2018

Number of direct labour opportunities 0.953975 -0.87946 0.916553

Annual income real value dollar 0.400724 -0.28385 0.300148

Fish available for local consumption Mt -0.32469 0.451668 -0.52042Growth rate 0.324694 -0.45167 0.520425

Market concentration rate -0.35353 0.100497 -0.24825Competitiveness 0.766213 -0.07213 0.329563NTM prevalence rate 1 -0.99457 -0.99928Government Investment for improve fishing vessels rs -0.01151 0.039303 0.006405Number of boats have VMS and log bookpercentage 0.009377 0.853713 1Percentage of boat inspect at arrival and departure percentage -0.25 0.9 1

Percentage of boat used lone line -0.91379 -0.62069 1Number offishermen atressted in foreign sea number -0.76286 0.262857 0

IOTC complience rate percentage -0.67244 0.919654 1Product quanitty (MT) import with catch certificate) -0.19017 0.904984 1

Expenditure trade off rupees 0.835964 -0.1622 1

Loan or mortgage percentage 0 -1 0.387755Take away catch (Kg) -0.36364 1 0Medicine rupees 1 -0.24003 0.936369Education 0.624153 -0.22864 1Food 0.384641 -0.2781 1

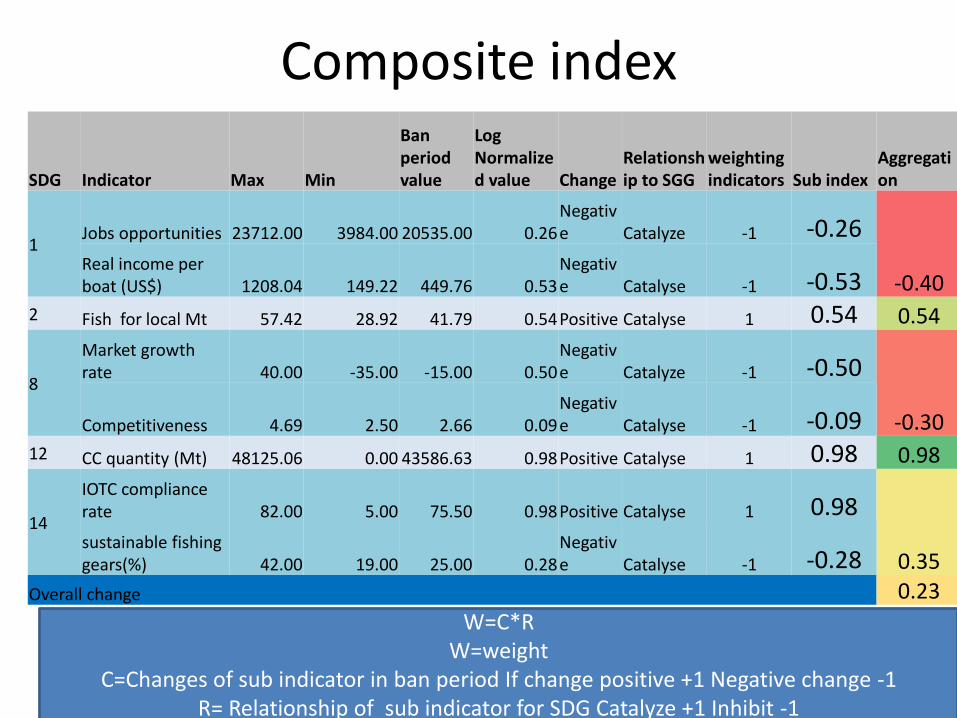

Composite index

SDG Indicator Max Min

Ban period value

Log Normalized value Change

Relationship to SGG

weighting indicators Sub index

Aggregation

1Jobs opportunities 23712.00 3984.00 20535.00 0.26

Negative Catalyze -1 -0.26

-0.40Real income per boat (US$) 1208.04 149.22 449.76 0.53

Negative Catalyse -1 -0.53

2 Fish for local Mt 57.42 28.92 41.79 0.54Positive Catalyse 1 0.54 0.54

8

Market growth rate 40.00 -35.00 -15.00 0.50

Negative Catalyze -1 -0.50

-0.30Competitiveness 4.69 2.50 2.66 0.09Negative Catalyse -1 -0.09

12 CC quantity (Mt) 48125.06 0.00 43586.63 0.98Positive Catalyse 1 0.98 0.98

14

IOTC compliance rate 82.00 5.00 75.50 0.98Positive Catalyse 1 0.98

0.35sustainable fishing gears(%) 42.00 19.00 25.00 0.28

Negative Catalyse -1 -0.28

Overall change 0.23

W=C*RW=weight

C=Changes of sub indicator in ban period If change positive +1 Negative change -1R= Relationship of sub indicator for SDG Catalyze +1 Inhibit -1

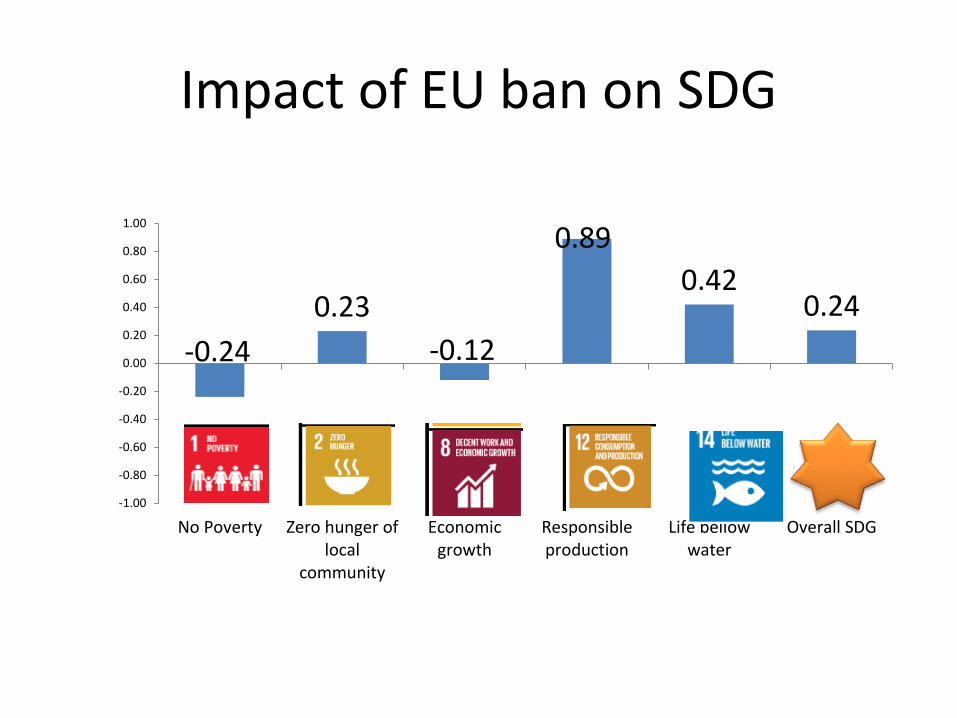

Impact of EU ban on SDG

-0.24

0.23

-0.12

0.89

0.420.24

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

No Poverty Zero hunger oflocal

community

Economicgrowth

Responsibleproduction

Life bellowwater

Overall SDG

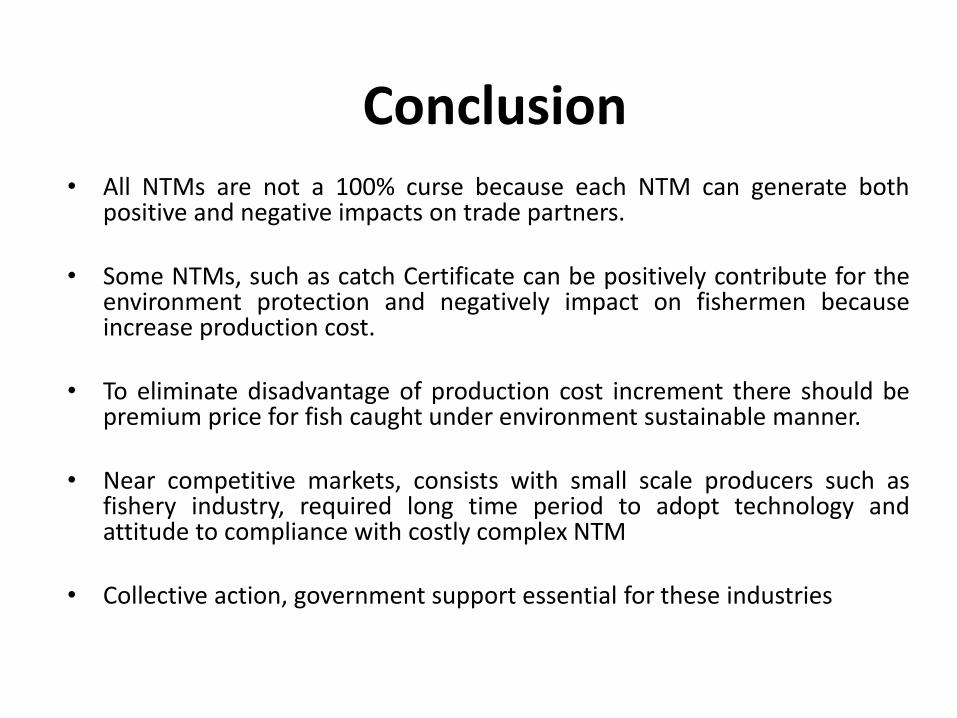

• All NTMs are not a 100% curse because each NTM can generate bothpositive and negative impacts on trade partners.

• Some NTMs, such as catch Certificate can be positively contribute for theenvironment protection and negatively impact on fishermen becauseincrease production cost.

• To eliminate disadvantage of production cost increment there should bepremium price for fish caught under environment sustainable manner.

• Near competitive markets, consists with small scale producers such asfishery industry, required long time period to adopt technology andattitude to compliance with costly complex NTM

• Collective action, government support essential for these industries

Conclusion

• The impact of NTM and impact of ban might begenerated contradictory outcome. For examplebecause of sanction there was no attractive pricefor the fish caught under sustainable fishingtechniques hence fishermen incline to low costdestructive fishing gears. On the other hand aftersanction fishermen attract towards thesustainable fishing gears because the fish withcatch certificate had significantly high price.

• The NTMs should not be a weapon to attacke tradecompetitors or opponent of international politicalarena.

• It should be a constructive tool to motivatesustainable development. The spontaneousdecision should not be taken regarding NTMsbecause the NTMs as very sensitive invisiblelinkages with sustainable development goals ofdifferent stake holders. It is recommendedimplementing fine studies to cover most of theimpacts and adjust the nature of NTMs to generateholistic sustainable development for whole planet.

Thank you

27.000

32.000

37.000

42.000

47.000

52.000

57.000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Mt

Annual average Supply quantity of fish for local market by a IUML boat

53334467304598841162

47401

665337411677418

899549194699799

93625

135647

117366105524

156618

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

US$

th

ou

san

d

Fish Import

Frozen fish

Dried fish

Total fish export

5.00

5.50

6.00

6.50

7.00

7.50

US$

/Kg

The average price in wholesale level

35

40

45

50

55

60

65

Mt

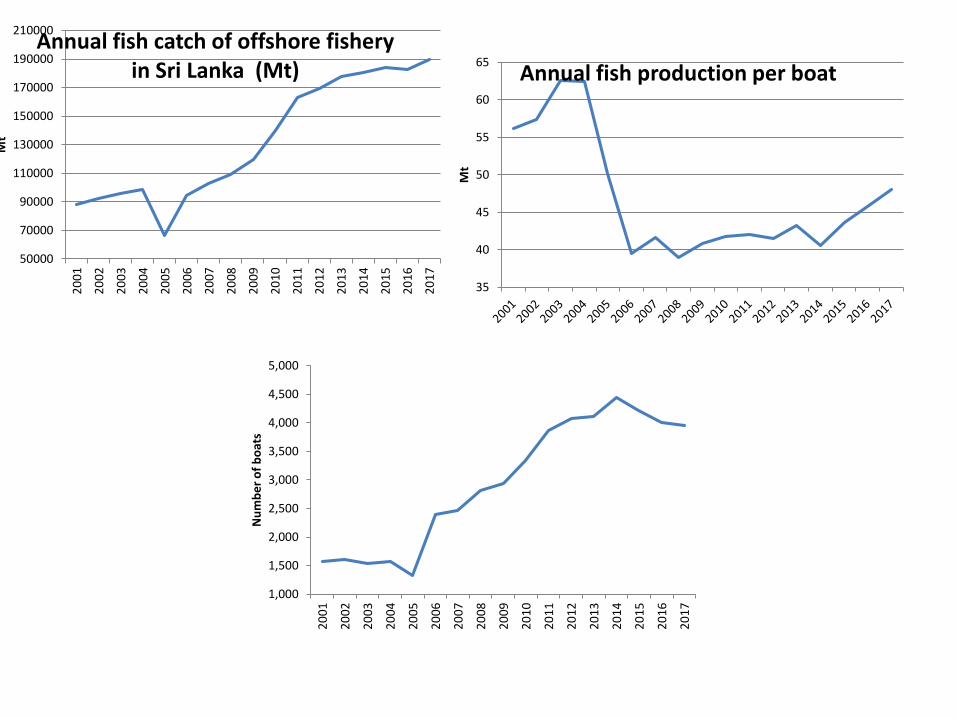

Annual fish production per boat

50000

70000

90000

110000

130000

150000

170000

190000

210000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Mt

Annual fish catch of offshore fishery in Sri Lanka (Mt)

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Nu

mb

er

of

bo

ats

Very sorry…. Still I am working on this

SGD index ln max ln min lnvalue

Index Aggregated index

1 income 11.83 10.54 11.04 0.38 Gematricmean calculate

1 Debt 10.32 8.75 9.13 0.42

2 Local fish consumption

2

2

3

3

Composite index

• It is a web diagram to show NTM impact on each SDG

Conclusion

References

Thank you

1922 24

30

46

57

68

7573

67

53

41 41 41

22 21

30

15

25

35

45

55

65

75

85

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Shar

e in

Sri

Lan

kan

exp

ort

mar

ket

(%)

Market Share of EU in Sri Lankan Fish Export Market (2001-2017)

0

5000

10000

15000

20000

25000

300002

00

1

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17N

um

be

r o

f d

ire

ct f

ish

ing

job

op

pe

rtu

nit

ies

Number of offshore boat registered

Overviwe of Sri Lankan fisheries industry

Chi-Square Tests

Value dfAsymp. Sig. (2-sided)

Pearson Chi-Square 11.901a 3 0.008Likelihood Ratio 12.151 3 0.007Linear-by-Linear Association 8.313 1 0.004N of Valid Cases 258a 0 cells (0.0%) have expected count less than 5. The

minimum expected count is 12.40.

Symmetric Measures

ValueApprox. Sig.

Nominal by Nominal Phi 0.215 0.008

Cramer's V 0.215 0.008

N of Valid Cases 258

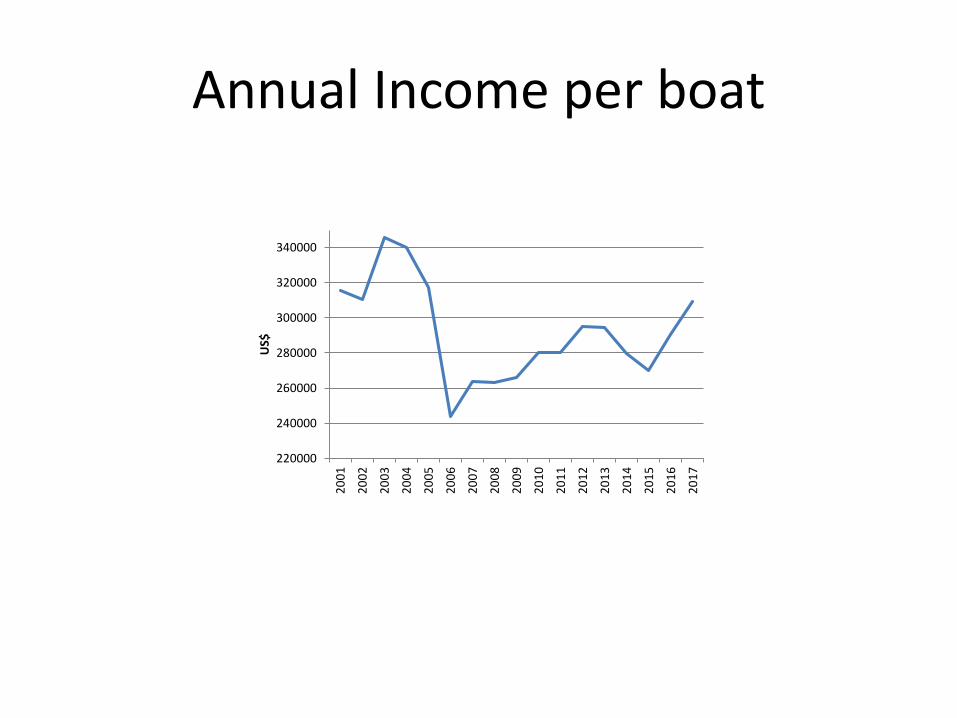

Annual Income per boat

220000

240000

260000

280000

300000

320000

340000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

US$

Component

1 2 3 4

IOTC compliance rate VAR00016 0.911

Reduce labour opportunitiesVAR00017 0.847

Fish availability for local consumption

VAR00018 -0.811

Reduce Annual income per boat (US$)

VAR00014 0.792 -0.46

Number of boats use VMS VAR00015 0.523 -0.328

Market competitionVAR00020 0.93

Number of fishers arrested in foreign sea territories VAR00010 0.714 -0.411

Provide subsistence to improve facilities of IMUL VAR00005 0.87

Market concentration index

VAR00011 -0.5 0.782

Usage of destructive fishing gears(%)

VAR00012 -0.554 0.348 -0.579

Product quantity export with catch certificate VAR00019 0.703

Export growth rate VAR00002 0.533 0.318 0.697NTM temporal adjusted

prevalence score VAR00013 0.354 0.673

percentage of boat inspection VAR00001 -0.464 0.659Extraction Method: Principal Component Analysis. 4 components extracted Rotation Method: Varimax with Kaiser Normalization. The rotation converged in 8 iterations.

fishing Gear * period Cross tabulationperiod Total

2015-2016 2017-2018fishing Gear Logline Count 64 82 146

% within period 50.0% 63.1% 56.6%Gill net with large size Count 21 28 49

% within period 16.4% 21.5% 19.0%Gill net with small mesh size Count 27 11 38

% within period 21.1% 8.5% 14.7%Purse seining Count 16 9 25

% within period 12.5% 6.9% 9.7%Total Count 128 130 258% within period 100.0% 100.0% 100.0%

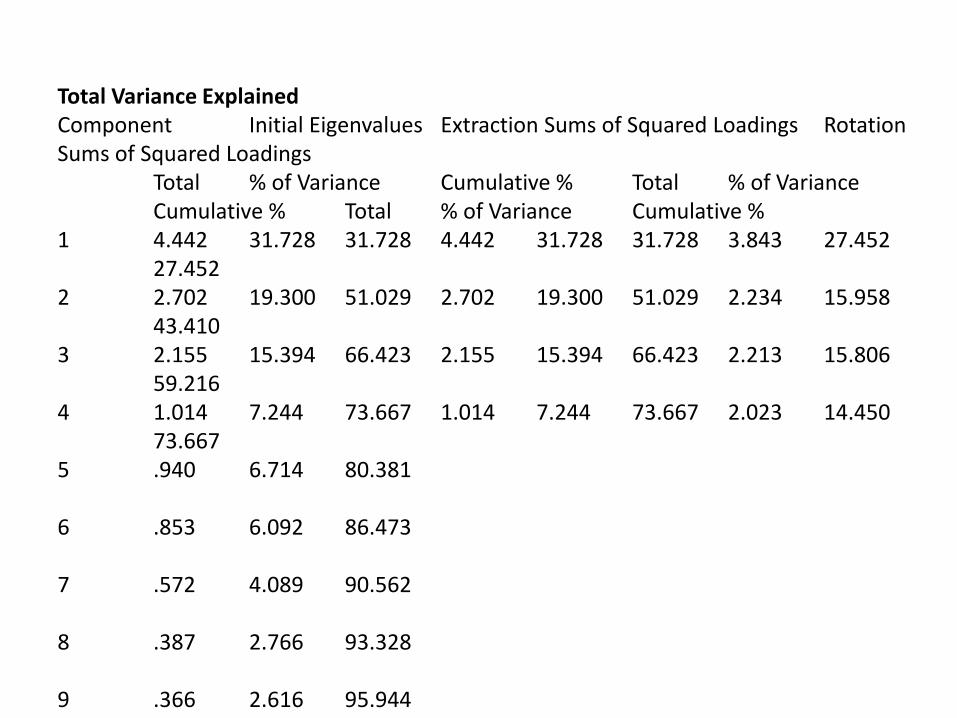

Total Variance ExplainedComponent Initial Eigenvalues Extraction Sums of Squared Loadings Rotation Sums of Squared Loadings

Total % of Variance Cumulative % Total % of VarianceCumulative % Total % of Variance Cumulative %

1 4.442 31.728 31.728 4.442 31.728 31.728 3.843 27.45227.452

2 2.702 19.300 51.029 2.702 19.300 51.029 2.234 15.95843.410

3 2.155 15.394 66.423 2.155 15.394 66.423 2.213 15.80659.216

4 1.014 7.244 73.667 1.014 7.244 73.667 2.023 14.45073.667

5 .940 6.714 80.381

6 .853 6.092 86.473

7 .572 4.089 90.562

8 .387 2.766 93.328

9 .366 2.616 95.944

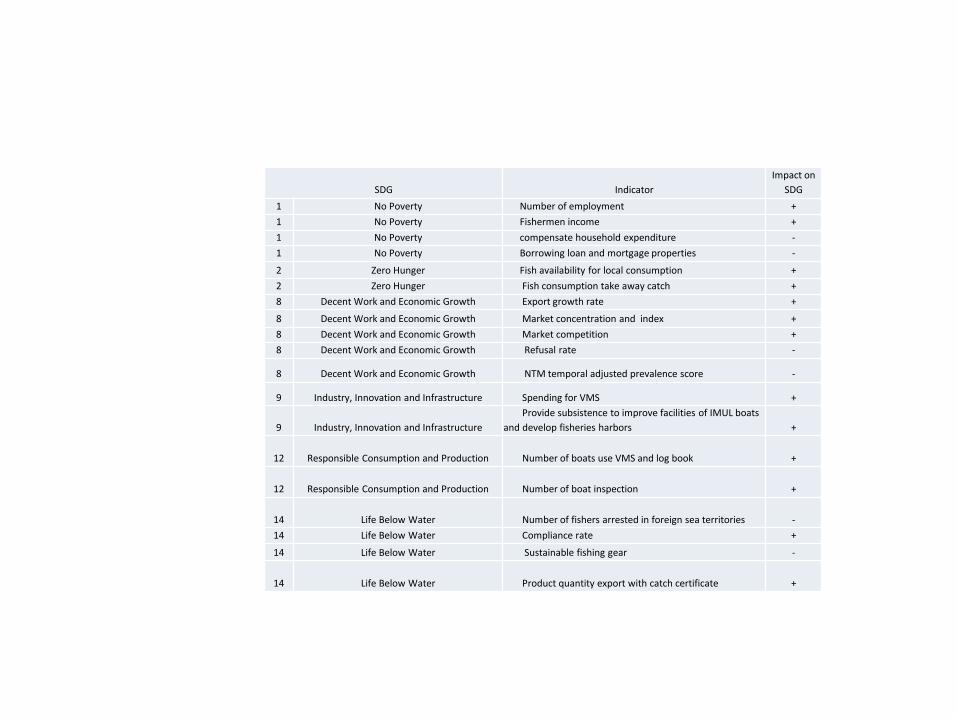

SDG Indicator

Impact on

SDG

1 No Poverty Number of employment +

1 No Poverty Fishermen income +

1 No Poverty compensate household expenditure -

1 No Poverty Borrowing loan and mortgage properties -

2 Zero Hunger Fish availability for local consumption +

2 Zero Hunger Fish consumption take away catch +

8 Decent Work and Economic Growth Export growth rate +

8 Decent Work and Economic Growth Market concentration and index +

8 Decent Work and Economic Growth Market competition +

8 Decent Work and Economic Growth Refusal rate -

8 Decent Work and Economic Growth NTM temporal adjusted prevalence score -

9 Industry, Innovation and Infrastructure Spending for VMS +

9 Industry, Innovation and Infrastructure

Provide subsistence to improve facilities of IMUL boats

and develop fisheries harbors +

12 Responsible Consumption and Production Number of boats use VMS and log book +

12 Responsible Consumption and Production Number of boat inspection +

14 Life Below Water Number of fishers arrested in foreign sea territories -

14 Life Below Water Compliance rate +

14 Life Below Water Sustainable fishing gear -

14 Life Below Water Product quantity export with catch certificate +

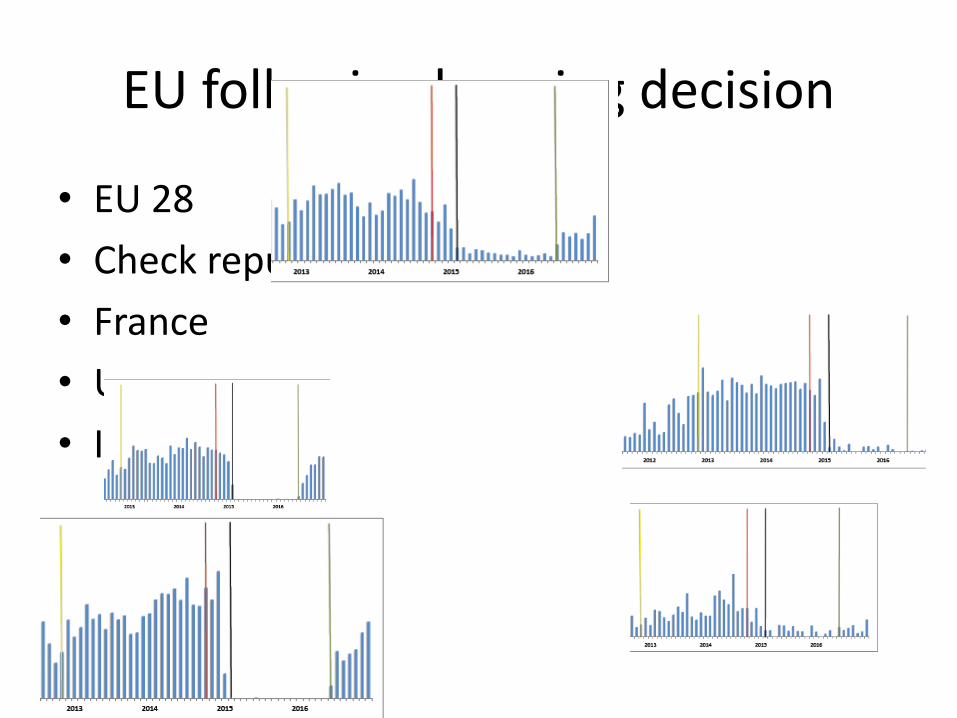

EU following banning decision

• EU 28

• Check republic

• France

• UK

• Itali

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

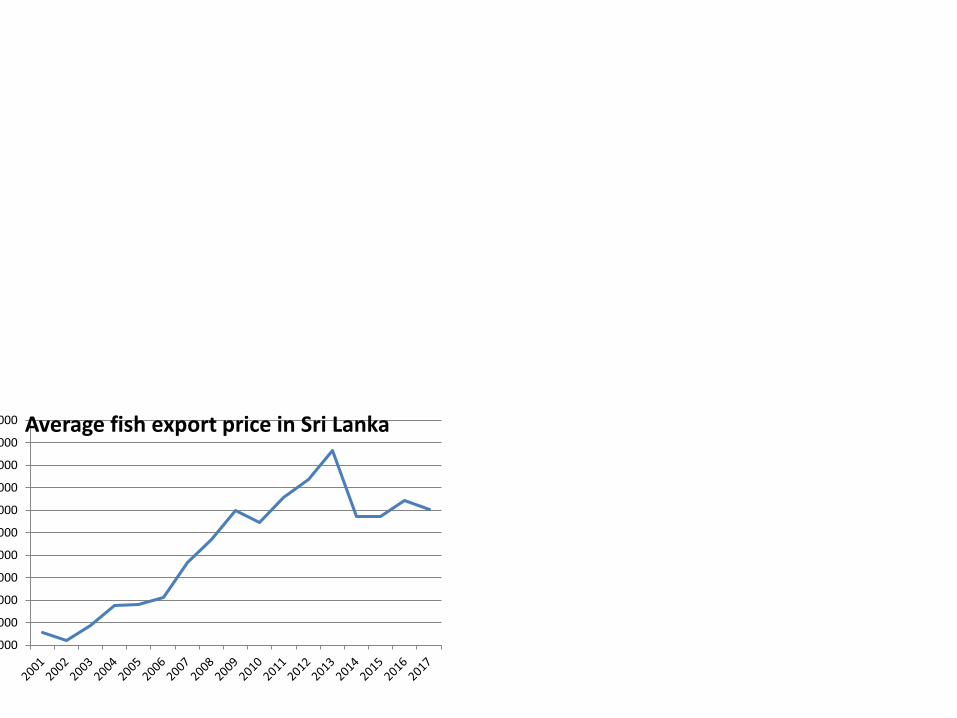

14000 Average fish export price in Sri Lanka

NTM of EU fish export

Type of regulation Act

Country authorization REGULATION (EU) No 1379/2013

Vessel approval Article 20(1) and (2) of the IUU Regulation

Health certificate Article 19 Specific labeling requirements for fish

Hygiene parameters Hazard Analysis and Critical Control Points (HACCP)

Traceability and labeling

Directive No 1379/2013

Contaminants Regulation (CC) No 1876/2007

Microbiological contamination

Regulation (EC) No 2073/2005

Expected outcomeIncrease product quality and protect customers

Encourage sustainable use of environment resource

Establish social justice and encourage to protect human rights

Protect the right of consumer to know origin and quality of the product they bought

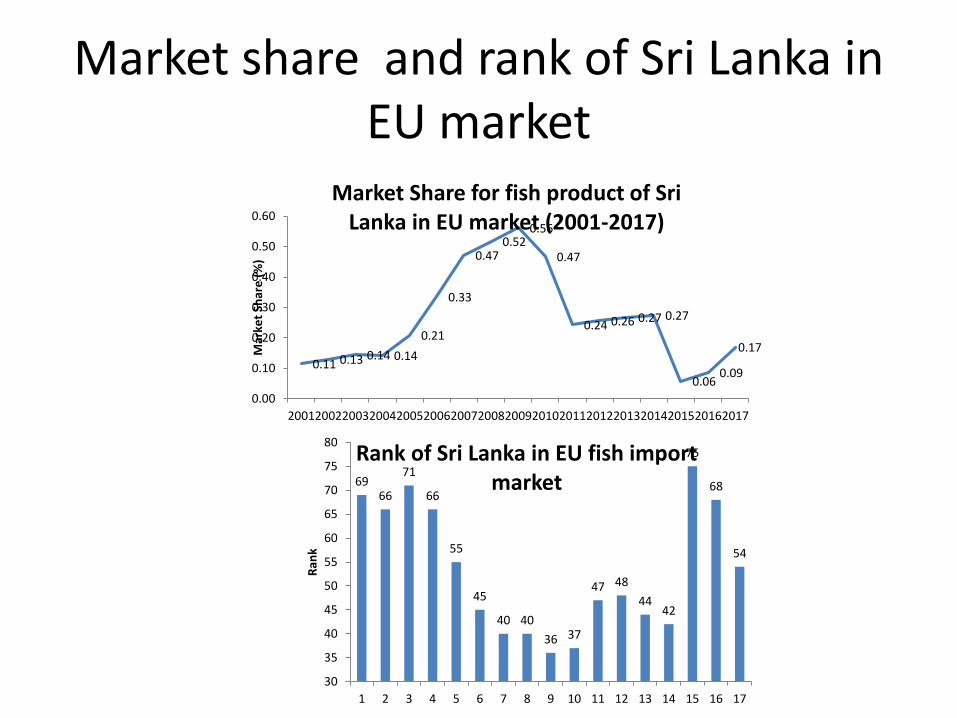

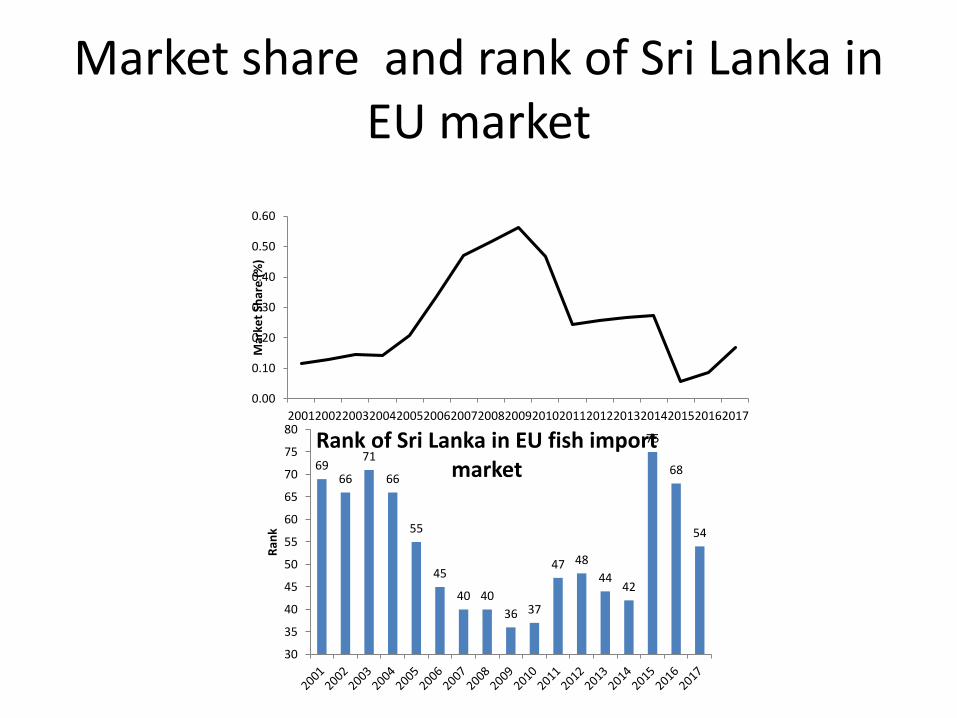

Market share and rank of Sri Lanka in EU market

0.11 0.13 0.14 0.14

0.21

0.33

0.470.52

0.56

0.47

0.24 0.26 0.27 0.27

0.060.09

0.17

0.00

0.10

0.20

0.30

0.40

0.50

0.60

20012002200320042005200620072008200920102011201220132014201520162017

Mar

ket

Shar

e (

%)

Market Share for fish product of Sri Lanka in EU market (2001-2017)

6966

71

66

55

45

40 40

36 37

47 48

4442

75

68

54

30

35

40

45

50

55

60

65

70

75

80

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Ran

k

Rank of Sri Lanka in EU fish import market

0

20

40

60

80

100

120

140

160

180

200

US$

mill

ion

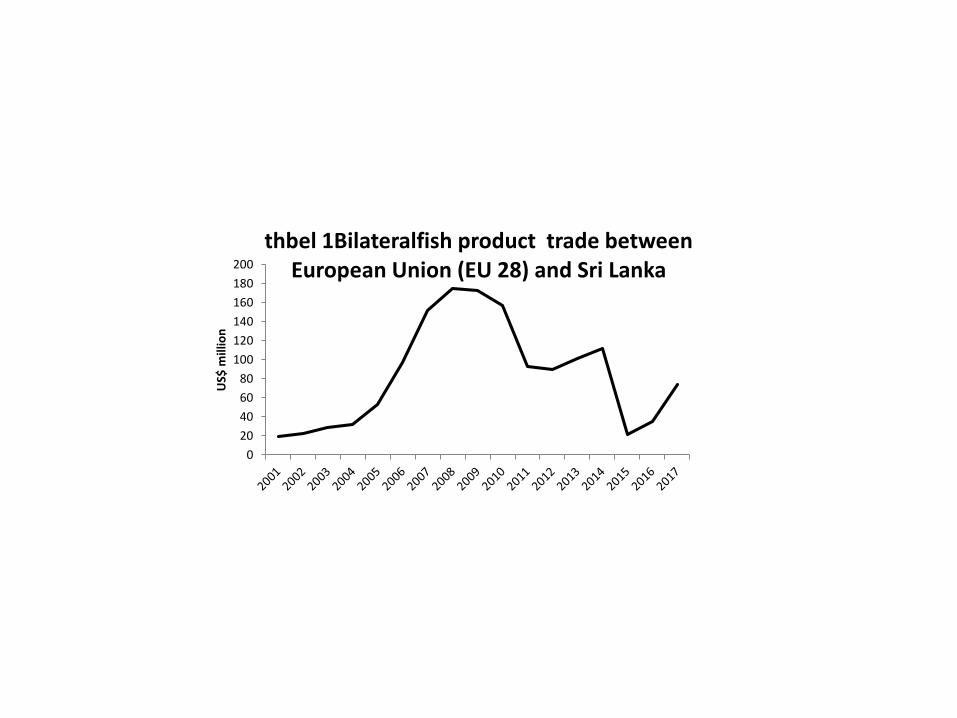

thbel 1Bilateralfish product trade between European Union (EU 28) and Sri Lanka

15

25

35

45

55

65

75

85

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Shar

e in

Sri

Lan

kan

exp

ort

mar

ket

(%)

Table 2 Market Share of EU in Sri Lankan Fish Export Market (2001-2017)

Fish species and fishing gears

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Longline Gill netwith large

size

Gill netwith smallmesh size

Purseseining

Ban

After

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Yellow fintuna

Othertuna

species

Billfish Minnerexport fish

species

Small fishspecies

Ban

After

Most competitive product mix H

S co

des

30349 1 2 2 1 1 1

30233 2 1 1

30232 3 3 3 2 2 2

30247 4 4 9 10 5

30579 5 9 10 7

30445 6 5 6 4 3

30449 7 7 10 9 3 6

30692 9 8 7

30259 10 6 7 9 4

30571 5 3 6 8

30614 8 6 4 5 7

30499 8 4 5 9

30617 10 8 8 10

2017 2016 2015 2014 2013 2012

Years

Market share and rank of Sri Lanka in EU market

0.00

0.10

0.20

0.30

0.40

0.50

0.60

20012002200320042005200620072008200920102011201220132014201520162017

Mar

ket

Shar

e (

%)

6966

71

66

55

45

40 40

36 37

47 48

4442

75

68

54

30

35

40

45

50

55

60

65

70

75

80

Ran

k

Rank of Sri Lanka in EU fish import market

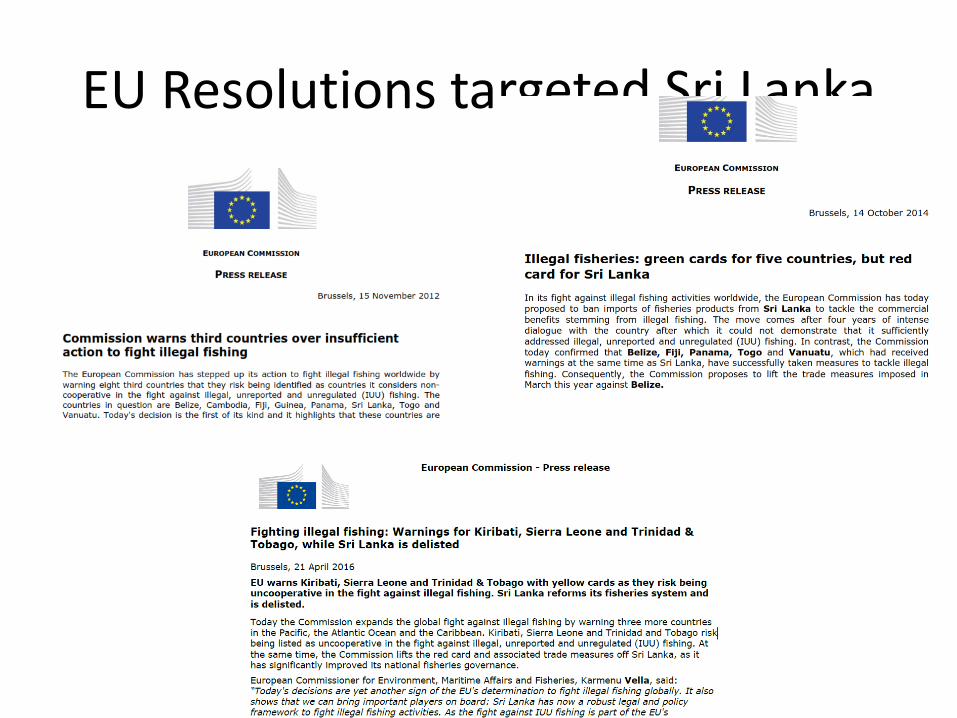

Table 1: Overview of third country authorisations to export seafood products to the EU (up to end 2017)

Yellow card pre-identification Identification (listing

as ban country)

Withdraw (delisting)

Number of the

countries

25 6 3

Names of the

Countries

Belize , Cambodia , Comoros Curacao ,

Fiji , Ghana ,Kiribati , Korea ,Liberia ,

Panama , Papua New Guinea ,

Philippines , Republic of Guinea , Sierra

Leone , Solomon Islands , Sri Lanka , St

Kitts

St Vincent and Grenadines , Taiwan ,

Thailand ,Togo , Trinidad and, Tobago ,

Tuvalu , Vanuatu , Vietnam

Republic of Guinea

Sri Lanka

St Vincent and

Grenadines

Belize

Cambodia

Comoros

Republic of Guinea

Sri Lanka

Belize

Source: Author preparation table base the list of banned and warn third country (European Commission

,2018)

EU Resolutions targeted Sri Lanka

Top 10 Export destination of Sri Lanka

Top 10 Export destination of Sri Lanka

Country 2012 2013 2014 2015 2016 2017

EU 1 1 2 2 2 1

USA 3 2 1 1 1 2

Japan 2 3 3 3 3 3

Hong Kong, China 4 5 6 6 6 6

Taipei, Chinese 6 4 5 5 5 7

Canada 5 6 4 4 4 4

Viet Nam 9 7 8 7 7 5

Saudi Arabia 8 8

Israel 8 9 10 9 9

United Arab Emirates 9 8 10 10

Singapore 7 8 7 9

Thailand 10 10 10

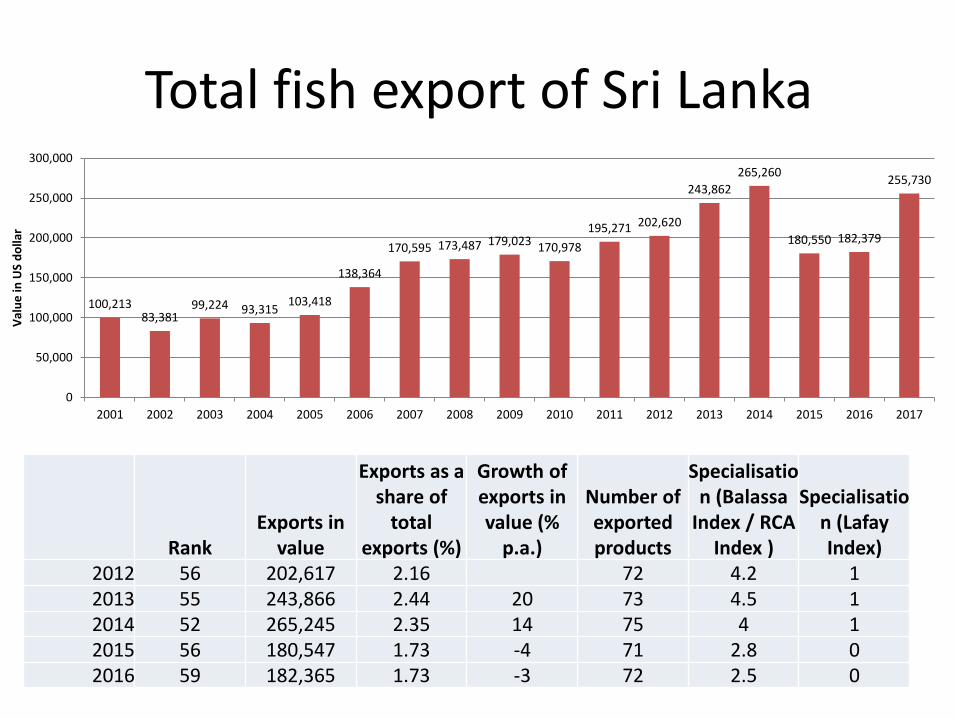

Total fish export of Sri Lanka

100,21383,381

99,224 93,315103,418

138,364

170,595 173,487 179,023 170,978

195,271 202,620

243,862

265,260

180,550 182,379

255,730

0

50,000

100,000

150,000

200,000

250,000

300,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Val

ue

in U

S d

olla

r

RankExports in

value

Exports as a share of

total exports (%)

Growth of exports in value (%

p.a.)

Number of exported products

Specialisation (Balassa

Index / RCA Index )

Specialisation (LafayIndex)

2012 56 202,617 2.16 72 4.2 12013 55 243,866 2.44 20 73 4.5 12014 52 265,245 2.35 14 75 4 12015 56 180,547 1.73 -4 71 2.8 02016 59 182,365 1.73 -3 72 2.5 0