Embed Size (px)

Citation preview

Impact of the economic recession on

the pharmaceutical sector

February 2010

I.M. Buysse (UU)

Supervised by:

R.O. Laing (WHO)

A.K. Mantel (UU)

WHO COLLABORATING CENTRE FOR PHARMACOEPIDEMIOLOGY & PHARMACEUTICAL

POLICY ANALYSIS

Impact of the economic recession on the pharmaceutical sector

Ta

ble

of

con

ten

ts

2

Table of contents

Executive summary ................................................................................................................................. 3

Introduction ............................................................................................................................................ 6

Background ............................................................................................................................................. 8

History of recessions ............................................................................................................................................................. 8

Asian Crisis 1997-2000 .......................................................................................................................................................... 9

Economic crisis 2008-2009 .................................................................................................................................................. 12

WHO involvement in assessing the impact of the recession .............................................................................................. 14

Hypotheses ......................................................................................................................................................................... 15

Methods ................................................................................................................................................ 16

IMS data collection ............................................................................................................................................................. 16

Provision of indexed data ................................................................................................................................................... 18

Graphical transformation methods..................................................................................................................................... 18

Economic indicators ............................................................................................................................................................ 19

Shift from private to public sector ...................................................................................................................................... 19

Country selection ................................................................................................................................................................ 19

Impact of the recession on specific groups and individual medicines ................................................................................ 20

Results ................................................................................................................................................... 22

Overall pharmaceutical consumption ................................................................................................................................. 22

Consumption of medicines for acute and chronic indications ............................................................................................ 26

Consumption of original & licensed brands and others brands & unbranded medicines ................................................... 29

Price per IMS Standard Unit ................................................................................................................................................ 32

Pharmaceutical expenditure ............................................................................................................................................... 35

Shift from private to public sector ...................................................................................................................................... 37

Impact of the recession on specific groups and individual medicines ................................................................................ 39

Discussion.............................................................................................................................................. 47

Conclusion ........................................................................................................................................................................... 51

References: ........................................................................................................................................... 52

Annexes ................................................................................................................................................. 54

Impact of the economic recession on the pharmaceutical sector

Exe

cuti

ve s

um

ma

ry

3

Executive summary

Introduction

The global financial crisis which started in 2008 may have considerable impact on governments’

budgets and the available funding for health services. Past economic recessions (especially the ‘97

Asian financial crisis) have shown that the impact on public health can be severe. At a high level

meeting in January 2009 WHO was requested to investigate the impact of the current economic

recession on global health. As part of this investigation a programme was established which focused

on the impact of the global economic crisis on the pharmaceutical sector.

The goal of this study was to assess the impact of global recession on consumption of medicines and

pharmaceutical expenditures and prices. A secondary objective was to investigate which medicines

were affected the most and the least by the recession in those countries that showed a clear decline

in medicines consumption.

Methods

IMS Health provided indexed data for pharmaceutical consumption, expenditures and prices in 84

countries from the first quarter of 2007 (Q1 07) until the last quarter of 2009 (Q4 09). Changes in

medicines consumption, pharmaceutical expenditure and prices over time (compared to the first

quarter of 2008 (Q1 08); the last quarter before the recession) were assessed per WHO region (AFR,

AMR, EMR, EUR, SEAR and WPR) and World Bank income category (high, upper middle, lower middle

and low income countries). Linear regression analysis was used to establish a potential relationship

between a decline in GDP and pharmaceutical consumption in the European region. The

consumption of medicines was subdivided into medicines for acute and chronic indications to

examine if there was a difference in development of consumption between these two categories. To

investigate a shift from original & licensed brands to other brands & unbranded medicines the

consumption patterns of both categories were compared.

A potential relationship between a decline in GDP and an increase in pharmaceutical prices was

assessed by linear regression as well.

A shift in pharmaceutical consumption from the private sector to the public sector was investigated

in four countries where data for both private and public sector were available.

Four countries were selected for further analysis based on the observed decline in medicines

consumption: Estonia, Latvia, Lithuania, and Romania. Poland was hardly affected by the global

recession and was thus selected as a comparator. For these five countries data was retrieved on the

volume of different medicine groups (EphMRA ATC 2 level). First a Pareto analysis was performed to

identify 30% of medicine groups which accounted for 80% of total consumption. The periods

Q4 07 + Q1 08 and Q4 08 + Q1 09 were compared as a period before and period during the economic

recession, respectively, to detect medicine groups which declined the most. Medicine groups which

declined in three of the four selected countries and not in Poland were considered to be of interest.

Of these medicine groups data was gathered at therapeutic groups (EphMRA ATC 3 level). The same

analyses were used to select categories which declined the most and had a possible negative effect

on public health. Of these categories data on consumption volume on product level (EphMRA ATC 4)

was used for more detailed analyses of changes in volume of consumption.

Impact of the economic recession on the pharmaceutical sector

Exe

cuti

ve s

um

ma

ry

4

Results and discussion

Although the economic recession affected many countries only a few showed a substantial decline in

pharmaceutical consumption. The European region was the WHO region with the most severe

decline (-6%, Q3 09 compared to Q1 08). The South East Asian region had the biggest increase in

pharmaceutical consumption (+28% in Q4 09) and the American region had the smallest increase

(+12% in Q4 09). Only the high income countries showed a small decrease in pharmaceutical

consumption of -3% (Q3 09 compared to Q1 08), in the other income categories the pharmaceutical

consumption increased ranging from +7% in the upper middle income countries to +17% in the low

income countries (Q4 09 compared to Q1 08). The countries with the most severe decline in

pharmaceutical consumption were Estonia (-18%), Latvia (-14%) and Lithuania (-17%) (Q3 09

compared to Q1 08). The correlation between a decline in GDP and decline in pharmaceutical

consumption of a country in the European region was moderate and differed from quarter to

quarter (r2 ranged from 0,39 to 0,65).

It is not yet clear when these Baltic States will return to their pre-recession levels of consumption,

although the numbers of Q4 09 showed a lesser decline in consumption.

The expectation that the decline of consumption of medicines for acute indications would be more

severe than for chronic indications was not seen in this study. Only the European region did show

this difference in decline of the two groups, although the differences were minimal.

To reduce pharmaceutical expenditure it was expected that there would be a shift from the use of

patent protected and licensed products to branded and other non patent protected products would

occur, but this shift was not seen in this study.

Almost all countries showed a price increase but there was no correlation between the level of

increase in pharmaceutical prices and a more severe recession in a country.

The shift from private to public sector was not common in the four countries, where this data was

available. In Brazil, Uruguay and South Africa the consumption in both private and public sector grew

although not at the same pace. Mexico did show a shift from private to public sector. The

consumption of original & licensed brands increased in Mexico in the public sector and declined in

the private sector. These changes may have been due to health section reform that occurred at the

same time as the economic recession.

Most of the declining EphMRA ATC 2 categories were not considered to have a negative impact on

public health if used less (i.e. vitamins declined by -22% to -15%, mineral supplements by -23% to

-5%, nasal by -24% to -8% and cold preparations by -20% to -4%). Categories of interest for further

analysis were systemic antirheumatics, opthalmologicals, psycholeptics and psychoanaleptics. The

decline of the systemic antirheumatics was probably caused by a decline in the use of NSAIDs.

EphMRA ATC 3 categories anti-infectives and artificial tears were probably the cause of the decline

in the ATC 2 category ophthamologicals. The ATC 3 categories N5A antipsychotics and N6A

antidepressants and moodstabilizers were considered of interest because these categories declined

in at least three of the four recession struck countries and could have a negative impact on public

health if used less.

Further analyses of the most frequently used products in these categories did not show a consistent

change in consumption with the economic recession. No individual marker products were found

which could be used by governments to track their pharmaceutical consumption and the functioning

of their health systems to provide early warning signs.

Impact of the economic recession on the pharmaceutical sector

Exe

cuti

ve s

um

ma

ry

5

The time span of this study was limited to one year before and two years after the recession. Many

countries were already beginning to recover from the economic recession in 2010 and the value of

this study for those recovered countries as a measure of the impact of the economic crisis on the

pharmaceutical sector is thus limited.

However there may be more to learn from this recession which could guide future policy responses

to future recessions. For example some countries experienced severe declines in GDP but did not

show any decline in pharmaceutical consumption.

Conclusions

The economic recession which began in 2008 has had a mixed effect on pharmaceutical

consumption, expenditures and prices. The largest changes have occurred in high income countries

and in Europe. On country level, particulary the Baltic States showed large changes in their

pharmaceutical consumption, expenditure and prices.

No consistent pattern in the decline of consumption of particulair classes or individual medicines

were seen.

This recession provides an opportunity to identify which policy approaches most effectively

prevented or contributed to declines in pharmaceutical consumption.

Impact of the economic recession on the pharmaceutical sector

Intr

od

uct

ion

6

Introduction With the collapse of the housing market in the USA and parts of Europe in 2007 the world entered a

financial crisis which lasted at least through the years 2008 and 2009. Depending on the country

governments adjusted their budgets, which had considerable impact on the available funding to pay

for health services.(1-3) In the Organisation for Economic Cooperation and Development (OECD)

countries the average amount spend on healthcare before the recession was about 9% of the gross

domestic product (GDP), ranging from 6% in Korea, Mexico and Poland to 15,3% in the USA

(numbers of 2005).(4) In a recession governments may choose to lower their health care budgets.

Since medicines or pharmaceuticals are a substantial part of the health care budget world wide

(around 17% in OECD countries) it is likely that governments may take measures to reduce these

costs. As a consequence patients may find themselves unable to pay for their health services.

It is hard to gauge the implications of the recession on people's health. Experience from past

recessions has shown that the impact can be severe. (5) Stukler et al. showed that suicides and

homicides rose among working-age men and women when unemployment rose rapidly during times

of recession in Europe. A one percent increase in unemployment caused an increase in suicides of

0,79%. (6) An increase in underweight rates among primary school children and low birth weight

were observed during the crisis in Thailand.(7) In Mexico mortality among elderly and children was

5-7% higher during the crisis of 1995-1996 when compared to non-crisis years. According to the

authors this increase is most likely related to the magnitude of economic crisis and a reduction in

public sector medical services. (8) These are some examples of the possible impact of an economic

crisis on public health.

At the 2009 Executive Board meeting held in January 2009, WHO was requested to investigate the

impact of the current recession on health. (9) As part of this investigation, a programme has been

established which focuses on the impact of the global economic crisis on the consumption,

expenditure and prices of medicines.(9) This present report will address the impact of the economic

recession on the pharmaceutical sector from the beginning of 2007 to the end of 2009.

In this report other economic recessions during the twentieth century will be described, beginning

with the Great Depression in 1930’s, to put the 2008-2009 economic crisis in perspective. The Asian

Crisis in 1997 was the first crisis where the impact of a recession on public health was assessed.

Therefore this crisis will be highlighted. We will also describe the development of the present

economic crisis. We will highlight some policy changes with respect to public health in countries

severely affected by the economic recession, like Estonia, Latvia and Lithuania.

After this background section we will describe the data and methods used for analysing the changes

in pharmaceutical consumption in relation to the economic situation. Data on pharmaceutical

consumption, expenditure and prices was provided by IMS Health for 84 countries for each quarter

in the period 2007-2009.(10) The results of these analyses will be presented in the results section.

First we will present the changes in pharmaceutical consumption in different areas over the world

where we will look in more detail at countries with interesting changes in their consumption pattern.

The consumption divided in acute and chronic indication and in original & licensed brands and other

brands & unbranded medicines will be investigated to see if there is a different effect of the

Impact of the economic recession on the pharmaceutical sector

Intr

od

uct

ion

7

economic recession on the consumption of these different categories. We will also focus on

pharmaceutical expenditure and prices to see if these were affected by the crisis. In countries with a

clear decline in consumption we will look in more detail to the pharmaceutical consumption at

different ATC levels (Anatomic therapeutic classification) and we will try to identify marker products

which could predict a decline in pharmaceutical consumption in times of economic recession. These

marker products could thus act as sentinel products.

A shift was expected from the use of private to public health facilities because they are less

expensive. Data of four countries will be analysed to detect such a shift.

In the discussion this study will be compared to other studies carried out especially those regarding

the Asian Financial crisis. Some of the implications for (pharmaceutical) policy and public health will

be given and finally some recommendations for further research will be made.

The purpose of this report is to provide an overview of the changes in pharmaceutical consumption,

expenditure and prices for different regions in the world and some observed changes will be

highlighted in more detail. This report provides information that can be used by policy makers,

development planners and pharmaceutical experts to guide their responses in addressing the

present recession and in monitoring a next recession.

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

8

Background

History of recessions

The world has already faced multiple financial crises during the 20th century. Some resulted in an

economic crisis in which not only the financial sector collapsed but the Gross Domestic Product

(GDP) dropped and unemployment rose.

One of the most severe recessions was the Great Depression which started in 1929 in the USA with

the collapse of the USA stock market prices. (11) It quickly spread over the world because the USA

invested and loaned substantial amounts of money to Europe to recover from World War I. Although

the Great Depression started in the USA, Australia, Canada and Germany were the countries which

were most severely affected by this crisis.(12) Recovery started in most countries in 1933 although

they did not fully recover until the beginning of World War II, when governments increased their

spending to produce war materials.

Another recession which had a great impact world wide was the 1973 oil crisis. As a response to the

re-supply of the Israeli military by the USA during the Yom Kippur war, the Organization of the

Petroleum Exporting countries (OPEC) brought an oil embargo into force. (13) As a consequence the

price of oil increased by 395%. (14) This price increase of crude oil had a negative impact on

industrial production. In March 1974 the embargo was lifted and the recovery began.

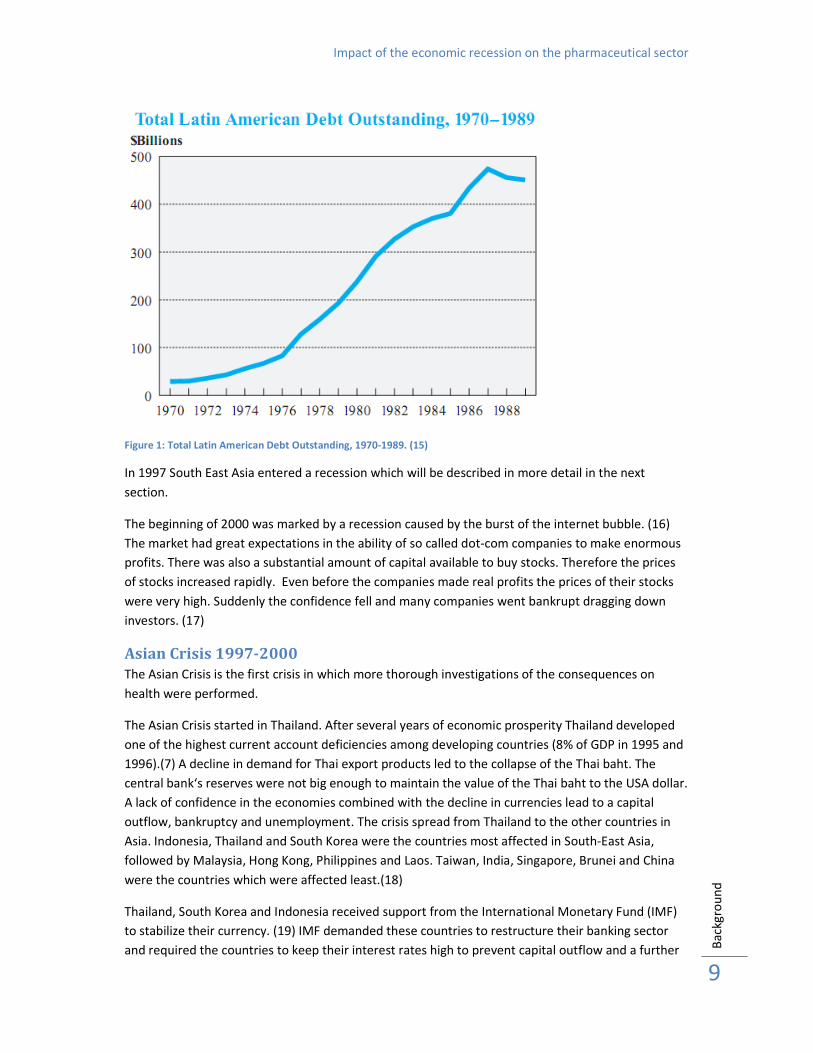

At the end of the 1970s Latin-America entered a recession. In the 1960s and 1970s Latin-American

countries, especially Brazil, Mexico and Argentina, borrowed large amounts of money for

industrialization. (15) Mexico, Brazil, Argentina and Venezuela had a debt of $29 billion in 1970

which increased to $159 billion in 1978 (see Figure 1). In 1979 interest rates in Europe and USA

increased making it more difficult for the Latin American countries to pay back their debts. When the

international capital markets discovered that the Latin American countries could not pay back their

loans (August 1982), they refused new loans to these countries. This caused a halt to the increase of

investments in industrialization. To prevent a more severe increase of the debts the Latin American

countries changed their import substitution industrialization economies to be export-oriented

industrialized economies. Large capital outflow caused a depreciation of the exchange rates which

led to an increase of interest rates. This improved the situation in these countries although they still

face large debts to date.

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

9

Figure 1: Total Latin American Debt Outstanding, 1970-1989. (15)

In 1997 South East Asia entered a recession which will be described in more detail in the next

section.

The beginning of 2000 was marked by a recession caused by the burst of the internet bubble. (16)

The market had great expectations in the ability of so called dot-com companies to make enormous

profits. There was also a substantial amount of capital available to buy stocks. Therefore the prices

of stocks increased rapidly. Even before the companies made real profits the prices of their stocks

were very high. Suddenly the confidence fell and many companies went bankrupt dragging down

investors. (17)

Asian Crisis 1997-2000

The Asian Crisis is the first crisis in which more thorough investigations of the consequences on

health were performed.

The Asian Crisis started in Thailand. After several years of economic prosperity Thailand developed

one of the highest current account deficiencies among developing countries (8% of GDP in 1995 and

1996).(7) A decline in demand for Thai export products led to the collapse of the Thai baht. The

central bank‘s reserves were not big enough to maintain the value of the Thai baht to the USA dollar.

A lack of confidence in the economies combined with the decline in currencies lead to a capital

outflow, bankruptcy and unemployment. The crisis spread from Thailand to the other countries in

Asia. Indonesia, Thailand and South Korea were the countries most affected in South-East Asia,

followed by Malaysia, Hong Kong, Philippines and Laos. Taiwan, India, Singapore, Brunei and China

were the countries which were affected least.(18)

Thailand, South Korea and Indonesia received support from the International Monetary Fund (IMF)

to stabilize their currency. (19) IMF demanded these countries to restructure their banking sector

and required the countries to keep their interest rates high to prevent capital outflow and a further

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

10

decline of their national currencies. Malaysia refused the assistance of IMF because of these

restrictions. (19)

The crisis in Indonesia became more complex than the crises in the other countries since it turned

into a political and social crisis, thereby complicating the Indonesian economic situation and

responses of the Indonesian government to the economic crisis. (20) WHO investigated the impact

of the Asian financial crisis on the pharmaceutical sector in Indonesia. It was expected that the use

of health facilities would decrease, but the health centres and hospitals did not report significant

changes in the number of patient visits. However Indonesia did experience a significant shortage of

raw materials for pharmaceutical production due to changes in exchange rates. The government

took several measures to protect the pharmaceutical sector. One of these measures was monitoring

the availability of 12 key indicator medicines. Another measure was to provide additional funds for

the provision of a national buffer stock of essential medicines. The monitoring of the availability of

generic products was also a measure to guarantee the access to generic products. To cover the

excess of exchange rate to buy raw materials above Rp 8000 per USA dollar the government

provided additional subsidies to pharmaceutical companies producing generic products. The

government also established the Jaring Pengaman Sosial Bidang Kesehatan (JPS-BK), a social security

net for health. This fund was especially meant for poor households.

Figure 2: Pharmaceutical consumption in South East Asia Q2 1996 - Q2 2002. These figures show that the decline in

pharmaceutical consumption (b) started later than the decline in GDP (a). (21)

Intercontinental Medical Statistics (IMS) Health has performed a retrospective investigation of the

consumption of medicines during the crisis in South-East Asia. (21) Their research covered the

consumption data for six years (see Figure 2). They measured the overall pharmaceutical

consumption and pharmaceutical consumption split by acute and chronic indication. The observed

decline in volume of pharmaceutical consumption (see Figure 3) was the most severe in Indonesia

(-13%), Thailand (-22 %) and South-Korea (-16 %). Therefore IMS Health concentrated their more in

depth research on these three countries. The decline in pharmaceutical consumption was consistent

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

11

with the economic situation in three countries. The decrease in GDP was also the most severe in

Indonesia, Thailand and South-Korea.

The data gathered by IMS Health showed that the pharmaceutical consumptions dropped when GDP

growth dropped, although the decline started some quarters later (see Figure 2 and Table 1, the left

figure about the development of GDP shows a decline at t=0-1 quarters and the right figure about

the pharmaceutical consumption t=2-3 quarters). The recovery of pharmaceutical consumption took

longer than GDP.

Pharmaceutical consumption South East Asia 1997/1998

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

INDONES

IA

PHILIPPINES

THAILA

ND

MAL

AYS

IA

SINGAPO

RE

TAIW

AN

SOUTH

KORE

A

HONG KONG

Volu

me G

rowth

(%

)

-80%

-60%

-40%

-20%

0%

20%

40%

Valu

e G

rowth

(%

)

Volume Growth Value Growth (Local Currency) Value Growth (USD) Figure 3: This figure reflects the change in volume of pharmaceutical consumption in South East Asia in 1997-1998. The

value of the pharmaceutical consumption is given in local currencies and in US dollars. Indonesia, Thailand and South

Korea showed the most dramatic decline in pharmaceutical consumption. (9)

Looking at the difference between consumption of acute and chronic medication one can see that

the consumption for chronic indication recovered quicker than the overall consumption (Table 1).

Table 1: One can see in this how many quarters it took for real GDP (expressed in local currency), overall drug

consumption, consumption of medicines for acute and chronic indication (expressed in supply units) to decline, get to

the bottom of the decline and to recover. (9)

Real GDP (LCU) Overall Drug Consumption

(SU)

Consumption for Chronic

Disease (SU)

Consumption for Acute

Disease (SU)

Qtrs.

to

decline

Qtrs.

to

bottom

Qtrs. to

recovery

Qtrs.

to

decline

Qtrs. to

bottom

Qtrs. to

recovery

Qtrs.

to

decline

Qtrs. to

bottom

Qtrs. to

recovery

Qtrs.

to

decline

Qtrs.

to

bottom

Qtrs. to

recovery

Thailand 1 5 (.86) 18 2 5 (.78) 18 3 4 (.79) 9 2? 6 (.72) 26

Indonesia 2 6 (.85) 17 2 7 (.81) 13 2 4 (.75) 15 2 7 (.80) 12

Korea 2 4 (.92) 8 1 5 (.80) 10 3 3 (.90) 8 1 5 (.67) Never

Average 1.67 5 12.67 1.67 5.67

(.80) 13.67 2.67

3.67

(.81) 10.6 1.67 6 (.73) 19

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

12

Economic crisis 2008-2009

The main cause of the current economic crisis is thought to be that US banks had provided high-risk

loans to people with poor credit history to purchase homes prior to 2007. (22) Between 2004 and

2006 house prices fell and interest rates in the US rose from 1% to 5,35% thereby triggering a

slowdown of the housing market. (22) Homeowners could no longer afford the large mortgages they

had taken to buy their houses. As a consequence banks and investors suffered losses and would not

take on any more risk, leading to a freezing of the credit market. The same problem occurred in

Europe. The European Central Bank (ECB) and the US Federal Bank made funds available for banks

and they have cut interest rates so the banks could start providing loans again. Since banks were still

very cautious about loans and did not lend to one another, the measures of the ECB and the Federal

Reserve did not prevent the crisis progressing.

From the beginning of 2008, banks and investors faced severe problems. (22) Governments tried to

keep banks and investors in business by providing them very large loans in exchange for shares in

the banks. On September 15, 2008 Lehman Brothers, a major investment bank in the USA, filed for

bankruptcy being the first of many banks in the US and Europe to collapse.

The lack of confidence in the credit market led to a decline in economic growth and from the second

half of 2008 many countries all over the world entered a recession. (22)

This recession started in the developed countries and caused a decline in revenues. The developed

countries needed money to stabilize their own economy and had no extra funds left to provide loans

to and invest in developing countries. The decline in loans and investments is the reason why

developing countries (which were highly dependent on loans and development assistance) were hit

hard by the current economic recession. The costs of existing loans became higher due to the

decline in exchange rates. Some export oriented economies such as China or India saw a decline in

demand for their exports, with consequences for their national revenues.(23)

Examples of countries which were hit hard by the recession are Estonia, Latvia and Lithuania. (24)

After years of rapid growth of their GDP, all three countries saw their GDP decline rapidly during the

’08-’09 recession. Estonia saw a decline in GDP of -15,0% in the first quarter of 2009 and Latvia

showed a bigger decline of -18,6% in the same quarter (see table 2). (25)

In the Euro area (EA16) and European Union (EU27) the decline of GDP in 2009 compared to 2008

decreased (see Table 2).(25) In Q1 09 these declines were respectively -5,0% and -4,9%. In Q4 09 these

declines were -2,1% for the Euro area and -2,3% for the European Union. Declines in GDP were still

large in Estonia, Latvia, Lithuania and Romania compared to the Euro area and the European Union

but not as large as in Q1 09. Poland had no decline in GDP although the growth rate became less

(from 1,5% in Q1 09 to 1,0% in Q3 09).

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

13

Table 2: Growth rates of GDP in volume of 2009 compared to the same quarter of 2008. (25)

Q1 09 Q2 09 Q3 09 Q4 09

EA161

-5,0 -4,8 -4,0 -2,1

EU272

-4,9 -5,0 -4,3 -2,3

Estonia -15,0 -16,1 -15,6 -9,4

Latvia -18,6 -17,3 -19,3 -17,9

Li thuania -13,1 -19,7 -14,2 -13,0

Romania -6,2 -8,7 7,1 -6,6

Poland 1,5 1,3 1,0 na

Percentage change compa red wi th the same quarter of the

previous year

1) EA 16 consist of Austria, Belgium, Cyprus, Denmark, Estonia, Finland, France, Germany, Greece, Ireland, Italy,

Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain. 2) EU27 includes Austria, Belgium, Bulgaria, Cyprus, the Czech Republic, Finland, France, Germany, Greece, Hungary,

Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia,

Spain, Sweden and the United Kingdom.

NA = not available.

The governments of the Baltic States needed to have a careful look at their budgets because of

declining revenues. Health care is one of the largest expenses on the budgets of governments. Some

of the measures the Baltic governments took with respect to their health system/budget are

highlighted below.

The three Baltic States intended to adopt the Euro as their national currency in 2011. Therefore they

did not want to consider a devaluation of their currency, otherwise they would have to start over

with the application for joining the euro zone. (24) Besides the adoption of the euro there was

another issue. Most loans in the Baltic States were financed with money from Sweden. If the Baltic

countries devalued their currencies their debts would increase.

In Estonia several (health care) reforms were implemented. One of the biggest changes was the

policy of payments on sick leave. Before the recession people would receive money from day 2 of

their sick leave out of the National Health Insurance Fund. Now people only receive money after 3

days of sick leave by their employers during maximal 5 days and the National Health Insurance Fund

(EHIF) only starts to pay on day 9 of the sick leave. This could save the Estonian government 29

million Euros. (26) The government also decided to simply reduce the budget of the EHIF by 40

million Euros. (1) The budget of EHIF is used to cover medical services for all insured people.

The Latvian government decided to increase the fees of healthcare paid by patients as a

measurement to reduce the expenses on health care. (27) The overall budget cut of the ministry of

health was 12,7 million Euros of a total budget cut of 71,1 million Euros for the entire government.

(2, 3) In January 2009, the government decided to reduce the reimbursement levels from 90% to

75% and from 75% to 50% for different categories of care. (3) Other measures taken were transfer of

some medical treatments from hospitals to out-patient clinics and reduction of hospital funding by

30-45%.

The Lithuanian government reduced their public expenditure by 956,52 million Euros (28). This

included a reduction in the budget of the Compulsory Health Insurance Fund (CHIF) by 86,55 million

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

14

Euros. (22) A reduction of the budget for subsidizing medicines of 9,04 million Euros was agreed at

the same time.

In all the Baltic countries the governments decided to increase their Value Added Tax (VAT) on

pharmaceuticals. One of the reasons was to put the taxes in line with some European tax levels, but

the most important reason to implement this change was to increase government revenues. (27, 29-

31)

WHO involvement in assessing the impact of the recession

To discuss the impact of the financial crisis on global health, WHO convened a high-level meeting on

January 19, 2009. (9) At the time of this meeting there was a widely stated expectation that this

current crisis would be the worst since the Great Depression in the 1930s. Increases in food and fuel

prices before the recession brought more than 100 million people back into poverty. (16) There was

a concern expressed that the poor would be hit the hardest by the economic recession as

unemployment would lead to a drop in household income and in many countries unemployed

people would lose their health insurance. (19) This would lead to an inability to pay for health care.

Figure 4 shows the relation between an economic crisis and a decreased health status. An economic

crisis means that there is less economic growth, which leads to higher unemployment and inflation.

This can lead to bankruptcies. It also means that household income and tax revenue decrease. When

families have less to spend they will buy less food and food of less quality. They also cut back their

expenses on health and education. Governments have to cut back on their budgets when tax

revenues decline.

Figure 4: This flowchart shows the relation between an economic crisis and a decreased health status. An economic crisis

implies an increase in unemployment and inflation. It also leads to bankruptcies. This causes a decrease in household

income and tax revenues. People spend less money on food, health and education. Decreased revenue means that

governments have to cut back on their budgets. A cut back on the heath and education budget can mean that funding

for immunization, health insurance and improvements in technology declines. This can lead to a decreased health status

of the population. Mortality rates will increase and life expectancy will decrease. (19)

Impact of the economic recession on the pharmaceutical sector

Ba

ckg

rou

nd

15

Some important shifts in health expenditure were expected to be seen. Private out-of-pocket

expenditure usually declines in a recession because most services are also available in the public

sector at lower costs. In the Mexican crisis of 1995-1996 out of the pocket health expenditures

declined from 3,9% of GDP in 1994 to 3,1% of GDP in 1995.(8) The demand for public services would

exceed the available supply and cause problems in access for those who normally depend on public

services.

A recession is often accompanied by inflation and sometimes devaluation of domestic currencies

which causes an increase in the price of imported raw materials, medicines and medical equipment.

A more efficient way of health sector spending could lead to an increase in the use of the cheaper

generic medicines instead of branded medicines. Usually branded medicines are priced higher but in

some circumstances they are not (i.e. when a country has a reference price system).

Because of the rapid evolution of the economic recession it was decided at the high-level meeting on

January 19, 2009 that monitoring of early warning signs was of great importance. The monitoring

requires information from various sources. The WHO has established a programme to track the

impact of the recession on health and the pharmaceutical sector. IMS Health provides quarterly

reports on pharmaceutical consumption, expenditure and prices in 84 countries. Changes in general

consumption, consumption of medicines for acute and chronic indication, consumption of original &

licensed brands and other brands & unbranded medicines, expenditure and price per Standard Unit

are monitored in the 84 countries. These 84 countries world-wide represent 81% of the global

population, only the countries in Africa were covered less.

Hypotheses

The quarterly reports of IMS Health/WHO offer only an aggregate overview of the changes in

consumption. Therefore we decided to look in more detail at the detected changes. Based on

experiences from previous recessions this study was undertaken to test the following hypotheses in

more depth:

• A decrease of GDP will lead to a decrease in pharmaceutical consumption. The more severe

the decline in GDP, the more severe the decline in pharmaceutical consumption will be.

• Consumption of medicines for an acute indication will decrease more than medicines used

for a chronic indication.

• A shift of the consumption of branded medicine to generic medicines would occur.

• Prices in national currency units (NCU) will increase more in countries which were more

severely affected by the economic crisis.

• The overall pharmaceutical expenditure will stay the same or drop while expenditure in the

public sector will increase and the private sector will decrease, where such information is

available.

• In countries which have a substantial decline in pharmaceutical consumption marker

products can be detected to track changes in pharmaceutical consumption due to an

economic recession.

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

16

Methods

IMS data collection

The data for this study was obtained by Intercontinental Medical Statistics (IMS Health). IMS Health

is a company which provides market intelligence and expert analysis to healthcare providers and

pharmaceutical industries. IMS collects pharmaceutical consumption data from wholesalers,

hospitals and/or dispensing outlets such as pharmacies and drugstores.(10) To gather this

consumption data IMS uses different methods. Within countries IMS uses the same method but the

methodology used varies between countries and depends on the nature of the pharmaceutical

supply systems. IMS collects data in over a hundred countries world-wide. Data used for this study

originates from 84 countries. These 84 countries represent about 81% of the global population.

There is a lack of coverage in the African countries. Only South Africa, Algeria, and some countries in

French West Africa are covered. Morocco, Tunisia and Egypt were covered as well but these

countries belong to the WHO Eastern Mediterranean region. In Central America the data is

combined for Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panama and in French

West Africa for Benin, Burkina, Cameroon, Congo, Gabon, Ivory Coast, Mali, Senegal and Togo.

If IMS does not collect data from all suppliers in a country they project the sample of a particular

distribution channel to the national level. In most low- and middle-income countries, IMS measures

consumption in the private sector. In many countries the private sector is the major or only supplier

to the public sector, which makes it hard to measure both private and public sector. If IMS collects

information on the distribution chain of the private sector, they do not give an estimate based on

this gathered information for the public sector. IMS makes an explicit distinction between countries

where they are able to cover both public and private sector and countries where they are not.

Consumption is expressed as volume in standard units (SU). This is a measure used by IMS derived

from the number of doses. It is measured differently depending on the formulation of the medicine.

It is different from the measure WHO uses, the Defined Daily Dose (DDD). DDD is defined by the

WHO as the assumed average maintenance dose per day for a drug used for its main indication in

adults. (32) Usually one SU equals one capsule, one tablet, one prefilled syringe, one dose of inhaled

medicine or 5 ml of an oral suspension etc. DDD’s and SU’s are used as a measure of consumption of

medicines by patients. Care is needed when standard units are compared between countries as

formulations can differ between countries. In this study we compare changes in SU’s so the

difference in formulation between countries is not an issue.

The European Pharmaceutical Market Research Association (EphMRA) developed an anatomical

classification system (AC-system) which is used by IMS to make the subdivision in acute and chronic

indication. (24) IMS based the subdivision of acute and chronic medicines on an analysis of primary

care records in the United Kingdom as well as subsequent medical review.

The AC-system of EphMRA is used as a base for the Anatomical Therapeutic Chemical classification

system (ATC-system) which is used by WHO as an international standard. Drugs are classified in

three or four different levels in the EphMRA system, while the WHO-ATC-classification uses four to

five levels. The fourth level in the EphMRA system is the molecule level. The fourth level in the WHO-

ATC-classification is a therapeutic/chemical/pharmacological subgroup and the fifth level is the

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

17

chemical substance subgroup. Both classification systems use the abbreviation ATC. In this report

ATC refers to the EphMRA classification.

For the purpose of this study medicines were grouped in two categories: original & licensed brands

and other brands & unbranded medicines. A subdivision in original & licensed brands versus other

brands & unbranded medicines can be used to detect movements from the use of originator

medicines to generics, although there are some complexities within different classes of drugs that

must be taken into account before definitive conclusions can be made. IMS Health defines an

original brand as a brand to be designated as an original brand, with a molecule in the product which

has or has had a molecule patent and is marketed by the patent holder (originator) of that product.

(10) Licensed brands are brands with a license which are sold by a different company than the

originator. Original and licensed brands also include products whose patents are expired but which

are still sold under their brand name. A formulation or process patent or a supplementary protection

certificates are not sufficient criteria on their own to be included in this group.

Products which are being marketed by companies which are neither the originator nor hold a license

from the originator belong to the category other brands & unbranded medicines. Other brands &

unbranded medicines are not the same as generics since products protected by formulation, process

and supplementary protection certificates may be included in this group if no molecule patient

existed. This group also includes branded products that contain ingredients for which there are no

originators. Some examples of these products are some oral contraceptives and insulins, vitamins,

infant milk and homeopathic products. The distinction between other brands & unbranded

medicines can sometimes appear somewhat artificial, depending on how the product is described

rather than how it is either priced or marketed.

Generally IMS collects information about the price of a product from various sources but only from a

single point in the supply chain. This information can relate to average weighted prices, price lists,

reimbursement prices or a combination of all three. IMS estimates the prices charged at other points

in the supply chain using averages based on local country knowledge. Therefore the estimated prices

do not represent actual prices charged at individual product level. The index Price per Standard Unit

is calculated by dividing the total reported value of sales by total volume for each country.

Movements in this index can be a result of new product introductions, government policies relating

to reimbursement prices and approved margins through the distribution chain and/or increases in

generic market share. It is not necessarily a sign of higher prices of individual products. IMS Health

usually collects information based on national currency units. Therefore changes in exchange rates

will not be reflected in prices, unless the change affects the price being charged in the local currency

due to importation costs. In the multi-country audits such as French West Africa and Central

America local currency has been converted to $US or €. As a result exchange rate fluctuations

directly affect the prices seen in IMS Health audits.

Pharmaceutical expenditure depends on the volume of consumption and prices of medicines.

Therefore changes in pharmaceutical expenditure can relate to changes in volume and changes in

prices. Since the pharmaceutical expenditure depends on the prices which are estimated by IMS the

same uncertainties can be applied to the expenditure as to the prices. As with the prices, the

expenditure is also expressed in national currency units.

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

18

Provision of indexed data

IMS provided a dataset with the pharmaceutical consumption in 84 countries for the first quarter of

2008 till the fourth quarter of 2009. Data was provided for two different indices. The first index

shows the evolution compared to the first quarter of 2008 (Q1 08). The first quarter of 2008 was

considered to be at least one quarter before the economic recession struck. By using this index a

comparison can be made between the period before the recession and during or after the recession.

A general formula for the calculation of these index numbers based on Q1 08 for the consumption

expressed in SU’s is:

08 1

nn

Q in s SU'Total

Q in s SU'TotalQ number index =

To calculate the index numbers for expenditure or price per IMS SU total SU’s have to be replaced by

the value for expenditure or price per IMS SU.

To take seasonal variation into account another index number was calculated based on the year

before:

1-n

nn

Q in price or eExpenditur or s SU'total of Value

Q in price or eExpenditur or s SU'total of ValueQ number ndexi =

To acquire more data points for the graphical transformation index numbers for the period Q1 2007 to

Q4 2007 were calculated for consumption, consumption split by acute and chronic indication and split

by original & licensed brands and other brands & unbranded medicines. These index numbers (Q1 07

– Q4 07) are based on Q1 08 and were calculated with the aid of the index numbers based on the year

before and the index numbers of Q1 08:

before year on indexedQ number index

Q on indexedQ number indexQ on indexed Q number Index

08 x

08 1 08 x

08 1 07x =

Graphical transformation methods

After the calculation of index numbers for Q1 07 - Q4 07 MS Excel was used for graphical

representation. To display different changes in the different areas over the world, graphics were

made with the pharmaceutical consumption per WHO region (AFR, AMR, EMR, EUR, SEAR and WPR)

and a global average. To see if the changes were dependent on the income level, countries were

divided into World Bank income categories (high income, upper middle, lower middle and low

income countries). To look in more detail at the countries, which showed an interesting change,

graphics were made with the consumption of these particular countries, other countries of interest

in this WHO region, global average and the average of the WHO-region to which the countries

belong. The weighted averages of pharmaceutical consumption (split by acute and chronic indication

and split by original & licensed brands and other brands & unbranded medicines) were provided by

IMS Health. The averages of the pharmaceutical consumption (split by acute and chronic indication

and split by original & licensed brands and other brands & unbranded medicines), pharmaceutical

expenditure and price per IMS SU per World Bank income category and the averages of the

pharmaceutical expenditure and price per IMS SU per WHO Region were calculated as a crude

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

19

average of the indexed data of the individual countries. The global averages were also calculated as

crude averages of the indexed data of the individual countries.

Economic indicators

Economic indicators describe the statistics of the economy of countries. Different economic

indicators are used for different purposes. Gross Domestic Product (GDP) is a measure for the total

production of a country in a year and therefore a measure for the economic performance of a

country. GDP is defined as the total market value of all final products and services produced within

the borders of a country in a year.

To investigate if a decrease in pharmaceutical consumption correlates with a decrease in growth of

GDP a linear regression analysis was performed. The volumes of GDP in index numbers for the 29

European countries were extracted from the website of EUROSTAT, the statistical agency of the

European Union. The index numbers of Q1 09−Q3 09 compared to the same quarter a year before for

pharmaceutical consumption and GDP were used to correct for seasonal variation. The periods Q1

09−Q3 09 were chosen to compare GDP and pharmaceutical consumption of the most recent periods.

A decline in GDP leads to a decline in exchange rate of a local currency against a hard currency as the

Euro or the US dollar. A lower exchange rate causes an increase in the price of imported raw

materials and medicines. As a result price per IMS SU in national currency will increase. To assess

whether prices (in national currency units) showed a bigger increase if the country was more

affected by the economic recession a linear regression analysis was performed.

For the same reasons as mentioned before the index numbers of GDP and pharmaceutical prices in

European countries for Q1 09 compared to Q1 08 were used.

Shift from private to public sector

People have less to spend during a recession and therefore it was expected that people would make

more use of the facilities in the public sector instead of the private sector. To see if this shift

occurred graphics were made for the countries where IMS could provide data for both sectors:

Brazil, Mexico, South Africa and Uruguay. For the consumption of acute and chronic medication and

original & licensed brands and other brands & non branded medicines graphics were made for each

country. For the overall consumption one graphic is made. Indexed consumption data for the period

Q1 07 – Q4 09 is used for the graphical display of this possible shift. The data is indexed on the first

quarter of 2008.

Country selection

Based on the analysis of the initial series of tables and graphics on the overall consumption countries

with a substantial decline in pharmaceutical consumption were selected to be examined in more

detail on EphMRA ATC 2/3/4 level. Pharmaceutical consumption depends like consumption of other

products on the demand of the consumers. Therefore natural fluctuations in pharmaceutical

consumption are common. Because we did not correct for seasonal variation we only selected

countries with a decrease in pharmaceutical consumption of more than 5% for three consecutive

quarters. Countries were selected based on the data provided up to the first quarter of 2009.

Countries which showed a decline of three consecutive periods after this point in time were not

included in these more detailed analyses.

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

20

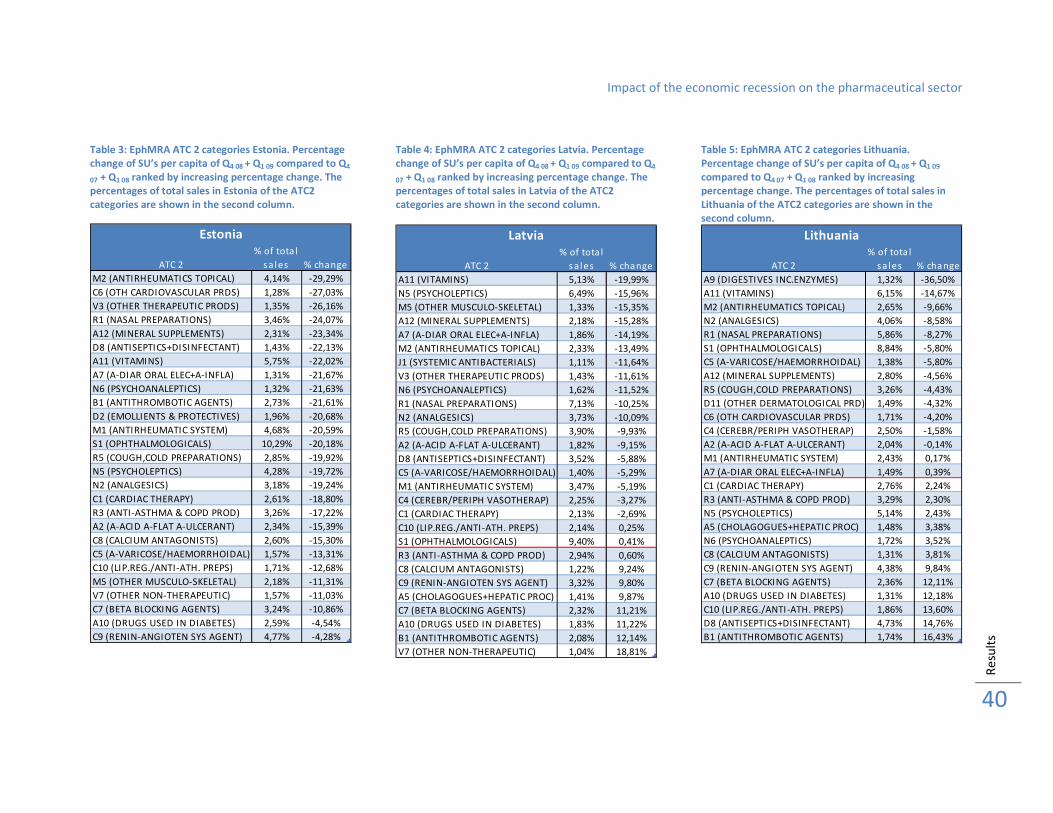

Estonia, Latvia, Lithuania and Romania were selected since these countries showed a substantial

decline in overall consumption. Russia showed a number of declines as well but was not selected

because of the problems with acquiring insight in their health systems. Poland was selected as a

comparator because this is one of the few countries in Eastern Europe which was hardly affected in

terms of the economic crisis. The consumption in Poland dropped by -9% in Q2 08 compared to Q1 08.

However, when looking at the consumption pattern from Q1 07−Q4 09 one observes an increase in

consumption in the first quarter of every year and a constant consumption during the rest of the

year although at a lower level compared to this first quarter.

Impact of the recession on specific groups and individual medicines

One of the goals of this analysis was to detect groups of medicine which showed a big decrease in

consumption and groups of medicines which consumption hardly changed. If possible a selection of

marker medicines in these groups was made.

IMS Health provided a dataset with the SU’s per EphMRA ATC 2 category for the Estonia, Latvia,

Lithuania, Romania and Poland for the period 2007-2009. After sorting the data per country, the

total SU’s per quarter for each country were calculated. With the aid of this total, the SU’s per

EphMRA ATC 2 category were expressed as a percentage of the total SU’s of the corresponding

quarter. An average of these percentages for each EphMRA ATC 2 category was calculated. These

averages were used to make a Pareto analysis per country. For this analysis the EphMRA ATC 2

categories were sorted by highest average percentage of total SU’s. After the data was sorted a

cumulative percentage was calculated to generate a graphic to show the distribution of EphMRA

ATC 2 categories of total consumption. Based on this Pareto analysis 30% of EphMRA ATC 2

categories were selected which accounted for about 80% of total consumption.

Seasonal variation has great influence on the changes in consumption. Therefore it was decided to

compare a specific quarter with the corresponding quarter a year before. The periods Q4 08 and Q1 09

were chosen as quarters during the recession, because these periods contain the most recent data

and it is still possible to compare the values to a period before the recession started. The winter is

also one of the periods in which people have many costs and pharmaceutical consumption is more

likely to be affected.

The SU’s were converted in SU’s per capita for a better comparison of the data between countries.

Population data for the countries in question was extracted from the website of EUROSTAT. The SU’s

per capita for Q4 07 and Q1 08 were added as well as the values for Q4 08 and Q1 09. Of these two values

the absolute and percentage change were calculated. After this calculation a ranking was made

based on the increase in percentage change. These rankings were examined to look for categories

which had a decline in at least three of the four recession hit countries (Estonia, Latvia, Lithuania and

Romania) and preferable not in Poland. This selection was used to select the EphMRA ATC 2

categories of interest for further analysis on EphMRA ATC 3 level. Only EphMRA ATC 2 groups which

could have a potential harmful effect on public health if they are used less by patients were selected.

IMS Health provided a dataset with the SU’s for these specific EphMRA ATC 3 categories, which were

selected. For the EphMRA ATC 3 categories the SU’s per capita were calculated for the period

Q4 07 + Q1 08 and for Q4 08 + Q1 09 and were compared. The percentage change during these periods was

Impact of the economic recession on the pharmaceutical sector

Me

tho

ds

21

calculated. Again it was checked which EphMRA ATC 3 categories in this case met the criteria of

declining in three of the four recession hit countries and not in Poland.

Of these categories the development at product level was investigated to identify possible marker

products to track changes in a recession. Graphics were made of products when SU’s per capita were

available for all five countries (Estonia, Latvia, Lithuania, Romania and Poland). The developments

were checked for selection of possible marker products. A marker product would be a product that

has a sudden change in consumption shortly after the initiation of the recession in Q1 08. Changes in

consumption pattern that started in the beginning of 2007 and continually developed were not

considered to be caused by the economic recession.

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

22

Results

Overall pharmaceutical consumption

Based on the indexed data provided by IMS Health figures were produced to show changes in the

consumption of pharmaceuticals from the first quarter of 2007 to the fourth quarter of 2009. Data

was indexed on the first quarter of 2008 which is at least one quarter before the recession. In most

parts of the world it appears that the pharmaceutical consumption was not affected by the

economic recession. Figure 5 shows that the European region (EUR) the only WHO region is where

consumption is lower compared to before the recession (-6% in Q3 09 compared to Q1 08), although

the consumption in Q4 09 increased. In the other WHO regions the consumption increased, ranging

from +12% (Q4 09) in the American region (AMR) to +28% (Q4 09) in the South East Asian region (SEAR).

1,16

0,93

1,14

1,12

1,18

0,99 1,02

0,95

1,28

1,22

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

1,30

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average pharmaceutical consumption index

Global and WHO regions(Evolution on Q1 08)

GLOBAL AFR AMR EMR EUR SEAR WPR

Figure 5: Pharmaceutical consumption global and by WHO regions. Volumes of consumption in SU’s indexed on Q1 08

were used for this figure. The pharmaceutical consumption in the European region declined after the recession started

(Q1 08) until Q3 09, while the pharmaceutical consumption in the other WHO regions increased.

The current economic recession began in the developed world. To see if the more developed

countries were affected more by the recession change in pharmaceutical consumption was assessed

for different income levels according to World Bank classification (Figure 6). This figure shows that

only the high income countries showed a small decline of -4% (Q3 09 compared to Q1 08) while the

other countries with less income all had an increase in their consumption. The low income countries

even had an increase of +18% in Q4 09 compared to the first quarter of 2008.

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

23

1,16

0,97

1,04

0,96

1,06

0,93

1,12

1,01

1,18

0,90

0,95

1,00

1,05

1,10

1,15

1,20

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average pharmaceutical consumption index

Global and World Bank income categories(Evolution on Q1 08)

Global High income Upper middle income Lower middle income Low income

Figure 6: Pharmaceutical consumption global and by World Bank classification. Volumes of consumption in SU’s indexed

on Q1 08 were used for this figure. Only the high income countries showed a slight decline for three consecutive quarters

after the recession, until Q3 09.

Since averages per region do not give a clear picture about developments at country level, charts

were produced to look in more detail at developments in specific regions. Most of the 84 countries

did not show a decline in their pharmaceutical consumption. China even had an increase in

pharmaceutical consumption of +40% (Q4 09 compared to Q1 08) (see Figure 7). However there were

some exceptions: Estonia (-28% Q3 09), Latvia (-24% Q3 09), Lithuania (-17% Q3 09), Romania

(-11% Q3 09), Mexico private sector (-14% Q3 09) and Russia both private (-19% Q3 09) and public sector

(-35% Q2 09) all showed a severe decline in pharmaceutical consumption. Italy and the United Arab

Emirates showed a decline for three consecutive quarters as well, but their pharmaceutical

consumption increased in Q1 09. Malaysia only showed a decline of five consecutive quarters starting

in Q4 08 (-7% Q4 09 compared to Q1 08) (Figures 7 & 8).

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

24

1,16

0,95

1,22

0,90

1,40

0,97

0,93

0,80

0,90

1,00

1,10

1,20

1,30

1,40

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Pharmaceutical consumption

WPR, China and Malaysia(Evolution on Q1 08)

GLOBAL WPR CHINA MALAYSIA

Figure 7: Pharmaceutical consumption in WPR, China and Malaysia. Volumes of consumption in SU’s were used for this

figure and indexed on Q1 08. Malaysia showed a decline of -7% in Q4 09 compared to Q1 08, while China showed an

increase of +40% in the same period.

0,99

1,021,02

0,97

0,89

0,86

1,03

0,88

0,98

0,70

0,75

0,80

0,85

0,90

0,95

1,00

1,05

1,10

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Pharmaceutical consumption

EUR, Poland, Romania and Baltics(Evolution on Q1 08)

EUR Poland Estonia Latvia Lithuania Romania

Figure 8: Pharmaceutical consumption in EUR, Poland, Romania and the Baltic States. Volumes of consumption in SU’s

were used for this figure and indexed on Q1 08. Romania and the Baltic States showed substantial declines in their

pharmaceutical consumption.

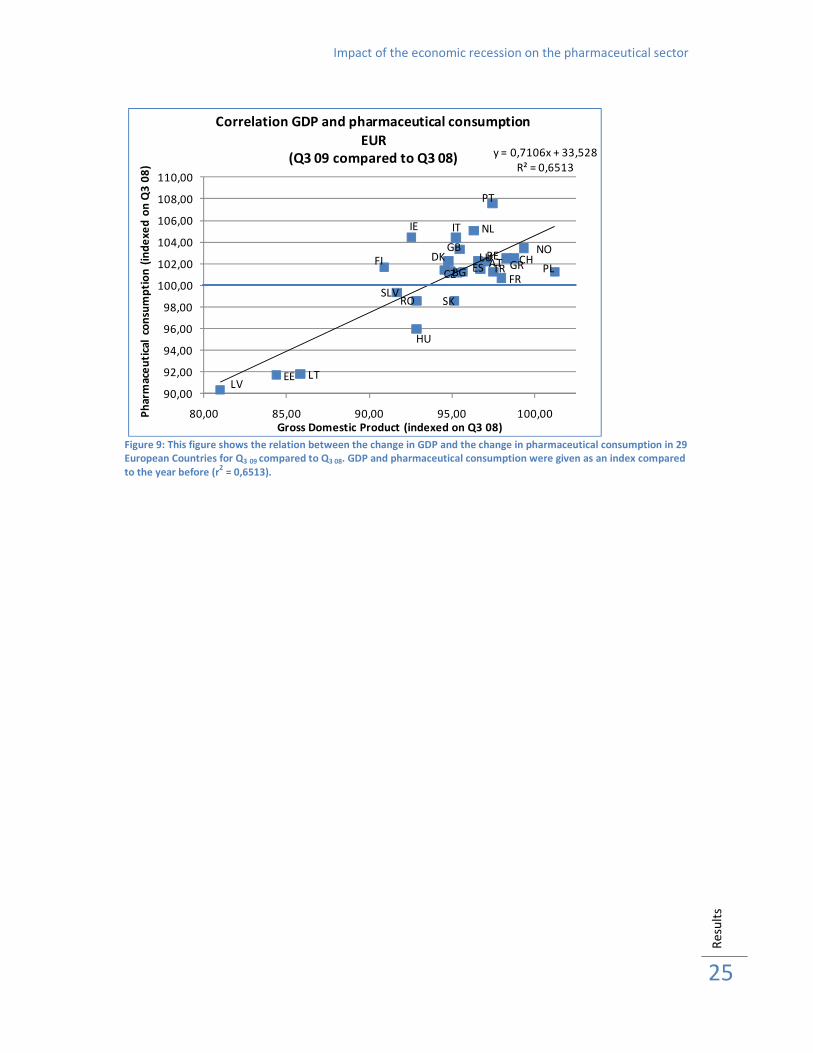

One of the hypotheses was that a decline in GDP will lead to a decrease in pharmaceutical

consumption. Figure 9 shows that in the European region a greater decline in GDP may be associated

with a lower pharmaceutical consumption, although this relationship is moderate and varied over

different quarters(r2 = 0,3914 to 0,6513 see Annex 1: Correlation decline in GDP and pharmaceutical

consumption). Many countries had a decline in GDP but only a limited number of countries (i.e.

Estonia, Latvia, Lithuania and Romania) had a severe decline in pharmaceutical consumption.

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

25

ATBE

BGCZ

DK

EE

FI

FR

IT

GR

HU

IE

LVLT

LU

NL

NO

PL

PT

RO SKSLV

ESCH

TR

GB

y = 0,7106x + 33,528

R² = 0,6513

90,00

92,00

94,00

96,00

98,00

100,00

102,00

104,00

106,00

108,00

110,00

80,00 85,00 90,00 95,00 100,00Ph

arm

ace

uti

cal

con

sum

pti

on

(in

de

xe

d o

n Q

3 0

8)

Gross Domestic Product (indexed on Q3 08)

Correlation GDP and pharmaceutical consumption

EUR

(Q3 09 compared to Q3 08)

Figure 9: This figure shows the relation between the change in GDP and the change in pharmaceutical consumption in 29

European Countries for Q3 09 compared to Q3 08. GDP and pharmaceutical consumption were given as an index compared

to the year before (r2 = 0,6513).

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

26

Consumption of medicines for acute and chronic indications

The research IMS Health performed on the ‘97-’98 Asian Crisis showed that the consumption of

medicines for acute indications decreased more and took longer to return to the pre-recession

values than the consumption of medicines for chronic indications. Figures 10 & 11 show that there is

little difference between the development of the consumption of medicine for an acute or chronic

indication on global and WHO region level. Again the European region is the only region where the

consumption of medicines for both acute and chronic indication declined, until Q3 09. The

consumption of medicines for acute indications decreased from Q1 08 onwards to -9% in Q3 09. The

consumption of medication for chronic indications decreased from Q1 08 with a recovery in Q4 08 and

Q1 09 to a decline of -6% in Q3 09. The increase in the other regions ranged from +7−+26% (Q4 09

compared to Q1 08) for the acute indications and from +13−+29% (Q4 09 compared to Q1 08) for the

chronic indications.

0,96

1,13

1,07

1,11

0,93

1,20

1,00

0,98

1,26

1,18

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

1,30

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index of medicines for acute indication

Global and WHO regions(Evolution on Q1 08)

GLOBAL AFR AMR EMR EUR SEAR WPR

Figure 10: Consumption of medicines for acute indication for the WHO regions. The European region showed a decline in

consumption of medicines with an acute indication up to -9% in Q3 09 compared to Q1 08. The other regions showed an

increase in the consumption of medicines with an acute indication.

0,92

1,13

1,17

0,981,03

1,29

0,96

1,23

0,85

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

1,30

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index of medicines for chronic indication

Global and WHO regions(Evolution on Q1 08)

GLOBAL AFR AMR EMR EUR SEAR WPR

Figure 11: Consumption of medicines for chronic indication for the WHO regions. Again the European region was the

only region with a decline (-6% in Q3 09 compared to Q1 08).

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

27

0,96

1,13

0,98

1,001,02

0,93

1,12

1,17

0,90

0,95

1,00

1,05

1,10

1,15

1,20

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index medicines with acute indication

Global and World Bank income categories(Evolution on Q1 08)

Global High income Upper middle income Lower middle income Low income

Figure 12: Consumption of medicines with an acute indication for the World Bank income categories. Countries with a

high income showed a decline from the beginning of the recession. After an initial increase, the consumption decreased

in the upper middle income countries in 2009 and seems to recover in Q3 09 and Q4 09.

0,95

1,17

0,97

1,06

1,07

0,93

1,02

1,13

0,90

0,95

1,00

1,05

1,10

1,15

1,20

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index of medicines with chronic indication

Global and World Bank income categories(Evolution on Q1 08)

Global High income Upper middle income Lower middle income Low income

Figure 13: Consumption of medicines with a chronic indication. In all the World Bank income categories there was an

initial increase in consumption of medicines for a chronic indication. Only the high income countries showed a decline of

-3% in Q3 09 compared to Q1 08.

High- and upper middle income countries did show a difference between the consumption of acute

and chronic medicines (Figures 12 & 13). While the consumption of acute medicines declined slightly

by -4% (Q3 09 compared to Q1 08), the consumption of chronic medication increased by approximately

+2 to +3% until Q2 09 in the upper middle income countries and by -7% and -3% (Q3 09) respectively in

the high income countries. In Q3 09 the consumption in the upper middle income countries seemed to

be recovering, whereas the consumption of both acute and chronic medication in the high income

countries was still decreasing in Q3 09 and seemed to be recovering in Q4 09. In the lower middle and

low income countries the development was similar, the consumption of both categories increased

within a range of +12−+17% (Q4 09) for acute and +13−+17% (Q4 09) for chronic indications. Similar

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

28

patterns were observed in those countries which had the largest overall decline (see Annex 2

Consumption of medicines for acute and chronic indications).

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

29

Consumption of original & licensed brands and others brands & unbranded

medicines

People have less money to spend during a recession. Therefore it would be expected that a shift

would occur from the original & licensed brands to the other brands & unbranded medicines if the

original & licensed brands are more expensive.

No shift from original & licensed brands to other brands & unbranded medicines is seen so far at

WHO regional and global level (Figures 14 & 15). The American region seemed to be an exception to

this pattern. The consumption of original & licensed brands decreased continually, in Q4 09 it was -5%

less than the consumption in Q1 08. This decrease is probably not caused by the recession since the

decrease is seen ever since the beginning of 2007. The consumption of other brands & unbranded

medicines in the American region is increasing from Q1 07 onwards to +13% in Q4 09 compared to Q1 08.

Except for a greater variation in the consumption of original & licensed brands there was no

difference between the consumption of original & licensed brands and other brands & unbranded

medicines at World Bank level (Figure 16Figures 16 & 17). The consumption of both original &

licensed brands and other brands & non branded medicines was increasing in all the income

categories with +6−+20% (Q4 09). Only in the high income countries the consumption of both original

& licensed brands and other brands & unbranded medicines decreased, in Q3 09 with respectively -5%

and -2% compared to the first quarter of 2008. The consumption of both original & licensed brands

and other brands & unbranded medicines declined in Malaysia (see Annex 3: Consumption of

original & licensed brands and others brands & unbranded medicines). The consumption of original &

licensed brands and other brands & unbranded medicines increased at the same pace in China

(respectively with +27% and +29% in Q3 09 compared to Q1 08).

Impact of the economic recession on the pharmaceutical sector

Re

sult

s

30

0,99

1,08

1,18

1,07

0,95

0,91

1,011,00

0,88

1,05

0,97

1,12

0,85

0,90

0,95

1,00

1,05

1,10

1,15

1,20

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index original & licensed brands

Global and WHO regions(Evolution on Q1 08)

GLOBAL AFR AMR EMR EUR SEAR WPR

Figure 14: Consumption of original & licensed brands for the different WHO regions. The American region (AMR) shows

a small decline from the beginning of 2007.

0,98

1,13

0,93

1,04

1,18

0,95

1,22

0,85

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Average consumption index other brands & unbranded medicines

Global and WHO regions(Evolution on Q1 08)

GLOBAL AFR AMR EMR EUR SEAR WPR

Figure 15: Consumption of other brands & unbranded medicines for the different WHO regions. In most regions the