Embed Size (px)

Citation preview

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 1/13

IMPORTANT POINTS

A. INDIVIDUAL TAXATION –– FILING STATUS

• FILING

• Due date :- April 15

• With either extension, due date for payment of taxes remains April 15

• FILING STATUS

• END OF YEAR test

• In order to file a joint return, the parties must be MARRIED at the end of the year .

Exception: If the parties are married but are LEGALLY SEPARATED under the laws

of the state in which they reside, they cannot file a joint return (they will file either

under the single or head of household filing status).

• In order to avoid confusing the required time period for different filing statuses, justremember:

Widow/widower = Whole year

Head of household = Half a year (more than)

B. INDIVIDUAL TAXATION –– EXEMPTIONS

• PERSONAL EXEMPTIONS

• 2008 -- $3,500

• Persons claimed as dependents

• Married taxpayers◦ each spouse receives personal exemption

◦ Spouse as personal exemption on a separate return ( spouse is not a

dependent & spouse is not filing any return)

• Birth or Death during the Year

◦ entitled to personal exemption for the entire year

• DEPENDENCY EXEMPTIONS

• For each qualifying child and qualifying relative

• A taxpayer will be entitled to a full dependency exemption for anyone that a taxpayer

““CARES”” for, or that they ““SUPORT””, even if the dependent:Was born during the year

OR

Died during the year

• Option 1 : Qualifying Child (CARES)

1. Close Relative

2. Age Limit

◦ child under age 19 (or age 24 in case of a full-time student)

◦ exception – totally & permanently disabled

3. R esidency Requirement

◦ taxpayer = child = same principal place for more than half of the year

4. Eliminate Gross Income Test

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 2/13

◦ does not apply to a qualifying child

5. Support Test Changes

◦ to determine if the child did not contribute more than one-half of his or her

own support

◦ legally adopted vs foster child.txt

◦ Qualifying Child Rules 2008 vs 2009.doc

• Option 2 : Qualifying Relative (SUPORT)

1. Support (over 50%)Test

◦ tax payer must have supplied more than 50% of the support of a person in

order to claim him or her as a dependent

◦ Multiple support agreements (2 or more taxpayers together contribute more

than 50%, not individually)A contributor must have contributed more than 10% of the person ’ s support

◦ Child of a Divorced Parent

-GR: Custodial parents -- takes the exemption

Exception: - Noncustodial parent is allowed a dependency exemption

if custodial parent waives right

QR doesn’t depend on the age of the child because...

1. A child who is permanently disabled the age test does not apply.

2. For divorced or separated parents the rule should be whoever

provided a) more than half of the support b) whatever the divorcee

decree states3.Child of any age can be claimed as a dependent as long as (s)he

does NOT file a joint return or if s(he) does its for a refund of tax.

Yes, that is correct. After that age limit, they are no longer a qualifying

child. Then the qualifying relative rules come into play.

2. Under a specific amount of (taxable) gross income test

◦ less than exemption amount ($3,500 for 2008)

◦ tax free income is ok

3. Precludes dependent filing a joint tax return

◦ A taxpayer will lose the exemption for a married dependent who files a joint return unless the joint return is filed solely for a refund of all taxes paid or

withheld for the taxable year (i.e., the tax is zero)

4. Only citizens (residents of U.S./Canada or Mexico) test

5. R elative test

◦ children, grandchildren, parents, grandparents, brothers, sisters, aunts &

uncles, nieces & nephews, stepchildren, in-laws, legally adopted children,

foster children, child born at any time during the year

OR

6. Taxpayer lives with individual for whole year test – if not related

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 3/13

◦ Foster parents and cousins

◦ Others not qualifying as a relative

• RULE :-

◦ No additional exemption for being old (age 65) or/and blind

◦ It is an increased standard deduction

• PHASE OUT OF PERSONAL AND DEPENDENCY EXEMPTIONS

C. INDIVIDUAL TAXATION –– GROSS INCOME

• Gross Income in General

◦ Taxable event = FMV income = FMV Basis

◦ Non-taxable event = N-O-N-E income = NBV Basis

• Specific Items of Income and Exclusions

1. Salaries and Wages

Refer “handwritten” table

2. Interest Income

- Taxable Interest

◦ General Rule – ALL INTEREST IS TAXABLE

◦ Premiums received for opening a savings account included at FMV

◦ Interest paid by federal or state government for late payment of tax refund is

taxable◦ Interest income from U.S. obligations is generally taxable.

◦ Tax Exempt Interest ( reportable but not taxable)

▪ Interest on state & local bonds/obligations is tax exempt.

▪ Mutual fund dividends for funds invested in tax-free bonds are tax

exempt

▪ Interest on series EE (U.S. Savings Bond) – to pay for educational

expenses reduced by tax free scholarships

Phaseout starts when modified AGI exceeds an indexed amount

◦ Kiddie Tax –– unearned income of a child under 18

▪ Taxed at his parent ’ s higher tax rate

3. Dividend Income

◦ Source determines taxability

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 4/13

◦ Taxable dividends

▪ special (lower) tax rate:-

Qualified dividends holding period – stock held for more than 60 days during

the 120-day period beginning 60 days before the ex-dividend dates

◦ Tax-Free dividends

• Return of capital

• Stock split

• Stock dividend (unless cash or other property option/taxable FMV)

If a taxpayer has the option of taking a dividend either in stock or in other property

(e.g., cash), the dividend is taxable regardless of the option the taxpayer selects.

• Life insurance dividend – dividends caused by ownership of insurance with a mutual

company (premium return)

◦ Capital Gain Distribution No earnings & profits / shareholder has recovered his or her entire basis,

are treated as taxable gross income

4. State and Local Tax Refunds

• Prior year itemized deduction = taxable state or local refund

• Prior year used standard deduction = nontaxable state or local refund (1040 EZ on the

exam)

5. Payments pursuant to a divorce

• Alimony/Spousal support :- Income• Child Support :- Non-Taxable

◦ DeadBeat Dad :- Payment first applies to child support

• Property settlements :- Non-taxable

• Alimony Recapture.doc

6. Business Income or Loss, Schedule C or C-EZ

• Net income from self-employment

• Gross Business Income – Business expense = Profit or Loss

• Income from farming activities is reported in a manner very similar to other businesses (those reporting on a Schedule X), but the related income and expenses are

reported on Schedule F .

For tax purposes, a “farmer ” is a person (or entity) who operates or

manages a farm with the intent of earning a profit.

Farming income - communication.MDI

• Gross Income

• guaranteed payment to partner - self employment tax.doc

• Expenses = incurred & paid

◦ business meal & entertainment expenses at 50% (100% deductible as itemized

deduction where all proceeds go to charity)

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 5/13

◦ interest expense on business loans (only for the tax year/period to which the

interest relates)

◦ Bad debts actual w/o for accrual basis taxpayer ( direct write off method)

• Nondeductible expenses (on Schedule C)

◦ salaries paid to sole proprietor

◦ federal income tax

◦ any personal portion of expenses

◦ Bad debt expense of a cash basis tax payer (who never reported the income)

◦ Charitable contributions ( use Schedule A)

• It is important to ONLY subtract business expenses from business income. Itemized

deductions and/or other adjustments are deducted elsewhere

• Net Business Income or Loss is taxable

◦ two taxes on net income – income tax & federal self-employed (SE) tax

◦ a business with a loss may deduct the loss against other sources of income

Loss > other sources of income: - 2-year carryback OR 20-year carryforward

• Uniform Capitalization Rules

For inventory, even a sole proprietor will be required to apply the following

rules:-

Capitalized as inventory: - direct materials, direct labor & factory OH

Period expense: - selling, general, administrative, research & development

7. Gains and Losses on Disposition of property

• Realized = amount realized – adjusted basis of assets sold

8. IRA Income (retirement money)

• GR :taxable when withdrawn – cannot be withdrawn until the age of 59.5

• Traditional and Roth- Non-Deductible IRAs.doc

• Taxation of Distributions (benefits)

- Regular tax:

Traditional Deductible IRA

Distributions

Roth IRA Traditional Non-deductible IRA

Ordinary Income Qualified benefits Principal – non-taxable

Taxable Non-Taxable Accumulated earnings – taxable (when

withdrawn)

◦ Penalty tax: 10% on premature distribution in addition to regular income tax

◦ Exception to penalty tax

Home buyer (1st time)

Insurance (Medical) – unemployed & self employed

Medical expenses

Disability (permanent or indefinite)

Education

And

Death

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 6/13

9. Annuities

• Treat like depreciation

• Non-taxable = investment/factor (based on age of annuitant)

• Live longer than Actuarial Payout period : further payments are fully taxable

• Death before full recovery : unrecovered portion is a miscellaneous itemized

deduction

10. Rental Income (Passive Activity )

• Schedule E

• Rental real estate, royalties

• From schedule K-1 : partnerships & LLCs, S-Corporations, Estates & Trusts

• Formula :- Net Rental income or Net Rental Loss

Gross Rental Income

Prepaid rental income (non-refundable deposit)

Rent Cancellation paymentImprovement In-Lieu-of rent (at FMV)

< Rental expenses>

• Rental of vacation home

◦ less than 15 days :-

a. Personal residence

b. Mortgage interest & real interest taxes deductible

c. Depreciation, utilities & repairs not deductible

◦ rented 15 or more days

a. if used for personal purposes for the greater of (i) more than 14 days or (ii)more than 10% of the rental days, is treated as a personal/rented residence

b. expenses pro-rated on basis of usage (different pro-ration for mortgage

interest & property taxes – annual b/w rented & personal)

c. Rental use expenses restricted to extent of rental income

• Passive Activity Losses (PALs)

◦ May not be deducted against wages, salaries, other active income or against

interest & dividends or capital gains income

◦ Carryforward without any time limit held in suspension

a. used to offset passive income in future years b. unused – become fully tax deductible in the year the property is disposed of

(sold)

c. passive to active – then can be offset against active income in same activity

◦ Exceptions –– if either of following 2 conditions are met

a. Mom and Pop Exception

◦ $25,000 and “Active”

◦ Carryforward

◦ Phaseout – $25,000 reduced by 50% of excess of taxpayer ’ s AGI over

$100,000. allowance completely eliminated when AGI exceeds $150,000

b. Real Estate Person/Professional (Not Passive Activity)

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 7/13

◦ more than 50% of the taxpayer ’s personal services during the year are performed in

real property businesses, and

◦ the taxpayer performs more than 750 hours of services in real property businesses

during the year

◦ The rule limiting the allowability of passive activity losses and credits applies

to personal service corporations.

- The passive activity limitations apply to the various partners in the partnership as

opposed to the partnership itself.

◦ The passive activity limitations apply to the various shareholders in the S

corporation as opposed to the corporation itself.

- The passive activity rules do not apply to widely-held C corporations.

◦ Passive Activity Losses - irs.gov.doc

11. Unemployment Compensation

• Full amount received included in gross income

• 2009: $2,400 amount to be excluded

12. Social security income

• Low income = No SS benefits taxable

• Upper Income = 85% of SS benefits taxable

13. Taxable Miscellaneous Income

• Prizes and Awards : Taxable at FMV

• Gambling winnings: included in gross income

• Gambling Losses: deductible ONLY to the extent of gambling winnings. On schedule

A as itemized deduction but not subject to 2% of AGI limitation on miscellaneous

itemized deductions

• Business Recoveries: if damage award is compensation for lost profit, the award is

income

• Punitive damages: fully taxable as ordinary income

◦ The pension distributions from a qualified plan, paid for exclusively by the

employer, are fully taxable.

◦ Jury duty pay is fully taxable as other income on Form 1040, page 1.

14. Partially Taxable Miscellaneous Items : Scholarships & Fellowships

• Degree seeking student - Taxable : Room & Board OR services required

• Non degree seeking student - Taxable : full amount at FMV

15. Nontaxable Miscellaneous Items

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 8/13

• Life insurance proceeds

• Gifts & inheritances

• Medicare benefits

• Workers’ compensation

• Personal (Physical) Injury award

• Accident insurance – premiums paid by taxpayer

• Foreign earned income exclusion (for taxpayers working abroad) $87,600 (yr 2008)

Any one of the following 2 tests:-

◦ Bona Fide Residence test – of foreign country for an entire taxable year

◦ Physical presence test – present in foreign country for 330 days out of any

12-consecutive-month period (which may begin on any day)

◦ Exclusion cannot exceed the taxpayer ’ s foreign earned income reduced by the

taxpayer ’ s foreign housing exclusion

• RECONCILIATION B/W MODIFIED AGI and AGI

• MAGI – Modified Adjusted Gross Income – provisional income (needed to calculate

contributions to Roth IRA and phaseouts)

• The below items are not taken into account while determining AGI vs. MAGI :-

a. Any income you excluded because of the foreign

earned income exclusion b. Any exclusion or deduction you claimed for foreign

housing

c. Any interest income from series EE bonds that you

were able to exclude because you paid qualified

higher EE

d. Any deduction you claim for student loan interest or

qualified tuition & related expenses

e. Any employer-paid adoption expense you excluded

f. Any deduction you claimed for annual (non-

rollover) contribution to a regular IRA

• POINTS FROM PASSMASTER

◦ Self-employment tax and self-employment health insurance expenses are

adjustments from total gross income. They are not deducted from self-

employment earnings (i.e., not reported net on line 12 of the Form 1040).

• A payment to a student for a part-time teaching assignment is taxable income just as

a payment for any other campus job would be. This is not a scholarship or fellowship.

There is no exclusion in the tax law for amounts paid to a degree candidate

for participation in university-sponsored research.

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 9/13

• An exclusion from income for certain prizes and awards applies where the winner

is selected for the award without entering into a contest (i.e., without any action on

their part) and then assigns the award directly to a governmental unit or charitable

organization.

D. INDIVIDUAL TAXATION –– CAPITAL GAINS AND LOSSES

• DEFINITIONS

◦ Real property – Land and Building

◦ Personal Property – Machinery and equipment – not classified as real

property

◦ Capital Assets – Real and personal property

◦ Non-capital Assets –

◦ inventory or property held for sale in the ordinary course of business

◦ depreciable personal property & real estate used in trade or business ( for

example, Section 1231, Section 1245, and Section 1250 property)

• CALCULATON RULES

◦ Gain or Loss = Amount Realized – adjusted basis of asset sold

◦ Amount Realized

◦ cash received (boot)

◦ cancellation of debt (boot) – whether or not buyer expressly assumes the

mortgage◦ property received at FMV

◦ services received at FMV

◦ reduce the amount realized by any selling expenses

◦ Adjusted Basis of asset sold

◦ Purchased Property basis= Cost

a. Increase basis for capital improvements

b. Reduce basis for accumulated depreciation (=NBV)

c. “ Spreading ” adjustments (example, nontaxable stock dividend lowers

the per share basis of stock held)

◦ Gift Property basis

a. GR : Donor ’ s Rollover Cost Basis (Rollover cost/NBV)

Increased by any gift tax paid

b. Exception : Lower FMV at Date of Gift

Sell higher than rollover basis à Use “donor basis” to determine gain

Sell between à No gain or loss

Sell lower than FMV à Use “lower FMV at date of gift “to determine

loss

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 10/13

c. Holding Period

Recipient of the gift normally assumes the donor ’s holding

period

If FMV at the time of the gift is used (loss basis) as the

gift basis, the holding period starts as of the date of the gift

◦ Inherited Property basis

a. GR : Date of Death FMV becomes basis ( step up FMV)

b. Alternate valuation date – available only if its use lowers the entire gross estate &

estate tax

If the alternate valuation date is validly elected, the asset is valued

using FMV at the earlier of:

- Distribution date of asset

- Alternate valuation date (earlier of 6 months after death or date of distribution/sale) – MAX. 6 MONTHS

c. Holding Period

Long term

◦ All realized gains and losses are recognized (i.e., reported on the tax return)

unless “HIDE IT”” or “WRaP”” applies

◦ Gains (Excluded or Deferred)◦ Homeowner ’s exclusion

partial homeowners exclusion.txt

◦ Involuntary conversions

◦ Divorced property settlement

◦ Exchange of like-kind business/investment assets (tangible)

▪ Recognized gain = lower of realized gain or the boot received

▪ New basis = Carryover basis – cash (boot) received + Gain

recognized

▪ GR: When boot is given no gain or loss is recognized. Exception: When property with a difference between FMV and NBV

is distributed.

Like kind property.doc

◦ Installment sale

Not available for sales of stocks or securities traded on an established market.

Immediate recognition can be selected

Recognize when cash is received

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 11/13

Reportable Installment Sale Gain/Income

Gross profit = Sale – COGS

Gross profit% = Gross profit/sales price

Earned revenue = cash collections x gross profit%

◦ Treasury & capital stock transactions (by corporation)

◦ Losses (Non Deductible)

◦ Wash sale loss

The CPA examination has often tested the wash sales rules by having the

taxpayer purchase shares of the same stock 30 days before the sale of the stock

that resulted in a loss.

This is still a wash sale, and the loss is disallowed. For example, on 1/4/08 you

buy one share for $100. On 3/5/09, you buy another share for $40. Then, on

3/15/09, the first share is sold for $41. While you have“realized

”a $59 loss, itwill not be recognized due to wash sale rules.

◦ R elated party transactions

Capital gains

Capital gains taxes imposed except:

a. sales b/w husband & wife (where basis is merely

transferred ), &

b. an individual and a 50% + controlled corporation or

partnership (where the gain is taxed as ordinary income)

Capital losses Disallowed on most related party sales transactions even if they were made at

an “ arms-length” FMV price

Basis rules

Sell higher than first relative’’s basis à Use “relative basis” to

determine gain

Sell between à No gain or loss

Sell lower than purchase price by second relative à Use “ purchase

price” to determine loss

◦ and

◦ Personal loss: - Loss on the sale of the family car is a non-deductible

personal loss.

No deduction is allowed for the loss on a non-business disposal or loss.

An itemized deduction may be available in the category of casualty & theft

• INDIVIDUAL CAPITAL GAIN AND LOSS RULES

◦ Net Capital Gains rules

a. Long term

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 12/13

Holding period – more than one year

Tax rate – 15% is the max, use 5% if taxpayer is in the 10% or

15% income tax bracket. In 2008, 2009, and 2010, the tax rate

on eligible dividends and long term capital gains is 0% for those

in the 10% and 15% income tax brackets

b. Short term

Holding period – one year or less

Tax rate – treated as ordinary income

◦ Net Capital Loss deduction and Loss carryover rules

◦ $3,000 maximum deduction

◦ Carryforward excess net capital loss an unlimited time until exhausted

- Personal (non-business) bad debt loss is treated as a short term capital loss in

the year debt becomes totally worthless

◦ Netting Procedures

Short-term Capital Gains and Losses

1. If there are any short-term capital losses (this includes any short-

term capital loss carryovers), they are first offset against any short-term gains

that would be taxable at the ordinary income rates.

2. Any remaining short-term capital loss is used to offset any long-

term capital gains from the 28% grate group (e.g., collectibles).

3. Any remaining short-term capital loss is then used to offset any

long-term gains from the 25% group ( e.g., un-recaptured Section 1250 gains).4. Any remaining short-term capital loss is used to offset any long-

term capital gains applicable at the lower (e.g., 15%) tax rate.

Long-term Capital Gains and Losses

1. If there are any long-term capital losses (this includes any long-term

capital loss carryovers ) from the 28% rate group, they are first offset against

any net gains from the 25% rate group and then against net gains from the

15% rate group.

2. If there are any long-term capital losses (this includes any long-term

capital loss carryovers) from the 15% rate group, they are offset first against any net gains from the 28% rate group and then against net gains from the

25% rate group.

• CORPORATION CAPITAL GAIN AND LOSS RULES (applies to C

Corporations only)

◦ Net Capital Gains (Long-term & Short-term)

Net of short-term and long-term capital gains & losses of a corporation are

added to ordinary income and taxed at the regular tax rate

◦ Net Capital Losses (Long-term & Short-term)

8/4/2019 Important Points r1

http://slidepdf.com/reader/full/important-points-r1 13/13

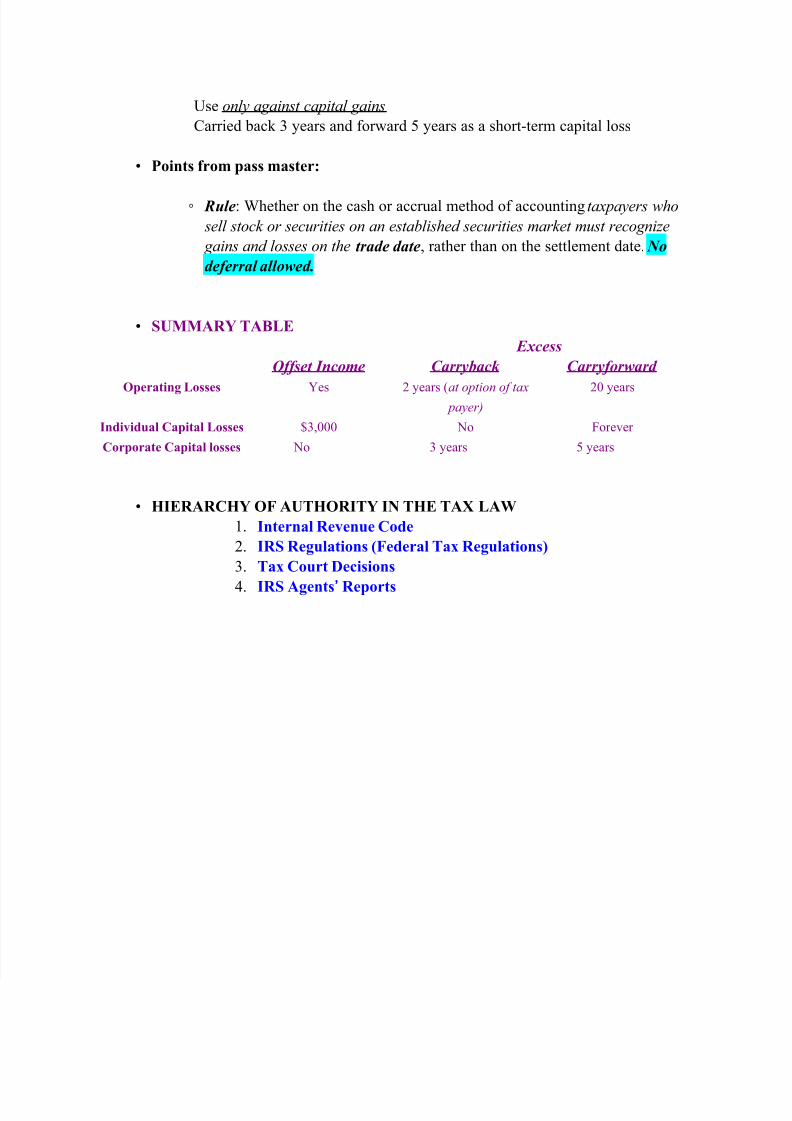

Use only against capital gains

Carried back 3 years and forward 5 years as a short-term capital loss

• Points from pass master:

◦ Rule: Whether on the cash or accrual method of accounting taxpayers who

sell stock or securities on an established securities market must recognize

gains and losses on the trade date, rather than on the settlement date. No

deferral allowed.

• SUMMARY TABLE

Excess

Offset Income Carryback Carryforward

Operating Losses Yes 2 years (at option of tax payer)

20 years

Individual Capital Losses $3,000 No Forever

Corporate Capital losses No 3 years 5 years

• HIERARCHY OF AUTHORITY IN THE TAX LAW

1. Internal Revenue Code

2. IRS Regulations (Federal Tax Regulations)

3. Tax Court Decisions

4. IRS Agents’’Reports