Embed Size (px)

Citation preview

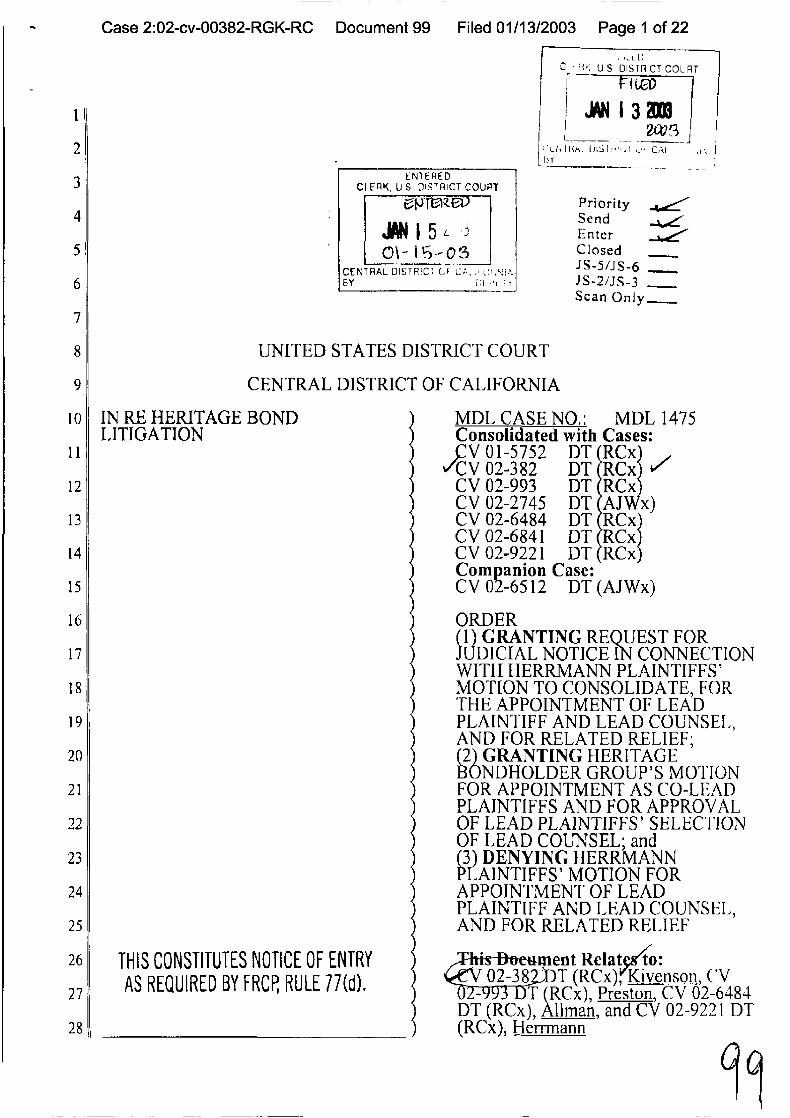

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 1 of 22

2

ENTEREDCLERK . U 5 DISTRICT COURT

PTip

,SIN 15 L

CENTRAL DISTRICT (,F Cam, ' ,)+,h!,.$Y iil 'P' E `T

UNITED STATES DISTRICT COURT

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

U 5 DISTRICT COURT

JAN 13 M

1)Y

CENTRAL DISTRICT OF CALIFORNIA

IN RE HERITAGE BONDLITIGATION

THIS CONSTITUTES NOTICE OF ENTRYAS REQUIRED BY FRCP, RULE 17(d).

PrioritySendEnterClosedJS-5/J S-6JS-2/JS-3Scan Only

MDL CASE NO.: MDL 1475Consolidated with Cases:V 01-5752 DT RCx

3CV 02-382 DT RCxCV 02-993 DT RCxCV 02-2745 DT AJ x)CV 02-6484 DT RCxCV 02-6841 DT RCxCV 02-9221 DT RCxCompanion Case:CV 02-6512 DT (AJWx)

ORDER1 GRANTING REQUEST FORDICIAL NOTICE IN CONNECTION

WITH HERRMANN PLAINTIFFS'MOTION TO CONSOLIDATE, FORTHE APPOINTMENT OF LEADPLAINTIFF AND LEAD COUNSEL,AND FOR RELATED RELIEF;(2) GRANTING HERITAGEBONDHOLDER GROUP'S MOTIONFOR APPOINTMENT AS CO-LEADPLAINTIFFS AND FOR APPROVALOF LEAD PLAINTIFFS' SELECTIONOF LEAD COUNSEL- and

DENYING HERRMANNPAINTIFFS' MOTION FORAPPOINTMENT OF LEADPLAINTIFF AND LEAD COUNSEL,AND FOR RELATED RELIEF

ent Relat to:2-382-DT (RCx), Kivenson , CV

T (RCx), Preston , CV 02-6484DT (RCx), A11man , and CCV 02-9221 DT(RCx), Herrmann

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:02-cv-00382-RGK-RC Document 99

1. Background

A. Factual Summary

Filed 01/13/2003 Page 2 of 22

Plaintiffs Gilbert Kivenson , Howard Preston , Rosanna Preston, Ray

Stits, Edith Stits, Ralph Allman, Sigrid Allman, Barrett Anderson, Scott McKenry,

and Laurence Pilgeram bring this action on behalf of themselves and all others

similarly situated against U.S. Trust Company of Texas, N.A.; U.S. Trust Corp.;

Danforth Health Facilities Corp.; Tarrant County Health Facilities Development

Corp.; City of Mexico Beach; City of Chicago; Desert Hot Springs Public

Financing Authority; Jerold Goldstein; Onofrio V. Bertolini; Stephen P. Goodman,

Evan Greenspan; Andrew Kornreich; Cary Medill; Estate of Emery Rubin; Larry

A. Rubin; Herbert Saltzman; Virgil Lim; Clarke Underwood; Donald B. Chalker;

Marshall Wexler; Robert Kasirer; Debra Kasirer; Bistra & Munkacs Holdings;

Inc.; JDDJ Holdings, L.P.; Health Care Holdings, LLC; CareContinuum, LLC;

Louis Pontarelli; William Filippone; Leo Dierckman; Alan Pollak; Geri Ostlund;

Richard Kuhl; WRS Architects, Inc.; James E. Iverson; Victor P. Dhooge; John M.

Clarey; James F. Dlugosh; Edward J. Hentges; Kenneth R. Larsen; Jerome E.

Tabolich; Steven W. Erickson; Paul R. Ekholm; Kenneth E. Dawkins; Joel T.

Boehm; Sabo & Green; Atkinson, Adelson, Loya, Ruud & Roma; Valuation

Counselors Group, Inc.; Coddington Appraisal Services; Capital Consulting

Group, Inc.; Healthcare Financial Solutions Group, Inc.; Zelenofske, Axelrod &

Co., Ltd; Berman and Bertolini, Inc., aka Berman & Associates; Michael

Sobelman; and Sobelman Cohen & Sullivan LLP (collectively "Defendants").

The Second Amended Consolidated Class Action Complaint alleges eighteen

causes of action for (I) Violation of Rule I Ob-5 and Section 10(b) of the Securities

Exchange Act of 1934; (2) Control Person Liability under Section 20 of the

Securities Exchange Act; (3) Control Person Liability under California

2

- Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 3 of 22

1 Corporations Code Section 25504; (4) Joint and Several Liability under California

2 Corporations Code Section 25504 . 1; (5) Joint and Several Liability under

3 California Corporations Code Section 25504 . 2; (6) Negligent Misrepresentation;

4 (7) Negligence ; ( 8) Breach of Fiduciary Duties ; (9) Aiding and Abetting Breach of

5 Fiduciary Duties ; ( 10) Breach of Contract; (11) Civil Conspiracy to Commit

6 Fraud ; ( 12) Unjust Enrichment ; ( 13) Breach of Contract against U.S. Trust; (14)

7 Negligence against U.S . Trust ; ( 15) Breach of Fiduciary Duty against U.S. Trust;

8 (16) Fraudulent Concealment against U.S. Trust; ( 17) Intentional

9 Misrepresentation against U . S. Trust ; and (18 ) Negligent Misrepresentation

10 against U.S. Trust.

11 The following facts are alleged in the Second Amended Consolidated

12 Class Action Complaint ("SACC") and are relevant to the motions before this

13 Court:

14 This action arises from damages sustained by Plaintiffs in eleven (11)

15 municipal bond offerings , which raised over $ 130,000,000 between December

16 1996 and March 1999. (SACC, ¶ 1). The monies raised in the bond offerings

17 were to be used to acquire, renovate and reopen former hospitals to assist elderly

18 people in Texas , Florida, Illinois and California (the "Heritage Facilities"). ( Id.).

19 Due to wrongful disbursements , diversions of bond proceeds and improper co-

20 mingling of funds, however, many of the facilities were not completed and all of

21 them went into receivership - foreclosure shortly after the bond offerings. (Id.).

22 Because a substantial portion of the monies raised in the first few

23 offerings was improperly diverted , monies raised in the later offerings and

24 intended to be used only in connection with the facility covered in the specific

25 offering , were improperly used to fund the earlier Facilities. (id. at ^ 2). The

26 money was typically transferred between the Facilities in the form of "loans"

27

28 3

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 4 of 22

1 between the Heritage Entities and accounted for inaccurately as "advances of

2 funds." (Id.). Many of these "loans" and "advances" were eventually

3 reclassified as payments for services never performed. (Id.). By 1999, the CPA

4 for the Heritage Entities insisted that $900,000 obtained via fraudulent means be

5 returned to the Heritage Entities and the underwriter of the offerings refused to

6 conduct any more offerings. (Id.). Shortly thereafter, the scheme collapsed and all

7 of the Facilities, with the exception of Rancho Hospital, went into receivership.

8 (Id.). Rancho Hospital filed bankruptcy. (Id.).

9 Additionally, some if not all, of the Heritage Entities were

10 fraudulently obtaining reimbursements from the U.S. Government under the

11 Medicare program. (Id. at ¶ 3). The Chapter 11 bankruptcy filing by Rancho

12 Hospital was converted into a Chapter 7 proceeding after the government asserted

13 a $10-20 million claim due to the Medicare fraud. (Id.).

14 Defendant U.S. Trust was the Trustee for each of the eleven bond

15 offerings and, as such, failed to properly perform its duties. (Id. at ¶ 4). U.S.

16 Trust ultimately attempted to hide its wrongdoing by falsely informing the

17 bondholders that it would protect their interests and, instead, entering into a

18 settlement agreement with the Heritage Entities, Jerold Goldstein, Clarke

19 Underwood, Geri Ostlund, and Virgil Lim, where all parties were released from

20 liability and agreed not to cooperate with any third party who filed suit. (Id.).

21 Despite representations to the bondholders that it would sue all responsible third

22 parties, U.S. Trust filed suit against only a handful of the Heritage Directors and

23 Officers because the U.S. Trust executive responsible for the oversight, William

24 Barber, was deeply involved in the scheme from the very beginning. (Id.).

25 This class action is brought by Plaintiffs on behalf of all persons who

26 purchased or otherwise acquired Heritage Bonds, excluding the Defendants,

27

28 4

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 5 of 22

1 members of their families and any Entity to which a Defendant has interest (the

2 "Class"). (Id. at ¶ 87). Among other things, the Class alleges that Defendants

3 made material misstatements and omissions in the Official Statements upon which

4 investors relied to purchase the Heritage Bonds, wrongfully diverted funds, and

5 abandoned their responsibilities resulting in substantial losses to the Class.

6 B. Procedural Summary

7 On November 30, 2001, Plaintiff Gilbert Kivenson filed his

8 Complaint in The Superior Court of the State of California, County of Los

9 Angeles, entitled Kivenson v. U.S. Trust Corp.. N.A., et al. and bearing Case No.

10 BC 262740 for (1) Violations of California Corporations Code; (2) Breach of

11 Fiduciary Duties; (3) Aiding and Abetting Breach of Fiduciary Duties; (4)

12 Negligence; (5) Negligent Misrepresentation; and (6) Violations of Federal

13 Securities Laws.

14 On January 15, 2002, Defendant Jerold Goldstein filed a Notice of

15 Removal of Action Under 28 U.S.C. § 1441(b), in that the case is governed by

16 federal statutory law; specifically, the Securities Litigation Uniform Standards Act

17 of 1998, 15 U.S.C. § 77p, and the Securities Litigation Reform Act of 1995, 15

18 U.S.C. § 78u-4. Upon removal, this case was assigned to Judge Baird.

19 On January 25, 2002, U.S. Trust Defendants consented to the

20 Removal to Federal Court.

21 On January 31, 2002, Defendant Jerold Goldstein filed a Certificate

22 of Service of Notice of Assignment to United States Magistrate Judge, where

23 Magistrate Judge Rosalyn M. Chapman was designated to hear discovery motions

24 for this case at the discretion of the assigned District Judge.

25 On January 28, 2002, this case was transferred to this Court from

26 Judge Baird pursuant to the low number rule involving case no. CV-01 5752 DT.

27

28 5

1

2

3

4

5

6

7

8

9

l0

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 6 of 22

On February 7, 2002, Defendants Marshall Wexler and Andrew

Kornreich joined in the removal of this action.

On February 11, 2002, Defendant Donald B. Chalker joined in the

removal of this action.

On March 8, 2002, Defendants Evan Greenspan, Donald King, and

Gary Medill joined in the removal of this action.

On May 28, 2002, Kivenson's Stipulation and Proposed Pre-Trial

Order No. I was denied, without prejudice to the bringing of a formally noticed

motion.

On June 11, 2002, Kivenson filed a Motion to Enter Pre-Trial Order

No. 1, which this Court granted in part and denied in part on July 22, 2002. In

such Order, this Court Ordered the following cases consolidated: Betker Partners

One LP, et a]. v. U.S. Trust Corp., N.A. , Case No. CV 01-5752 DT; Kivenson v.

U.S. Trust Corp., N.A., et al. , Case No. CV 02-382 DT; Preston v. U.S. Trust

Corp., et al. , CV 02-993 DT; and U.S. Trust Co. of Texas, N.A., et al. v. O.V.

Bertolini, et al. ,' Case No. CV 02-2745 DT.Z

On September 13, 2002, Plaintiffs filed a Consolidated Class Action

Complaint.

On October 29, 2002, Plaintiffs filed a Second Amended

Consolidated Class Action Complaint.

' Pursuant to this Court's September 30, 2002 Order Granting Bank of NewYork's Motion for Order Substituting Plaintiff, this case is now referred to asBank of New York, Inc. v. O.V. Bertolini, et al. .

z On October 15, 2002, this Court issued a Minute Order further ordering

that Allman v. Bertolini , CV 02-6484 and Betker Partners One, et al, v. Kasirer ,

CV 02- 6841 be consolidated with CV 01-5752.

6

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 7 of 22

1

2

3

4

5

6

7

8

9

10

On November 4, 2002, this Court issued an Order Setting the Briefing

Schedule for the Consolidated Class Action.

On November 5, 2002, this Court issued an Order Setting the

Schedule for Settlement Conference to be held on or before December 16, 2002

before Retired Judge Elwood Lui.

On November 12, 2002, Plaintiffs in the case styled Herrmann v. U.S.

Trust Co.,N.A., et al. , CV 02-9221 DT ("Herrmann Plaintiffs"), filed a Notice of

Motion and Motion to Consolidate Cases, for the Appointment of Lead Plaintiff

and Lead Counsel, and for Related Relief and a Request for Judicial Notice in

Support of such motion, which are presently before this Court.'

On November 15, 2002 , Defendants Evan Greenspan, Cary Medill,

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Herbert Saltzman filed an Ex Parte Application for Status Conference or,

alternatively, for Continuance of the Briefing Schedule Regarding Response to the

Second Amended Consolidated Complaint. On November 18, 2002, Defendant

Jerold Goldstein filed a Joinder to the Ex Parte Application.

On November 22, 2002, this Court issued an Order Granting

Defendants Ex Parte Application for a Continuance of the Briefing Schedule

Regarding Response to the Second Amended Consolidated Class Action

Complaint and Setting Schedule for Hearing on Motion to Consolidate, Motion for

Lead Plaintiff/Lead Counsel, Filing of Third Amended Consolidated Complaint

and Response to all Operative Complaints. The Court ordered the following: (1)

Motions to Consolidate and for Appointment of Lead Plaintiff/Lead Counsel to be

Although the Herrmann Motion was not filed in this action, it is relevant

to the procedural history in that, based on this Court ' s January 13, 2003 Tentative

Order Granting the Herrmann Plaintiffs' Motion to Consolidate , it is a competing

motion for Lead Plaintiff/Lead Counsel which will be discussed in the Current

Order.

7

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 8 of 22

1 heard in this Court on January 13, 2003; (2) Should the Court consolidate the

2 Herrmann Action with the Second Amended Consolidated Class Action

3 Complaint, Lead Counsel selected for the Class shall file a Third Amended

4 Consolidated Class Action Complaint by February 3, 2003; (3) Defendants in all

5 actions shall respond to the operative complaints against them by February 24,

6 2003; (4) All opposition briefs shall be filed by March 17, 2003; (5) All reply

7 briefs shall be filed by March 31, 2003; and (6) The hearing on all motions shall

8 be held on April 14, 2003.

9 On November 25, 2002, the Heritage Bondholder Group4 filed a

10 Notice of Motion and Motion for Appointment of Co-Lead Plaintiffs and

11 Approval of Lead Plaintiffs' Selection of Lead Counsel, which is presently before

12 this Court.

13

14 II. Discussion

15 A. Standards

16 1. Request for Judicial Notice

17 A court must take judicial notice if a party requests it and supplies the

18 court with the requisite information. Fed. R. Evid. 201(d). "A judicially noticed

19 fact must be one not subject to reasonable dispute in that it is either (1) generally

20 known within the territorial jurisdiction of the trial court or (2) capable of accurate

21 and ready determination by resort to sources whose accuracy cannot reasonably be

22 questioned." Fed. R. Evid. 201(b). This Court may take judicial notice of facts

23

24 4 Five individual members of the putative class who acquired Heritage

25 Bonds and now move this Court for appointment as Co-Lead Plaintiffs havedesignated themselves as the "Heritage Bondholder Group." The five individuals

26 are David M. Sinow, Howard Preston, Langdon Parrill, Ray Stits and Barrett27 Anderson.

28 , 8

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 9 of 22

i outside the pleadings without converting the motion to one for summary judgment.

2 See Mack v. South Bay Beer Distributors , 798 F.2d 1279, 1282 (9th Cir. 1986)

3 (citing Sears, Roebuck & Co. v. Metropolitan Engravers, Ltd. , 245 F.2d 67, 70

4 (9th Cir. 1956)). In addition, documents whose contents are alleged in a complaint

5 and whose authenticity is not in question may be considered in a motion to

6 dismiss. See Branch v. Tunnell , 14 F.3d 449, 453-54 (9th Cir. 1994).

7 This Court may take judicial notice of its own records, and documents

8 that are public records and capable of accurate and ready confirmation by sources

9 that cannot reasonably be questioned. See MGIC Indem. Corp. v. Weisman , 803

10 F.2d 500, 504 (9th Cir. 1986) (courts may take judicial notice of matters of public

11 record outside the pleadings); United States v. Wilson , 631 F.3d 118, 119 (9th Cir.

12 1980) ("In particular, a court may take judicial notice of its own records in other

13 cases, as well as the records of an inferior court in other cases.").

14 2. Appointment of Lead Plaintiff and Lead Counsel

15 Section 21D of the Exchange Act, as amended by the Private

16 Securities Litigation Reform Act ("PSLRA"), establishes the procedure for the

17 selection of lead plaintiff to oversee class actions brought under federal securities

18 laws, and provides as follows:

19 Not later than 20 days after the date on which the complaint

20 is filed, the plaintiff or plaintiffs shall cause to be published,

21 in a widely circulated national business-oriented publication

22 or wire service, a notice advising members of the purported

23 plaintiff class -

24 (I) of the pendency of the action, the claims

25 asserted therein, and the purported class

26 period; and

27 (11) that, not later than 60 days after the date on

28 9

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 10 of 22

1 which the notice is published, any member

2 of the purported class may move the court to

3 serve as lead plaintiff of the purported class.

4 15 U.S.C. § 78u-4(a)(3)(A)(i).

5 The Securities Exchange Act further directs the court to "consider any

6 motion made by a purported class member in response to the notice" within 90

7 days after such notice is published, or as soon after decisions on motions for

8 consolidation are rendered as practicable. §§ 78u-4(a)(3)(B)(i) & (ii). The court

g should "appoint as lead plaintiff the member or members of the purported plaintiff

10 class that the court determines to be most capable of adequately representing the

11 interests of the class members ...." § 78u-4(a)(3)(B)(i). In doing so, the court

12 should presume that the most adequate lead plaintiff

13 (aa) has either filed the complaint or made a motion in

14 response to a notice ...;

15 (bb) in the determination of the court, has the largest

16 financial interest in the relief sought by the class;

17 and

18 (cc) otherwise satisfies the requirements of Rule 23 of

19 the Federal Rules of Civil Procedure.

20 § 78u-4(a)(3)(B)(iii)(I). Such presumption may be rebutted only upon proof by

21 another member of the putative class that the presumptively most adequate

22 plaintiff

23 (aa) will not fairly or adequately protect the interests

24 of the class; or

25 (bb) is subject to unique defenses that render such

26 plaintiff incapable of adequately representing the

27 class.

28 10

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 11 of 22

§ 78u-4(a)(3)(B)(iii)(II).

"The most adequate plaintiff shall, subject to the approval of the

court, select and retain counsel to represent the class." § 78u-4(a)(3)(B )(v). The

PSLRA "evidences a strong presumption in favor of approving a properly-selected

lead plaintiff ' s decisions as to counsel selection and counsel retention." In re

Cavanaugh , 306 F.3d 726, 734 n.14 (9th Cir. 2002).

B. Analysis

1. Herrmann Plaintiffs' Request for Judicial Notice is

Granted

In conjunction with their Motion to Consolidate, for the Appointment

of Lead Plaintiff and Lead Counsel, and for Related Relief, Herrmann Plaintiffs

request this Court take judicial notice of the following two documents: (1) Award

against Miller & Schroeder Financial, Inc. by the NASD Dispute Resolution, Inc.

in the matter Robert H. Lundquist , Individually and as Trustee of the Lundquist

Family Trust UAD 12/09/83 v. Miller & Schroeder Financial, Inc. , attached to

Request for Judicial Notice as Exhibit 1; and (2) Class Action Complaint filed on

November 20, 2001 in the matter entitled Herrmann v. Miller & Schroeder

Financial, Inc. , San Diego Superior Court Case No. 778499, attached to Request

for Judicial Notice as Exhibit 2.

Because such documents are public records capable of accurate and

ready determination by resort to sources whose accuracy cannot reasonably be

questioned, have not been opposed, and bear a direct relation to matters at issue in

the present proceeding, Herrmann Plaintiffs' Request for Judicial Notice as to the

aforementioned documents is granted.

ll

ll

ll

11

Case 2 : 02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 12 of 22

1 2. This Court Appoints the Heritage Bondholder Group as

2 Co-Lead Plaintiffs for the In re Heritage Bond Litigation

3 Consolidated Class Actions

4 Competing motions for Lead Plaintiff and Lead Counsel in the In re

5 Heritage Bond Litigation consolidated class actions have been submitted to this

6 Court. Lewis G. Herrmann ("Herrmann"), the named plaintiff in Herrmann v. U.S.

7 Trust Co. of Texas. N.A., et al. , moves to be named lead plaintiff, and a group of

8 five individual investors designated the Heritage Bondholder Group move to be

g named co-lead plaintiffs (collectively, "Moving Plaintiffs"). Thus, both motions

10 are currently before this Court.

11 The Ninth Circuit has stated that the PSLRA "provides a simple

12 three-step process for identifying" the proper lead plaintiff in a securities class

13 action. In re Cavanaugh , 306 F.3d 726, 729 (9th Cir. 2002). The three steps are:

14 (1) a determination as to whether publication to potential class members was

15 adequate; (2) consideration by the court of the losses allegedly suffered by the

16 various plaintiffs and selection of the presumptive lead plaintiff, "the one who has

17 the largest financial interest in the relief sought by the class and otherwise satisfies

18 the requirements of rule 23 . . ."; and (3) consideration by the court of proof by

19 other plaintiffs rebutting "the presumptive lead plaintiff's showing that it satisfies

20 Rule 23's typicality and adequacy requirements." See id. at 729-30.

21 a. Publication of the Initial Notice to Purported Class

22 Members is Adequate

23 The PSLRA requires that notice to purported plaintiff class members

24 be published in a "widely circulated national business-oriented publication or wire

25 service" advising them of the pendency of a class action, the claims asserted, the

26 purported class period and that any member of the purported class may move the

27

28 12

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 13 of 22

court to serve as lead plaintiff within 60 days of the date of publication. 15 U.S.C.

2 § 78u-4(a)(3)(A)(i).

3 Brian Barry ("Barry"), current counsel for the Heritage Bondholder

4 Group, published notice of the pendency of the class action on September 25,

5 2002 on Internet Wire. ( See Declaration of Brian Barry, Exh. A). Moving

6 Plaintiffs do not dispute the adequacy of the publication. However, U.S. Trust

7 Defendants contend that the initial notice is defective and deficient and that,

8 therefore, a lead plaintiff should not be selected until a proper initial notice is

9 published. Specifically, U.S. Trust Defendants argue that the Heritage Bondholder

10 Group makes no showing that Internet Wire is "a widely circulated national

11 business-oriented publication or wire service" as required by the PSLRA. 15

12 U.S.C. § 78u-4(a)(3)(A)(i). Furthermore, U.S. Trust Defendants contend that even

13 if this Court finds that Internet Wire is widely circulated, the notice fails to

14 provide required information including (1) the requisite case identification

15 information; (2) the specific dates and content of the alleged misstatements and

16 misrepresentations; (3) the existence of potential intra-class conflicts; and (4) the

17 qualifications of the proposed lead plaintiffs to serve as such.

18 The PSLRA does not provide a definition of "widely circulated."

19 Therefore, courts are required to make a determination as to whether the particular

20 vehicle used for publication was adequate. Lax v. First Merchants Accep. Corp. ,

21 1997 WL 461036, * 4 (N.D. Ill.). Although U.S. Trust Defendants argue that

22 Moving Plaintiffs have not met their burden of showing that Internet Wire satisfies

23 this requirement, they do not actually attempt to show that Internet Wire is not

24 widely circulated. I lowever, as Herrmann points out, courts have consistently

25 found that Business Wire is an adequate means of notice under the PSLRA. See

26 Yousefi v, Lockheed Martin Corp. , 70 F. Supp. 2d 1061, 1067 (C.D. Cal. 1999).

27 In making such a finding, one court reasoned that "Business Wire is subscribed to

28 13

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 14 of 22

1 by hundreds of print publications and wire services, encompassing news media in

2 all fifty states." Greebel v. FTP Software Inc. , 939 F. Supp. 57, 62-63 (D. Mass.

3 1996). Like Business Wire, Internet Wire is distributed to thousands of news

4 media services, including The Wall Street Journal and Investor's Business Daily,

5 on a national and international level. Therefore, this Court finds that Internet Wire

6 likely does satisfy the definition of "widely circulated."

7 This Court acknowledges U.S. Trust Defendants' argument that

8 necessary information is missing from the published notification. However, the

9 PSLRA simply requires that notification advise putative class members of the

10 pendency of the action, the purported class period, the claims asserted and the

11 deadline for filing motions for lead plaintiff. The notice published by Barry meets

12 these requirements. Although U.S. Trust Defendants cite cases requiring more

13 detailed information, these cases are specific to the factual circumstances

14 involved. Therefore, this Court finds that notice appears to be sufficient, and that

15 U.S. Trust Defendants' arguments are not so persuasive as to preclude a

16 determination of lead plaintiff at this time.

17 b. The Heritage Bondholder Group Has the Largest

is Collective Financial Interest of the Moving Plaintiffs

19 and , Therefore, is the Presumptive Lead Plaintiff

20 The "presumptively most adequate plaintiff- and hence the

21 presumptive lead plaintiff - is the one who has the largest financial interest in the

22 relief sought by the class" and otherwise satisfies the typicality and adequacy

23 requirements of Rule 23. In re Cavanaugh, 306 F.3d at 730. In appointing a lead

24 plaintiff, a district court must first "compare the financial stakes of the various

25 plaintiffs and determine which one has the most to gain from the lawsuit." Id.

26 Moving Plaintiffs provide declarations of their respective financial

27 interests in the In re Heritage Bond Litigation . Proposed lead plaintiff Herrmann

28 14

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 15 of 22

states that he has an interest of $770,771.00 based on his losses in eleven of the

2 twelve Heritage Bond Offerings. (See Declaration of Lewis G. Herrmann, Exh. 1).

3 Proposed co-lead plaintiffs, the Heritage Bondholder Group, declare collective

4 losses of $4,016,090.60 with the following individual losses: (1) David M. Sinow

5 - $1,656,164.38; (2) Howard Preston - $700,400; (3) Langdon Parrill - $680,263;

6 (4) Ray Stits - $613,476; and (5) Barrett Anderson - $365,787.29.5 Therefore, the

7 Heritage Bondholder Group contends that it is the presumptive lead plaintiff

8 because it has suffered the largest financial losses. Herrmann, however, argues

g that the losses of individual plaintiffs may not be aggregated into group losses to

10 create a lead plaintiff group with the greatest financial interest. Therefore,

11 Herrmann argues that his interest is the greatest and that he is the presumptive lead

12 plaintiff.

13 While a "group of persons" can serve as lead plaintiff, courts

14 throughout the country and within the Ninth Circuit are divided on the question of

15 whether individual losses of unrelated investors may be aggregated to satisfy the

16 largest financial interest requirement.6 See id. at 731. Moving Plaintiffs have

17 cited many of these cases, the majority of which differ from the case before us as

18 to the specific facts. However, a court in this circuit recently addressed facts very

19

20 While Herrmann does not contest the financial stake of Preston, Parrill,

21 Stits or Anderson, he does question the financial interest asserted by Sinow.However, the aggregate loss of the other four proposed members of the Heritage

22 Bondholder Group, $2,359,926.22, exceeds Herrmann's financial stake even23 without Sinow's contribution. Therefore, it is unnecessary for this Court to

24address Herrmann's argument at this time.

25 6 In In re Cavanaugh , the Ninth Circuit specifically stated that it was notasked to, and therefore, would not address the undecided question of "whether a

26 group can satisfy the `largest financial interest' requirement by aggregating27 losses." 306 F.3d at 731.

28 15

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 16 of 22

1 similar to those at issue here. In In re Versata , competing motions for lead

2 plaintiff were presented by a group arguing that, collectively, it had the greatest

3 financial interest and an individual who argued that he alone had a greater

4 financial loss than any individual member of the proposed group. 2001 WL

5 34012374 (N.D. Cal.). Like Herrmann, the individual plaintiff argued that the

6 group members' losses should not be aggregated because they had nothing in

7 common other than the same lawyer. The court looked at the policy behind the

8 PSLRA and reasoned that a "case-by-case approach allows a district court

9 maximum flexibility to select a lead plaintiff who will best represent the interests

10 of the class and exercise control of the litigation." Id. at * 5. As a result, it held

11 that "under appropriate circumstances small groups, whether or not they have any

12 pre-litigation relationship, can aggregate their financial losses." Id. This Court

13 agrees.

14 A primary purpose of the "lead plaintiff provisions of the PSLRA was

15 to encourage a meaningful investor with a substantial stake in the litigation ... to

16 initiate and control the litigation," and "to prevent lawyer-driven litigation." See

17 id.; see also Aronson v. McKesson HBOC, Inc., et al. , 79 F. Supp. 2d 1146, 1152

18 (N.D. Cal. 1999). "The principal concern is that the proposed group will actively

19 represent the class." In re Versata , at * 5 (citing In re Advanced Tissue Sciences

20 Sec. Litig , 184 F.R.D. 346, 352 (S.D. Cal. 1998)). If the characteristics required to

21 adequately represent a class are present in a group, it should be permitted to

22 aggregate its losses and serve as lead plaintiff, regardless of whether a pre-existing

23 relationship existed between the members. This approach will allow courts to

24 select the investors who are the most willing and able to represent the class.

25 Therefore, this Court finds that the Heritage Bondholder Group has the largest

26

27

28 16

Case 2 : 02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 17 of 22

financial stake in the In re Heritage Bond Litigation , and is the presumptive lead

plaintiff.?

c. The Heritage Bondholder Group Satisfies the

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Typicality and Adequacy Requirements of Rule 23

"Once it determines which plaintiff has the biggest stake, the court

must appoint that plaintiff as lead, unless it finds that [it] does not satisfy the

typicality or adequacy requirements" of Rule 23. In re Cavanaugh , 306 F.3d at

732. Thus, a court must focus on that plaintiff and base its decision on

information in the pleadings and declarations submitted. Id. at 730. As it would

where an individual investor seeking appointment as lead plaintiff had the largest

financial interest, this Court must evaluate whether the Heritage Bondholder

Group is qualified to serve as lead plaintiff.

Herrmann also argues that the Heritage Bondholder Group should not be

appointed lead plaintiff because it is a direct result of Barry's solicitation in anattempt to "cobble together" a group that would collectively have the largestfinancial stake in the litigation. Although this Court acknowledges Herrmann'sargument it finds it unpersuasive.

In arguing that Barry solicited the members of the Heritage BondholderGroup, Herrmann appears to be referring to the required publication of notice topurported class members and to a mass mailing by Barry to all known Heritagebondholders. However, this Court finds that direct mail is appropriate in cases of

this type. (See, e.g., In re Network Assoc., Inc. Sec. Litig. , 76 F. Supp. 2d 1017,

1031.32 (N.D. Cal. 1999); Ravens v. Iftikar , 174 F.R.D. 651, 676 (N.D. Cal.

1997)). Furthermore, each proposed group member has stated that he came to his

own decision regarding whether or not to act as lead plaintiff and chose to contact

Barry to discuss participating in the case. Finally, as Barry points out, numerous

individuals who submitted certifications suffered losses greater than those of the

proposed Group members. Therefore, the argument that Barry was simply

attempting to create a group with the largest financial interest is unconvincing.

17

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 18 of 22

1 In this case, four of the proposed members of the Heritage

2 Bondholder Group are elderly individual investors who purchased Heritage Bonds

3 in reliance on Official Statements between December, 1996 and March, 1999, the

4 purported class period. (See Declaration of Jill Levine Betts, Exhs. 3-6). All of

5 these individuals suffered substantial losses when the Heritage Bonds defaulted.

6 Thus, it appears to this Court that the claims of these individuals are representative

7 of the class, and Herrmann does not argue otherwise.

8 Herrmann does, however, argue that Sinow's, the fifth proposed

g member of the Heritage Bondholder Group, claims are not typical of the class in

10 that (1) he is an investment advisor who originally purchased the Heritage Bonds

1 t on behalf of his clients; (2) his firm undertook substantial due diligence before

12 recommending the purchases to their clients; (3) he may be subject to unique

13 defenses not applicable to other class members;' and (4) he does not provide

14 competent admissible evidence that the stock he transferred for the bonds was

15 truly worth $1.7 million. Sinow admits that he originally purchased the Heritage

16 Bonds on behalf of his clients and, after the bonds defaulted, re-purchased them at

17 par value. He further states that he then purchased the bonds from his company,

1 g pursuant to a settlement agreement, in exchange for his shares in the company.

19 Although this Court acknowledges the arguments set forth by Herrmann, it also

20

21 8 Specifically, Herrmann argues that transactions through which Sinowacquired his shares occurred after the Heritage Bond fraud was uncovered, and

22 that, therefore, he was not an innocent purchaser. However, Sinow has submitted23 evidence that the bonds were initially purchased in the Heritage Bond offerings

prior to default. ( See Betts Decl., Exh. 2 at ^ 3).24

25 Herrmann further argues that Sinow has not explained the basis for re-purchasing the stock or whether he or his company was potentially liable for

26 culpable conduct. However, Herrmann's argument is not based on proof but mere

27 speculation.

28 18

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 19 of 22

1'

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

notes that courts have appointed investment advisors as lead plaintiffs, particularly

as part of a group. See Takeda v. Turbodyne Tech., Inc., et al. , 67 F. Supp. 2d

1129, 1136 n.18 (C.D. Cal. 1999). The Takeda court, in particular, stated that it

failed to see how the fact that the proposed group member incurred losses on

behalf of his clients rather than personally, detracted from his suitability as a lead

plaintiff. Id. The court noted that this was especially true in light of the

congressional preference for large, institutional investors as lead plaintiffs and

found that an investment advisor would add sophistication to the class. Id. This

Court agrees and further notes that Sinow should not be eliminated from the class

on the grounds that he chose to repurchase the bonds after default. Furthermore,

for the same reasons, this Court also finds that it is irrelevant that Sinow may have

conducted due diligence prior to investing because he specifically states that his

company chose to purchase the Heritage Bonds after reviewing the Official

Statements. (See Betts Decl., Exh. 2, ¶ 3). Furthermore, "representative claims

are typical if they are reasonably co-extensive with those of absent class members;

they need not be substantially identical." Takeda, 67 F. Supp. 2d at 1136. Finally,

other class members may only rebut a presumptive lead plaintiff's typicality with

proof, not mere speculation. Thus, this Court finds that the Heritage Bondholder

Group satisfies the typicality requirements of Rule 23.

Finally, this Court finds that the Heritage Bondholder Group will

adequately represent the other members of the class in this litigation. Each of its

proposed members has expressed a desire to actively participate and oversee

counsel in the litigation. ( See Betts Decl, Exhs. 2-6). Furthermore, each of these

individuals has an impressive business background with professions including,

physicist, attorney, physician, professor of finance, company President and/or

owner, and management consultant. (See id.) All have worked with attorneys in

the past and feel comfortable doing so, indicating that they will not be controlled

19

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 20 of 22

1 or manipulated by counsel. (See id.). The Group has developed a plan for

2 participating in the litigation that includes engaging in regular conference calls,

3 the first of which has already taken place. As a whole, the Heritage Bondholder

4 Group suffered losses in each of the twelve bond offerings at issue providing them

5 with a basis to strenuously represent the class in its entirety. In reviewing the

6 information presented, this Court feels that the diversity and individual

7 characteristics of each of the proposed group members will enhance their ability

8 and desire to actively litigate on behalf of the entire class. Thus, this Court finds

9 that the Heritage Bondholder Group and its individual members satisfy the

10 adequacy requirements of Rule 23.

11 As previously stated, upon determining that it meets the typicality and

12 adequacy requirements of Rule 23, this Court must appoint the presumptive lead

13 plaintiff. It need not address the qualifications of each plaintiff moving to be

14 appointed lead plaintiff. Accordingly, this Court grants the Heritage Bondholder

15 Group's Motion for Appointment as Lead Plaintiff and denies Lewis G.

16 Herrmann's Motion for the Appointment of Lead Plaintiff and Lead Counsel.

17 3. The Heritage Bondholder Group ' s Selection of Lead

is Counsel i s Approved

19 "While the appointment of counsel is made subject to the approval of

20 the court, the Reform Act clearly leaves the choice of class counsel in the hands of

21 the lead plaintiff." In re Cavanaugh , 306 F.3d at 734. The Heritage Bondholder

22 Group has selected the Law Offices of Brian Barry and Glancy & Binkow, LLP as

23 Co-Lead Counsel to pursue this litigation on behalf of the class. In addition,

24 proposed Co-Lead Counsel have associated Cohen Milstein Hausfeld and Toll, a

25 nationally recognized class action law firm. Finally, the said proposed Lead

26 Counsel have associated Blaies & Hightower LLP, a firm in Fort Worth, Texas, to

27 assist in service of process and discovery in Texas where properties involved in

28 20

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 21 of 22

1 many of the bond offerings at issue took place. Proposed counsel have submitted

2 substantial evidence that they are qualified to represent the class in this case.

3 Furthermore, each of the members of the Heritage Bondholder Group has

4 indicated his desire that these firms represent the class in the In re Heritage Bond

5 Litigation . Finally, aside from Herrmann's argument that Barry improperly

6 solicited Group members, which this Court has already rejected, no evidence has

7 been presented that proposed Lead Counsel is not qualified. Therefore, this Court

8 grants the Heritage Bondholder Group's Motion for Approval of Lead Plaintiffs'

9 Selection of Lead Counsel.

10 11

11 /1

12 11

13 1/

14 11

15 11

16 11

17 11

18 1/

19 11

20 11

21 11

22 11

23 11

24 11

25 11

26 /1

27 11

28 21

Case 2:02-cv-00382-RGK-RC Document 99 Filed 01/13/2003 Page 22 of 22

1 III. Conclusion

2 Based on the foregoing, this Court (1) grants Herrmann Plaintiffs'

3 Request for Judicial Notice in Connection with Plaintiffs' Motion to Consolidate,

4 for the Appointment of Lead Plaintiff and Lead Counsel, and for Related Relief;

5 (2) grants the Heritage Bondholder Group ' s Motion for Appointment as Lead

6 Plaintiffs and for Approval of the Law Offices of Brian Barry and Glancy &

7 Binkow , LLP as Lead Plaintiffs' Selection of Lead Counsel ; and (3 ) denies Lewis

8 G. Herrmann ' s Motion for the Appointment of Lead Plaintiff and Lead Counsel,

9 and for Related Relief.' Furthermore , pursuant to its November 22, 2002 Order,

10 this Court directs Lead Counsel to file a Third Amended Consolidated Class

11 Action Complaint reflecting the consolidation of Herrmann v. U.S. Trust Co. of

12 Texas, N .A., et al. , CV 02-9221 DT, by February 3, 2003.

13

14 IT IS SO ORDERED.

15DICKRAH TEVRIZIAH

lb DATED: 3 200jDickran Tevrizian, Judge

17 United States District Court

18

19

20

2 1 In his motion , Herrmann also requests that "assuming the court is inclinedto consolidate the Herrmann case and to establish the leadership structure

22 proposed herein, the Herrmann Plaintiffs respectfully suggest that the Court's

23 order dated July 22, 2002 be modified " to (1) grant the Herrmann Plaintiffs ten

days leave to File a Consolidated Amended Complaint; (2) order all parties to24 attend a scheduling conference before the Magistrate Judge ; and (3) establish a25 briefing schedule for a motion for class certification . ( See Notice of Motion and

Motion to Consolidate , for the Appointment of Lead Counsel , and for Related26 Relief. 11:11-12:23). Because this Court denied Herrmann ' s motions for lead27 plaintitfand lead counsel , this request is moot.

28 22